Tactical Optics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 13.10 Billion |

| Market Size (2030) | USD 17.49 Billion |

| Growth Rate (2025 - 2030) | 5.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tactical Optics Market Analysis by Mordor Intelligence

The tactical optics market size reached USD 13.10 billion in 2025 and is forecasted to climb to USD 17.49 billion by 2030 at a 5.96% CAGR. Battlefield digitization programs, miniaturized sensor breakthroughs, and heightened geopolitical flashpoints collectively lift demand for precision‐guided fire-control and 24/7 situational-awareness solutions. Growing budgets for soldier system upgrades in the US, India, and several NATO allies reinforce long-term spending, while falling thermal-core prices derived from automotive-scale production lower entry barriers for mid-tier suppliers. Procurement teams now specify optical subsystems that plug into wider C5ISR architectures, favoring vendors that can fuse electro-optical, infrared, and on-board processing in a single line-replaceable unit. Competitive intensity rises as artificial-intelligence start-ups pitch software-defined sighting modules that promise faster target detection, compelling legacy prime contractors to accelerate R&D roadmaps.

Key Report Takeaways

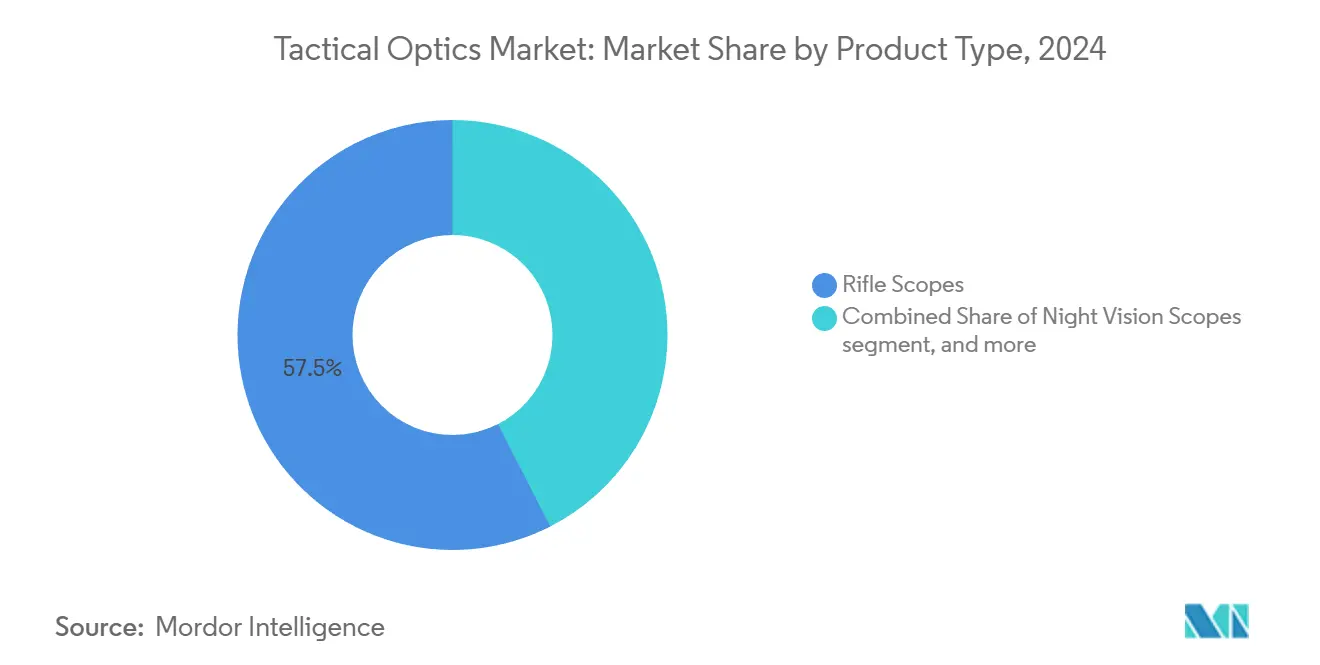

- By product type, rifle scopes held 57.51% of the tactical optics market share in 2024, while night-vision scopes are projected to advance at a 9.84% CAGR through 2030.

- By platform, ground forces accounted for 65.36% of the tactical optics market size in 2024; airborne platforms are projected to expand at an 8.70% CAGR between 2025 and 2030.

- By end user, military agencies accounted for 74.89% of the revenue in 2024; law enforcement demand is projected to rise at a 6.95% CAGR through 2030.

- By technology, electro-optical systems secured a 55.36% share in 2024; infrared/thermal optics are projected to grow at a 7.39% CAGR through 2030.

- By weapon platform, fixed installations generated 62.92% of the 2024 revenue; portable systems are expected to increase at a 6.44% CAGR during the forecast period.

- By geography, North America led with 40.31% revenue in 2024, whereas Asia-Pacific is forecasted to register the highest regional CAGR of 7.38% to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tactical Optics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in soldier-borne sensor integration | +1.20% | North America and Europe first adopters, global roll-out | Medium term (2-4 years) |

| Growing counter-sniper demand in asymmetric warfare | +0.80% | Middle East and Africa, urban centers worldwide | Short term (≤ 2 years) |

| Optics miniaturization enabling integration on UAVs | +1.10% | Asia-Pacific core, spreading trans-Atlantic | Medium term (2-4 years) |

| Rapid adoption of clip-on thermal sights by special forces | +0.90% | NATO nations and partners | Short term (≤ 2 years) |

| AI-enabled fire-control optics for next-gen infantry weapons | +1.40% | North America plus aligned allies | Long term (≥ 4 years) |

| Civilian long-range shooting sports boom | +0.50% | North America and Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Soldier-Borne Sensor Integration

Modern infantry doctrine treats every soldier as an interconnected node, prompting armies to specify optics that push real-time imagery into secure tactical clouds. Programs such as the US Defense Innovation Unit’s Advanced Soldier Borne Sensor illustrate this pivot, fielding nano-class UAVs weighing roughly 150 g for high-risk reconnaissance.[1]US Department of Defense, “DIU Product Catalog – Advanced Soldier Borne Sensor,” defense.gov Contractors supplying weapon-mounted sights, helmet displays, and handheld target designators must align hardware interfaces with Modular Open Systems Architecture (MOSA) guidelines and comply with cybersecurity frameworks such as NIST SP 800-171. Procurement contracts increasingly bundle optics with radios and edge processors, accelerating multipurpose design priorities.

Growing Counter-Sniper Demand in Asymmetric Warfare

Urban operations elevate sniper threats, spurring agencies to invest in multispectral detect-and-defeat suites. Systems like CILAS SLD-500 employ coded laser illumination paired with high-definition optics to locate hostile scopes, yet field trials reveal countermeasures—anti-reflection coatings, lens covers, and decoys—that erode single-sensor effectiveness. Vendors respond by layering acoustic arrays, radar trackers, and AI algorithms that cross-validate signatures before triggering alarms, thereby trimming false positives. Middle-Eastern deployments during 2024 peacekeeping missions highlight the urgency, with special forces citing reduced engagement times when optical and acoustic sensors operate in tandem. Budget allocations for such hybrid solutions are already embedded in several FY 2026 US and EU defense appropriations.

Optics Miniaturization Enabling Integration on UAVs

Hand-launched unmanned aircraft now carry dual-axis stabilized gimbals weighing under 400 g, blending day cameras, uncooled LWIR cores, and laser rangefinders. AeroVironment’s MANTIS payload family fits inside 2.5-inch housings while delivering HD video links over soldier radios.[2]AeroVironment Inc., “Multi-Sensor Payloads,” avinc.com Semiconductor yield improvements from automotive driver-assistance sensors drop cost per pixel, allowing militaries in India, Japan, and Australia to procure swarms of low-altitude ISR drones with sophisticated optic suites. The design emphasis shifts from optical glass to lightweight polymer lenses coated for scratch resistance, shaving tens of grams off airborne payload budgets and extending battery endurance.

Rapid Adoption of Clip-On Thermal Sights by Special Forces

Special operations teams prefer add-on thermal units that preserve the zeroed daytime scope and demand zero re-sighting time. Leonardo DRS’s Family of Weapon Sights–Sniper variant, supplied under a USD 52 million NATO framework, mounts ahead of existing glass to enable smoke-piercing engagement beyond 1 km. Safran’s ECOTI attachment clicks onto binocular night-vision goggles without helmet changes, fusing image-intensified and thermal channels to reveal hidden hot spots.[3]Safran Electronics & Defense, “ECOTI – Enhanced Clip-On Thermal Imager,” safran-group.com Procurement officials favor clip-on designs because they simplify logistics and training, accelerating fielding cycles compared with full sight replacements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-control restrictions on IR cores | -1.10% | Non-aligned nations most affected | Short term (≤ 2 years) |

| Supply-chain fragility for germanium lenses | -0.80% | Worldwide, acute in Asia and Europe | Medium term (2-4 years) |

| Weight and battery-life trade-offs in multifunction optics | -0.60% | All portable programs | Long term (≥ 4 years) |

| Data-fusion cybersecurity vulnerabilities | -0.40% | Advanced C5ISR networks globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Export-Control Restrictions on IR Cores

Thermal focal-plane arrays with sensitivity above specific NETD thresholds fall under US International Traffic in Arms Regulations Category XII. The Bureau of Industry and Security’s ECCN 0A504 further restricts exports of integrated weapon sights.[4]Bureau of Industry and Security, “Supplement No. 1 to Part 774—The Commerce Control List,” bis.gov End-user documentation, third-party licensing fees, and lengthy inter-agency reviews delay shipments by up to 15 months for non-allied buyers. Several Asia-Pacific states, therefore, negotiate government-to-government Foreign Military Sales packages to bypass commercial licensing, reinforcing the dominance of US and Israeli suppliers but curbing market diversity.

Supply-Chain Fragility for Germanium Lenses

China’s 2023 export quotas on refined germanium sparked a 75% spot-price jump, extending lead times for infrared lens blanks beyond 40 weeks. US optics manufacturer LightPath announced a joint R&D project with the Naval Research Laboratory to develop chalcogenide alternatives promising similar refractive indices without strategic material dependencies. Despite progress, coating adhesion and scratch resistance challenges remain, forcing integrators to dual-source lens assemblies and maintain larger safety stocks, which ties up working capital.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Night-Vision Scopes Outpace Traditional Glass

Night-vision scopes are projected to compound at a 9.84% CAGR through 2030, quickly narrowing the revenue gap with rifle scopes, the long-standing category leader with 57.51% market share. Militaries operating in dense urban terrain seek fused image-intensified and thermal channels to spot masked threats, and law enforcement SWAT teams mirror this preference for low-light clarity. The tactical optics market size for night-vision equipment is forecast to reach USD 7.9 billion by 2030, capturing incremental upgrades funded within broader soldier-lethality portfolios.

Digital intensifiers, exemplified by L3Harris BNVD-F goggles, combine high-figure-of-merit tubes with uncooled LWIR cores to deliver depth perception alongside heat signatures. Program requirements emphasize backward compatibility with Picatinny-mounted accessories, allowing for clip-on acquisition without requiring retraining. Meanwhile, civilian precision-rifle competitors drive volume for first-focal-plane glass, indirectly reducing the cost of military night-vision modules per unit. Export-control thresholds of 350 µA/lm photocathode sensitivity effectively bifurcate civilian and defense models, preserving clear differentiation in the tactical optics market.

By Platform: Airborne Payloads Command Faster Growth

Ground systems represented 65.36% of 2024 revenue thanks to steady vehicle and infantry procurement, yet airborne payloads will notch the highest 8.7% CAGR to 2030 on the back of proliferating Group-1 and Group-2 UAV fleets.

Persistent surveillance concepts championed by the US Special Operations Command include stabilized gimbals that send EO/IR video to handheld Android Tactical Assault Kits, forecasting a tactical optics market size uplift of USD 1.1 billion over five years. Raytheon's Raiven sensor combines hyperspectral bands, LiDAR, and AI target-recognition kernels into a compact turret qualified for Future Vertical Lift aircraft. Asian defense ministries replicate the approach, issuing tenders for micro-gimbals under 3 kg to outfit reconnaissance quadcopters. Naval programs remain a niche but resilient buyer segment, focusing on long-range search-and-track sights for littoral combat vessels; however, expansion is tempered by budget reallocations to missile defense.

By End User: Law-Enforcement Momentum Builds

Military agencies still own 74.89% of the market thanks to multi-year modernization pipelines, but police departments will deliver dynamic incremental volumes. The FBI’s USD 11 million contract for Aimpoint Duty RDS and CompM4s reflects a broader state-and-local trend toward ruggedized red-dot sights with 30,000-hour batteries.[5]Aimpoint Inc., “FBI Selects Aimpoint Duty RDS,” aimpoint.com Public-safety grants, including variants of the US Homeland Security Urban Areas Security Initiative, partially subsidize optic purchases, accelerating penetration.

Tactical optics industry suppliers tailor SKUs with simplified user interfaces, swapping ballistic-drop compensators for manual turrets compatible with standard patrol rifle calibers. Export restrictions continue to fence off advanced image-intensified tubes, but law-enforcement interest in uncooled thermal imagers remains strong, especially for perimeter surveillance and manhunt operations. As doctrine converges with military concepts of networked response, vendors forecast law-enforcement revenue share to crest 20% by 2030.

By Technology: Thermal Imaging Races Ahead

Electro-optical glass and laser systems held 55.36% of 2024 turnover, yet thermal optics will widen their footprint, driven by shutterless microbolometer breakthroughs that slash SWaP-C metrics. The tactical optics market share for infrared solutions is set to hit 46% by 2030 as frame rates climb past 100 Hz and pixel pitch shrinks below 10 µm.

Automotive safety mandates for pedestrian automatic-emergency-braking sensors have translated into mass-production lines that deliver economies of scale to defense purchasers. Embedded sigma-delta ADCs and on-chip non-uniformity correction eliminate mechanical shutters, boosting reliability in sandstorm environments. Operators value the all-weather performance, noting higher mission readiness during 2024 Indo-Pacific typhoon disaster-relief operations. Complementary metal-oxide-semiconductor (CMOS) developments will keep electro-optical systems relevant for daylight precision fire, yet combined EO/IR packages will become the program office default.

By Weapon Platform: Portable Optics Gain Traction

Fixed emplacements—main battle tanks (MBTs), infantry fighting vehicles (IFVs), and remote-weapon stations (RWS)—secured 62.92% of revenue in 2024, but soldier-carried optics will grow at 6.44% CAGR to 2030 as military doctrine stresses dispersed, agile formations. The tactical optics market size for portable systems will breach USD 6 billion by the decade’s close.

Safran’s JIM COMPACT binocular weighs under 2 kg and includes dual batteries, yet it spots vehicles at 10 km. Battery endurance remains the chief design bottleneck; thus, man-portable sights now integrate USB-C power-in ports for shared-battery ecosystems covering handheld radios and tablets. Weight caps push suppliers toward carbon-composite chassis and hollow-core adjustment turrets without sacrificing shock resistance.

Geography Analysis

North America controlled 40.31% of the revenue in 2024, buoyed by the US FY 2025 defense appropriation that earmarks USD 3.2 billion for soldier lethality enhancements, including advanced optics packages. Ongoing trials of augmented-reality weapon sights and fused NVG-thermal goggles underscore the region’s appetite for next-generation solutions. Canada’s Strong, Secure, Engaged defense policy refresh likewise dedicates funds to modular optical upgrades for its C20 designated marksman rifle program.

Asia-Pacific is rising fastest at a 7.38% CAGR, propelled by territorial disputes and indigenous industrialization. India’s FY 2025-26 defense budget tops USD 75 billion and funnels Innovation for Defence Excellence (iDEX) grants toward local clip-on thermal sight prototypes. Meanwhile, Japan’s Mid-Term Defense Program prioritizes compact EO/IR sensors for Type 16 maneuver combat vehicles. Australia’s Land 159 tranche 2 aims to equip every soldier with variable-power optics, tightening regional competition for supply contracts. The tactical optics market size in the region is on track to eclipse USD 4 billion by 2030.

Europe posts steady mid-single-digit expansion as NATO allies fill capability gaps exposed by heightened eastern-flank tensions. France’s Leclerc XLR upgrade swaps analog video for digital optronic cores, and Germany’s Infanterist der Zukunft – Erweitertes System (IdZ-ES) program orders hybrid electro-optical sights for Sturmgewehr G95 rifles. Export-control challenges complicate direct sales to some Eastern European states, but Foreign Military Financing grants mitigate procurement friction.

Competitive Landscape

The tactical optics market features moderate fragmentation: a half-dozen incumbents exceed USD 500 million annual optical revenue, while dozens of niche players carve out specialty domains. Trijicon and EOTech leverage extensive US defense relationships, routinely winning sole-source contracts for small-arms sights. Elbit Systems extends its reach through OEM partnerships, embedding miniature laser rangefinders into infantry day scopes delivered under FMS channels to Southeast Asia.

M&A activity concentrates on vertical integration and material security. LightPath’s acquisition of ISP Optics adds internal infrared lens-blank capacity, buffering against germanium supply shocks. Israeli firm HENSOLDT broadens multi-spectral offerings by purchasing German start-up MAKIND’s AI sensor-fusion algorithms to consolidate night-vision and fire-control product lines. Meanwhile, software-centric entrants such as Edge Autonomy target layered-intelligence architectures, offering plug-and-play AI modules compatible with legacy glass via bolt-on computing pods.

Cyber-readiness emerges as a new competitive differentiator. Following the US Department of Justice suit against Georgia Tech, the prime audit subcontractor compliance weeded out suppliers lacking FedRAMP-aligned secure-development pipelines. Companies advertising supply-chain provenance documentation and Secure Development Lifecycle processes gain bid-evaluation points, tilting award probabilities in favor of larger, process-mature vendors.

Tactical Optics Industry Leaders

Trijicon, Inc.

Elbit Systems Ltd.

Nightforce Optics, Inc.

Leupold & Stevens, Inc.

EOTECH, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Kopin received US Army funding to mature MicroLED display prototypes for augmented-reality weapon sights.

- July 2024: Teledyne FLIR secured a USD 15 million NATO contract for ThermoSight HISS-XLR clip-on MWIR sights featuring 640×480 detectors.

- February 2024: Aimpoint won a USD 11 million FBI order for Duty RDS and CompM4s red-dot optics.

- February 2024: French DGA awarded Nexter and Safran a Leclerc XLR tank-sight modernization package that installs PASEO panoramic viewers.

Global Tactical Optics Market Report Scope

| Rifle Scopes |

| Night Vision Scopes |

| Handheld Sighting Devices |

| Cameras and Displays |

| Ground Forces |

| Airborne |

| Naval |

| Military |

| Law Enforcement |

| Civilian/Hunting and Sports Shooting |

| Electro-Optical |

| Infrared/Thermal |

| Image-Intensified |

| Fixed |

| Portable |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Israel |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| Product Type | Rifle Scopes | ||

| Night Vision Scopes | |||

| Handheld Sighting Devices | |||

| Cameras and Displays | |||

| Platform | Ground Forces | ||

| Airborne | |||

| Naval | |||

| End User | Military | ||

| Law Enforcement | |||

| Civilian/Hunting and Sports Shooting | |||

| Technology | Electro-Optical | ||

| Infrared/Thermal | |||

| Image-Intensified | |||

| Weapon Platform | Fixed | ||

| Portable | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Israel | |

| Saudi Arabia | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the tactical optics market in 2025?

The tactical optics market size stands at USD 13.1 billion in 2025.

What is the forecast CAGR for tactical optics through 2030?

Aggregate revenue is projected to rise at a 5.96% CAGR between 2025 and 2030.

Which product segment is growing fastest?

Night-vision scopes are advancing at a 9.84% CAGR on the back of 24/7 operational demands.

Which region will see the highest growth?

Asia-Pacific is expected to post a 7.38% CAGR as modernization budgets climb across India, Japan, and Australia.

Why are thermal optics gaining market share?

Uncooled microbolometer advances cut size, weight, power, and cost, enabling all-weather imaging and accelerating adoption.

How are export-control rules affecting suppliers?

ITAR and EAR licensing prolong delivery cycles for advanced IR cores, steering non-aligned buyers toward government-to-government procurement channels.

Page last updated on: