Military Lighting Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

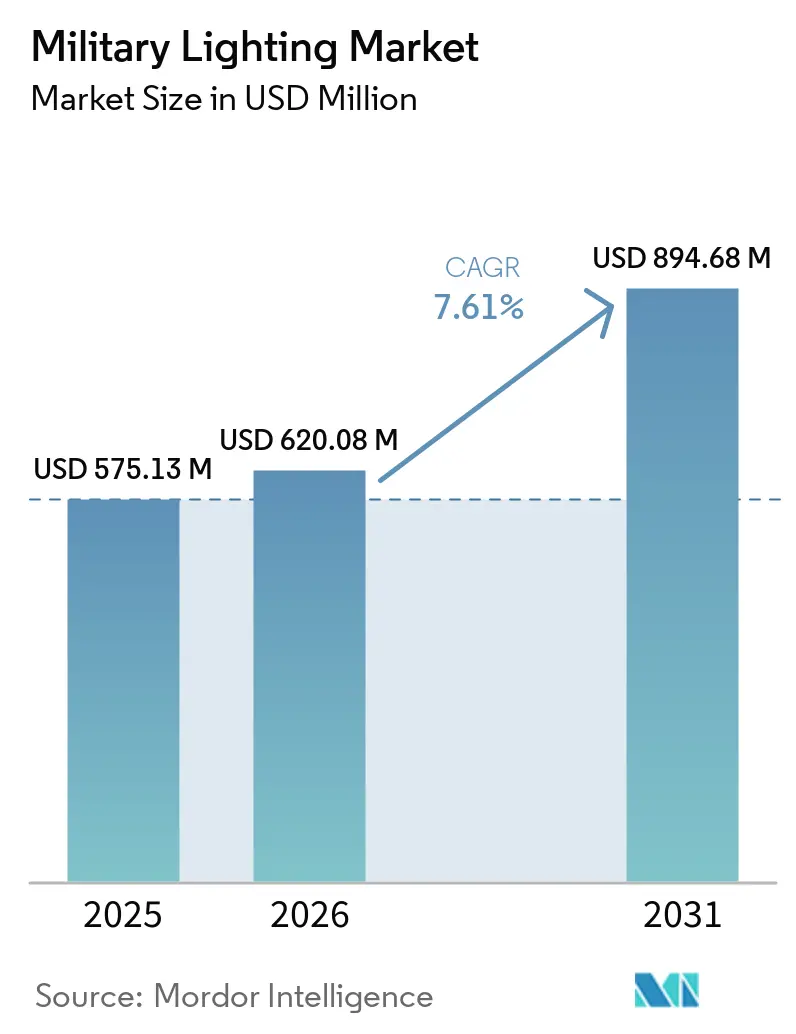

| Market Size (2026) | USD 620.08 Million |

| Market Size (2031) | USD 894.68 Million |

| Growth Rate (2026 - 2031) | 7.61% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Military Lighting Market Analysis by Mordor Intelligence

The military lighting market size is projected to expand from USD 575.13 million in 2025 and USD 620.08 million in 2026 to USD 894.68 million by 2031, registering a CAGR of 7.61% between 2026 and 2031. The rise from the 2026 base reflects a procurement reset after a strong 2025 buying cycle. Still, it does not change the longer replacement path for cockpit, exterior, and vehicle lighting systems across military fleets. The military lighting market is being reshaped by the steady move away from incandescent and halogen systems toward solid-state technologies that reduce maintenance, cut power draw, and improve spectral control on aircraft, land vehicles, and fixed installations. Applications requiring NVIS compliance, dual-mode visible and infrared signaling, and extended operational life are most critical, especially for aircraft, tactical vehicles, and expeditionary systems that operate in low-light conditions, often alongside crews equipped with night vision. Regional growth is also being reinforced by defense modernization budgets in the US, Japan, and India, where new aircraft, deck lighting, cockpits, and vehicles already include embedded lighting specifications that cannot be easily deferred once platform procurement begins. Competitive positioning in the military lighting market still rests on platform certifications, domestic sourcing compliance, and the ability to support long program cycles, which is why incumbent suppliers with proven airborne credentials continue to hold an advantage in the highest-value contracts.[1]Source: U.S. Department of Defense Office of Inspector General, “DoD Compliance with the Buy American Act for Light Emitting Diode Lighting Improvement Projects,” U.S. Department of Defense Office of Inspector General, media.defense.gov

Key Report Takeaways

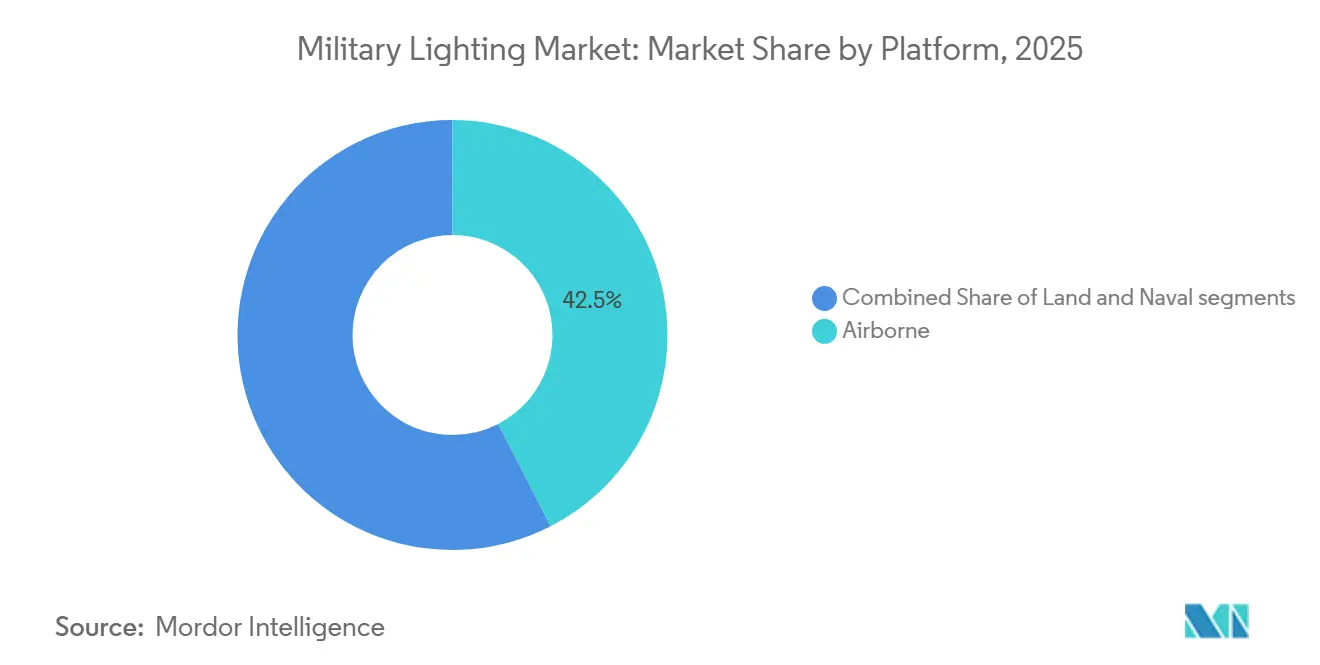

- By platform, airborne led with 42.45% of the military lighting market size in 2025, while land is forecast to grow at an 8.75% CAGR through 2031.

- By technology, LED accounted for 56.80% of the military lighting market size in 2025, while OLED and micro-LED are projected to grow at an 8.95% CAGR through 2031.

- By solution, hardware accounted for 47.35% of the military lighting market size in 2025, while software is expected to grow at a 7.99% CAGR through 2031.

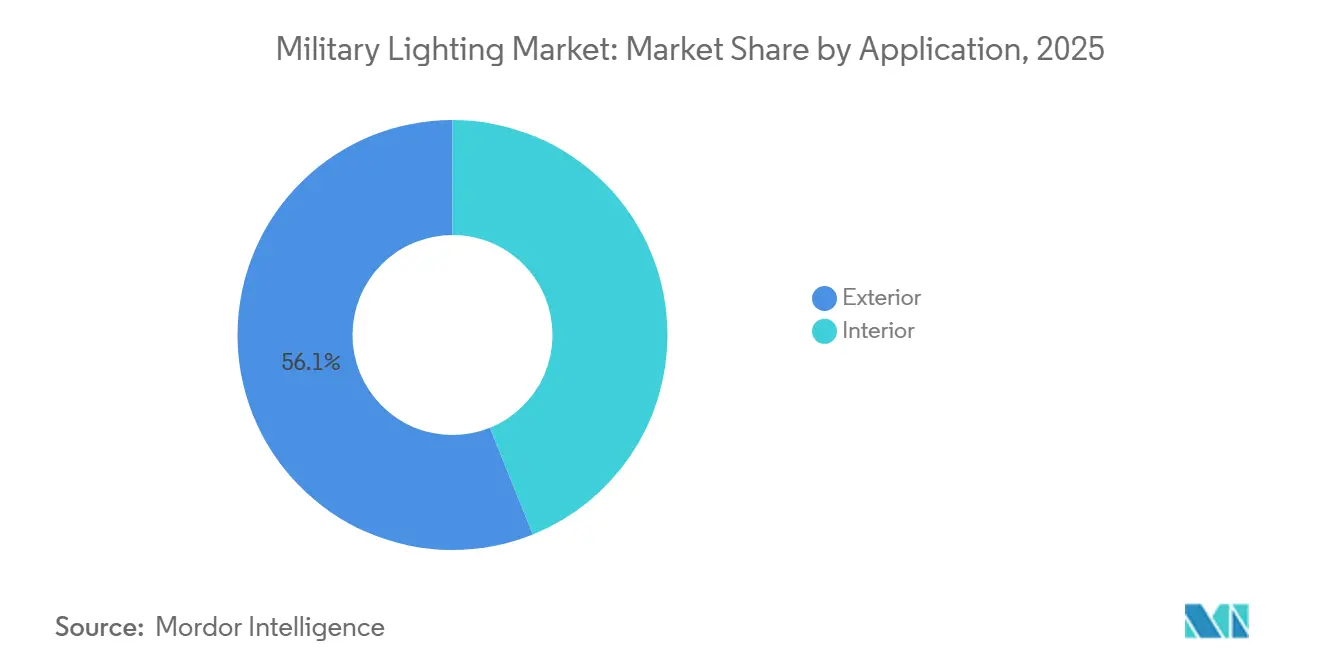

- By application, exterior accounted for 56.10% of the military lighting market size in 2025, while interior is forecast to expand at an 8.20% CAGR through 2031.

- By end-user, the Air Force held 41.95% of the military lighting market share in 2025, while the Army is projected to record the fastest CAGR of 8.73% through 2031.

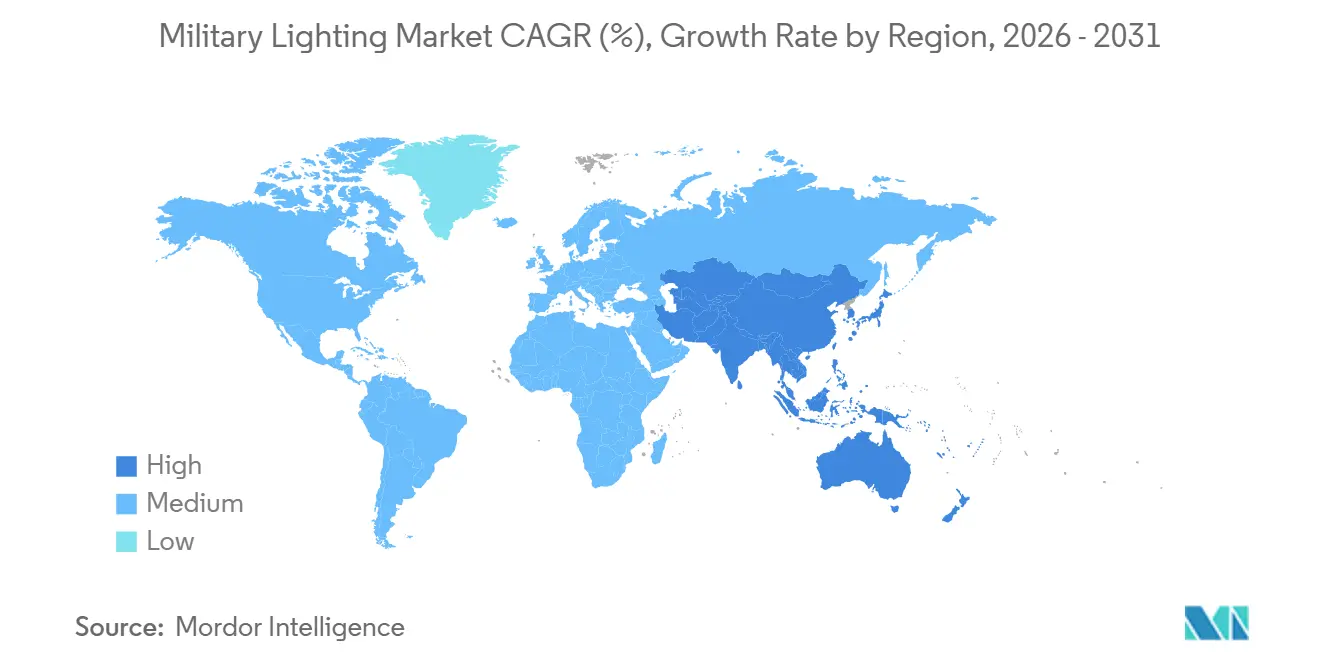

- By geography, North America accounted for 36.60% of the military lighting market in 2025, while Asia-Pacific is forecast to grow at a 8.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Military Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LED retrofitting for lower power load and lower IR signature | +1.8% | Global, with early gains in North America and Western Europe | Short term (≤ 2 years) |

| Standard-mandated NVIS cockpit upgrades under MIL-STD-3009 | +1.5% | Global, with NATO fleets first and expansion into allied APAC programs | Short term (≤ 2 years) |

| Integration of adaptive multi-spectral luminaires for stealth | +1.0% | North America and Europe | Medium term (2-4 years) |

| Modular plug-and-play light kits for expeditionary forces | +0.7% | Global, especially North America, Europe, and the Middle East and Africa | Medium term (2-4 years) |

| Dual-mode (visible/IR) beacon demand for coalition IFF | +0.8% | Global, with NATO interoperability first and APAC expansion following | Medium term (2-4 years) |

| DoD zero-maintenance preference accelerating solid-state adoption | +0.7% | North America first, with spillover into allied procurement standards | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

LED Retrofitting Cuts Power Consumption and Reduces Platform IR Signatures

LED retrofitting has moved from a preferred option to a program requirement across a growing share of the military lighting market. Honeywell's CH-47 LED red/IR dual-mode anti-collision light replaces the traditional xenon ACL, providing up to 52% lower power consumption, a 65% weight reduction, and a photometric life of up to 40,000 hours.[2]Source: Honeywell Aerospace, “LED Dual-Mode Red and IR Anti-Collision Light for the CH-47,” Honeywell Aerospace, aerospace.honeywell.com These benefits contribute to a robust sustainment case by reducing scheduled maintenance requirements, enhancing aircraft availability, and eliminating the need for routine flashtube and capacitor-bank replacements. The value extends beyond efficiency because solid-state systems also help limit unwanted heat and broad-spectrum emission that can make older lighting assemblies more visible to hostile thermal sensors. In practice, the military lighting market benefits from LED conversions, which reduce maintenance events, improve reliability, and align with the broader move toward more power-conscious platform design. These factors also shorten payback periods within normal program funding windows, which helps sustain retrofit demand even when procurement teams face pressure to delay less critical subsystems.

Standard-Mandated NVIS Upgrades Force Fleet-Wide Cockpit Replacements

MIL-STD-3009 remains one of the clearest structural drivers in the military lighting market because it applies to aircraft systems that operate with night vision imaging systems and governs radiance, chromaticity, and luminance performance for illuminated cockpit components. The standard remains active, with the DLA listing a document date of April 2024 in Notice 2 – Validation, and the next review is scheduled for April 2029, ensuring ongoing compliance relevance for aircraft operators, lighting suppliers, and retrofit teams involved in cockpit, display, and illuminated-control refresh programs. Every avionics system that touches displays, panels, indicators, keyboards, or push-button switches can, therefore, trigger a broader lighting replacement requirement, even when the original program objective is not framed as a lighting project. Oxley Group's MIL-STD-3009-compliant NVIS cockpit components and C-130 upgrade projects illustrate the adaptability of a NATO-approved C-130 lighting modification for international C-130 operators.[3]Source: Oxley Group, “NVIS Cockpit Components & Upgrades,” Oxley Group, oxleygroup.com This approach extends beyond cockpit lighting to include external, cargo cabin, and loading ramp lighting solutions, thereby supporting the aircraft's extended service life. As a result, the military lighting market benefits primarily from standards-driven replacements rather than solely from the production of new platforms.

Dual-Mode Visible/IR Beacons Enable Multinational Coalition IFF Operations

Coalition operations are adding a separate demand layer to the military lighting market because lighting systems now support identification, deconfliction, and interoperability in addition to basic illumination. Dual-mode visible and infrared beacons allow aircraft and ground vehicles to remain visible to unaided crews while also providing covert recognition under NVGs, which reduces fratricide risk during joint operations and night missions. Honeywell's C-130 LED retractable landing light demonstrates technological advancements by integrating dual-mode visible and covert infrared operation. It offers 100 times the covert infrared output of the existing C-130 halogen retractable landing light. It features an LED photometric lifespan of up to 50,000 hours within the same retractable landing light assembly. Changes in allied naval aviation programs are becoming increasingly evident. Japan's FY2026 defense budget allocated funding to advance the conversion of JS Izumo and JS Kaga for F-35B operations, including installing deck status lights and testing landing guidance systems on JS Izumo. These upgrades highlight the growing integration of military lighting requirements into platform conversion programs, emphasizing flight-deck safety, night operations, and interoperability with US and allied F-35B operations as key priorities. In the military lighting market, this means interoperability gaps in older fleets are increasingly being solved through lighting upgrades rather than through software-only changes. That pushes demand into installed fleets and raises the importance of suppliers that can certify visible and infrared performance across multiple platform classes.

DoD Zero-Maintenance Policy Systematically Displaces Incandescent Technology

Maintenance reduction has become a powerful buying criterion in the military lighting market because deployed replacement labor is expensive and often operationally disruptive. The DoD’s LED-focused procurement direction for facilities and infrastructure reinforces the case for long-life solid-state systems that can maintain performance for far longer than lamp-based systems. The same logic now applies to platform lighting, where reduced failure rates can support higher readiness and fewer interruptions during training, deployment, and depot maintenance cycles. The July 2024 DoD OIG audit did not challenge the adoption of LED technology but identified compliance gaps related to the Buy American Act in DoD LED lighting projects. As domestic or qualifying-country content thresholds increase from 65% through 2028 to 75% starting in 2029, suppliers with traceable U.S. or allied supply chains are positioned to gain a procurement advantage supporting the military lighting market by favoring certified suppliers with compliant manufacturing facilities, even if it raises barriers to low-cost foreign competition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter EM and EMC certification thresholds | -0.5% | Global, with the strongest effect in North America and Europe | Medium term (2-4 years) |

| Supply bottlenecks in high-reliability GaN LED die | -0.6% | Global, with concentration in Asia-Pacific manufacturing chains | Short term (≤ 2 years) |

| Tritium regulations raising lifecycle cost | -0.3% | North America and Europe | Long term (≥ 4 years) |

| Budget diversion toward counter-UAS and autonomy programs | -0.4% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High-Reliability GaN LED Supply Constraints Add Component Lead-Time Risk

High-reliability GaN devices sit close to the performance ceiling for advanced military lighting market applications because they support demanding thermal, switching, and power conditions in driver subsystems. The constraint is that their supply chain remains exposed to material concentration and semiconductor chokepoints, with the Defense Business Board noting China’s dominant role in rare earths and gallium production. US-linked high-reliability supply response is in progress. EPC Space has announced JANS MIL-PRF-19500 certification for GaN HEMTs and, in its May 2025 QPL update, introduced its first qualified Power GaN JANS devices. The company also stated its intention to qualify 16 additional GaN JANS devices over the next 12 months. Even so, certified volume remains limited, meaning military lighting market programs that depend on high-reliability GaN-based electronics can still face long lead times and uneven supply availability, which is vital in airborne and high-specification ground programs where component qualification cannot be substituted at short notice. Until wafer capacity is certified, procurement teams will continue to build schedule buffers into advanced lighting contracts.

EM/EMC Certification Thresholds Create Non-Trivial Program Schedule Risk

EM and EMC testing remains a real brake on the military lighting market because lighting systems now sit beside denser electronic architectures on modern aircraft and vehicles. MIL-STD-461 qualification may lead to extended redesign cycles if suppliers underestimate the interaction between LED driver circuitry and active protection systems, radar, electronic warfare suites, or other sensitive electronics on the same platform. The burden is greater in NVIS applications, where suppliers must demonstrate both spectral compliance and stable operation under night-vision-sensitive wavelength conditions during testing and integration. Testing capacity is also limited because qualified laboratories are few, so scheduled slots can become a bottleneck even when product design is largely complete. In the military lighting market, this makes early certification planning a commercial advantage rather than only an engineering task. Programs that treat compliance as a late gate continue to face the greatest risk of delivery delays and follow-on cost pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Airborne Leads Revenue While Land Expands the Fastest

Airborne accounted for 42.45% of revenue in 2025, giving this segment the largest footprint in the military lighting market as aircraft continue to carry the highest lighting content per platform. Fixed-wing and rotary platforms require dense arrays of cockpit, navigation, anti-collision, landing, inspection, and covert lights, which keep airborne programs central to both replacement and new-production demand. NVIS compliance also weighs more heavily in aircraft than in other platform groups, which ties the segment closely to MIL-STD-3009 refresh cycles and cockpit modernization budgets. Exterior lighting on aircraft tends to command higher unit values because assemblies must withstand vibration, weather exposure, and strict certification standards over long service periods, keeping airborne at the core of the military lighting market even when broader defense procurement moves unevenly from year to year.

Naval demand remains stable but less dynamic because shipboard and deck-light replacement cycles are longer and more tied to platform refit windows than to annual procurement spikes. Land is the fastest-growing platform segment, with a 8.75% CAGR through 2031, indicating where the next broad conversion wave is taking shape in the military lighting market. The demand for lighting in armored vehicles, tactical vehicles, and shelters is transitioning toward LED-based, NVG/IR-compatible, and low-maintenance solutions. Budget allocations prioritize tactical vehicle modernization, JLTV modifications, shelter integration, power distribution, command and control (C2) upgrades, and addressing obsolescence issues. Supplier data indicates widespread adoption of LED technology across military vehicles and shelters. Honeywell's selection of the MV-75 FLRAA LED Landing Search Light highlights the growing emphasis on LED-first design requirements in next-generation military aviation platforms and other rugged military applications.

By Technology: LED Dominates Today While OLED and Micro-LED Gain in Advanced Displays

LED accounted for 56.80% of revenue in 2025, making it the most established technology in the military lighting market. That position reflects its use across exterior assemblies, cockpit utility lights, vehicle systems, and military facilities, where long life, lower maintenance, and lower power draw now carry more weight in procurement decisions than before. The technology is also helped by the fact that DoD procurement rules increasingly favor efficient solid-state systems, while domestic content requirements narrow the approved supplier base for future contracts. Incandescent and halogen systems still retain some demand, where compatibility, thermal performance, or legacy design lock-in make substitution more difficult. Still, their footprint continues to shrink with each new platform cycle. In the military lighting market, LED therefore remains both the default choice for new procurement and the main retrofit path for older fleets.

OLED and micro-LED are the fastest-growing technologies, with a 8.95% CAGR through 2031, because advanced cockpit displays and HUD applications require higher brightness, deeper contrast control, and better power-to-performance than standard lighting modules provide. This growth sits closest to the cockpit boundary, where display systems increasingly overlap with lighting requirements in aircraft modernization work. The military lighting market is therefore expanding not only through lamps and luminaires but also through display-linked optical systems that enhance pilot visibility during day and night operations. Tritium and betalight solutions are relevant for military applications that require self-luminous functionality without batteries, wiring, or external power, such as weapon sights, compasses, gauges, markers, and safety devices. However, regulations like 10 CFR 32.22 and 10 CFR 32.53 impose licensing, safety, labeling, handling, and transfer requirements, limiting scalability compared to conventional electrical lighting. LED technology remains the primary choice for most military lighting applications, while OLED and micro-LED are emerging options for cockpit displays, HUDs, head-mounted systems, and soldier-vision interfaces.

By Solution: Hardware Holds the Largest Base While Software Adds the Most Growth

Hardware accounted for 47.35% of solution revenue in 2025, giving it the largest current position in the military lighting market, as luminaires, drivers, fixtures, and integrated assemblies still account for the largest share of platform spending. Hardware also anchors long procurement cycles since it must pass platform-level certification, environmental testing, and fitment requirements before installation can begin. Services remain tightly linked to that base because installation, retrofit support, recertification, and sustainment work often travel with the same contract or platform program, creating sticky customer relationships for suppliers that can support the full lifecycle rather than only the original hardware sale. The military lighting market maintains this structure because mission-critical lighting cannot be treated as a disposable component.

Software is the fastest-growing solution segment, with a 7.99% CAGR through 2031, as lighting control becomes more programmable and more tightly integrated with avionics, vehicle electronics, and fixed-facility management systems. Dimming profiles, adaptive switching between NVIS-compliant and standard-visible modes, and software-controlled mission settings are becoming part of system differentiation rather than being treated as secondary features. That increases the value of suppliers that can combine certified hardware with embedded controls and systems integration. The DoD Unified Facilities Guide Specification (UFGS) for interior lighting introduces a compliance framework for connected military installations. UFGS 26 51 00 mandates that networked lighting control systems and devices comply with the cybersecurity requirements in Section 25 05 11 for facility-related control systems. This emphasizes the importance of cybersecurity, control-system certification, and lighting-control integration for suppliers catering to fixed military sites. In the military lighting market, software growth therefore expands revenue per platform and deepens supplier involvement after the original hardware installation is complete.

By Application: Exterior Systems Lead Spending While Interior Lighting Gains Speed

Exterior lighting accounted for 56.10% of revenue in 2025, giving it the largest market share in the military lighting market. Anti-collision, landing, taxi, formation, and covert exterior systems usually cost more because they face more demanding environmental and certification requirements than many interior units. They are also a frequent entry point for NVIS compliance and dual-mode visible and infrared capability, especially on aircraft where exterior visibility and covert signaling must coexist. Collins Aerospace's portfolio across the Eurofighter, A400M, Saab Gripen, and other military aircraft demonstrates the breadth and platform-specific nature of exterior lighting demand across allied fleets. This keeps exterior assemblies at the forefront of the military lighting market, even as newer spending shifts toward the cabin and crew station.

Interior lighting is forecast to grow at an 8.20% CAGR through 2031, reflecting rising investment in crew stations, cargo areas, and adaptive wash lighting in aircraft and other mission platforms. Operators are paying closer attention to interior light quality because crew endurance, readability, and situational awareness matter during long missions and low-light operations. The same efficiency case that supports exterior upgrades is now extending to cabins and crew compartments, with Honeywell's UH-60 dual-mode anti-collision LED system showing an 88% reduction in power draw and an 8.6 lb weight reduction compared to the legacy xenon system on a military aircraft platform. These performance improvements impact buyers' considerations for interior retrofits, as every watt saved and maintenance hour reduced is critical for aircraft operating within strict power, weight, and readiness constraints. As a result, interior systems are reducing the performance and procurement gap compared to exterior programs within the military lighting market.

By End-User: Air Force Is the Largest Buyer While Army Programs Set the Pace

The Air Force accounted for 41.95% of end-user revenue in 2025, making it the largest customer group in the military lighting market, as aircraft fleets require dense lighting content and frequent compliance-driven upgrades. Combat aircraft, transports, trainers, helicopters, and unmanned systems all need combinations of cockpit, navigation, anti-collision, and covert lighting that are both platform-specific and tightly regulated. That mix gives the Air Force the largest installed base of high-value lighting assemblies across most major defense regions. Navy demand remains important, especially in carrier operations, deck lighting, navigation, search functions, and submarine interiors, where reliability and compact power-efficient systems are highly valued. Together, the Air Force and Navy keep the higher-value end of the military lighting market anchored in air and maritime mission sets.

The Army is projected to grow at an 8.73% CAGR through 2031, making it the fastest-growing end-user segment in the military lighting market. Ground-force programs are moving through LED conversion at the same time as upgrades to vehicle electronics, night operations equipment, and survivability systems, creating a broader replacement base than many air-only suppliers once targeted. India’s October 2025 contract for night-sight devices worth INR 659.5 crore (USD 78.50 million) with more than 51% indigenous content follows a similar pattern in APAC, where lighting compatibility and night-vision adoption are increasingly moving together in army modernization programs and positioning the Army as a more influential participant in the military lighting market than its current revenue share indicates.

Geography Analysis

North America accounted for 36.60% of revenue in 2025, making it the largest regional contributor to the military lighting market. The region benefits from the scale of US defense procurement, long aircraft upgrade pipelines, and a regulatory framework that favors LED adoption and compliance with domestic content requirements in future awards. Honeywell's selection in January 2026 for the MV-75 FLRAA LED Landing Search Light and Astronics' increasing military aircraft sales highlight the growing impact of next-generation US aviation programs on North America's role in high-value military aircraft lighting and safety systems. However, this serves as evidence of robust US program momentum rather than conclusive proof of North American dominance in the broader military lighting market.

Europe remains the second-largest region and an important source of demand for the certified military lighting market, as NATO-aligned aircraft and defense autonomy programs continue to support local supply positions. The UK, France, and Germany maintain national and multilateral platform programs that favor proven suppliers with NVIS and exterior-lighting certification histories. Oxley Group's extensive experience in NVIS aircraft upgrades for the UK and allied fleets highlights the importance of certification, expertise in legacy platforms, and sovereign support in maintaining the long-term involvement of domestic suppliers. Collins Aerospace's lighting installations on Eurofighter, A400M, Tornado, and Gripen platforms highlight its role in supporting multinational European aircraft fleets. This presence drives repeat demand across various operators and countries, rather than being limited to a single national fleet. This is particularly significant for platform sustainment, retrofitting, spare parts, and NVIS/LED upgrades, which are required throughout the extended service lives of these aircraft.

Asia-Pacific is projected to grow at an 8.05% CAGR through 2031, making it the fastest-growing regional block in the military lighting market. The main support comes from record defense budgets, active platform procurement, and rising alignment with night-vision and interoperability requirements in Japan, India, and other regional allied programs. Japan approved a FY2026 defense budget of JPY 9.04 trillion (USD 57.87 billion), including funding for carrier conversion work on JS Izumo and JS Kaga, covering deck lighting and associated landing support systems. India's FY2026-27 defense allocation reached INR 7.85 lakh crore (USD 90.20 billion), and that spending is expected to raise demand for cockpit, vehicle, and aircraft-class lighting systems across a broader modernization cycle. Procurement records from Japan's Air Self-Defense Force (JASDF) show repeated LED base-lighting purchases, with deliveries scheduled for early 2026. This highlights a regional shift toward LED lighting in both major defense budgets and routine acquisitions. Korea's adoption of SWIR-based friend-or-foe identification devices underscores interest in advanced low-visibility lighting. In the Middle East and Africa, while lighting markets are smaller, demand is driven by fleet modernization, defense facility upgrades, and local defense-industrialization efforts in countries like Saudi Arabia and the UAE. South America remains a narrower opportunity set, with aging-fleet upgrades supporting the need, even though procurement speed is limited by fiscal pressure in several markets.

Competitive Landscape

The military lighting market shows moderate concentration at the top, with a small group of established suppliers holding the strongest positions in airborne applications. At the same time, a wider field of specialists competes in adjacent and lower-value niches. Astronics, Honeywell International, Collins Aerospace, and Oxley Group remain prominent because platform certification, program history, and design authority are difficult to displace once a supplier is embedded in aircraft or fleet upgrade work. Astronics reported USD 116.3 million in military aircraft revenue in 2025, up 32.1% year over year, with lighting and safety products playing a major role in that expansion. That revenue growth suggests the military lighting market still rewards suppliers that can align with long-cycle aircraft programs and deliver certified content at scale.

Honeywell's selection in January 2026 for the MV-75 FLRAA landing search light demonstrates incumbents establish their position early in next-generation platform programs, securing roles that can endure for decades. Collins Aerospace is following a similar path by installing broad exterior lighting across major military aircraft, helping it spread certification costs across multiple programs and customers. Oxley Group continues to benefit from its long history of NVIS upgrades, especially where legacy aircraft fleets still require certified cockpit modifications rather than full platform replacement. These examples show that the military lighting market does not reward price competition alone, because qualification history and platform familiarity often matter more than marginal component cost.

Strategic developments in 2025 and 2026 indicate that suppliers are prioritizing advancements in certification and integration capabilities, moving beyond a primary focus on basic hardware production. Honeywell has advanced its dual-mode and platform-specific LED upgrades for platforms such as the CH-47, UH-60, C-130, and MV-75, bolstering its position in both retrofit and new-build markets. Similarly, EPC Space's work on GaN certification is significant as it strengthens the domestic component base essential for future advanced lighting electronics. The military lighting market continues to offer opportunities for niche specialists in areas such as self-luminous products, NVIS vehicle systems, and advanced controls. However, market entry remains challenging due to the lengthy process required for MIL-SPEC, NVIS, and EMC qualifications, which can take years to establish a commercially viable offering. This dynamic sustains competition while providing a degree of protection for top-tier players.

Military Lighting Industry Leaders

Collins Aerospace (RTX Corporation)

Astronics Corporation

Honeywell International Inc.

Oxley Group

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bell Textron selected Honeywell's LED Landing Search Light for the US Army MV-75 Future Long-Range Assault Aircraft (FLRAA) program. The light is manufactured at Honeywell's Urbana, Ohio, facility and supports growth capability for laser pro-tracker integration. The MV-75 contract is expected to extend beyond 2050.

- August 2025: The US Navy awarded a USD 5 billion MAAC contract to accelerate Virginia-class submarine procurement, encompassing new EMI-hardened interior lighting suites.

- February 2025: Teledyne Technologies Incorporated completed the acquisition of select aerospace and defense electronics businesses from Excelitas Technologies Corp. for USD 710 million. The acquisition includes the Qioptiq® optical systems business in Northern Wales, UK, and the advanced electronic systems business in the US.

Global Military Lighting Market Report Scope

Military lighting encompasses specialized lighting systems, control solutions, and associated support designed for use across various defense platforms and military operational environments. These include aircraft, land vehicles, naval vessels, and mission-specific field applications. The military lighting market report excludes commercial lighting, civilian infrastructure lighting, decorative lighting, and non-defense lighting products unless they are explicitly designed, certified, procured, or integrated for military purposes.

The military lighting market is segmented by platform, technology, solution, application, end-user, and geography. By platform, the market is segmented into airborne, land, and naval platforms. By technology, the market is segmented into LED, incandescent/halogen, OLED and micro-LED, and tritium and betalights. By solution, the market is segmented into hardware, software, and services. By application, the market is segmented into interior and exterior lighting. By end user, the market is segmented into the army, navy, and air force. The report also covers the market sizes and forecasts for the military lighting market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Airborne | Fixed-wing |

| Rotary-wing | |

| Unmanned Aerial Vehicle (UAVs) | |

| Land | Tactical Vehicles |

| Main Battle Tanks | |

| Mine Resistant Ambush Protected (MRAP) | |

| Others | |

| Naval | Surface Combatants |

| Sub-surface Vessels | |

| Carrier Decks |

| LED |

| Incandescent/Halogen |

| OLED and Micro-LED |

| Tritium and Betalights |

| Hardware |

| Software |

| Services |

| Interior |

| Exterior |

| Army |

| Navy |

| Air Force |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Israel |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform | Airborne | Fixed-wing | |

| Rotary-wing | |||

| Unmanned Aerial Vehicle (UAVs) | |||

| Land | Tactical Vehicles | ||

| Main Battle Tanks | |||

| Mine Resistant Ambush Protected (MRAP) | |||

| Others | |||

| Naval | Surface Combatants | ||

| Sub-surface Vessels | |||

| Carrier Decks | |||

| By Technology | LED | ||

| Incandescent/Halogen | |||

| OLED and Micro-LED | |||

| Tritium and Betalights | |||

| By Solution | Hardware | ||

| Software | |||

| Services | |||

| By Application | Interior | ||

| Exterior | |||

| By End-User | Army | ||

| Navy | |||

| Air Force | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Israel | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving growth in military lighting demand through 2031?

Growth is being supported by LED retrofits, NVIS cockpit compliance, dual-mode visible and IR signaling needs, and new defense platform programs. The military lighting market is projected to reach USD 894.68 million by 2031 at a 7.61% CAGR.

Which platform category leads revenue today?

Airborne platforms led with 42.45% of revenue in 2025 because aircraft carry dense lighting content across cockpits, navigation systems, anti-collision lights, and covert mission lighting.

Which technology is growing the fastest in defense lighting systems?

OLED and micro-LED are the fastest-growing technologies, with an 8.95% CAGR through 2031, driven by their use in advanced cockpit displays and HUD applications.

Why are NVIS standards so important for aircraft lighting upgrades?

MIL-STD-3009 governs radiance, chromaticity, and luminance requirements for aircraft operating with night vision imaging systems. That makes cockpit refresh programs a recurring trigger for lighting replacement.

Which region is expanding the fastest?

Asia-Pacific is forecast to grow at an 8.05% CAGR through 2031, supported by large defense budgets in countries such as Japan and India and by growing alignment with night-operations and interoperability requirements.

Which end-user segment has the strongest future momentum?

The Army is expected to grow the fastest at an 8.73% CAGR through 2031 as vehicle lighting, shelter lighting, and night-vision compatible systems are upgraded alongside broader ground-force modernization.

Page last updated on: