Sniper Rifle Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 2.56 Billion |

| Growth Rate (2026 - 2031) | 4.89% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

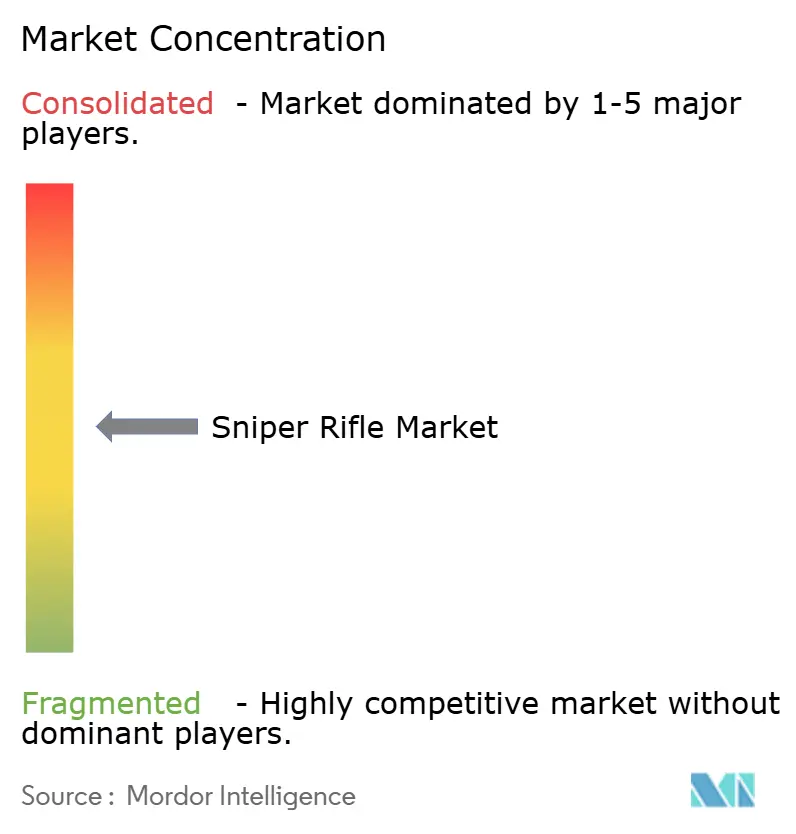

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sniper Rifle Market Analysis by Mordor Intelligence

The sniper rifle market size in 2026 is estimated at USD 2.01 billion, growing from 2025 value of USD 1.92 billion with 2031 projections showing USD 2.56 billion, growing at 4.89% CAGR over 2026-2031. Ongoing defense-modernization programs, the proliferation of multi-caliber weapon platforms, and demand for digitally enabled optics sustain this steady trajectory. Military recapitalization programs in the United States, Europe, and the Gulf states continue to anchor procurement volumes, while long-range competitive shooting and hunting build a sizeable civilian revenue base. Accelerating innovation in optical fire-control, the emergence of lead-free precision ammunition, and rising homeland-security procurements in response to urban counter-sniper requirements further reinforce future growth. At the same time, tightened export-control regimes and higher life-cycle costs temper adoption among budget-constrained end users, fostering measured but resilient expansion across the sniper rifles market.

Key Report Takeaways

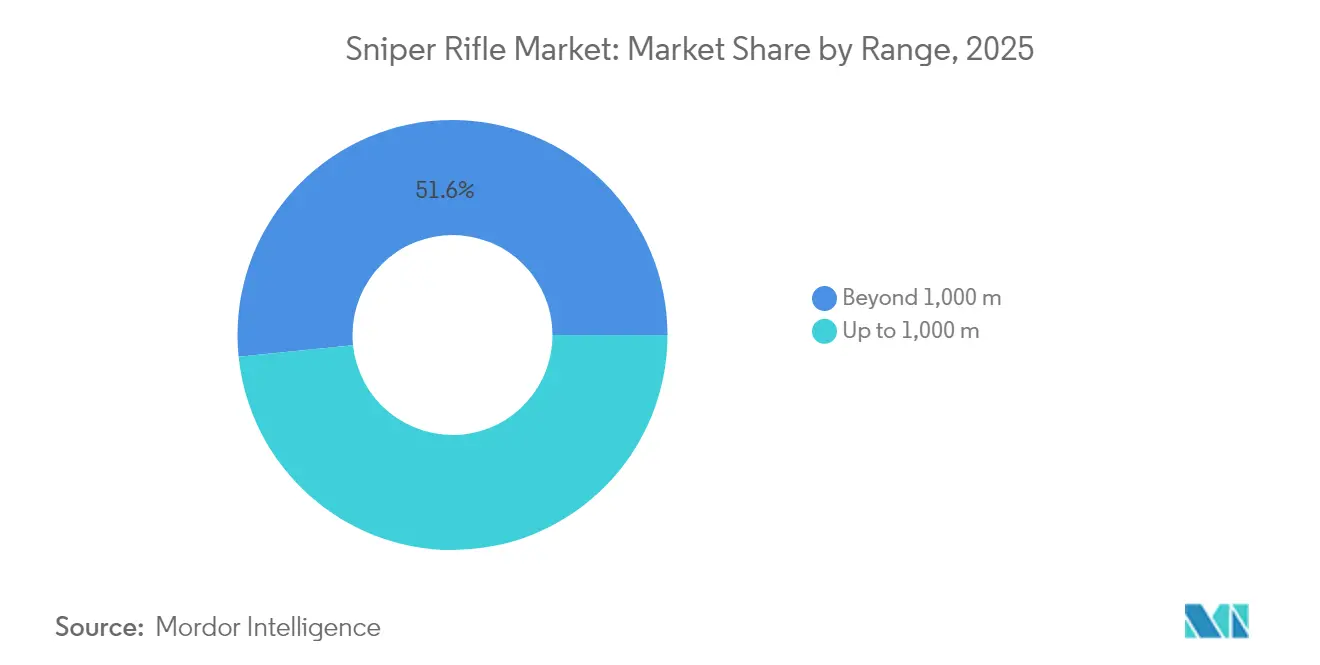

- By range, beyond-1,000 m weapon systems led with 51.62% revenue share in 2025, and the same category is projected to post the fastest 5.86% CAGR through 2031.

- By application, the military segment held 60.35% of the sniper rifles market share in 2025, whereas homeland security procurement is forecasted to advance at a 6.72% CAGR to 2031.

- By caliber, .338 Lapua Magnum accounted for 23.44% of the sniper rifles market size in 2025, while “other calibers” are set to expand at a 5.65% CAGR through 2031.

- By operating mechanism, bolt-action platforms commanded 64.55% revenue in 2025; semi-automatic systems are expected to grow at a 6.21% CAGR during the outlook period.

- By geography, North America contributed 38.22% of 2025 revenue, yet the Middle East and Africa region is forecasted to deliver the highest 6.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sniper Rifle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased defense modernization budgets fueling sniper rifle procurement | +1.8% | North America, Europe, Middle East | Medium term (2-4 years) |

| Growing popularity of long-range precision shooting in the civilian market | +0.9% | North America, Europe | Long term (≥ 4 years) |

| Counter-sniper capability upgrades driving law enforcement modernization | +0.7% | Developed markets worldwide | Short term (≤ 2 years) |

| Integration of digital optics and multisensor fusion enhancing targeting systems | +1.2% | Global, early NATO uptake | Medium term (2-4 years) |

| Logistics benefits driving adoption of modular multi-caliber sniper platforms | +0.8% | Worldwide military users | Medium term (2-4 years) |

| Environmental regulations accelerating shift toward lead-free sniper ammunition | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Defense Modernization Budgets Fueling Sniper Rifle Procurement

Escalating allocations for precision-fire capabilities in NATO and partner nations translate into multi-year rifle replacement programs and optics upgrades. The US Army earmarked USD 367.3 million for Next-Generation Squad Weapons in fiscal 2025, and the US Marine Corps completed its 587-unit MK22 program ahead of schedule, underscoring institutional priority for multi-caliber, extreme-range performance. Gulf-state outlays—headlined by Saudi Arabia’s USD 100 billion framework purchase—add another sizeable demand pool, while smaller European militaries such as Norway and Germany standardize on new long-range rifles to match near-peer threats. These synchronous initiatives reward manufacturers that pair first-round hit probability with simplified logistic chains, positioning the sniper rifles market for enduring large-volume orders.

Growing Popularity of Long-Range Precision Shooting in the Civilian Market

Competitive shooting leagues, long-range hunting, and recreational precision matches create a vibrant non-military sales channel. Smith & Wesson attributed a meaningful share of its USD 535.8 million FY2024 net sales to precision long guns tailored for the 1,000-yard firing line. Higher civilian throughput allows shared manufacturing lines with military programs, lowering unit costs and accelerating the trickle-down of aftermarket tunable triggers, carbon-fiber barrels, and advanced ballistic calculators. The sub-MOA performance standard now expected by civilian enthusiasts pressures suppliers to maintain continuous product refresh cycles, indirectly benefiting military users that leverage the same production tooling for government contracts.

Counter-Sniper Capability Upgrades Driving Law-Enforcement Modernization

Protective-service details and tactical-response teams increasingly specify rifles chambered in 6.5 mm or similar high-BC calibers to double hit probability at 1,000 m compared with legacy .308 Winchester. Federal tenders emphasize quick-change barrels, suppressor-ready muzzle devices, and compatibility with semi-automatic carbine accessories to streamline operator transition. Urban deployment doctrines demand precision at stand-off distances to defeat barricaded threats without collateral risk, sustaining premium demand among state-level procurement even when broader public-safety budgets remain flat.

Integration of Digital Optics and Multisensor Fusion Enhancing Targeting Systems

Digitally enabled fire-control optics transform traditional rifles into networked sensors. The US Army’s USD 94 million award for Advanced Infrared Weapon Sights calls for micro-cooled thermal cores that feed real-time ballistic solutions to snipers, widening engagement windows in low-light and degraded-weather conditions. Optical manufacturers now embed laser rangefinders, atmospheric sensors, and wireless data links that synchronize with soldier systems, turning every sniper into a node on the tactical network. As these capabilities migrate from prototype to program-of-record status, adoption accelerates across allied inventories and eventually trickles into high-end civilian optics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightened export controls and ITAR restrictions limiting international sales opportunities | -1.1% | US exporters and global buyers | Short term (≤ 2 years) |

| Elevated procurement and long-term maintenance costs restricting broader adoption | -0.8% | Budget-constrained markets | Medium term (2-4 years) |

| Emergence of counter-UAS directed-energy systems diminishing the strategic role of snipers | -0.6% | NATO countries and advanced military forces | Long term (≥ 4 years) |

| Limited integration with next-gen soldier systems and battlefield networks delaying modernization uptake | -0.7% | Global, with emphasis on technologically advanced militaries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightened Export Controls and ITAR Restrictions Limiting International Sales Opportunities

The May 2024 amendments to the US Export Administration Regulations introduced new license requirements for an expanded group of firearms and “crime-control” items, adding lead time and compliance cost for American manufacturers.[1]Bureau of Industry and Security, “Addition of ECCNs 0A504 and 0A505,” federalregister.gov While aimed at curbing illicit diversion, the rules inadvertently steer some foreign buyers toward suppliers operating under less stringent regimes. Compliance overhead includes legal reviews, individual part number classification, third-party due diligence fees, eroding margin on small-lot exports, and complicated after-sales support agreements.

Elevated Procurement and Long-Term Maintenance Costs Restricting Broader Adoption

A next-generation multi-caliber sniper rifle paired with digital optics can reach USD 25,000 per complete system, before factoring in specialized armorer training and software sustainment. Bulk military buys partially offset these costs, yet smaller forces and municipal police departments often postpone replacement cycles. Examples such as canceling ultra-long-range prototypes after preliminary trials illustrate how total program cost can override impressive ballistic test results. Over the weapon's life, higher barrel-replacement frequency for magnum-class calibers and firmware updates for smart optics add budget pressure that discourages universal fielding.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Range: Heightened Demand for Extreme-Range Capability

Beyond 1,000 m rifles generated 51.62% of the total 2025 revenue, and the segment is advancing at a 5.86% CAGR as militaries prioritize overmatch at standoff distances. The sniper rifle market size for these extreme-range systems is forecast to widen by USD 0.34 billion between 2026 and 2031, reflecting procurement of .338 NM and .50 BMG platforms in active theaters. First-round hit efficacy at two kilometers underpins tactical doctrines emphasizing counter-battery engagements and anti-materiel roles. Procurement contracts increasingly include integrated suppressors and multi-sensor day-night optics to reduce signature while preserving target acquisition.

Up to 1,000 m rifles remain vital for police tactical units and urban warfare where line-of-sight is constrained. These weapons, generally chambered in 7.62 NATO or 6.5 mm Creedmoor, log consistent volume because training costs are lower and logistical commonality with service rifles simplifies ammunition supply. While their share of the sniper rifles market revenue slips slightly through the forecast horizon, consistent replenishment and replacement cycles ensure a solid customer base among national guard and gendarmerie formations.

By Caliber: Entrenched .338 Lapua Magnum Leadership Meets New Cartridge Innovation

The .338 Lapua segment accounted for 23.44% of 2025 revenue thanks to widespread military qualification and established supply chains across Europe, North America, and Asia. As many armies extend qualified engagement ranges to 1,500 m, this caliber remains the benchmark for anti-personnel precision with acceptable recoil. The sniper rifle market share held by .338 Lapua erodes only marginally as new entrants arrive, but absolute demand grows in line with overall market expansion.

“Other Calibers,” encompassing .300 Norma Magnum, 8.6 Blackout, and emerging 9.4 mm cartridges, register the fastest 5.65% CAGR amid efforts to balance ballistic coefficient, barrel life, and suppressed-fire performance. Multi-caliber actions allow units to select cartridges matched to altitude, temperature, and target set, insulating users from availability shocks in any commodity supply chain. Legacy 7.62*51 mm NATO is the default training round, preserving institutional knowledge while minimizing per-shot expenditure.

By Operating Mechanism: Bolt-Action Precision Versus Semi-Automatic Responsiveness

Bolt-action rifles held 64.55% of revenue in 2025 by their mechanical simplicity, rigid lock-up, and unrivaled single-shot accuracy. These attributes align with doctrinal emphasis on first-round lethality at extended range, particularly for anti-materiel or counter-sniper roles. The sniper rifle market size attached to bolt-action platforms continues to grow on absolute terms, yet their proportion gradually dips as specialized teams experiment with self-loading designs.

Semi-automatic rifles, charting a robust 6.21% CAGR, attract users who value rapid follow-up shots, reduced shooter signature, and smoother recoil impulse. Technological gains in barrel metallurgy, two-stage match triggers, and piston systems close historical accuracy gaps, making these rifles viable for designated marksman roles and protective services requiring multi-target engagement. Software-defined fire-control optics further level the playing field, nudging procurement committees to blend both mechanisms in future force structures.

By Application: Military Core with Surging Homeland-Security Demand

Military customers controlled 60.35% of 2025 revenue as doctrinal updates prioritize precision fires alongside indirect assets. Fielding schedules within brigade combat teams, special-operations forces, and naval boarding units drives predictable order patterns that underpin prime contractors and specialized gunsmiths' business models. Cross-functionality with emerging soldier systems, including powered rails and secure datalinks, strengthens the integration narrative favored by acquisition boards.

Homeland security agencies register a 6.72% CAGR, the fastest among application segments. High-visibility incidents have prompted major Western and several Asia-Pacific police departments to replace legacy .308 platforms with higher-ballistic-coefficient (BC), lower-recoil rifles capable of sub-0.5 MOA precision at 1,000 m. Procurement frameworks increasingly tie funding releases to operator certification milestones, ensuring that training budgets rise with equipment orders, cementing recurring revenue for ammunition and sustainment kits.

Geography Analysis

North America anchored 38.22% of 2025 turnover owing to sustained US defense appropriations and the world’s largest civilian precision-shooting community. The sniper rifle market size in the region benefits from economies of scale as manufacturers spread fixed R&D costs over government and commercial runs. At the same time, buy-American provisions keep domestic content above 80% in most federal contracts. Canadian special operations units follow US modernization patterns, further bolstering regional demand.

Europe maintains a significant share through gradual but steady recapitalization among NATO members seeking interoperability and extended effective ranges. Procurement agendas here emphasize integrated suppressors, lead-free ammunition compliance, and digital day-night optics, aligning with stringent environmental and soldier-sustainability standards. High-altitude training sites in Norway, Germany, and Italy also provide grounds for extreme-cold barrel metallurgy, feeding innovation that circulates back into global product lines.

The Middle East and Africa are poised for a 6.45% CAGR as Gulf monarchies advance multi-billion-dollar rearmament programs and sub-Saharan forces invest in counter-terror and border-security capabilities. Large-volume orders from Saudi Arabia and the United Arab Emirates influence platform standardization across the broader region. African special forces gravitate toward European bolt-action models compatible with NATO ammunition supply chains. Local maintenance-training partnerships often accompany these contracts, building indigenous armorer skill sets that support lifecycle sustainment.

Asia-Pacific records rising adoption propelled by India’s emerging indigenous manufacturing base and Australian special operations requirements for anti-materiel systems with multi-role optics. Parallel economic growth in Southeast Asia yields discretionary security budgets that include long-range sniper assets, though deliveries remain sensitive to export-control approvals from Western OEMs. South America shows moderate demand, driven mainly by specialized police units combating transnational crime in mixed urban-jungle environments, with procurement cycles closely tied to multilateral public-security funding.

Regulatory Landscape

The sniper rifle market operates under stringent national firearms laws and defense trade controls that govern both complete weapons and critical components such as barrels, suppressors, and digitally enabled optics. In the United States, exports are shaped by the split between the Department of State (ITAR/USML) and the Department of Commerce (EAR/CCL), and the May 2024 BIS amendments to the Export Administration Regulations expanded firearms-related license requirements for an enlarged set of firearms and parts. This raises classification and licensing workload for US suppliers.

Procurement and compliance requirements also shape demand through government tenders and contracting frameworks. In the United Kingdom, the Ministry of Defence is using Project SHAMER market engagement activity (including a March 2026 PME-2/RFI round) to define a multi-caliber sniper capability spanning 7.62x51 NATO, .338 Lapua Magnum, and .300 Norma Magnum, reinforcing interoperability and qualification requirements for suppliers targeting UK and NATO-aligned programs. Separately, a June 2026 US Department of State proposal to amend ITAR Part 130 (political contributions, fees, and commissions reporting) signals continued tightening of compliance processes that can affect how OEMs structure international sales, agent relationships, and offset-related reporting.

Value Chain Analysis

The value chain starts with raw materials and precision manufacturing inputs, including steel and specialty alloys for actions and barrels, carbon-fiber or composite stocks, and coatings. It then moves to sub-system suppliers for triggers, suppressor interfaces, rails, and advanced optics, such as thermal cores, laser rangefinders, onboard ballistic computation, and secure connectivity. OEMs and specialized precision-rifle manufacturers integrate these components into complete weapon systems and carry out qualification testing, documentation, and configuration control to meet military, homeland security, and civilian specifications. Downstream distribution follows government contract channels and authorized defense distributors, with civilian retail supported by training, armorer services, spare parts, and lifecycle sustainment.

Recent supply-side shifts point to how industrial partnerships and consolidation are reshaping control over precision capacity and technology. India is building localized assembly and manufacturing nodes through technology transfer, illustrated by the ICOMM-CARACAL Small Arms Complex in Hyderabad and subsequent local production of the CSR 338 for the CRPF, which affects regional sourcing for barrels, actions, and final integration. At the premium end of bolt-action precision manufacturing, corporate consolidation is also changing the competitive set, with FN Browning Group moving to acquire Accuracy International. The combination can bring brand, distribution, and manufacturing scale together across the precision-rifle ecosystem, while suppliers still manage export-control friction for cross-border deliveries and after-sales support.

Competitive Landscape

Competitive intensity is moderate, characterized by a mix of long-established firearm brands and diversified defense primes. Barrett Firearms has expanded its Tennessee production footprint through a USD 76 million facility investment to meet backlogged orders for the MK22 multi-role adaptive design.[2]Barrett Firearms, “Barrett Announces Headquarters Expansion,” barrett.net The company leverages decades of large-caliber expertise while integrating quick-change barrels that align with current modularity trends. European suppliers such as Heckler & Koch match domestic demand for future soldier programs, having secured the German Army G210 contract for next-generation semi-automatic sniper rifles. These platforms prioritize ergonomics, low-visual-signature coatings, and suppressor optimization, aligning with continental end-user requirements for stealth and rapid engagement. At the component level, optic manufacturers, including Leonardo DRS, ELCAN, and smaller AI-enabled sight vendors, compete on onboard computation power, sensor fusion, and network security features.[3]Leonardo DRS, “DRS Awarded U.S. Army Contract for Advanced Infrared Weapon Sights,” drs.com

New market entrants increasingly focus on sustainable materials and reduced sound signatures, addressing two fast-emerging customer pain points: environmental compliance and urban warfare concealment. Lead-free projectile makers partner with barrel suppliers to mitigate accelerated wear, forming cross-company consortia to accelerate qualification trials. Meanwhile, enterprise cyber-security companies collaborate with optic OEMs to harden wireless ballistic-calculator links against electronic-warfare threats, signaling a convergence of defense electronics and traditional firearms expertise within the sniper rifles market.

Sniper Rifle Industry Leaders

SNT Motiv Co., Ltd.

Accuracy International Ltd.

Strategic Armory Corps, LLC

Barrett Firearms Mfg, Inc.

Knights Armament Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Multi-caliber sniper systems and modular architectures offer a procurement and product-development whitespace, since they reduce the need to field multiple dedicated rifles across mission sets. This is reflected in ongoing acquisition activity such as the UK Ministry of Defence Project SHAMER market engagement, which calls for a single multi-caliber bolt-action sniper weapon capability spanning 7.62x51 NATO, .338 Lapua Magnum, and .300 Norma Magnum. In the US, continued contracting activity around legacy semi-automatic sniper systems, including pre-solicitation activity for M110 SASS parts and accessories, indicates sustainment demand alongside recapitalization. That supports opportunities for OEMs and tier suppliers in spares, upgrades, and configuration-managed retrofit kits.

Modernization scope is expanding beyond the rifle into ammunition, signature management, and training infrastructure, widening the addressable opportunity for primes and niche suppliers. The US Army is developing the XM1224 Hybrid-Anti Materiel Round to support MK22 Precision Sniper Rifle effects, and Army-led testing of multispectral signature management at sniper training highlights demand for materials and accessories that reduce detection by thermal sensors. As engagement distances extend, range and training modernization also becomes a procurement lane tied to fielding advanced systems, supporting demand for integrated packages that include optics, ballistic tools, suppressor-ready configurations, spares, and operator and armorer training, rather than standalone rifle sales.

Recent Industry Developments

- May 2026: FN Browning Group and Accuracy International announced a strategic acquisition that brings a specialist UK precision bolt-action rifle manufacturer into a larger firearms group. The acquisition links premium sniper-platform design and production with a broader global distribution and industrial footprint, shaping competitive dynamics for military and specialist police programs.

- April 2025: Icomm Tele Ltd and CARACAL inaugurated the ICOMM CARACAL Small Arms Complex in Hyderabad, India, to support local production of bolt-action sniper rifles including CSR 338, CSR 308, and CSR 50. The facility expands in-country assembly and sustainment capacity and reinforces procurement pathways that favor localized manufacturing and technology transfer.

- May 2024: Strategic Armory Corps signed an agreement with the City of Bryan, Texas, to establish a new world headquarters and facility. The planned investment adds manufacturing and corporate capacity that can support scaling of precision firearms output and associated aftermarket services for both government and civilian channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the sniper rifle market covers purpose-built rifles designed for precision fire at extended ranges, across military, homeland security, and civilian use, and counted as revenue from the sale of the rifles in USD across major regions.

Scope exclusions: This sizing excludes ammunition, scopes and optics, suppressors, tripods, training services, and broader small-arms categories that are not sold as dedicated sniper rifles.

Segmentation Overview

- By Range

- Up to 1,000 m

- Beyond 1,000 m

- By Caliber

- 7.62*51 mm

- .300 Winchester Magnum

- .338 Lapua Magnum

- .50 BMG

- Other Calibers

- By Operating Mechanism

- Bolt-Action

- Semi-Automatic

- By Application

- Military

- Homeland Security

- Civilian

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public defense budget documents and procurement publications, then moved to import and export statistics for small arms and parts where codes were relevant for directional checks. Open sources such as SIPRI arms transfer material, UN Comtrade tables, NATO standardization and interoperability references, and government contract award portals were reviewed for product descriptions and disclosed quantities.

To keep the market model practical, we complemented these with company annual reports and investor presentations, defense ministry and law enforcement modernization notes, and reputable press coverage of contract wins and fielding timelines. Patent databases and shipment-level import or export data were used selectively to sanity check technology shifts and cross-border supply patterns for key calibers and platforms. The desk research sources listed here are illustrative, and other public references were also used to gather, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with defense procurement and sustainment specialists, firearms distribution and training channel participants, and subject matter experts tracking precision shooting demand. These discussions were used to confirm what is counted as a sniper rifle versus adjacent precision rifles, pressure-test unit pricing bands by caliber and mechanism, and then adjust regional adoption assumptions for military and homeland security buying cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | APAC: 51% |

| Mid tier: 56% | Functional/Unit leaders: 32% | EMEA: 29% |

| Smaller Players: 14% | Managers: 55% | Americas: 20% |

Market-Sizing & Forecasting

Our sizing starts from a top-down build that reconstructs demand using defense and security procurement signals, then maps them into likely rifle volumes by program type and replacement cadence, followed by pricing bands that reflect caliber and operating mechanism. Once that structure was set, we corroborated the totals using selective bottom-up approximations, including sampled contract quantity checks, channel price points for civilian precision platforms, and supplier-side volume discussions where disclosure allowed.

Key model inputs included adoption by application (military, homeland security, civilian), caliber mix shifts (for example 7.62x51 mm versus.338 Lapua Magnum and.50 BMG), bolt-action versus semi-automatic share changes, regional modernization timelines, and observable unit price progression by specification and order size. For forecasting, scenario analysis was used so procurement timing risk, export-control friction, and modernization acceleration could be reflected without forcing one narrow path. Where bottom-up signals were incomplete, gaps were handled through conservative penetration assumptions that were then rechecked with primary feedback and historical program behavior.

Data Validation & Update Cycle

Results were cross-checked through multiple passes, where model outputs were compared against independent signals such as known contract cycles, defense budget direction, and regional procurement narratives visible in public sources. Outliers were flagged for review, and assumptions were reworked when implied pricing or volumes did not match what interviewees said is achievable in real purchase orders.

Before sign-off, a second analyst review is completed to test the math, scope boundaries, and year-to-year continuity, and then a final pass is done close to delivery to capture new awards or policy events. Reports are refreshed annually, and interim updates are triggered when a material procurement event or regulatory change is observed and confirmed.

Mordor Intelligence's Sniper Rifle Market Sizing Compared With Other Published Estimates

Published sniper rifle market values often differ because the counted product boundary changes, and then the pricing and demand indicators used to scale volumes also change. Differences can also come from whether the year represents booked procurement, deliveries, or a blended view that mixes civilian and defense timing.

Contract award tracking, caliber-level platform mix checks, and regional procurement cadence validation are the evidence points that keep Mordor Intelligence aligned to a rifle-only revenue pool in 2026, instead of expanding the total with adjacent precision firearms or attached accessories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.01 B (2026) | |

| Global Consultancy A | USD 3.36 B (2024) | The higher value appears linked to a broader interpretation of the market boundary and a base year that can blend earlier procurement peaks with civilian demand, which lifts the implied volume and average selling price versus a rifle-only count. |

| Industry Publisher B | USD 3.30 B (2025) | This estimate is likely influenced by a wider inclusion set and a different treatment of pricing progression, where list pricing and bundled configurations can be reflected more directly rather than being filtered through program-level award and delivery timing. |

The table shows that year choice and what is included around the rifle itself drive most of the spread, and then pricing logic amplifies the difference. By keeping the scope anchored to sniper rifles and validating the total with procurement cadence and caliber mix signals, the final number stays traceable to repeatable steps.

Key Questions Answered in the Report

What is the current value of the sniper rifle market?

The sniper rifle market stood at USD 2.01 billion in 2026 and is projected to climb to USD 2.56 billion by 2031, reflecting a CAGR of 4.89% during the forecast period.

Which range category holds the largest share?

Beyond-1,000 m weapon systems held 51.62% of revenue in 2025 and will maintain leadership through 2031.

Which region is growing the fastest?

The Middle East and Africa region is forecasted to record the quickest 6.45% CAGR through 2031, boosted by large Gulf procurement programs.

Why are export controls considered a key restraint?

Recent US rule changes added new license steps for many rifles and optics, increasing compliance costs and delaying shipments for exporters.

How is civilian demand influencing product innovation?

Competitive shooting leagues push for sub-MOA accuracy and smart optics, compelling manufacturers to introduce features that later migrate into military variants.

What technological trend will shape future procurements?

Integrated digital fire-control optics that combine thermal imaging, ballistic computation, and wireless networking are expected to become standard on next-generation sniper rifles.

Page last updated on: