Termite Bait Systems Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 90 Million |

| Market Size (2031) | USD 122 Million |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Termite Bait Systems Market Analysis by Mordor Intelligence

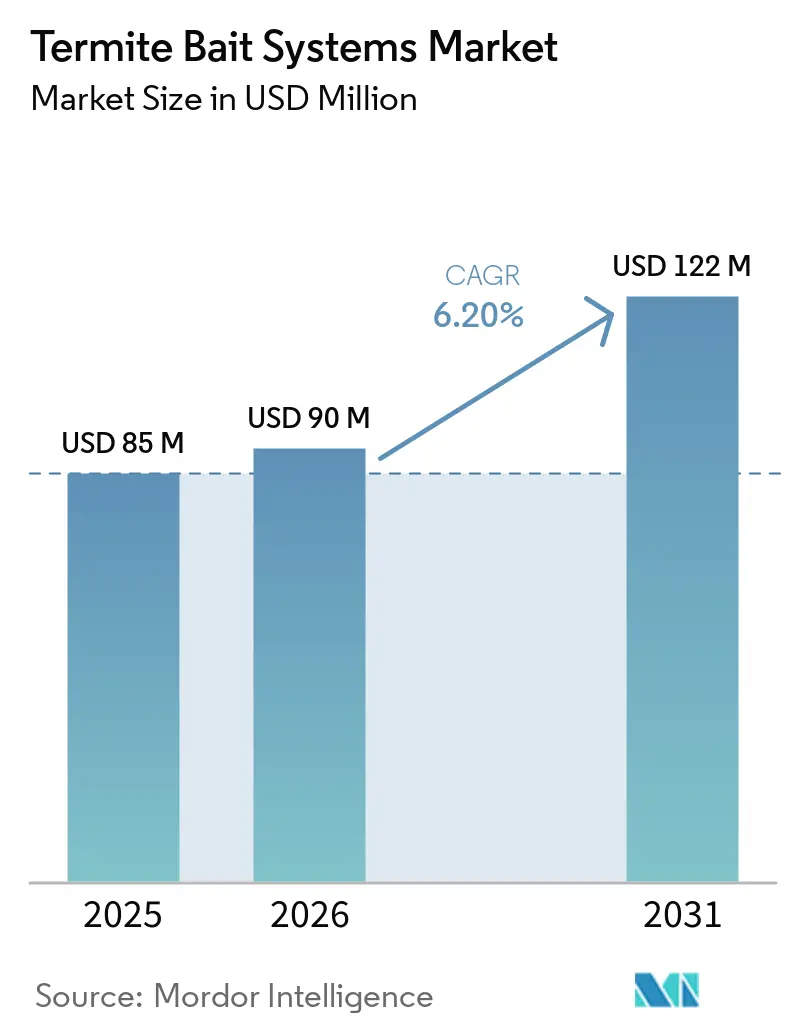

The Termite Bait Systems Market size is projected to be USD 85 million in 2025, USD 90 million in 2026, and reach USD 122 million by 2031, growing at a CAGR of 6.20% from 2026 to 2031. Increasing restrictions on soil-applied termiticides, expanding infrastructure in termite-prone regions, and the adoption of Internet of Things (IoT) monitoring are driving demand for colony-elimination platforms that reduce environmental exposure and labor costs. Restrictions by the Environmental Protection Agency (EPA) on chlorpyrifos and ongoing reviews of fipronil in several Asia-Pacific countries are accelerating the adoption of insect growth regulators (IGRs). Additionally, growing agro infrastructure in countries such as India, the Philippines, and Nigeria is expanding the potential customer base for above-ground stations designed for installation on concrete columns where soil access is limited.

Key Report Takeaways

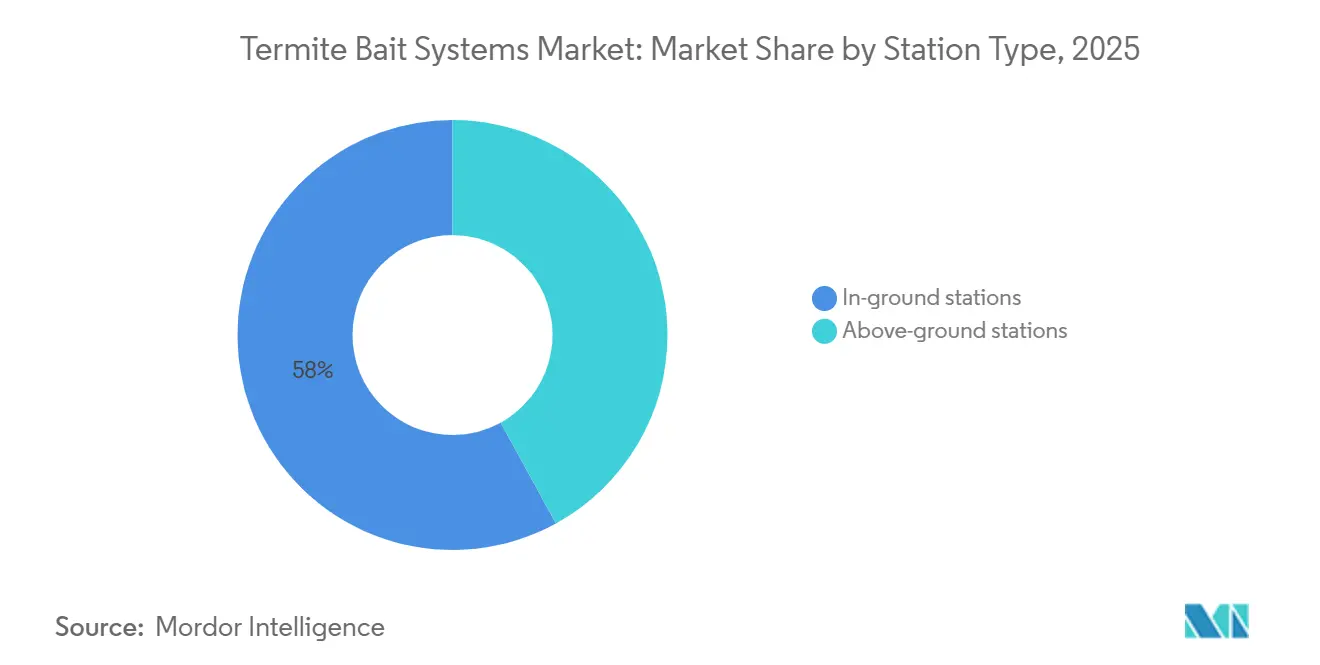

- By station type, in-ground systems led with the largest 58% of the termite bait systems market share in 2025. The Above-ground units market size is projected to grow at the fastest 7.9% CAGR from 2026 to 2031.

- By active ingredient, insect growth regulators accounted for the largest 54% of the termite bait systems market share in 2025. The chlorfenapyr market size is projected to grow at the fastest 8.7% CAGR from 2026 to 2031.

- By termite species, subterranean termites accounted for the largest 68% of the termite bait systems market share in 2025. Dampwood termites market size is projected to grow at the fastest 6.8% CAGR from 2026 to 2031.

- By end-user, commercial farms held the largest 46% of the termite bait systems market share in 2025. The agro-industrial and infrastructure market size is anticipated to expand at the fastest 8.6% CAGR from 2026 to 2031.

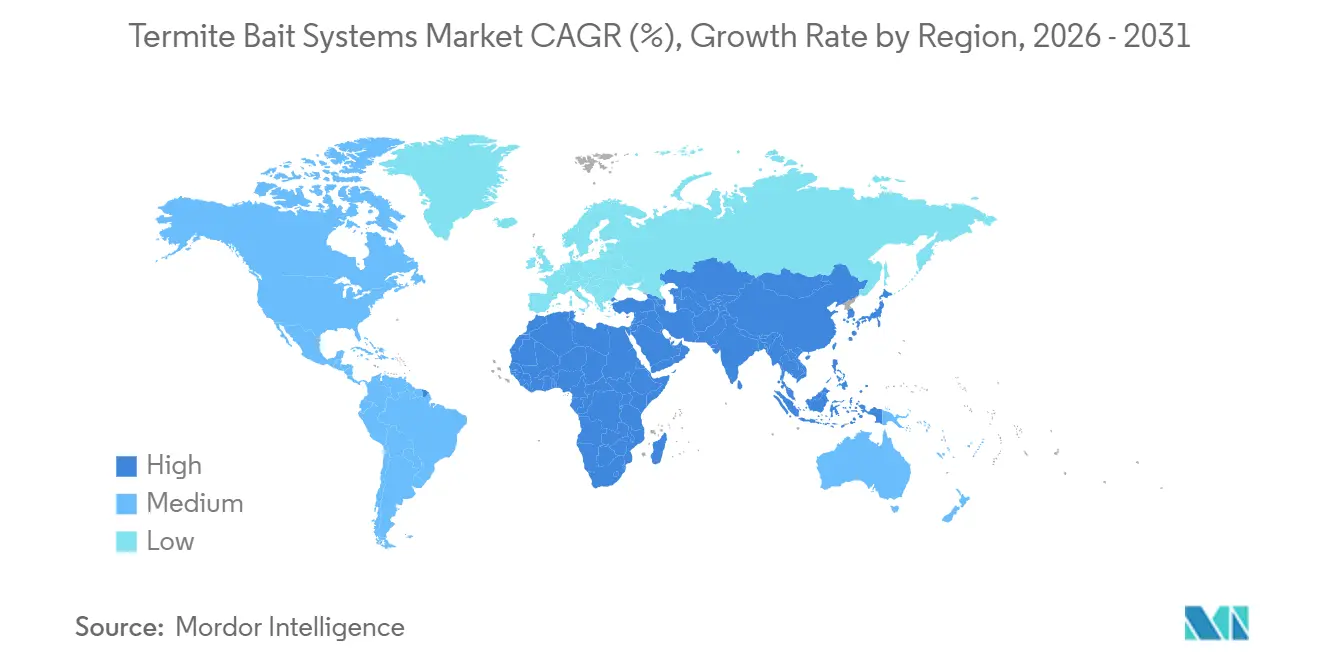

- By geography, Asia-Pacific dominated with the largest 40% of the termite bait systems market share in 2025. Africa market size is projected to grow at the fastest 7.8% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Termite Bait Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Restrictions on liquid termiticides tightening globally | +1.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Infrastructure expansion in termite-prone climates | +1.0% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Rising crop-loss awareness among commercial farms | +0.8% | South America, Africa, and Asia-Pacific | Short term (≤ 2 years) |

| Government subsidy programs for smallholder control | +0.6% | Africa and South Asia, early gains in Botswana and Ghana | Medium term (2-4 years) |

| Embedded IoT monitoring that reduces service labor | +0.7% | North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Direct-to-farm subscription models lowering upfront cost | +0.5% | Global, early traction in North America and Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Restrictions on Liquid Termiticides Tightening Globally

Restrictions on liquid termiticides are tightening globally due to rising concerns over groundwater contamination and environmental safety. Regulatory bodies are increasingly limiting the use of conventional soil-applied chemicals, encouraging a shift toward safer alternatives. According to the United States Environmental Protection Agency (EPA), in December 2024 the agency proposed revoking most tolerances for chlorpyrifos and limiting its use to only 11 food and feed crops, reflecting stricter regulatory control [1]Source: United States Environmental Protection Agency, “Chlorpyrifos,” epa.gov. These developments are accelerating the adoption of insect growth regulator (IGR)-based bait systems, which offer targeted pest control with minimal environmental impact, thereby supporting demand growth in the termite bait systems market.

Infrastructure Expansion in Termite-Prone Climates

The rapid expansion of agriculture and related infrastructure in China is increasing the risk of termite infestations, driving demand for preventive control measures such as bait stations. A 2026 study by researchers from Northwest University, China, utilizing a MaxEnt model, identified termite species like Coptotermes and Reticulitermes as significant ecological and agricultural threats. The study revealed that risk habitats for these species span approximately 0.73 million km² and 2.25 million km², respectively [2]Source: Northwest University, China, “Assessing the Invasive Risk of Rhinotermitidae in China Using the MaxEnt Model,” 2026 . Additionally, the findings emphasize that termites cause substantial damage to crops, forestry systems, and agricultural assets, highlighting the growing vulnerability of cultivated areas and storage facilities.

Rising Crop-Loss Awareness Among Commercial Farms

Rising awareness of termite-induced crop losses is encouraging the adoption of bait systems among commercial agricultural operators. As per the National Center for Biotechnology Information reported termite infestation in cocoa farms in Cote d’Ivoire highlights the substantial yield risks under specific farming conditions. These kinds of losses are driving growers to implement preventive, colony-elimination strategies, such as bait systems, rather than relying on reactive chemical treatments. Large-scale plantation crops, including cocoa, sugarcane, and coffee, are increasingly incorporating termite monitoring and baiting programs to safeguard productivity and mitigate long-term damage.

Government Subsidy Programs for Smallholder Control

Government-supported subsidy programs are driving the adoption of termite bait systems, particularly in developing regions. Public initiatives are encouraging integrated pest management strategies that emphasize safer and more targeted control methods instead of traditional chemical treatments. These programs often provide financial assistance along with training and technical support, reducing the barriers to adopting bait-based solutions. As awareness and accessibility increase, subsidy-driven adoption is accelerating the growth of the termite bait systems market and expanding its presence in rural agricultural areas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront installation cost versus soil sprays | -0.9% | Global, acute in Africa and South Asia | Short term (≤ 2 years) |

| Limited availability of trained rural technicians | -0.6% | Africa, South America, and rural Asia-Pacific | Medium term (2-4 years) |

| Seasonal farm cash-flow delaying bait replacement cycles | -0.5% | South America, Africa, and South Asia | Short term (≤ 2 years) |

| Fragmented registration status of novel ingredients | -0.7% | Global, delays in Asia-Pacific and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Installation Cost Versus Soil Sprays

The high upfront installation cost continues to be a significant restraint for termite bait systems when compared to conventional liquid treatments. Soil-applied termiticides are commonly used due to their lower initial cost and ease of application. This cost advantage makes liquid treatments more appealing, especially for smallholder farms and cost-conscious users. While bait systems offer long-term benefits such as colony elimination and reduced environmental impact, the higher initial investment remains a barrier to widespread adoption. Although financing models and subsidy programs are being introduced, large-scale adoption is still hindered by these initial cost challenges.

Limited Availability of Trained Rural Technicians

The limited availability of trained technicians in rural areas hampers the effective implementation of termite bait systems. Uneven access to skilled agricultural extension services in developing regions further diminishes the effectiveness of advanced pest management practices. Proper installation of bait systems necessitates accurate identification of termite activity, optimal placement of stations, and continuous monitoring factors often absent in remote locations. Consequently, improper implementation can lower system efficiency and deter adoption. Although simplified bait designs and training programs are being introduced, the lack of technical expertise remains a significant barrier.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Station Type: In-Ground Dominance Meets Urban Retrofit Demand

In-ground systems are accounted for the largest 58% market share of the termite bait systems market in 2025. This dominance is attributed to their effectiveness in targeting subterranean termite colonies and their compatibility with pre-construction treatment practices. In agricultural settings, these systems are extensively used to protect crop fields, plantations, irrigation infrastructure, and storage facilities, where termites pose risks to roots, seedlings, and wooden farm structures. Installed directly into the soil, these systems enable continuous interaction with termite foraging tunnels, enhancing bait interception rates. Their capability to provide long-term colony elimination with minimal disruption to soil structure supports their adoption in farming and related agricultural operations.

Above-ground units are projected to grow at the fastest CAGR of 7.9% from 2026 to 2031, driven by rising demand for retrofit solutions in existing structures and urban environments. In agriculture and related sectors, these systems are increasingly utilized for targeted treatment of infested crops, greenhouse structures, post-harvest storage units, and wooden farm assets. Designed for direct placement on affected surfaces, they eliminate the need for soil disturbance and enable precise control in sensitive cultivation environments. Their ease of installation and suitability for controlled agricultural systems are fostering their adoption as flexible and efficient termite management solutions.

By Active Ingredient: IGRs Lead, Chlorfenapyr Gains Momentum

Insect growth regulators (IGRs) accounted for the largest share, 54%, of the termite bait systems market in 2025. This dominance is attributed to their compatibility with integrated pest management frameworks and lower environmental persistence. By disrupting the molting process, IGRs facilitate gradual colony elimination while reducing non-target exposure to beneficial soil organisms. Their alignment with sustainable farming practices and regulatory preferences for low-toxicity solutions further supports their adoption in crop protection and agricultural infrastructure management.

Chlorfenapyr is projected to grow at the fastest CAGR of 8.7% from 2026 to 2031. This growth is driven by its unique mode of action, which disrupts mitochondrial function in termites. In agricultural applications, chlorfenapyr is increasingly used to protect stored crops, greenhouse structures, and wooden farm assets, particularly in cases where resistance to conventional treatments has been observed. As a non-repellent chemistry, it enables effective transfer within termite colonies, enhancing control outcomes. Its delayed toxicity and compatibility with integrated pest management strategies make it a valuable solution for managing termite infestations in agriculture and related industries.

By Termite Species: Subterranean Dominance, Dampwood Expansion

Subterranean termites accounted for the largest 68% share of the termite bait systems market in 2025, supported by their widespread distribution and high structural impact. These termites form extensive underground colonies and depend on soil contact, making them highly responsive to in-ground baiting systems. Their predictable foraging behavior enhances bait interception rates, thereby improving treatment efficiency. Consequently, most commercial bait system designs are tailored to subterranean termite behavior, solidifying their dominance in various applications.

Dampwood termites are projected to grow at the fastest 6.8% CAGR from 2026 to 2031, driven by expanding habitat conditions linked to rising humidity and temperature levels. These termites primarily infest moist wood, necessitating specialized bait formulations with higher moisture retention. The increasing prevalence of dampwood termites in forest-adjacent and coastal regions is fostering the adoption of tailored bait systems. As climate variability influences termite distribution patterns, the demand for species-specific solutions is rising, positioning dampwood-targeted bait systems as a growing segment within the termite control market.

By End-User: Commercial Farms Lead, Agro-Industrial Accelerates

Commercial farms accounted for the largest 46% share of the termite bait systems market in 2025, driven by the need to protect high-value crops such as cocoa, sugarcane, and citrus. Large-scale plantations utilize dense bait station networks to prevent yield losses caused by termite infestations. These systems facilitate continuous monitoring and targeted colony elimination, reducing dependence on broad-spectrum chemical treatments. Adoption is further supported by integrated pest management practices that emphasize sustainable and long-term crop protection strategies.

The agro-industrial and infrastructure segment is projected to grow at the fastest CAGR of 8.6% from 2026 to 2031, primarily due to the growing incorporation of termite protection measures into construction standards. In agriculture and related industries, farm infrastructure such as grain storage units, irrigation systems, greenhouses, and wooden support structures is increasingly utilizing pre-installation and preventive baiting systems to reduce long-term damage risks. Greater awareness of crop loss prevention, storage protection, and lifecycle cost savings is driving this adoption. As agricultural intensification and mechanization progress, the demand for durable and preventive termite control solutions is rising across farming operations.

Geography Analysis

Asia-Pacific accounted for the largest termite bait systems market share of 40% market share 2025. This growth is attributed to extensive agricultural activities and the increasing adoption of pest management solutions in crop cultivation and plantation systems. In this region, termite control is essential for safeguarding crop roots, irrigation infrastructure, wooden farm structures, and post-harvest storage facilities. Agricultural guidelines and integrated pest management practices prioritize preventive termite control, ensuring steady demand for bait systems. Enhanced awareness among farmers and agribusiness operators, coupled with the presence of established agro-service providers and monitoring technologies, improves treatment efficiency and supports widespread adoption across agriculture and related sectors.

The Africa market size is projected to grow at the fastest CAGR of 7.8% from 2026 to 2031. This growth is driven by expanding agricultural activities, increasing termite risk zones, and the need to protect crop productivity. Rising investments in farm infrastructure, storage systems, and irrigation networks are promoting the adoption of preventive termite management solutions. Government-led agricultural programs and farmer training initiatives are enhancing awareness and technical capabilities. While fragmented rural distribution networks present challenges, the growing emphasis on crop protection, reduction of post-harvest losses, and sustainable farming practices is boosting the use of termite bait systems across agriculture and allied industries.

The rapid expansion of agricultural activities and related infrastructure across various regions has increased exposure to termite infestations, driving demand for preventive control solutions such as bait systems. A 2024 study published in the Journal of Experimental Agriculture International indicated that termite infestation in wheat crops caused up to 28.32% plant damage under field conditions, emphasizing significant risks to crop productivity in tropical and semi-arid regions [3]Source: Journal of Experimental Agriculture International, “Seasonal Correlation in Prevalence of Termite on Wheat Crop,” 2024, journaljeai.com. This extent of damage highlights the susceptibility of crops, irrigation systems, and storage infrastructure. Consequently, regions in Africa, Asia, and the Middle East are increasingly implementing preventive termite management practices to protect agricultural output.

Competitive Landscape

The termite bait systems market is moderately concentrated, with key players such as BASF SE, Corteva, Inc., Rentokil Initial plc, Rollins Inc., and Sumitomo Chemical Co., Ltd. focusing on integrated solutions. These solutions combine active ingredients, bait stations, and monitoring technologies. Leading companies prioritize research and development to improve efficacy, reduce treatment time, and enhance environmental safety. Strategic collaborations and product innovations are shaping competitive positioning, while regulatory compliance remains a critical factor influencing market entry and expansion. Additionally, companies are increasingly investing in digital monitoring systems to enhance service efficiency and customer retention.

Regional players maintain competitiveness by leveraging localized expertise and offering customized services tailored to specific termite species and environmental conditions. Technology-driven entrants are introducing smart monitoring solutions that improve detection accuracy and reduce labor dependency. Distribution strategies are evolving, with direct-to-consumer and subscription-based models enhancing accessibility. The competitive landscape is shifting toward integrated pest management solutions that combine chemical, biological, and digital approaches for termite control.

According to Rentokil Initial plc, in October 2024, the company launched India’s first termite baiting service, “Anti-Termite Fortress,” along with the GoldSeal Service 4D for all commerical operations including agro infrastructure. These services provide a non-invasive and eco-friendly solution by using strategically placed bait stations to eliminate termite colonies. This initiative enhances the company’s service portfolio in regions with high termite risks and improves its ability to serve agricultural infrastructure, storage facilities, and plantation environments. The launch also supports the company’s expansion into emerging markets and facilitates the cross-selling of advanced pest control solutions.

Termite Bait Systems Industry Leaders

BASF SE

Corteva, Inc.

Rentokil Initial plc

Rollins Inc.

Sumitomo Chemical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Rentokil Initial plc launched India’s first termite baiting service, “Anti-Termite Fortress,” along with the GoldSeal Service 4D. This service is also designed to protect crop roots and manage plantations by utilizing strategically placed bait stations to eliminate termite colonies in soil environments.

- April 2024: Rentokil Initial plc acquired HiCare Services in India, expanding its termite and pest control operations across approximately 30 branches. This acquisition enhances its capacity to safeguard grain storage facilities, warehouses, and plantation assets in regions with high termite risks.

- March 2024: Ensystex, Inc. introduced the Exterra Ever-Ready Termite Colony Elimination System, which includes pre-loaded EZ in-ground bait stations that activate immediately upon installation. This system is effective for protecting crop root zones and plantation ecosystems, ensuring rapid interception of termites in soil environments.

Global Termite Bait Systems Market Report Scope

Termite bait systems are pest control solutions that utilize strategically placed stations containing slow-acting toxic baits to eradicate termite colonies. These systems function by enabling termites to consume the bait and distribute it within the colony, ultimately resulting in the colony's collapse over time. The termite bait systems market report is segmented by station type (in-ground and above-ground), by active ingredient (insect growth regulators and chlorfenapyr), by termite species (subterranean termites, drywood termites, and dampwood termites), by end-user (smallholder farms, commercial farms, and agro-industrial and infrastructure), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| In-ground |

| Above-ground |

| Insect Growth Regulators |

| Chlorfenapyr |

| Subterranean Termites |

| Drywood Termites |

| Dampwood Termites |

| Smallholder Farms |

| Commercial Farms |

| Agro-Industrial and Infrastructure |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Station Type | In-ground | |

| Above-ground | ||

| By Active Ingredient | Insect Growth Regulators | |

| Chlorfenapyr | ||

| By Termite Species | Subterranean Termites | |

| Drywood Termites | ||

| Dampwood Termites | ||

| By End-user | Smallholder Farms | |

| Commercial Farms | ||

| Agro-Industrial and Infrastructure | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Termite bait systems market in 2026?

The Termite bait systems market size stands at USD 90 million in 2026 and is on track to hit USD 122 million by 2031.

Which region is growing fastest for termite bait adoption?

Africa leads growth with the fastest 7.8% CAGR from 2026 to 2031.

What active ingredient currently dominates bait formulations?

Insect growth regulators, led by hexaflumuron and noviflumuron, hold the largest share due to reduced-risk regulatory status.

Why are above-ground stations gaining popularity?

High-rise construction and retrofits in dense urban centers demand non-invasive installation methods, driving the fastest 7.9% CAGR from 2026 to 2031 for above-ground configurations.

Page last updated on: