Butadiene Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

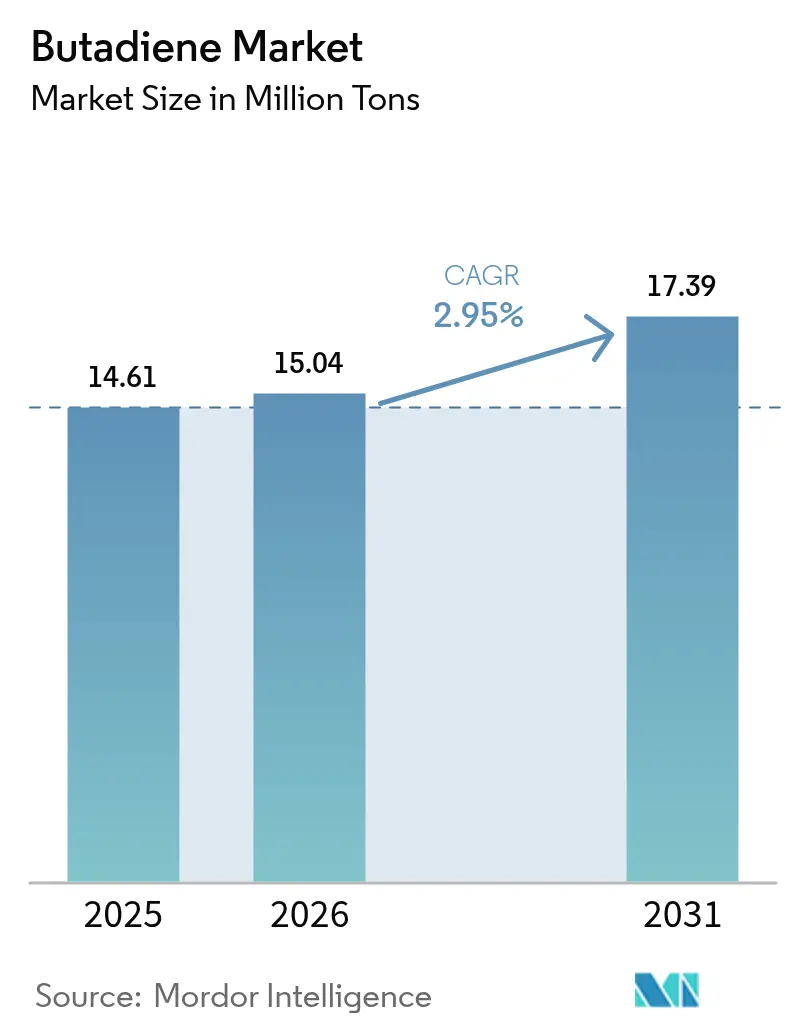

| Market Volume (2026) | 15.04 Million tons |

| Market Volume (2031) | 17.39 Million tons |

| Growth Rate (2026 - 2031) | 2.95% CAGR |

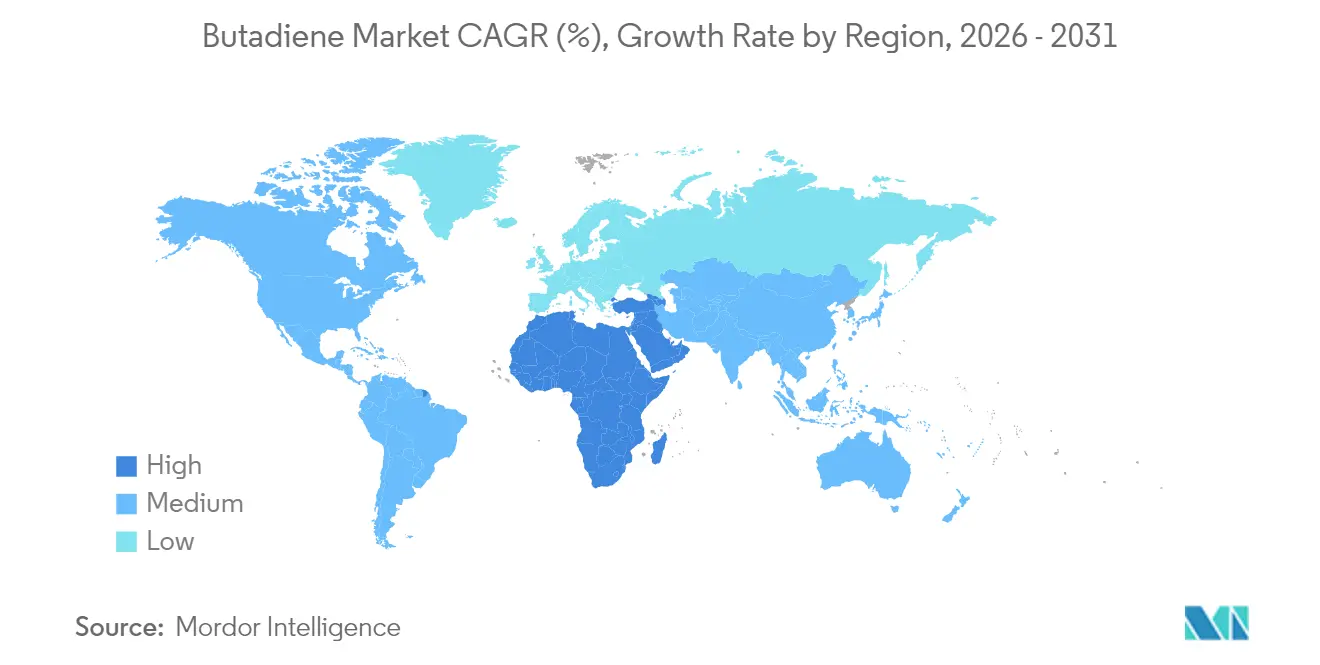

| Fastest Growing Market | Middle-East and Africa |

| Largest Market | Asia Pacific |

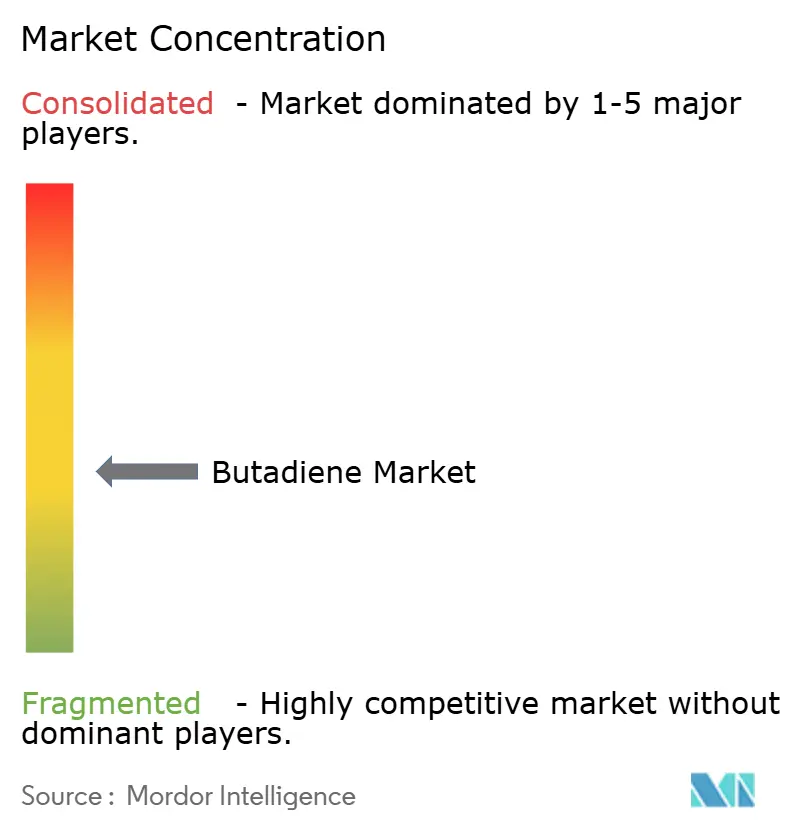

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Butadiene Market Analysis by Mordor Intelligence

The Butadiene market size is expected to grow from 14.61 million tons in 2025 to 15.04 million tons in 2026 and is forecast to reach 17.39 million tons by 2031 at 2.95% CAGR over 2026-2031. Sustained momentum stems from Asia-Pacific capacity additions, rising electric-vehicle (EV) tire production that favors solution styrene-butadiene rubber (S-SBR), and pilot-scale bio-based feedstocks that erode legacy steam-cracker cost advantages. Polybutadiene accounted for 26.67% of the 2024 application volume, as tire makers continued to specify high-cis grades for tread compounds. Meanwhile, acrylonitrile-butadiene-styrene (ABS) is projected to grow at a 4.02% CAGR through 2030, driven by consumer-electronics brands localizing their supply chains to offset tariff costs. End-user demand skewed toward tire and rubber at 32.12% of the 2024 volume, yet the chemical segment’s 3.74% CAGR indicates that adiponitrile producers are pivoting to butadiene cyanation routes that lower capital intensity compared to cyclohexane oxidation. Regionally, the Asia-Pacific held 52.12% of the 2024 volume, as Chinese propane-dehydrogenation (PDH) complexes increased nameplate capacity by 77% between 2022 and 2025, despite spot prices slipping below USD 900 per ton in early 2024. Competitive intensity remains high, with Sinopec leading synthetic-rubber nameplate capacity at 1,915 kilotons, closely followed by ARLANXEO at 1,889 kilotons and PetroChina at 1,380 kilotons.

Key Report Takeaways

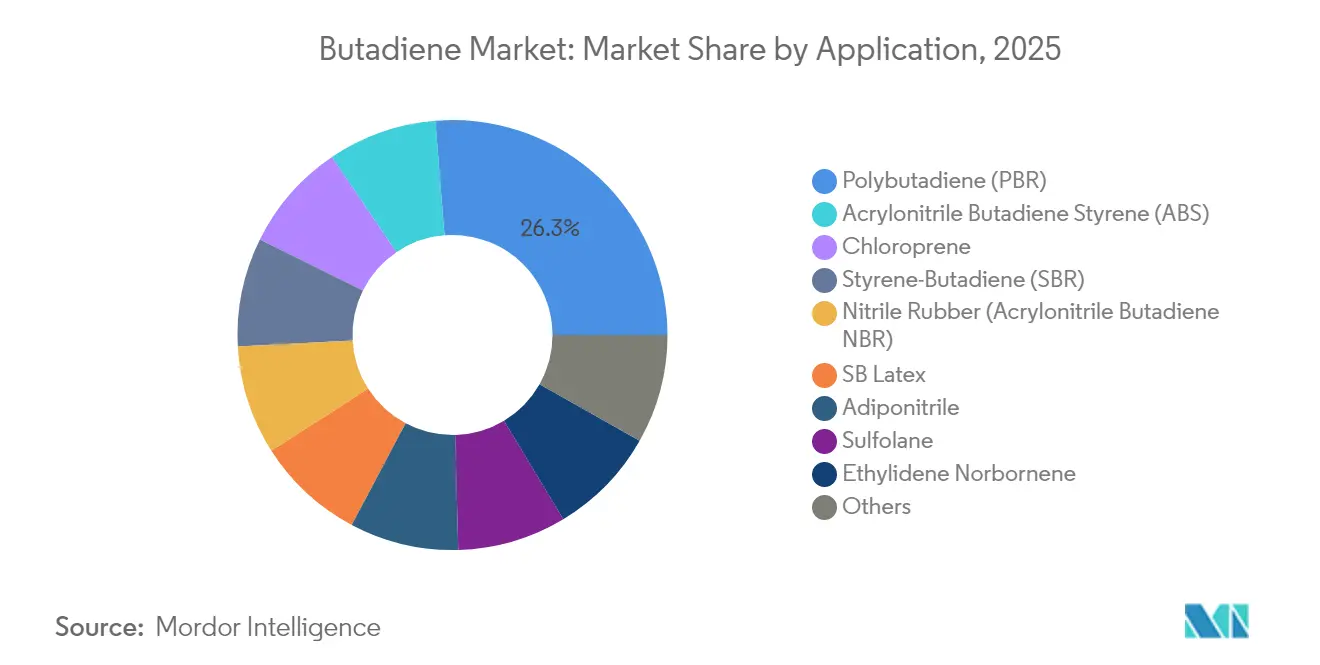

- By application, polybutadiene led with 26.27% of the butadiene market share in 2025, while ABS is projected to expand at a 3.94% CAGR through 2031.

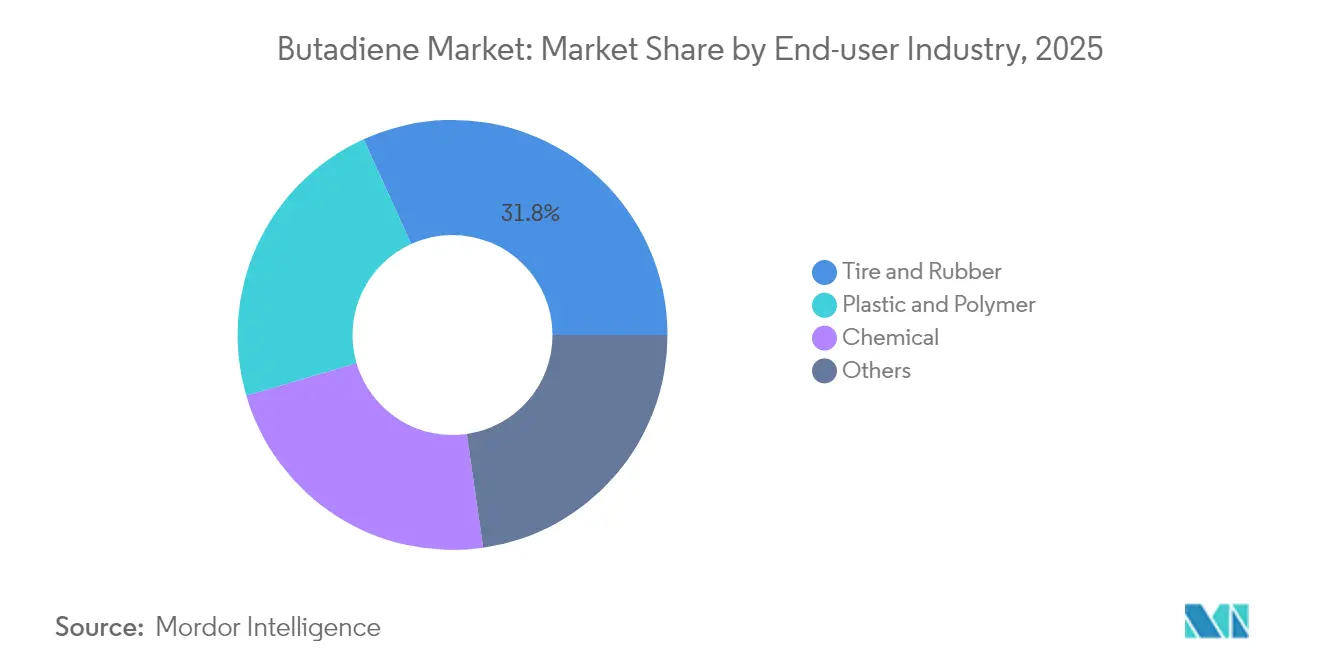

- By end-user industry, the tire and rubber segment accounted for a 31.78% share of the butadiene market size in 2025, whereas the chemical segment is expected to advance at a 3.62% CAGR to 2031.

- By geography, the Asia-Pacific region commanded 51.62% of the 2025 volume, and the Middle East & Africa region is forecast to register the fastest growth of 5.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Butadiene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising automotive and tire production in Asia-Pacific | +0.9% | Asia-Pacific core; spillover to ASEAN | Medium term (2-4 years) |

| Expanding ABS demand from consumer electronics | +0.5% | Global; most acute in North America, Europe, East Asia | Short term (≤ 2 years) |

| EV-ready high-performance S-SBR adoption | +0.7% | Global EV hubs | Medium term (2-4 years) |

| Rapid capacity additions in bio-butadiene | +0.3% | Europe, North America pilots; future Asia-Pacific scale-up | Long term (≥ 4 years) |

| Growth of Li-ion battery binders using SBR | +0.4% | Asia-Pacific, expanding to Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Automotive and Tire Production in Asia-Pacific

Asia-Pacific tire output surpassed 1.3 billion units in 2024, supported by China, India, and Japan, which jointly contributed about 70% of regional volume[1]European Tyre & Rubber Manufacturers’ Association, “Quarterly Statistics Q1 2025,” etrma.org. High-cis polybutadiene accounts for 10-15% of passenger-tire tread formulations, thereby directly increasing butadiene market demand. Thailand’s strong natural-rubber supply and Indonesia’s motorcycle-tire ecosystem underpin regional growth, while India and Vietnam’s shift toward radial truck tires increases synthetic-rubber use per unit. Imports into the European Union and the United Kingdom increased by 18% year-over-year in 2024, indicating that Asian producers are capturing incremental demand even in mature markets.

Expanding ABS Demand from Consumer Electronics

ABS resin maintains a 15-20% price premium over high-impact polystyrene because it offers superior impact strength and a smoother surface finish. US trade measures enacted in 2025 lifted landed costs for imported electronics by roughly 10%, prompting brands to nearshore assembly and secure domestic ABS, tightening butadiene balances in North America. Because butadiene accounts for 20-25% of ABS composition, each incremental percentage point of ABS output drives 0.2-0.25 percentage points of additional butadiene consumption. Automotive interior-trim growth further supports ABS volumes, as ABS-polycarbonate blends meet stringent flame-retardancy standards without the use of halogenated additives.

EV-Ready High-Performance S-SBR Adoption

Solution-polymerized S-SBR delivers lower rolling resistance than emulsion SBR because its linear microstructure and controlled vinyl content minimize hysteresis losses. Tire makers chasing rolling-resistance coefficients below 6.5 kg per ton for EV range targets favor these grades. LG Chem and Synthos commercialized S-SBR compounds with 40–50% vinyl content in 2024 that support EU AA/AAA labels while preserving tread life. Bridgestone patents filed the same year describe functionalized chain ends that chemically bond to silica fillers, reducing costly coupling agents by roughly 8% and further improving wet grip[2]Bridgestone Corporation, “Functionalized SBR Patent Filing 2024,” bridgestone.com.

Rapid Capacity Additions in Bio-Butadiene

Michelin, IFP Energies Nouvelles, and Axens initiated a French demonstration unit in January 2024, which converts bioethanol into butadiene, achieving a 64% single-pass conversion and 68% selectivity. The route bypasses naphtha cracking and can cut Scope 3 tire emissions up to 50% when feedstock is sourced from sugarcane or corn stover. Reliance Industries plans to integrate bio-naphtha co-processing at its Jamnagar complex by 2030, indicating that refiners view renewable feedstocks as a hedge against impending carbon border taxes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicity and tightening exposure limits | −0.4% | Global; strictest in North America, Europe | Short term (≤ 2 years) |

| Crude-oil price volatility | −0.6% | Global; acute in naphtha-cracker regions | Short term (≤ 2 years) |

| China overcapacity depressing margins | −0.8% | Asia-Pacific core; export pressure elsewhere | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Toxicity and Tightening Exposure Limits

The US Occupational Safety and Health Administration enforces an 8-hour permissible exposure limit of 1 ppm and a 15-minute excursion limit of 5 ppm for butadiene, prompting cracker operators to install closed-loop vapor-recovery systems and continuous monitors, often costing USD 5–8 million per facility. California’s Proposition 65 labeling requirements add downstream compliance expenses, while the European Chemicals Agency is proposing a 0.5 ppm workplace limit, half the current US threshold. Smaller extraction units are disproportionately impacted, driving consolidation and trimming the global count of butadiene extraction facilities to an estimated 160 by 2026.

Crude-Oil Price Volatility

Spot butadiene fell below USD 900 per ton in early 2024 as Brent crude fluctuated between USD 70 and USD 85 per barrel, compressing naphtha-cracker margins to USD 60 per ton of ethylene. A USD 10-per-barrel swing in oil generally shifts butadiene realizations by USD 100–120 per ton. Chinese PDH units maintained 85–90% utilization rates when propane-naphtha spreads exceeded USD 150 per ton, partly insulating them from crude price swings and intensifying pressure on steam-cracker economics across Europe and Northeast Asia.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Polybutadiene Dominance Anchored in Tire Tread

Polybutadiene captured 26.27% of 2025 application volume, confirming its entrenched role in tire tread and sidewall formulations where high-cis grades maximize abrasion resistance and cold-weather flexibility. SIBUR expanded its Russian polybutadiene capacity in 2024, while ARLANXEO is building a 140,000-ton-per-year ultra-high-cis facility in Jubail, slated for a 2026 start-up. ABS resins are projected to advance at a 3.94% CAGR to 2031, driven by demand for consumer electronics and automotive interior trim, which is expected to tighten regional butadiene market balances. Styrene-butadiene rubber remains vital for mainstream tire producers that balance wet grip and rolling resistance; solution grades are steadily displacing emulsion types in EV fitments.

Nitrile rubber accounts for 60% of automotive seal applications, while emerging hydrogenated nitrile rubbers target EV battery packs that face sustained 150°C thermal cycling. Adiponitrile produced from butadiene cyanation feeds nylon 6,6 for under-hood components, with Invista increasing its North American capacity in 2024 to meet a 4–5% annual growth in this segment. Smaller outlets, such as chloroprene rubber, sulfolane, and ethylidene norbornene, help maintain a stable baseline demand; price rises of USD 500 per ton in 2024 reflected higher feedstock and energy costs.

By End-User Industry: Tire and Rubber Lead, Chemical Segment Accelerates

Tire and rubber held a 31.78% share of 2025 demand, supported by global tire output approaching 1.8 billion units and steady replacement-market pull even amid automotive downturns. The Asia-Pacific region accounts for approximately 60% of that volume, although North American and European producers are introducing higher-margin ultra-high-performance lines that rely on functionalized S-SBR and specialty polybutadiene grades. The chemical segment is projected to expand at a 3.62% CAGR as adiponitrile, ABS, and lithium-ion binder applications scale; each 1% uptick in ABS production alone lifts butadiene demand by 0.2–0.25 percentage points.

Localization trends are encouraging electronics and auto OEMs to source nearshore polymers, tightening butadiene supply in Mexico and the US Gulf Coast. Bio-based pilot streams, such as Michelin’s 2024 demonstration unit with a 64% single-pass conversion rate, provide derivative producers with a pathway to reduce Scope 3 emissions by up to 50% and capture premium pricing from sustainability-focused customers. Smaller sectors, including adhesives and coatings, comprise roughly 11% of total demand and move broadly in line with construction cycles.

Geography Analysis

The Asia-Pacific region represented 51.62% of the 2025 volume, thanks to Chinese PDH complexes that added capacity 77% above 2022 levels, enabling on-purpose production costs 10–15% below naphtha-cracker averages when propane-naphtha spreads widen beyond USD 150 per ton. Lotte Chemical increased its extraction capacity to 210,000 tons per year in 2024, while Reliance Industries plans a 0.7-million-ton expansion at Jamnagar, featuring bio-naphtha integration, by 2030. Despite capacity gains, spot prices dipped below USD 900 per ton in early 2024, compelling Chinese producers to export at discounts that squeezed Middle Eastern and North American competitors. Japan and South Korea are curbing output—Zeon intends to reduce Tokuyama elastomer lines in fiscal 2026—and the Lotte-Ube JV in Malaysia is winding down after years of margin pressure.

Middle East & Africa is projected to grow at a 5.89% CAGR, led by Saudi approvals for a Sipchem-LyondellBasell mixed-feed cracker capable of 1.5 million tons of ethylene and 1.8 million tons of derivatives, including butadiene, with a final investment decision reached in February 2025. Tasnee’s 3.3 million-ton petrochemical complex, due by 2030, and ADNOC’s bid to acquire specialty assets, such as Covestro, illustrate the region’s move to monetize associated gas via integrated platforms. Gulf Cooperation Council chemical revenue is forecast to climb from USD 85.8 billion in 2023 to USD 133.3 billion by 2030, anchoring incremental butadiene demand tied to downstream diversification.

North America and Europe contend with margin compression and asset rationalization. Shell sold its Geismar extraction unit to INEOS in 2023, and Versalis shuttered its 105,000-ton polybutadiene line at Grangemouth in 2024 as energy costs outstripped peer regions. Goodyear’s announced divestiture of its Beaumont and Houston chemical assets under a USD 1.3 billion cost-reduction program underscores the shift toward higher-value performance tires over commodity elastomers. European tire output rose 3% in Q1 2025, but Chinese tire imports surged 18% in 2024, highlighting competitiveness challenges for regional producers. South America remains a smaller contributor but benefits from ARLANXEO’s expanded Triunfo capacity and proximity to natural-rubber plantations that facilitate blended formulations.

Competitive Landscape

The Butadiene market is moderately fragmented. Sinopec leads global synthetic-rubber capacity at 1,915 kilotons, followed by ARLANXEO at 1,889 kilotons, PetroChina at 1,380 kilotons, and Sibur at 1,278 kilotons, according to IISRP’s 2024 rankings. Consolidation continues: Eneos acquired JSR’s elastomers arm in 2022, Synthos bought Trinseo’s rubber assets in 2021, and INEOS secured Shell’s Geismar facility in 2023, leaving mid-tier competitors challenged by feedstock volatility and stricter environmental rules.

Butadiene Industry Leaders

China Petroleum & Chemical Corporation

LyondellBasell Industries Holdings BV

BASF

LG Chem

INEOS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: A joint project between Russia's Tatneft and Kazakhstan's Samruk-Kazyna wealth fund to build a butadiene plant was announced to begin its investment phase, with China Tianchen Engineering Corporation serving as the contractor.

- February 2025: Zeon Corporation and The Yokohama Rubber Co., Ltd. announced that they have agreed to establish a bench facility to demonstrate technology for producing butadiene from ethanol derived from plant-based and other sustainable materials with high efficiency. The facility will be installed at Zeon’s Tokuyama Plant.

Global Butadiene Market Report Scope

Butadiene is a colorless, non-corrosive gas used for the production of resins and plastics, including butadiene rubber, styrene rubber, adiponitrile, polychloroprene, nitrile rubber, and others. It is primarily produced through the extractive distillation of by-products from steam crackers during the production of ethylene and propylene.

The butadiene market is segmented by application, end-user industry, and geography. By application, the market is segmented into polybutadiene (PBR), chloroprene, styrene-butadiene (SBR), nitrile rubber (acrylonitrile butadiene NBR), acrylonitrile butadiene styrene (ABS), adiponitrile, sulfolane, ethylidene norbornene, styrene-butadiene latex, and other applications. By end-user industry, the market is segmented into plastic and polymer, tire and rubber, chemical, and others. The report also covers the market size and forecasts for the butadiene market in 16 countries across the major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Polybutadiene (PBR) |

| Chloroprene |

| Styrene-Butadiene (SBR) |

| Nitrile Rubber (Acrylonitrile Butadiene NBR) |

| SB Latex |

| Acrylonitrile Butadiene Styrene (ABS) |

| Adiponitrile |

| Sulfolane |

| Ethylidene Norbornene |

| Others |

| Plastic and Polymer |

| Tire and Rubber |

| Chemical |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Polybutadiene (PBR) | |

| Chloroprene | ||

| Styrene-Butadiene (SBR) | ||

| Nitrile Rubber (Acrylonitrile Butadiene NBR) | ||

| SB Latex | ||

| Acrylonitrile Butadiene Styrene (ABS) | ||

| Adiponitrile | ||

| Sulfolane | ||

| Ethylidene Norbornene | ||

| Others | ||

| By End-user Industry | Plastic and Polymer | |

| Tire and Rubber | ||

| Chemical | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected global volume for the butadiene market in 2031?

The butadiene market is expected to reach 17.39 million tons by 2031, reflecting a 2.95% CAGR between 2026 and 2031.

Which application currently dominates demand for butadiene?

Polybutadiene remains leading, accounting for 26.27% of 2025 application volume due to its critical role in tire tread compounds.

Which region shows the fastest growth outlook for butadiene derivatives?

The Middle East & Africa region is forecast to record the fastest 5.89% CAGR through 2031, driven by large mixed-feed cracker projects.

How are electric vehicles influencing future butadiene consumption?

EVs boost demand for high-performance S-SBR, which requires butadiene feedstock, and adoption is projected to lift butadiene requirements by 0.7 percentage points annually.

What are the main regulatory challenges facing butadiene producers?

Tightening exposure limits, such as OSHA’s 1 ppm TWA and proposed 0.5 ppm limits in Europe, compel costly vapor-recovery upgrades at production and handling sites.

Page last updated on: