Riflescopes Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

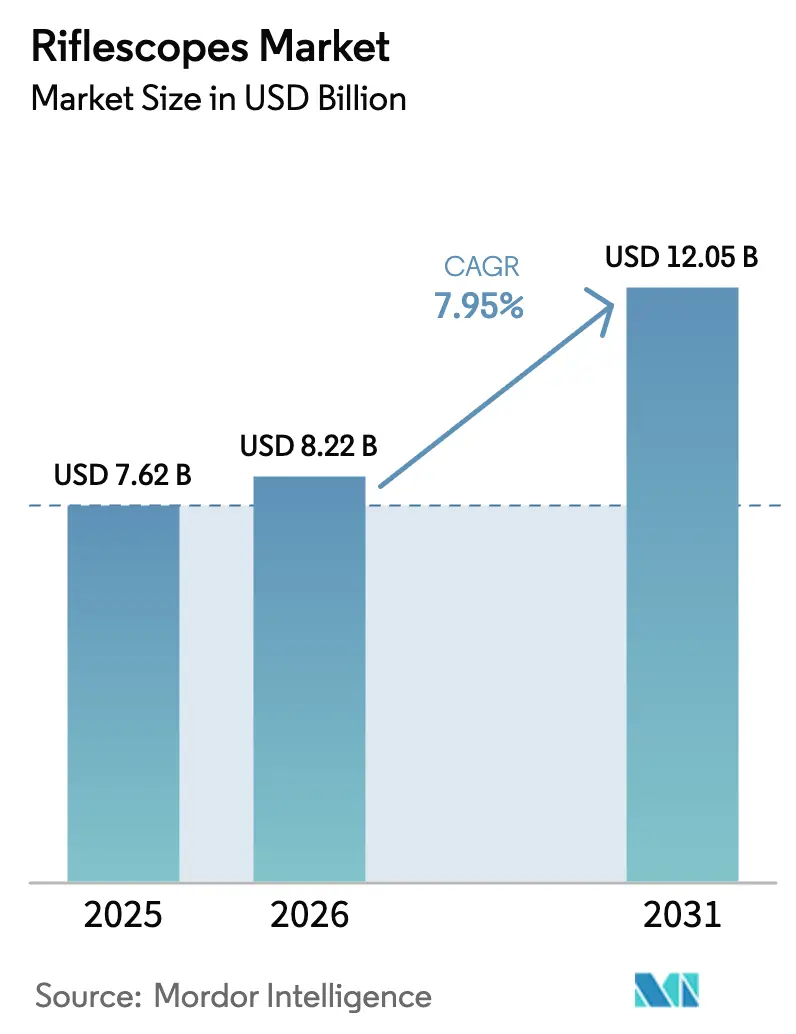

| Market Size (2026) | USD 8.22 Billion |

| Market Size (2031) | USD 12.05 Billion |

| Growth Rate (2026 - 2031) | 7.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Riflescopes Market Analysis by Mordor Intelligence

The riflescopes market size is expected to grow from USD 7.62 billion in 2025 to USD 8.22 billion in 2026 and is forecasted to reach USD 12.05 billion by 2031 at a 7.95% CAGR over 2026-2031. This growth curve is underpinned by an upswing in global defense budgets, resilient participation in recreational shooting, and the accelerated migration from passive glass to digitally enabled fire-control optics. US and allied infantry modernization programs are specifying smart scopes that fuse laser range-finding, environmental sensing, and active reticles, while consumer e-commerce channels are expanding access to mid-tier and premium optics. Simultaneously, falling thermal sensor costs and relaxed night-hunting rules in Europe and several US states are driving the adoption of thermal imaging toward mainstream use. Competitive dynamics reveal that premium incumbents are defending their share through military contracts and warranty differentiation, even as East Asian entrants are compressing price points with feature-rich reflex sights.

Key Report Takeaways

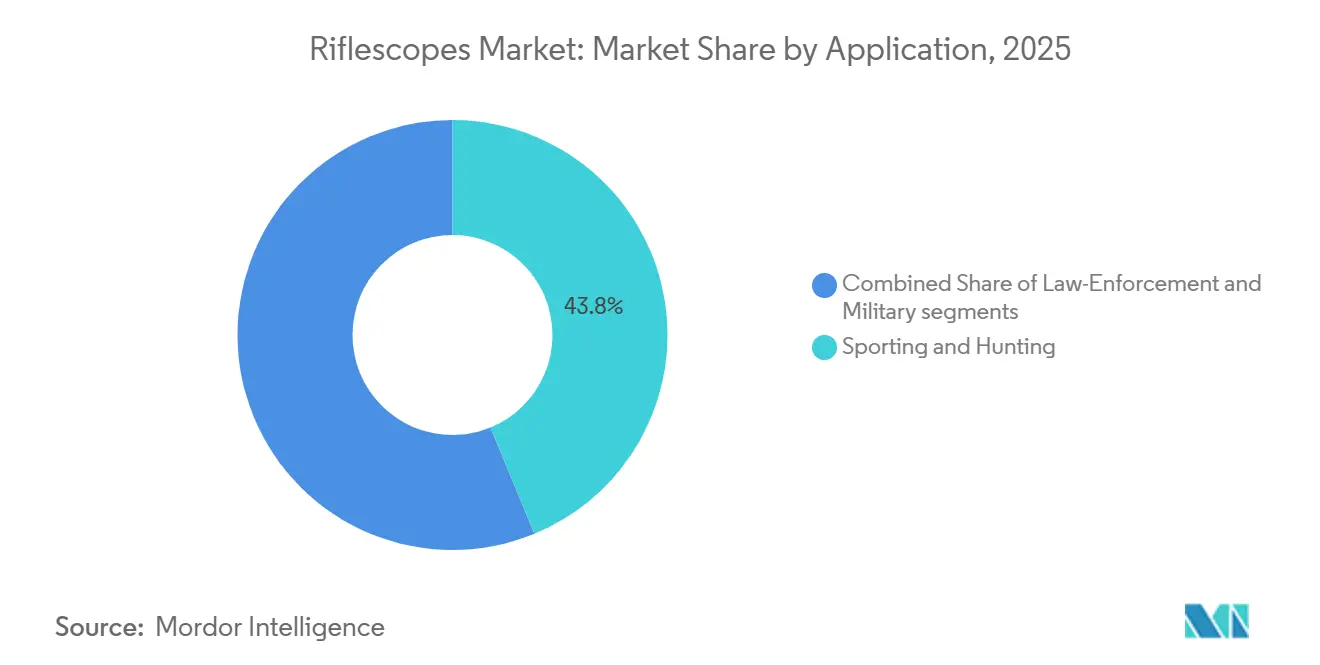

- By application, sporting and hunting led the riflescopes market with 43.78% market share in 2025, while law-enforcement procurement is advancing at a 9.78% CAGR through 2031.

- By sight type, telescopic configurations commanded 74.78% of the riflescopes market in 2025, whereas reflex and red-dot sights are growing at a 10.94% CAGR to 2031.

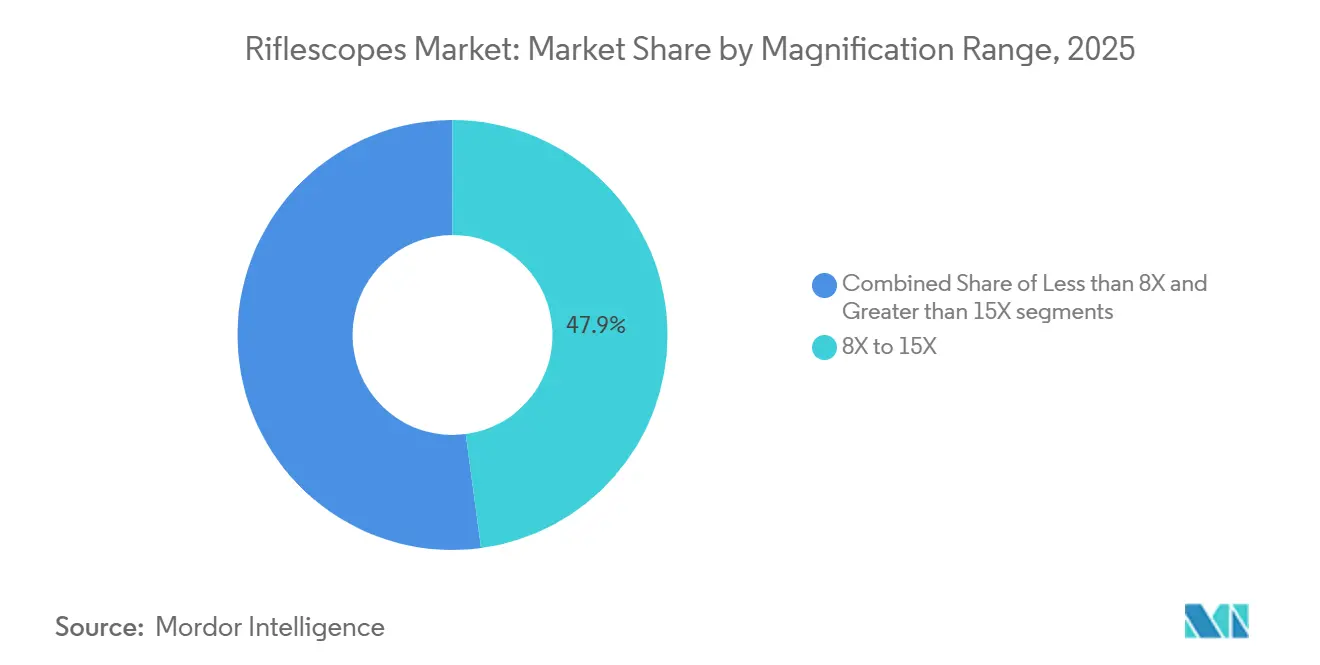

- By magnification range, 8X to 15X optics accounted for 47.89% of the riflescopes market size in 2025, yet scopes above 15X are set to expand at an 8.94% CAGR.

- By technology, electro-optical systems accounted for 51.27% of the riflescopes market share in 2025, with thermal imaging poised to grow at an 8.69% CAGR through 2031.

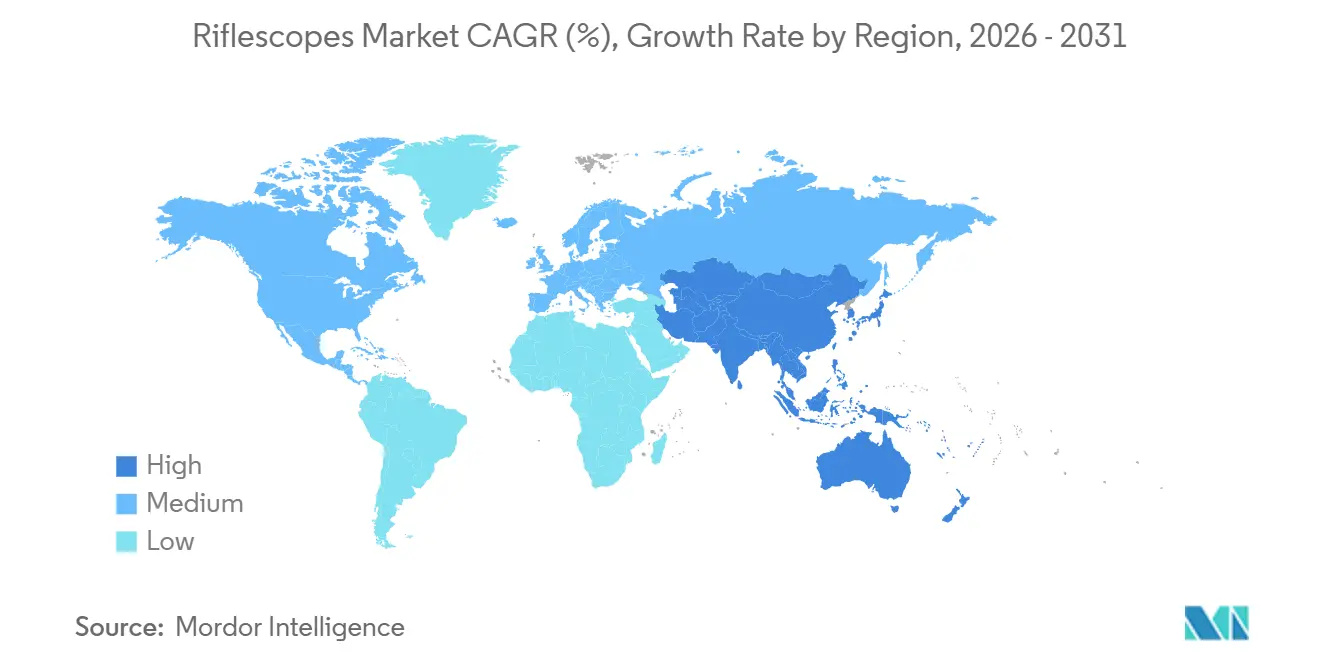

- By geography, North America held 40.12% of the riflescopes market in 2025, whereas Asia-Pacific is forecasted to deliver a 9.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Riflescopes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global defense spending and infantry modernization programs | +1.20% | Global, especially North America and Asia-Pacific | Long term (≥ 4 years) |

| Rapid optical technology upgrades (HD glass, integrated range-finding) | +1.10% | Global | Medium term (2–4 years) |

| Growing participation in recreational shooting sports | +0.80% | North America, Europe | Medium term (2–4 years) |

| Expansion of e-commerce channels for hunting optics | +0.70% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Escalating wild-boar populations driving night-hunting demand | +0.60% | Europe, North America | Medium term (2–4 years) |

| Emergence of AI-enabled “smart rifle” platforms | +0.30% | North America, select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Participation in Recreational Shooting Sports

US target-shooting participation stabilized at 47 million enthusiasts in 2022, creating a dependable upgrade cycle for mid-range and premium scopes.[1]U.S. Fish & Wildlife Service, “2022 National Survey of Fishing, Hunting, and Wildlife-Associated Recreation,” fws.gov Many shooters are transitioning from entry-level 3-9x glass to higher-magnification first-focal-plane models that support precision rifle disciplines. In Europe, Germany’s 1.4 million licensed shooters face recurring permit renewals, motivating them to spend more on optics to maximize the value of a limited firearms fleet. Consequently, the riflescopes market sees robust demand for premium European glass in Central Europe, while North American volume sustains competitive mid-tier brands. Growing female participation and collegiate-shooting programs add new customer cohorts who favor lighter, low-power variable optics. These factors collectively lift average selling prices and unit volumes across the riflescopes market.

Rising Global Defense Spending and Infantry Modernization Programs

World military outlays surged to USD 2,718 billion in 2024, the steepest annual increase since records began, and a sizable portion is earmarked for soldier-borne optics. The US Army’s XM157 program demonstrates a doctrinal appetite for electro-optical fire control systems that blend laser range-finding with atmospheric sensing.[2]Army Technology, “US Army Awards Contract for XM157 Fire Control System,” army-technology.com Allied nations are following suit: Japan lifted its 2025 defense allocation by 16.4%, India is channeling USD 130 billion into domestically designed gear, and Australia’s 2024–2025 budget prioritizes AUKUS-aligned rifle-optic upgrades. Multi-spectral solutions that merge day, thermal, and laser channels are now standard requirements in special-operations solicitations, guaranteeing high-margin follow-on orders for firms with prior NATO stock numbers. These procurement waves not only boost immediate sales but also drive long-tail revenue through spares, training, and lifecycle upgrades.

Rapid Optical Technology Upgrades (HD Glass, Integrated Range-Finding)

HD extra-low-dispersion glass, onboard ballistic computers, and Bluetooth firmware updates have shifted from military exclusivity to mainstream sporting offerings within three years. Leica’s 2024 Calonox Sight features a 640×480 sensor and a 1,700-meter detection range, available for USD 4,500, making thermal imaging accessible to affluent hunters.[3]Leica Camera AG, “Calonox Sight Thermal Riflescope,” leica-camera.com Burris’s Eliminator series auto-illuminates holdover points, eliminating the need for laminated drop charts. Driven by component-cost deflation, FLIR’s 12-micron detectors saw retail monocular prices drop from USD 800 to USD 599 between 2020 and 2024. This price drop enabled value brands to bundle feature-rich electronics for under USD 1,000. In retaliation, premium brands are now extending warranties and emphasizing their distinctive lens coatings. The riflescopes market is now mirroring consumer electronics trends, shifting from a traditional decade-long purchase pattern to shorter replacement cycles.

Expansion of E-Commerce Channels for Hunting Optics

Gross merchandise value at OpticsPlanet reached USD 347 million in 2024, with optics representing roughly 40% of transactions. Direct-to-consumer storefronts help brands like Vortex pocket higher margins; online revenue averaged USD 2.83 million per month in 2024. Digital storefronts also enable the rapid promotion of limited-run military-clone scopes, which fetch premium prices. However, ease of online ordering fuels counterfeit proliferation: Leupold continues to flag fake VX-3 optics on global e-marketplaces. Brands are therefore investing in serialization, blockchain-based provenance, and exclusive online bundles to preserve integrity and differentiate from copycats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent firearm-ownership and hunting regulations | –0.9% | Europe, Canada, parts of Asia-Pacific | Long term (≥ 4 years) |

| Proliferation of low-cost counterfeit scopes from East Asia | –0.6% | North America, Europe | Short term (≤ 2 years) |

| Shift toward unmagnified red-dot sights on modern sporting rifles | –0.8% | North America, Europe | Medium term (2–4 years) |

| Stricter lead-glass environmental directives raising production costs | –0.4% | EU member states | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Stringent Firearm-Ownership and Hunting Regulations

Obtaining a German hunting license requires a 120-hour course and fees exceeding EUR 2,000 (USD 2,328.42), thereby narrowing the pool of potential optics buyers. France levies annual license costs of EUR 150-390 (USD 174.63-454.04) and caps magazine capacity at three rounds, thereby curbing demand for tactical-style scopes. The EU’s 2017/853 directive harmonizes stricter renewals and medical checks, further tightening civilian access.[4]European Union, “REACH Regulation 2015/628,” eur-lex.europa.eu These administrative and financial barriers reduce unit volumes but encourage remaining buyers to opt for high-end optics, thereby cushioning revenue while limiting the expansion of the riflescopes market.

Proliferation of Low-Cost Counterfeit Scopes from East Asia

Leupold’s serial-number look-up reveals a rising share of forgery queries on platforms such as AliExpress, where counterfeit VX-3 models sell for approximately one-quarter of the price of authentic models. The NRA uncovered fake Meprolight and Magpul sights that shattered under recoil, exposing users and agencies to liability. While Holosun’s legitimate USD 159 red-dot blurs price disparities, unchecked counterfeits erode consumer trust. Major brands combat the issue with holographic stickers and online authenticity portals, but enforcement lags due to jurisdictional hurdles. The riflescopes market, therefore, faces margin compression and potential safety recall costs in the entry-level tiers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Law Enforcement Outpaces Legacy Segments

Law enforcement demand for electro-optical and thermal fusion sights is forecasted to grow at a 9.78% CAGR between 2026 and 2031, surpassing the broader riflescopes market. Sporting and hunting still account for 43.78% of the riflescopes market share in 2025, driven by 47 million US recreational shooters and Europe’s 1.5 million licensed hunters. Agency procurements bundle optics with new service rifles, illustrated by a USD 1.29 million NYPD package that included Nightforce scopes. Military contracts remain lumpy yet lucrative; SOCOM’s USD 96 million multi-application scope award in 2024 evidences premium pricing.

The riflescopes market size gains in law enforcement reflect modernization budgets that prioritize low-power variable and clip-on thermal devices for active-shooter scenarios. Sporting optics bifurcate: cost-sensitive buyers opt for scopes under USD 500 from China, while affluent hunters purchase scopes costing USD 2,000 or more. Government sales pipelines favor vendors with GSA schedules and proven durability metrics, creating barriers to entry for newer brands. Consequently, optics makers balancing civilian volume with institutional contracts will capture outsize market share gains in the riflescopes market.

By Sight Type: Reflex Platforms Gain at Telescopic Expense

Telescopic models still accounted for 74.78% of the riflescopes market revenue in 2025; however, reflex and red-dot platforms are projected to grow at a 10.94% CAGR through 2031. Aimpoint’s factory collaboration with Glock introduces enclosed red dots on service pistols, signaling institutional confidence in unmagnified optics. Meanwhile, Holosun’s solar-charging dots, priced at USD 235, reduce maintenance burdens.

Traditional scopes retain the lion’s share of the riflescopes market size for hunting and long-range target sports. Still, entry-level 3X to 9X SKUs are bleeding volume to 1X to 8X low-power variable optics and budget red dots. Market leaders, therefore, diversify with hybrid designs that embed fiber-optic illumination and quick-throw levers to stay relevant. The telescopic segment’s premium sub-category, however, enjoys insulated demand among precision rifle competitors and high-end hunters who value rugged turrets and lifetime warranties.

By Magnification Range: Ultra-Long-Range Gains Traction

Mid-range 8X to 15X optics held a 47.89% market share in the riflescopes market in 2025, striking a balance between versatility and cost. Yet scopes above 15X will expand at an 8.94% CAGR as disciplines like King-of-2-Miles popularize 25X-plus optics. Nightforce’s 5X to 25X civilian variant, priced at USD 2,800-3,200, caters to this surge.

Low-power 1X to 4X and 1X to 6X products grow in absolute terms, but they concede market share as shooters either skip magnification entirely or opt for high-powered glass for ethical long-range shots. Digital overlays, such as Swarovski’s dS Gen II, which compute holdover in real-time, further differentiate ultra-long-range offerings. The riflescopes market therefore stratifies, with distinct buyer segments for dynamic carbine matches, mainstream hunting, and extreme-distance competitions.

By Technology: Thermal Imaging Closes Gap on Electro-Optical

Electro-optical platforms still commanded 51.27% of the riflescopes market share in 2025; however, thermal imaging is advancing at an 8.69% CAGR. FLIR’s Scout TK price cut to USD 599 illustrates sensor cost erosion. Finland’s legal green light for thermal wild-boar hunts accelerates adoption, and Germany’s state derogations add further momentum.

Export-control ceilings cap resolution and frame rate on internationally shipped units, compelling vendors to maintain dual product lines. Nonetheless, thermal clip-ons that preserve existing zero positions are proving popular among hunters invested in premium day scopes. As a result, the riflescopes market size attributed to thermal devices will steadily converge toward that of electro-optical devices over the medium term.

Geography Analysis

North America’s 40.12% of the riflescopes market in 2025 rested on the US’ defense-procurement pipeline and 47 million recreational shooters. The US Army’s XM157 rollout from 2026 ensures recurring spares demand, while SOCOM’s USD 96 million night-scope award in 2024 underscores appetite for multi-spectral systems. Canada’s 8% drop in license sales reflects demographic shifts, yet premium optics sales remain stable due to a committed core of hunters. Mexico’s consumer market is negligible due to stringent ownership rules, which limit optics demand to official agencies.

Asia-Pacific will chart a 9.54% CAGR to 2031, fueled by India’s USD 130 billion defense budget, Japan’s 16.4% spending hike, and Australia’s AUKUS-aligned modernization. South Korea directs part of its USD 44.9 billion allocation to advanced fire-control systems, boosting local optical manufacturing. China’s domestic night-vision market surpassed RMB 1 billion (USD 143.10 million) in 2019 and continues to grow at an annual rate of over 20% backed by localized detector production.

Europe’s riflescopes market expansion is tempered by strict licensing; Germany counts 400,000 hunters, France 1.1 million, and a preference for premium optics that rationalize high compliance costs. Thermal-scope uptake is climbing after Finland’s regulatory shift and Germany’s state derogations, while competitive-shooting circuits in the UK sustain high-magnification demand despite only 710,000 firearm certificates. Beyond Europe, the UAE and Saudi Arabia earmarked USD 28 billion and USD 75.8 billion, respectively, for defense in 2024, with infantry optics high on their procurement lists. South America remains nascent, though Brazil’s regulatory softening modestly lifts law-enforcement optics purchases. Africa’s fragmented economies limit broader adoption, aside from niche hunting-tourism demand in South Africa.

Competitive Landscape

Global market concentration is moderate: the top five players, Leupold & Stevens Inc., Vista Outdoor, Vortex Optics, Burris Company, and Nightforce Optics, account for a significant share, leaving the remaining to a long tail of regional premium houses and price-aggressive Asian entrants. Premium incumbents, such as Leupold, Vortex, and Nightforce, defend their turf with military contracts, lifetime warranties, and high-quality glass, thereby reinforcing pricing power in the USD 1,500-plus bracket. East-Asian challengers like Holosun and HIKMICRO are nibbling away at the entry-level and mid-tier segments by offering solar-charged red dots and sub-USD 1,800 thermal optics.

Strategic moves trend toward vertical integration and direct-to-consumer playbooks. Vortex’s e-commerce channel alone generated nearly USD 34 million in annual online sales, enabling the swift launch of contract-clone optics without involving distributors. Aimpoint’s OEM partnership with Glock places its ACRO P-2 red-dot on factory pistols and guarantees institutional volume. On the technology front, Swarovski’s dS Gen II and Zeiss’s OLED overlays represent the push toward bright optics within the premium tier. Patent filings, including 12 by Vortex and multiple by Leupold from 2022 to 2024, underscore a pivot toward embedded sensors and modular rangefinder add-ons.

Regulatory compliance is emerging as a moat: EU lead-free mandates raise barriers for low-budget producers, while US export-control regimes restrict high-resolution thermal sales, favoring firms with dual product lines. Counterfeit risk persists; however, brands embracing serialization and blockchain provenance gain consumer trust. Overall, the riflescopes market is characterized by accelerated product cycles, higher feature density, and omnichannel sales strategies.

Riflescopes Industry Leaders

Nightforce Optics

Leupold & Stevens, Inc.

Revelyst (Vista Outdoor Operations LLC)

Sheltered Wings, Inc. d/b/a Vortex Optics

Burris Company (Beretta Holding S.A.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Israeli electro-optics company Meprolight (SK Group) was awarded a contract by the armed forces of a Southern European country to provide its MIL-SPEC MVO™ 1–8×28 LPVO riflescopes for short- to mid-range tactical operations.

- July 2025: Aimpoint, in collaboration with GLOCK, announced an exclusive package of the GLOCK x Aimpoint COA™ that will be offered on select 9mm pistols, featuring factory-installed optics utilizing the new Aimpoint A-CUT™ interface.

Global Riflescopes Market Report Scope

The riflescopes market comprises optical and electro-optical sighting devices designed to enhance aiming precision, target acquisition, and engagement range. These devices are used in civilian, law enforcement, and military applications. The market encompasses telescopic scopes, reflex/red-dot sights, and advanced systems that feature thermal imaging, laser, and digital technologies.

The riflescopes market is segmented by application, sight type, magnification range, technology, and geography. By Application, the market is segmented into sporting and hunting, law enforcement, and military. By sight type, the market is segmented into telescopic and reflex/red-dot. By magnification range, the market is segmented into less than 8X, 8X to 15X, and greater than 15X. By technology, the market is segmented into electro-optical, thermal imaging, and laser. The report also covers the market sizes and forecasts for the riflescopes market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Sporting and Hunting |

| Law-Enforcement |

| Military |

| Telescopic |

| Reflex/Red-Dot |

| Less than 8X |

| 8X to 15X |

| Greater than 15X |

| Electro-Optical |

| Thermal Imaging |

| Laser |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Sporting and Hunting | ||

| Law-Enforcement | |||

| Military | |||

| By Sight Type | Telescopic | ||

| Reflex/Red-Dot | |||

| By Magnification Range | Less than 8X | ||

| 8X to 15X | |||

| Greater than 15X | |||

| By Technology | Electro-Optical | ||

| Thermal Imaging | |||

| Laser | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the riflescopes market in 2026 and how fast will it grow?

The riflescopes market size reached USD 8.22 billion in 2026 and is forecasted to grow at a CAGR of greater than 7.95%, hitting USD 12.05 billion by 2031.

Which application will add the most new revenue through 2031?

Law-enforcement agencies are projected to outpace all other segments with a 9.78% CAGR as they replace legacy glass with thermal-capable and rapid-acquisition optics.

What technology trend is reshaping product portfolios the fastest?

Thermal imaging is advancing at an 8.69% CAGR thanks to sensor cost declines and regulatory changes allowing night-hunting in Europe and parts of the US.

Which region offers the strongest growth outlook?

Asia-Pacific is expected to post a 9.54% CAGR, fueled by rising defense budgets in India, Japan, South Korea, and Australia.

How are brands protecting themselves against counterfeit optics?

Leading manufacturers now embed serial-number lookup tools, holographic seals, and blockchain-based provenance systems to help consumers verify authenticity and safeguard brand equity.

Why are red-dot sights challenging traditional low-power scopes?

Competitive shooting rules, law-enforcement preferences, and aggressive USD 159–USD 300 pricing from Asian suppliers have shifted demand toward unmagnified reflex sights for engagements within 100 meters.

Page last updated on: