Europe Synthetic Media Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

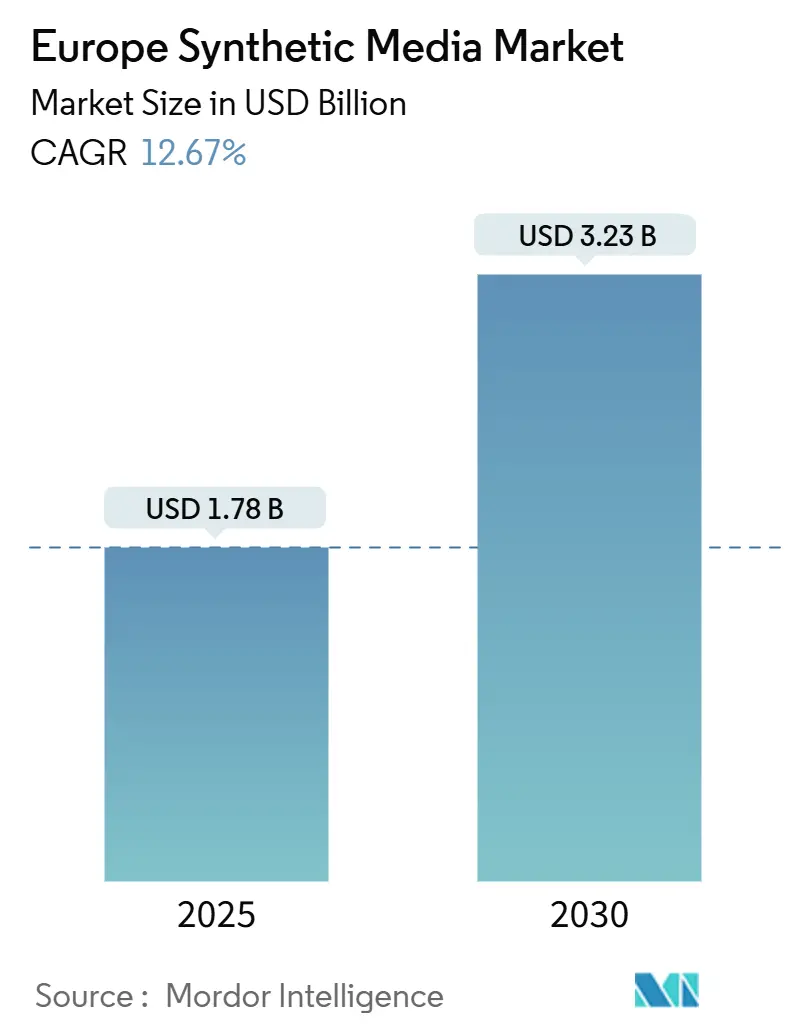

| Market Size (2025) | USD 1.78 Billion |

| Market Size (2030) | USD 3.23 Billion |

| Growth Rate (2025 - 2030) | 12.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Synthetic Media Market Analysis by Mordor Intelligence

The Europe synthetic media market size stands at USD 1.78 billion in 2025 and is forecast to reach USD 3.23 billion by 2030, reflecting a 12.67% CAGR. This sustained expansion is rooted in regulatory-driven credibility, sovereign data priorities and a maturing startup ecosystem that positions Europe as a trusted hub for enterprise-grade generative tools. Investments such as the European Commission’s EUR 4 billion AI innovation package have catalyzed AI Factories that lower entry barriers for small and midsize creators.[1]European Commission, “The New AI Innovation Package to Support Artificial Intelligence Startups and SMEs,” cedar-heu-project.eu Corporate demand for cost-efficient multilingual content, rapid time-to-market and inclusive design keeps adoption rates high, while GPU cloud-credit programs temper infrastructure costs. Meanwhile, compliance with the EU AI Act accelerates watermarking and provenance solutions that differentiate regional vendors from global rivals. Fragmented copyright rules, however, prolong licensing negotiations and create notable go-to-market friction.

Key Report Takeaways

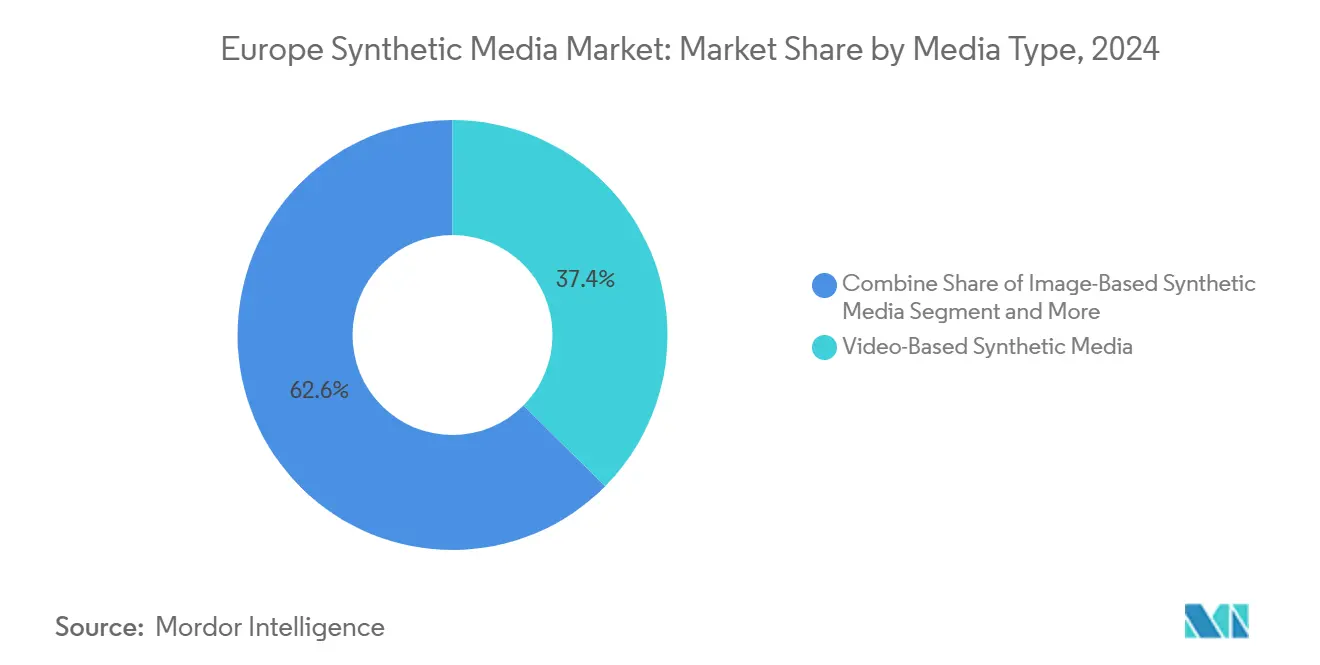

- By media type, video-based solutions commanded 37.43% of the Europe synthetic media market share in 2024, while Audio-Based Synthetic Media has the fastest growth at 12.71% over forecast period.

- By geography, Germany held 31.21% of the Europe synthetic media market size in 2024, whereas the United Kingdom is advancing at a 13.23% CAGR through 2030.

- By technology, generative AI held 43.76% share of the Europe synthetic media market size in 2024, yet natural language processing registers the fastest 12.83% CAGR for 2025-2030.

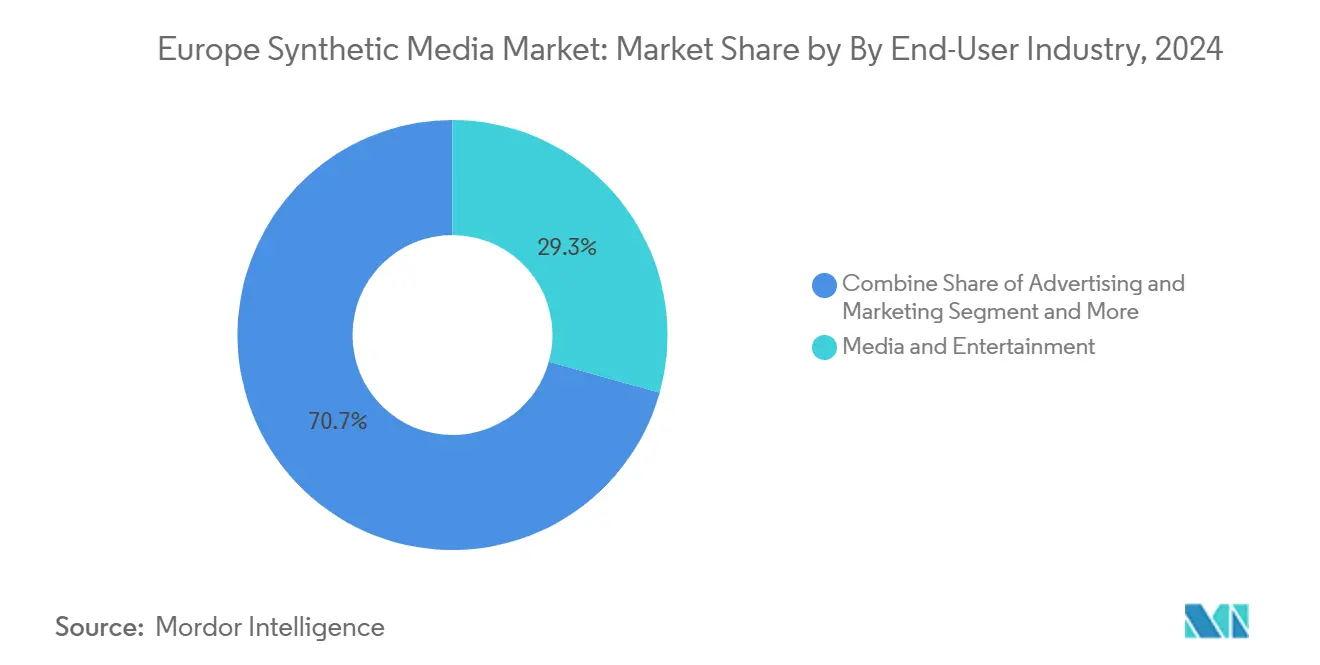

- By end-user industry, gaming and metaverse applications are expanding at a 13.11% CAGR to 2030, overtaking the 29.32% share that media and entertainment retained in 2024.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global synthetic media market data by Mordor Intelligence represents that combined structure.

Europe Synthetic Media Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-efficient localized video translations | +2.1% | Germany, France, Netherlands | Medium term (2-4 years) |

| Near-real-time synthetic voice cloning | +1.8% | EU-wide; strongest in Nordics | Short term (≤ 2 years) |

| Decreased model-training expenses from GPU cloud credits | +2.3% | Germany, United Kingdom, France | Short term (≤ 2 years) |

| Regulatory focus on European-language data sovereignty | +1.9% | EU-wide; led by Germany and France | Long term (≥ 4 years) |

| Open-source diffusion models for European cultural IP | +1.7% | Germany, France, Netherlands | Medium term (2-4 years) |

| Metaverse-ready 3-D avatar pipelines | +2.0% | United Kingdom, Germany, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-Efficient Solutions for Localized Video Translations Drive Enterprise Adoption

Corporate training, marketing and compliance teams increasingly rely on AI video tools that cut dubbing and subtitling costs by up to 80%, as demonstrated by Colossyan’s roll-out across Porsche and Vodafone.[2]Tech.eu Staff, “Colossyan’s AI Text-to-Video Platform Attracts $22M,” tech.eu Broadcasters using the Speechmatics-Limecraft workflow save GBP 100,000 monthly by automating subtitles.[3]Speechmatics, “Limecraft Case Study,” speechmatics.com The EuroLLM project’s 4 trillion-token multilingual model further reduces per-language deployment expenses. Compliance requirements mandating accessibility in 24 official languages amplify demand within German and French markets.

Near-Real-Time Synthetic Voice Cloning Enhances Disability Inclusion Efforts

Accessibility directives spur adoption of voice cloning that instantly translates and vocalizes content for users with disabilities. ElevenLabs’ model now outperforms Google and OpenAI across 99 languages, enabling universities to embed multilingual captions at scale. A Polish-EU innovation pact channels public funds toward voice technology for government communication. BBC StoryWorks highlights inclusive speech applications in partnership with Speechmatics. Healthcare pilots under the SYNTHIA project employ synthetic audio to ease clinician-patient exchanges. Nordic countries lead uptake thanks to robust welfare policies that foreground digital inclusion.

Model-Training Expenses Decrease Through GPU Cloud Credits Across Europe

AI Factories within the EuroHPC network grant startups discounted access to the LUMI supercomputer and other HPC nodes, trimming model-training budgets by more than half . Germany allocates part of its EUR 1 billion AI fund to cloud credits, nurturing a dense pipeline of generative startups. Supply-side stresses persist because Europe controls a minor portion of global hyperscale capacity , yet the hybrid mix of supercomputers and sovereign clouds maintains cost relief in the near term.

Open-Source Diffusion Models Optimized for European Cultural IP

Germany and France back diffusion models that embed local artistic styles while honoring IP constraints. Community-driven repositories accelerate iteration, reduce vendor lock-in and foster collaboration across universities and studios. Adoption gains strength where cultural preservation is politically salient.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inconsistent copyright regulations across EU member states | -1.4% | EU-wide | Medium term (2–4 years) |

| Non-compliance penalties under the EU AI Act Title VIII | -2.1% | EU-wide | Short term (≤ 2 years) |

| Export restrictions contributing to high-performance GPU shortages | -1.8% | EU-wide (import-dependent regions) | Short to Medium term (1–3 years) |

| Creator economy resistance over revenue displacement concerns | -1.2% | Major content-producing economies (e.g., Germany, France, United Kingdom) | Medium to Long term (2–5 years) |

| Source: Mordor Intelligence | |||

Inconsistent Copyright Regulations Challenge Cross-Border Operations

GEMA’s lawsuit against OpenAI illustrates divergent national rules on AI training data. Italy’s personality-rights protections permit deepfake victims to claim damages. Scholars warn that DSM Directive text-and-data-mining exceptions may exclude generative training, triggering bespoke licensing . Surveys reveal that 95% of music creators demand transparency and compensation, adding transaction costs for startups.

EU AI Act Non-Compliance Penalties Intensify Market Entry Barriers

The Act permits penalties of up to EUR 35 million or 7% of global turnover, creating substantial financial risk. Mandatory AI literacy programs, watermarking and labeling begin in August 2025. Each non-compliant AI unit could cost EUR 29,277 annually, squeezing thinly capitalized ventures. Uncertainty around “prohibited practices” such as emotional manipulation delays product launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Media Type: Video Leadership Holds as Audio Accelerates

In 2024, video-based synthetic media captures a commanding 37.43% of the market, fueled by enterprises seeking cost-effective solutions for corporate communications and training. Synthesia's milestone of achieving USD 100 million in annual recurring revenue underscores the commercial potential of AI-generated video platforms, with a clientele boasting over 70% of Fortune 100 companies. Meanwhile, audio-based synthetic media emerges as the fastest-growing segment, charting a robust 12.71% CAGR, propelled by ElevenLabs' expansion of real-time dubbing services in 99 languages.

Image-based synthetic media reaps the rewards of generative AI advancements, particularly those tailored for European cultural nuances. Concurrently, text-based solutions are harnessing multilingual models like EuroLLM, adept at processing a staggering 4 trillion tokens across diverse EU languages. As the EU AI Act rolls out mandatory content labeling in August 2025, video and image sectors brace for heightened scrutiny, especially with deepfake detection becoming paramount for compliance. Highlighting the industry's shift, Bertelsmann's collaboration with ElevenLabs to develop audio tools showcases traditional media's embrace of synthetic technologies, streamlining their production timelines.

By Technology: Generative AI Dominance Meets NLP Momentum

Generative AI maintained 43.76% share of the Europe synthetic media market size in 2024, underpinned by Stability AI and Mistral AI’s rapid scaling. Natural language processing grows fastest at 12.83% through 2030 as enterprises seek culturally aware, legally sourced content in 24 official languages. The Europe synthetic media market benefits from public HPC access that accelerates model refinement without prohibitive capex.

Voice synthesis rides ElevenLabs’ USD 3.3 billion valuation to attract new verticals, especially healthcare, where synthetic audio improves patient engagement AR/VR frameworks converge with avatar pipelines as the EU’s virtual-worlds roadmap aligns funding and standard-setting.

By End-User Industry: Gaming Push Challenges Media Dominance

Media and entertainment retained 29.32% share of the Europe synthetic media market size in 2024, thanks to entrenched studio relationships and rapid ROI on localized video. Gaming and metaverse deployments, however, grow at a blistering 13.11% CAGR on the back of EUR 800 billion virtual-world value potential. Advertisers capitalize on AI avatars to cut multilingual campaign lead times, while e-commerce players deploy product-demo videos that heighten conversion metrics.

Education gains from cost-efficient training content; Colossyan users trimmed learning-video budgets by 80%. Healthcare uptake accelerates via the SYNTHIA synthetic-data initiative that de-risks privacy exposure. Financial services and telecom firms pilot synthetic voice agents to streamline customer support, balancing innovation with AI Act compliance.

Geography Analysis

Germany accounted for 31.21% of the Europe synthetic media market size in 2024.Germany's ascent in the European synthetic media landscape is fueled by its robust tech infrastructure, dynamic creative sectors, and a workforce renowned for its expertise. Both established digital studios and nimble startups are harnessing AI-driven content creation, diving into realms from virtual productions to synthetic influencers and voiceovers, igniting waves of innovation. Bolstered by ambitious government initiatives and synergistic public-private collaborations, investments in cutting-edge technologies flourish, cultivating a nurturing ground for startups. Furthermore, with a pronounced appetite for media content in the local language, especially tailored for German-speaking audiences, businesses are increasingly crafting bespoke synthetic media solutions, positioning Germany ahead of numerous European counterparts.

The United Kingdom grows at 13.23% CAGR, The country is strengthening its position in the European synthetic media market, driven by its dynamic creative industries, advanced technology ecosystem, and strong focus on innovation. London, in particular, has emerged as a key creative hub, where leading companies are leveraging AI to develop visual effects, virtual influencers, and immersive storytelling solutions. This growth is underpinned by a highly skilled talent pool of engineers, creatives, and entrepreneurs, alongside a favorable legal and business framework that promotes innovation. With rising consumer demand and accessible investment capital, the United Kingdom is playing a pivotal role in driving the expansion of synthetic media across Europe.

France blends sovereignty rhetoric with ambitious venture creation. Mistral AI’s EUR 2 billion valuation achieved in under a year demonstrates investor appetite for open-source, European-trained LLMs.National grants enable universities to refine diffusion models that safeguard cultural heritage, appealing to broadcasters and publishers. Italy differentiates through personality-rights protections that deter malicious deepfakes, carving a niche for “responsible AI as a service” platforms

The synthetic media market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Asia, South America, and Middle East and Africa.

Competitive Landscape

The Europe synthetic media market exhibits moderate fragmentation. Leaders leverage capital to hard-wire compliance into product roadmaps, converting regulation into competitive advantage. Synthesia and ElevenLabs each raised USD 180 million, earmarking funds for watermarking infrastructure and AI literacy programs. Adobe’s strategic stake in Synthesia signals incumbent alignment with specialist capabilities.

Open-source alliances such as OpenGPT-X lower development costs and foster a shared compliance baseline. Smaller vendors differentiate via domain expertise—healthcare synthetics, accessibility or creative verticals—while outsourcing heavy-lift regulatory tasks to consultancy partners. The Coalition for Content Provenance and Authenticity advances cross-industry standards that may accelerate consolidation as compliance overhead rises.

White-space opportunity lies in sovereign cloud integration, verified 3-D avatar pipelines and industry-specific synthetic datasets. Service providers that bundle technical toolkits with EU AI Act audits stand to capture value as enforcement nears.

Europe Synthetic Media Industry Leaders

Synthesia Limited

Stability AI Ltd

DeepMind Technologies Ltd

Speechmatics Ltd

AIVA Technologies SARL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: OpenAI has rolled out its Sora video generator in the European Union and Britain, just months after its debut in the U.S. and other regions. This cutting-edge technology enables users to craft high-resolution video clips. Subscribers of OpenAI's ChatGPT service can access Sora in the EU, UK, and select countries: Switzerland, Norway, Liechtenstein, and Iceland. Basic "Plus" subscribers are entitled to produce up to 50 standard-definition videos each month, each lasting approximately 20 seconds. However, "Pro" users, who pay a premium, can enjoy even more generous offerings.

- January 2025: ElevenLabs, a Polish company specializing in generative AI for audio, has partnered with Poland’s presidency of the Council of the European Union. Through a no-cost agreement, AI-driven audio technology will dub the content of each press conference, held after informal meetings of EU ministers in Warsaw, into Polish, English, and French.

- November 2024: OpenGPT-X, a prominent research initiative, has unveiled its latest offering: "Teuken-7B". Boasting seven billion parameters, Teuken-7B has been meticulously trained from the ground up in all 24 official languages of the European Union (EU). This endeavor was made possible with the expertise of Forschungszentrum Jülich and the computational prowess of the JUWELS supercomputer. Both researchers and enterprises can harness this open-source model, now commercially viable, for diverse artificial intelligence (AI) applications. The project, under the aegis of the OpenGPT-X consortium, received backing from the German Federal Ministry of Economic Affairs and Climate Action (BMWK). Spearheaded by the Fraunhofer Institutes – specifically the Institute for Intelligent Analysis and Information Systems IAIS and the Institute for Integrated Circuits IIS – the consortium has crafted a large language model that not only champions open-source principles but also embodies a distinctly European perspective.

Europe Synthetic Media Market Report Scope

| Audio-Based Synthetic Media |

| Image-Based Synthetic Media |

| Text-Based Synthetic Media |

| Video-Based Synthetic Media |

| Generative AI |

| Computer Graphics and Visual Effects |

| Natural Language Processing |

| Voice Synthesis and Recognition |

| Others (Augmented Reality and Virtual Reality, Generative Adversarial Networks, and others) |

| Media and Entertainment |

| Advertising and Marketing |

| Gaming and Metaverse |

| E-commerce and Retail |

| Education and Training |

| Healthcare and Life-Sciences |

| Other End-user Industries |

| United Kingdom |

| Germany |

| France |

| Italy |

| Rest of Europe |

| By Media Type | Audio-Based Synthetic Media |

| Image-Based Synthetic Media | |

| Text-Based Synthetic Media | |

| Video-Based Synthetic Media | |

| By Technology | Generative AI |

| Computer Graphics and Visual Effects | |

| Natural Language Processing | |

| Voice Synthesis and Recognition | |

| Others (Augmented Reality and Virtual Reality, Generative Adversarial Networks, and others) | |

| By End-User Industry | Media and Entertainment |

| Advertising and Marketing | |

| Gaming and Metaverse | |

| E-commerce and Retail | |

| Education and Training | |

| Healthcare and Life-Sciences | |

| Other End-user Industries | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe synthetic media market in 2025?

The Europe synthetic media market size is USD 1.78 billion in 2025 and is projected to reach USD 3.23 billion by 2030.

Which segment is growing fastest within European synthetic media?

Audio-based solutions register the highest 12.71% CAGR for 2025-2030 as enterprises demand multilingual dubbing and accessibility features.

Which country leads Europe in synthetic media revenue?

Germany holds 31.21% of regional revenue in 2024, underpinned by EUR 1 billion federal AI funding and strong creative industries.

Why is compliance important for European synthetic media vendors?

The EU AI Act imposes watermarking, transparency and potential fines up to EUR 35 million, making compliance a core differentiator.

What drives investment in European synthetic media startups?

Sovereign data priorities, multilingual market needs and public funding for HPC resources lower technical hurdles and attract venture capital.

Page last updated on: