T-cell Immunotherapy Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

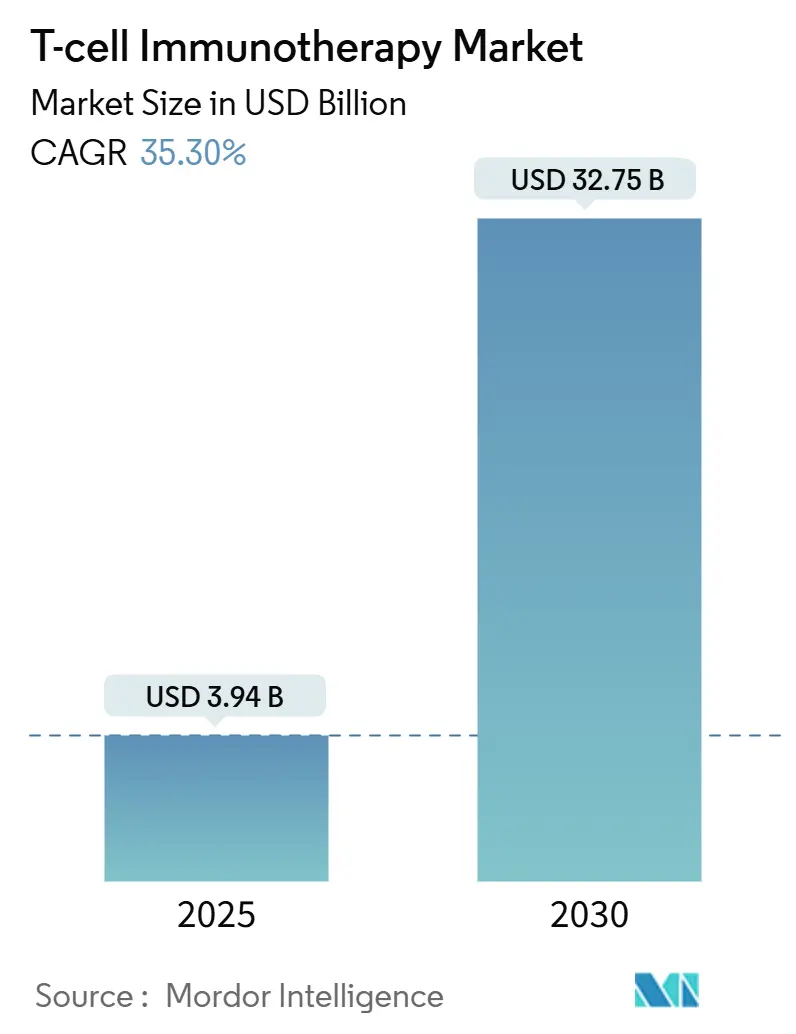

| Market Size (2025) | USD 3.94 Billion |

| Market Size (2030) | USD 32.75 Billion |

| Growth Rate (2025 - 2030) | 35.30% CAGR |

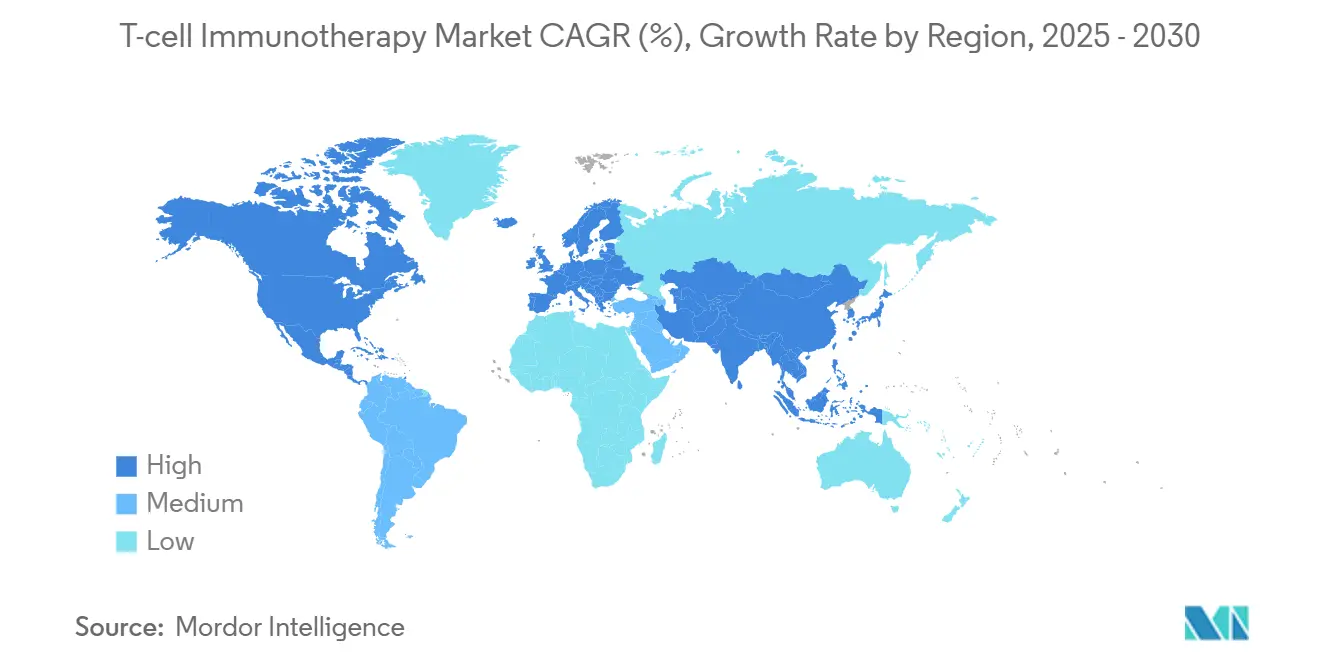

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

T-cell Immunotherapy Market Analysis by Mordor Intelligence

The T-cell immunotherapy market size stood at USD 3.94 billion in 2025 and is forecast to climb to USD 32.75 billion by 2030, translating into a 35.33% CAGR through the period. This expansion reflects escalating adoption in oncology, earlier-line approvals, and accelerated reimbursement pilots that collectively widen patient eligibility. Clinical momentum is shifting beyond B-cell malignancies as engineered platforms penetrate solid tumor settings, while automation improves lot-to-lot reproducibility and compresses production lead times. Regulatory convergence between the U.S. Food and Drug Administration and the European Medicines Agency further lowers development friction, and value-based contracts start to temper payer concerns around six-figure list prices. Competitive intensity is sharpening as manufacturers double down on allogeneic pipelines, integrate gene-editing safeguards, and consolidate capacity through long-term CDMO reservations, all of which position the T-cell Immunotherapy market for sustained double-digit growth.

Key Report Takeaways

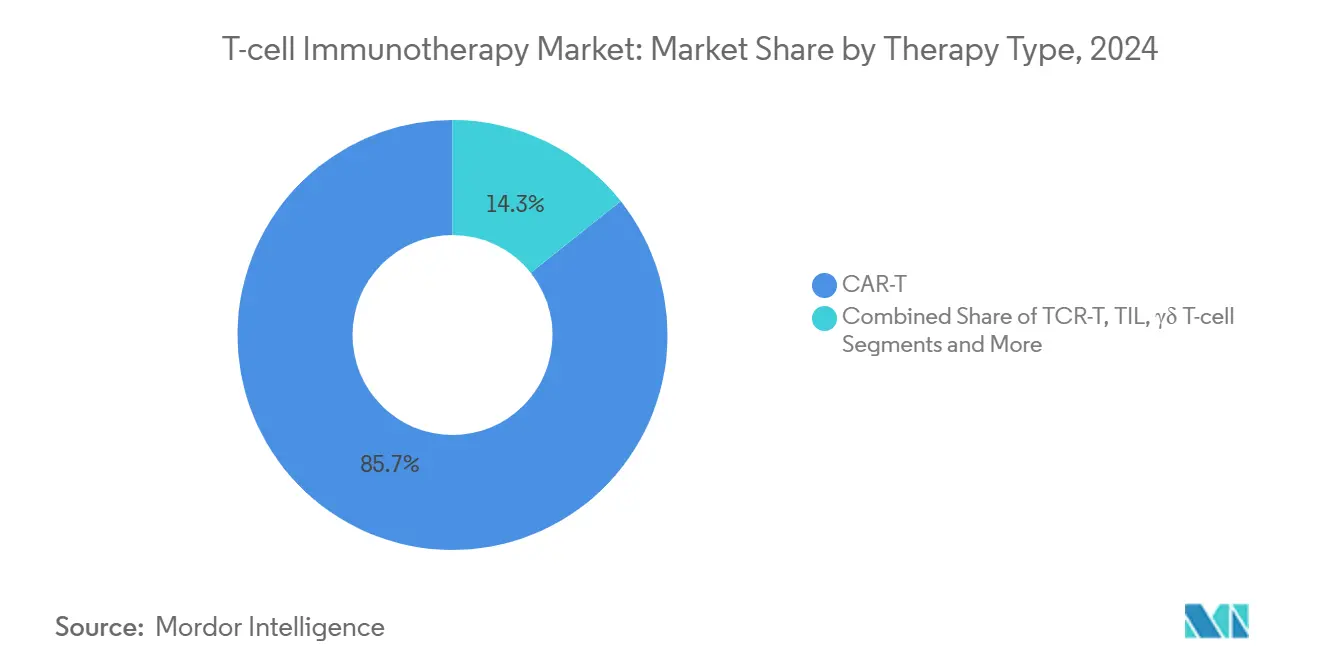

- By therapy type, chimeric antigen receptor T cells accounted for 95.7% of the T-cell immunotherapy market share in 2024, while allogeneic constructs are advancing at a 32.6% CAGR between 2025 and 2030.

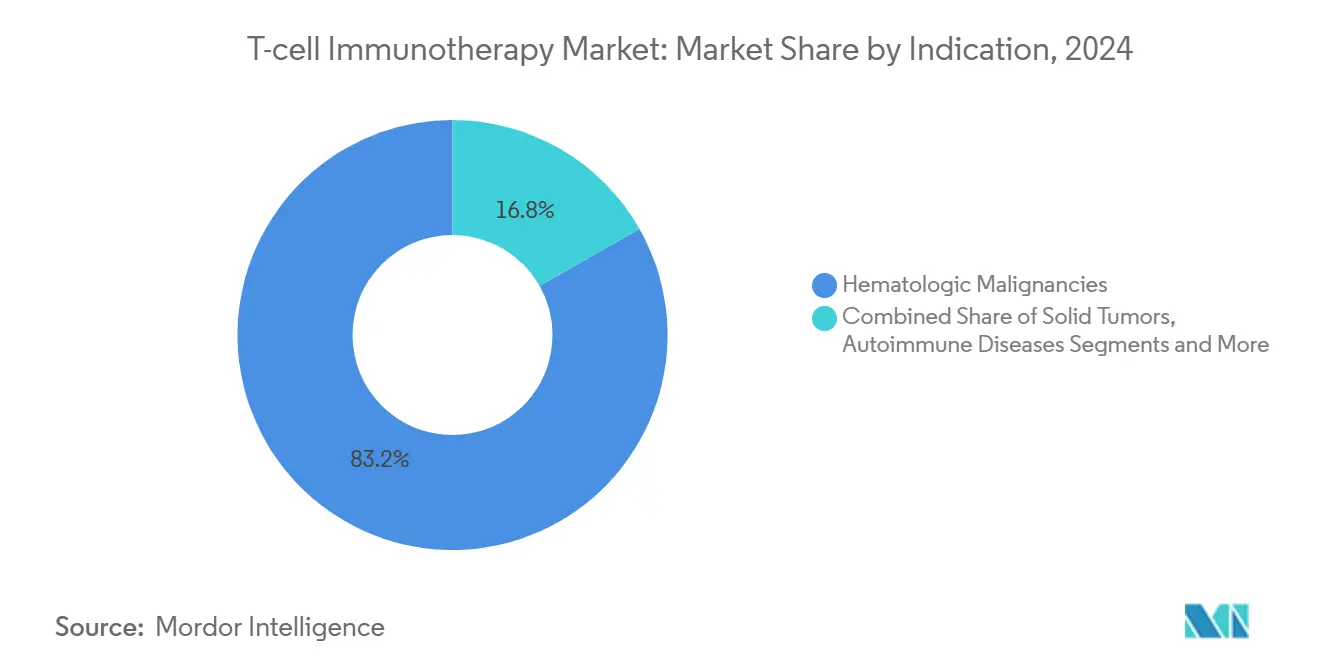

- By indication, hematologic disorders held 83.2% of the T-cell immunotherapy market size in 2024; solid tumors are on track to rise at a 35.4% CAGR to 2030.

- By geography, North America led with 53.4% of the T-cell immunotherapy market share in 2024, whereas Asia-Pacific is poised to register a 25.2% CAGR through 2030.

Global T-cell Immunotherapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing global cancer burden and aging population | +8.20% | Global with highest impact in North America & Europe | Long term (≥ 4 years) |

| Expanding indications and label extensions for T-cell therapies | +6.80% | Global led by U.S. FDA & EMA | Medium term (2-4 years) |

| Favorable regulatory pathways and accelerated approval programs | +5.40% | North America & EU expanding to APAC | Short term (≤ 2 years) |

| Increasing investment in cell and gene therapy infrastructure | +4.90% | Global concentrated in U.S., China, Germany | Medium term (2-4 years) |

| Technological advances in cell engineering and manufacturing automation | +3.80% | Global led by U.S. & European hubs | Medium term (2-4 years) |

| Strategic collaborations across pharma, biotech, and academia | +2.90% | Global concentrated in major markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Global Cancer Burden and Aging Population

Cancer incidence is rising fastest in economies with limited trial infrastructure, leaving large swaths of eligible patients untreated despite robust clinical proof of concept.[1]Stanley Hamilton, “Phase 1 Clinical Trials: Challenges and Opportunities in Latin America,” Journal of Immunotherapy and Precision Oncology, allenpress.com In the United States and Europe, aging populations disproportionately present with hematologic malignancies that align well with autologous and allogeneic CAR-T targets. China hosts the world’s largest oncology patient cohort and already sponsors more than 300 active CAR-T trials, vaulting the country into a leadership position alongside the United States. Latin American markets illustrate the mismatch between need and access, with a projected 66% uptick in cancer cases by 2040, yet only 4% of global oncology trials occur locally. Across regions, the persistent demographic tailwind guarantees continued demand for curative-intent modalities, underpinning the long-run trajectory of the T-cell immunotherapy market.

Expanding Indications and Label Extensions for T-Cell Therapies

The U.S. FDA approved afamitresgene autoleucel for metastatic synovial sarcoma in 2024, the first T-cell receptor product to break through the solid tumor ceiling.[2]U.S. Food and Drug Administration, “FDA Eliminates Risk Evaluation and Mitigation Strategies (REMS) for Autologous CAR-T Cell Immunotherapies,” fda.gov Subsequent approvals are trending toward earlier therapy lines, broadening the treatable population by close to half compared with later-line restrictions. Pipeline programs targeting lupus and other autoimmune disorders showcase the modality’s versatility, signaling future diversification beyond oncology. Allogene Therapeutics’ IND submission for ALLO-329 in systemic autoimmune disease exemplifies this frontier. Harmonized ISO and GMP frameworks now guide label expansion, ensuring that safety surveillance scales in lockstep with new indications. Together, these factors enlarge the T-cell immunotherapy market and intensify competition for first-mover advantage in non-traditional disease spaces.

Favorable Regulatory Pathways and Accelerated Approval Programs

The CoGenT Global pilot formalizes cross-agency collaboration that streamlines filing requirements and compresses review cycles, a boon to sponsors juggling multiregional submissions. RMAT and PRIME designations shorten clinical development timelines, while the June 2025 removal of REMS for autologous products cuts operational overhead for infusion centers, especially in rural settings. Regulators anticipate 10-20 new approvals annually by 2025, a volume that reinforces the T-cell immunotherapy market as one of the fastest-growing segments in biopharma. Collectively, these policies shape a regulatory environment that encourages innovation while safeguarding patient welfare, contributing directly to sustained high-thirty-percent CAGR projections.

Increasing Investment in Cell and Gene Therapy Infrastructure

Bristol Myers Squibb locked in a USD 380 million capacity reservation with Cellares to leverage the Cell Shuttle platform, highlighting the pivot toward automated, closed systems that lower contamination risk and drive batch-over-batch consistency. Meanwhile, Gilead Sciences is on track to quadruple CAR-T output by 2026, fueled by strategic facility expansions and modular suites. High-density microfluidic bioreactors are pushing yields beyond traditional static cultures, trimming the cost of goods and making the economics of the T-cell immunotherapy market more defensible. These infrastructure infusions address chronic slot shortages and shorten vein-to-vein intervals, thereby enhancing the commercial viability of autologous products while preparing the field for scalable allogeneic launches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment costs and an uncertain reimbursement landscape | -4.10% | Global most acute in emerging markets | Medium term (2-4 years) |

| Complex manufacturing supply chains and capacity constraints | -3.70% | Global is concentrated in specialized sites | Short term (≤ 2 years) |

| Safety concerns, including cytokine release syndrome and neurotoxicity | -2.80% | Global with regulatory focus in the U.S. & EU | Long term (≥ 4 years) |

| Competitive pressure from alternative immunotherapy modalities | -2.20% | Global is the most intense in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Uncertain Reimbursement Landscape

List prices averaging USD 300,000-USD 4.25 million per treatment impede uptake in both public and private health systems.[3]IPG Health, “Million-Dollar Medicine: Insights on Payer Management of Cell and Gene Therapies,” ipghealth.com The U.S. Cell and Gene Therapy Access Model initiates outcomes-based agreements in 2025, but operational complexity and data-tracking requirements have slowed early adoption. Europe anticipates cumulative expenditures of EUR 28.5 billion (USD 31 billion) over five years, pressuring budgets and widening cross-border access gaps. In China, limited reimbursement leaves most patients reliant on personal savings, slowing conversion from clinical trial participation to commercial therapy. At the same time, value-based pricing pilots and installment schemes show promise; widespread implementation hinges on coordinated policy reforms.

Complex Manufacturing Supply Chains and Capacity Constraints

Autologous workflows take three to five weeks from leukapheresis to infusion, forcing clinicians to administer bridging chemotherapy that can blunt therapeutic impact. CDMOs still run below 50% commercial utilization, underscoring the imbalance between clinical demand and industrial capacity. Multi-step quality control, including mycoplasma and sterility testing, adds days to release timelines and increases the probability of batch failure. Cryogenic transport is logistically intricate, particularly for transcontinental shipments to low-and middle-income countries. Although decentralized and automated systems promise relief, substantial capital and regulatory harmonization are prerequisites.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Allogeneic Surge Redraws CAR-T Leadership

Autologous CAR-T products such as Kymriah and Yescarta drove a combined 95.7% of the T-cell immunotherapy market share in 2024, anchoring the segment with strong remission durability in B-cell malignancies. The T-cell immunotherapy market size for autologous constructs is projected to climb at a high-twenties CAGR, yet manufacturing limitations cap absolute volume growth. Allogeneic CAR-T approaches now exhibit a 32.6% CAGR through 2030, propelled by CRISPR- and base-edited platforms that neutralize graft-versus-host concerns. Hospitals prize these off-the-shelf lots for immediate availability, a trait that aligns with acute oncology timelines. Clinical evidence, such as ALLO-501’s 58% overall response rate in large B-cell lymphoma, showcases efficacy parity with autologous peers.

Allogeneic scalability addresses back-end bottlenecks that currently restrict infusion slots to a minority of eligible patients, notably outside major urban centers. As closed-system bioreactors and automated fill-finish suites come online, per-patient manufacturing costs are expected to fall, improving the addressable base within the T-cell immunotherapy market. Regulatory agencies are acclimating to allogeneic data packages, granting RMAT and similar designations that carve expedited routes to market. Innovation in safety switches, such as suicide genes and ligand-induced dimerization domains, further boosts confidence among payers and clinicians. Collectively, these trends position allogeneic products to recalibrate competitive hierarchies by the latter half of the decade.

By Indication: Hematologic Stronghold Meets Solid Tumor Upside

Hematologic malignancies retained 83% of the T-cell immunotherapy market share in 2024, buoyed by validated antigens like CD19, BCMA, and CD22 that translate into predictable manufacturing outputs and robust complete response rates. Early-line approvals in multiple myeloma and diffuse large B-cell lymphoma expand absolute patient pools and extend duration-of-treatment benefits. Consequently, the T-cell immunotherapy market size tied to blood cancers remains the revenue backbone for near-term cash flows.

Solid tumors record the fastest trajectory at a 35.4% CAGR through 2030, catalyzed by the Tecelra approval in synovial sarcoma and a surge of tumor-microenvironment-modulating construct designs. Nano-body-based CARs and armored T cells aim to dismantle immunosuppressive barriers and improve trafficking into dense tumor matrices. Positive early signals in renal cell carcinoma and glioblastoma support a widening pipeline, while local delivery methods such as hepatic artery infusions tackle on-target off-tumor toxicity concerns. Breakthrough designations in rare epithelial cancers leverage orphan incentives to accelerate development, broadening the potential contribution of solid tumors to the overall T-cell immunotherapy market by decade’s end.

Geography Analysis

North America retained 53.4% of the T-cell immunotherapy market share in 2024 on the back of the FDA’s agile review structures, Medicare add-on payments, and a dense network of certified infusion sites. The region also hosts the majority of commercial-scale GMP facilities, enabling domestic sourcing that sidesteps customs delays. Canada and Mexico add incremental volume through cross-border clinical trial participation and early access programs, though reimbursement heterogeneity persists across provinces and states.

Asia-Pacific displays the fastest 25.2% CAGR, fueled by China’s pro-innovation policies, more than 300 active CAR-T trials, and provincial approvals that precede national listing. Japan’s fast-track regenerative medicine law compresses review timelines to under one year, while South Korea offers tax credits for GMP build-outs. India’s green light for talicabtagene autoleucel, combined with public-private manufacturing hubs, illustrates emerging-market potential to widen the T-cell immunotherapy market size for middle-income populations.

Europe posts moderate growth amid EMA harmonization but faces variable country-level uptake; France achieves roughly 30% penetration among eligible hematologic cases compared with Italy’s 11%. The GoCART Coalition addresses affordability head-on by decentralizing production across academic nodes, a model that could cut per-dose costs by half. Meanwhile, Brazil demonstrates a disruptive low-cost template at USD 35,000 per dose, spotlighting South America as a future swing territory for access expansion. Collectively, these regional narratives demonstrate how regulatory agility, manufacturing ingenuity, and financing innovations interact to shape geographic penetration of the T-cell immunotherapy market.

Competitive Landscape

The T-cell immunotherapy market shows moderate concentration anchored by five multinational firms that collectively control more than 70% of global revenue. Novartis leverages first-mover advantage with Kymriah’s multicenter label, while Gilead’s Yescarta races ahead in volume based on capacity scaling plans and an expanding diffuse large B-cell lymphoma label. Bristol Myers Squibb’s Breyanzi gains ground through sequential approvals and an automated production upgrade. In contrast, Johnson & Johnson’s Carvykti is now the second-largest CAR-T seller on the strength of stringent minimal residual disease data.

Mid-cap innovators focus on allogeneic disruption; Allogene Therapeutics, CRISPR Therapeutics, and Cellectis amass intellectual property in gene editing and immune evasion. Big pharma hedge bets via equity stakes and multi-billion-dollar option deals, evidenced by BioNTech’s USD 200 million minority investment in Autolus and AbbVie’s USD 1.44 billion milestone-laden tie-up with Umoja. Manufacturing is the principal battleground, with automated shuttles and closed-system bioreactors shortening lead times and improving lot success rates. Academic institutions, armed with hospital exemption carve-outs, further democratize access by offering cost-based products that pressure commercial price ceilings. These dynamics collectively sharpen the competitive contours of the T-cell immunotherapy market and catalyze ongoing R&D diversification.

T-cell Immunotherapy Industry Leaders

Novartis AG

Gilead Sciences

Bristol Myers Squibb

Johnson & Johnson

Iovance Biotherapeutics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The FDA approved Aucatzyl (obecabtagene autoleucel) for adults with relapsed/refractory B-cell acute lymphoblastic leukemia, achieving a 63% complete remission rate.

- February 2025: Cellectis reported positive Phase 1 data for UCART22 and UCART20x22, both receiving dual Orphan Drug Designations.

- February 2024: BioNTech and Autolus unveiled a USD 250 million CAR-T collaboration that includes a USD 200 million equity investment.

Global T-cell Immunotherapy Market Report Scope

| CAR-T |

| TCR-T |

| TIL |

| ?? T-cell |

| Others (CAAR-T, MILs) |

| Hematologic Malignancies |

| Solid Tumors |

| Autoimmune Diseases |

| Viral Infections |

| Others (Rare Cancers) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | CAR-T | |

| TCR-T | ||

| TIL | ||

| ?? T-cell | ||

| Others (CAAR-T, MILs) | ||

| By Indication | Hematologic Malignancies | |

| Solid Tumors | ||

| Autoimmune Diseases | ||

| Viral Infections | ||

| Others (Rare Cancers) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the T-cell Immunotherapy market forecast to grow through 2030?

The market is projected to post a 35.33% CAGR, reaching USD 32.75 billion by 2030.

Which therapy type leads current commercial revenue?

Autologous CAR-T products dominate with 95.7% share, but allogeneic constructs are the fastest-growing sub-segment.

What region will see the highest growth?

Asia-Pacific is expected to expand at a 25.2% CAGR as China, Japan, and South Korea accelerate approvals and capacity build-outs.

Why are costs such a significant hurdle for broader access?

List prices from USD 300,000 to USD 4.25 million strain payer budgets, and reimbursement frameworks remain inconsistent, particularly in emerging markets.

Which safety issues receive the most regulatory scrutiny?

Cytokine release syndrome and neurotoxicity remain top concerns, prompting extended post-marketing surveillance and specialized ICU readiness.

What technological shift could redefine manufacturing economics?

Automated, closed-system bioreactors and gene-edited allogeneic platforms aim to cut production costs and offer off-the-shelf availability.

Page last updated on: