Propanol Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

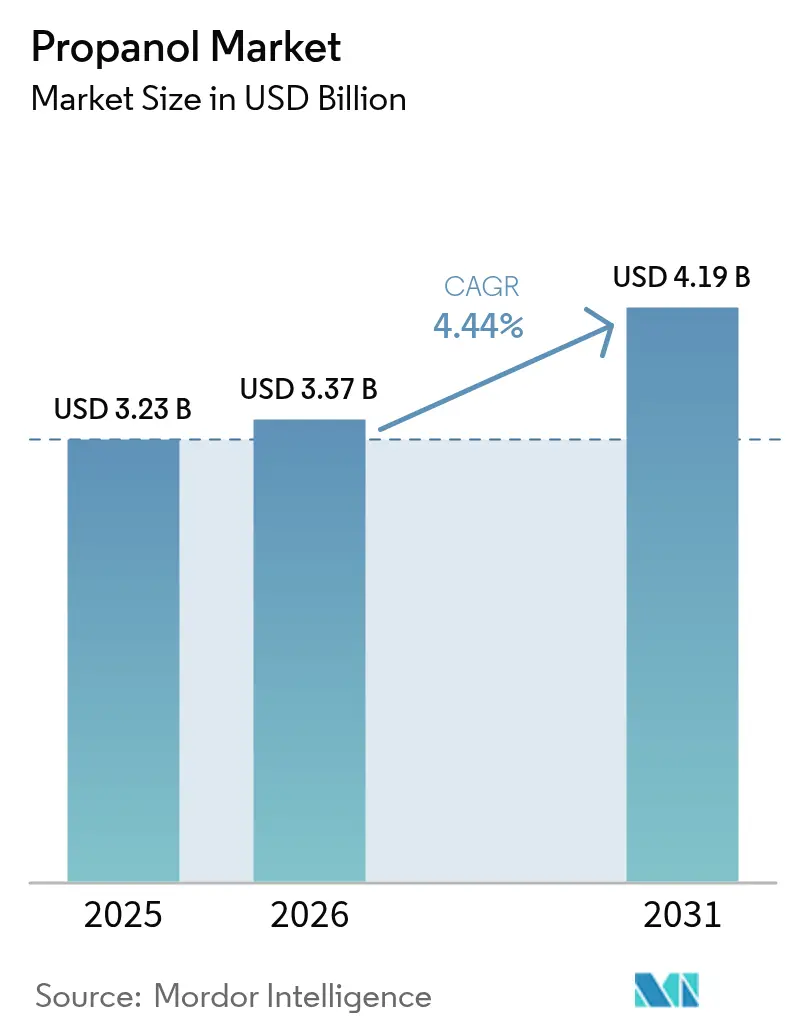

| Market Size (2026) | USD 3.37 Billion |

| Market Size (2031) | USD 4.19 Billion |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Propanol Market Analysis by Mordor Intelligence

The Propanol market size is expected to grow from USD 3.23 billion in 2025 to USD 3.37 billion in 2026 and is forecast to reach USD 4.19 billion by 2031 at 4.44% CAGR over 2026-2031. Moderate expansion stems from rising adoption in semiconductor cleaning, sustainable aviation fuel pathways, and pharmaceutical synthesis, even as regulatory pressures reshape solvent formulations. High-purity isopropanol demand for 5 nm and below chip fabrication, new API production hubs in Asia, and alcohol-to-jet projects in North America collectively underpin steady volume gains. Feedstock volatility and evolving VOC limits temper momentum, but continuous oxo-alcohol integration and investment in purification technologies help producers defend margins. Integrated petrochemical players therefore retain cost advantages, while bio-based entrants carve out growth niches within the wider propanol market.

Key Report Takeaways

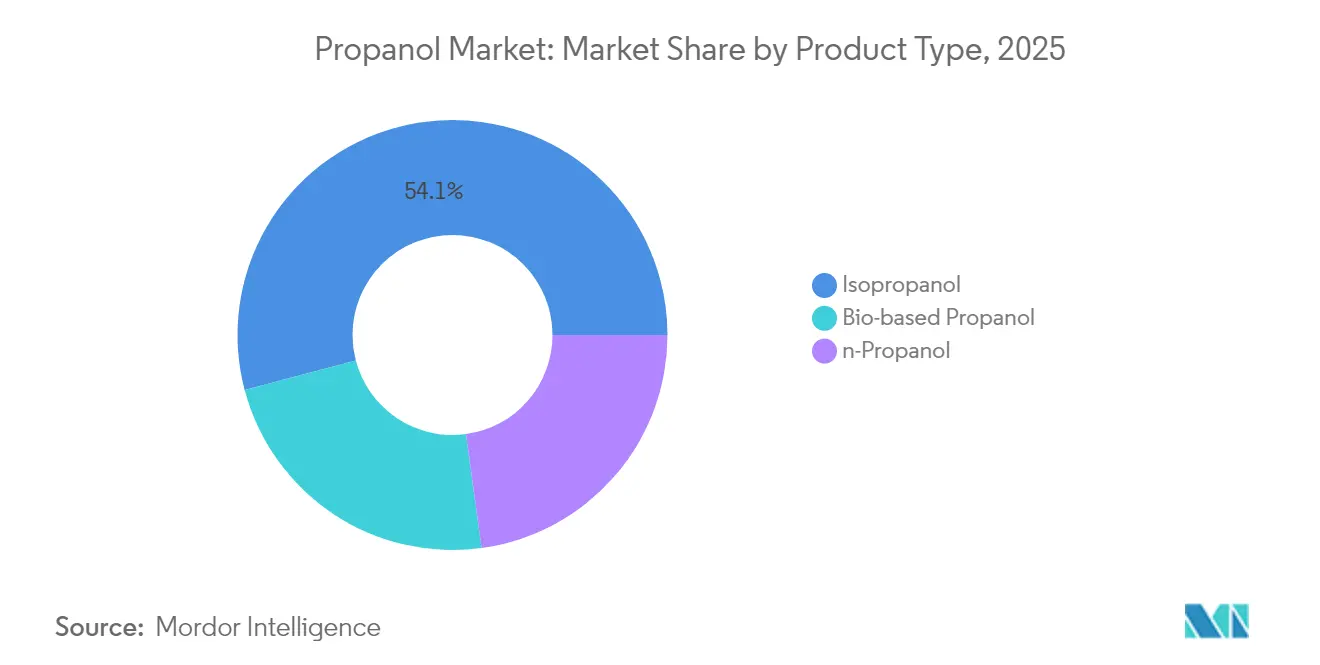

- By product type, isopropanol led with 54.12% revenue share in 2025; bio-based propanol is projected to expand at a 6.55% CAGR through 2031.

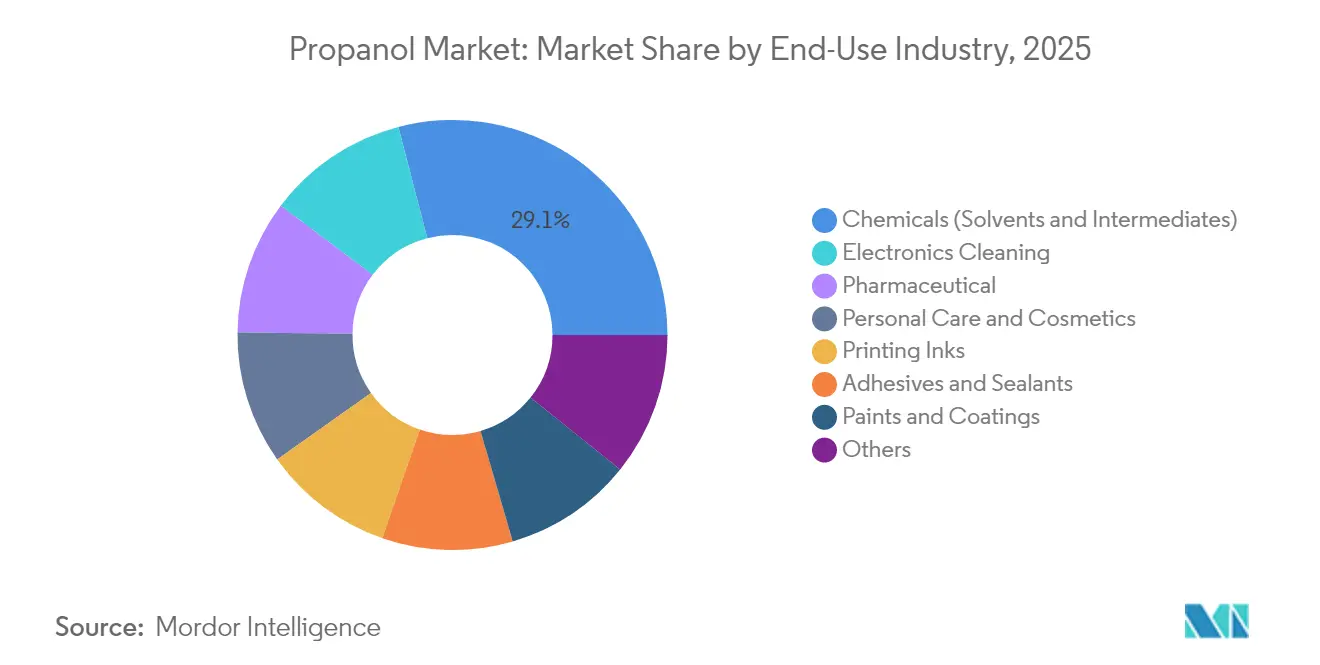

- By end-use industry, the chemicals segment held 29.05% of propanol market share in 2025, while electronics cleaning is advancing at a 5.82% CAGR to 2031.

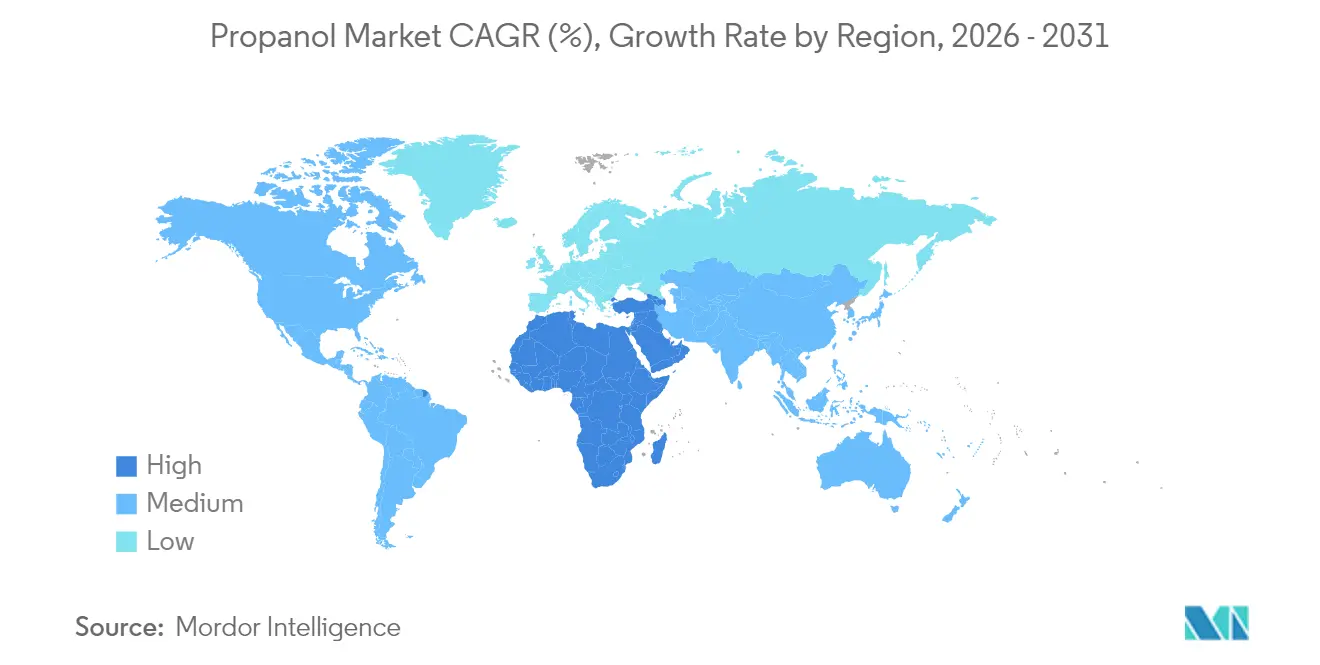

- By geography, Asia Pacific commanded 39.85% of the propanol market in 2025; the Middle East and Africa region is forecast to post the fastest regional CAGR of 6.73% over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Propanol Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-purity (isopropyl alcohol) IPA demand in electronics cleaning | +1.20% | Global, with concentration in Asia Pacific and North America | Medium term (2-4 years) |

| Construction-led solvent demand in paints & coatings | +0.80% | Global, strongest in Asia Pacific and Middle East | Long term (≥ 4 years) |

| Rising pharma API output in Asia Pacific | +0.90% | Asia Pacific core, spill-over to other regions | Medium term (2-4 years) |

| Emerging bio-propanol for low-carbon aviation fuel | +0.70% | North America and Europe leading, global expansion | Long term (≥ 4 years) |

| Cost cuts via continuous oxo-alcohol integration | +0.50% | Global, particularly in integrated petrochemical complexes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High-purity IPA Demand in Electronics Cleaning

Ultra-high-purity isopropanol exceeding 99.999% purity has become indispensable for advanced node semiconductor fabrication. ExxonMobil is upgrading its Baton Rouge unit to supply this grade by 2027, ensuring secure domestic supply for United States chipmakers. Contamination at parts-per-trillion levels can impair wafer yields, pushing device makers to specify ever-cleaner solvents[1]NCBI, “Effects of Ultrapure IPA on Semiconductor Yields,” ncbi.nlm.nih.gov . Electronics cleaning consequently grows faster than the overall propanol market, and suppliers are installing additional distillation columns, filtration trains, and real-time analytics to certify product purity. The resulting price premiums partly offset feedstock volatility, allowing integrated producers to protect spreads while meeting stringent customer audits.

Construction-led Solvent Demand in Paints & Coatings

Strong residential and commercial construction in Asia Pacific and the Middle East is driving demand for architectural coatings that rely on propanol-based co-solvents to balance viscosity, open time, and film formation. Regulators in the United States and Europe continue tightening VOC thresholds, spurring formulation shifts toward waterborne systems that still require controlled levels of propanol for flash-off control. The U.S. Environmental Protection Agency has extended aerosol coating compliance deadlines to January 2027, giving manufacturers critical runway to redesign products while maintaining performance[2]Federal Register, “Extension of Aerosol Coating Compliance,” federalregister.gov . Continuous solvent innovation helps coatings producers satisfy durability criteria without breaching emission limits, supporting incremental consumption across the propanol market.

Rising Pharma API Output in Asia Pacific

India’s Production Linked Incentive scheme and the creation of three Bulk Drug Parks backed by INR 30,000 crore (USD 360 million) in government funding encourage local synthesis of key active ingredients, decreasing dependence on Chinese imports. Large-scale reactors at facilities such as WuXi STA’s Taixing site, which reached 3,773 m³ of capacity in 2024, require high-purity propanol for crystallization and extraction steps. These expansions lift demand for pharmaceutical-grade volumes and promote long-term contracts that stabilize throughput for producers active in the propanol market.

Emerging Bio-propanol for Low-carbon Aviation Fuel

Alcohol-to-jet pathways use bio-propanol as an intermediate, creating attractive offtake opportunities that deliver higher margins than commodity solvent sales. USA BioEnergy is investing USD 2.8 billion in Texas to manufacture 65 million gallons of sustainable aviation fuel annually. In the United Kingdom, Project Speedbird secured GBP 11.2 million to commercialize similar routes by 2028. Airlines facing carbon-reduction mandates contract long-term supply, encouraging bio-based entrants to scale fermentation technology and integrate backward into renewable feedstock.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile propylene feedstock prices | -1.10% | Global, particularly impacting integrated producers | Short term (≤ 2 years) |

| Stricter VOC rules for solvent formulations | -0.60% | North America and Europe leading, global adoption | Medium term (2-4 years) |

| Scale-up hurdles for bio-propanol fermentation | -0.40% | Global, concentrated in regions with bio-propanol investments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter VOC Rules for Solvent Formulations

The U.S. National VOC Emission Standards impose lower allowable limits on consumer and commercial coatings, forcing reformulation to meet January 2027 deadlines[3]EPA, “National VOC Emission Standards,” epa.gov . Similar policies are unfolding in the European Union, compelling users to substitute or reduce traditional solvent volumes. Compliance costs, additional testing, and certification requirements slow demand growth in legacy coatings, inks, and adhesives application areas, dampening part of the propanol market’s potential.

Scale-up Hurdles for Bio-propanol Fermentation

Laboratory yields often fail to translate linearly at industrial scale because shear stress, oxygen mass transfer, and substrate inhibition diminish productivity. Research found notable titer drop-off when reactors expanded beyond 100 L, underscoring the challenge of maintaining metabolic efficiency at commercial capacity. Continuous fermentation improves throughput—1,3-propanediol rates reached 3.67 g/L·h using optimized feeding—but capital intensity remains a barrier. Until technology de-risks, petrochemical routes will continue supplying the majority of the propanol market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Isopropanol Dominance Amid Bio-based Growth

Isopropanol accounted for 54.12% of the propanol market in 2025, leveraging its quick evaporation rate, antimicrobial efficacy, and versatile solvency for pharmaceuticals, personal care, and industrial cleaning. Semiconductor manufacturers are sharpening this dominance by contracting supply of 99.999% grades, and ExxonMobil’s upcoming Baton Rouge line illustrates capital commitment toward ultra-high-purity batches. N-propanol maintains a niche but reliable presence in specialty inks and chemical intermediates, benefiting formulators requiring slower evaporation and distinct reactivity. Bio-based propanol delivers the steepest growth curve at 6.55% CAGR, aided by policy incentives targeting sustainable aviation fuel. USA BioEnergy’s investment has increased confidence that offtake agreements can underwrite scale-up, positioning renewable producers for entry into the broader propanol market.

Isopropanol’s extensive global distribution network and mature manufacturing footprint underpin reliable supply, yet escalating semiconductor demand is pressuring logistics and quality-control capacity. Producers are updating purification trains with ion-exchange, ultrafiltration, and advanced gas chromatography to verify part-per-trillion impurity thresholds. Conversely, bio-based output must overcome fermentation productivity limits and variable feedstock availability. Over the forecast horizon, the faster growth of renewable grades narrows the gap, but the absolute propanol market size for isopropanol remains well ahead, illustrating the inertia of entrenched production assets and customer familiarity.

By End-use Industry: Electronics Cleaning Drives Growth

The chemicals segment retained 29.05% of propanol market share in 2025 through its wide interface with paints, resins, and extractive processes that rely on balanced solvency and miscibility. Nonetheless, electronics cleaning is growing at 5.82% CAGR as fabs add capacity for AI accelerators, 5G radios, and power-efficient memory. Fabricators pursue zero-defect targets under shrinking line widths, prompting tighter solvent purity specifications and frequent bath replacements, which lift volumetric demand.

Pharmaceuticals offer a steady consumption base thanks to rising generic production in India and formulation exports from China. Here, propanol underpins purification, crystallization, and wash stages, securing long-term offtake stability. Personal care applications continue to diversify into sanitizers, antimicrobial gels, and fragrance carriers, adding consistent albeit modest volume. Paints and coatings, once the cornerstone of solvents, see slower uptake as VOC ceilings tighten. Yet reformulation still requires propanol to manage viscosity profiles in low-VOC systems, retaining relevance even if total volumes level out. The emerging sustainable aviation fuel niche provides a differentiated, high-value outlet for bio-based molecules, reshaping perceptions of the propanol market beyond traditional chemistry.

Geography Analysis

Asia Pacific leads the propanol market with 39.85% share in 2025. Government programmes like India’s PLI scheme and Bulk Drug Parks funnel investment into API synthesis lines that consume pharmaceutical-grade propanol. China remains the largest chemical producer globally, commanding 50% share of world output and driving solvent needs across paints, inks, and electronics assembly. High-purity demand is amplified by advanced node semiconductor activity in Japan and South Korea, where fabs stipulate stringent contamination thresholds. Growing integration between refineries and chemical complexes in Southeast Asia further stabilizes regional feedstock supply.

North America exhibits mature but resilient consumption. The United States exported USD 345 million of propanol in 2023 while importing USD 128 million, a sign of domestic self-sufficiency coupled with specialized grade requirements. ExxonMobil’s plan to produce 99.999% purity isopropanol in Louisiana aligns with the domestic semiconductor incentive framework, reducing dependence on imported high-spec material. Concurrently, USA BioEnergy’s Texas SAF project elevates the region’s renewable propanol profile, signaling diversification of demand.

Europe faces cost-side pressure from energy prices and stricter environmental norms. BASF saw a 21% sales decline in 2023, emblematic of subdued industrial output, yet specialty grades for pharmaceuticals and personal care protect pockets of profitability. The Middle East and Africa region holds the highest forward CAGR potential. Advanced Petrochemical and SK Gas are constructing an isopropanol plant at Jubail, harnessing local propylene surpluses and integrated infrastructure. South America registers moderate growth, with Brazil’s push toward SAF via sugarcane waste and biomethane unlocking future bio-propanol demand.

Value Chain Analysis

The propanol value chain begins with upstream petrochemical feedstocks, primarily propylene, and related syngas/oxo intermediates for oxo-alcohol routes, so costs and availability track refinery and cracker operating rates as well as regional logistics. On the bio-based side, renewable feedstocks such as glycerine are converted into propanol intermediates via fermentation or catalytic routes, creating a parallel chain that depends on steady biomass-derived input streams and industrial-scale scale-up performance.

Midstream production is concentrated in integrated complexes that pair propylene supply with oxo synthesis and purification assets (distillation, filtration, and on-line analytics) to make solvent and high-purity grades for electronics and pharmaceutical customers. In downstream channels, propanol is distributed through bulk terminals and drum/IBC packaging to chemical distributors and via direct contracts with coatings, inks, pharma, and electronics fabs; as a result, grade certification, contamination control for ultra-high-purity IPA, and short-notice feedstock disruptions increasingly shape delivery performance, including the India government action in April 2026 to reallocate propane/propylene streams to major IPA producers (including DFPCL) to stabilize supply for the pharmaceutical chain.

Competitive Landscape

The propanol market is moderately consolidated. BASF, Dow, and ExxonMobil leverage integrated steam crackers, acetone derivatives, and downstream specialty lines to control costs and assure quality. Feedstock volatility therefore disproportionately pressures smaller producers lacking captive propylene streams. ExxonMobil’s Baton Rouge upgrade signals competition moving toward ultra-high-purity segments targeting semiconductor yields. Larger firms are also trialing continuous oxo-alcohol reactors that raise throughput and lower energy intensity, reinforcing scale advantages.

Sustainability is a boundary for differentiation. LanzaJet’s alcohol-to-jet technology positions it as a first mover in renewable aviation fuel, working with airlines on offtake agreements that secure volume and provide margin visibility. Petrochemical incumbents react by announcing bio-propyl alcohol pilots or co-processing initiatives within existing cracker complexes. Strategic partnerships increasingly focus on carbon capture, renewable hydrogen, and circular feedstocks that align with Scope 3 targets demanded by end customers.

Technology licensing and geographic expansion round out competitive moves. Growth in Asia Pacific spurs partnerships with contract manufacturers near end customers, allowing quick response to purity deviations and shorter logistics chains. Intellectual property around purification, real-time analytics, and fermentation strains becomes central to negotiating leverage and long-term relevance within the evolving propanol market.

Propanol Industry Leaders

BASF SE

Dow

Eastman Chemical Company

Exxon Mobil Corporation

LyondellBasell Industries N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunity is centered on asset upgrades and integration measures that increase output flexibility across propanol, n-propanol derivatives, and adjacent oxo chains, while also improving the carbon profile of existing sites. OXEA's July 2026 final investment decision for a major Bay City, Texas expansion, alongside a long-term syngas supply agreement with Air Liquide for a new on-site syngas unit using CO2 recirculation technology (site preparation scheduled for Q3 2026, completion by end-2028), signals brownfield investment intended to support higher propanol and butanol production through upstream and utilities integration.

A second opportunity relates to tiered, application-specific supply where high-purity solvent needs (notably semiconductor cleaning) and pharmaceutical-grade requirements drive additional purification, QA, and dedicated logistics relative to commodity solvent distribution. The combination of specialty-grade pull from advanced-node electronics and policy-linked pharma build-out in Asia (for example, India PLI-linked API capacity additions referenced in the report context) supports contract structures that prioritize reliability and compliance, while bio-based pathways for aviation fuel offer a higher-value outlet in which producers can differentiate through feedstock traceability and process emissions management rather than competing only on propylene-linked economics.

Recent Industry Developments

- July 2026: OXEA confirmed a final investment decision for a major capacity expansion at its Bay City, Texas site, increasing propionaldehyde capacity to enable higher propanol and butanol production. The company also entered a long-term syngas supply agreement with Air Liquide for a new on-site syngas unit using CO2 recirculation technology, with site preparation scheduled for Q3 2026 and completion targeted by end-2028. This adds integrated feedstock and utilities resilience at a key North American oxo platform and supports supply availability for downstream propanol users.

- March 2026: Eastman Chemical Company announced an off-list price increase for Eastman N-Propyl Alcohol in North America and Latin America, effective March 17, 2026. The announcement reflects ongoing cost and supply tightness management in oxo-alcohol chains and passes through part of volatility tied to upstream feedstocks and operating conditions. For buyers in inks, coatings, and intermediates, it reinforces the value of secured contracts and qualified alternate sourcing.

- June 2024: Moeve initiated construction of Spain's first isopropyl alcohol plant, designed for 80,000 tons of capacity with a stated investment of EUR 75 million. Building regional IPA capacity supports European supply diversification and reduces dependence on imports for solvent and sanitizer applications. The project also strengthens local availability for higher-spec grades as downstream users tighten quality and compliance requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of propanol sold for industrial and commercial use, across n-propanol, isopropanol, and bio-based propanol. The sizing tracks demand from key downstream uses such as solvents, chemical intermediates, and cleaning applications, with views built across major regions.

Scope exclusions: The model excludes internal plant transfers that are not priced market sales, and it also excludes downstream finished products where propanol is only a minor ingredient.

Segmentation Overview

- By Product Type

- n-Propanol

- Isopropanol

- Bio-based Propanol

- By End-use Industry

- Pharmaceutical

- Chemicals (Solvents and Intermediates)

- Personal Care and Cosmetics

- Printing Inks

- Paints and Coatings

- Electronics Cleaning

- Adhesives and Sealants

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacifc

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base model structure and to set realistic ranges for production, trade, and end-use pull. We used public references such as the US Energy Information Administration (EIA), US International Trade Commission (USITC) trade statistics, UN Comtrade, and US EPA publications on VOC related rules that can influence solvent demand.

In parallel, we reviewed company annual reports, investor presentations, and technical papers in peer reviewed chemistry and process journals to confirm how propanol is produced and where it is consumed. Patent databases and an import and export shipment-level database were also used selectively to sense-check capacity additions, plant restarts, and shifting trade lanes when public disclosures were limited. The sources listed here are illustrative, and additional public references were consulted for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary interviews focused on validating pricing logic, product mix, and the actual demand split across solvents, intermediates, and electronics cleaning, since these components move differently by region. We spoke with a mix of producers, distributors, and large end users across APAC, EMEA, and the Americas, then used follow-up questions to close gaps on utilization, typical contract length, and how bio-based volumes are counted in day-to-day reporting.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 49% |

| Mid tier: 58% | Functional/Unit leaders: 29% | EMEA: 29% |

| Smaller Players: 16% | Managers: 58% | Americas: 22% |

Market-Sizing & Forecasting

The core sizing starts from a top-down reconstruction where production capacity signals, trade flows, and downstream consumption indicators are combined to rebuild regional demand, then converted into value using observed price bands. To keep the output practical, we corroborate this view with selective bottom-up approximations, such as sampling supplier shipments to major end uses and checking implied volume times average selling price. Where the two views do not align, we adjust based on which signals better match the region and product split.

Key variables in this market include the split between n-propanol and isopropanol, the share of demand tied to solvents and chemical intermediates, and the pull from electronics cleaning where purity requirements can shift pricing. We also tracked indicators such as announced capacity additions and restarts, import and export movements by major trading regions, and typical contract pricing behavior versus spot pricing, since these shape the yearly value line. For forecasting, we ran scenario analysis to reflect different paths for feedstock and energy costs, then selected the preferred case after primary feedback on how end users expect volumes to recover and how quickly pricing is likely to normalize. When direct volume visibility was weak, we filled gaps with proxy splits based on trade patterns and validated them through interview-based utilization and channel checks.

Data Validation & Update Cycle

Validation was performed using several checks to keep the numbers consistent with real market signals. Model outputs were compared with independent indicators, including regional trade totals, capacity movement timelines, and known end-use demand trends, and unusual jumps were reworked until the driver was clearly explained in the context of those inputs.

Before sign-off, the work is reviewed in steps, beginning with internal consistency checks, then an analyst review of key assumptions like price ranges and product mix, and then re-contact triggers are used when a major mismatch appears during the final read. The report is refreshed annually, with interim updates made when material events occur, such as large capacity changes or sharp shifts in feedstock-linked pricing. Right before delivery, a final pass is completed so the latest view can be traced back to specific inputs.

Mordor Intelligence's Propanol Market Size Measured Against Other Published Estimates

Published propanol market estimates can vary widely because authors do not always align on what is being counted, how prices are averaged, and which year is treated as the headline reference point. Differences also show up when one study leans more on capacity headlines, while another emphasizes confirmed consumption signals.

Some external figures take a broader framing by mixing adjacent alcohol value pools or by applying a single global price curve that does not reflect purity and end-use differences. In Mordor Intelligence, the total is limited to n-propanol, isopropanol, and bio-based propanol sales, and prices are set using region-level bands checked against trade movement and primary channel feedback.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.37 B (2026) | |

| Global Consultancy A | USD 3.83 B (2025) | Uses an earlier reference year and a wider product framing, and it can compress regional price differences by relying on averaged pricing assumptions across end uses. |

| Industry Publisher B | USD 3.22 B (2024) | Leans more on reported sales aggregates and conservative growth settings, and it does not clearly show how product mix and purity-driven pricing are adjusted across regions. |

Looking at the table, the spread is mainly explained by scope breadth, price-setting logic, and the chosen reference year for the headline value. By linking volumes to production and trade signals, then validating price bands through primary checks, the estimate stays transparent, repeatable, and easier to reconcile with real market movement over time.

Key Questions Answered in the Report

What is the current size of the propanol market?

The propanol market is valued at USD 3.37 billion in 2026 and is projected to reach USD 4.19 billion by 2031.

Which product segment dominates the propanol market?

Isopropanol leads with 54.12% revenue share in 2025, driven by its versatility in pharmaceutical, personal care, and industrial cleaning applications.

Why is electronics cleaning the fastest-growing end-use for propanol?

Advanced node semiconductor fabrication requires ultra-high-purity isopropanol to prevent particle contamination, pushing segment growth at a 5.82% CAGR.

How are volatile propylene prices affecting propanol producers?

Feedstock cost swings squeeze standalone producers’ margins, favoring integrated petrochemical players that secure propylene from captive crackers.

What role does bio-propanol play in sustainable aviation fuel?

Bio-propanol serves as a key intermediate in alcohol-to-jet pathways, and projects such as USA BioEnergy’s Texas facility highlight its emerging importance in low-carbon fuel strategies.

Which region offers the strongest growth prospects?

The Middle East and Africa region is poised for the fastest CAGR as new isopropanol capacity in Saudi Arabia leverages abundant propylene and rising local demand.

Page last updated on: