Military Antenna Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

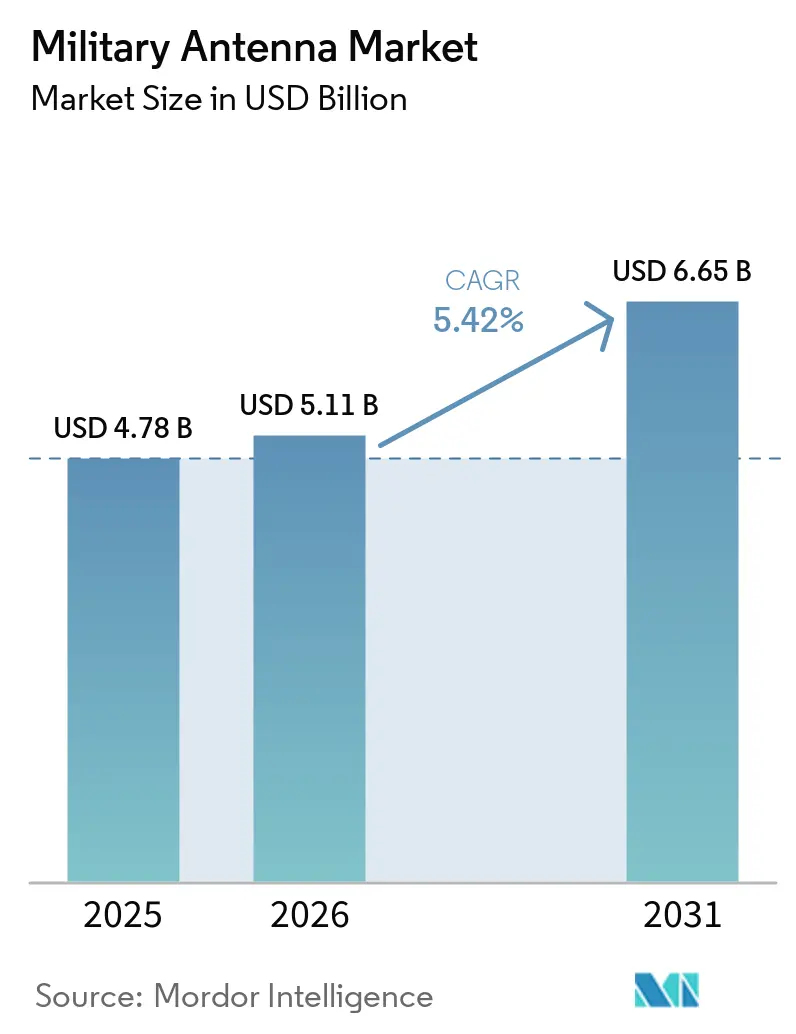

| Market Size (2026) | USD 5.11 Billion |

| Market Size (2031) | USD 6.65 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

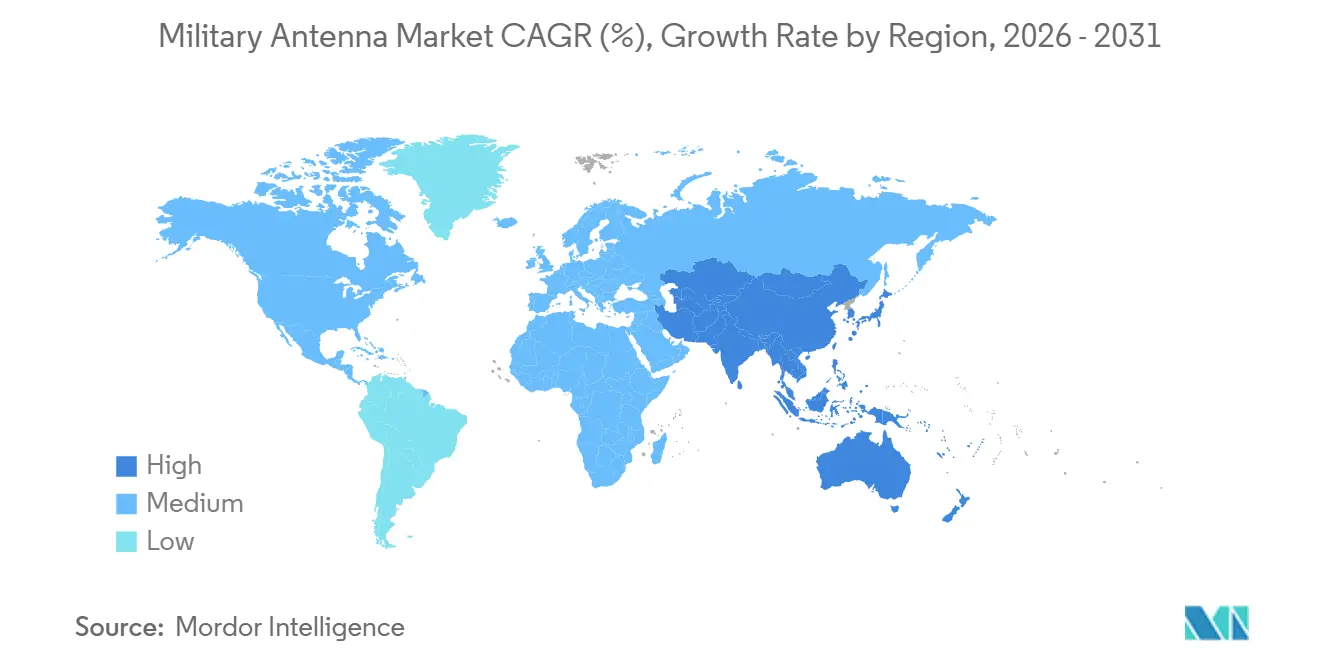

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Military Antenna Market Analysis by Mordor Intelligence

The military antenna market size is projected to expand from USD 4.78 billion in 2025 and USD 5.11 billion in 2026 to USD 6.65 billion by 2031, registering a CAGR of 5.41% between 2026 and 2031. Advanced communication-on-the-move programs continue to be a significant demand driver as armed forces transition from static communication nodes to continuously connected mobile platforms. The military antenna market benefits from modernization in the command-and-control (C2) systems. The US Government Accountability Office (GAO) noted that the Department of Defense (DoD) requested over USD 1.4 billion for Combined Joint All-Domain Command and Control (CJADC2) activities in the FY2025 budget. Although GAO does not directly link CJADC2 funding to antenna upgrades, the program's focus on connecting assets across domains sustains demand for resilient communication systems and connectivity enhancements. The military antenna market is gaining another layer of support from rising demand for multi-orbit SATCOM, submarine communications, unmanned systems, and space payloads, all of which require smaller, lighter, and more software-driven apertures than earlier generations. Even so, the military antenna market still faces timing friction from export controls and the concentration of trusted-source components, which can slow allied integration schedules and limit production scalability for some suppliers.

Key Report Takeaways

- By platform, ground platforms held 37.55% of the military antenna market size in 2025, while space platforms are projected to record the fastest growth at an 8.90% CAGR through 2031.

- By frequency band, UHF accounted for 34.10% in 2025, while SHF is forecast to expand at a 9.01% CAGR through 2031.

- By technology, array antennas led with 35.68% in 2025, while microstrip antennas are projected to grow at an 8.77% CAGR through 2031.

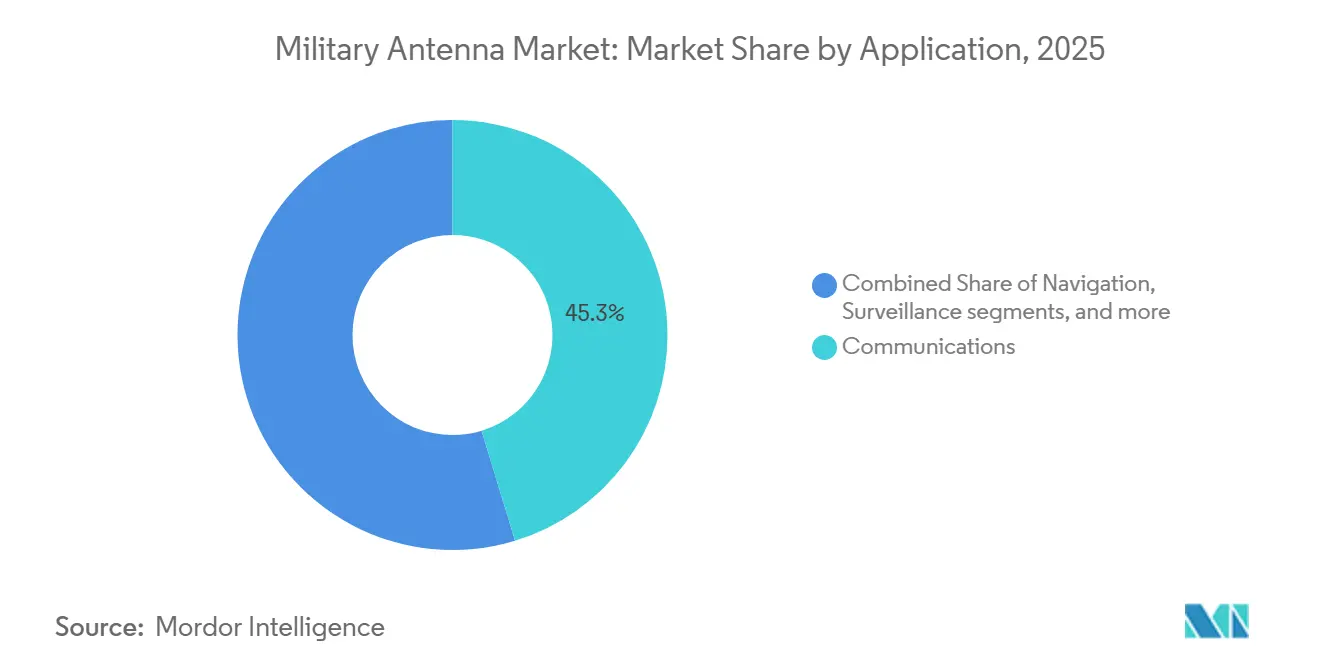

- By application, communications accounted for 45.30% of the military antenna market in 2025, while telemetry is projected to grow at a 7.99% CAGR through 2031.

- By component, radiating elements captured 40.25% in 2025, while radomes are forecast to grow at a 7.15% CAGR through 2031.

- By geography, North America held 47.35% of the military antenna market share in 2025, while Asia-Pacific is projected to register the highest CAGR of 6.90% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Military Antenna Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Phased-array and electronically steered antenna upgrades | +1.20% | Global, with near-term gains in North America and Europe | Short term (≤ 2 years) |

| Tactical SATCOM expansion across LEO, MEO, and GEO networks | +1.00% | Global, with highest intensity in North America and Asia-Pacific | Medium term (2-4 years) |

| C4ISR and multi-domain secure communications modernization | +0.90% | NATO members and Indo-Pacific partners | Medium term (2-4 years) |

| Unmanned and attritable platform proliferation | +0.70% | Global, with concentration in Asia-Pacific and North America | Short term (≤ 2 years) to Medium term (2-4 years) |

| Shared-aperture multifunction antenna adoption | +0.50% | North America and Europe, with spillover to Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Protected multi-orbit connectivity for polar and contested theater | +0.40% | North America, Northern Europe, and Arctic littoral states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Phased-Array and Electronically Steered Antenna Upgrades

The market is gradually shifting toward phased-array and electronically steered systems due to user demand for increased mobility, faster beam control, and reduced reliance on moving parts in exposed platforms.[1]Office of Naval Research, "Active Aperture Array," onr.navy.mil The US Army conducted the second-phase Armored Formation Network On-The-Move (AFN-OTM) pilot in early 2025 with the 1st Infantry Division during National Training Center rotations at Fort Irwin, California. AFN-OTM vehicles featured LEO SATCOM, kick-out SATCOM terminals, LOS radios, cellular transport, bandwidth-diversity tools, and Variable Height Antenna drones to support C2 operations. The market is seeing the same shift toward higher-end unmanned missions, as AeroVironment received a USD 43 million contract in May 2026 to integrate its PANTHER phased-array antenna onto SkyRange platforms for hypersonic telemetry.[2]Source: AeroVironment, “AV Awarded $43M DoW Contract to Integrate PANTHER Phased Array Antenna on SkyRange Platforms for Hypersonic Telemetry,” avinc.com Research published in 2026 demonstrated that a wing-conformal phased-array antenna prototype for UAV applications achieved ±65° azimuth scanning, a 24.8% relative bandwidth, and less than 3 dB of gain fluctuation at key frequencies. These findings confirm the technical feasibility of conformal phased arrays for UAV radar applications. In May 2025, China’s CETC showcased a radar portfolio at the 11th World Radar Expo, including S-band digital-array surveillance radar, S-band active phased-array systems, UHF-band fully digital phased-array anti-stealth radar, and C-band all-digital active phased-array weather radar, highlighting the expanding use of electronically agile aperture technologies across radar roles and frequency bands.

Tactical SATCOM Expansion Across LEO, MEO, and GEO Networks

The military antenna is being influenced by the expansion of tactical SATCOM across low, medium, and geostationary orbits, as operators increasingly require mobile terminals capable of transferring traffic across multiple networks rather than being restricted to a single orbit. Japan's FY2026 defense budget included JPY 88.2 billion (USD 563.01 million) for a next-generation defense communications satellite and JPY 8.7 billion (USD 55.50 million) for the PATS multi-band satellite communications system, which supports continued demand for advanced antenna payloads and multi-band ground terminals. The US Navy's PMW/A 170 documentation for 2025 emphasized SATCOM resiliency, multi-orbit connectivity, and band/vendor diversity. STNG and CBSP initiatives enhance access across GEO and NGSO constellations for naval platforms, driving demand for multi-band terminals, certified apertures, and multi-beam array technologies. However, Navy sources do not explicitly state that antenna procurement is the primary requirement for fleet upgrades. In February 2026, L3Harris secured a full-rate production contract from General Dynamics Electric Boat to deliver 26 submarine communications shipsets for Virginia- and Columbia-class submarines by 2033. While antenna procurement was not explicitly mentioned, the contract highlights demand for reliable naval communication systems. In March 2026, Kymeta introduced the KuKa 8-Series, enabling simultaneous Ku- and Ka-band operation within a compact, electronically steered flat-panel antenna, reflecting the military antenna market's shift toward smaller, multi-band, and easily integrable SATCOM terminals.

C4ISR and Multi-Domain Secure Communications Modernization

The market continues to receive significant support from C4ISR modernization, as nearly all C2 upgrades necessitate a corresponding update to the communication infrastructure. The US Government Accountability Office reported in April 2025 that the DoD requested more than USD 1.4 billion for CJADC2 activities in the FY2025 budget, underscoring the scale of the secure networking push driving antenna demand. Japan added to this trend through its FY2026 budget, which allocated JPY 364 billion (USD 2.33 billion) to command, control, and intelligence functions and maintained funding for defense communications satellites and multi-band SATCOM systems. In December 2025, NATO approved its 2026 common-funded budgets, allocating EUR 528.2 million (USD 610.00 million) for the civil budget and EUR 2.42 billion (USD 2.84 billion) for the military budget. These allocations aim to strengthen collective defense, enhance interoperable communications, and support shared military infrastructure. This alignment with the military antenna market highlights the growing importance of factors beyond waveform or gain performance. Suppliers now face competition based on through-life support, certification readiness, and secure integration into broader command architectures, which are increasingly critical in the military antenna market.

Unmanned and Attritable Platform Proliferation

The demand is also increasing due to unmanned and attritable platforms, which require lighter, more conformal apertures than traditional crewed systems. Japan's FY2026 defense budget has allocated approximately JPY 277.3 billion (USD 1.77 billion) for unmanned defense capabilities. This includes JPY 100.1 billion (USD 639 million) designated for the development of Synchronized, Hybrid, Integrated, and Enhanced Littoral Defense (SHIELD) using unmanned assets. The SHIELD funding encompasses various unmanned platform categories, including UAVs, USVs, and UUVs, aligning with Japan's objective to establish a layered unmanned defense system across the air, maritime surface, and underwater domains. In May 2026, AeroVironment won a USD 43 million contract to integrate its all-digital PANTHER phased-array antenna onto SkyRange high-altitude platforms, demonstrating that advanced array antennas are moving deeper into unmanned and specialized test roles. The military antenna market is seeing similar progress in research-backed conformal designs, with Scientific Reports publishing 2026 work that demonstrated wide-angle scanning performance suitable for UAV-borne surveillance radar. As attritable platforms scale further, the market is likely to shift more value toward compact beamforming, low-profile installation, and resilient operation in crowded spectrum conditions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ITAR and sovereign procurement export bottlenecks | -0.40% | Global, with highest friction in Indo-Pacific and Middle East allied procurement | Medium term (2-4 years) |

| Electromagnetic congestion and platform-level EMC complexity | -0.30% | Global, acute in dense platform environments such as carriers and land vehicles | Short term (≤ 2 years) to Medium term (2-4 years) |

| GaN and advanced RF component supply concentration | -0.30% | Global, with supply risk concentrated in US and European prime ecosystems | Medium term (2-4 years) |

| Long defense budget cycles delaying next-wave upgrades | -0.30% | Europe and Middle East, with lower intensity in the United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ITAR and Sovereign Procurement Export Bottlenecks

The military antenna market still faces persistent delays due to export-control rules, especially when high-performance apertures are tied to sensitive platform electronics and military communications functions. The US Department of State issued an interim final rule in January 2025, followed by a final rule in August 2025, which became effective in September 2025.[3]Source: U.S. Department of State, “International Traffic in Arms Regulations, U.S. Munitions List Targeted Revisions,” govinfo.gov This rule removed certain Controlled Reception Pattern Antennas for Position, Navigation, and Timing (PNT) from the US Munitions List and placed them under the Export Administration Regulations (EAR). This regulatory change reduces ITAR-related export challenges for PNT-focused anti-jam antennas. However, exporters must still evaluate EAR classification and licensing requirements. That step improved conditions for some GNSS-related products, but it did not remove broader licensing pressure on higher-performance military antenna systems, especially active phased arrays above sensitive thresholds. The military antenna market, therefore, continues to face long approval cycles on foreign programs because buyers must account for licensing, technology release conditions, and downstream integration effects on the rest of the platform, also encouraging allied governments and local defense firms to invest in sovereign alternatives, thereby redirecting future business away from export-dependent suppliers in the military antenna market.

GaN and Advanced RF Component Supply Concentration

The market faces constraints due to the concentration of trusted GaN and advanced RF supply, as phased-array output relies significantly on a limited number of qualified foundries. Qorvo has been the leading GaN-on-SiC supplier for defense since 1998, holding US DoD DMEA Category 1A Trusted Source accreditation for its Richardson, Texas, foundry and shipping over 10 million GaN products. supporting performance, reliability, and trusted supply needs for defense radar, electronic warfare, SATCOM, and other RF front-end applications. However, potential capacity risks are a concern across the industry. Rising demand across defense programs may pressure GaN-on-SiC wafers, foundry capacity, packaging, and trusted-source supply chains, rather than indicating a Qorvo-specific issue in the military antenna market. The DoD’s DMEA SBIR/STTR Topic DMEA254-P001, pre-released in September 2025, focused on RF front-end design using GlobalFoundries’ 200-mm GaN-on-Silicon 130RFG1 process to demonstrate integrated LNA and PA solutions for military and commercial radio systems, aligning with efforts to enhance US -based GaN RF manufacturing. Its impact on antenna costs, procurement timelines, and smaller integrators should be considered a market risk rather than a definitive conclusion by the DoD.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Space Architecture Accelerating Above a Ground-Dominant Base

Ground platforms accounted for 37.55% of the military antenna market size in 2025, remaining the largest platform segment by value. This reflects the installed base of armored vehicles, tactical wheeled platforms, and man-portable systems being upgraded for mobile communications. The US Army reinforced tactical communications demand in January 2025 when it awarded L3Harris nearly USD 300 million in full-rate production orders for Manpack and Leader radios under the handheld, manpack, and small form fit program, supporting continued demand for secure, interoperable, and field-ready communications systems where antenna compatibility, waveform performance, and SATCOM/LOS connectivity remain critical to operational effectiveness. The military antenna industry, therefore, continues to depend heavily on large ground fleet modernization cycles, where unit volumes remain much higher than in many naval and space programs.

The market is experiencing rapid growth in the space platform segment, which is projected to expand at a CAGR of 8.90% through 2031, driven by increasing investments in satellite payloads and relay architectures. For instance, Japan's FY2026 budget allocates JPY 88.2 billion (USD 563 million) for a next-generation defense communications satellite and JPY 8.7 billion (USD 55.50 million) for the PATS multi-band SATCOM system. The market is expected to witness higher demand at the payload level as proliferated constellations, relay networks, and on-orbit processing increase the deployment of military apertures beyond traditional GEO architectures. Additionally, airborne platforms represent the second-largest segment, supported by upgrades to fighter radars, refresh cycles for ISR aircraft, and the need for survivable communications in tactical aviation fleets. Naval demand remains robust as submarines and surface combatants require multi-band and multi-orbit connectivity, particularly in environments where terrestrial communication alternatives are limited.

By Frequency Band: SHF Growth Reflects SATCOM Pivot, UHF Sustains Tactical Backbone

Ultra High Frequency (UHF) accounted for 34.10% in 2025, maintaining its position as the largest frequency band segment in the military antenna market. Its position remains durable because tactical communications, narrowband SATCOM, shipboard links, and many dispersed field operations still rely on UHF as a dependable backbone. The US Navy’s PMW/A 170 documentation emphasizes that multi-orbit SATCOM resiliency is a key fleet communications priority. CBSP and STtNG enhance access across GEO and NGSO constellations for band and vendor diversity, as well as multi-band failover. UHF remains integral to the Navy’s communications through DMR, MUOS, BFTN, and legacy systems, sustaining demand for advanced multi-orbit terminals and UHF-compatible antenna systems. HF and VHF also remain relevant where long-range or over-the-horizon links still offer operational value, especially in austere settings and across mixed platform fleets.

Super High Frequency (SHF) is the fastest-growing band and is projected to expand at a 9.01% CAGR through 2031, reflecting the move toward Ka- and Ku-band SATCOM capacity. The military antenna market is seeing this change through demand for smaller mobile terminals, faster beam switching, and more compact multi-band feed assemblies. Japan’s FY2026 communications satellite and PATS allocations prioritize protected, anti-jam satellite links, supported by funding for next-generation defense communications satellites and PATS-compatible equipment. In March 2026, Kymeta launched the KuKa 8-Series, which features simultaneous Ku- and Ka-band operation within a single electronically steered flat-panel aperture. This development underscores the increasing demand for compact, multi-band, multi-orbit SHF/Ku-Ka SATCOM terminals. While the EHF segment is smaller, it continues to play a critical role in providing survivable, protected, and jam-resistant communications for strategic, naval, air, and ground missions.

By Technology: Array Antennas (AESA) Dominate, Microstrip Gains in Compact Platforms

Array antennas accounted for 35.68% of the market in 2025, making them the largest technology segment in the military antenna market. This leadership is grounded in beam agility, multi-mission flexibility, and the growing need to support radar, SATCOM, EW, and data links through more software-driven apertures. China's 2025, China's CETC highlighted the relevance of electronically scanned radar apertures by showcasing digital-array, active phased-array, and fully digital phased-array systems. These systems spanned S-band, C-band, and UHF radar applications, including low-altitude surveillance, 3D air surveillance, and anti-steal CETC section. CETC's portfolio also includes L-band AESA systems, emphasizing the shift toward electronically agile apertures. Aperture and reflector antennas still hold an important place where very high gain and proven cost structures matter more than fast electronic steering.

Microstrip antennas are projected to grow at an 8.77% CAGR through 2031, which makes them the fastest-growing technology segment in the military antenna market. Their lightweight, conformal form factor suits UAVs, small satellites, and compact vehicle installations where size, weight, and power constraints are strict. Research published in July 2025 on a 32 GHz Ka-band microstrip patch antenna with a Frequency Selective Surface (FSS) for military drones demonstrated a simulated return-loss of -29.3 dB, improved gain and directivity, and a compact design, supporting Ka-band antenna use in UAVs and space-constrained defense platforms. The military antenna industry is therefore seeing a gradual substitution away from larger exposed forms in select unmanned and space applications. Wire and lens antennas remain relevant in narrower use cases, but the growth curve is clearly strongest where low-profile integration offers an operational advantage.

By Application: Communications Commands the Market, C2 Data Link Emerging Fastest

Communications are projected to account for 45.30% of the military antenna market in 2025, underscoring the need to support voice, data, and video links across nearly all military platforms in operation. In November 2024, L3Harris secured a US Navy IDIQ contract worth up to USD 999 million to supply MIDS JTRS terminals over five years for US and coalition forces. This contract enhances Link 16 interoperability across the US armed services and 57 allied nations, highlighting the demand for connectivity hardware, RF integration, and antenna systems for secure tactical data exchange in contested environments. Navigation also retains a meaningful role because anti-jam and anti-spoofing requirements continue to support the demand for protected antennas on aircraft and other mobile systems.

Telemetry is expected to be the fastest-growing application segment, with a projected CAGR of 7.99% through 2031. This growth is driven by the expansion of hypersonic weapon testing, increased activity in attritable UAV range operations, and rising demand for space launch monitoring. The need for dedicated telemetry link antennas for each test flight of attritable unmanned systems significantly increases antenna volumes at the program level compared to reusable platforms. This trend is becoming more evident as the US Air Force Research Laboratory expands its portfolio of attritable aircraft. Additionally, surveillance and reconnaissance antennas, including those used in SAR-equipped UAVs and SIGINT aircraft, as well as command and control data link applications, are benefiting from increased budgets for counter-drone initiatives and spectrum dominance programs.

By Component: Radiating Elements Lead, Radomes Signal Survivability Investment

Radiating elements accounted for 40.25% in 2025, making them the largest component category in the military antenna market. That position reflects their direct roles in signal transmission and reception, and the high value placed on active elements in AESA systems. Feed networks and coax assemblies continue to absorb meaningful spending because many upgrades replace or improve selected components rather than whole antenna chains. Switches and phase shifters also benefit as beamforming architectures spread more widely across radar, SATCOM, and electronic warfare programs.

Radomes are expected to grow at a CAGR of 7.15% through 2031, positioning them as the fastest-growing component segment in the military antenna market. This pattern shows that survivability, environmental protection, and signature control are becoming more important in procurement decisions rather than remaining secondary design considerations. The military antenna market is seeing more attention on ruggedized assemblies as higher power density and more complex waveforms make exposed apertures more vulnerable in demanding operating conditions. That direction aligns with the broader move toward integrated, hardened subsystems rather than simple, exposed antenna hardware. It also suggests that future component spending will increasingly reward suppliers that can combine protection, durability, and electromagnetic performance in one package.

Geography Analysis

North America held 47.35% of the military antenna market share in 2025, maintaining its position as the largest regional contributor. The US remains the anchor of regional demand because mobile communications, submarine connectivity, and tactical network modernization are all moving through active procurement pipelines. In January 2025, the US Army advanced the military antenna market through its Fort Bliss network-on-the-move pilot, which validated electronically steered vehicle-mounted antennas in armored formations. North America also gained from L3Harris' February 2026 full-rate production contract for Virginia-class and Columbia-class submarine communication systems covering 26 shipsets through 2033.

Europe remained the second-largest regional block in the military antenna market, supported by NATO-led interoperability needs and wider communications modernization across allied militaries. NATO's December 2025 approval of its 2026 common-funded budgets reinforced the need for stronger collective defense, shared military infrastructure, and interoperable communications networks. The regional supplier base remains active, as evidenced by Rohde & Schwarz's launch in April 2025 of compact, lightweight, and rapidly deployable military spectrum-monitoring systems. These systems aim to assist armed forces in spectrum management, emitter detection and geolocation, EMCON monitoring, and ensuring reliable radio communications in contested electromagnetic operating environments. Europe's position in the military antenna market is therefore supported by both procurement demand and a local industrial base focused on secure communications and spectrum operations.

Asia-Pacific is the fastest-growing region in the military antenna market and is projected to expand at a 6.90% CAGR through 2031. Regional growth is being shaped by budget expansion, domestic production goals, and the need to strengthen maritime and air surveillance networks. Japan's FY2026 budget added visible support through funding for command, control, and intelligence functions, unmanned systems, next-generation defense communications satellites, and the PATS multi-band SATCOM program. China's CETC also showed in May 2025 that active phased-array production across multiple bands is already well established in the region's defense industrial base. Middle East and Africa, along with South America, account for the remaining share of the military antenna market, and activity in these regions remains tied to selective platform upgrades and subsystem outsourcing, including MTI Wireless Edge's January 2025 military antenna development and manufacturing contracts from an Israeli system house.

Competitive Landscape

The military antenna market is moderately consolidated, with L3Harris Technologies, RTX Corporation, Lockheed Martin, BAE Systems plc, and Rohde & Schwarz GmbH & Co. KG holding strong positions in Western defense programs. Even so, the military antenna market is not closed to smaller specialists, because platform-specific outsourcing remains active across communications, SATCOM, and antenna subsystem manufacturing. MTI Wireless Edge said in January 2025 that Israeli system houses were increasing outsourcing of military antenna manufacturing, which supports the view that mid-tier suppliers still have room to win focused work even when large primes dominate end programs, leaving the military antenna market with a mixed structure where prime contractors lead on large platforms, while specialists compete on subsystems, integration, and niche performance requirements.

Strategic positioning is increasingly tied to program depth and installed relationships rather than only to one-time product launches. L3Harris strengthened its position in the military antenna market through nearly USD 300 million in US Army resilient communications production orders in January 2025 and its February 2026 full-rate submarine communications contract with General Dynamics Electric Boat. AeroVironment advanced in the value chain in May 2026 by securing the SkyRange PANTHER phased-array integration contract, demonstrating antenna specialists' ability to diversify into mission-critical test and telemetry functions. Kymeta's 2026 KuKa 8-Series launch is another example, as it targeted the open space in multi-band, multi-orbit mobile terminals where no single supplier has yet secured clear dominance across all defense users.

Competition is also shifting toward software-defined apertures, integrated survivability, and easier certification across several mission sets. The military antenna market rewards suppliers that can shorten installation time, reduce aperture count, and support multi-band operation on constrained platforms. Rohde & Schwarz's launch of transportable spectrum monitoring systems shows that electromagnetic awareness and communications support are becoming increasingly closely linked in the military antenna market. The military antenna market is also being shaped by trusted manufacturing and industrial-based policy, because buyers increasingly want secure supply, domestic support, and proven long-term sustainment. As a result, competitive advantage now comes from a mix of technology performance, production resilience, and the ability to stay embedded in multi-year defense programs rather than from product specifications alone.

Military Antenna Industry Leaders

-

RTX Corporation

-

Lockheed Martin Corporation

-

BAE Systems plc

-

Rohde & Schwarz GmbH & Co. KG

-

L3Harris Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: AeroVironment was awarded a USD 43 million contract by the Department of War’s Test Resource Management Center to integrate the PANTHER phased array antenna system onto SkyRange platforms. This strategic move highlights the defense sector’s focus on advancing hypersonic telemetry capabilities. By enabling scalable, multi-target tracking with a modular design, PANTHER supports the shift toward agile testing solutions, enhancing the nation’s defense infrastructure and accelerating weapons testing timelines.

- March 2026: Kymeta Corporation unveiled the KuKa 8-Series terminal, marking a significant advancement in SATCOM technology. This multi-band, multi-orbit flat-panel antenna enables simultaneous operation across Ku and Ka bands, offering enhanced connectivity and adaptability for defense and enterprise sectors. Strategically targeting US and allied national security markets, this innovation addresses challenges in contested environments, positioning Kymeta as a key player in advancing resilient, multi-network satellite communication solutions.

- September 2025: Cubic Defense was awarded a contract by the Air Force Research Laboratory to advance its Halo SATCOM antenna, a software-defined system enabling hybrid operations across multiple satellite constellations. This development underscores the growing demand for scalable, low-SWaP communication solutions with multiband and multibeam capabilities. Strategically, this contract positions Cubic Defense to strengthen its role in secure, interoperable SATCOM services for government and commercial applications through 2027.

Global Military Antenna Market Report Scope

Military antennas are specialized systems and related RF components used across defense platforms to provide secure, reliable radio-frequency connectivity in tactical and strategic operating environments. The military antenna market report excludes commercial antennas, consumer communication antennas, civilian telecom antennas, and non-defense RF products unless specifically designed, qualified, procured, or integrated for military applications.

The military antenna market is segmented by platform, frequency band, technology, application, component, and geography. By platform, the market is segmented into airborne, ground, naval, and space. By frequency band, the market is segmented into high frequency (HF), very high frequency (VHF), ultra-high frequency (UHF), super-high frequency (SHF), and extremely high frequency (EHF). By technology, the market is segmented into wire antennas, aperture antennas, array antennas, reflector antennas, lens antennas, and microstrip antennas. By application, the market is segmented into communications, navigation, surveillance, electronic warfare (EW), and telemetry. By component, the market is segmented into radiating elements, feed networks and coax assemblies, RF/microwave switches and phase shifters, radomes, and other components. The report also covers the market sizes and forecasts for the military antenna market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Airborne |

| Ground |

| Naval |

| Space |

| High Frequency (HF) |

| Very High Frequency (VHF) |

| Ultra High Frequency (UHF) |

| Super High Frequency (SHF) |

| Extremely High Frequency (EHF) |

| Wire Antennas |

| Aperture Antennas |

| Array Antennas |

| Reflector Antennas |

| Lens Antennas |

| Microstrip Antennas |

| Communications |

| Navigation |

| Surveillance |

| Electronic Warfare (EW) |

| Telemetry |

| Radiating Elements |

| Feed Networks and Coax Assemblies |

| RF/Microwave Switches and Phase Shifters |

| Radomes |

| Other Components |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Egypt | |

| South Africa | ||

| Rest of Africa | ||

| By Platform | Airborne | ||

| Ground | |||

| Naval | |||

| Space | |||

| By Frequency Band | High Frequency (HF) | ||

| Very High Frequency (VHF) | |||

| Ultra High Frequency (UHF) | |||

| Super High Frequency (SHF) | |||

| Extremely High Frequency (EHF) | |||

| By Technology | Wire Antennas | ||

| Aperture Antennas | |||

| Array Antennas | |||

| Reflector Antennas | |||

| Lens Antennas | |||

| Microstrip Antennas | |||

| By Application | Communications | ||

| Navigation | |||

| Surveillance | |||

| Electronic Warfare (EW) | |||

| Telemetry | |||

| By Component | Radiating Elements | ||

| Feed Networks and Coax Assemblies | |||

| RF/Microwave Switches and Phase Shifters | |||

| Radomes | |||

| Other Components | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | Egypt | ||

| South Africa | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the military antenna market?

The military antenna market size is projected to expand from USD 4.78 billion in 2025 and USD 5.11 billion in 2026 to USD 6.65 billion by 2031, registering a 5.41% CAGR during 2026-2031.

Which technology is leading adoption across defense programs?

Array antennas led with 35.68% in 2025 because they support beam agility, multi-mission use, and better fit with radar, SATCOM, and EW requirements.

Which platform is growing the fastest through 2031?

Space is the fastest-growing platform with an 8.90% CAGR, supported by defense communications satellites, relay architectures, and more electronically steerable payloads.

Why is SHF growing faster than other frequency bands?

SHF is forecast to grow at 9.01% through 2031 because Ka-band and Ku-band SATCOM demand is rising for multi-orbit communications and mobile broadband military links.

What is the biggest application area for these systems?

Communications held 45.30% in 2025, reflecting broad demand from tactical radios, shipborne terminals, aircraft links, and networked ground systems.

Which region offers the strongest growth outlook?

Asia-Pacific is expected to grow the fastest at a 6.90% CAGR through 2031, supported by budget expansion, indigenous production, and higher demand for surveillance and secure communications.

Page last updated on: