Naval Optronics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

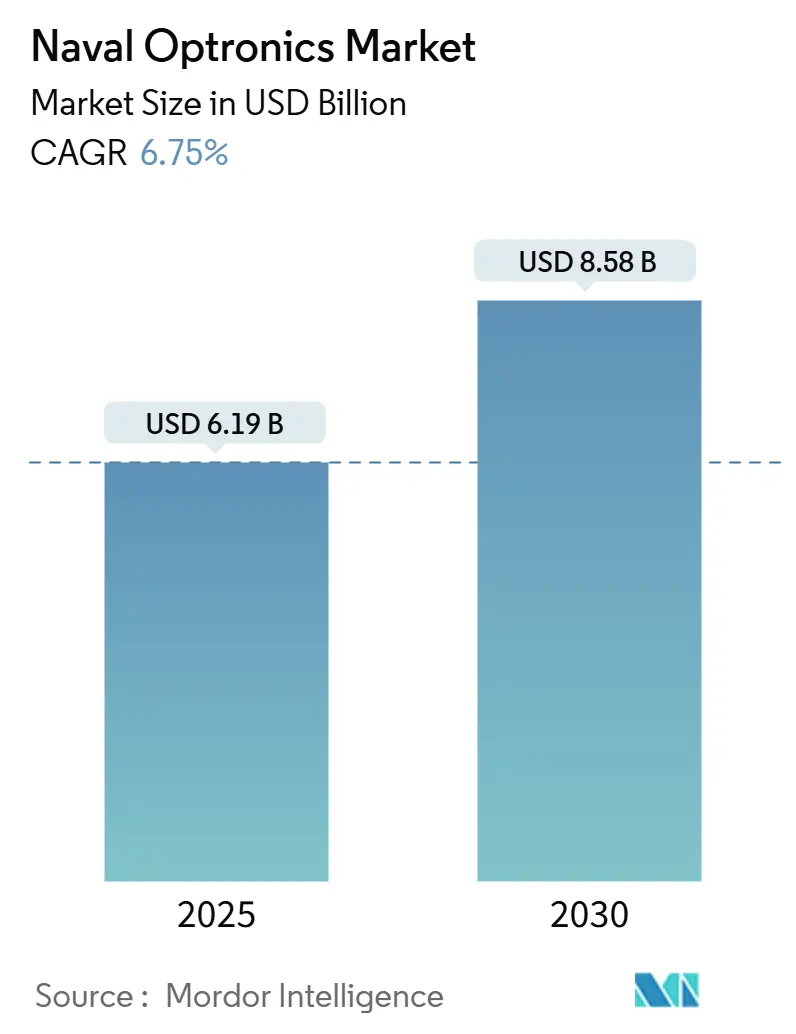

| Market Size (2025) | USD 6.19 Billion |

| Market Size (2030) | USD 8.58 Billion |

| Growth Rate (2025 - 2030) | 6.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Naval Optronics Market Analysis by Mordor Intelligence

The naval optronics market size stood at USD 6.19 billion in 2025 and is forecasted to reach USD 8.58 billion by 2030, expanding at a 6.75% CAGR. Rising defense budgets, accelerating fleet-modernization programs, and the spread of unmanned platforms form the bedrock of this uptrend, as navies seek resilient electro-optic and infrared (EO/IR) capabilities for round-the-clock maritime domain awareness. Program urgency is most visible in the Indo-Pacific and Mediterranean theaters, where contested sea lanes demand real-time threat detection, low-probability-of-intercept tracking, and precision engagement. Vendor competition is sharpening because established primes must now integrate AI-enabled sensor fusion, compact quantum-ready navigation, and laser warning modules typically pioneered by smaller innovators. Subsystem interoperability also matters; navies increasingly insist that optronic payloads plug seamlessly into combat management systems, cyber-hardened data links, and shipboard power architectures. Finally, industrial-policy moves such as the US Supply Chain Resiliency Initiative inject financing to localize detector and cryocooler production, mitigating export-control risk while sustaining the naval optronics market’s growth trajectory.[1]Source: Brownstein Hyatt Farber Schreck, “EXIM Launches Supply Chain Resiliency Initiative to Bolster U.S. Competitiveness,” bhfs.com

Key Report Takeaways

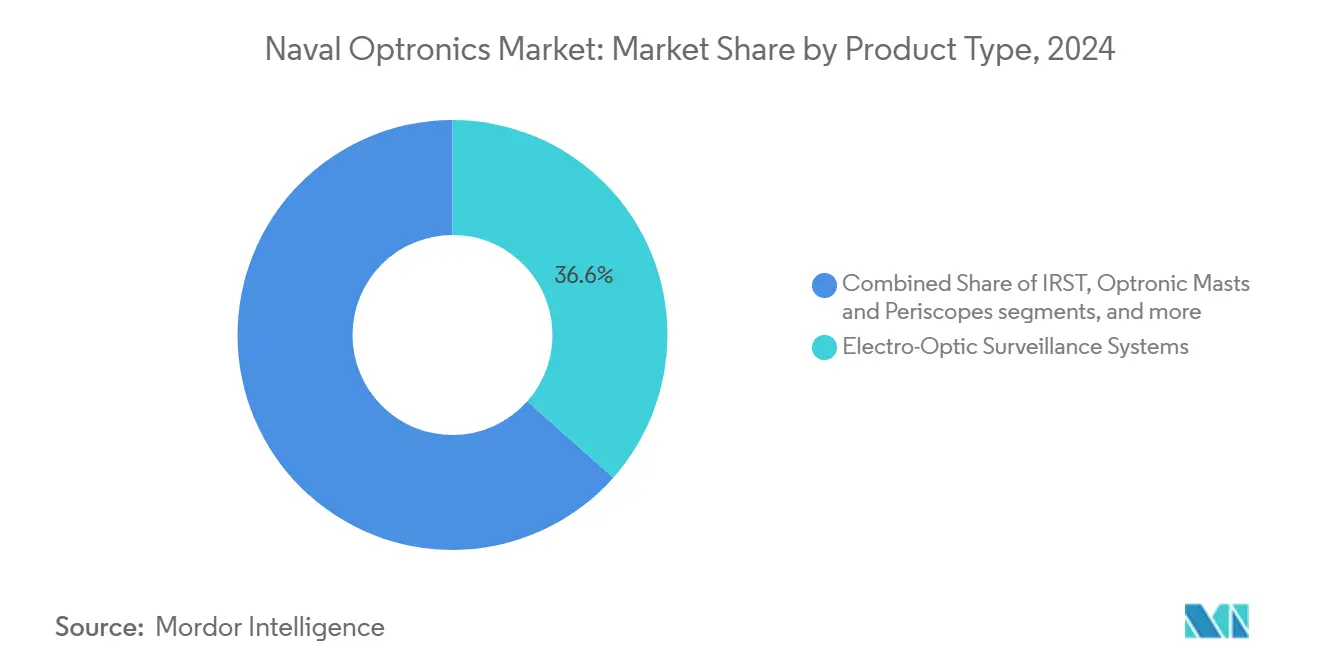

- By product category, electro-optic surveillance systems led with 36.55% revenue share in 2024; optronic masts and periscopes are projected to advance at an 8.34% CAGR to 2030.

- By platform, surface vessels accounted for 54.87% of the naval optronics market share in 2024, while unmanned naval vessels are poised to expand at a 10.45% CAGR through 2030.

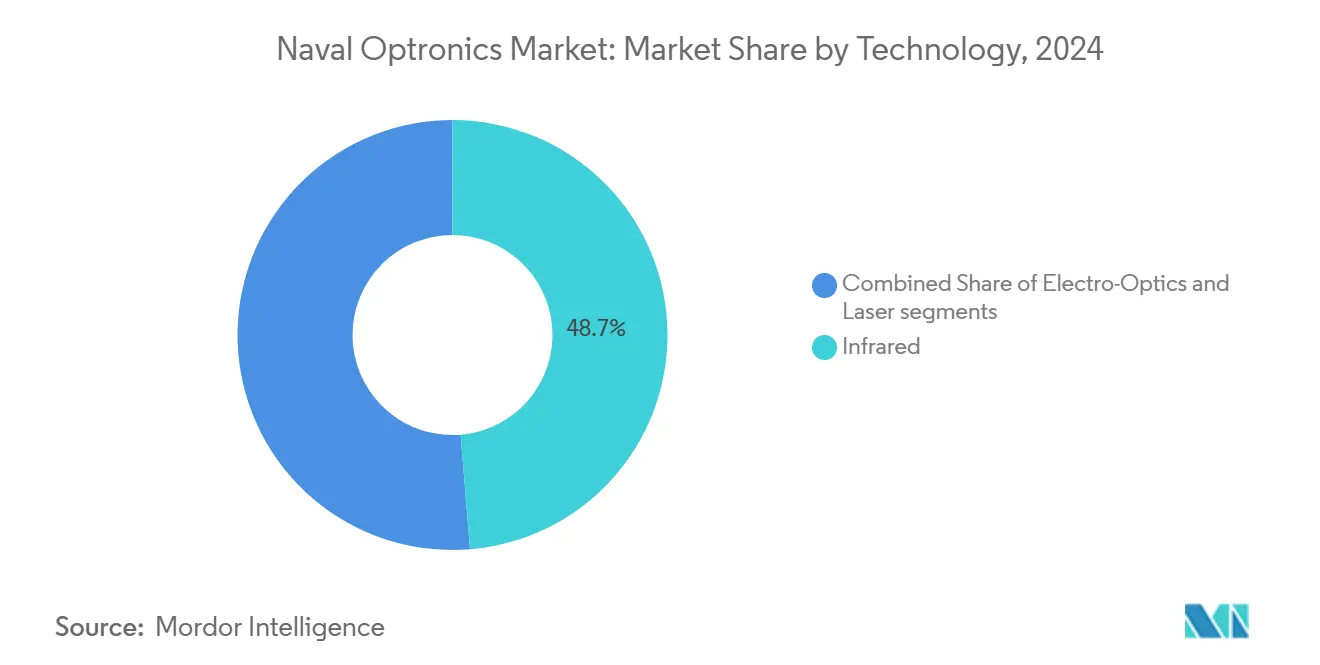

- By technology, infrared sensors commanded a 48.70% share of the naval optronics market in 2024, and lasers are set to grow at an 8.30% CAGR over 2025-2030.

- By end-user, naval forces held a 70.90% share in 2024; coast-guard and maritime police demand is forecasted to rise at a 7.67% CAGR during the same horizon.

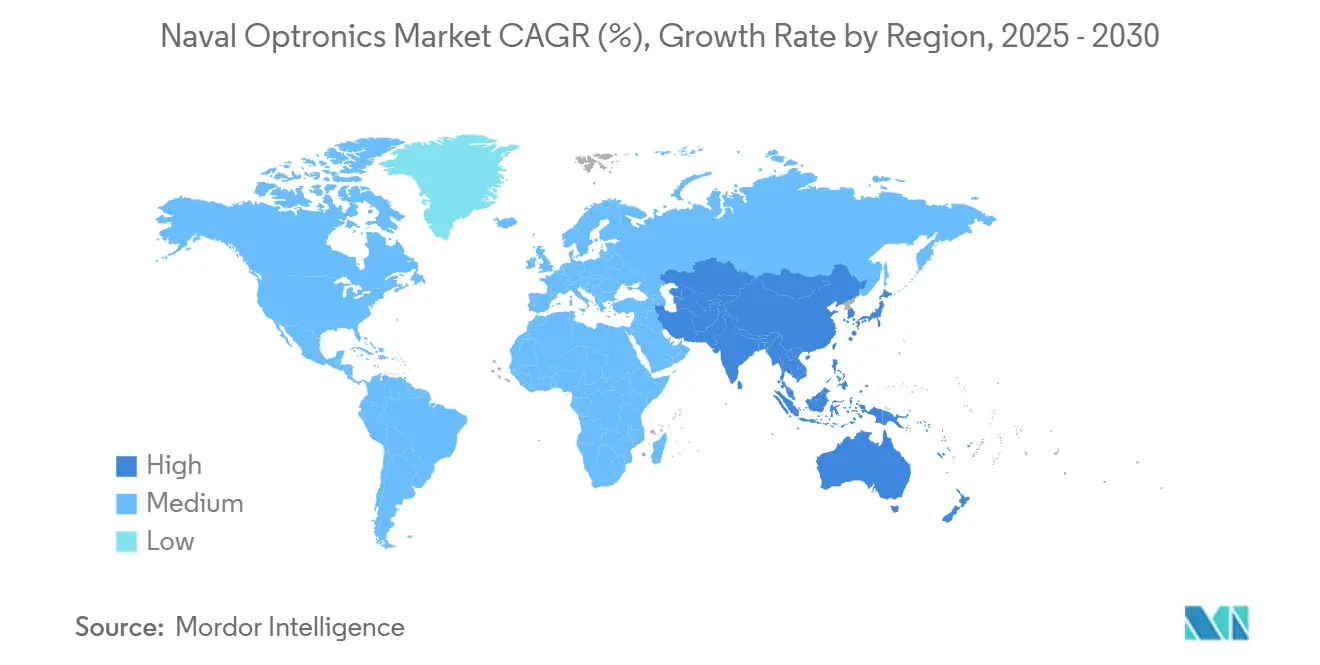

- By geography, North America generated 32.41% of 2024 revenue, whereas Asia-Pacific is on track for the fastest 8.10% CAGR through 2030.

Global Naval Optronics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Naval fleet-modernization programs accelerating EO/IR demand | +1.8% | Global, with concentration in US, China, India, Europe | Medium term (2-4 years) |

| Growing need for maritime domain awareness ISR suites | +1.5% | Global, particularly Indo-Pacific and Mediterranean | Long term (≥ 4 years) |

| Retrofit boom for 360-degree infrared search and track (IRST) | +1.2% | North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| Rising naval defense budgets amid geopolitical tensions | +1.1% | Global, with emphasis on contested maritime regions | Long term (≥ 4 years) |

| Proliferation of unmanned maritime platforms needing compact payloads | +0.9% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Anti-drone laser warning capability emerging as a driver | +0.7% | Global, with early adoption in NATO and allied navies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Naval Fleet-Modernization Programs Accelerating EO/IR Demand

Global surface-combatant and submarine upgrade cycles translate directly into batch procurements of optronic directors, pan-tilt-zoom cameras, and cooled MWIR imagers that replace legacy analog optics. France’s EUR 200 million (USD 235.21 million) FREMM retrofit, which installs Thales PASEO XLR day-night sights and STIR 1.2 Mk 2 fire-control modules, typifies how navies embed standard sensor stacks across multiple hull classes for logistics efficiency.[2]Source: Naval News Staff, “France Is Fitting PASEO XLR EO/IR System on All Its FREMM and Air Defense Destroyers,” navalnews.com India’s plan to operate 170 frontline vessels by 2030 unlocks multiyear demand for mast-mounted electro-optics under its USD 15 billion domestic-build doctrine. Similar trajectories appear in Saudi, Australian, and Japanese new-build programs, each stipulating full-motion-video fusion, automatic tracker cueing, and cyber-secure firmware. These mandates reinforce the naval optronics market as a spend-priority line item within multi-domain deterrence strategies.

Growing Need for Maritime Domain Awareness ISR Suites

Expanding exclusive economic zones and the surge in gray-zone tactics compel fleets to stitch EO/IR, radar, and AIS feeds into continuous surface pictures. China’s People’s Liberation Army Navy (PLAN) intends to operate 550 hulls by 2030 and already networks shipboard optronics with shore-based fusion hubs for persistent wide-area surveillance. Western suppliers respond by bundling automated target-recognition software that flags suspicious vessels inside a single user interface, trimming operator load and enabling earlier rules-of-engagement decisions. Port authorities also piggyback on military networks, shifting portions of the naval optronics market demand toward dual-use coastal systems.

Retrofit Boom for 360° Infrared Search and Track (IRST)

Low-observable anti-ship missiles and radar-evading drones expose the limits of RF sensors in sea-skimming profiles. Consequently, navies retrofit 360-degree cooled IRST clusters on destroyer masts and aircraft pylons, ensuring passive cueing without revealing emitter location. The US Navy’s IRST 21 Block II full-rate production award validates budget appetite for such upgrades, and allied fleets from Australia to Taiwan mirror the architecture to outpace hypersonic threats. High-dynamic-range focal-plane arrays, cryocoolers rated beyond 10,000 hours MTBF, and FPGA-based real-time trackers spur a brisk aftermarket that lifts the naval optronics market beyond original-equipment sales.

Rising Naval Defense Budgets Amid Geopolitical Tensions

World military outlays hit USD 2.7 trillion in 2024, with maritime allocations climbing fastest as governments prioritize sea-lane security. A record 17 NATO members now spend above the 2% GDP threshold, while Asia-Pacific procurement pipelines exceed USD 200 billion over 2025-2035 according to SIPRI data. Legislative packages such as the US National Defense Industrial Strategy incentivize local assembly of infrared detectors and germanium optics, buffering programs against ITAR bottlenecks and energizing regional naval optronics market ecosystems.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and maintenance cost of cooled IR sensors | -1.4% | Global, particularly affecting smaller navies and coast guards | Long term (≥ 4 years) |

| Export regulations (ITAR/ML11) limiting detector supply | -1.1% | Global, with primary impact on non-allied nations | Medium term (2-4 years) |

| Corrosive marine environment raises lifecycle cost | -0.8% | Global, with higher impact in tropical and arctic regions | Long term (≥ 4 years) |

| Shipboard power/space limits adoption of high-res imaging | -0.6% | Global, particularly affecting smaller platforms and retrofits | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Maintenance Cost of Cooled IR Sensors

Cooled MWIR assemblies, priced at USD 80,000–100,000 per unit even before ship integration, require closed-cycle Stirling coolers that demand depot-level overhauls every 8,000 hours. Over 15 years, maintenance charges can treble the original invoice, squeezing coast-guard budgets and tier-2 navies. DTRA procurement files illustrate how small-lot orders amplify per-unit expenses, because economies of scale quit at run lengths below 100 sensors.[3]Source: Defense Threat Reduction Agency, “Active Contract List,” dtra.mil These high lifecycle costs deter wide deployment on auxiliary ships, restraining parts of the naval optronics market until uncooled performance narrows the gap.

Export Regulations (ITAR / ML11) Limiting Detector Supply

Advanced InSb and HgCdTe focal-plane arrays sit squarely under US ITAR and Wassenaar ML11 control, elongating export licensing by 9-12 months and triggering offset demands. Non-aligned states often pivot to domestic substitutes that lag Western sensitivity benchmarks by a full Noise-Equivalent-Temperature-Difference generation, constraining capability while fragmenting supply chains. The naval optronics market thus faces predictable demand pockets but unpredictable deal closure timelines whenever end-users fall outside preferred-partner lists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Surveillance Systems Lead Modernization Wave

Electro-optic surveillance suites captured 36.55% of the naval optronics market share in 2024, reflecting their central role as long-range eyes for destroyers, frigates, and patrol vessels. Fleet commanders prize these multi-sensor blocks because they combine high-definition color cameras, autotrackers, and gyro-stabilization that cuts jitter under Beaufort-6 seas, enabling reliable identification ranges beyond 18 km. Demand is further bolstered by software-defined video pipelines that support periodic algorithm refreshes without hardware swaps, prolonging asset relevance through the 2030s. Meanwhile, optronic masts and periscopes are storming ahead at an 8.34% CAGR, largely because submarines ditch line-of-sight optics for digital modules that transmit real-time feeds to below-deck consoles, freeing designers to enhance hull stealth by eliminating sail penetrations. Suppliers such as Safran and HENSOLDT have standardized optronic mast footprints, so retrofit downtime shrinks to a single maintenance period, accelerating volume adoption and fortifying the Naval Optronics market growth curve.

Across the remaining categories, IRST arrays ride the retrofit wave as navies counter low-observable threats, and their passive nature pleases rules-of-engagement lawyers by avoiding electromagnetic disclosure. Laser rangefinders and designators are integrating with anti-drone beams and precision-guided munition suites, pushing average selling prices upwards. Night-vision and low-light cameras, though niche, anchor humanitarian and search-and-rescue missions, particularly for coast-guard patrols in high-traffic chokepoints. These varied procurement drivers mean suppliers must juggle high-volume visible-light optics lines against low-volume, custom-cooled infrared modules, a balancing act that shapes competitive strategy across the naval optronics market.

By Platform: Surface Vessels Dominate While Unmanned Systems Surge

Surface combatants owned 54.87% of revenue in 2024 because every new or mid-life-refit hull mandates at least two stabilized EO directors plus secondary cameras for navigation and fire-control redundancy. The FREMM and Type 26 programs exemplify this integration density, with each hull receiving mast-head day-night panoramics augmented by deckhouse missile-guidance channels. These high-spec installations preserve surface dominance within the naval optronics market size calculus. Submarine outfitting stays steady as nuclear and conventional boats swap legacy optics for digital masts that export encrypted feeds to command centers. Still, the real momentum comes from unmanned surface and underwater vessels growing at a 10.45% CAGR.

Adoption of compact EO/IR payloads on autonomous craft dovetails with doctrines calling for risk reduction and dispersed lethality. Because unmanned platforms must minimize mast signatures and battery drain, vendors accelerate R&D on wafer-bonded ROICs and graphene heat spreaders. These innovations promise 30% lighter gimbals at equal line-resolution performance. These advances spur a virtuous cycle: lighter payloads enable smaller hulls, which demand even leaner sensors, which broaden addressable demand and reinforce the naval optronics market’s medium-term expansion.

By Technology: Infrared Leads While Laser Systems Accelerate

Infrared imaging secured a 48.70% share in 2024 because MWIR and LWIR channels deliver all-weather target detection well beyond visible-light horizon limits. Navies consistently prioritize cooled detector performance—even against high unit cost so long-wave thermal clarity at dawn, dusk, and bad-weather windows remains unmatched. Manufacturers invest in larger-format 1280×1024 arrays and closed-cycle cryocoolers with improved mean-time-between-overhauls to sustain naval optronics market credibility for mission-critical sensors. Electro-optic visible-light channels retain importance for color depth, flag identification, and positive visual confirmation under rules of engagement.

Laser technology is the breakout story, forecast at an 8.30% CAGR on the strength of dual-use ranging and counter-UAS applications. The US Navy’s HELIOS journey proves photonic integration can live aboard destroyers. European counterparts now request beam-combining optics co-boresighted with day-night cameras for instant switch from identification to neutralization. Suppliers able to package high-energy transport fibers, low-lag beam directors, and broadband detectors in a single environmental housing find themselves at the centre of tender shortlists, amplifying the naval optronics market opportunity within laser subsystems.

By End-User: Naval Forces Dominate While Coast Guards Modernize

Naval forces generated 70.90% of 2024 revenue because blue-water fleets require deep inventories of optronics across destroyers, carriers, patrol aircraft, and helicopters. Procurement rationales emphasize common sensor architectures so mixed-platform task forces share metadata layers and accelerate kill-chains, a principle showcased by the US Navy’s Distributed Maritime Operations concept. Coastal defense and maritime police agencies, though historically budget-constrained, now modernize to monitor illegal fishing, trafficking, and Arctic route incursions. Their 7.67% CAGR stems from lighter gimbals, lower-cost uncooled cores, and multi-year financing models funded through development-bank blue-economy lines.

Such law-enforcement programs prize ease of use and simplified maintenance, driving vendors to offer three-year warranty packages with embedded training. Interoperability with naval battle-management systems delivers force-multiplier effects during joint operations, blending coast-guard patrols into larger security architectures. This synergy enlarges the user base and further hardwires naval optronics market dynamics into national maritime-security planning.

Geography Analysis

North America retained 32.41% of 2024 holds to steady procurement by the US Navy and Canada’s Surface Combatant project, which locks in multi-decade sensor support contracts that favor domestic manufacturers under Buy-American and Industrial-Technological-Benefits clauses. The US Export-Import Bank’s Supply Chain Resiliency Initiative earmarks USD 135 billion in credit to upstream optics and semiconductor firms, enabling local indium-antimonide wafer fabs and germanium lens grinders that de-risk detector supply. These policy levers reinforce regional self-sufficiency and sustain North America’s leading slice of the naval optronics market.

Europe’s mixed fleet architecture and multinational build partnerships create a fertile environment for collaborative sensor programs funded under the European Defence Fund. France’s ongoing FREMM retrofits and the UK’s Type 31 Frigate optic suites showcase how continental navies standardize EO/IR turrets across dissimilar hulls to curb lifecycle costs. Meanwhile, PESCO cross-border projects promote shared requirements documents that shrink development duplication and broaden supplier prospects. Such cohesion keeps Europe in second place on revenue tables while promoting technology depth that underpins the naval optronics market’s long-term innovation pipeline.

Asia-Pacific, posting an 8.10% CAGR, is propelled by China’s and India’s parallel blue-water ambitions, Japan’s helicopter-carrier upgrades, and Australia’s AUKUS-aligned sensor orders. Territorial flashpoints from the South China Sea to the Sea of Japan necessitate day-night sensor granularity to monitor gray-zone activities, prompting large-lot purchases of long-wave panoramic IRST bars and mast-mounted optronics. Export-control frictions encourage indigenous manufacturing in India and South Korea, altering global supply-chain maps and adding fresh competitors to the naval optronics market roster. At the same time, ASEAN coast-guards pool procurement via joint maritime-security funds, further expanding regional demand.

Competitive Landscape

The naval optronics market sits at a moderate concentration level. The top five vendors hold roughly semi-consolidated market share, leaving ample room for newcomers specializing in niche subsystems or AI-enhanced signal processing. Thales, Leonardo, and BAE Systems defend incumbency by bundling EO/IR payloads with ship integration, logistics, and through-life support. HENSOLDT and Elbit Systems carve out a share through software-definable architectures that allow firmware pushes to unlock new target-recognition algorithms, thereby future-proofing installed bases. L3Harris and Teledyne excel in cryocooler reliability, an often overlooked metric that drives repeat contracts, given the high cost of deckhouse teardown.

Innovation focus has shifted toward autonomous target-classification engines that cut operator workload. Raytheon’s Raiven demonstrator fuses hyperspectral cues with mid-wave imagery to deliver automatic threat prioritization within two seconds, a leap that leading navies see as indispensable for distributed lethality concepts. Quantum-enhanced inertial navigation units co-developed by Imperial College and the Royal Navy promise to keep optronics accurately bore-sighted even under GNSS jamming, signaling the next frontier of differentiation. Start-ups targeting lightweight laser-warning receivers or photonic beam expanders attract venture funding, underscoring fresh competitive pressure that compels primes to pursue partnership or acquisition strategies. As a result, the market’s competitive narrative is less about unit volumes and more about who controls upgradeable software stacks, resilient supply chains, and multidisciplinary IP.

Naval Optronics Industry Leaders

Thales Group

Safran SA

Leonardo S.p.A.

HENSOLDT AG

Elbit Systems Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: LightPath Technologies' subsidiary G5 Infrared secured a USD 2.2 million contract from L3Harris Technologies for infrared camera systems. The contract will enhance naval defense capabilities by supporting the US Navy's Shipboard Panoramic Electro-Optic/Infrared (EO/IR) Program.

- March 2024: France committed EUR 200 million (USD 235.21 million) to fit PASEO XLR electro-optics across all FREMM frigates and air-defense destroyers.

- June 2023: Paras Defence and Space Technologies Limited secured a contract from the Instrument Research & Development Establishment (IRDE) to develop optical periscopes for ICS. The contract includes optical periscope development and installation support to enhance the Indian Navy's submarine surveillance capabilities.

Global Naval Optronics Market Report Scope

| Electro-Optic Surveillance Systems |

| Infrared Search and Track (IRST) |

| Laser Rangefinders and Designators |

| Night-Vision and Low-Light Cameras |

| Optronic Masts and Periscopes |

| Surface Vessels |

| Submarines |

| Unmanned Naval Vessels |

| Electro-Optics |

| Infrared |

| Laser |

| Naval Forces |

| Coast Guards and Maritime Law Enforcement Agencies |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Electro-Optic Surveillance Systems | ||

| Infrared Search and Track (IRST) | |||

| Laser Rangefinders and Designators | |||

| Night-Vision and Low-Light Cameras | |||

| Optronic Masts and Periscopes | |||

| By Platform | Surface Vessels | ||

| Submarines | |||

| Unmanned Naval Vessels | |||

| By Technology | Electro-Optics | ||

| Infrared | |||

| Laser | |||

| By End-User | Naval Forces | ||

| Coast Guards and Maritime Law Enforcement Agencies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the Naval Optronics market in 2030?

The market is forecasted to reach USD 8.58 billion by 2030, up from USD 6.19 billion in 2025, expanding at a 6.75% CAGR.

Which product category currently dominates procurement?

Electro-optic surveillance systems hold the leading 36.55% revenue share thanks to fleet-wide ISR modernization.

How fast are unmanned naval vessels adopting optronic payloads?

Unmanned platforms represent the fastest-growing segment, expanding at a 10.45% CAGR through 2030.

Why are infrared sensors prioritized despite higher costs?

MWIR and LWIR channels deliver superior all-weather detection ranges, making them indispensable for surface-combatant defense.

Which region will see the highest growth through 2030?

Asia-Pacific is projected for the strongest 8.10% CAGR due to rapid fleet expansion and rising maritime tensions.

Page last updated on: