Integrated Risk Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.76 Billion |

| Market Size (2030) | USD 26.55 Billion |

| Growth Rate (2026 - 2031) | 8.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Integrated Risk Management Market Analysis by Mordor Intelligence

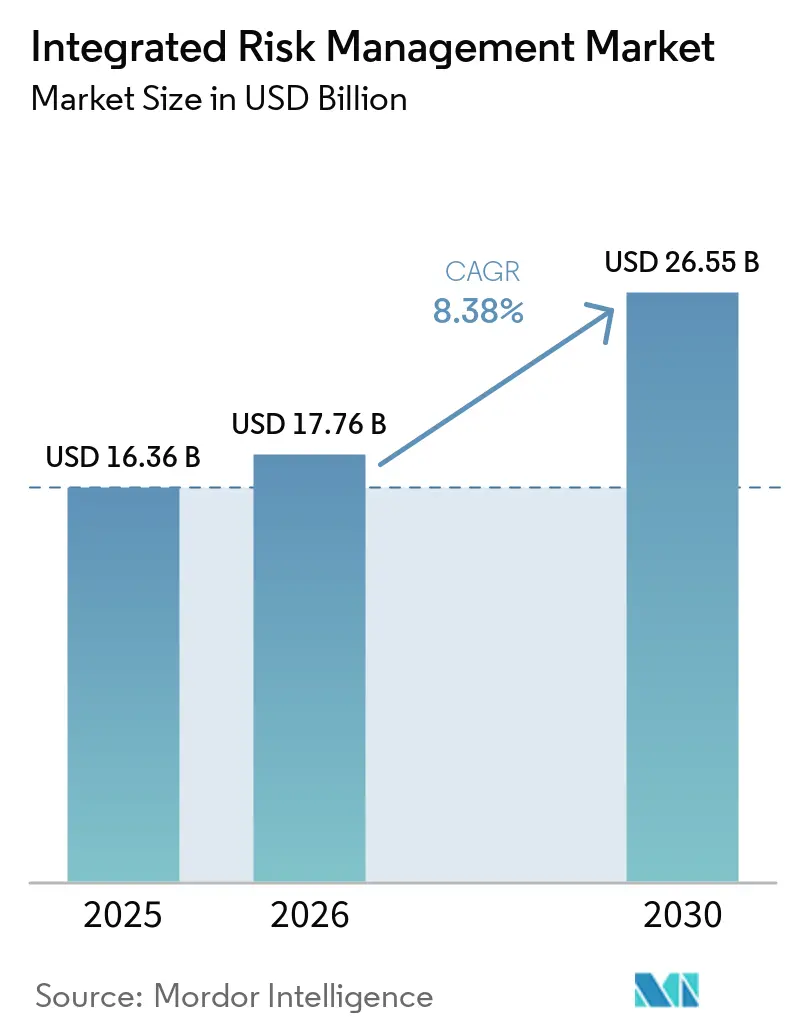

The integrated risk management market size is expected to increase from USD 16.36 billion in 2025 to USD 17.76 billion in 2026 and reach USD 26.55 billion by 2031, growing at a CAGR of 8.38% over 2026-2031. Several forces are converging to propel this expansion. Europe’s Digital Operational Resilience Act requires financial entities to embed operational-risk controls, ransomware losses averaged USD 4.54 million per breach in 2024, and the Corporate Sustainability Reporting Directive obliges 50,000 European firms to disclose climate and ESG exposures.[1]European Commission, “Corporate Sustainability Reporting Directive,” ec.europa.eu Software solutions already dominate the integrated risk management market thanks to real-time dashboards that aggregate cyber, compliance, and third-party risks, while cloud deployment compresses roll-out cycles from 18 months to six. Spending momentum is reinforced by heavy fines: the U.S. Department of Health and Human Services levied USD 5.1 billion in HIPAA penalties between 2023 and 2025. North American demand remains strong under stringent SEC cybersecurity and climate-disclosure rules, and Asia-Pacific is scaling quickly as China and India tighten personal-data statutes.

Key Report Takeaways

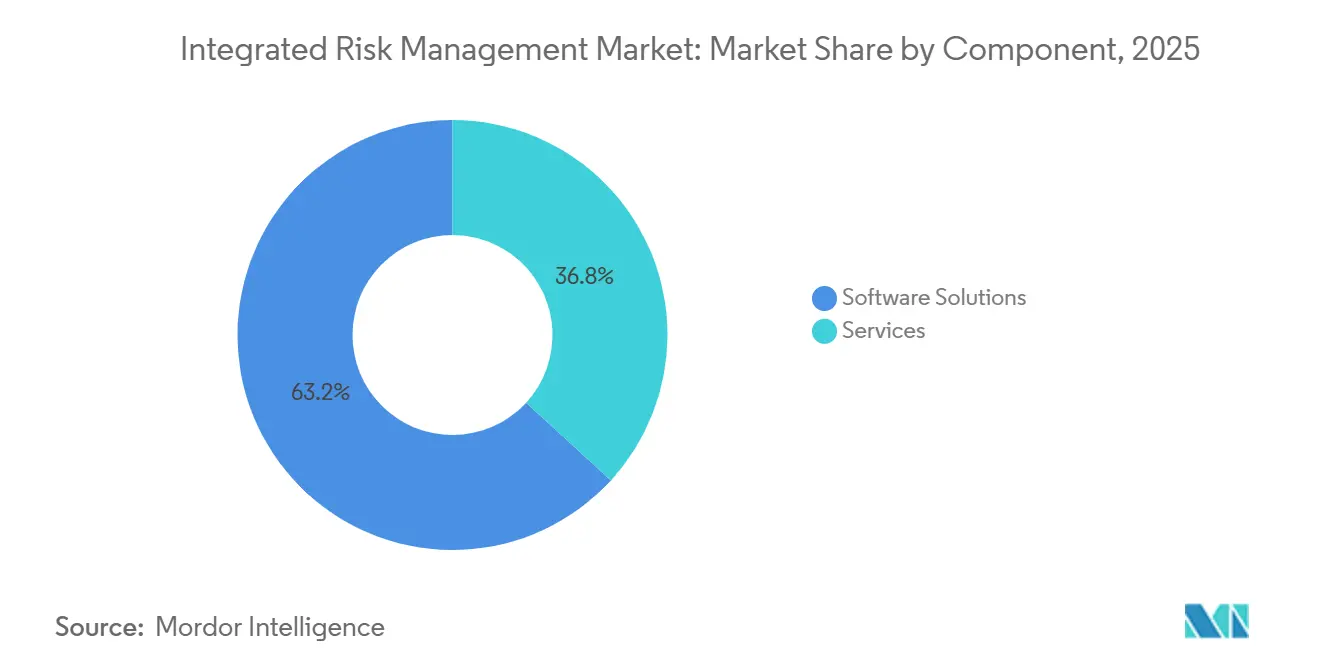

- By component, software captured 63.18% revenue share in 2025, while risk analytics and reporting modules are advancing at a 9.11% CAGR through 2031.

- By deployment mode, cloud deployments held 71.24% of spending in 2025 and are projected to grow at an 8.41% CAGR to 2031.

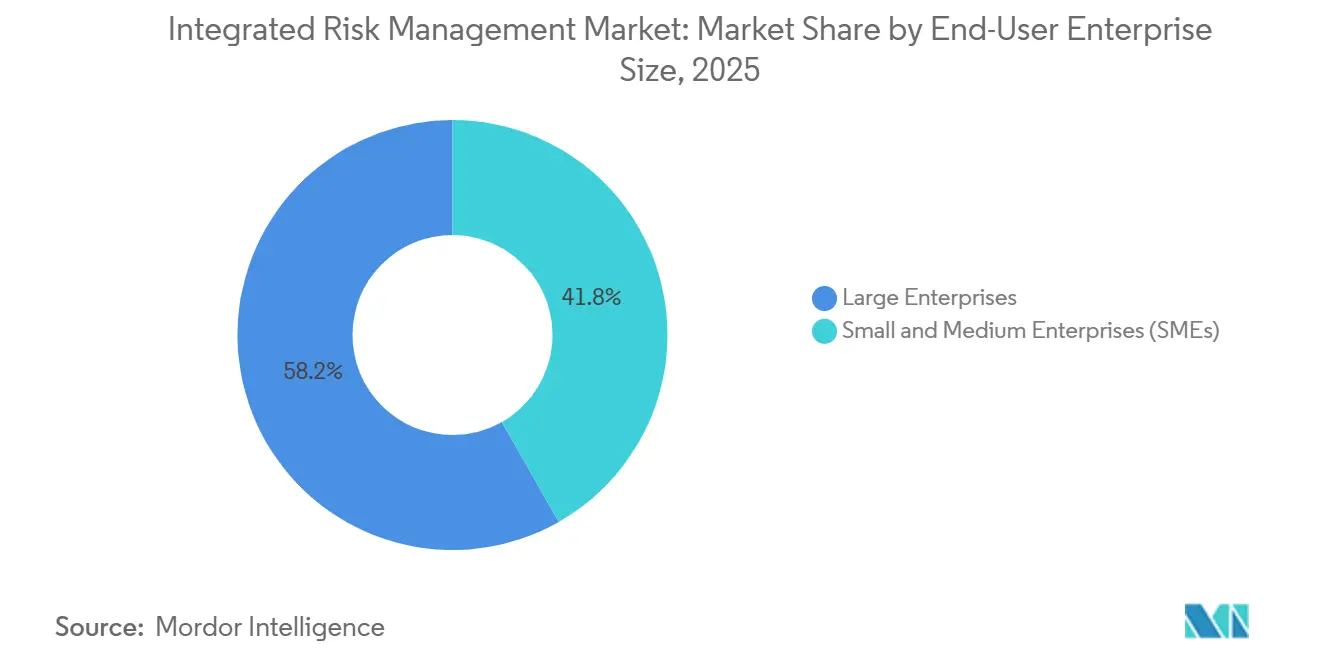

- By enterprise size, large enterprises commanded 58.23% of 2025 expenditure, whereas small and medium enterprises are accelerating at a 10.51% CAGR between 2026 and 2031.

- By end-user industry, banking, financial services, and insurance accounted for 23.91% of 2025 spending, but healthcare and life sciences represent the fastest trajectory at a 12.49% CAGR through 2031.

- By geography, North America retained 41.84% integrated risk management market share in 2025, as Asia-Pacific charts the quickest rise with an 11.42% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Integrated Risk Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complexity of Global Regulatory Frameworks | +2.1% | Europe, North America, spillover to Asia-Pacific multinationals | Medium term (2-4 years) |

| Escalating Cybersecurity Threats and Data Breaches | +1.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Rapid Digital Transformation and Cloud Adoption | +1.5% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Expansion of Third-Party and Supply-Chain Ecosystems | +1.2% | Global, concentrated in Asia-Pacific and Europe hubs | Long term (≥ 4 years) |

| Mandatory ESG and Climate-Risk Disclosure Regimes | +1.0% | Europe, North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Digital-Twin Risk Simulation for Critical Infrastructure | +0.6% | North America, Europe, pilot use in Middle East energy corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complexity of Global Regulatory Frameworks

The European Union’s Digital Operational Resilience Act entered full enforcement in January 2025 and obliges financial entities to prove the resilience of information and communication technologies within strict reporting windows.[2]European Banking Authority, “Digital Operational Resilience Act,” eba.europa.eu Parallel mandates such as the Corporate Sustainability Reporting Directive and revised GDPR consent rules compel firms to aggregate privacy, cyber, ESG, and third-party exposures in one system, elevating demand for integrated risk management market platforms. Multinational banks also face DORA clauses that ban outsourcing to vendors without resilience certifications, generating cascades of due diligence audits that spreadsheets cannot handle. Overlapping statutes now influence access to capital; prospectuses filed with the European Securities and Markets Authority must include sustainability disclosures, making operational compliance a prerequisite for fundraising. Together, these pressures transform risk management from a back-office function into a board-level imperative.

Escalating Cybersecurity Threats and Data Breaches

Ransomware assaults rose 68% in 2025, with average recovery costs of USD 4.54 million per incident, intensifying the focus on Supply Chain Risk Management as a critical enterprise priority. Sophisticated supply-chain compromises, such as the 2024 cloud-service breach that exposed credentials of 8,200 enterprises, reveal that perimeter defenses alone no longer suffice. In response, organizations embed incident workflows into integrated risk management market suites, enabling automatic breach-notification letters and real-time heat-map updates. SEC rules require public companies to report material cyber events within four business days, collapsing the window for manual remediation. Banks confront additional directives from the Federal Financial Institutions Examination Council that extend cyber-risk assessment across fourth-party subcontractors, boosting platform adoption. The convergence of IT and operational technology further enlarges the attack surface, encouraging utilities and manufacturers to unify IT alerts with OT asset inventories inside a single dashboard.

Rapid Digital Transformation and Cloud Adoption

Seventy-eight percent of enterprises ran at least half of their workloads in public or hybrid clouds by 2025, but governance practices lag behind this velocity. Shadow IT consumes 41% of cloud spend, creating blind spots in access controls and data residency that integrated risk management market platforms are well suited to illuminate through direct API connectors. FedRAMP now requires monthly security attestations from cloud providers, effectively mandating automated control-testing engines. Multicloud architectures introduce configuration drift; platforms with infrastructure-as-code scanning detect misaligned security policies before regulators do. Serverless and containerized workloads, which spin up and retire in seconds, drive the need for dynamic asset inventories that traditional spreadsheets cannot match, reinforcing the shift toward automated, cloud-native risk solutions.

Expansion of Third-Party and Supply-Chain Ecosystems

Enterprises depend on an average of 5,800 vendors, yet only one firm in eight conducts comprehensive annual assessments. The 2025 shutdown of a Taiwanese semiconductor supplier after a ransomware attack halted production for 23 automotive OEMs, highlighting how localized failures cascade globally. Proposed EU supply-chain due diligence legislation will obligate companies with more than 500 employees to map human rights and environmental risks across tiers, spurring adoption of vendor risk modules. U.S. regulators now expect banks to audit fintech partners on-site, a logistical load that automated questionnaires and remediation trackers alleviate. Continuous monitoring replaces annual reviews because a supplier’s security posture can degrade within weeks of an acquisition or leadership change.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership and Long Implementation Cycles | -1.4% | Global, acute in cost-sensitive SMEs across Asia-Pacific and South America | Medium term (2-4 years) |

| Shortage of IRM-Skilled Professionals | -0.9% | Global, critical gaps in North America and Europe | Long term (≥ 4 years) |

| Vendor Consolidation Creating Lock-In Concerns | -0.5% | Global, heightened in large enterprises across North America and Europe | Medium term (2-4 years) |

| Uncertain AI Governance Standards Across Jurisdictions | -0.4% | Global, fragmentation between major regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership and Long Implementation Cycles

Deployments average USD 3.2 million over five years, covering licenses, integration labor, and training, and on-premise rollouts can stretch to 18 months. Small manufacturers cannot field six-person project teams for such durations, even when fines loom. Although cloud delivery trims timelines to about six months, 40% of budgets still vanish into configuration and user enablement. Projects are often derailed by underestimated data-cleansing workloads, such as reconciling inconsistent vendor names across hundreds of spreadsheets. Subscription fatigue is rising as vendors replace perpetual licenses with escalating annual fees, forcing procurement teams to demand clearer ROI metrics before signing multiyear agreements.

Shortage of IRM-Skilled Professionals

The world faces 4.8 million unfilled cybersecurity roles, with integrated risk management industry skill sets, mastery of ISO 31000, COSO ERM, and NIST CSF, especially scarce.[3]International Information System Security Certification Consortium, “Cybersecurity Workforce Study 2025,” isc2.org Universities graduate fewer than 30,000 candidates annually who possess formal credentials, while demand grows 18% each year. The median U.S. salary for a certified risk analyst hit USD 128,000 in 2025, leaving mid-market firms priced out. Burnout aggravates attrition: 47% of compliance officers spend more than 20 hours a week assembling regulatory reports, work that mature platforms could automate. Vendor certification courses cost USD 5,000 per seat, adding further friction for resource-constrained organizations. While AI-assisted scoring may relieve some strain, expert judgment remains essential for interpreting probabilistic outputs and deciding acceptable risk thresholds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Consolidates Control, Analytics Accelerate

Software solutions held 63.18% integrated risk management market share in 2025, reflecting the pivot from spreadsheet registers to unified platforms that centralize policies, incidents, and compliance evidence. The integrated risk management market size captured by risk analytics and reporting modules is projected to expand at a 9.11% CAGR between 2026 and 2031, the fastest pace inside the software stack as boards insist on real-time executive dashboards. Large banks deploy automated control-testing engines to meet DORA’s quarterly assessment rules, while healthcare systems embrace incident modules that streamline HIPAA breach processes.

Services represented 36.82% of 2025 spending, split between professional and managed offerings. System integrators such as Deloitte and PwC dominate complex rollouts, whereas managed-service providers now operate 24/7 platforms under outcome-based contracts. Demand for services will persist because many enterprises lack in-house skills to fine-tune taxonomies, build APIs, and train distributed users, yet automation and preset content libraries are trimming billable hours for commoditized tasks.

By Deployment Mode: Cloud Commands Scale, On-Premise Persists for Sovereignty

Cloud deployments captured 71.24% of the integrated risk management market in 2025 and will maintain momentum with an 8.41% CAGR through 2031. Regulatory clarity helped: the European Banking Authority confirmed that properly certified SaaS platforms meet DORA expectations, unlocking investment across European finance houses. Multi-tenant architectures push quarterly feature drops, ServiceNow shipped four major enhancements in 2025 alone, without customer upgrade pain, reinforcing cloud’s appeal.

On-premise installations still account for 28.76% of spending, concentrated in defense, government, and highly regulated financial segments where data-sovereignty laws or CUI mandates prohibit public-cloud storage. Hybrid approaches that keep sensitive data on-site while off-loading analytics to the cloud are gaining ground, signaling a phased, rather than binary, migration pattern.

By Enterprise Size: SMEs Democratize Governance

Large enterprises generated 58.23% of revenue in 2025, but small and medium enterprises represent the swiftest advance at a 10.51% CAGR over 2026-2031. Lower entry-level subscriptions and no-code workflow builders now bring sophisticated governance within reach of 500-employee firms. Cyber-insurance carriers increasingly require documented policies and quarterly vulnerability scans before issuing coverage, pushing even resource-constrained businesses toward integrated risk frameworks.

Large organizations remain the spending bedrock, layering AI-driven risk scoring, digital-twin simulations, and enterprise-architecture links across 10-plus modules. Their insistence on data portability and open APIs is reshaping vendor road maps and encouraging best-of-breed challengers to plug gaps in massive suites.

By End-User Industry: BFSI Leads While Healthcare Accelerates

In 2025, banking, financial services, and insurance sectors accounted for 23.91% of total revenue, driven by Basel and DORA's operational-risk mandates, which delve deep into third-party ecosystems and emphasize the need for robust compliance frameworks. These regulations have significantly influenced the adoption of integrated risk management solutions across the sector, ensuring better oversight and risk mitigation strategies. Meanwhile, the integrated risk management market for healthcare and life sciences is projected to expand at a robust 12.49% CAGR, fueled by HIPAA penalties and FDA's cybersecurity regulations for medical devices. The increasing focus on safeguarding sensitive patient data and ensuring the security of medical devices has been a key driver for this growth.

IT and telecom companies are leading the charge, heavily adopting measures in response to stringent data-breach notification laws that demand swift and transparent reporting of incidents. These firms are investing in advanced risk management tools to address evolving cybersecurity threats and regulatory requirements. Retailers, on the other hand, are prioritizing uptime guarantees for their omnichannel operations, as uninterrupted service is critical to maintaining customer satisfaction and operational efficiency. Energy firms are merging operational technology (OT) and IT risk perspectives to comply with critical infrastructure directives, which aim to enhance the resilience and security of essential services. Concurrently, government bodies are hastening their moves under zero-trust mandates, with a culmination set for 2026. These mandates are driving the adoption of comprehensive risk management frameworks to protect sensitive data and ensure secure operations across public sector entities.

Geography Analysis

North America sustained 41.84% integrated risk management market share in 2025 due to formidable SEC climate- and cyber-disclosure rules, a mature cyber-insurance ecosystem, and high breach penalties. Canada’s stricter privacy amendments and Mexico’s fintech initiatives add regional tailwinds. The United States Federal Trade Commission collected USD 1.2 billion in settlements for lax data security in 2025, signaling regulators’ rising intolerance and prompting widespread adoption in mid-market cohorts.

Asia-Pacific posts the fastest 11.42% CAGR through 2031 as China’s Personal Information Protection Law and India’s Digital Personal Data Protection Act drive localization of risk registers and automated consent modules. Japan’s banking sector must run annual ransomware tabletop exercises, which fuels uptake of scenario-planning engines, while Australia’s soaring breach numbers make incident management a board priority. ASEAN harmonization efforts further boost cross-border compliance needs, creating fertile ground for vendors with multi-jurisdiction libraries.

Europe retained 28% share in 2025, energized by the January 2025 go-live of DORA and phased CSRD rollouts that eventually cover 50,000 entities. Germany’s BaFin issued multiple enforcement actions against banks found wanting in third-party risk, reinforcing compliance urgency. The United Kingdom’s operational-resilience framework and France’s sizeable GDPR fines underline a shift from principles-based supervision toward measurable controls. South America, the Middle East, and Africa together hold 12% share; adoption is concentrated in Brazilian finance, Gulf smart-city infrastructure, and South African privacy enforcement, though infrastructure gaps and currency volatility temper broader demand.

Competitive Landscape

The integrated risk management market is moderately concentrated. The top five suppliers—IBM, ServiceNow, SAP, MetricStream, and OneTrust—are projected to command roughly 38% of the market's 2025 revenue. Platform consolidators are capitalizing on established bases in ERP, IT services, and workflows to cross-sell modules. In contrast, pure-play challengers are carving out their niche through specialized vertical content and swift configurability. ServiceNow is harnessing low-code engines to streamline customization efforts, a strategy that particularly appeals to mid-market buyers. Meanwhile, IBM and SAP are bolstering their predictive analytics capabilities using global partner ecosystems and embedded AI, although this expansive approach can sometimes hinder the agility of their features.

Private-equity roll-ups are altering the competitive landscape, merging individual point products into comprehensive suites. This consolidation is leading to a reduction in price premiums that were once associated with standalone incident or policy tools. A notable 42% surge in patent filings for AI-driven risk scoring in 2025 underscores a competitive push to align unstructured threat feeds with organized control data. Concerns about vendor lock-in are escalating, especially as consolidators tighten API access or hike export fees. This has led many large enterprises to seek assurances of interoperability before committing to lengthy multiyear contracts. Additionally, managed-service providers are gaining prominence, offering round-the-clock monitoring services to clients facing talent shortages. This growing influence is encouraging software vendors to adopt revenue models that are more accommodating to partners.

Regional dynamics are also shaping the market's trajectory. North America continues to dominate due to its advanced technological infrastructure and early adoption of integrated risk management solutions. However, the Asia-Pacific region is witnessing rapid growth, driven by increasing regulatory requirements and the rising awareness of risk management practices among enterprises. This regional expansion is prompting vendors to tailor their offerings to meet diverse compliance standards and localized needs.

Integrated Risk Management Industry Leaders

ServiceNow, Inc.

Archer Technologies LLC.

IBM Corporation

NAVEX Global Inc.

MetricStream Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ServiceNow agreed to acquire an AI risk-analytics specialist for USD 420 million, integrating machine-learning models that map threat intelligence to control gaps.

- December 2025: SAP rolled out Integrated Risk Management Cloud within S/4HANA, embedding real-time ESG analytics for firms falling under CSRD reporting.

- November 2025: IBM added 2,400 analysts to its managed security services division through a USD 1.2 billion expansion to operate client platforms under outcome-based terms.

- October 2025: OneTrust secured USD 300 million Series D funding to develop AI-powered consent modules and expand across Asia-Pacific.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the integrated risk management (IRM) market as every software platform and the related implementation or managed-service revenues that let an organization identify, assess, aggregate, and monitor operational, cyber, compliance, strategic, and third-party risks through one shared data model. Values are expressed in constant 2025 US dollars.

Scope exclusion: Stand-alone point tools (for example, vulnerability scanners or insurance underwriting analytics) fall outside this count.

Segmentation Overview

- By Component

- Software Solutions

- Risk and Compliance Management

- Incident and Issue Management

- Policy Management

- Risk Analytics and Reporting

- Services

- Professional Services

- Managed Services

- Software Solutions

- By Deployment Mode

- Cloud

- On-Premise

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-User Industry

- BFSI

- Healthcare and Life Sciences

- IT and Telecommunications

- Retail and Consumer Goods

- Manufacturing

- Energy and Utilities

- Government and Public Sector

- Transportation

- Education

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Next, we interviewed chief risk officers, system integrators, and SaaS product leads across North America, Europe, and Asia-Pacific. Their guidance on buying cycles, seat counts, and upcoming regulations helped us close information gaps and align model drivers with on-the-ground realities before final triangulation.

Desk Research

We began by mapping the addressable universe through open sources such as U.S. SEC filings, European Banking Authority statistics, NIST Framework adoption studies, and releases from the Risk Management Society. Government procurement portals, patent families accessed via Questel, and Volza shipment data highlighted technology diffusion, while company 10-Ks and investor decks anchored typical contract values. These illustrate, but do not exhaust, the secondary inputs consulted for fact-checking and base building.

Market-Sizing & Forecasting

A top-down construct converts vertical enterprise software spend into an IRM demand pool via penetration-rate matrices. Then, selective bottom-up vendor revenue roll-ups and channel checks corroborate totals. Core levers include the number of regulated financial institutions, cloud migration ratio, median subscription price, cybersecurity incident frequency, and regional data-protection mandates. We project to 2030 using multivariate regression plus scenario analysis around regulatory shocks, while weighted averages from interview data plug residual gaps.

Data Validation & Update Cycle

Outputs face three layers of analyst review; variance flags trigger re-verification calls. Mordor Intelligence refreshes every twelve months, with interim updates when material events, such as DORA enforcement milestones, shift the outlook. A final sense-check occurs immediately before publication.

Why Mordor Intelligence's Integrated Risk Management Baseline Commands Reliability

Published estimates often diverge because firms apply different risk modules, price curves, and refresh cadences.

Key gap drivers include broader GRC inclusion by some publishers, conservative seat-price assumptions, and currency-conversion timing mismatches versus our 2025 base.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 16.36 billion | Mordor Intelligence | - |

| 17.45 billion | Global Consultancy A | Bundles eGRC and third-party risk tools; relies mainly on secondary data with limited field validation |

| 14.72 billion | Market Publisher B | Omits professional-service revenue and keeps 2019-2023 average seat prices, ignoring new cloud premiums |

The comparison shows that we couple transparent scope selection with mixed-method verification, giving decision-makers a balanced baseline that is traceable to clear variables and repeatable steps. This is where Mordor Intelligence quietly differentiates itself.

Key Questions Answered in the Report

How large will spending on integrated risk management be by 2031?

The market is forecast to reach USD 26.55 billion by 2031, reflecting an 8.38% CAGR from 2026.

Which segment is growing fastest inside integrated risk management platforms?

Risk analytics and reporting modules are set to expand at a 9.11% CAGR through 2031 as boards demand real-time dashboards.

Why are small and medium enterprises adopting integrated risk solutions quickly?

Cloud-native platforms with pre-configured templates and low subscription tiers allow SMEs to satisfy new regulatory mandates without hiring dedicated compliance teams.

What drives Asia-Pacific’s rapid uptake of integrated risk tools?

Stricter data-protection laws in China and India plus region-wide harmonization efforts under ASEAN rules are accelerating adoption in multinationals operating there.

Page last updated on: