North America Synthetic Media Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

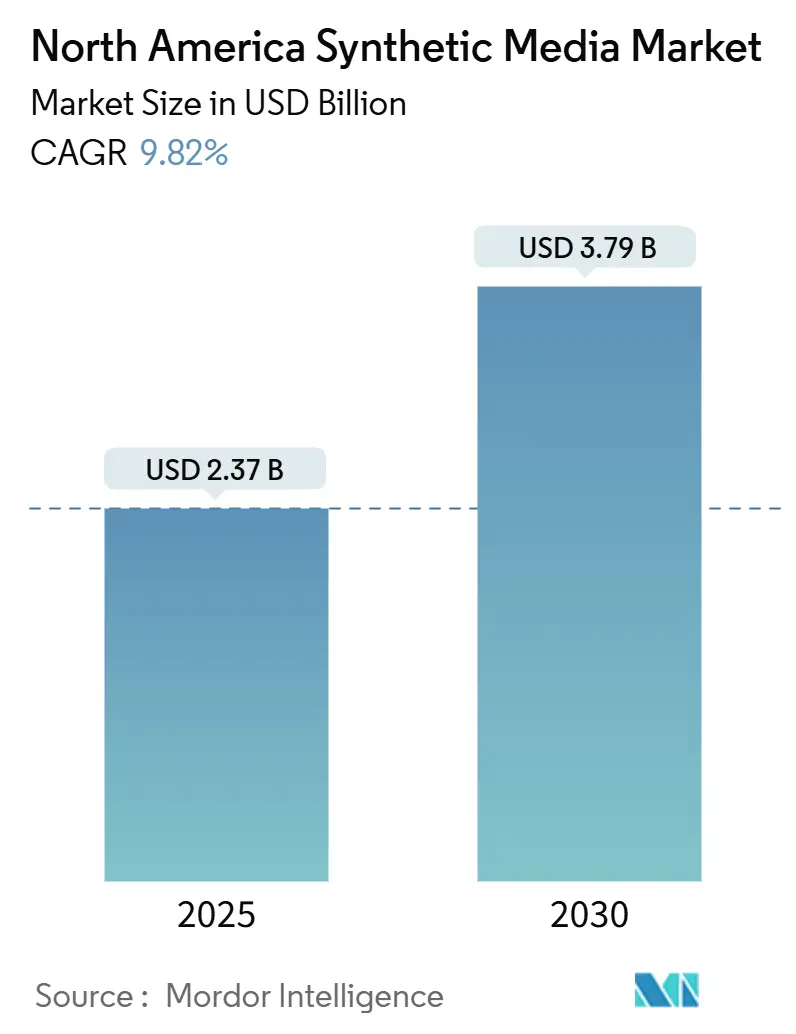

| Market Size (2025) | USD 2.37 Billion |

| Market Size (2030) | USD 3.79 Billion |

| Growth Rate (2025 - 2030) | 9.82% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Synthetic Media Market Analysis by Mordor Intelligence

The North America synthetic media market size stands at USD 2.37 billion in 2025 and is projected to reach USD 3.79 billion by 2030, expanding at a 9.82% CAGR. Price-performance gains in cloud GPUs, expanding enterprise proof-points, and sustained venture funding keep the growth curve steep as new entrants leverage lower compute thresholds and mature API layers. The market’s leadership position rests on hyperscale infrastructure density, large language model (LLM) advancements, and a supportive capital market that values platform extensibility over point solutions. Generative AI funding rounds Runway AI’s USD 308 million Series D and Synthesia’s USD 180 million raise signal institutional confidence that synthetic media will remain a core layer of future content supply chains. On the demand side, media companies cut production timelines by 60% through virtual sets while enterprises shave 90% off training-video costs, establishing a direct link between cost efficiency and adoption velocity. Simultaneously, regulatory guardrails emerge around deepfake disclosure, pushing vendors toward authenticated outputs and watermarking standards that could become table stakes for enterprise deals.

Key Report Takeaways

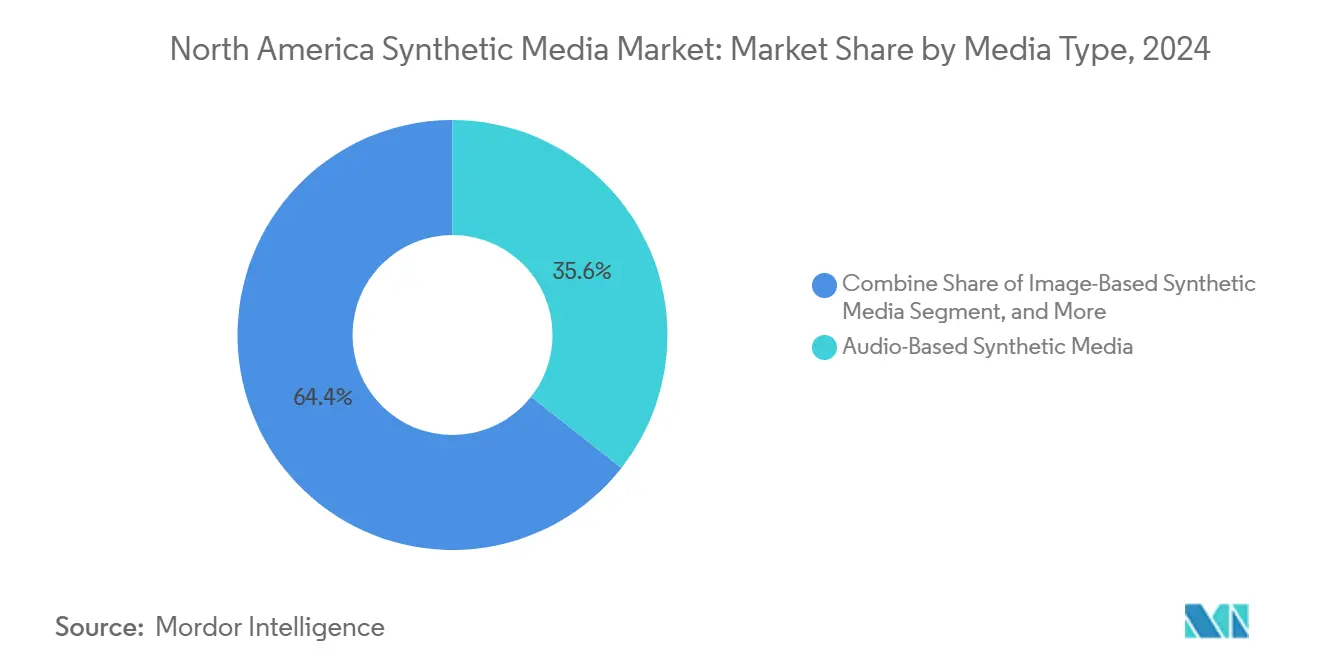

- By Media Type, Video-Based Synthetic Media led with 35.61% revenue share of the North America synthetic media market size in 2024, while Audio-Based Synthetic Media are advancing at a 9.84% CAGR, through 2030.

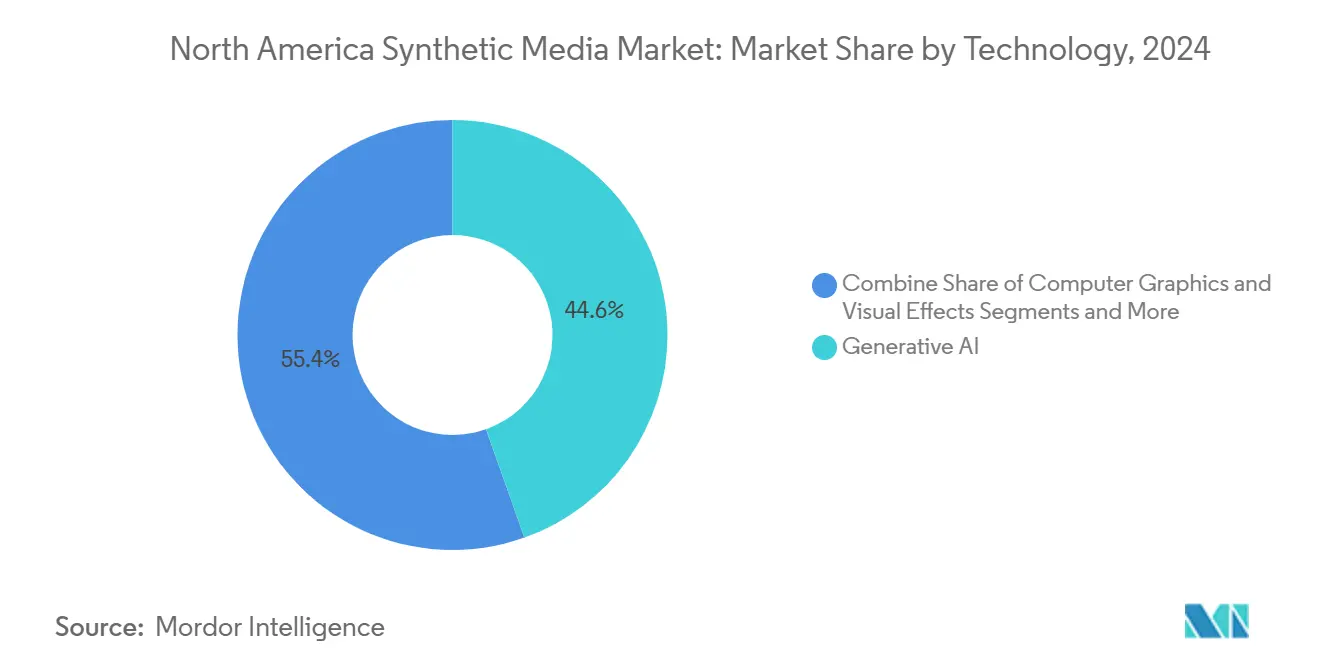

- By Technology, Generative AI engines captured 44.56% of the North America synthetic media market share in 2024, while natural language processing is projected to grow at 9.91% CAGR.

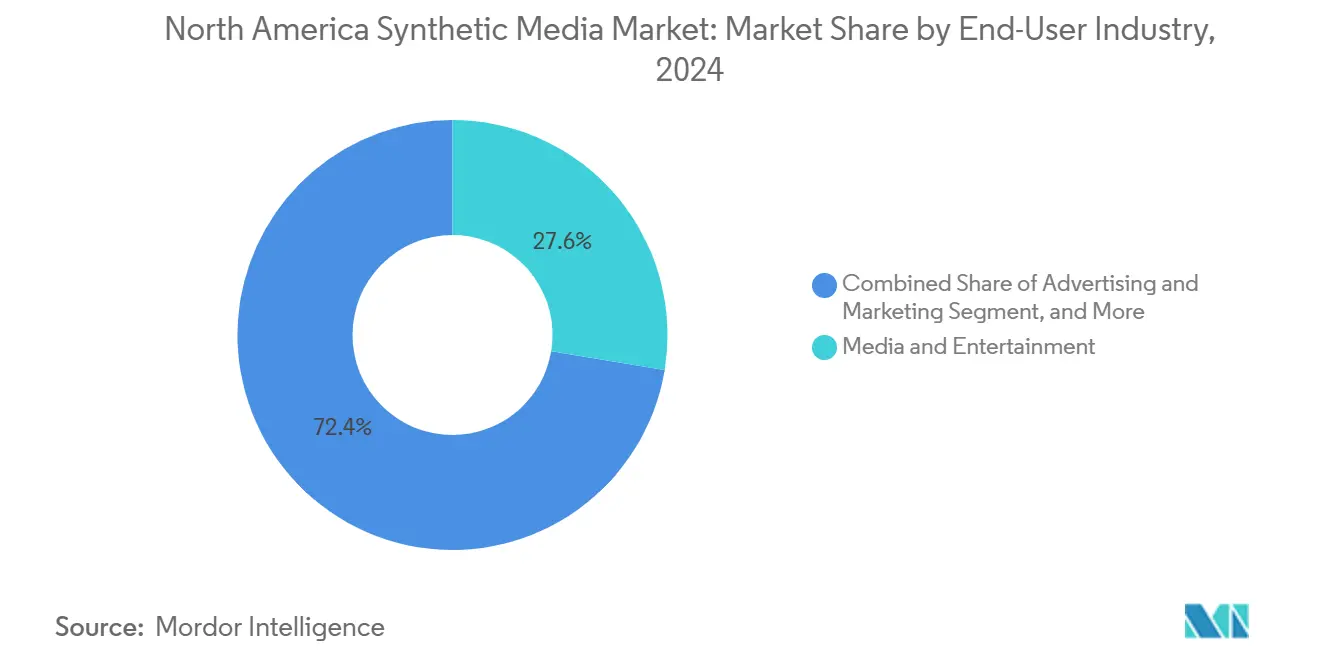

- By End-User Industry, Media and entertainment accounted for 27.46% of the North America synthetic media market size in 2024; while gaming and metaverse use cases are forecast to expand at 10.11% CAGR through 2030.

- By Country, The United States commanded 85.12% of the North America synthetic media market size in 2024, whereas Canada is on track for the highest national CAGR at 10.15% through 2030.

Worldwide, activity is shaped by contributions from multiple regions, with North america representing one of the more structurally developed among them. The global report on synthetic media market by Mordor Intelligence reflects how these regional layers combine into a single system.

North America Synthetic Media Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Broadcast-quality virtual production | +2.1% | United States West & East Coast creative hubs | Medium term (2-4 years) |

| Hyper-personalized advertising delivery | +1.8% | Early adoption in United States and Canadian metros | Short term (≤ 2 years) |

| Cost reductions across creative workflows | +1.6% | Enterprise-dense regions across North America | Short term (≤ 2 years) |

| Improved GPU price-to-performance ratio | +1.2% | United States hyperscale data-center regions | Medium term (2-4 years) |

| Breakthroughs in text-to-3D/4D generation | +0.9% | Silicon Valley and Seattle research corridors | Long term (≥ 4 years) |

| Inclusive-media regulatory support | +0.6% | State-level initiatives led by California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advancements in Media Production Enabling Broadcast-Quality Output in Virtual Environments

Virtual sets now meet linear-broadcast benchmarks, erasing the quality gap that once dissuaded professional studios. Netflix’s integration of Runway AI illustrates how synthetic backlots can compress content calendars by 60% while preserving cinematic fidelity.[1]Sarah Krouse, “For Data-Guzzling AI Companies, the Internet Is Too Small,” Wall Street Journal, wsj.comIndependent filmmakers gain parity with major houses, leveraging cloud pipelines for Hollywood-grade effects without brick-and-mortar stages. The economics flip traditional budgeting norms: a single creator can now orchestrate multi-hour productions once requiring hundreds of staff. Studios reframe synthetic media from a cost-cutting tactic to a premium-pricing differentiator, bidding for advanced capabilities that unlock new monetization layers.

Scalable Delivery of Hyper-Personalized Advertising Experiences

Synthetic media transforms advertising from broadcast campaign blasts to dynamic one-to-one storytelling. Retailers posting AI-generated spokesperson videos tailored to micro-segments report higher engagement than generic ads. Thousands of creative variants emerge from a single template, allowing daily refresh cycles that align with evolving consumer data. Real-time engines adapt tone, imagery, and even actor likeness per viewer, turning media buys into perpetual A/B tests. The budget shift follows the performance uplift: brands channel spend from large-studio shoots toward platforms offering granular audience control, accelerating adoption among direct-to-consumer and multinational advertisers alike.

Significant Cost Reductions Across Creative and Production Workflows

Enterprises gravitate toward platforms like Synthesia after DuPont documented USD 10,000 savings per training video and 90% faster cycle times compared with live-action shoots. Translation layers render multilingual versions in hours, eliminating studio re-booking and talent scheduling. Beyond direct savings, organizations reduce coordination overhead and iteration lag, positioning synthetic media as baseline infrastructure akin to SaaS office suites. Procurement teams increasingly list AI-generated content capabilities as mandatory in RFPs for learning-management or marketing-automation software, revealing synthetic media’s elevation from pilot projects to production-grade tools.

Improved Price-to-Performance Ratio of Cloud-Based GPUs Accelerating Adoption

NVIDIA’s H100 release and forthcoming B200 line pushed per-flop pricing down 30-50% from 2024, while spot instances on AWS, Azure, and Google Cloud slash variable costs a further 60-80% for elastic workloads. The downward spiral democratizes advanced generation tasks—mid-market firms prototype high-resolution avatars without cap-ex-heavy GPU clusters. Chip-maker volume ramps and cloud-provider efficiency improvements reinforce the virtuous cycle, expanding the total addressable base beyond Fortune 500 budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intellectual-property ambiguities | −1.4% | United States copyright environment | Medium term (2-4 years) |

| Deepfake misinformation threat | −1.1% | United States and Canada regulatory scrutiny | Short term (≤ 2 years) |

| Limited domain-specific datasets | −0.8% | Specialized global verticals | Long term (≥ 4 years) |

| High computational cost for smaller players | −0.7% | Emerging markets lacking hyperscale capacity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ambiguities in Intellectual Property Ownership

Lehrman v. Lovo and music-industry lawsuits expose the grey zone around AI-generated voice likenesses, spurring CFOs and legal teams to demand indemnification clauses before scaling deployments. Start-ups scramble to license training data transparently and embed provenance metadata to satisfy escalating due-diligence checklists. The legal uncertainty freezes experimentation in high-value franchises where IP missteps jeopardize brand equity and revenue streams, particularly across entertainment and advertising verticals that anchor the North America synthetic media market.

Rising Threat of Deepfake Misinformation

Legislation like the ELVIS Act and platform policies mandate disclosure labels, forcing vendors to integrate detection and watermark layers that inflate engineering overhead. Brands weigh reputational risk, often limiting synthetic media to internal learning or controlled ad networks. Compliance workflows now rival creative pipelines in complexity, tilting the competitive field toward providers with robust governance stacks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Media Type: Video Dominance Meets Audio Acceleration

Video-based generation garnered 35.61% of the North America synthetic media market share in 2024, underpinned by corporate learning modules, marketing explainers, and virtual sets that sidestep costly on-site shoots. Enterprises report significant cost reductions and faster iteration, reinforcing video as the default entry path for synthetic content deployment. Parallelly, the audio segment, though smaller, is sprinting at 9.84% CAGR. Voice cloning now covers multilingual and emotional permutations, unlocking localization at scale for global brands. ElevenLabs’ USD 180 million raise at a USD 3.3 billion valuation captures investor belief that lifelike speech will become a universal interface for both consumer and enterprise applications.[2]ElevenLabs Press, “Series B Raises USD 180 Million,” Elevenlabs.io, elevenlabs.io

In the next five years, converged audio-video pipelines emerge as competitive necessities. Platforms layer synchronized synthetic speech over gestural avatars, producing turnkey spokesperson assets that plug into e-commerce, help-desk, and advertising systems. As production frameworks standardize, the North America synthetic media market size tied to cross-modal solutions will eclipse standalone silos, prompting vendors to acquire or partner for missing capabilities.

By Technology: Generative AI Leadership Faces NLP Challenge

Generative diffusion engines controlled 44.56% of 2024 revenues, anchoring the North America synthetic media market size through photorealistic imagery, cinematic video, and procedural environments. However, natural language processing is projected to clock a 9.91% CAGR, inserting contextual understanding into otherwise visually impressive but semantically shallow assets. Cohere’s USD 5.5 billion valuation underlines enterprise hunger for domain-tuned language models that can direct scene composition, dialog, and multilingual subtitling. Over the period, competitive differentiation shifts from raw pixel fidelity to narrative coherence and brand alignment.

Convergence is already visible: Adobe’s investment in Synthesia blends classic creative-suite tooling with AI generation, promising frictionless hand-offs between design teams and algorithmic render engines. Voice synthesis models continue compression breakthroughs, reaching near-human output at lower compute footprints, broadening mobile and edge deployment scenarios. Meanwhile, AR/VR-centric generative adversarial networks serve niche interactive showcases but await hardware mass adoption.

By End-User Industry: Gaming Surge Challenges Media Dominance

Media and entertainment held 27.46% of 2024 revenue, yet gaming and metaverse pipelines are outpacing at a 10.11% CAGR through 2030. Studios harness AI avatars and procedural worlds to shorten build cycles while personalizing player experiences, drawing budgets away from linear content. The digital human economy is expected to grow, signaling durable demand for hyper-real characters that traverse films, interactive media, and branded corporate experiences. Advertising spending also tilt toward synthetic media as micro-targeting proves ROI-positive against conventional shoots.

Healthcare, education, and life-sciences adopt synthetic simulations for patient education and multilingual instructor-led scenarios, mitigating scarcity of specialized personnel. Although smaller in absolute dollars, these regulated verticals provide sticky, long-duration contracts once vendors clear compliance barriers, thereby stabilizing revenue amid cyclical entertainment budgets.

Geography Analysis

The United States commanded 85.12% of the North America synthetic media market size in 2024, powered by dense hyperscale data centers, venture capital abundance, and AI talent clusters in Silicon Valley and Seattle. Federal guidance coexists with state-level statutes California’s deepfake disclosure rules, for instance that shape national operational baselines Streaming giants such as Netflix integrate AI-based pipelines end-to-end, lowering costs while upholding studio-grade cinematography, which reinforces domestic demand loops.

Canada, growing at a 10.15% CAGR, benefits from progressive AI strategies like the CAD 450 million Pan-Canadian AI Initiative, academic pipelines, and Toronto’s vibrant start-up ecosystem. Bilingual mandates spur demand for multilingual voice and subtitle solutions, nudging local broadcasters and e-learning providers toward synthetic dubbing. Cohere’s hometown presence anchors talent retention, seeding ancillary ventures that deploy advanced NLP within content pipelines.

Mexico remains an emerging but high-potential node. Limited domestic GPU capacity pushes enterprises to cross-border cloud contracts, linking them to United States and Canadian synthetic-media vendors. The Spanish-speaking population offers a springboard to Latin American markets once localization engines mature.

Mordor Intelligence provides coverage of the synthetic media market across other key regional markets, including Europe, Asia, and South America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The competitive environment features both mega-cap cloud providers and nimble, specialist start-ups. Horizontal platforms emphasize integrated stacks combining text, audio, and video generation with branding controls. Incumbents leverage proprietary data corpora and custom silicon to lock in enterprise accounts, while newcomers secure footholds through breakthrough efficiencies or vertical-specific modules. Strategic moves in 2024-2025 include Adobe’s stake in Synthesia to fold AI video into Creative Cloud, and DNEG’s Brahma acquisition of Metaphysic to fuse VFX heritage with AI generative prowess.[3]Brahma Communications, “Brahma Announces the Acquisition of Metaphysic,” Dneg.com, dneg.com

Funding velocity remains brisk, but investors prioritize defensible IP and route-to-enterprise playbooks. Model-hosting costs act as a moat, advantaging firms with multi-tenant inference architectures. Consolidation accelerates as point-solution vendors seek liquidity or scale, evidenced by video-ad-tech merger talks between Connatix and JW Player DIGIDAY.COM. White-space persists in regulated sectors where compliance wrappers and domain data confer durable differentiation.

While total supplier count remains high, top-tier revenue concentration is moderate, with incumbent cloud triopoly and a handful of AI studios capturing the lion’s share. Model openness vs. proprietary control constitutes a strategic fork—open-weight releases like Cohere’s Aya 23 build community mindshare, whereas closed-source models aim for premium enterprise margins.

North America Synthetic Media Industry Leaders

DeepBrain AI

ElevenLabs

Colossyan Inc.

Adobe Inc.

NVIDIA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Elon Musk's AI venture has launched Grok Imagine, an image and video generator, exclusively for SuperGrok and Premium+ X subscribers on its iOS app. Staying true to Musk's vision of Grok as a bold and unfiltered AI, the generator empowers users to create NSFW content.

- April 2025: In a strategic move, Adobe's venture capital arm has poured undisclosed funds into Synthesia, a British AI startup, signaling its belief in the transformative potential of AI in video production. While the partnership is labeled "strategic," Adobe has chosen not to divulge specific financial or commercial details.

- January 2025: D-ID has unveiled its latest feature, Scenes, in its Creative Studio, streamlining the process of crafting multi-scene videos. With this enhancement, users can weave comprehensive narratives within a single project, merging as many as 10 distinct scenes, each boasting its own avatars, backgrounds, and content elements.

North America Synthetic Media Market Report Scope

| Audio-Based Synthetic Media |

| Image-Based Synthetic Media |

| Text-Based Synthetic Media |

| Video-Based Synthetic Media |

| Generative AI |

| Computer Graphics and Visual Effects |

| Natural Language Processing |

| Voice Synthesis and Recognition |

| Other Technologies (AR and VR, and Generative Adversarial Networks) |

| Media and Entertainment |

| Advertising and Marketing |

| Gaming and Metaverse |

| E-commerce and Retail |

| Education and Training |

| Healthcare and Life-Sciences |

| Other End-user Industries(Real Estate, Hospitality, and More) |

| United States |

| Canada |

| Mexico |

| By Media Type | Audio-Based Synthetic Media |

| Image-Based Synthetic Media | |

| Text-Based Synthetic Media | |

| Video-Based Synthetic Media | |

| By Technology | Generative AI |

| Computer Graphics and Visual Effects | |

| Natural Language Processing | |

| Voice Synthesis and Recognition | |

| Other Technologies (AR and VR, and Generative Adversarial Networks) | |

| By End-User Industry | Media and Entertainment |

| Advertising and Marketing | |

| Gaming and Metaverse | |

| E-commerce and Retail | |

| Education and Training | |

| Healthcare and Life-Sciences | |

| Other End-user Industries(Real Estate, Hospitality, and More) | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the projected value of the North America synthetic media market by 2030?

The market is forecast to reach USD 3.79 billion by 2030, reflecting a 9.82% CAGR.

Which media type currently leads in revenue?

Video-based synthetic content led with 35.60% market share in 2024, driven by demand for virtual production and training videos.

Why is Canada the fastest-growing national segment?

Government AI programs, bilingual content needs, and a strong research ecosystem underpin Canada’s 10.15% CAGR trajectory.

Which end-user vertical is expanding the quickest?

Gaming and metaverse applications are growing at a 10.11% CAGR due to demand for AI-generated avatars and immersive worlds.

What legal challenge most affects enterprise rollout?

Ambiguity around copyright ownership for AI-generated content is prompting enterprises to seek stronger indemnification and governance.

Page last updated on: