Military Fiber Optic Cables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.09 Billion |

| Market Size (2031) | USD 5.77 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Military Fiber Optic Cables Market Analysis by Mordor Intelligence

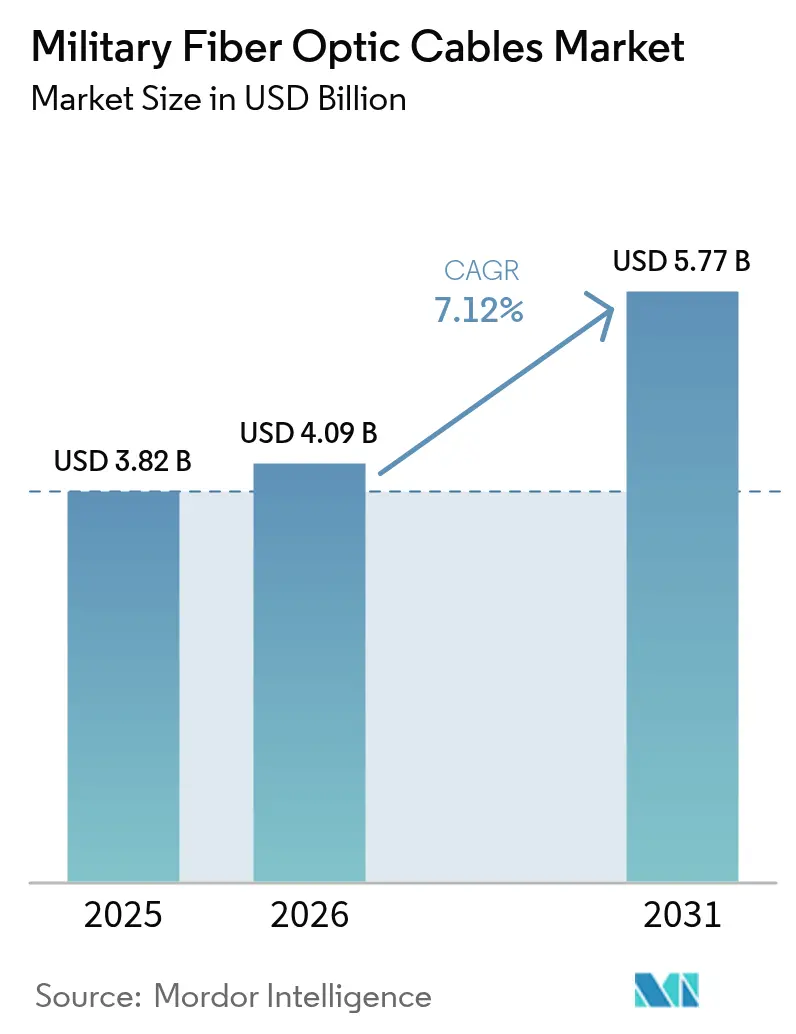

military fiber optic cables market size in 2026 is estimated at USD 4.09 billion, growing from 2025 value of USD 3.82 billion with 2031 projections showing USD 5.77 billion, growing at 7.12% CAGR over 2026-2031. Growth reflects the swift replacement of copper links with fiber solutions that withstand electromagnetic interference while carrying far higher data loads. Investments in fiber-optic drones, directed-energy weapons, and 5G-enabled tactical networks are reshaping battlefield connectivity, prompting armies to refit legacy platforms with high-bandwidth optical backbones. Defense ministries also view fiber as a hedge against jamming and cyber risks, since light-based signals resist interception and radiate no electromagnetic signature. Procurement spending is further supported by multi-domain sensor fusion programs that push data rates above 100 Gbps on ships, vehicles, and aircraft.

Key Report Takeaways

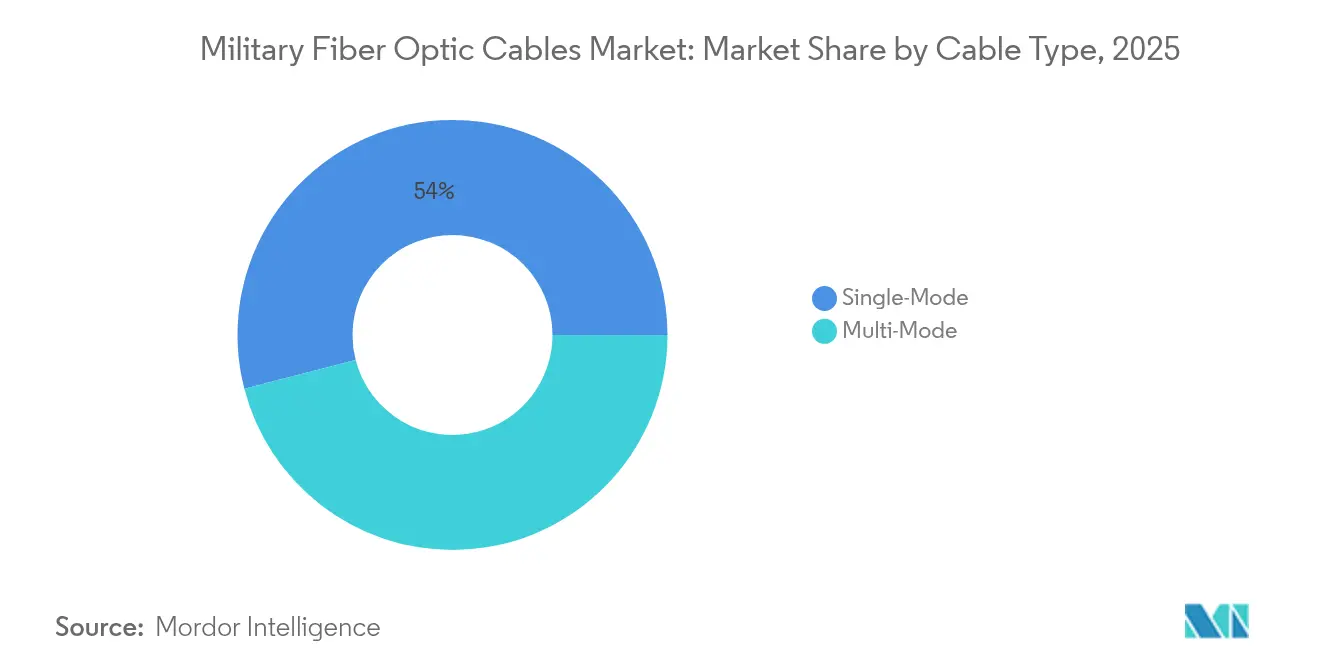

- By cable type, single-mode fiber led with 54.02% of the military fiber optic cables market share in 2025; multi-mode is forecasted to grow at an 8.43% CAGR through 2031.

- By material, glass fiber accounted for 90.10% share of the military fiber optic cables market size in 2025, while plastics show a 10.02% CAGR outlook to 2031.

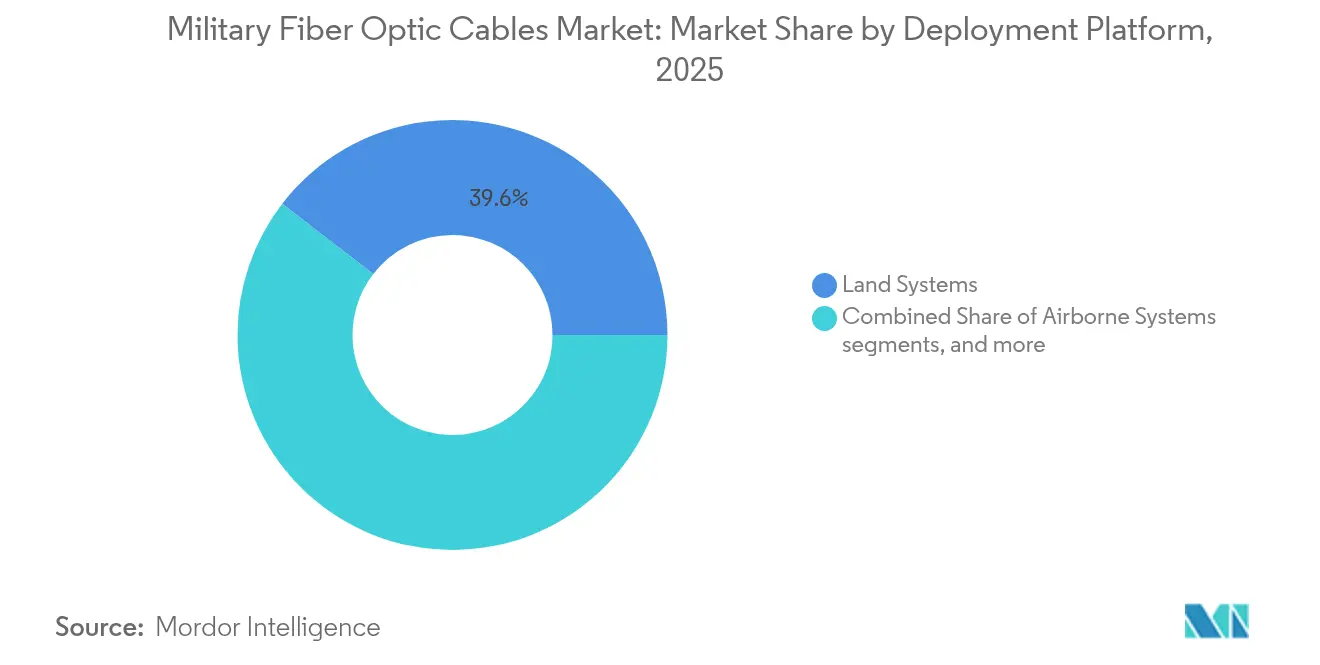

- By deployment platform, land systems captured 39.55% of 2025 revenue; naval and sub-sea assets are set to advance at a 10.01% CAGR to 2031.

- By installation environment, harsh-environment armored cables held a 42.10% share in 2025; underwater installations are projected to expand at a 9.76% CAGR.

- By application, C3ISR represented 42.25% revenue in 2025; directed-energy weapons are advancing at an 11.05% CAGR through 2031.

- By geography, North America commanded 34.10% of 2025 revenue, while Asia-Pacific posts the fastest 9.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Military Fiber Optic Cables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battlefield demand for loss-less, EMI-immune data links | +2.1 | Global, with concentration in active conflict zones and NATO countries | Short term (≤2 yrs) |

| Militarisation of 5G tactical networks | +1.8 | North America, Europe, advanced Asia-Pacific militaries | Medium term (≈3-4 yrs) |

| Surge in ISR sensor density | +1.2 | Global, with emphasis on naval and airborne platforms | Medium term (≈3-4 yrs) |

| Directed-energy weapons integration | +1.9 | North America, advanced Asia-Pacific militaries | Long term (≥5 yrs) |

| Miniaturised rugged fiber terminations | +0.8 | Global, with higher impact in technologically advanced militaries | Medium term (≈3-4 yrs) |

| NATO STANAG shift towards fiber-centric avionics architectures | +1.4 | NATO member countries, with spillover to strategic allies | Medium term (≈3-4 yrs) |

| Source: Mordor Intelligence | |||

Battlefield demand for loss-less, EMI-immune data links

Electronic warfare has saturated modern battlefields, so fiber-optic lines now replace copper to keep signals intact under jamming. Ukrainian forces operate fiber-tethered FPV drones that penetrate 41 km while streaming high-resolution video unaffected by interference. NATO planners observed these results, and the US Army plans 1,100 similar systems to close capability gaps.[1]Todd South, “Army races to field fiber-optic drones after battlefield lessons,” Stars and Stripes, stripes.com These combat-proven accelerators accelerate the procurement of rugged micro-fiber reels and quick-deploy connectors for squads and command posts. The military fiber optic cables market benefits directly as each drone uses multi-kilometre spools and replacement kits that must meet MIL-spec pull and bend limits. Demand is reinforced by national mandates to harden forward bases against electronic attack.

Militarisation of 5G tactical networks

Private 5G roll-outs at bases in the United States, Spain, Germany, and Norway depend on dense fiber backhaul that handles multi-gigabit traffic while meeting strict latency and security targets. Spending on defence 5G infrastructure will total USD 1.5 billion during 2024-2027, with roughly one-third flowing to optical cabling and terminations. Programs adopt Open RAN interfaces, so suppliers must certify fibers for diverse radio units and edge clouds. The military fiber optic cables market thus gains sustained orders for single-mode trunk lines, field-deployable indoor/outdoor patch cords, and hardened MPO connectors able to survive fuel spills and vehicle loads.

Surge in ISR sensor density

Modern destroyers, fighters, and armored vehicles now host dozens of cameras, lidars, and passive RF arrays that create multi-terabyte data streams. The US Navy replaced legacy copper on AEGIS cruisers with ship-wide fiber rings after proving they survive vibration, flooding, and shock.[2]SPIE Authors, “Fiber optics for naval shipboard systems,” SPIE Digital Library, spiedigitallibrary.org Each hull requires thousands of fiber terminations and watertight penetrators, creating a sizeable retrofit market. Similar upgrades appear on airborne early-warning aircraft and wide-area persistent-surveillance drones. As sensor counts rise, operators adopt 100 Gbps Ethernet over OM4 fiber to avoid bottlenecks. The military fiber optic cables market responds with bend-insensitive cores and low-smoke, zero-halogen jackets that comply with naval fire codes.

Directed-energy weapons integration

Fiber lasers stand out for shipborne and ground-based high-energy systems because they deliver excellent beam quality and 40%-plus wall-plug efficiency. Researchers demonstrated coherent beam combining that scales to 100 kW output, paving the way for drone and missile defence modules. These weapons drive demand for specialty fibers doped with erbium or ytterbium, tight-tolerance cleaves, and high-photon-flux connectors. Program offices specify fibers resistant to photodarkening and capable of moving hundreds of watts through small cores without thermal runaway. Suppliers that master these qualifications capture premium margins within the military fiber optic cables market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Field-level repair complexity | -0.9% | Global, remote deployments | Short term (≤ 2 years) |

| Supply chain security vulnerabilities | -1.5% | North America, Europe | Medium term (2-4 years) |

| High lifecycle cost vs copper | -0.5 | Emerging markets and budget-constrained militaries | Short term (≤2 yrs) |

| Vulnerability to bend-loss | -0.4 | Global, with emphasis on land-based armored vehicles | Short term (≤2 yrs) |

| Source: Mordor Intelligence | |||

Field-level repair complexity

Splicing fibers in remote combat zones is labour-intensive and tool-heavy, so cut lines can idle critical sensors. Military trials “crimp & cleave” connectors that install in under three minutes, trading 0.5 dB extra loss for rapid restoration. Training backlogs persist, and shortages of certified technicians slow large-scale roll-outs. Vendors answer with pre-terminated reels and colour-coded boots that reduce human error. While these advances ease the issue, the military fiber optic cables market still faces delayed contracts until armies field enough maintenance teams.

Supply chain security vulnerabilities

Rare-earth doped preforms and radiation-hardened fibers fall under ITAR controls that complicate global sourcing.[3]Army Acquisition Directorate, “Securing the optical supply chain,” army.mil Geopolitical tensions heighten scrutiny of suppliers, leading to dual-sourcing strategies and higher certification costs. Researchers also warned that adversaries can tamper with optical timing links over hundreds of kilometres, altering frequency references without detection.[4]arXiv Authors, “Stealth tampering of fibre frequency links,” arxiv.org Procurement agencies now request provenance audits and tamper-evident seals, adding time and expense. These hurdles trim forecast growth for the military fiber optic cables market during the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By cable type – Single-mode fibers anchor long-haul missions

Single-mode lines command the largest military fiber optic cables market share at roughly 54.02% in 2025 and are forecast to maintain a mid-single-digit CAGR through 2031. Their narrow core enables ultra-long links on destroyers, airborne early warning aircraft, and underground fiber trunks interconnecting forward operating bases. A useful consequence is that each single-mode run often carries spare dark fibers, creating latent capacity that future-proofs the investment.

Second, multi-mode occupies a smaller slice today, yet is predicted to outpace overall market growth with an 8.43% CAGR. Cost-effective transceivers, tolerance of wider launch conditions, and recent breakthroughs in radiation-hard multimode fiber suggest wider deployment inside armored vehicles and aircraft cabins. This uptick implies that vendors offering hybrid cable bundles—combining both core types—gain a commercial edge by simplifying logistics for integrators.

By material – Glass fibers remain dominant

Glass commands about 90.10% of the military fiber optic cables market, thanks to its unmatched bandwidth and robustness. Naval architects favour glass for topside and below-decks runs because its thermal window aligns with maritime shock standards. The inferred benefit for suppliers is volume stability: fleet refit cycles assure ongoing demand independent of new-build schedules.

Plastic optical fiber (POF) may hold less than a tenth of the market value, but it is advancing at roughly 10.02% CAGR owing to flexibility and quick field termination. Embedded wear sensors in bearings and hatch seals illustrate niche yet recurring orders. POF’s progress suggests that a diversified materials portfolio gives contractors a hedge against glass-specific geopolitical supply risks.

By deployment platform – Land systems dominate through sheer volume

Land systems account for an estimated 39.55% share of the military fiber optic cables market size in 2025. Army digitisation projects swap copper harnesses for lighter, interference-free fiber, shaving kilograms from weight-constrained vehicles. A direct implication is that every kilogram saved can be re-allocated to armor or battery capacity, reinforcing the preference for optical links.

Naval and subsea platforms are forecast to log the fastest CAGR of 10.01% between 2026 and 2031. Rising concern over seabed-based infrastructure protection triggers investments in hardened undersea cables and autonomous monitoring nodes. Consequently, shipyards increasingly specify armored optical cables at keel-laying rather than the retrofit stage, anchoring future growth.

By installation environment – Armored designs lead sales

Harsh-environment armored cables now hold roughly 42.10% of the military fiber optic cables market share. High-density braid jackets, crush-resistant buffers, and low-smoke coatings enable reliable performance in exploding-wire test rigs and arctic deployments. The practical upshot is that lessons learned here spill into civilian disaster-relief kits, broadening the addressable market for the same rugged designs.

Underwater and submarine installations are projected to notch the highest CAGR, nudging 9.76% through 2031. Long-haul seabed links sustain autonomous sensor nets that flag unauthorised vessel activity. This surge implies that anti-tamper enclosures and real-time integrity-monitoring fibers will emerge as must-have accessories, adding incremental revenue streams for established cable manufacturers.

By application – C3ISR forms the backbone

C3ISR represents roughly 42.25% of the military fiber optic cables market. Network architects value fiber's immunity and capacity when fusing radar, SIGINT, and hyperspectral camera inputs. The immediate corollary is that optical-first design principles move upstream into platform concept phases, locking in fiber costs well before production.

Directed-energy weapons exhibit the steepest growth curve, with a projected 11.05% CAGR. Successful shipboard demonstrations have cemented confidence that fiber lasers can track and neutralise swarms of low-cost drones. Given power-in-aperture needs, every incremental watt of beam power drives additional demand for high-purity, large-mode-area fibers, expanding total military fiber optic cables industry revenue by design.

Geography Analysis

North America retained 34.10% revenue in 2025 due to sustained defense budgets and technology leadership. Programs such as the 1,100-unit fiber drone rollout highlight how procurement scales quickly once performance is proven. Research at national laboratories advances coherently combined lasers and bend-insensitive, rugged fibers, securing the region’s technical edge. The military fiber optic cables market size in North America further widens as each new platform standardises on optical backbones.

Asia-Pacific records the fastest 9.05% CAGR to 2031 as India, Japan, South Korea, and Australia step up modernisation. India’s Network For Spectrum contracts worth USD 207 million cover 57,015 km of fiber builds. Regional carriers partner on the ALPHA cable that offers 18 Tbps per pair, giving navies resilient routes. Defense ministries invest in 5G-backed training ranges that depend on dense optical fronthaul. These initiatives raise the military fiber optic cables market profile across the region.

Europe maintains solid demand, led by NATO projects that secure undersea infrastructure and cross-border land routes. The Baltic Sentry mission uses naval drones to patrol pipelines and cables, triggering orders for impact-proof fiber bundles. Sweden and Finland opened a SEK 75 million (USD 7.8 million) three-cable land corridor able to carry 3 Pbps, reinforcing regional resilience. As EU forces converge on common architectures, suppliers with pan-European approvals gain share in the military fiber optic cables market.

Competitive Landscape

The market is moderately fragmented. Specialist defense cable makers compete with diversified telecom groups that formed dedicated defense divisions. Firms differentiate by certifying products to MIL-DTL-38999 connector mates, shock levels under MIL-STD-810, and high-pressure immersion. Partnerships with prime contractors are critical because optical harnesses integrate deeply into platform architectures. Recent agreements link cable suppliers with avionics, radar, and laser integrators to co-design turnkey assemblies.

Technical innovation is a core lever. W. L. Gore & Associates markets 100 Gbps-rated cable that survives 10,000 flex cycles on combat vehicles while staying under 0.5 dB loss.[6]W. L. Gore & Associates, “GORE Fiber Optic Cables for Defense Air & Land,” gore.comCompetitors explore hermetic expanded-beam termini that clean with a simple wipe and reconnect in seconds. Vendors also add traceability chips that store lifetime bend data to predict failure before mission impact. Such features help win multi-year framework agreements and lift customer switching costs, sustaining margins across the military fiber optic cables market.

Vertical integration is gaining pace. Some fiber producers acquire connector shops and termination houses to offer full harness kits, slashing lead times and simplifying liability. Others invest in radiation test labs to certify batches in-house. These moves improve supply security, counterfeiting control, and customer confidence at a time when tampering risks attract headline attention. The resulting ecosystem raises the entry bar, concentrating value among firms with broad process capabilities.

Military Fiber Optic Cables Industry Leaders

Prysmian S.p.A.

OFS Fitel, LLC

Sumitomo Electric Industries, Ltd.

Optical Cable Corporation

Gooch & Housego PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: NATO began the Baltic Sentry mission to guard subsea infrastructure with naval drones

- January 2025: GlobalConnect finished a Sweden-Finland fiber corridor handling 3 Pbps as part of a 2,600 km build.

- January 2025: Intelligent Waves and Signify formed a joint venture to advance LiFi secure communications for the US DoD

- June 2024: Safran Electronics & Defense unveiled a 5 Gbps to 50 Gbps laser optical communication solution for armed forces

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the military fiber optic cables market as all armored or ruggedized glass or plastic optical fibers that move high-speed data, power, or sensing signals across land vehicles, ships, submarines, aircraft, and fixed defense installations. The definition, which we follow throughout the model, begins only when a cable is factory-certified to military or aerospace standards and ends at initial system integration in the platform.

Scope exclusion: civil telecom backbone, metro, or last-mile fiber projects are left outside the count because they follow very different specifications and buying cycles.

Segmentation Overview

- By Cable Type

- Single-mode

- Multi-mode

- By Material Type

- Glass Optical Fiber

- Plastic Optical Fiber

- Deployment Platform

- Land Systems

- Airborne Systems

- Naval and Sub-sea Systems

- By Installation Environment

- Tactical Field-Deployable

- Harsh-Environment Armored

- Under-water / Submarine

- By Application

- C3ISR and Tactical Communications

- Radar and Electronic Warfare

- Guided and Directed-Energy Weapons

- On-board Data Networks / Avionics

- Others (Power-over-Fiber, Sensors)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Singapore

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Israel

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts speak with fiber-optic design engineers, defense procurement officers, and network-upgrade program managers across North America, Europe, Asia-Pacific, and the Middle East. Interviews and online surveys help us validate typical cable lengths per platform, contract lead times, and average selling prices, filling gaps that public data leave open.

Desk Research

We start by mining open defense budgets, NATO Standardization Agreements, U.S. Bureau of Industry and Security export filings, and SIPRI shipment logs. Then, we layer in trade-body papers from the International Electrotechnical Commission and the Optical Internetworking Forum. Investor decks and Form 10-K notes from cable makers add pricing clues, while paid tools such as D&B Hoovers, Dow Jones Factiva, and Questel let us pull revenue splits, news cadence, and patent velocity. These are illustrative sources only; many others are tapped to cross-check volumes, values, and technical baselines.

Market-Sizing & Forecasting

The model begins with a top-down reconstruction of demand by mapping each country's command-and-control modernization budget to the share historically awarded to fiber solutions, which is then stress-tested with bottom-up roll-ups of supplier revenues and sample ASP × meter volumes. Key inputs include platform fleet additions, mean kilometers of cable per hull or airframe, inflation-adjusted ASP of radiation-hardened fiber, adoption of high-energy weapons that require low-loss links, and regional defense CAPEX growth. A multivariate regression, reviewed by primary-research experts, projects these drivers to 2030; any residual gaps are adjusted through scenario analysis around currency and procurement timing.

Data Validation & Update Cycle

Every quarter, we run variance checks that compare fresh contract awards, customs values, and vendor earnings against our baseline, and anomalies trigger re-contact with sources before sign-off. Reports refresh annually, and a last-mile analyst review ensures clients receive the newest view.

Why Mordor's Military Fibre Optic Cables Baseline Commands Reliability

Published market numbers often diverge because firms adopt different platform scopes, pricing years, and refresh cadences, and because some mix civil aerospace or telecom fiber with strictly defense-grade demand.

Key gap drivers include: a) others fold civil aircraft into their totals while our scope stays military-only; b) some models lock exchange rates at 2019, whereas we update currency quarterly; c) a few rely on a single supplier survey, yet we triangulate against budget lines and platform counts before finalizing the figure.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.82 B (2025) | Mordor Intelligence | |

| USD 4.90 B (2022) | Regional Consultancy A | Includes civil platforms and keeps prices in 2019 dollars |

| USD 2.80 B (2023) | Trade Journal B | Excludes under-sea naval cables and scales telecom adoption curves |

| USD 1.12 B (2024) | Global Consultancy C | Counts only airborne and ground cables, limited geographic sample |

These comparisons show that when scope alignment, up-to-date pricing, and multi-source validation are applied consistently, our baseline lands nearer the center of real-world spending and offers decision-makers a transparent, repeatable starting point.

Key Questions Answered in the Report

What is the current size of the Military Fiber Optic Cables market?

The market is valued at USD 4.09 billion in 2026 and is projected to reach USD 5.77 billion by 2031, registering a 7.12% CAGR.

Which region holds the largest share of the Military Fiber Optic Cables market?

North America leads with 34.10% revenue in 2025, driven by sustained defence budgets and rapid technology adoption.

Which segment is growing fastest within the Military Fiber Optic Cables market?

Directed-energy weapons applications show the highest 11.05% CAGR as fiber lasers move toward operational deployment.

Why are single-mode fibers preferred for military backbones?

Single-mode fibers deliver low attenuation over tens of kilometres, resist electromagnetic interference, and support bandwidth beyond 100 Gbps, making them ideal for naval and strategic networks.

What are the main restraints facing the Military Fiber Optic Cables market?

Field-level repair complexity and supply chain security vulnerabilities slow adoption by increasing maintenance burdens and compliance costs.

How are 5G tactical networks impacting demand for military fiber optics?

Private 5G deployments require dense fiber backhaul to meet multi-gigabit throughput and low-latency targets, driving consistent order flow for rugged single-mode cables and connectors.

Page last updated on: