Tactical Communication Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 23.05 Billion |

| Market Size (2031) | USD 31.86 Billion |

| Growth Rate (2026 - 2031) | 6.69% CAGR |

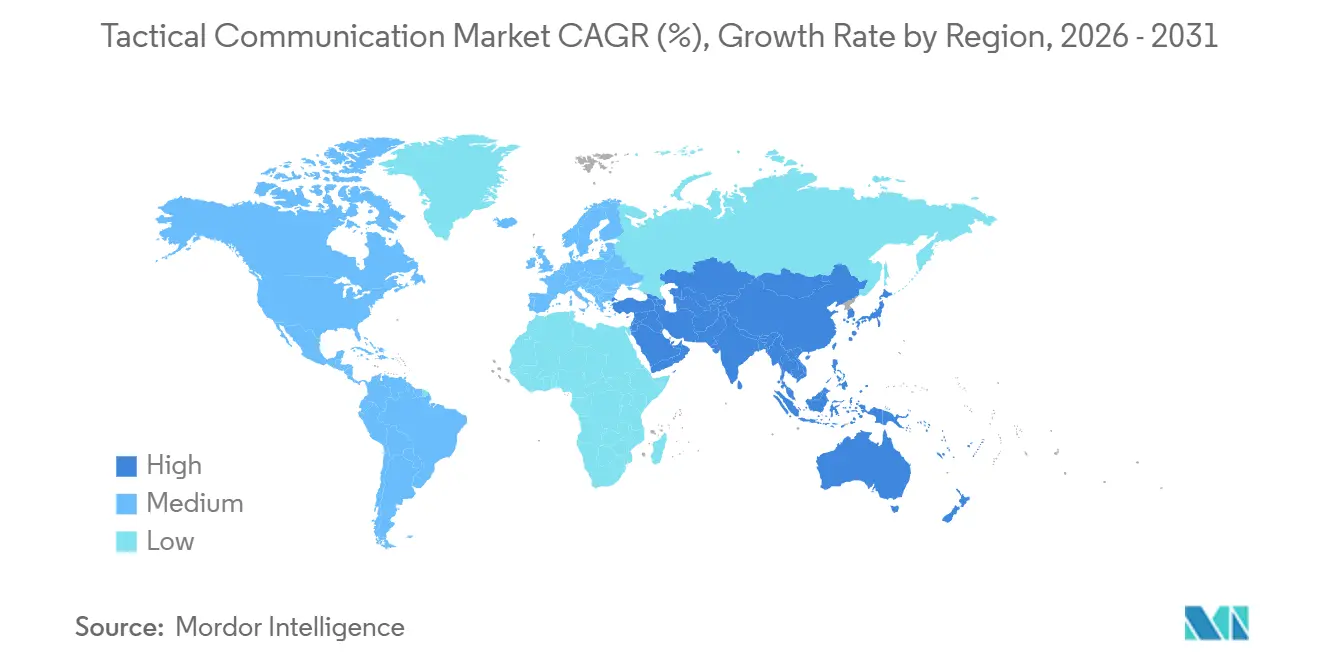

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

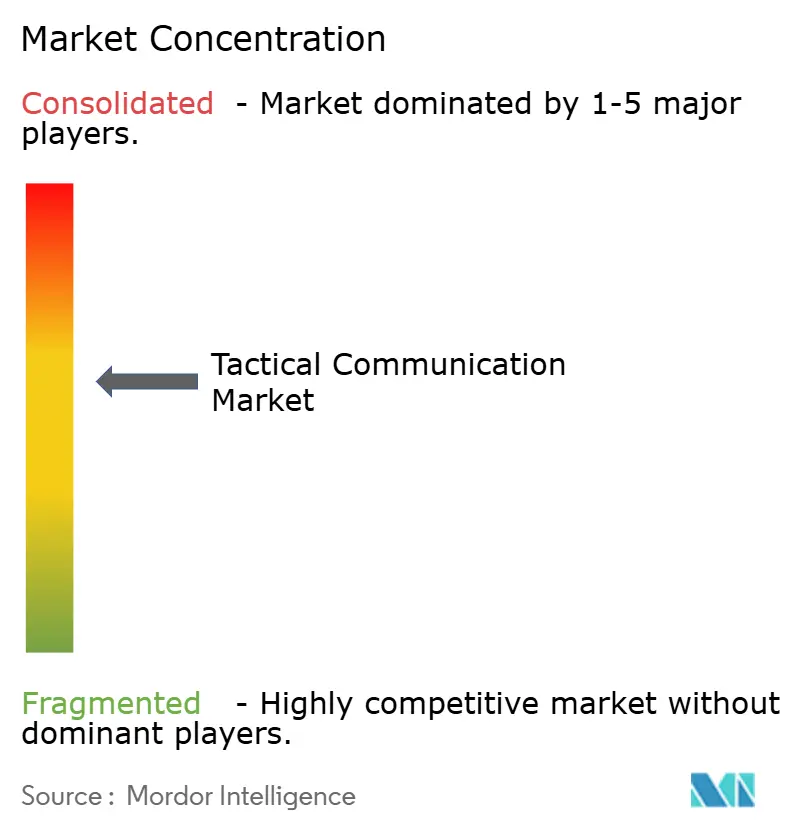

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tactical Communication Market Analysis by Mordor Intelligence

The tactical communication market size is expected to grow from USD 21.6 billion in 2025 to USD 23.05 billion in 2026 and is forecasted to reach USD 31.86 billion by 2031 at a 6.69 % CAGR over 2026-2031. Rapid migration from platform-centric to network-centric doctrines fuels spending on software-defined radios (SDRs), AI-driven spectrum management, and low-Earth-orbit (LEO) connectivity. Growing defense budgets in the US, China, India, and the Middle East sustain procurement pipelines, while NATO interoperability mandates shorten replacement cycles. Adoption of mesh networking and anti-jamming waveforms expands opportunities for vendors offering plug-and-play modules. However, spectrum congestion in the 225-400 MHz band and the high cost of post-quantum encryption temper near-term growth.

Key Report Takeaways

- By platform, land systems led the tactical communication market, accounting for a 44.76% market share in 2025. Space platforms are forecasted to expand at a 9.91% CAGR through 2031.

- By component, hardware captured 57.68% of the 2025 tactical communication market size, yet services are rising at a 7.61% CAGR.

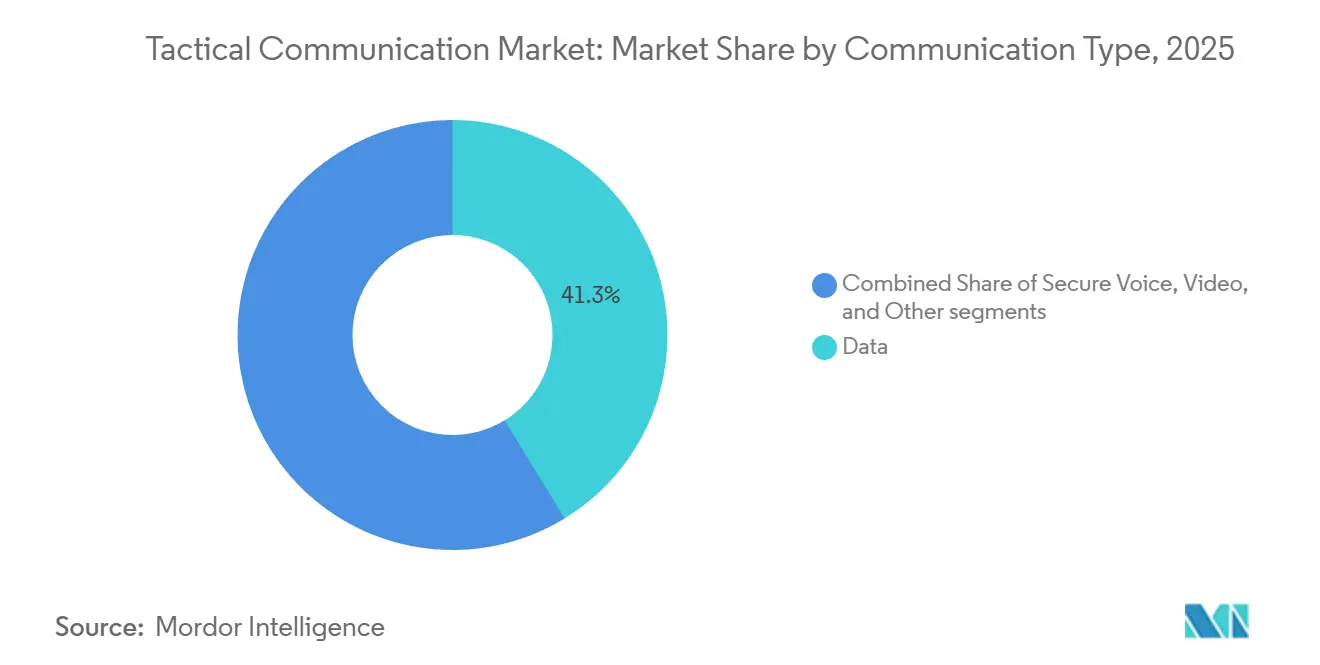

- By communication type, data retained leadership with 41.26% of the tactical communication market share in 2025, while video is poised to expand the fastest at an 8.49% CAGR through 2031.

- By end-user, defense forces commanded 79.23% of demand in 2025, while homeland security agencies are advancing at an 8.54% CAGR.

- By geography, North America held 39.45% revenue share in 2025, whereas the Asia-Pacific is forecasted to grow at a 7.15% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tactical Communication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense modernization and network-centric warfare (NCW) | +1.80% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growing global defense expenditure | +1.50% | United States, China, India, Middle East | Long term (≥ 4 years) |

| Demand for secure, resilient, high-throughput links | +1.20% | North America, Europe, select Asia-Pacific | Medium term (2-4 years) |

| 5G-NTN and private LTE enabling high-bandwidth ISR | +1.00% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| AI-driven cognitive radios for dynamic spectrum use | +0.90% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Miniaturized SWaP-C soldier-worn mesh devices | +0.70% | Global early adopters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Defense Modernization and Network-Centric Warfare

Network-centric doctrine places radios at the center of joint operations, transforming them into data routers that fuse sensor feeds, targeting coordinates, and logistics updates in real time. The US Army allocated USD 1.8 billion in 2025 to field AI-enabled software-defined radios that prioritize critical traffic and slash latency for fire-control data. NATO’s Federated Mission Networking initiative compels members to adopt standard waveforms by 2027, thereby accelerating the retirement of legacy fleets.[1]NATO Public Affairs, “Federated Mission Networking,” nato.int Australia proved mesh-networked soldier radios could relay drone imagery directly to infantry, shaving decision loops by 40%. These advances boost demand for anti-jamming and satellite backup channels to protect increasingly valuable data links.

Growing Global Defense Expenditure

World military spending touched USD 2.44 trillion in 2025, a 7.2% nominal rise from 2024, with communications taking a larger share as commanders prioritize information dominance.[2]Stockholm International Peace Research Institute, “World Military Spending Reaches New Record High in 2025,” sipri.org China directed 12% of its USD 296 billion 2025 budget to C4ISR upgrades. India has earmarked USD 4.2 billion for indigenous tactical radios under the Atmanirbhar Bharat initiative. Saudi Arabia and the UAE jointly invested over USD 8 billion to align their networks with those of the US and European forces. Budgetary divergence across Europe, however, leaves some fleets reliant on software patches to extend the life of analog systems.

Demand for Secure, Resilient, High-Throughput Links

Peer adversaries fielding advanced jammers have pushed anti-jamming and low-probability-of-intercept waveforms from optional to baseline requirements. L3Harris delivered AN/PRC-163 radios in 2025 that dynamically select transmission bands, cutting susceptibility to narrowband jamming by 60%. High-definition video from soldier cameras consumes 8 Mbps, outstripping legacy voice-centric links. Militaries are testing millimeter-wave radios that offer gigabit speeds for intra-squad data while supplementing battalion links with satellite or 5G-NTN backhaul.

AI-Driven Cognitive Radios for Dynamic Spectrum Use

Low-Earth-orbit (LEO) constellations now backhaul ISR data when terrestrial networks are degraded. SpaceX won a USD 70 million contract to integrate Starlink terminals with tactical radios, expanding bandwidth for forward units. The US Marine Corps achieved sub-20 millisecond latency on a private LTE range network that supports robotic vehicle telemetry. A 2025 cyberattack on a European satellite provider revealed supply-chain risks, prompting calls for sovereign constellations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum congestion and limited bandwidth allocation | -0.8% | Europe, Asia-Pacific urban areas | Medium term (2-4 years) |

| High cyber-hardening costs under zero-trust mandates | -0.6% | North America, Europe | Short term (≤ 2 years) |

| Export controls and ITAR slow multinational programs | -0.5% | Global | Long term (≥ 4 years) |

| Interoperability issues with legacy analog systems | -0.4% | Nations with aging fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Spectrum Congestion and Limited Bandwidth Allocation

Military radios now contend with shrinking spectrum windows because the International Telecommunication Union reassigned parts of the 3.3-3.8 GHz range to commercial 5G during its 2023 conference, squeezing tactical systems into already crowded UHF channels. Commercial carriers then deployed thousands of urban base stations, which raised the noise floor, forcing militaries to lower their transmit power or risk interference with civilian networks. Japan formalized this approach in 2025 by capping radiated power in city centers, which reduced the effective range of ground radios by 25% and necessitated the addition of relay nodes to maintain coverage. In the US, radio procurement schedules slipped as program offices waited for Federal Communications Commission rulings on whether defense users can keep priority access to the 3.1-3.45 GHz band, clouding waveform design choices for at least two fiscal years.[3]Federal Communications Commission, “FCC Proposes Rules for 3.1-3.45 GHz Band,” fcc.gov Spectrum scarcity also inflates ownership costs; several Middle Eastern defense ministries now pay more than USD 5 million each year for exclusive licenses, diverting funds from equipment upgrades and slowing fleet refresh cycles.

High Cyber-Hardening Costs Under Zero-Trust Mandates

The US Department of Defense (DoD) zero-trust framework requires every tactical radio to encrypt data at rest and in transit, driving extensive software rewrites that add USD 2-5 million per radio family for certification once post-quantum algorithms are integrated.[4]National Institute of Standards and Technology, “NIST Releases First Post-Quantum Cryptography Standards,” nist.gov Vendors must also fund independent penetration testing and continuous vulnerability monitoring, which raises non-recurring engineering bills that disproportionately impact small and midsize suppliers. General Dynamics disclosed that cyber-hardening consumed 18% of its 2025 radio development budget, up from 11% in 2023, shifting internal resources away from new feature development. Europe’s NIS2 Directive amplified the burden by obligating defense contractors to audit every software component in their supply chains, lengthening time-to-market for new models by nine months and tying up engineering talent in compliance tasks rather than innovation. Smaller companies lacking dedicated cybersecurity teams often exit the market or partner with primes, which reduces competitive pressure and may slow price declines for end users.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Space Segment Redefines Resilience

Space platforms added resilience by routing data around jammed or destroyed nodes. The US Space Development Agency's (SDA's) 126-satellite Tranche 1 Transport Layer maintained 98% link availability during simulated attacks, a milestone that underscores the segment's 9.91% CAGR through 2031. In contrast, land platforms retain the largest allocation because infantry, vehicles, and headquarters demand high radio volumes. The 2025 F-35 Block 4 upgrade illustrates how airborne assets enrich multi-domain networks with 274 Mbps data links.

Land systems recorded a 44.76% share in the tactical communication market in 2025; however, budget shifts toward unmanned systems and precision fires are moderating growth. Naval programs focus on ruggedization, as evidenced by Rohde & Schwarz delivering M3SR radios with coatings that increase the mean time between failures to 15,000 hours at sea.[5]Rohde & Schwarz, “Delivers M3SR Tactical Radio to German Navy,” rohde-schwarz.com Overall, diversified platform investment sustains the tactical communication market beyond land force demand.

By Component: Services Surge As Software Defines Capability

Hardware commanded 57.68% of the tactical communication market size in 2025, but the commoditization of RF parts erodes margins. Gallium nitride amplifier unit prices fell from USD 450 in 2023 to USD 320 in 2025 as Asian suppliers entered the field. Services expand at a 7.61% CAGR because waveforms, encryption, and cyber patches now define capability. The US Army spends approximately USD 12 million annually per brigade on Integrated Tactical Network software, more than the hardware cost amortized over the service life.

Software maintenance shifts from depot repairs to over-the-air updates. Elbit Systems launched a cloud portal in 2025 that remotely diagnoses and patches E-LynX radios in 14 nations, lowering sustainment costs while locking customers into long-term contracts. Integration services remain lucrative as militaries customize commercial radios for classified networks, illustrated by BAE Systems’ USD 85 million integration work on the UK’s Bowman replacement.

By Communication Type: Data Overtakes Voice

Data communication captured 41.26% of the tactical communication market share in 2025 as commanders demanded text, imagery, and sensor telemetry that support real-time decision-making. High-throughput SDRs now push situational data to and from dismounted soldiers, armored vehicles, and command posts, replacing legacy voice-centric workflows that struggled with bandwidth constraints. The shift is reinforced by multi-domain operations that rely on blue-force tracking packets and logistics updates to maintain tempo in contested environments. Growth in the data sub-segment is tempered by spectrum congestion and cybersecurity mandates; however, continuous waveform and compression innovations preserve its lead throughout the forecast period.

Video is projected to be the fastest-growing sub-segment, advancing at an 8.49% CAGR from 2026 to 2031 as helmet-mounted cameras, unmanned aerial vehicle (UAV) feeds, and robotic platforms stream high-definition imagery to tactical clouds. Low-Earth-orbit backhaul and private LTE ranges now deliver the gigabit speeds required for live video, while AI-driven codecs reduce bandwidth demand. Adoption accelerates further as after-action reviews and remote medical support depend on real-time visuals rather than text descriptions. However, the surge in video traffic increases the use of electronic signatures, prompting parallel investments in low-probability-of-intercept waveforms and edge processing to mitigate detection risk.

By End User: Homeland Security Acceleration

Defense forces held 79.23% of 2025 revenue, yet homeland security agencies are advancing at an 8.54% CAGR as missions require encrypted, interoperable communications. The US Customs and Border Protection (CBP) deployed 2,400 AN/PRC-163 radios in 2025, trimming response times by 14 minutes during border incidents. Frontex allocated EUR 340 million (USD 396.92 million) to equip guards with military-compatible radios, enabling joint anti-smuggling operations.

Homeland security radios cost an average of USD 4,200, less than half the cost of their military counterparts, reflecting reduced waveform and encryption complexity. Motorola launched a dual-use radio certified for both public safety and the army networks, tapping into demand for devices that straddle defense and civilian standards.

Geography Analysis

North America retained 39.45% market share in 2025 as the US DoD transitioned from procurement to sustainment, focusing on software upgrades over new hardware. The Integrated Tactical Network awarded USD 3.2 billion between 2023 and 2025 and now shifts toward iterative software releases. Canada budgeted CAD 1.8 billion (USD 1.29 billion) for interoperability-focused radios aligned with NORAD missions. Mexico increased tactical radio purchases by 60% to bolster counternarcotics operations.

Asia-Pacific advances at 7.15% CAGR. India’s DRDO fielded indigenous SDR-Tactical Units to 12 battalions, thereby reducing its reliance on imports. Australia’s USD 1 billion Project Land 2072 Phase 2B integrates E-LynX radios with its battle management system for coalition interoperability.

Europe concentrates on NATO-compliant modernization. The UK awarded BAE Systems a contract for the Morpheus program. France has selected Thales Contact radios under an agreement that will deliver through 2030. South America emphasizes border security; Brazil procured 3,200 HF radios for Amazon patrols. The Middle East invests in coalition compatibility; Saudi Arabia ordered USD 420 million in radios and infrastructure, while the UAE deployed E-LynX sets across joint commands. Africa remains a nascent market; South Africa purchased 1,800 radios for its peacekeeping missions.

Regulatory Landscape

Tactical communications procurement increasingly hinges on interoperability and security compliance set by defense standards bodies. In the United States, DoD Instruction 4630.09 and Joint Staff guidance such as CJCSI 6610.01F reinforce interoperability and standards governance for tactical waveforms and data links, including the 2025 removal of legacy Link 11 from the DoD Information Technology Standards Registry. This creates pressure for programs to retire older terminals and align with current joint and coalition requirements.

In Europe, spectrum and satellite policy is moving in parallel with NATO standardization. The United Kingdom implemented The Wireless Telegraphy (Direct to Device Satellite Communications) (Exemption) Regulations 2026 (February 2026), enabling license-exempt direct-to-device satellite services under specified standards, while the European Commission in May 2026 proposed an EU-wide authorization approach for 2 GHz mobile satellite services that reserves a portion of the band for governmental and defense use. On operational standards, NATO has been implementing Federated Mission Networking (FMN) Spiral 4 as a coalition baseline and has been formalizing cellular and non-terrestrial network concepts for defense communications through relevant STANAG activity, tightening compliance expectations for vendors supplying multi-bearer tactical networks.

Value Chain Analysis

The tactical communications value chain runs from specialized RF and semiconductor inputs (including gallium nitride substrates and millimeter-wave components) to radio and terminal design and manufacture, waveform and encryption software development, and systems integration into platforms. It also includes multi-year sustainment and lifecycle cyber updates. Prime contractors typically lead end-to-end delivery and contract with defense and homeland-security buyers, while Tier-1 manufacturers and systems integrators support subassemblies, ruggedization, and platform-specific integration. As capability shifts toward software-defined functions, integration, network management, and maintenance services account for a larger share of total program spend.

Supply resilience and local industrial participation are increasingly visible value-chain features. L3Harris signed an MoU with Kalyani Strategic Systems Limited (KSSL) in February 2025 to collaborate on C4ISR and tactical communications network development in India, aligning product delivery with in-country ecosystem needs. Its March 2025 long-term FOXTROT agreement with the Dutch Ministry of Defence reflects a multi-year route to fielding and sustaining Falcon IV radios. Cross-domain partnerships also connect commercial mobile technology with defense middleware, highlighted by Nokia and blackned GmbH signing an MoU in May 2025 to integrate 5G tactical technology with deployable defense-network software, along with collaborations such as L3Harris with Epirus (publicly described in 2024) that point to demand for integrated, threat-driven capability updates across the chain.

Competitive Landscape

The tactical communication market is moderately concentrated, with the top five vendors, L3Harris Technologies, Inc., RTX Corporation, General Dynamics Corporation, BAE Systems plc, and Northrop Grumman Corporation, capturing a significant share of 2025 revenue. Incumbents leverage their installed bases and long-standing relationships, which impose switching costs, as evidenced by the continued production of the AN/PRC-117G sixteen years after its introduction. Smaller specialists disrupt through modular waveforms and cognitive algorithms. In February 2022, Silvus Technologies secured orders from the US Special Operations Command (USSOCOM) for StreamCaster radios, capable of delivering 100 Mbps at ranges of 10 km. Also, in December 2025, the US DoD's Defense Innovation Unit (DIU) incorporated the StreamCaster 4400 Enhanced (SC4400E) mobile ad-hoc network (MANET) radio to its Blue UAS Framework. This framework is a stringent testing and certification program that greenlights technologies for deployment in US military unmanned aircraft systems (UAS) operations.

The Defense Innovation Unit's 5G-to-Next-G prototypes aim to reduce radio unit costs by 40% by utilizing commercial modems, with trials scheduled for 2026. Patent activity in cognitive radio increased by 32% in 2025; however, defense contractors lag in licensing commercial innovations, creating opportunities for collaboration with companies such as Qualcomm, Ericsson, and Huawei. Emerging IEEE protocols for heterogeneous tactical networks may weaken vendor lock-in after 2030.

Strategic moves highlight portfolio expansion. L3Harris secured a USD 485 million US Army contract for AN/PRC-163 radios in January 2025. Thales and Leonardo formed a joint venture pooling EUR 220 million (USD 256.83 million) into a NATO-compliant SDR platform in March 2025. BAE Systems bought Bohemia Interactive Simulations' tactical division for USD 95 million in May 2025 to couple radios with virtual training environments. Elbit launched a post-quantum encrypted E-LynX-5000 in July 2025, winning a USD 120 million NATO order. Northrop Grumman demonstrated a 10 Mbps broadcast satellite terminal at Valiant Shield in September 2025, securing a USD 310 million production award. General Dynamics received USD 275 million to integrate radios with the Marine Corps' distributed operations in November 2025. Lockheed Martin and RTX invested USD 180 million in a multi-domain gateway targeting Project Convergence 2026.

Tactical Communication Industry Leaders

General Dynamics Corporation

RTX Corporation

BAE Systems plc

L3Harris Technologies, Inc.

Northrop Grumman Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Modernization programs are translating into demand for transport-agnostic tactical networking, where radios, data links, SATCOM terminals, and edge networking kits are bought and upgraded as an integrated system rather than standalone hardware. U.S. service procurement and experimentation provide a direct pull-through. In 2026, the U.S. Army moved Next Generation Command and Control (NGC2) from prototyping to delivery workstreams, and it demonstrated operational uses of private 5G during Lightning Surge 2 (May 2026) while also establishing an NGC2 common data layer baseline (June 2026). Together, these steps broaden the opportunity for vendors that can connect line-of-sight radios, private LTE and 5G, SATCOM, and gateway software into a managed tactical data fabric with security and lifecycle patching.

Coalition interoperability and ongoing investment in data-link and tactical networking hardware and services keep opportunity concentrated around scalable production and support. In January 2026, Data Link Solutions (a BAE Systems and Collins Aerospace joint venture) received a USD 248 million U.S. Navy contract for MIDS JTRS terminals for U.S. and coalition forces, reinforcing the upgrade cycle for interoperable data links. The Navy also placed a USD 96.1 million order in May 2026 for KRAKEN tactical edge networking kits (Fuse Integration), indicating procurement appetite for deployable edge networking beyond radios. In Europe, procurement initiatives oriented to sovereignty and interoperability are being organized alongside EU-level funding mechanisms (SAFE disbursement activity noted in May 2026), supporting vendor strategies built around compliant waveforms, open integration, and regional industrial participation rather than one-off radio buys.

Recent Industry Developments

- July 2026: L3Harris Technologies received U.S. Army delivery orders for NGC2 manpack Falcon systems. The award supports fielding of radio sets designed to operate as nodes in a broader data-centric command-and-control architecture, strengthening L3Harris positioning in brigade-level modernization tied to NGC2.

- May 2026: General Dynamics Mission Systems was awarded a contract modification by the U.S. Air Force for the Next Generation Survival Radio. The work reinforces demand for secure, resilient communications for aircrew and contested-recovery missions, supporting a steady pipeline for specialized tactical radios alongside larger network upgrades.

- January 2026: Data Link Solutions (a joint venture between BAE Systems and Collins Aerospace, RTX) won a USD 248 million U.S. Navy production contract for MIDS JTRS terminals for U.S. and coalition forces. The contract supports coalition interoperability and sustains terminal production programs that connect platforms into joint tactical data networks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the tactical communication market covers secure voice, data, and video communications used in mission settings, where reliability and information security are required. It includes equipment, enabling software, and long-term service support tied to defense and homeland-security use.

Scope exclusions: Commercial push-to-talk devices and broad public-safety radio network infrastructure are excluded from this market sizing.

Segmentation Overview

- By Platform

- Land

- Airborne

- Naval

- Space

- By Component

- Hardware

- Transceivers/Transmitters

- Receivers

- Antennas

- Encryption Devices

- Headsets and Microphones

- Other Hardware

- Software

- Waveform Software

- Encryption Software

- Network Management Software

- Services

- Integration

- Maintenance and Support

- Training

- Hardware

- By Communication Type

- Secure Voice

- Data

- Video

- Other

- By End User

- Defense Forces

- Homeland Security

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Israel

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean fact base around defense communications demand, spending cycles, and procurement patterns. We refer to public sources such as SIPRI defense-expenditure series, NATO burden-sharing and capability releases, World Bank macro indicators for inflation and currency context, ITU spectrum and telecommunications indicators, and US DoD budget justification materials for communications and C4ISR related lines.

Along with these, we also review company annual reports, investor presentations, contract award announcements, and defense ministry press releases to understand where funding is moving (for example, modernization programs, network upgrades, and radio replacement cycles). Select paid subscriptions are used mainly for company financial intelligence, contract and tender tracking, patent lookups, and shipment-level import export checks when public data is thin. These sources are illustrative only, and many other references were used to collect data, confirm assumptions, and resolve open questions.

Primary Interviews and Surveys

Primary work is used to pressure-test what we built from public material, especially on service attachment rates, upgrade timing, and how platforms shift spend between radios, SATCOM terminals, encryption, and network management software. We spoke with a mix of suppliers, integrators, procurement specialists, and defense users across Americas, EMEA, and APAC so regional budgeting differences and program maturity levels could be reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 43% |

| Mid tier: 55% | Functional/Unit leaders: 30% | EMEA: 31% |

| Smaller Players: 17% | Managers: 57% | Americas: 26% |

Market-Sizing & Forecasting

The model begins with a top-down build where defense and homeland-security communications demand is reconstructed from budget signals, program pipelines, and platform-level adoption patterns for secure voice and data networks. Once the demand pool is shaped, results are corroborated with selective bottom-up approximations, like sampled program values, channel checks on typical unit volumes, and ASP ranges for radios, SATCOM terminals, and encryption modules, which are then used to adjust totals where needed.

Inputs used in the sizing and forecast include indicators such as defense spending direction by region, modernization timing for tactical networks, platform mix across land, air, and naval fleets, the shift from analog to software-defined and IP-based systems, and expected service and support attachment over the life of the system. Because not every program discloses full values, gaps are handled using conservative ranges guided by comparable awards, procurement cadence, and expert feedback.

For forecasting, scenario analysis is used so budget variability and procurement delays are reflected without overreacting to one-time contract spikes. Assumptions on growth are anchored to macro conditions, policy priorities, and interview-based consensus on upgrade cycles, followed by a final check that the trend stays consistent with observable procurement momentum.

Data Validation & Update Cycle

Validation is done through repeated cross-checks between the model output and independent signals, including budget lines, contract awards, and timing of major platform upgrades. When a number looks unusual, the assumptions behind volumes, pricing, and service mix are reviewed again, and interviews are re-opened if the variance cannot be explained by a specific event.

Before sign-off, the workbook is reviewed in steps so formulas, conversions, and regional rollups are checked by more than one analyst. Reports are refreshed annually, and interim updates are made when there are material changes such as major procurement shifts, sudden funding revisions, or significant geopolitical events. Right before delivery, a final pass is done so clients receive the most current view available at that time.

Mordor Intelligence's Tactical Communication Market Size Compared Against Other Published Estimates

Published values for tactical communication often do not match because each study draws the market boundary differently and then uses different signals to validate spending. The year used for normalization, how service and support are counted, and the treatment of adjacent public-safety communications can also move the total up or down.

Contract award patterns, defense budget justification lines, and platform modernization schedules are the checks that keep Mordor Intelligence's USD 21.60 B (2025) estimate tied to defense and homeland-security spending on secure voice, data, and video systems. The spread versus other numbers usually comes from counting commercial push-to-talk and wider public-safety networks, or from using a faster ASP progression without verifying it against procurement timing and mix shifts between radios, SATCOM, and encryption.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 21.60 B (2025) | |

| Global Consultancy A | USD 26.20 B (2025) | The estimate appears to use a broader inclusion set across tactical communications, with limited clarity on excluding public-safety network spending, and it may apply more aggressive price and upgrade assumptions across the forecast base. |

| Industry Publisher B | USD 22.30 B (2025) | The figure is close, but scope definitions are less specific on what portion of software and long-term services are counted, and the base-year construction relies more on historical trend framing than on procurement cycle validation. |

Overall, the gap is mostly explained by boundary choices around adjacent communication categories and by how service and software are attached to hardware spend. With clear inclusion rules and repeatable checks against budgets and awards, the final total stays balanced and easier to reconcile year to year.

Key Questions Answered in the Report

What is the projected value of the tactical communication market by 2031?

The tactical communication market is expected to reach USD 31.86 billion by 2031 under a 6.69% CAGR.

Which platform category is growing fastest through 2031?

Space platforms lead growth at a 9.91% CAGR as militaries adopt proliferated low-Earth-orbit constellations for resilient connectivity.

Why are services outpacing hardware in growth?

Continuous waveform, cybersecurity, and software updates drive a 7.61% CAGR for services, reflecting the shift to software-defined capability.

How are homeland security agencies influencing demand?

Homeland security adoption is rising at 8.54% CAGR as agencies require encrypted radios interoperable with defense forces for border and infrastructure security.

What regions present the strongest growth outlook?

Asia-Pacific shows the highest regional CAGR at 7.15% due to indigenous production initiatives in India, Japan, and Australia.

Which technological trend most alleviates spectrum congestion?

AI-driven cognitive radios that autonomously shift frequencies increase spectral efficiency by up to 40% in congested environments.

Page last updated on: