Light Weapons Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.26 Billion |

| Market Size (2031) | USD 20.64 Billion |

| Growth Rate (2026 - 2031) | 4.89% CAGR |

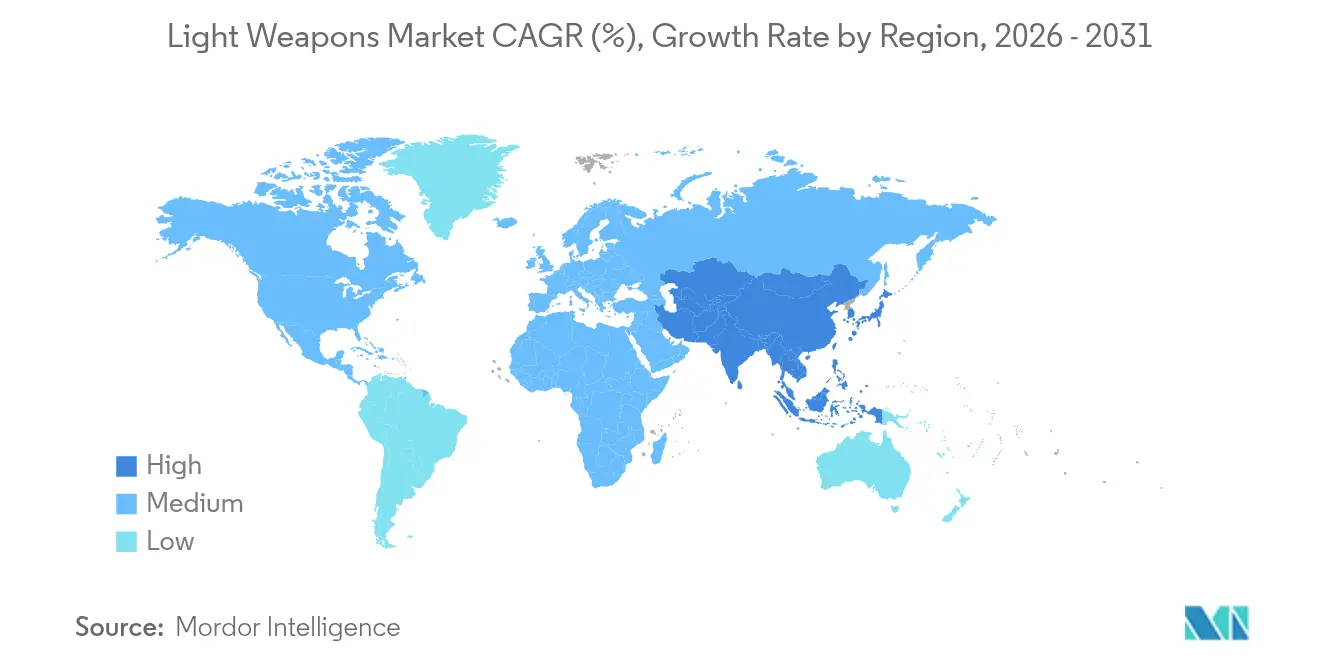

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

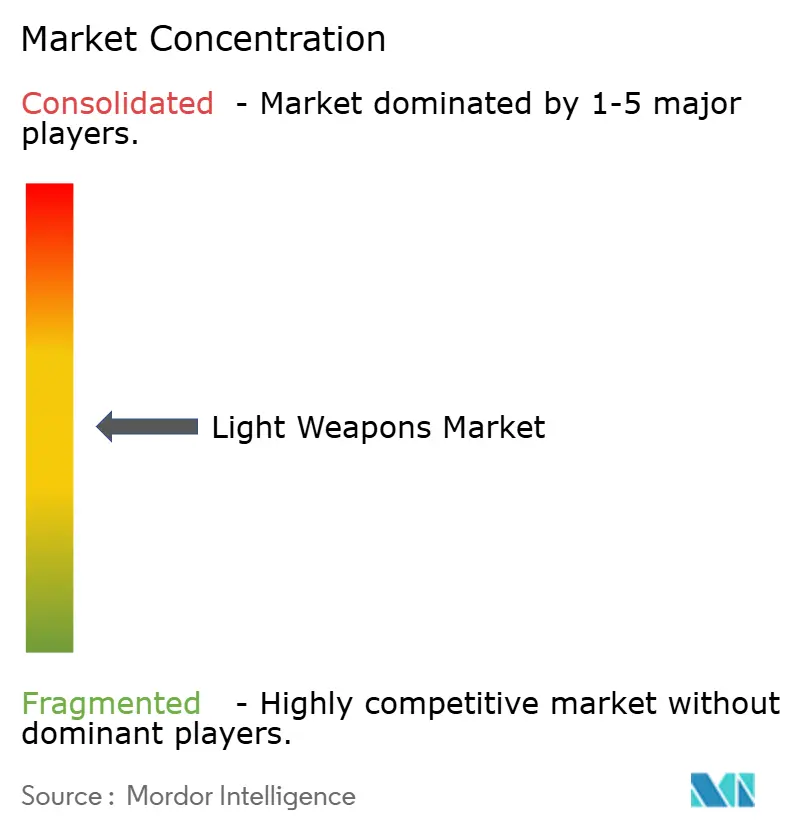

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Light Weapons Market Analysis by Mordor Intelligence

The light weapons market size was valued at USD 15.50 billion in 2025 and estimated to grow from USD 16.26 billion in 2026 to reach USD 20.64 billion by 2031, at a CAGR of 4.89% during the forecast period (2026-2031). This steady advance stems from defense-budget expansion in response to heightened geopolitical risk, with global military expenditure rising 9.4% to USD 2.718 trillion in 2024. Procurement priorities concentrate on man-portable precision systems, while naval close-in programs and polymer-composite ammunition illustrate parallel modernization currents. Technology convergence—especially AI-enabled fire-control modules—allows armed forces to upgrade legacy inventories at a lower cost than wholesale fleet replacement. Vendor competition remains moderate: established contractors guard incumbency through scale and compliance expertise, yet niche innovators exploit software-centric differentiation. Raw-material price volatility and tightening arms-export rules temper growth but outweigh the demand pull created by escalating regional flashpoints.

Key Report Takeaways

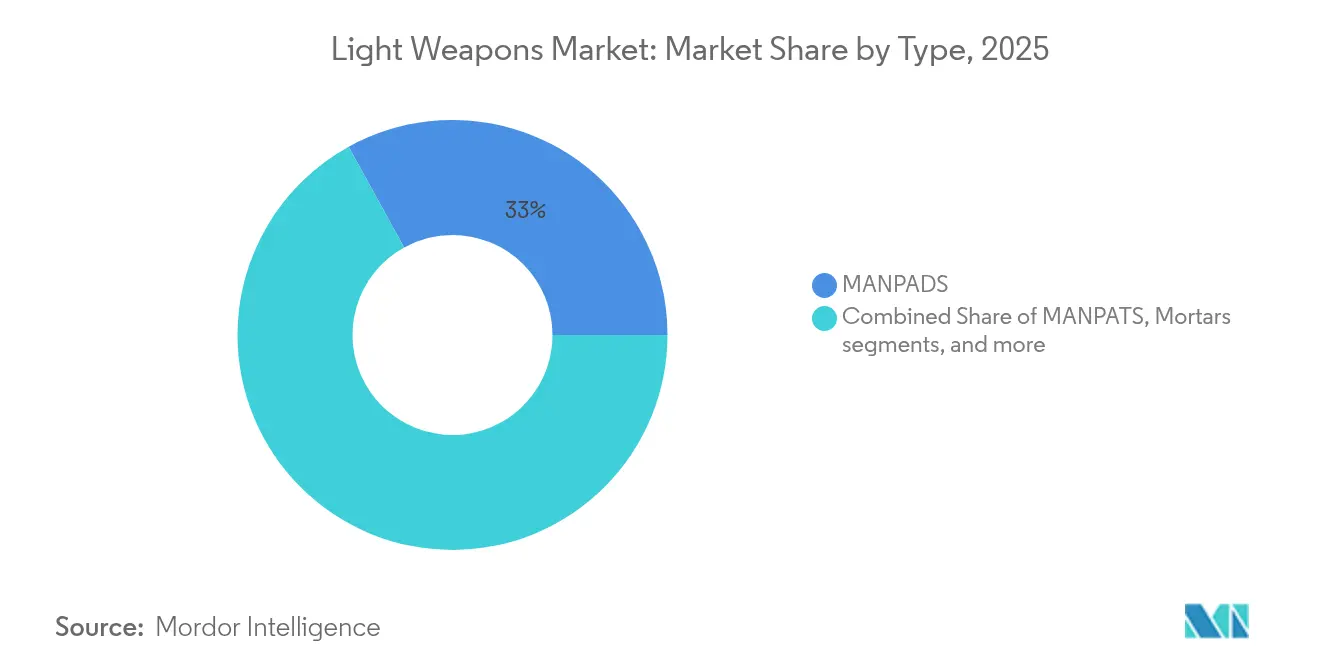

- By type, MANPADS held 33.02% of the light weapons market share in 2025; grenades and grenade launchers are set to expand at 8.74% CAGR to 2031.

- By technology, guided systems led with a 55.12% revenue share in 2025 and are projected to grow at a 7.28% CAGR through 2031.

- By platform, land applications dominated with a 60.55% share in 2025, while naval platforms are forecasted to post a 6.43% CAGR through 2031.

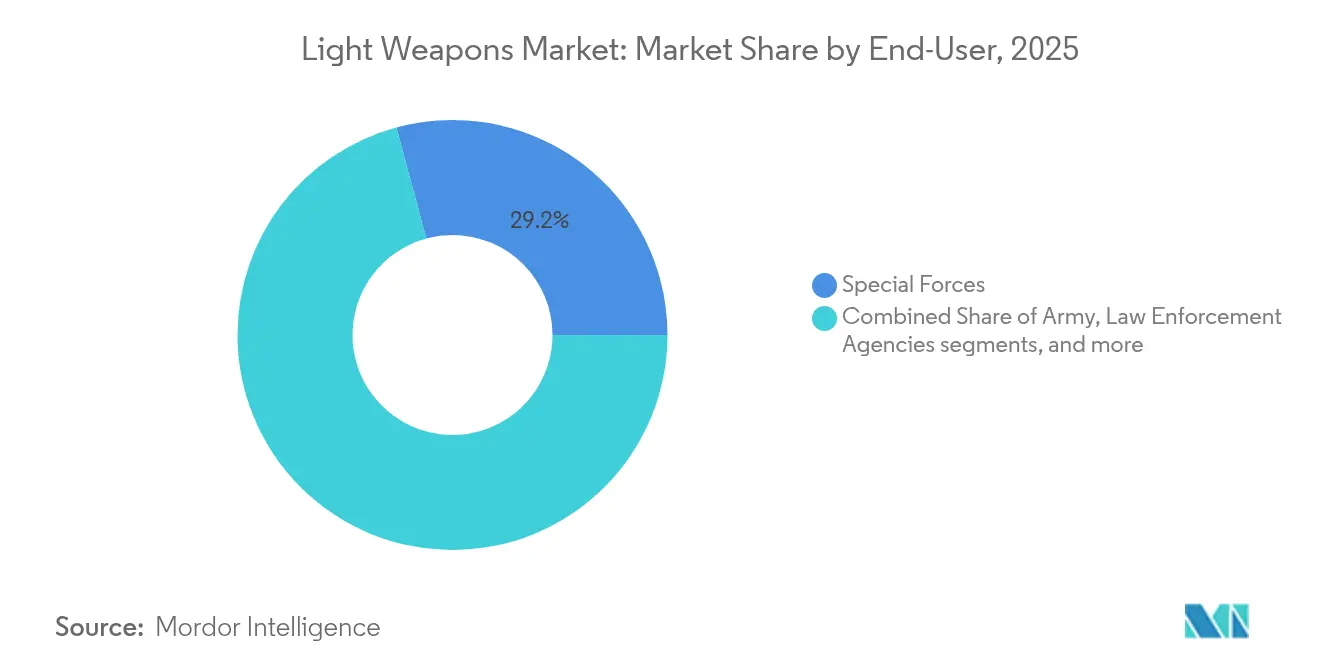

- By end-user, special forces commanded 29.21% of 2025 revenues; the army segment is on track for the fastest 9.32% CAGR up to 2031.

- By material, the aluminum and light-metal alloys segment held 29.92% share in 2025, and the polymer composites segment is expected to grow at the fastest rate of 5.36% CAGR up to 2031.

- By geography, North America accounted for 38.33% of 2025 revenue, whereas Asia-Pacific is expected to compound at 7.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Light Weapons Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating defense budgets amid geopolitical tensions | +1.8% | Europe and Middle East focused, global spill-over | Medium term (2-4 years) |

| Proliferation of asymmetric warfare driving demand for man-portable systems | +1.2% | Asia-Pacific core, widening to MEA | Long term (≥ 4 years) |

| Modernization of infantry units with lightweight modular weaponry | +0.9% | North America and EU, extending to APAC | Medium term (2-4 years) |

| Rising counter-terror operations and urban warfare requirements | +0.7% | Middle East and South Asia first, global later | Short term (≤ 2 years) |

| Integration of AI-enabled fire-control modules into legacy light weapons | +0.6% | North America and EU, allied transfers | Long term (≥ 4 years) |

| Emergence of polymer-cased ammunition reducing soldier load | +0.4% | Early adoption in advanced militaries, global uptake | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Defense Budgets Amid Geopolitical Tensions

European military outlays climbed 17% to USD 693 billion in 2024 as NATO states reacted to Russia’s invasion of Ukraine.[1]Stockholm International Peace Research Institute, “Trends in World Military Expenditure 2024,” sipri.org Poland will raise defense spending to 4.7% of GDP by 2025, while Germany’s EUR 100 billion (USD 109 billion) special fund underlines long-term commitment. The European Union's ReArm Europe proposal aims to mobilize EUR 800 billion (USD 870 billion), which includes EUR 150 billion (USD 163 billion) in joint-procurement loans.[2]European Parliament, “ReArm Europe Initiative Explained,” europarl.europa.eu This initiative has led to significant infantry weapon orders, such as Germany's EUR 8.5 billion (USD 9.2 billion) ammunition contract with Rheinmetall, strengthening the demand in the light weapons market.

Proliferation of Asymmetric Warfare Driving Demand for Man-Portable Systems

Ukraine’s battlefield experience shows how man-portable missiles blunt heavier forces, prompting regional actors to stockpile similar assets; European arms imports doubled in 2019-2023 versus 2014-2018.[3]Al Jazeera, “European Arms Imports Double Amid Ukraine War,” aljazeera.com Taiwan’s purchase of Switchblade 300 loitering munitions worth USD 360.2 million highlights Asia-Pacific uptake. Smart-rifle scopes such as the SMASH 2000L, fielded under a USD 13 million US Army program, illustrate counter-drone. Asymmetric doctrine thus sustains multi-role, low-footprint products within the light weapons market.

Modernization of Infantry Units with Lightweight Modular Weaponry

Japan began replacing Type 89 rifles in 2024 with 5.56 mm Type 20 models under a JPY 3.3 billion (USD 22.82 million) contract for 8,577 units. The UK’s Project Troubler seeks machine guns below 7.1 kg, and FN Herstal’s 5.5 kg Evolys meets that bar. Israel’s Arbel electronic firing system triples accuracy without new platforms. Weight-saving prototypes such as STV Group’s Archon Type L ultra-light LMG reinforce soldier-mobility priorities that are pervasive in the light weapons industry.

Rising Counter-Terror Operations and Urban Warfare Requirements

Drone-centred urban threats drive fresh procurement. The US Marine Corps will field counter-UAS kits service-wide in 2025. UK demonstrators defeated drone swarms with directed-energy weapons during 2024 trials. Israel’s Ten AI Weapon System detects targets at 700 m with 40x optical zoom for border security. Precision, discrimination, and multi-sensor fusion, therefore, underpin urban-warfare offerings inside the light weapons market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent international arms-transfer regulations | -0.8% | Global, intense on cross-border sales | Long term (≥ 4 years) |

| Volatile raw-material prices for specialty alloys and electronics | -0.6% | Worldwide, sharper in supply-constrained regions | Short term (≤ 2 years) |

| Battlefield shift toward loitering munitions curbing MANPATS demand | -0.4% | First in advanced militaries, global diffusion | Medium term (2-4 years) |

| Environmental and health concerns over legacy propellants | -0.3% | EU and North America lead, global echo | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent International Arms-Transfer Regulations

The US Commerce Department imposed tighter firearms-export rules in May 2024, presuming denial for many commercial deals. Washington’s revised Conventional Arms Transfer policy blocks shipments likely to enable rights abuses. The Arms Trade Treaty, now at 113 parties, mandates prior risk assessments.[4]United Nations, “Arms Trade Treaty Status,” un.orgThe UK’s 2024 Export Control amendment added emerging-tech coverage. Compliance overhead and license uncertainty curb smaller exporters’ access to the light weapons market.

Volatile Raw-Material Prices for Specialty Alloys and Electronics

Chinese export curbs on gallium and germanium heighten semiconductor-supply risk for guidance kits. Defense buyers estimate tariff-linked cost headwinds at USD 850 million per year. The US Defense Logistics Agency’s supplier base shrank to 8,500 firms, raising concentration risk. Such price swings compress program margins and complicate bidding across the light weapons market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: MANPADS Dominance Amid Guided-System Evolution

MANPADS generated 33.02% of 2025 revenue, the highest individual slice of the light weapons market size, reflecting broad procurement of Stinger-class missiles by Taiwan and Eastern European allies. Although loitering drones threaten substitution, established logistics chains and immediate availability keep demand resilient. Heavy machine guns and mortars retain niche relevance through service-life extension contracts, while counter-drone rifles form a fledgling but important category.

Grenades and grenade launchers delivered the fastest 8.74% CAGR outlook. Programmable air-burst rounds and precision launchers, such as the Mk 47 acquired by Colt CZ, illustrate value migration toward guided sub-munitions. Urban warfare doctrines and policing requirements underpin dual-use sales. Together, these trends ensure product-mix diversification inside the light weapons market.

By Technology: Guided Systems Drive Precision Revolution

Guided munitions commanded 55.12% revenue in 2025 and will outpace other technologies at 7.28% CAGR, underlining their mass in the light weapons market share hierarchy. Beam-riding laser models and IR fire-and-forget missiles reduce operator exposure and meet collateral-damage thresholds, as evidenced by Thales’ Lightweight Multi-role Missile trials.

Unguided systems persist due to their price advantage and resilience against jamming. Budget-constrained forces stockpile inexpensive rounds to ensure supply sufficiency. As electronic warfare (EW) threats expand, dual inventories—smart and dumb—provide hedge flexibility, securing a stable niche for unguided products within the light weapons industry.

By Platform: Naval Growth Accelerates Amid Maritime Tensions

Land platforms still comprised 60.55% of 2025 spending, yet naval applications will capture the highest 6.43% CAGR. The US Navy’s SeaRAM retrofit on Arleigh Burke destroyers demonstrates demand for extended-reach point defense. South Korea’s 4,200-rpm CIWS-II, due in 2026, shows similar requirements. As Indo-Pacific maritime competition intensifies, ship-borne quick-reaction guns and missiles attract fresh investment, expanding the light weapons market size for sea-based solutions.

Air-platform integration remains steady; helicopters and drones mount lightweight missiles for precision strikes. Modularity allows single-seeker architectures to span land, sea, and airframes, giving suppliers cross-platform revenue leverage.

By End-User: Special Forces Lead While Army Segment Accelerates

Special Forces units accounted for 29.21% of the 2025 demand thanks to premium gear cycles and rapid tech adoption. They remain early customers for polymer cases, advanced optics, and smart launchers, cementing their influence on design roadmaps.

Conventional armies will, however, post the fastest 9.32% CAGR to 2031 as mass modernization unfolds. Poland’s doubling of troop strength exemplifies volume procurement. NATO orchestration of common requirements accelerates bulk orders, pushing overall light weapons market growth into high gear over the forecast horizon.

By Material: Polymer Innovation Drives Weight Reduction

Aluminum-alloy assemblies delivered 29.92% of 2025 turnover, but polymer composites will enjoy a 5.36% CAGR, the strongest advance among materials. Favorable strength-to-weight ratios enable longer missions with unchanged carry loads. Ceramic-hybrid solutions promise additional ballistic resilience, encouraging incremental adoption that should maintain healthy momentum within the light weapons market.

Geography Analysis

North America led the market with 38.33% revenue in 2025, anchored by the United States’ USD 997 billion defense budget. Robust domestic orders underpin economies of scale, while Foreign Military Sales extend reach into allied fleets. Lockheed Martin’s Missiles and Fire Control sales climbed 13% to USD 3.37 billion in Q1 2025 as backlog visibility improved.

Asia-Pacific's light weapons market size is projected to grow at a 7.53% CAGR through 2031, the fastest regional rate. India’s 20% compound defense-capital growth through FY24-FY29 sustains local sourcing mandates covering 65% of contracts. The Philippines earmarked USD 35 billion under Re-Horizon 3, while Japan’s 21% budget hike marks the largest since 1952. Rising China-related security anxiety fuels multi-country rearmament, giving suppliers an expansive pipeline.

Europe’s surge in military spending—up 17% year-on-year to USD 693 billion—creates the most immediate procurement spike. Germany’s EUR 100 billion (USD 109 billion) fund, Poland’s 4.7% of GDP target, and the EU’s ReArm proposal underpin a broad, multi-year refresh of infantry weapons. Joint programs such as the UK-Germany deep-strike missile demonstrate intra-European industrial cohesion, boosting the regional light weapons market.

Regulatory Landscape

International governance for small arms and light weapons is anchored by the UN Programme of Action (PoA) and the International Tracing Instrument (ITI). Together, they shape national licensing, marking, record-keeping, and cooperation practices that affect exportable light-weapon systems and associated components. In 2026, the PoA Open-ended Technical Expert Group (OETEG) convened discussions on technology-enabled risk areas including polymer frames, modular designs, 3D printing, and anti-diversion tools, showing how compliance expectations are extending beyond complete weapons to components and manufacturing methods.

In the United States, export-control administration and definitions remain a major gatekeeper for global suppliers. The BIS rule effective May 2024 tightened licensing for certain firearms and crime control items under the Export Administration Regulations (including controls that reference ECCN categories such as 0A501 and 0A509). A May 2026 Federal Register action then updated conforming references between the Department of State and the Department of Commerce in export control reform. Parallel efforts such as UNODA MOSAIC modules and ongoing policy activity around Arms Export Control Act component definitions point to a shift toward more granular component-level control and stronger traceability expectations for cross-border sales.

Value Chain Analysis

The light weapons value chain runs from raw inputs (specialty steels and light alloys, polymers and composites, energetics, propellants, optics and sensors, and semiconductors for guidance and fire-control) through precision machining, forging or casting, barrel and receiver manufacturing, electronics integration, final assembly, and qualification or testing. OEMs and prime integrators then deliver through direct defense procurement, foreign military sales channels, and long-term support contracts covering spares, training, and lifecycle upgrades such as optics, laser modules, and software-enabled fire-control.

As guided and AI-enabled subsystems take a larger share, secure electronics sourcing, calibration, and cyber-assurance become more significant alongside metallurgical and energetics competence. Supply availability and qualification of sub-tier producers remain constraints, particularly in energetics and metal parts, where single-source dependencies and long lead times can delay output. US government actions during 2026 show how buyers are responding with industrial-base interventions and procurement structures: the US Army Contracting Command issued solicitation W519TC25R0034 to qualify a second-source supplier for 5.56 mm, 7.62 mm, and .50 caliber ammunition for FY26-31, and the Department of Defense completed establishment of the Joint Energetics Transition Office (JETO) to steer energetics modernization. These steps reinforce a move toward multi-year frameworks, second-sourcing, and capacity enablement at the sub-tier level rather than relying only on prime-level throughput.

Competitive Landscape

Market power is shared among a dozen diversified primes and a larger cohort of mid-specialists. RTX Corporation, Lockheed Martin Corporation, Northrop Grumman Corporation, and BAE Systems plc dominate guided-systems intellectual property and maintain turnkey integration capacity. Rheinmetall’s USD 950 million acquisition of Loc Performance widens its US foothold, targeting the XM30 infantry-vehicle project. BAE’s USD 5.5 billion deal for Ball Aerospace extends sensor and space synergies.

Concurrently, niche firms such as Smart Shooter, ZeroMark, and FN Herstal gain traction by embedding software-defined accuracy into conventional rifles. Partnerships proliferate: Leonardo and Rheinmetall created a vehicle joint venture to serve Italy’s 1,000-unit armored requirement. Supply-chain geopolitics have spurred localization; Saudi Arabia’s domestic THAAD transporter assembly and Indonesia’s KF-21 fighter order from Türkiye illustrate south-south alliances.

Competitive factors pivot on technology fusion, regulatory compliance, and lifecycle support. The ability to certify AI algorithms, secure export licenses, and integrate eco-friendly propellants will define future winners as the light weapons market gradually tilts toward data-centric value propositions.

Light Weapons Industry Leaders

RTX Corporation

Lockheed Martin Corporation

Saab AB

Rheinmetall AG

FN Herstal, S.A. (FN Browning Group)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven product differentiation is creating whitespace in traceability, modularity governance, and post-delivery cooperation capabilities that can reduce diversion risk while still allowing field upgrades. The 2026 UN PoA OETEG workstream focused on polymer frames, modular design, and 3D printing, together with MOSAIC-based implementation tools, increases demand for manufacturing processes and digital records that support marking, serialization, component tracking, and auditable supply chains. Suppliers that bundle weapons with compliant documentation, integrate record-keeping, and provide inspection-ready lifecycle support have an advantage in cross-border competitions where export licensing and end-use scrutiny are decisive.

Procurement evidence also points to opportunities linked to standardization of dismounted-soldier enablers and European framework buying. Rheinmetall winning additional Bundeswehr orders for LLM-VarioRay laser light modules (with deliveries extending to 2032) highlights demand for scalable night-fighting and target-acquisition upgrades that can be retrofitted across rifle fleets without replacing core weapons. France placing an order with Saab for NLAW anti-tank weapons (deliveries scheduled across 2026-2030) and moving into a Franco-Belgian light-weapons cooperation framework that includes FN EVOLYS-class machine guns underline how multi-year, multi-country procurement mechanisms shape demand. These dynamics leave room for OEMs and subsystem specialists to compete on interoperable accessories, training systems, and upgrade kits aligned to allied requirements, particularly where rapid fielding and common logistics are prioritized.

Recent Industry Developments

- June 2026: Saab signed a contract with France for the supply of NLAW (Next Generation Light Anti-tank Weapon), with deliveries scheduled from 2026 to 2030. The order reinforces European demand for man-portable anti-armor capabilities and supports longer-horizon production planning for missile, trainer, and support-package supply chains.

- May 2026: Rheinmetall was awarded a further major Bundeswehr contract for LLM-VarioRay laser light modules, with deliveries scheduled through 2032. The multiyear procurement strengthens the installed base for soldier-system modernization and drives recurring requirements for optics, batteries, spares, and fleetwide configuration management.

- December 2025: Rheinmetall announced it would supply LLM-VarioRay laser light modules worth several hundred million euros. The scale of the award signaled accelerated investment in dismounted-soldier lethality and helped standardize accessory configurations across new assault-rifle fielding cycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the light weapons market is counted as the global value of man-portable and small crew-served weapon systems and their directly associated guided and unguided munitions that are procured for defense and security use across land, naval, and airborne platforms.

Scope exclusions: Crew-served artillery above 120 mm and fixed vehicle-mounted weapon systems are excluded from the market totals.

Segmentation Overview

- By Type

- Heavy Machine Guns (HMGs)

- Grenades and Grenade Launchers

- Mortars

- Man-portable Anti-tank Systems (MANPATS)

- Man-portable Air-Defense Systems (MANPADS)

- Other Types

- By Technology

- Guided

- Laser Guided

- Infra-red Guided

- Satellite Guided

- Semi-automatic Command to Line of Sight

- Unguided

- Guided

- By Platform

- Land-based

- Airborne

- Naval

- By End-user

- Army

- Special Forces

- Law Enforcement Agencies

- Homeland Security/Paramilitary

- Others

- By Material

- Steel and Specialty Alloys

- Aluminum and Light-Metal Alloys

- Polymer Composites

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- Israel

- UAE

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work set the base structure of the model and helped us pin down what gets included in light weapons versus adjacent categories. We mainly relied on public and official sources such as defense budget documents and procurement releases, UN Comtrade trade statistics for relevant weapon and ammunition codes, SIPRI arms transfer datasets, and publications from NATO and other defense standard bodies.

To avoid sizing off a single viewpoint, we also reviewed company annual reports and investor presentations, government tender portals, and credible defense press for contract timing and platform rollouts. Where it helped to normalize company scale and backlog signals, a paid subscription for company financials and another for global contracts and tenders were used as supporting inputs. The sources listed here are illustrative, and many other references were used to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work was used to confirm what buyers actually procure under light weapons, how programs are phased, and what typically sits outside scope even when it sounds similar on paper. We spoke with manufacturers, component suppliers, distributors, and defense procurement stakeholders across APAC, EMEA, and the Americas, so assumptions on unit demand, upgrade cycles, and pricing could be stress-tested before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 15% | APAC: 49% |

| Mid tier: 42% | Functional/Unit leaders: 30% | EMEA: 29% |

| Smaller Players: 22% | Managers: 55% | Americas: 22% |

Market-Sizing & Forecasting

Market sizing was built using a top-down approach where defense spending, procurement plans, and import-export signals were used to reconstruct demand for light weapon categories by region and platform, and then translated into value using realistic pricing bands. After the demand pool was shaped, we ran sampled bottom-up checks using selective supplier roll-ups and channel checks (for example, program-level unit quantities multiplied by typical average selling prices) to confirm the totals stayed within a sensible range.

Key inputs that were tracked include infantry modernization program cadence, announced tender volumes, unit mix across categories like heavy machine guns, mortars under 120 mm, grenade launchers, and man-portable air-defense and anti-armor systems, along with observed price progression for new-build versus upgrade and retrofit orders. When public data was thin for a country or year, gaps were handled by using proxy indicators such as neighboring procurement patterns, historical replacement cycles, and trade flows, followed by an interview-led sanity check.

Forecasts were produced using scenario analysis, since procurement often moves in steps instead of smooth lines, and scenario weights were adjusted using what experts shared on budget certainty, delivery lead times, and expected contract timing. The final curve was then aligned to known program start dates and typical delivery schedules so year-to-year movement stayed realistic.

Data Validation & Update Cycle

Outputs were validated through multiple checks so outliers did not slip through. Regional totals were compared against independent signals such as major contract announcements, shifts in defense budgets, and trade movement direction, and then reviewed again when pricing or volume appeared inconsistent with program realities.

Before sign-off, assumptions and calculations are reviewed in steps by another analyst, and we re-contact interviewees when a material mismatch appears between modeled demand and what is being procured in the field. The report is refreshed annually, and interim updates are made when major conflicts, policy changes, or procurement shocks materially alter expected demand. Right before delivery, a final pass is performed so clients receive the most current view available.

Mordor Intelligence's Global Light Weapons Market Market Estimate Compared With Other Published Estimates

Published market sizes for light weapons often differ because the product scope, pricing basis, and the timing of procurement recognition are not treated the same way across studies. Differences show up quickly when one estimate leans more on manufacturer revenues, while another is closer to defense procurement and delivery patterns.

The main gap comes from whether artillery-class systems and fixed vehicle-mounted weapons are folded into the same bucket, where Mordor Intelligence counts only man-portable and small crew-served systems (with mortars kept below 120 mm) and excludes the heavier mounted categories that can inflate totals. Some publishers also use factory-gate revenue and include related services, while others apply higher long-range price escalation or extend the definition toward small arms and accessories, which changes the value base and the growth curve.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.26 B (2026) | |

| Global Consultancy A | USD 16.46 B (2025) | Uses a different base year and a broader basket that explicitly includes items like landmines and some categories described as mounted systems, and it also applies a longer forecast window that can amplify compounded growth assumptions. |

| Industry Publisher B | USD 14.12 B (2025) | Built around factory-gate manufacturer revenues and includes related services, which can understate procurement-led totals in years with large government deliveries, and it can also shift value depending on what is treated as a service versus a weapon sale. |

The spread in the table is mainly explained by scope choices, base-year timing, and whether the value is tied to procurement demand signals or to manufacturer revenue definitions. By keeping inclusions clear and checking totals against program activity, budgets, and trade movement, the final number remains traceable to practical inputs that can be rechecked each update cycle.

Key Questions Answered in the Report

How large is the light weapons market in 2026?

The light weapons market size stood at USD 16.26 billion in 2026.

What is the expected CAGR for the light weapons market to 2031?

Revenue is projected to grow at 4.89% per year through 2031.

Which region will expand fastest?

Asia-Pacific is forecasted to record the quickest 7.53% CAGR owing to rising defense outlays.

What technology segment holds the largest market share?

Guided systems accounted for 55.12% of 2025 revenue and maintain the highest growth rate.

How will polymer-cased ammunition influence future demand?

Polymer rounds reduce soldier load by up to 30%, supporting a 5.36% CAGR for composite materials and encouraging broader adoption.

Which restraint poses the greatest long-term threat?

Stricter international arms-transfer regulations, with a -0.8% impact on forecasted CAGR, present the most significant structural headwind.

Page last updated on: