Veterinary Immunodiagnostics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

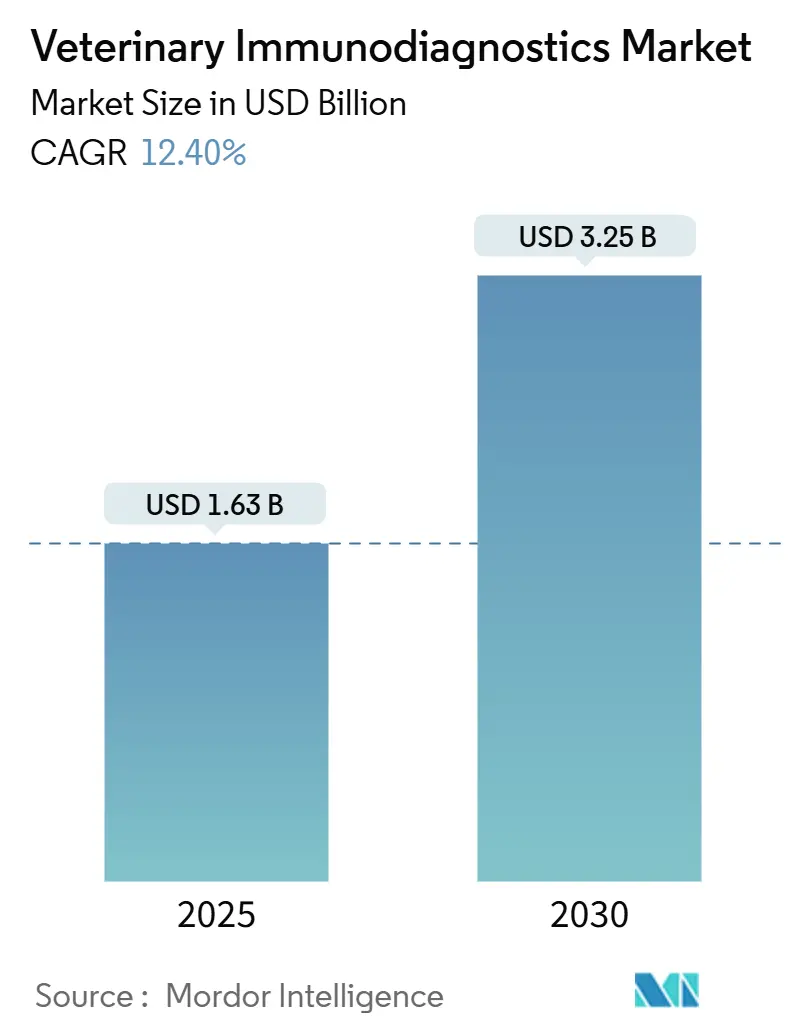

| Market Size (2025) | USD 1.63 Billion |

| Market Size (2030) | USD 3.25 Billion |

| Growth Rate (2025 - 2030) | 12.40% CAGR |

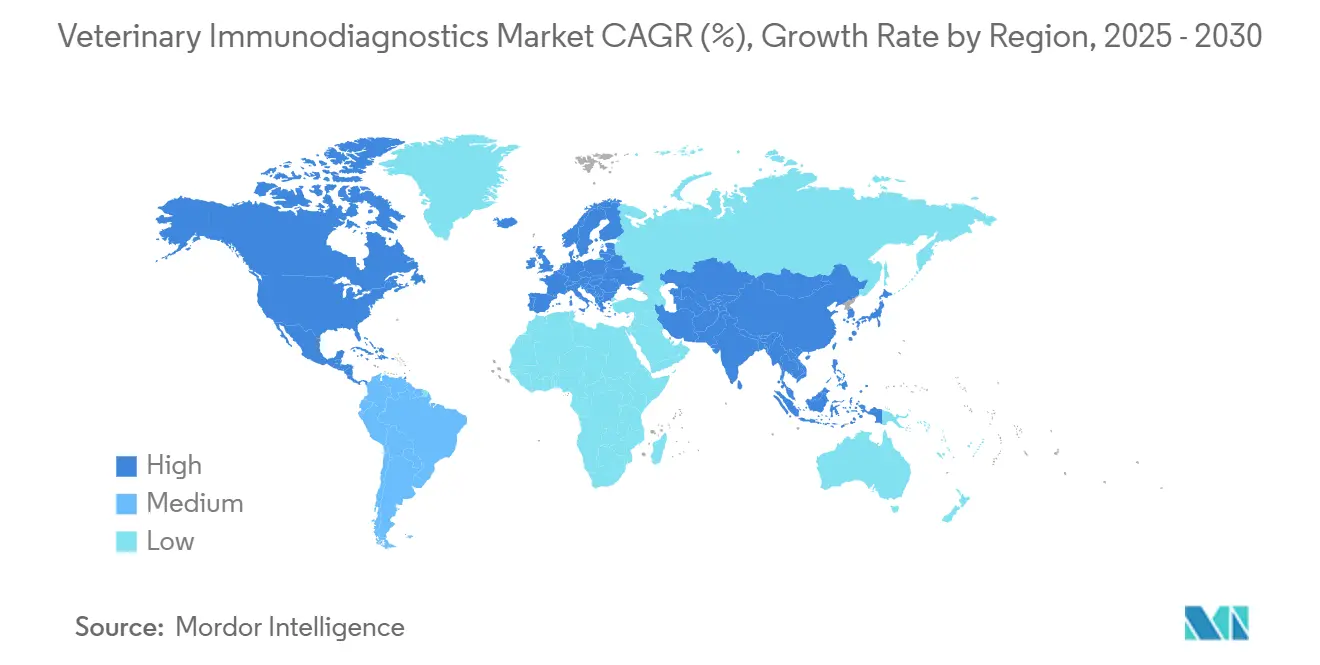

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Immunodiagnostics Market Analysis by Mordor Intelligence

The Veterinary Immunodiagnostics Market size is estimated at USD 1.63 billion in 2025, and is expected to reach USD 3.25 billion by 2030, at a CAGR of 12.40% during the forecast period (2025-2030).

Rising companion-animal spending, stricter zoonotic surveillance rules, and rapid test innovations are the strongest revenue catalysts. ELISA kits still anchor routine screening; yet, cartridge-based and AI-enabled point-of-care (POC) platforms are steadily displacing traditional batch testing, as speed becomes the decisive differentiator in clinical workflows. North America maintains its revenue lead, driven by corporate practice networks, increased pet insurance uptake, and sophisticated reference laboratory ecosystems. At the same time, the Asia Pacific region adds the most absolute dollars, thanks to expanding middle-class pet ownership and tightening livestock biosecurity standards. Market consolidation is gathering pace: IDEXX retains about half of global sales and is leveraging its scale advantages, Mars has integrated Cerba Vet and ANTAGENE into its diagnostics arm, and Zoetis is utilizing artificial intelligence to expand its Vetscan franchise. Meanwhile, climate-driven vector spread fuels double-digit growth in parasitic disease assays, reinforcing the strategic value of multiplex POC menus for mixed infections.

Key Report Takeaways

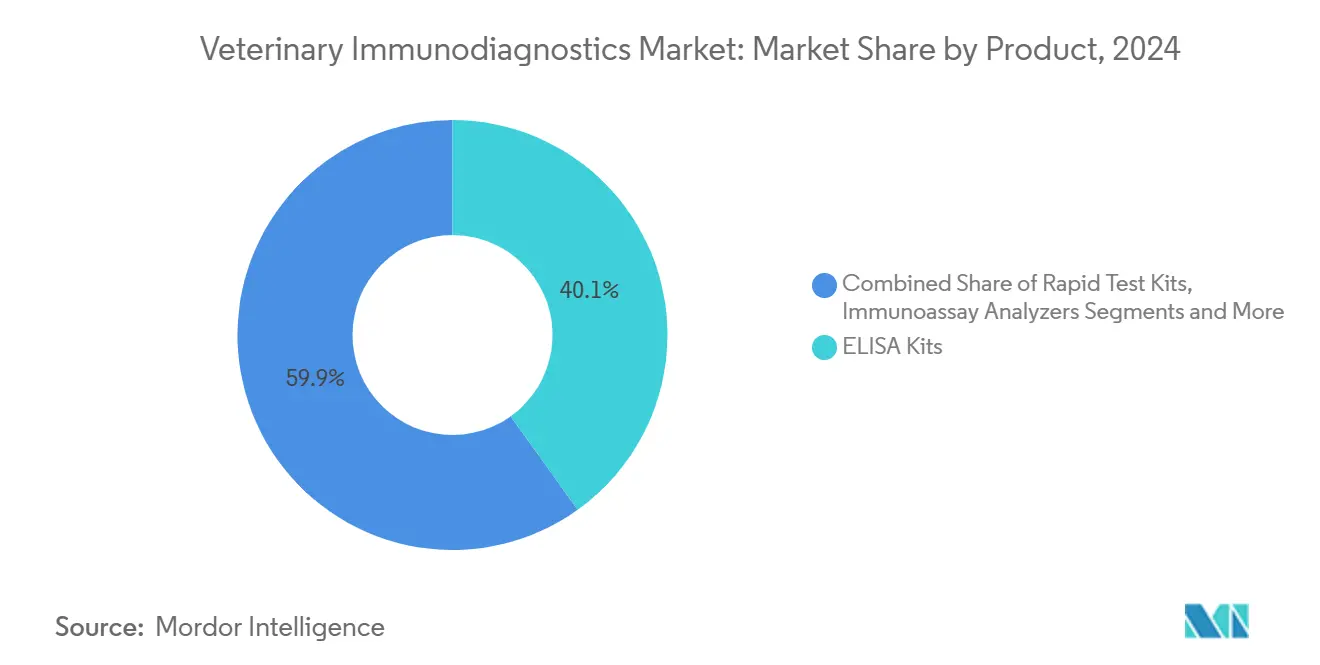

- By product, ELISA kits led with 40.1% revenue share in 2024; rapid test kits are projected to expand at a 12.1% CAGR to 2030.

- By animal type, companion animals accounted for 56.5% of total tests in 2024, while livestock diagnostics are set to rise at a 10.5% CAGR through 2030.

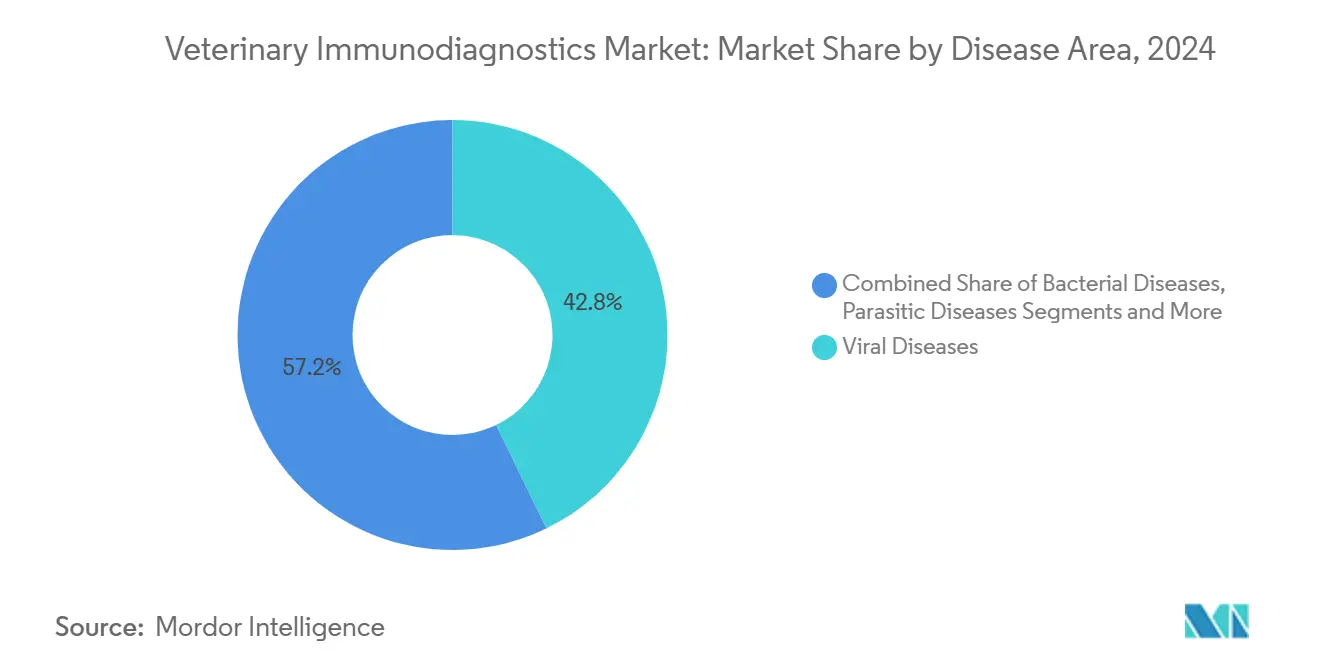

- By disease area, viral assays captured 42.8% of total testing volume in 2024; parasitic assays are forecast to grow at a 12.5% CAGR to 2030.

- By end user, veterinary reference laboratories held a 46.7% share of the veterinary immunodiagnostics market size in 2024; meanwhile, point-of-care settings are projected to advance at a 15.2% CAGR through 2030.

- By geography, North America held 45.9% of the veterinary immunodiagnostics market share in 2024, whereas the Asia Pacific is expected to expand at a 11.8% CAGR through 2030.

Global Veterinary Immunodiagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Companion Animal Spending Upswing | +2.80% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Zoonotic Disease Surveillance Mandates | +2.10% | Global, with emphasis on Asia Pacific & emerging markets | Long term (≥ 4 years) |

| Advancements In ELISA & Rapid Test Formats | +1.90% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Intensifying Livestock Bio-Security Norms | +1.60% | Asia Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Multiplex POC Panels For Mixed Infections | +1.40% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Tele-Vet Platforms Bundling Home-Test Kits | +1.20% | North America, with gradual global expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Companion Animal Spending Upswing

Households in the United States spent USD 279 billion on pet care in 2025, a trajectory driven by Millennials and Gen Z, who view routine diagnostics as preventive wellness investments rather than discretionary add-ons. Two-thirds of U.S. homes now include at least one pet, expanding the client base for advanced panels. Companion-animal owners show a higher willingness to pay for AI-assisted testing that promises immediate results and tailored treatment, sustaining premium pricing potential even when macroeconomic conditions soften. Corporate hospital chains and subscription wellness plans increase test penetration by normalizing annual screening protocols through bundled service models. These patterns collectively contribute to stable volume growth in the veterinary immunodiagnostics market, without the reimbursement complexities that frequently hinder growth in human diagnostics.

Zoonotic Disease Surveillance Mandates

National regulators are tightening reporting rules as part of One Health preparedness goals. In 2025, the USDA’s National List of Reportable Animal Diseases enforced 24-hour reporting on notifiable cases, compelling clinics and reference laboratories to broaden routine surveillance menus.[1]USDA APHIS, “National List of Reportable Animal Diseases FAQ,” aphis.usda.gov India, through its National One Health Programme, has set up sentinel sites that require continuous diagnostic throughput, locking in baseline demand. Outbreaks such as lumpy skin disease in Asia, with losses tallied at USD 1.45 billion, illustrate how epidemics spark urgent laboratory utilization.[2]FAO, “Introduction and Spread of Lumpy Skin Disease in Asia,” fao.orgIntegration of animal and human datasets under shared dashboards reinforces continuous testing requirements, turning compliance into a durable revenue stream for the veterinary immunodiagnostics market.

Advancements in ELISA & Rapid Test Formats

Research groups have developed time-resolved fluorescence strips that are 12,800 times more sensitive than legacy rose-bengal assays for brucellosis, enabling field users to achieve lab-grade accuracy within minutes. Multiplex PCR workflows can now pinpoint three swine viruses in a single run, cutting turnaround from days to under one hour. Zoetis’ cartridge-based Vetscan OptiCell packages AI-empowered hematology into a countertop unit, reducing operator dependency while pushing reference-lab precision into everyday clinics. Collectively, these breakthroughs accelerate migration from batch ELISA toward decentralized workflows and raise performance expectations across the veterinary immunodiagnostics market.

Intensifying Livestock Bio-Security Norms

Southeast Asia’s SEACFMD roadmap mandates stepped-up surveillance for foot-and-mouth disease, prompting governments to fund local test-kit manufacturing to safeguard regional supply chains. Australia earmarked resources under its National LSD Action Plan to establish neighboring-country screening hubs and to validate POC assays for rapid field response. China’s middle-class appetite for high-quality protein intensifies government commitments to a disease-free status, making continuous diagnostics a prerequisite for export eligibility. These requirements ensure long-term demand for livestock-focused reagents and genomic assays, particularly in the Asia Pacific veterinary immunodiagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost & Lack Of Reimbursement | -1.80% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Multi-Jurisdictional Kit-Approval Hurdles | -1.20% | Global, with complexity in EU and Asia Pacific | Long term (≥ 4 years) |

| Cross-Reactivity Causing False Positives | -1.00% | Global, with higher impact in multiplex testing markets | Short term (≤ 2 years) |

| Rural Lab Skill-Set Shortage | -1.40% | Global, with acute impact in emerging markets and rural regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost & Lack of Reimbursement

Veterinary medicine remains predominantly cash-pay, so every test must clear a willingness-to-pay threshold. Tariffs on imported diagnostics increased from 2.5% to 27% in the United States in 2025, thereby inflating equipment costs for practices.[3]AVMA, “Veterinary Practices Brace for Tariffs,” avma.orgPremium multiplex PCR runs and AI analyzers often command list prices that only high-volume urban clinics can justify. The gap is wider in emerging economies, where disposable income lags behind pet-health expectations, limiting uniform uptake and tempering the growth of the veterinary immunodiagnostics market.

Multi-Jurisdictional Kit-Approval Hurdles

Manufacturers face divergent regulatory paths: Japan vets diagnostics under human-device rules, the EU lacks harmonized provisions for in-clinic tests, and the U.S. relies on post-market surveillance instead of pre-market clearance. Navigating parallel dossiers drags launch timelines and adds compliance overhead, discouraging smaller innovators. Even as the European Medicines Agency’s Veterinary Regulation aims to establish smoother pathways by 2025, practical barriers persist, slowing the adoption of new formats in the veterinary immunodiagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: ELISA Dominance Faces Rapid-Test Disruption

ELISA kits maintained a 40.1% share of revenues in 2024, reaffirming their position as the backbone of broad screening protocols in the veterinary immunodiagnostics market. Rapid test kits, however, are expected to surge at a 12.1% CAGR to 2030, as clinics prioritize immediate results to increase same-visit treatment starts. The crossover momentum is reinforced by AI-enhanced cartridges that now rival ELISA sensitivity, compressing test duration from hours to ten minutes. Immunoassay analyzers are experiencing renewed relevance as clinics seek walk-away automation that frees up scarce technician time. Reagents and consumables deliver steady annuity income across all modalities, cushioning vendors against hardware replacement cycles. Multiplex innovation is the next leg of growth; a single cartridge that simultaneously detects parvovirus, coronavirus, and Giardia exemplifies how single-session breadth improves economic math for veterinarians coping with labor shortages.

The narrative extends to consumable pull-through: each rapid cartridge embeds proprietary chemistry, locking clinics into branded replenishment schedules. Vendors utilize cloud dashboards to tag each scan with anonymized metadata, thereby enriching epidemiological datasets and enabling predictive reorder algorithms. This closed-loop model sharpens forecasting accuracy and sustains competitive moats. The net effect is durable, high-margin consumables growth that anchors the financial profile of the veterinary immunodiagnostics market.

By Animal Type: Companion Care Drives Premium Diagnostics

Companion animals accounted for 56.5% of the total test volume in 2024, driven by pet parents' willingness to invest in comprehensive health screenings. Clinics report upticks in annual wellness panels that bundle hematology, clinical chemistry, and infectious disease serology, boosting the average revenue per visit. Meanwhile, livestock diagnostics are growing at a 10.5% CAGR as governments intensify biosecurity mandates, requiring constant herd monitoring. The economic incentive is clear: diagnostic outlays pale in comparison to the billion-dollar losses averted when outbreaks, such as lumpy skin disease, are contained early.

Exotic pets and wildlife form a small but profitable niche that commands premium pricing due to species-specific assay challenges. In livestock, genomic testing has gained popularity as breeders seek feed-conversion efficiency and disease-resistant lines. Reference labs offering combined genotyping and disease panels are reporting double-digit growth in order frequency. Such cross-functional assays increase ticket size and embed laboratories deeper into producer decision cycles, stimulating incremental volumes for the veterinary immunodiagnostics market.

By Disease Area: Viral Diagnostics Lead Amid Parasitic Surge

Viral assays accounted for 42.8% of disease-specific testing in 2024, highlighting the clinical urgency associated with conditions where early antiviral therapy can improve outcomes. PCR-based viral panels now dominate respiratory investigations in veterinary practice, including both canine and equine medicine. Yet, parasitic disease testing is sprinting ahead at a 12.5% CAGR, propelled by climate-driven tick and mosquito range expansion that exposes previously temperate zones to new vectors. Clinics deploy year-round heartworm and tick-borne panels, widening seasonal revenue windows.

Bacterial assays hold steady demand as antimicrobial stewardship pushes culture-and-sensitivity testing ahead of empirical treatment. Fungal and metabolic panels remain specialist orders, but they bring high average selling prices that offset the lower volume. Multiplex polymerase assays capable of flagging three protozoan parasites at once illustrate how vendors are converting complexity into clinician convenience, further scaling the veterinary immunodiagnostics market.

By End User: Reference Labs Dominate Despite POC Acceleration

Reference laboratories captured 46.7% of the veterinary immunodiagnostics market share in 2024, leveraging economies of scale to deliver comprehensive menus and rigorous quality programs. They remain indispensable for complex histopathology and molecular sequencing tasks. However, POC placements are rising at 15.2% CAGR as clinics seek to collapse diagnosis-to-treatment cycles into a single visit. Cartridge-based hematology analyzers and AI-guided cytology scanners have bridged historical performance gaps, enticing medium-volume practices to in-source.

Hospitals and clinics anchor POC demand, whereas research institutes contribute episodic spikes tied to surveillance studies and vaccine trials. Even large reference chains now deploy satellite POC hubs within high-density urban corridors to reduce courier hours and shave off turnaround times. This hybrid architecture combines breadth with speed, underscoring how service models are evolving within the veterinary immunodiagnostics market.

Geography Analysis

North America held a 45.9% share in 2024, driven by unrivaled per-capita pet spending and mature practice chains that bundle diagnostics into care plans. Pet insurance uptake supports premium pricing, and corporate consolidators leverage bulk purchasing to refresh analyzer fleets ahead of depreciation curves. Tariff hikes did raise hardware costs, but high procedure margins preserve clinic economics. Canada enjoys regulatory regimes that fast-track innovative assays, while Mexico’s growing middle class is widening the companion-animal addressable base.

Asia Pacific leads the growth charts with an 11.8% CAGR through 2030, reflecting synchronized expansion in pet ownership and livestock modernization. China’s urban households are spending more per pet visit, and provincial laboratories are pivoting to higher-complexity virology assays. India’s One Health sentinels funnel predictable volumes to district labs, ensuring baseline utilization even during off-season months. Southeast Asian producers battling foot-and-mouth disease rely on regional PCR confirmation before export clearance, embedding diagnostics into the trade compliance chain.

Europe operates as a mature, standards-driven market where regulatory coherence under EMA’s veterinary strategy fosters stable innovation cycles. Germany and the Nordics exhibit high test penetration due to strong welfare norms, whereas southern Europe demonstrates potential for catch-up. The Middle East and Africa remain under-penetrated but exhibit pockets of rapid adoption where commercial dairy hubs demand mastitis screening and export-grade certification. South America’s large beef herds sustain bacterial and viral assay demand, with Brazil spearheading uptake as it integrates diagnostics into herd-health insurance programs. Altogether, regional heterogeneity ensures that vendors must orchestrate diverse go-to-market strategies to capture the full value from the global veterinary immunodiagnostics market.

Competitive Landscape

IDEXX Laboratories accounts for roughly 50% of worldwide revenue and continues to widen its moat through test-menu expansions and digital ecosystem lock-in. Zoetis, leveraging its pharmaceutical roots, has parlayed Vetscan launches into a multipronged diagnostic ecosystem that now spans AI cytology, hematology, and urinalysis. Thermo Fisher remains a top-tier supplier of reagents and instruments and is realigning its diagnostics unit through selective divestitures to sharpen its focus on higher-growth modalities. Mars’ acquisition of Cerba Vet and ANTAGENE positions its pet-care empire deeper in the data stream, enabling cross-selling across nutrition, insurance, and practice management. Mid-cap players such as Neogen carve out defensible niches in food-chain safety and livestock genomics, while Bio-Rad leverages quality-control expertise to supply reagents that sit inside competing platforms.

Competitive intensity centers on speed-to-result and AI-driven decision support. Vendors that fuse hardware, reagents, analytics, and cloud reporting into turnkey subscriptions raise switching costs for clinics. Rural penetration remains a white-space opportunity where simpler cartridge systems can bypass reference-lab limitations. Meanwhile, environmental diagnostics for emerging pathogens represent a frontier where early movers can set de-facto standards, shaping the next wave of growth within the veterinary immunodiagnostics market.

Veterinary Immunodiagnostics Industry Leaders

IDEXX Laboratories

Zoetis Inc.

Thermo Fisher Scientific

Heska

Neogen Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Zoetis unveiled AI Masses cytology technology that screens lymph-node aspirates in the clinic within minutes, extending Imagyst to seven POC modalities.

- December 2024: Zoetis launched Vetscan OptiCell, a cartridge-based hematology analyzer slated for six Western markets in 2025.

- July 2024: Mars finalized purchases of Cerba Vet and ANTAGENE, expanding its European diagnostics footprint.

- June 2024: IDEXX added a Catalyst Pancreatic Lipase Test that generates results in under 10 minutes for rapid pancreatitis confirmation.

Global Veterinary Immunodiagnostics Market Report Scope

| ELISA Kits |

| Rapid Test Kits (Lateral Flow) |

| Immunoassay Analyzers |

| Reagents & Consumables |

| Companion Animals |

| Livestock Animals |

| Other Animals |

| Viral Diseases |

| Bacterial Diseases |

| Parasitic Diseases |

| Other Diseases |

| Veterinary Reference Laboratories |

| Veterinary Hospitals & Clinics |

| Point-of-Care / Field Testing |

| Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | ELISA Kits | |

| Rapid Test Kits (Lateral Flow) | ||

| Immunoassay Analyzers | ||

| Reagents & Consumables | ||

| By Animal Type | Companion Animals | |

| Livestock Animals | ||

| Other Animals | ||

| By Disease Area | Viral Diseases | |

| Bacterial Diseases | ||

| Parasitic Diseases | ||

| Other Diseases | ||

| By End User | Veterinary Reference Laboratories | |

| Veterinary Hospitals & Clinics | ||

| Point-of-Care / Field Testing | ||

| Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the veterinary immunodiagnostics market in 2025 and how fast is it growing?

The veterinary immunodiagnostics market size is USD 1.63 billion in 2025 and is on track to reach USD 3.25 billion by 2030 at a 12.4% CAGR.

Which product category is growing fastest?

Rapid test kits are registering a 12.1% CAGR to 2030 as clinics pivot toward immediate, cartridge-based workflows.

Why is Asia Pacific considered the most attractive growth region?

Urbanization-driven pet ownership, stricter livestock biosecurity rules, and government-backed One Health surveillance programs combine to deliver an 11.8% CAGR in Asia Pacific through 2030.

What share do reference laboratories hold today?

Reference labs account for 46.7% of total revenues, leveraging broad menus and quality infrastructure.

Which disease area offers the highest growth upside?

Parasitic disease assays are advancing at a 12.5% CAGR due to climate-induced vector expansion and year-round surveillance needs.

How concentrated is vendor competition?

IDEXX, Zoetis, and Thermo Fisher together control just over 60% of global revenues, indicating a moderately consolidated landscape with a concentration score of 6.

Page last updated on: