Firearm Sight Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

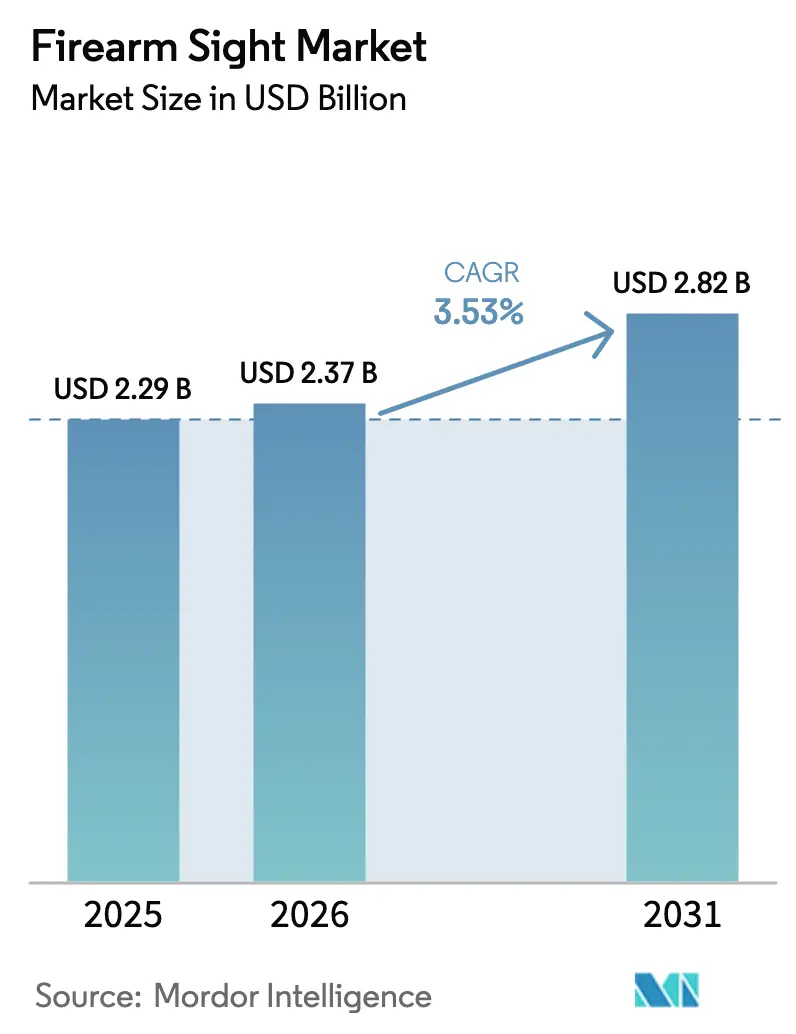

| Market Size (2026) | USD 2.37 Billion |

| Market Size (2031) | USD 2.82 Billion |

| Growth Rate (2026 - 2031) | 3.53% CAGR |

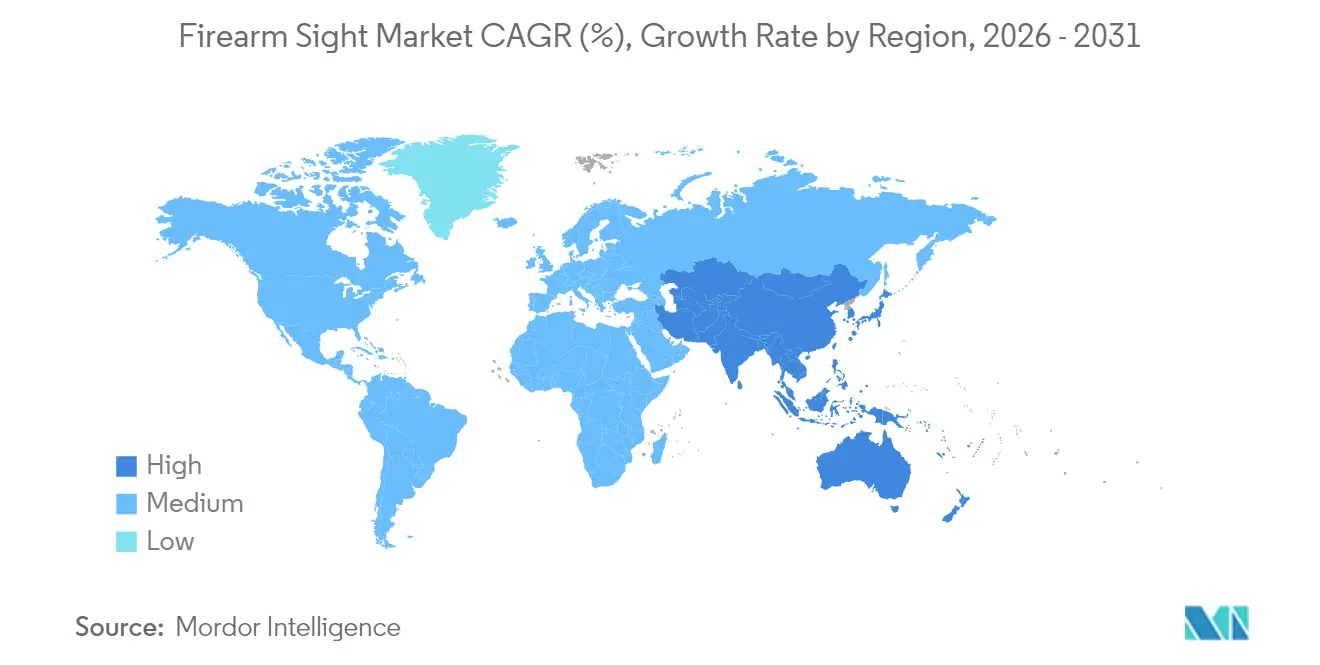

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Firearm Sight Market Analysis by Mordor Intelligence

The firearm sight market size in 2026 is estimated at USD 2.37 billion, growing from 2025 value of USD 2.29 billion with 2031 projections showing USD 2.82 billion, growing at 3.53% CAGR over 2026-2031. Robust modernization programs in defense and law-enforcement circles are widening the user base and lifting average selling prices, while the spread of digital fire-control ecosystems is reshaping procurement priorities. Telescopic optics keep demand anchored in legacy applications, yet the pull of innovative, AR-enabled platforms is undeniable as militaries specify integrated range-finding, wireless networking, and hardened electronics. Law-enforcement agencies now authorize optic-equipped service pistols at scale, generating economies that spill into civilian channels and sustaining a large aftermarket for mounts, batteries, and training services. Competitive advantage is migrating toward firms that can fuse software, sensors, and displays into rugged, swap-friendly housings, and supply-chain resilience around critical semiconductors has become a decisive differentiator. Regional growth is rebalancing as Asia-Pacific accelerates large-scale rifle programs, challenging historical North American dominance and prompting suppliers to diversify manufacturing footprints.

Key Report Takeaways

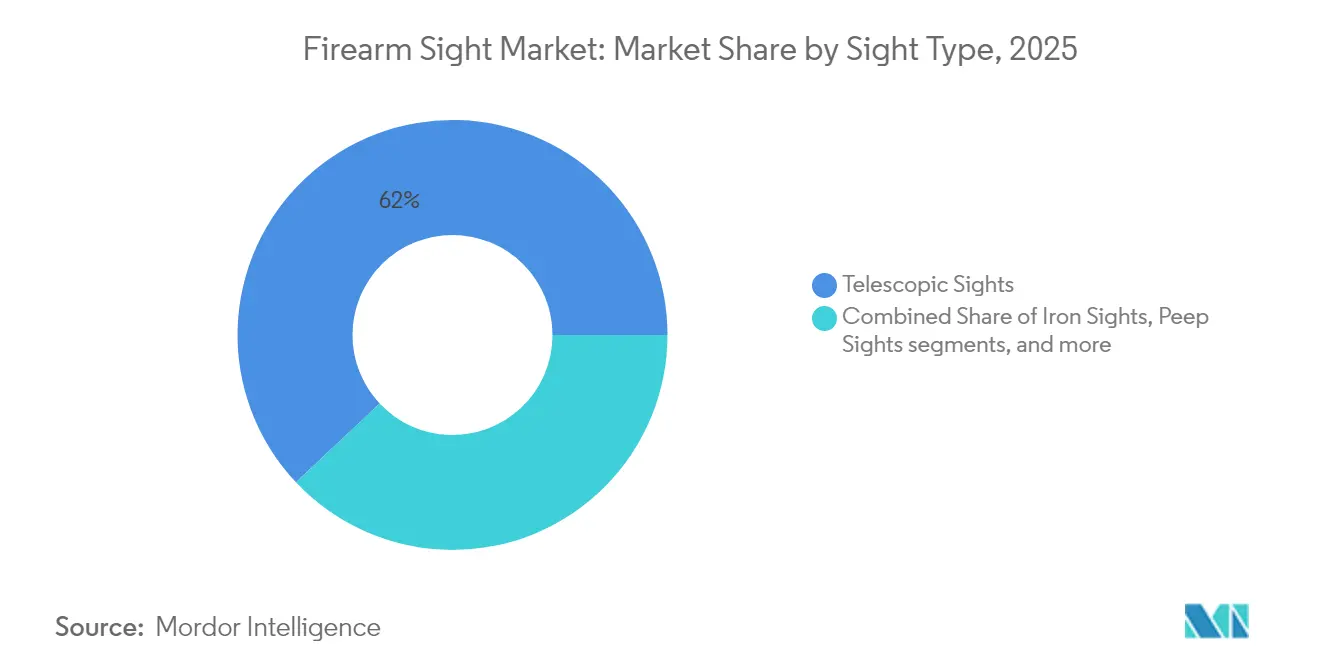

- By sight type, telescopic optics led with 62.02% of firearm sight market share in 2025, and are projected to grow at a 3.77% CAGR through 2031.

- By technology, optical platforms accounted for a 30.88% share of the firearm sight market in 2025; AR-enabled systems delivered the fastest expansion at a 4.48% CAGR to 2031.

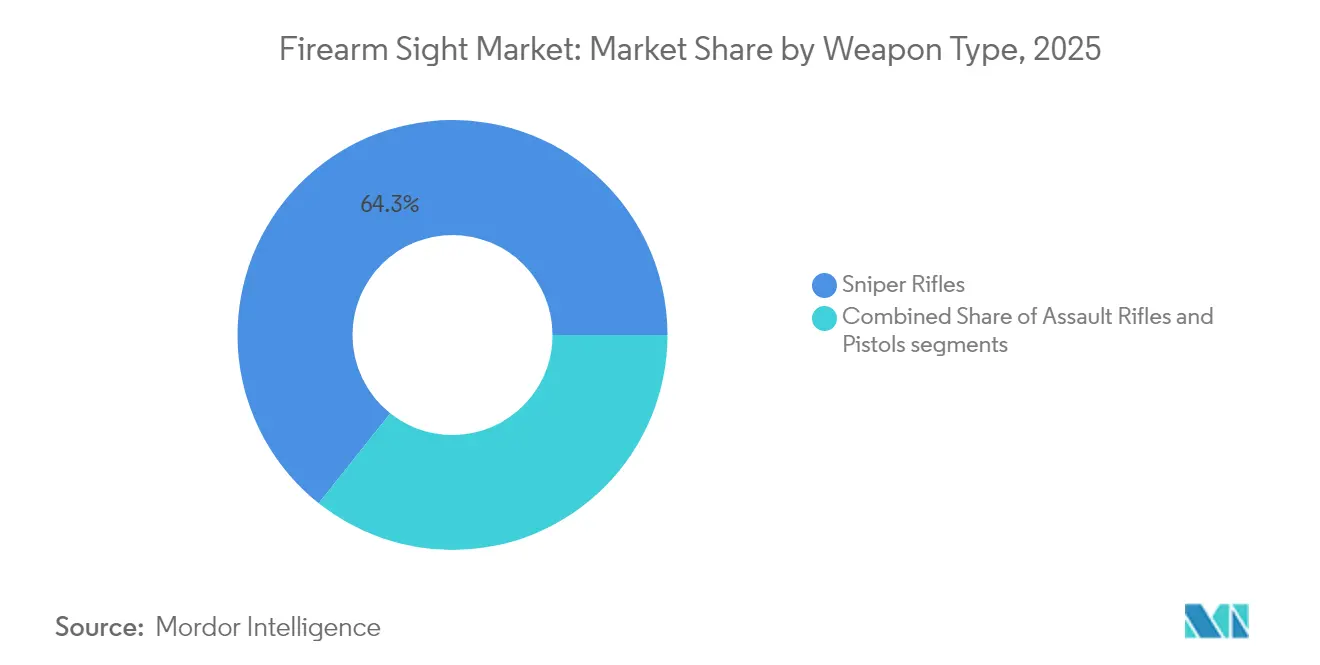

- By weapon type, sniper rifles captured 64.31% of the firearm sight market size in 2025 and are advancing at a 3.72% CAGR through 2031.

- By end user, the military segment held 68.12% of the firearm sight market share in 2025, growing at a 3.81% CAGR to 2031.

- By geography, North America retained a 31.04% share of the firearm sight market size in 2025, whereas the Asia-Pacific is expanding at a 4.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Firearm Sight Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing global interest in shooting sports and recreational hunting | +0.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Military modernization initiatives driving demand for advanced sighting systems | +1.2% | Global, concentrated in Asia-Pacific and North America | Long term (≥ 4 years) |

| Widespread adoption of red dot optics among law enforcement agencies | +0.6% | North America and Europe, expanding to APAC | Short term (≤ 2 years) |

| Technological advancements in lightweight and ruggedized optical systems | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Integration of augmented reality (AR) and digital reticle technologies | +0.7% | Global, early adoption in North America | Long term (≥ 4 years) |

| Easing of civilian firearm ownership regulations in select global markets | +0.4% | Regional, primarily North America and select Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Military Modernization Initiatives Driving Demand for Advanced Sighting Systems

Defense buyers are pivoting toward platform-level optics that merge laser range-finding, ballistics computation, and data-link functions in a single housing. The US Army’s multibillion-dollar XM157 program exemplifies this shift, giving suppliers that master software-hardware convergence a clear edge. Allied forces mirror the trend, as Britain fields the Talon Fused Weapon Sight to retrofit existing rifles with thermal tracking, lowering replacement costs and extending service life.[1]Alexander Candlin, “New Talon System Will Turn Conventional British Army Rifle Optic into Thermal Sight,” Forcesnews.com, forcesnews.com Such integration raises switching costs for armed services, tightening supplier relationships, and sharpening barriers to entry for firms lacking digital competencies. New contracts increasingly specify open-architecture firmware and secure wireless protocols, indicating that interoperability is now a baseline requirement rather than a differentiator. Consequently, the firearm sight market rewards innovators who can deliver end-to-end ecosystems that survive brutal recoil, temperature swings, and battlefield cyber scrutiny.

Widespread Adoption of Red Dot Optics Among Law-Enforcement Agencies

Police departments are operationalizing pistol-mounted red-dot sights after multiyear trials validated accuracy and response-time improvements. The Pennsylvania State Police contract for Aimpoint ACRO P-2 units has set a benchmark that smaller agencies imitate, boosting volume and reducing unit costs for civilian buyers. Field data from 35 officer-involved shootings has dispelled durability concerns, allowing risk-averse administrators to green-light optic programs more quickly. As individual officers purchase the same models for off-duty use, manufacturers gain secondary retail sales without additional marketing spend. Training academies have updated curricula to include optic-specific draw strokes and zeroing procedures, creating a pull-through effect on ancillary gear such as holsters and cleaning kits. The cascade into the firearm sight market is accelerating because warranty, battery-life, and lens-clarity improvements meet professional uptime demands while remaining affordable for recreational shooters.

Technological Advancements in Lightweight and Ruggedized Optical Systems

Breakthroughs in glass chemistry and additive manufacturing allow thinner lenses and shock-resistant housings that shave grams without sacrificing clarity. Chalcogenide substrates such as BDNL4 match germanium’s infrared performance yet tolerate higher thermal swings, mitigating supply-chain risk and enhancing image stability for thermal scopes. Digital fire-control sights hitting 100% accuracy with novice users highlight the convergence of optics and AI-driven ballistic solvers, limiting human error and shortening training cycles. Environmental micro-sensors now sit inside optic bodies, feeding algorithms that auto-adjust reticles for barometric pressure and cant, keeping zero under field conditions. These advances enlarge the total addressable firearm sight market by making premium precision feasible for patrol officers, hunters, and sport shooters who previously deemed electronics too fragile or heavy.

Integration of Augmented Reality and Digital Reticle Technologies

Weapon sights are transforming into data nodes that overlay ballistic predictions, target IDs, and network messages directly onto the shooter’s view. Programs such as the Enhanced Night Vision Goggle III link thermal crosshairs to helmet displays, confirming that optical devices are no longer isolated components but elements of a sensor-to-shooter grid. High-brightness micro-OLEDs maintain reticle visibility in desert sunlight, while secure Bluetooth channels push friend-or-foe cues to the glass without cluttering the field of view. Intellectual-property filings reveal work on eye-box tracking that centers digital overlays even under awkward firing postures, pointing to future head-up display symmetry with vehicle platforms. This blurring of optic and C4ISR roles means procurement officers assess sights not just on clarity and durability but on cyber resilience and firmware update logistics, expanding the competitive lens beyond traditional optics brands.

Restraints Impact Analysis*

| Restraint | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict international trade regulations governing optical sight exports and imports | -0.9% | Global, particularly US-China trade | Short term (≤ 2 years) |

| Uncertainty in defense procurement cycles impacting long-term contracts | -0.6% | Global, concentrated in major defense markets | Medium term (2-4 years) |

| High compliance costs for certification in civilian distribution channels | -0.4% | North America and Europe | Medium term (2-4 years) |

| Semiconductor supply constraints affecting compact optical electronics | -0.7% | Global, most severe in APAC manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strict International Trade Regulations Governing Optical Sight Exports and Imports

Revisions to US Export Administration Regulations have cut license validity to one year and introduced fresh classification codes, forcing optics makers to refile paperwork annually, which absorbs legal bandwidth and cash more easily borne by large contractors.[2]Bureau of Industry and Security, “Revision of Firearms License Requirements,” Federalregister.gov, federalregister.gov The UK’s 2024 control-list update mirrored Wassenaar obligations, lumping advanced weapon sights alongside emerging quantum sensors, thereby extending audit scopes. These overlapping regimes compel firms to triage market entries, often abandoning mid-tier countries whose compliance yields marginal returns. Distributors in high-risk regions face presumptive license denials, fragmenting stock availability, and hampering after-sales support. Collectively, the administrative weight crimps export momentum for smaller innovators and accelerates consolidation in the firearm sight market as buyers gravitate toward suppliers with in-house compliance departments.

Semiconductor Supply Constraints Affecting Compact Optical Electronics

Optics brands dependent on gallium-arsenide emitters have endured 75% price spikes and 40-week lead times after China limited exports of gallium and germanium, central inputs for night-vision modules. Pentagon-commissioned studies warn that defense imagery chains risk mission gaps if foreign wafer supply collapses, sparking domestic fab acquisitions such as the UK government’s purchase of a GaAs plant to ring-fence military optics needs. Manufacturers now redesign boards around whatever ASICs are in stock, sacrificing battery life or refresh rates. Prioritization of military orders diverts capacity from civilian SKUs, inflaming shortfalls in the hunting and competitive-shooting channels. Long term, vertical integration into chip packaging appears inevitable for Tier-1 vendors, potentially altering cost structures and deepening barriers to entry across the firearm sight market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sight Type: Telescopic Dominance Faces Digital Disruption

Telescopic products accounted for 62.02% of the firearm sight market size in 2025 as armed forces, hunters, and precision competitors relied on magnified optics for targets beyond 300 m. Despite their entrenched share, these models also clocked a 3.77% CAGR, underscoring that enhancements such as fiber-optic illumination and low-dispersion glass keep them relevant. Manufacturers combine legacy turrets with onboard ballistic computers, creating crossover SKUs that erode the boundary with reflex platforms. The run-rate of iron and peep sights stays modest, reserved for training or as emergency backups when electronics fail. Reflex and laser categories grow steadily in short-range duty pistols and personal-defense carbines where speed trumps magnification.

Parallel demand for dot sights is propelled by law-enforcement mandates and concealed-carry trends, adding volume without erasing telescopic share because users often own both styles for different firearms. Vortex’s XM157 design, which blends 1-8x glass with an integrated range-finder, illustrates how telescopic families absorb digital DNA, extending their lifecycle. As such, the firearm sight market supports a dual-track roadmap: classic glass for long-eye-relief accuracy and digitally infused optics that compress multiple accessories into one rugged shell.

By Technology: Digital Integration Accelerates Despite Optical Foundation

Optical architectures still underpinned 30.88% of the firearm sight market share in 2025, reflecting decades of invested manufacturing and verified field reliability. However, smart AR-enabled solutions lead growth at 4.48% CAGR as defense ministries embed networked targeting into infantry doctrines. Thermal and night-vision platforms remain procurement priorities for special operations units even if unit prices exceed USD 7,000, emphasizing mission over budget. Meanwhile, civilian buyers gravitate toward hybrid sights that retain etched glass reticles usable with dead batteries, reducing perceived risk of electronic failure.

Holosun’s Digital Pistol Sight thermal optic shows miniaturization breakthroughs that push active-imaging sensors into handgun form factors once limited to LED dots. Raytheon’s digital fire-control portfolio layers DOPE cards and wind holds atop a traditional FFP reticle, symbolizing reality-plus displays rather than wholesale replacement. The segmentation narrative thus pivots on integration proficiency: customers value firmware update streams, data-encryption hardening, and cross-platform accessory syncing as much as lens coatings, expanding the specification checklist that shapes the firearm sight market.

By Weapon Type: Sniper Applications Drive Premium Segment Growth

Sniper platforms owned 64.31% of the firearm sight market size in 2025 and are projected to outpace overall growth at 3.72% CAGR. Their influence stems from the command's willingness to allocate higher budgets per rifle, enabling optics with laser ranging, tilt sensors, and variable magnification in one chassis. Assault rifles retain the volume crown among infantry forces, yet confront per-unit cost ceilings that push suppliers to modularize offerings and share subassemblies across SKUs. Pistols are catching up due to the wholesale shift of police departments toward slide-mounted red dots, a pattern mirrored by competitive USPSA shooters whose equipment lists bend rule books.

Interoperable mount standards let users shift a USD 2,000 optic from a carbine to a designated marksman rifle overnight, raising utilization rates and justifying premium purchases. Japan's Type 20 rifle spec with NATO-pattern rails showcases how new weapon contracts bake optic-friendly interfaces into factory builds, boosting attach rates per soldier. Consequently, accessory spend per firearm is rising, enriching revenue pools within the firearm sight market even where absolute weapon procurement numbers stay flat.

By End User: Military Modernization Sustains Market Leadership

Militaries consumed 68.12% of the firearm sight market share in 2025 and will sustain a 3.81% CAGR as procurement pivots from bulk buys to high-spec sensors that enhance individual lethality. These programs often adopt spiral-upgrade models, inserting new electronics into existing optics housings to stretch service lives and budgets. Law-enforcement agencies form a bridge cohort, demanding MIL-STD shock thresholds but valuing size and cost closer to consumer gear. Hunting and target-shooting publics benefit from trickle-down features once fielded by special forces, such as auto-dimming reticles and Bluetooth chronograph pairing.

The US Fish and Wildlife Service counted 47 million target shooters in 2024, an addressable audience that underwrites volume production runs, keeping retail prices palatable and incentivizing continuous R&D. Commercial successes like EOTECH’s three millionth holographic unit prove that once-niche technology can become mainstream when manufacturing amortizes across defense and civilian channels. Consequently, product-roadmap decisions increasingly consider dual-use appeal, blurring the civil-military divide across the firearm sight market.

Geography Analysis

North America’s firearm sight market leadership rests on a blend of expansive defense funding, law-enforcement modernization, and a civilian sports ecosystem that together demanded more than 31% of global revenue in 2025. The XM157 and ENVG-BN programs anchor long-term factory utilization, while civilian demand for pistol red dots ensures continuous volume that smooths production cycles. Canada’s soldier systems modernization and Mexico’s border-security upgrades add incremental demand and sustain cross-border optics supply chains. Export controls tighten operating latitude, but domestic consumption still absorbs most output, cushioning manufacturers against external shocks.

Asia-Pacific is the growth engine, expanding at a 4.36% CAGR on record defense allocations such as India’s projected USD 415.90 billion budget and Japan’s bulk orders for Type 20 rifles with Aimpoint COMP M5 sights. Australia’s HIMARS and infantry-weapons packages incorporate optics from US and local vendors, reinforcing regional demand diversity. ASEAN nations, spurred by maritime disputes, procure modular carbines pre-drilled for reflex or magnified optics, widening install bases. Civilian shooting clubs in Thailand and the Philippines grow membership, adding small but resilient retail channels.

Europe maintains steady momentum tied to NATO initiatives and intensive hunting traditions. The UK’s USD 152 million Talon thermal program and Germany’s upcoming rifle replacement ensure defense visibility, while brands like ZEISS pivot toward digital growth even as they shutter historic glass plants. Eastern European states accelerate procurement amid security concerns, buying mid-price optics that marry durability with lower cost. Civil adoption stays robust in Scandinavia, where night-hunting permissions elevate demand for thermal clip-ons. Collectively, these factors retain Europe’s high value-per-unit standing in the firearm sight market.

Competitive Landscape

The firearm sight market is moderately concentrated, with a cohort of legacy optical specialists vying against electronics integrators that package sensors, AI, and comms in one optic. Vortex’s USD 2.7 billion US Army win underscores how digital prowess can leapfrog entrenched glass pedigree, spurring incumbents to acquire firmware talent or license algorithms. Aimpoint deepens pistol partnerships to capture the red-dot boom, while EOTECH capitalizes on holographic patents to diversify into magnifiers and thermal hybrids. Chinese entrants leverage domestic semiconductor capacity and challenge price tiers but face export-license headwinds that crimp penetration in NATO markets.

Supply-chain resilience has emerged as a board-level metric; the UK’s nationalization of a GaAs fab highlights government intervention where defense optics are deemed strategic.[4]UK Government, “UK Government Buys Coherent’s Newton Aycliffe Fab to Secure Defence Supply Chain,” Semiconductortoday.com, semiconductortoday.com Firms explore vertical moves into wafer-level optics or battery tech to insulate against geopolitical tremors. Cooperative R&D alliances between firearms OEMs and optic houses, such as the Glock-Aimpoint COA package, illustrate a pivot toward factory-bundled offerings that simplify end-user procurement and lock in ecosystem preferences. Patent races in AR overlays and cloud-connected ballistics hint at a future where software subscription models accompany hardware, recasting revenue streams within the firearm sight market.

Firearm Sight Industry Leaders

Bushnell (Revelyst, Inc.)

Leonardo DRS, Inc.

Beretta Holding S.A.

Aimpoint AB

SIG SAUER, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Leonardo DRS, Inc. received a USD 117 million order to continue producing next-generation thermal weapon sights for the US Army. The order falls under the Indefinite Delivery/Indefinite Quantity (IDIQ) contract for the Family of Weapon Sights – Individual (FWS-I) program.

- July 2024: Teledyne FLIR received a USD 15-million contract from the US Army to supply weapon sights to a NATO partner.

Global Firearm Sight Market Report Scope

Firearm sights, also known as gunsights, are optical devices that aid in the aiming of a firearm. They are mainly used to assist in the precise visual alignment of ranged weapons with the intended target.

The firearm sight market is segmented into sight type, weapon type, end user, and geography. By sight type, the market is segmented into iron or open sights, peep sights, telescopic sights, reflex sights, laser sights, and dot sights. By weapon type, the market is segmented into pistols, assault rifles, and sniper rifles. By end-user, the market is segmented into hunting, law enforcement, and military. The report also covers the market sizes and forecasts for the firearm sight market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Iron Sights |

| Peep Sights |

| Telescopic Sights |

| Reflex Sights |

| Laser Sights |

| Dot Sights |

| Optical |

| Digital/Smart (AR-enabled) |

| Thermal Imaging |

| Night-Vision Enhanced |

| Pistols |

| Assault Rifles |

| Sniper Rifles |

| Military |

| Law Enforcement |

| Hunting and Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Sight Type | Iron Sights | ||

| Peep Sights | |||

| Telescopic Sights | |||

| Reflex Sights | |||

| Laser Sights | |||

| Dot Sights | |||

| By Technology | Optical | ||

| Digital/Smart (AR-enabled) | |||

| Thermal Imaging | |||

| Night-Vision Enhanced | |||

| By Weapon Type | Pistols | ||

| Assault Rifles | |||

| Sniper Rifles | |||

| By End User | Military | ||

| Law Enforcement | |||

| Hunting and Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the firearm sight market and its expected size by 2031?

The firearm sight market size is USD 2.37 billion in 2026 and is projected to reach USD 2.82 billion by 2031.

Which sight type holds the largest share of global demand?

Telescopic optics led with 62.02% of firearm sight market share in 2025, reflecting their versatility across user groups.

Which region is growing fastest for firearm sights between 2025 and 2031?

Asia-Pacific is forecasted to expand at a 4.36% CAGR on the back of extensive military modernization programs between 2026 and 2031.

Why are red-dot sights gaining traction in policing?

Field studies show higher qualification scores and faster target acquisition, convincing agencies to authorize slide-mounted optics for duty pistols.

How are supply-chain risks influencing competitive strategy?

Restrictions on gallium and germanium drive up costs and lead times, prompting leading optics brands to secure vertical chip capacity or partner with domestic fabs.

What technological feature is shaping next-generation weapon sights?

Augmented-reality (AR) overlays that link optic reticles to networked sensors are becoming standard, turning sights into integrated information hubs.

Page last updated on: