Novel T-Cell Immunotherapy Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

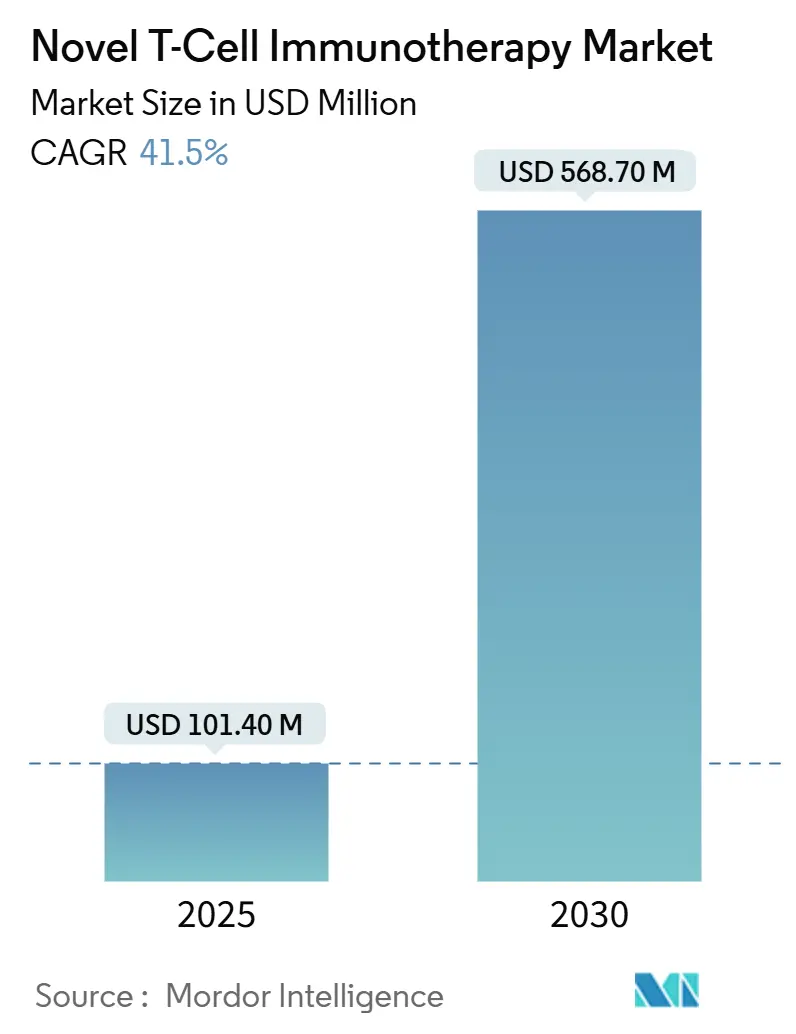

| Market Size (2025) | USD 101.40 Million |

| Market Size (2030) | USD 568.70 Million |

| Growth Rate (2025 - 2030) | 41.50% CAGR |

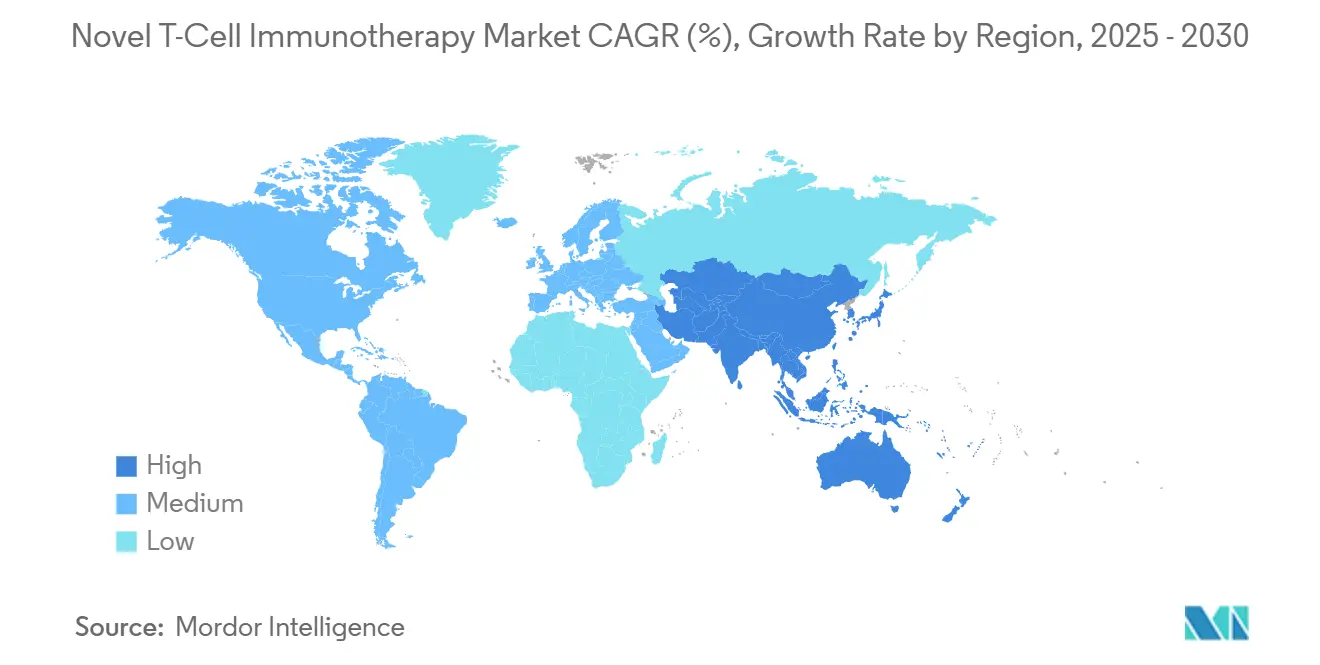

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Novel T-Cell Immunotherapy Market Analysis by Mordor Intelligence

The novel T-cell immunotherapy market size is expected to reach USD 101.4 million by 2025. It is forecast to reach USD 568.7 million by 2030, reflecting a steep 41.5% CAGR that underscores the sector's shift from experimental regimens to commercially scalable treatments. Breakthrough regulatory approvals, expanding clinical applications in autoimmunity and solid tumors, and accelerating investment in automated manufacturing are reshaping competitive dynamics. CAR-T platforms remain the revenue cornerstone, yet allogeneic, off-the-shelf approaches are gathering momentum as they resolve capacity bottlenecks tied to patient-specific production. North America continues to anchor demand, thanks to favorable reimbursement pathways, while the Asia Pacific's reform-driven clinical pipeline delivers the fastest regional growth. Manufacturing automation is beginning to compress costs and cycle times, positioning cell therapies for broader adoption once current reimbursement frictions ease.

Key Report Takeaways

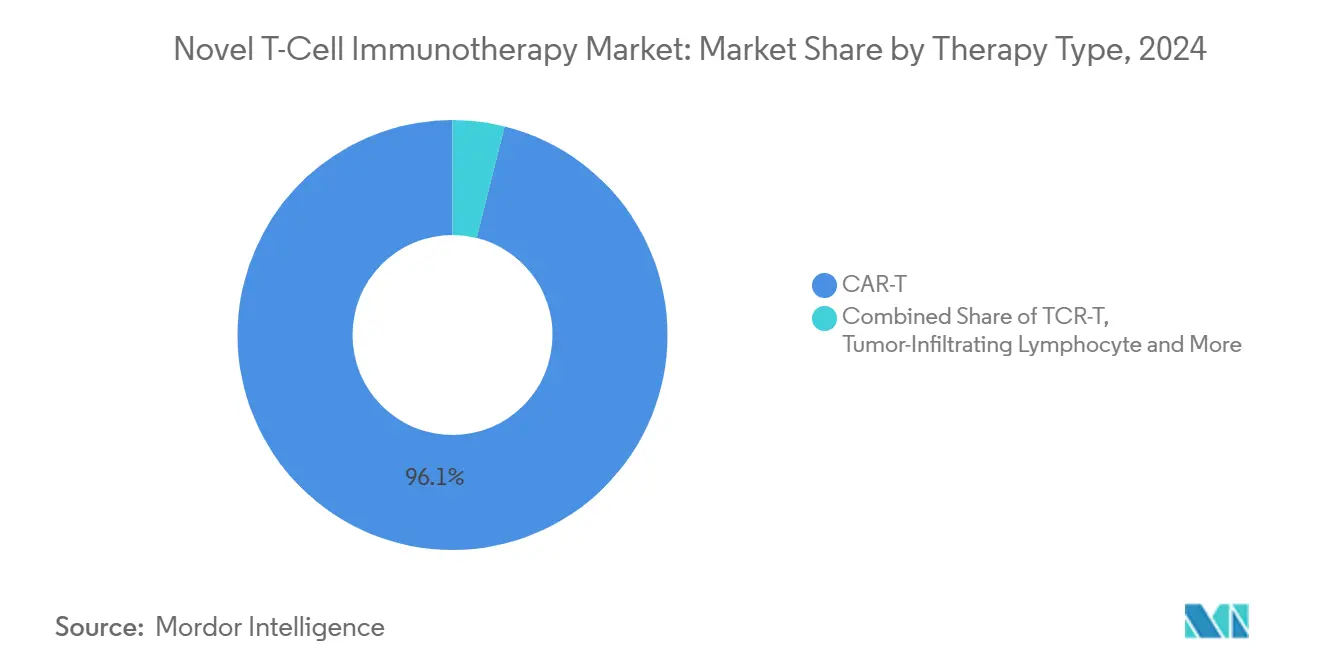

- By therapy type, CAR-T retained 96.1% of the novel T-cell immunotherapy market share in 2024, whereas allogeneic platforms are projected to expand at a 41.5% CAGR to 2030.

- By cell source, autologous products held 93.4% of the novel T-cell immunotherapy market share in 2024; allogeneic counterparts are expected to pace growth with a 38.9% CAGR through 2030.

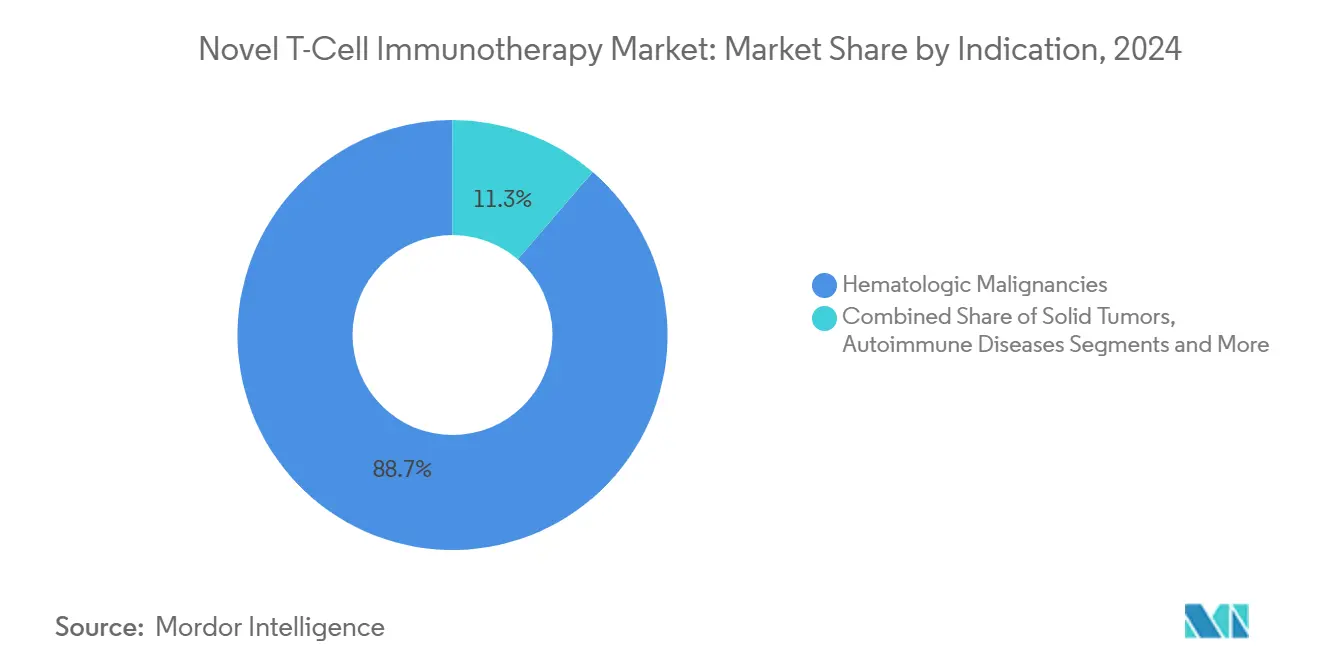

- By indication, hematologic malignancies commanded 88.7% revenue share in 2024, while autoimmune applications are forecast to post a 38.7% CAGR to 2030.

- By geography, North America led the novel T-cell immunotherapy market with 60.2% of the market size in 2024; the Asia Pacific is advancing at a 30.5% CAGR through 2030.

Global Novel T-Cell Immunotherapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory tailwinds via accelerated approval and RMAT/PRIME designations | +8.2% | North America, EU | Short term (≤ 2 years) |

| Rapid expansion of the late-stage clinical pipeline across oncology and autoimmunity | +7.5% | Global, APAC surge | Medium term (2-4 years) |

| Breakthroughs in gene-editing and cell-manufacturing platforms are boosting efficacy and yield | +6.8% | North America, EU | Medium term (2-4 years) |

| Strategic capital inflows and global partnerships scaling commercialization | +5.9% | Global biotech hubs | Short term (≤ 2 years) |

| Increasing the healthcare system's willingness to pay for curative one-time therapies | +4.7% | North America, EU | Long term (≥ 4 years) |

| Geographic expansion of accredited treatment centers is improving patient access | +3.4% | APAC and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory tailwinds via accelerated approval and RMAT/PRIME designations

The FDA’s RMAT pathway compressed standard review cycles to as little as eight months, with 25 designations granted as of March 2025.[1]Center for Biologics Evaluation and Research, “CBER RMAT Approvals,” fda.gov Early dialog sessions allow sponsors to refine trial endpoints, aligning clinical packages with expedited approval requirements. Parallel EMA PRIME designations improve harmonization across the United States and Europe, reducing duplicative trials and accelerating multinational launches. These programs shorten cash-burn periods for developers and derisk investor capital, which in turn fuels earlier entry of novel modalities such as iPSC-derived therapies. As other agencies adopt similar fast-track tools, the novel T-cell immunotherapy market benefits from synchronized global time-to-market gains.

Rapid expansion of the late-stage clinical pipeline across oncology and autoimmunity

More than 85 CRISPR-enabled trials were enrolling in 2025, a 340% rise over 2020 baselines.[2]ScienceDirect, “Automated Manufacturing of Cell Therapies,” sciencedirect.comSolid tumor milestones—most notably the FDA approval of Adaptimmune’s engineered TCR-T for synovial sarcoma—demonstrate widening therapeutic breadth. Autoimmune efforts are equally robust; early-phase CAR-T studies in systemic lupus erythematosus have reported sustained B-cell depletion lasting 12 months or longer. The surge in trial volume is attracting contract manufacturing organizations to build regional capacity, enabling faster vein-to-vein logistics. Collectively, a richer pipeline lays the groundwork for the novel T-cell immunotherapy market to reach a broader patient pool within the decade.

Breakthroughs in gene-editing and cell-manufacturing platforms are boosting efficacy and yield

Automation platforms such as Cellares’ Cell Shuttle have recorded 760% throughput gains and 30% cost reductions compared with legacy manual suites. Base-editing technologies further elevate safety by curtailing off-target mutations, addressing persistent regulatory concerns. Closed-system hardware integrates expansion, editing, and quality control in a single unit, lowering contamination risk and maintaining batch consistency. These advances unlock the capacity to satisfy future demand while pushing pricing trajectories downward. Over time, manufacturing efficiency is expected to drive market penetration into cost-sensitive healthcare systems.

Strategic capital inflows and global partnerships scaling commercialization

Industry-wide deal momentum remains strong: Roche acquired Poseida Therapeutics for USD 1.5 billion in November 2024, and AstraZeneca signed a USD 2.2 billion alliance with Cellectis the same quarter. Venture capital remains active in automation, illustrated by AvenCell’s USD 112 million Series B led by Novo Holdings. Big Pharma alliances expedite tech-transfer of emerging platforms into GMP settings, compressing commercialization timelines. Cross-border partnerships facilitate knowledge sharing and regulatory familiarity, accelerating approvals in newly receptive jurisdictions. Capital availability consequently sustains the scale-up ambitions underpinning the novel T-cell immunotherapy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-high cost of goods and uncertain long-term reimbursement frameworks | -12.3% | Global, cost-sensitive economies | Long term (≥ 4 years) |

| Complex resource-intensive manufacturing and logistics limiting scalability | -8.7% | Global, infra-constrained regions | Medium term (2-4 years) |

| Safety management challenges including cytokine storms and neuro-toxicity | -6.1% | North America, EU | Short term (≤ 2 years) |

| Regulatory heterogeneity and hospital-infrastructure gaps in emerging markets | -4.2% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ultra-high cost of goods and uncertain long-term reimbursement frameworks

Current therapy prices span USD 300,000 to USD 600,000 per infusion, yet total care episodes climb past USD 1 million when hospital stays and adverse-event management are included.[3]BioProcess International, “The Four Degrees of Automation,” bioprocessintl.com Labor accounts for half of manufacturing costs, making scale benefits elusive for small-batch autologous runs. Automated systems can reduce costs, but they require upfront capital that smaller biotechs often struggle to finance. Payment hurdles loom large; U.S. Medicaid programs still negotiate reimbursement on a state-by-state basis, prolonging cash-conversion cycles for manufacturers. Persisting fiscal frictions temper the adoption rates, curbing the near-term upside of the novel T-cell immunotherapy market.

Complex resource-intensive manufacturing and logistics are limiting scalability

Autologous production entails a 35-step workflow with multiple open manipulations, which invites batch-failure risk and extends vein-to-vein timelines to four weeks. Cold-chain transport of cryopreserved leukapheresis material requires –150 °C storage, a logistic constraint in emerging economies. Regional variability in GMP regulations complicates network optimization, forcing companies to maintain redundant capacity, thereby increasing costs. These structural inefficiencies suppress throughput and inflate per-patient costs. Unless automation and regulatory harmonization progress rapidly, scalability challenges will limit the global reach of the novel T-cell immunotherapy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: CAR-T Dominance Drives Market Evolution

CAR-T platforms generated 96.1% of the revenue within the novel T-cell immunotherapy market in 2024, reflecting their clinical experience, commercial infrastructure, and favorable reimbursement codes. Seven FDA-approved CAR-T products now span multiple B-cell malignancies, and long-term data show four-year survival rates above 70% in some patient cohorts. However, allogeneic CAR-T pipelines are on course for a 41.5% CAGR to 2030, aided by gene-editing safeguards that minimize host-versus-graft complications. Developers leverage universal donor cells to eliminate manufacturing wait times, a critical advantage for patients with acute illnesses.

Continued progress in tumor-infiltrating lymphocyte therapies, validated by lifileucel’s 31.5% objective response in metastatic melanoma, widens the modality mix. TCR-T success in synovial sarcoma highlights solid-tumor potential, while natural killer cell products offer innate cytotoxicity with a safety edge. Combination regimens pairing cell therapies with checkpoint inhibitors are under investigation to overcome immunosuppressive tumor microenvironments. As modality diversity grows, the novel T-cell immunotherapy market attracts investors seeking portfolios that balance exposure to both hematologic and solid-tumor indications.

By Cell Source: Autologous Leadership Faces Allogeneic Challenge

Autologous therapies accounted for 93.4% of the novel T-cell immunotherapy market share in 2024, benefiting from personalized antigen recognition and historically smoother regulatory paths. Patient-specific products minimize graft-versus-host risk and demonstrate robust engraftment profiles across hematologic indications. Yet vein-to-vein cycles extend beyond 20 days, and manufacturing failure rates of up to 5% create costly re-manufacture loops.

Allogeneic candidates are projected to expand at a 38.9% CAGR, promising immediate on-demand dosing and centralized production that unlock economies of scale. Fate Therapeutics’ iPSC-derived CAR-T line secured RMAT status for systemic lupus erythematosus, underscoring regulatory confidence in universal donor platforms. Centralized inventories streamline global distribution, and bulk manufacturing reduces raw material waste. If ongoing trials confirm persistence and safety, allogeneic supply could capture a sizeable share of the novel T-cell immunotherapy market over the forecast horizon.

By Indication: Hematologic Foundation Expands into New Territories

Hematologic malignancies accounted for 88.7% of revenue in 2024, a testament to the efficacy of CAR-T therapies in B-cell lymphomas and multiple myeloma. BCMA-targeted agents such as Abecma and Carvykti recorded triple-digit sales growth, reinforcing confidence in next-generation antigen targets. Response durability supports payer willingness to fund high upfront costs, solidifying blood cancers as the cash engine of the novel T-cell immunotherapy market.

Autoimmune diseases, however, are expected to drive growth with a 38.7% CAGR to 2030, as early-phase data reveal prolonged remission following B-cell depletion. Kyverna’s KYV-101 is tracking toward pivotal trials in multiple sclerosis, and early systemic lupus erythematosus readouts report 70% flare-free survival at six months. Solid tumor momentum builds around MAGE-A4, NY-ESO-1, and PRAME targets using either TCR-T or allogeneic CAR-T formats. As indications diversify, revenue risk disperses, accelerating the global adoption curve of the novel T-cell immunotherapy market.

Geography Analysis

North America commanded 60.2% of the novel T-cell immunotherapy market size in 2024 thanks to robust reimbursement frameworks, 311 accredited treatment centers, and the FDA’s leadership in accelerated pathways. Medicare’s fiscal-year 2025 6.4% base-rate rise to USD 274,413 per CAR-T case improves hospital margins, bolstering provider uptake. Manufacturers continue to scale capacity; Gilead plans to quadruple output by 2026, and Novartis operates seven multi-continental plants that ring-fence supply resilience. Despite these strengths, rural and minority patient access gaps persist, prompting investment in telemedicine triage and subsidized travel programs.

Asia Pacific is the fastest-growing territory, advancing at a 30.5% CAGR on the back of China’s streamlined Investigational New Drug process and Japan’s JPY 110 billion (USD 740 million) regenerative-medicine stimulus. The region hosts 48% of global cell therapy trials, offering sponsors rapid enrollment and genetic diversity. South Korea’s February 2025 Regenerative Medicine Law now provides a harmonized approval channel, drawing multinational firms to establish GMP plants near Seoul. Supply-chain localization reduces import duties and shipping risks, enabling price reductions that expand addressable patient pools. Nevertheless, heterogeneous reimbursement rules remain a hurdle across Asia Pacific markets.

Europe delivers steady growth anchored by EMA PRIME designations and a mature manufacturing ecosystem spanning Germany, the United Kingdom, and France. Cross-border clinical-trial networks benefit from harmonized protocols, allowing sponsors to activate multi-site studies in under six months. Post-Brexit regulatory divergence adds complexity, but mutual-recognition agreements mitigate delays for most therapies. Eastern European nations are investing in CAR-T infusion centers to stem outbound medical tourism.

Middle East & Africa and South America trail with limited infrastructure, though Brazil’s ANVISA has issued guidelines modeled on EMA standards. GCC countries are funding flagship centers to retain local oncology cases. High equipment costs and workforce shortages temper immediate uptake, but long-term demographic shifts position these regions as nascent contributors to the novel T-cell immunotherapy market.

Competitive Landscape

The market exhibits moderate concentration: Novartis, Gilead’s Kite Pharma, and Bristol Myers Squibb leverage first-mover CAR-T approvals and global manufacturing footprints to dominate revenue. Novartis reported USD 50.3 billion in total 2024 sales, with Kymriah’s double-digit growth underscoring durable demand. Bristol Myers Squibb’s cell therapy portfolio generated USD 6.4 billion, up 21% year over year, reflecting Abecma’s rapid penetration in multiple myeloma.

Cost-reduction races shape competitive strategies. Ori Biotech’s closed-system IRO platform achieved 69% transduction efficiency, outpacing legacy open processes and trimming per-dose labor needs by 30%. Cellares’ Cell Shuttle, offering nine parallel bioreactors, promises 760% throughput gains—technology that could re-rank manufacturers based on operational economics. Incumbents are forging partnerships with automation specialists to protect share; Kite Pharma’s 2024 pact with Shoreline Biosciences embeds off-the-shelf NK-cell capacity into Kite’s pipeline.

Allogeneic innovators, notably Allogene Therapeutics and Fate Therapeutics, threaten autologous incumbency with universal donor inventories targeting faster time-to-treat. Regulatory wins such as RMAT status for FT819 validate the strategy and invite capital inflows. Meanwhile, niche players are filing patents around multiplex CRISPR edits and novel cytokine cassettes to differentiate persistence profiles. As technology proliferates, the novel T-cell immunotherapy market gravitates toward platform-centric competition where manufacturing agility and target expansion trump sheer salesforce scale.

Novel T-Cell Immunotherapy Industry Leaders

Novartis AG

Gilead Sciences

Bristol Myers Squibb

Johnson & Johnson

Allogene Therapeutics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Capricor Therapeutics received an US FDA Priority Review of deramiocel for Duchenne muscular dystrophy cardiomyopathy, positioning the therapy for potential first-in-class approval.

- March 2025: The US FDA cleared ENCELTO, an allogeneic encapsulated ocular gene-cell therapy for idiopathic macular telangiectasia type 2, broadening cell therapy modalities beyond oncology.

- November 2024: The US FDA approved Aucatzyl, the eighth CAR-T therapy, for relapsed or refractory B-cell precursor acute lymphoblastic leukemia.

Global Novel T-Cell Immunotherapy Market Report Scope

As per the scope of the report, novel T-cell immunotherapy refers to innovative and emerging approaches that utilize T-cells, a type of immune cell, to treat diseases such as cancer. These therapies involve modifying, enhancing, or harnessing T-cells to better recognize and attack disease cells.

The novel T-cell immunotherapy market is segmented into various categories, including therapy type, which comprises CAR-T, TCR-T, tumor-infiltrating lymphocyte (TIL), T-cell engager/BiTE, and other novel modalities; cell source, divided into autologous and allogeneic; and indication, which includes hematologic malignancies, solid tumors, autoimmune diseases, viral infections, and other indications. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market forecasts are provided in terms of value (USD).

| CAR-T |

| TCR-T |

| Tumor-Infiltrating Lymphocyte (TIL) |

| T-Cell Engager/BiTE |

| Other Novel Modalities |

| Autologous |

| Allogeneic |

| Hematologic Malignancies |

| Solid Tumors |

| Autoimmune Diseases |

| Viral Infections |

| Other Indications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | CAR-T | |

| TCR-T | ||

| Tumor-Infiltrating Lymphocyte (TIL) | ||

| T-Cell Engager/BiTE | ||

| Other Novel Modalities | ||

| By Cell Source | Autologous | |

| Allogeneic | ||

| By Indication | Hematologic Malignancies | |

| Solid Tumors | ||

| Autoimmune Diseases | ||

| Viral Infections | ||

| Other Indications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the novel T-cell immunotherapy market in 2025?

The novel T-cell immunotherapy market size is USD 101.4 million in 2025 and is projected to reach USD 568.7 million by 2030 at a 41.5% CAGR.

Which therapy type currently dominates sales?

CAR-T commands 96.1% of global revenue, making it by far the predominant modality.

What is the fastest-growing segment by cell source?

Allogeneic platforms are forecast to climb at a 38.9% CAGR through 2030 due to their off-the-shelf convenience.

Which region is expanding most quickly?

Asia Pacific is expected to grow at a 30.5% CAGR, propelled by regulatory reforms and expanded clinical-trial activity.

What main factor restricts wider adoption?

Ultra-high cost of goods and still-evolving reimbursement models reduce affordability, especially in price-sensitive markets.

Page last updated on: