Asia Pacific Synthetic Media Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

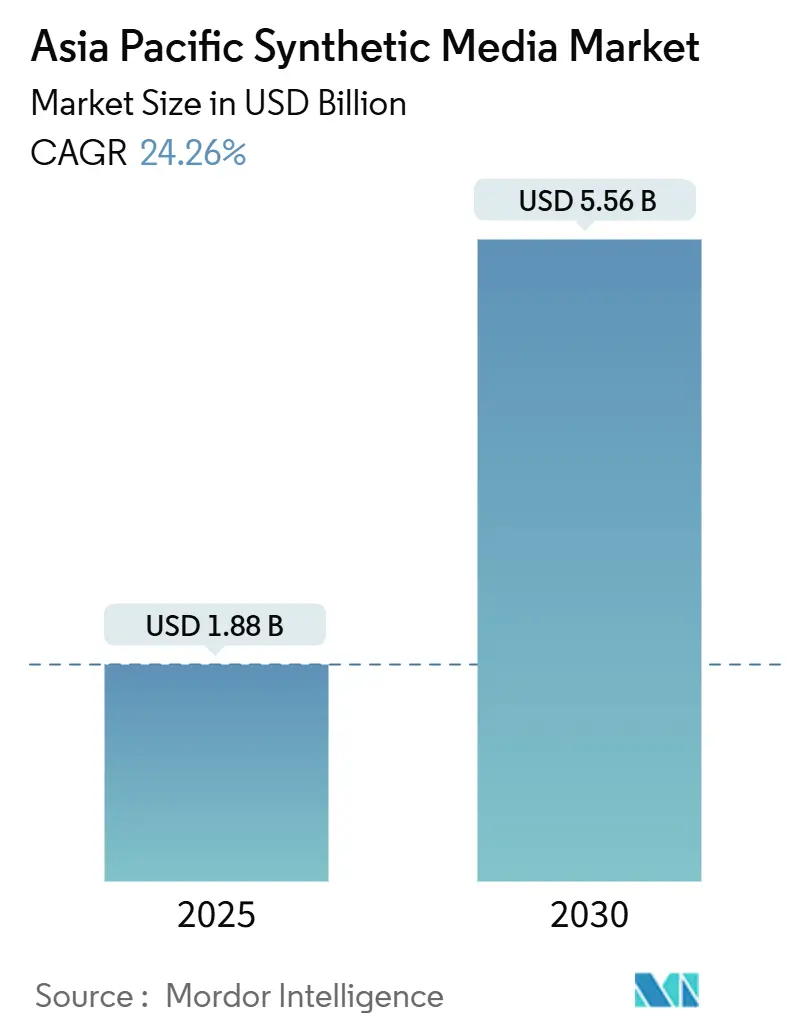

| Market Size (2025) | USD 1.88 Billion |

| Market Size (2030) | USD 5.56 Billion |

| Growth Rate (2025 - 2030) | 24.26% CAGR |

| Fastest Growing Market | South Asia |

| Largest Market | Asia Pacific |

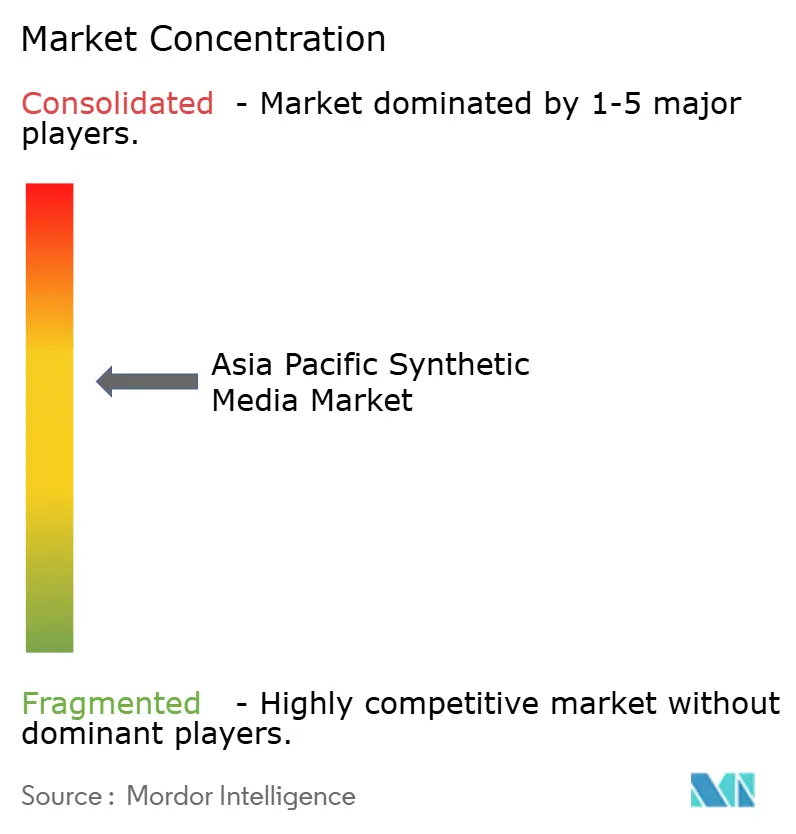

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Synthetic Media Market Analysis by Mordor Intelligence

The Asia Pacific synthetic media market size reached USD 1.88 billion in 2025 and is forecast to attain USD 5.56 billion in 2030, advancing at a 24.26% CAGR during 2025-2030. Favorable factors include steep improvements in generative-AI cost curves, accelerating 5G penetration, and escalating capital deployment by regional technology leaders. China currently anchors demand on the strength of a broad AI policy push, while India is setting the pace for growth as smartphones penetrate deep into tier-2 and tier-3 cities. Intensifying rivalry among digital conglomerates and start-ups continues to compress inference prices, expanding the addressable base of creators. At the same time, persistent GPU shortages are encouraging model-efficiency breakthroughs and edge-computing adoption, both of which support long-run scalability. Regulatory initiatives such as China’s Deep Synthesis Provisions and Singapore’s sectoral guidelines are shaping content-safety norms and nudging enterprises toward compliant toolchains.

Key Report Takeaways

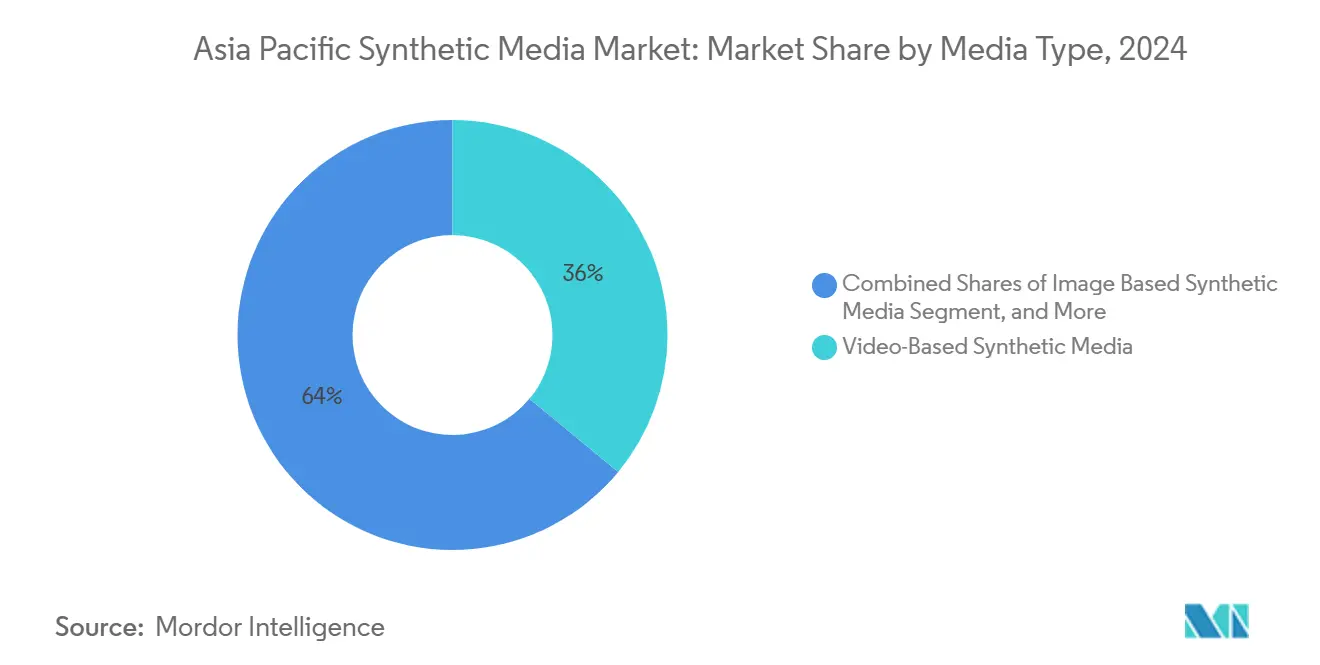

- By media type, video-based content led with 35.61% revenue share in 2024; audio-based solutions are projected to expand at a 25.72% CAGR through 2030.

- By technology, generative AI commanded 44.56% of the Asia Pacific synthetic media market share in 2024, while natural-language processing is on track for a 25.11% CAGR to 2030.

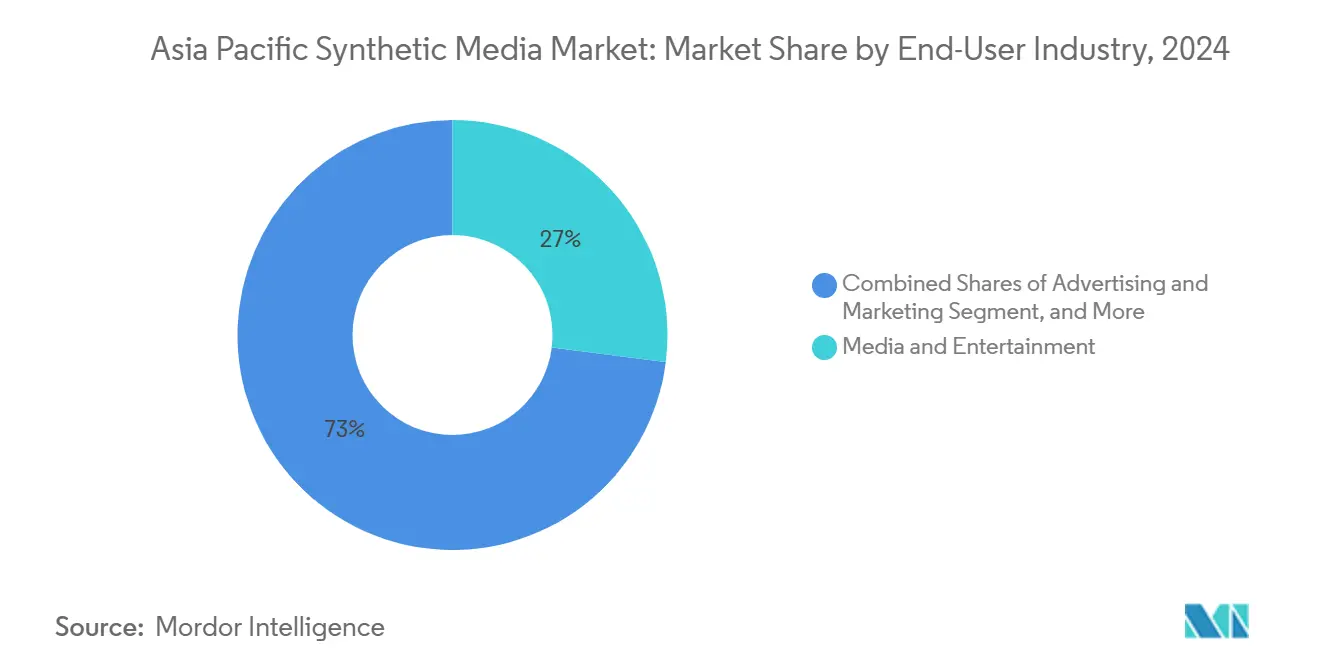

- By end-user industry, media and entertainment captured 27.46% of 2024 revenues; gaming and metaverse applications hold the fastest growth outlook at 24.66% CAGR.

- By geography, China accounted for 33.47% of 2024 spending, whereas India is forecast to post a 26.00% CAGR during the outlook period.

Global valuation is built by aggregating outputs from multiple regions, with Asia forming one of the important contributors. Mordor Intelligence's global synthetic media market size report represents that cumulative total.

Asia Pacific Synthetic Media Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling costs of generative-AI content | +3.2% | China, India, South Korea | Medium term (2-4 years) |

| Growing 5G coverage | +2.8% | Core Asia Pacific, extending to Southeast Asia | Short term (≤2 years) |

| Increased investment in AI video start-ups | +2.1% | China, India, Japan, ASEAN | Medium term (2-4 years) |

| Rising use of virtual influencers | +1.9% | North Asia and major Southeast Asian cities | Short term (≤2 years) |

| Voice-cloning tools for multilingual content | +1.7% | India, Singapore, multilingual markets | Medium term (2-4 years) |

| Government digital-human projects | +1.4% | China, South Korea, Singapore, Japan | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Falling Costs of Generative-AI Content Creation Drive Mass Adoption

Widening access to open-source video, image, and voice models is compressing production costs and encouraging experimentation among independent studios and small businesses. Alibaba’s Wan 2.2 model offers enterprise-grade video generation under a permissive license, enabling mid-tier agencies to deliver cinematic assets at a fraction of historical budgets. Game developer Fortune Mine reduced level-design hours by 72% after integrating Layer’s automation pipeline, freeing staff for creative tasks.[1]Layer, “Fortune Mine Games Cuts Level-Design Time by 72%,” layer.ai Chinese AI model providers Moonshot AI and MiniMax reduced their token costs in 2024, making AI models more accessible to student developers and small to medium enterprises in the region. Lower barriers spur a flywheel in which fresh user cohorts generate more edge cases, accelerating model refinement and propelling the Asia Pacific synthetic media market deeper into mainstream production workflows.

5G Infrastructure Expansion Enables Mobile-First Consumption

Asia Pacific is the world’s most advanced 5G cluster, and median mobile download speeds above 500 Mbps in South Korea exemplify the bandwidth surplus now available for real-time AI video rendering. A tenfold rise in regional 5G connections expected by 2030 will underpin latency-sensitive applications such as live virtual-influencer broadcasts. Mobile usage already accounts for over half of all internet activity in the region, so synthetic media solutions optimized for vertical screens and touch navigation naturally align with prevailing consumption habits. Esports firm Garena demonstrates the potential, layering augmented-reality elements onto live tournaments to heighten fan engagement. As radio-access networks densify across emerging Southeast Asian markets, comparable services will become viable beyond first-mover economies, unlocking fresh demand pockets and fortifying the Asia Pacific synthetic media market.

AI Video-Startup Investment Surge Fuels Innovation

Record-level funding rounds signal investor confidence in next-generation content engines. ByteDance earmarked USD 12 billion for large-scale GPU procurement and domain-specific research hubs, while the combined valuations of the “Six Tigers” cohort of Chinese AI firms exceed USD 10 billion. Capital intensity shortens iteration cycles, letting founders port research gains to commercial products in months rather than years. Cross-border spillovers follow naturally: talent spin-outs seed start-ups in Japan, Singapore, and Australia, disseminating know-how and broadening the competitive field.

Virtual-Influencer Adoption Transforms Brand Marketing

Consumer brands are pivoting toward synthetic spokes-characters that deliver higher engagement, consistent messaging, and multilingual reach without fatigue. South Korea’s virtual celebrity Rozy Oh has landed multimillion-dollar endorsements, while Japanese fashion houses collaborate with digital icon imma for seasonal look-books. In Singapore and Thailand, agencies now specialize in region-specific avatars like Rae, enabling hyper-local campaigns that resonate with Gen-Z audiences. Advertisers appreciate the 24/7 availability, scriptable persona management, and granular performance analytics that virtual influencers provide, accelerating penetration across retail, tourism, and consumer-goods verticals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inconsistent deepfake laws | -2.3% | Region-wide, acute for cross-border campaigns | Medium term (2-4 years) |

| GPU shortages | -3.1% | China, Japan, South Korea | Short term (≤2 years) |

| Creator revenue-share concerns | -1.8% | China, South Korea, Japan | Medium term (2-4 years) |

| Scarcity of bias-free local-language datasets | -2.0% | Southeast Asia and minority-language communities | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Regulatory Fragmentation Creates Compliance Complexity

China’s Deep Synthesis Provisions mandate labeling and provenance disclosures, whereas Singapore relies on sector-specific advisories. Hong Kong has recorded a tenfold rise in deepfake fraud complaints, prompting law-enforcement action but not yet a dedicated statute.[2]Hong Kong Government, “LCQ9: Combating Frauds Involving Deepfake,” info.gov.hk This patchwork forces platform operators to tailor workflows for each jurisdiction, raising legal overhead and slowing regional roll-outs. A marketing video permissible under Japanese guidelines may require on-screen watermarks in mainland China, eroding creative uniformity and inflating production budgets.

Semiconductor Supply Constraints Limit Scale-Up

Chronic shortages of high-end GPUs and advanced packaging capacity have tripled procurement lead times and driven spot-market prices above official list rates. Taiwan Semiconductor Manufacturing Co. expects constrained CoWoS supply into 2025, signaling limited short-term relief. In response, many Asia Pacific developers are pursuing model-compression techniques and quantization strategies to achieve real-time inference on edge devices. Although these optimizations enhance efficiency, they also divert engineering bandwidth away from frontier-model innovation, temporarily damping the ceiling for content fidelity in the Asia Pacific synthetic media market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Media Type: Video Content Drives Market Leadership

Video-based solutions generated 35.61% of 2024 revenue, the largest share within the Asia Pacific synthetic media market. The format’s versatility spans marketing shorts, corporate training, and cinematic visual effects, aligning closely with regional preferences for short-form mobile entertainment. Audio-based tools, while representing a smaller base, are scaling fastest at a 25.72% CAGR, powered by multilingual voice-cloning libraries that resonate in linguistically diverse markets.

Rapid diffusion of text-to-video pipelines from ByteDance and Alibaba is lowering the skill threshold for creators, while speech-synthesis breakthroughs are opening podcast and audiobook channels in vernacular languages. Image-generation platforms oriented toward e-commerce cut photography cycle times for sellers, and text-generation modules support localization at scale. Together, these modalities reinforce a cross-pollination flywheel, cementing video’s primacy yet ensuring balanced growth across complementary media streams within the Asia Pacific synthetic media market size hierarchy.

By Technology: Generative AI Dominates with NLP Acceleration

Generative AI commanded 44.56% of 2024 revenue, reflecting widespread enterprise adoption of diffusion models and large language models for multimodal creation. Natural-language processing is the momentum leader, projected to expand at 25.11% CAGR, as organizations pursue cross-language chatbots and content localization engines. Computer graphics and visual effects maintain relevance in gaming and metaverse production, and voice-synthesis stacks gain traction where hands-free interfaces are valued. Microsoft's expansion to 60+ realistic multilingual voices, including Southeast Asian language support, illustrates the market opportunity in this segment.[3]Microsoft, “Expanded Collection of Realistic Multilingual Voices,” microsoft.com

Technology differentiation is shifting from raw parameter counts to efficiency metrics such as tokens-per-second and watt-hour per inference. Consequently, start-ups able to tune models for mid-tier GPU clusters can undercut hyperscaler pricing, broadening customer reach. The Asia Pacific synthetic media market size associated with generative AI is set to compound further as IP-holder safeguards mature and pre-trained models incorporate robust watermarking.

By End-User Industry: Media Leadership with Gaming Surge

Media and entertainment captured 27.46% of 2024 spending, leveraging AI anchors, automated trailer generation, and cost-efficient post-production. Gaming and metaverse designers, however, lead the growth pack with a 24.66% CAGR, propelled by non-player character voice-overs and user-generated content plug-ins. Advertisers integrate virtual personas into omnichannel campaigns, and e-commerce retailers deploy synthesized try-ons and product-explanation videos to raise conversion rates.

Education ministries in Singapore and South Korea are piloting AI teaching assistants, illustrating the sector’s nascent but promising trajectory. Healthcare innovators, notably Ping An, are field-testing virtual doctors to extend primary-care capacity. Each vertical unlocks differentiated revenue pools, yet all share a reliance on foundational model ecosystems and GPU-backbone availability—factors that will condition the Asia Pacific synthetic media market share dynamics over the forecast horizon.

Geography Analysis

China accounted for 33.47% of 2024 revenue, underpinned by extensive government backing and integrated corporate ecosystems that fuse creation tools, cloud infrastructure, and distribution channels. The domestic Deep Synthesis Provisions furnish legal certainty, encouraging enterprises to scale. Aggressive investments—Alibaba alone has earmarked USD 52.9 billion for AI infrastructure—further buttress China’s leading position within the Asia Pacific synthetic media market.

India delivers the steepest trajectory with a 26.00% CAGR projection. A young, mobile-first population and state-level digital-public-infrastructure initiatives stimulate both supply and demand. Domestic start-ups benefit from English-language data abundance yet are also localizing for Hindi, Tamil, and Bengali users, enlarging total addressable reach.

Japan, South Korea, Australia, and Singapore collectively form a mature adopter cohort. OpenAI’s selection of Tokyo for its inaugural Indo-Pacific hub highlights the country’s supportive regulatory stance, while Seoul’s 5G saturation and gaming pedigree accelerate experiential content ventures. The broader Southeast Asian bloc is transitioning from exploratory pilots to commercialization, aided by rising disposable incomes and deepening e-commerce penetration. Across geographies, synchronized 5G network expansion constitutes a unifying catalyst that underpins the scalable delivery of synthetic media assets.

Coverage of the synthetic media market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for South America, Middle East and Africa, and North America.

Competitive Landscape

Market concentration is moderate, with heavyweight platforms vying against nimble specialists. ByteDance integrates creator tools (CapCut, Seedance) and distribution engines (TikTok, Douyin) to capture end-to-end value. Alibaba’s emphasis on open-source releases (Wan 2.2, Qwen) and elastic-compute bundling differentiates its proposition for enterprises. Tencent leverages its gaming franchises to embed real-time character generation and voice synthesis.

Hardware access is emerging as a strategic moat; firms securing priority queues for advanced GPUs can iterate faster and deliver higher-resolution outputs. Consequently, alliances with chip manufacturers and cloud providers are becoming standard playbooks for contenders looking to safeguard inference capacity. Start-ups focusing on vertical niches—such as medical-training avatars or legal-document synthesis—find breathing room by combining domain expertise with efficient model architectures. Patent filings related to neural rendering and multimodal copyright tagging indicate that IP portfolios will feature prominently in future competitive positioning.

Cross-border expansion remains a double-edged sword: it offers scale but forces mastery of heterogeneous compliance regimes. Companies that architect modular watermarking and audit-trail systems are better placed to navigate these complexities and, by extension, gain share within the Asia Pacific synthetic media market.

Asia Pacific Synthetic Media Industry Leaders

ByteDance Seed

Alibaba Group Holding Ltd

Meta

BRIA

NAVER Z CORP.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: TCS established a Google Cloud Gemini Experience Center at its Retail Innovation Lab in Chennai, India, enabling clients to test, conceptualize, and jointly develop solutions across the retail value chain.

- March 2025: SCiNiTO and iGroup Asia Pacific have established a partnership to provide research and publishing services across 12 countries in Asia and the Pacific region. The agreement enables SCiNiTO to offer its AI-based research and publishing tools to researchers, academics, and institutions in Asia, Australia, and New Zealand.

- February 2025: WAN-IFRA and OpenAI have partnered to introduce the South Asia Newsroom AI Catalyst accelerator program, which focuses on integrating artificial intelligence into newsroom operations.

- January 2025: Synthesia raised USD 180 million in Series D financing led by NEA to broaden its enterprise video suite

- January 2025: ElevenLabs secured USD 250 million in Series C funding to accelerate multilingual voice-AI research

Asia Pacific Synthetic Media Market Report Scope

| Audio-Based Synthetic Media |

| Image-Based Synthetic Media |

| Text-Based Synthetic Media |

| Video-Based Synthetic Media |

| Generative AI |

| Computer Graphics and Visual Effects |

| Natural Language Processing |

| Voice Synthesis and Recognition |

| Other Technologies (Augmented Reality and Virtual Reality, Generative Adversarial Networks, and More) |

| Media and Entertainment |

| Advertising and Marketing |

| Gaming and Metaverse |

| E-commerce and Retail |

| Education and Training |

| Healthcare and Life-Sciences |

| Other End-user Industries (Real Estate, Hospitality, and More) |

| China |

| India |

| Japan |

| South Korea |

| Rest of Asia Pacific |

| By Media Type | Audio-Based Synthetic Media |

| Image-Based Synthetic Media | |

| Text-Based Synthetic Media | |

| Video-Based Synthetic Media | |

| By Technology | Generative AI |

| Computer Graphics and Visual Effects | |

| Natural Language Processing | |

| Voice Synthesis and Recognition | |

| Other Technologies (Augmented Reality and Virtual Reality, Generative Adversarial Networks, and More) | |

| By End-User Industry | Media and Entertainment |

| Advertising and Marketing | |

| Gaming and Metaverse | |

| E-commerce and Retail | |

| Education and Training | |

| Healthcare and Life-Sciences | |

| Other End-user Industries (Real Estate, Hospitality, and More) | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

How fast is spending on synthetic media growing across Asia Pacific?

Aggregate revenue is projected to climb from USD 1.88 billion in 2025 to USD 5.56 billion by 2030, translating into a 24.26% CAGR.

Which country currently buys the most synthetic-media solutions?

China led with 33.47% of total 2024 spend thanks to strong policy support and sizable corporate outlays.

Which use case is expanding quickest in the region?

Gaming and metaverse applications are on track for a 24.66% CAGR through 2030 as studios embed AI characters and user-generated content tools.

Why are audio-based systems attracting investor attention

They offer the highest growth rate—25.72% CAGR—driven by demand for multilingual voice cloning in a linguistically diverse market landscape.

What is the biggest operational bottleneck today?

Limited access to high-end GPUs is slowing model training and scaling, prompting firms to focus on model-efficiency gains.

How are regulations affecting market expansion?

Divergent deepfake and content-labeling rules create compliance overhead, compelling companies to customize workflows by jurisdiction.

Page last updated on: