Middle East And Africa Synthetic Media Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

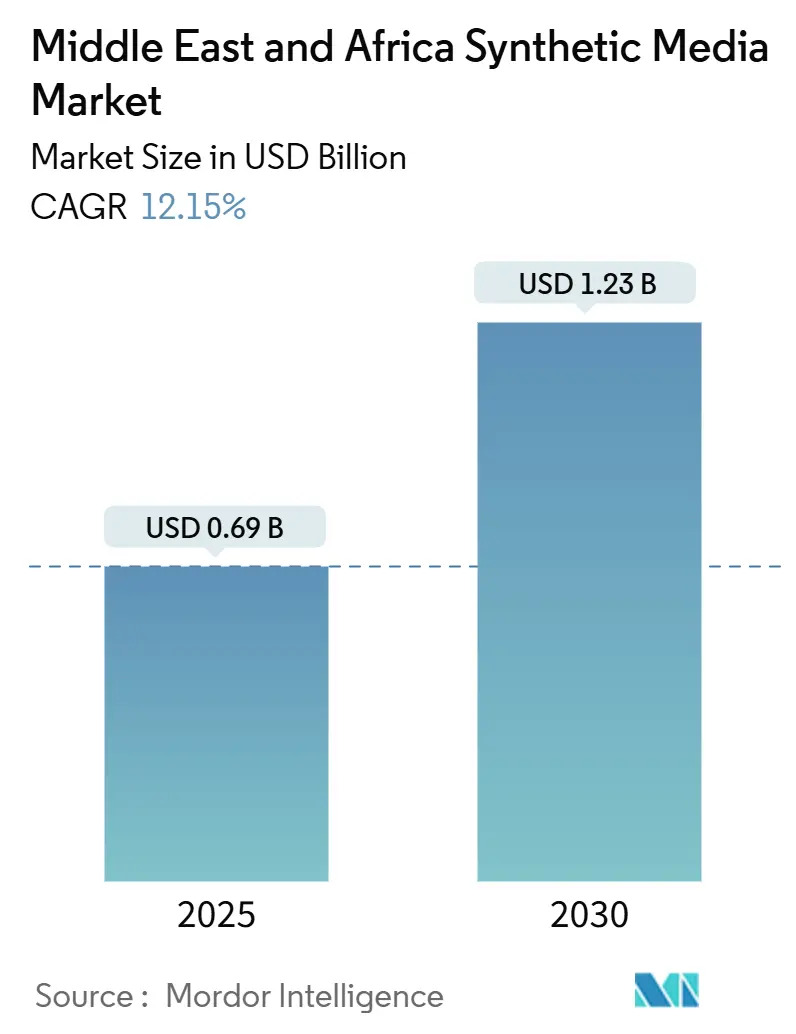

| Market Size (2025) | USD 0.69 Billion |

| Market Size (2030) | USD 1.23 Billion |

| Growth Rate (2025 - 2030) | 12.15% CAGR |

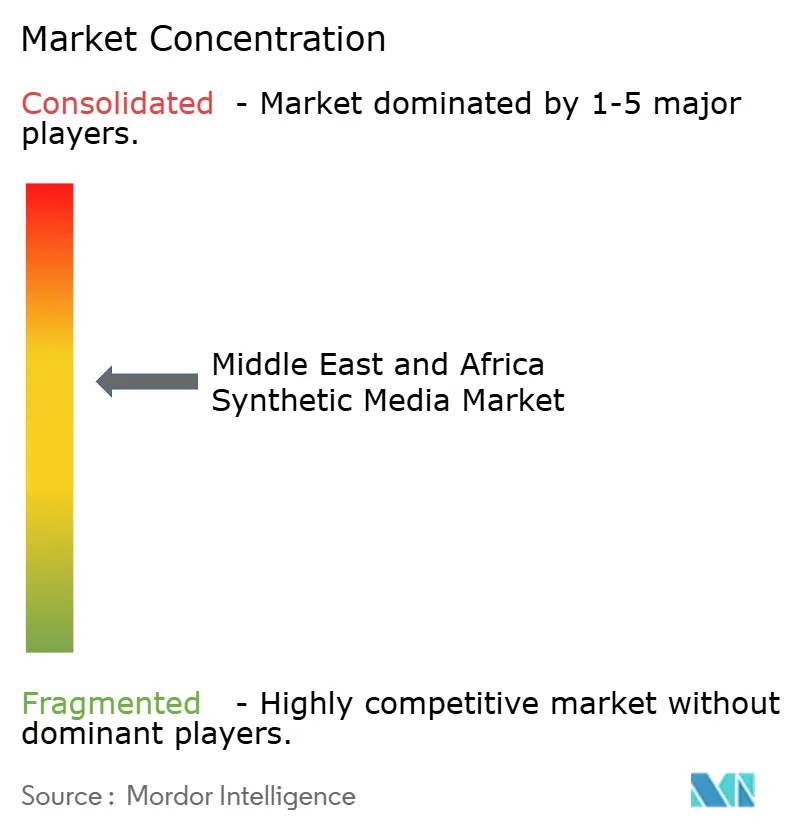

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Synthetic Media Market Analysis by Mordor Intelligence

The Middle East and Africa synthetic media market size stands at USD 0.69 billion in 2025 and is forecast to reach USD 1.23 billion by 2030, expanding at 12.15% CAGR. Surging government digital-transformation programs, a fivefold jump in sovereign-wealth-fund financing for generative-AI startups, and rapid advances in Arabic language models are accelerating enterprise and consumer deployments of video, audio, and text synthesis solutions across the region. Multilingual content localization has moved from experimental to enterprise scale, while public-sector AI budgets in Saudi Arabia and the UAE are enlarging procurement pipelines for synthetic media platforms. Strategic alliances such as Microsoft’s USD 1.5 billion stake in G42 and Google Cloud’s USD 10 billion partnership with Saudi Arabia’s Public Investment Fund are attracting global vendors that view the Middle East and Africa synthetic media market as a launchpad for emerging-market expansion. Although misinformation risks and dataset shortages persist, breakthroughs like G42’s JAIS 70B model show the region’s capacity to internalize key bottlenecks and localize innovation.

Key Report Takeaways

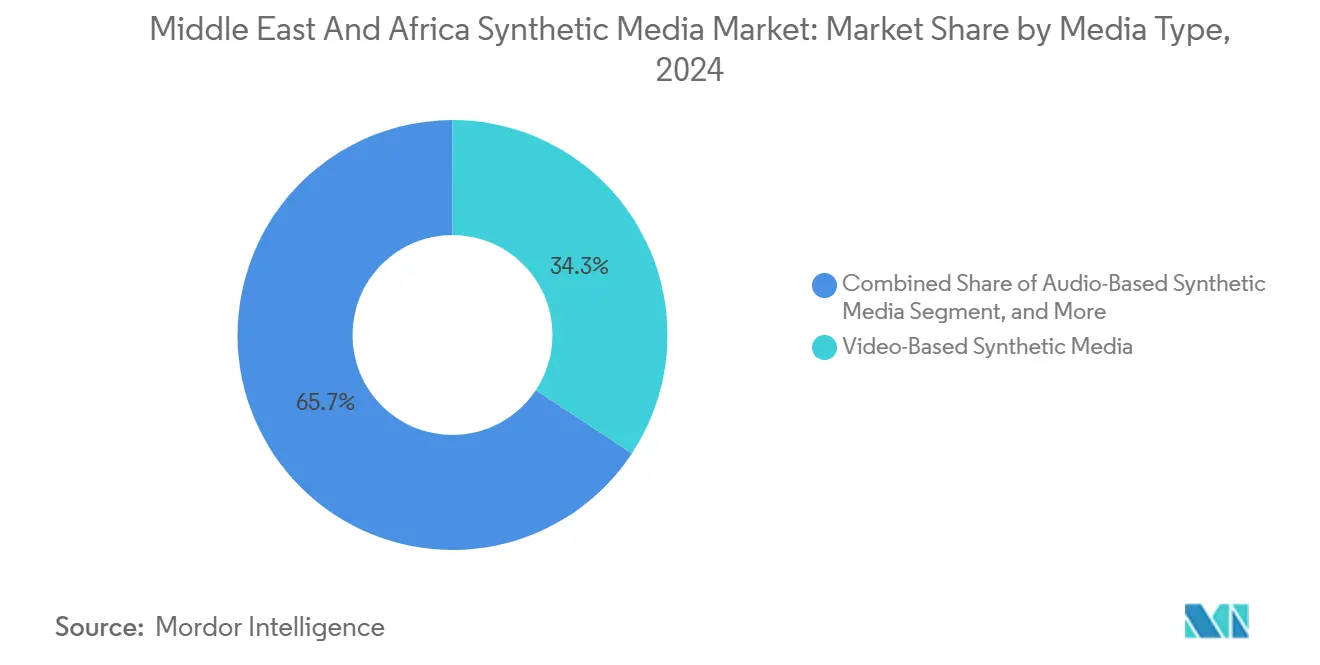

- By media type, video content led with 34.29% revenue share in 2024; audio-based applications are projected to advance at an 11.17% CAGR to 2030.

- By technology, generative AI captured 41.68% of the Middle East and Africa synthetic media market share in 2024, while natural-language processing is forecast to grow at a 13.87% CAGR through 2030.

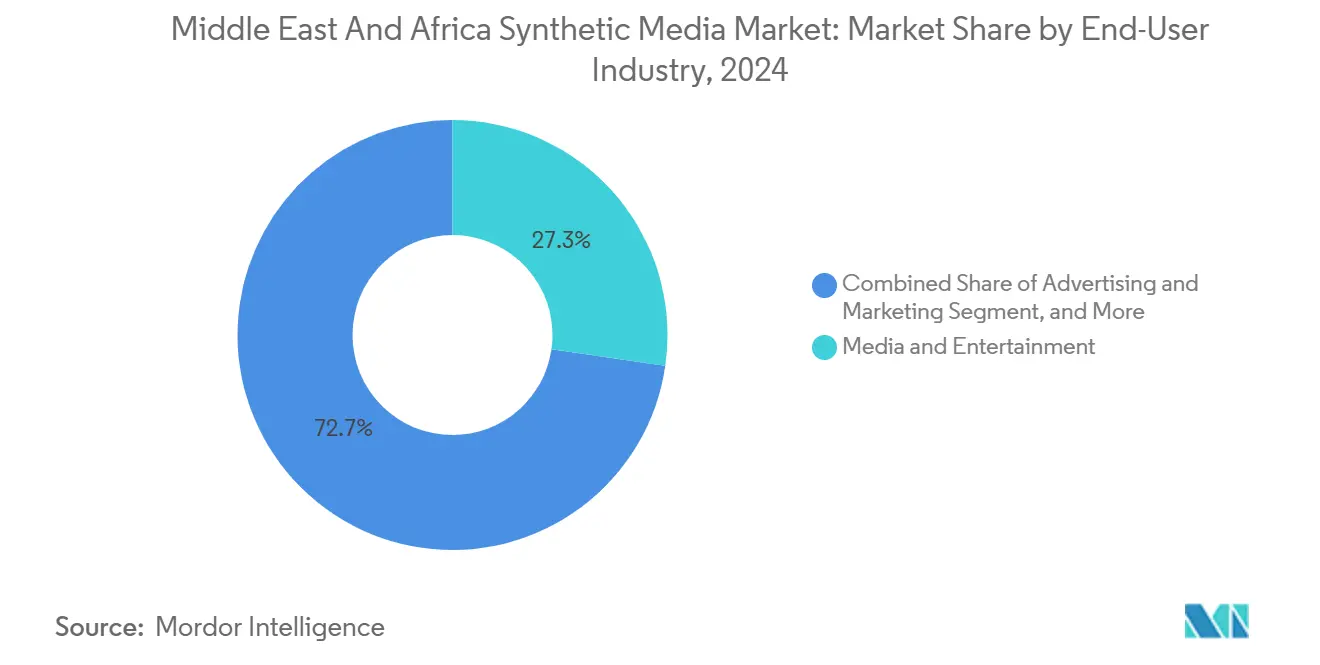

- By end-user industry, media and entertainment commanded 27.29% of the Middle East and Africa synthetic media market size in 2024, whereas gaming and metaverse applications are on track for a 12.94% CAGR between 2025 and 2030.

Competitive positioning in Middle east and africa includes both locally based firms and those operating across multiple regions. The market landscape in the global synthetic media industry research shows how these players are arranged internationally.

Middle East And Africa Synthetic Media Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of AI-driven content localization | +2.8% | UAE, Saudi Arabia, Egypt | Medium term (2-4 years) |

| Escalating demand for multilingual video production | +2.1% | Global, concentrated in Middle East and North Africa | Short term (≤ 2 years) |

| Government digital-transformation programme | +3.2% | Saudi Arabia, UAE, Egypt | Long term (≥ 4 years) |

| Sovereign-wealth fund investments in GenAI start-ups | +2.4% | GCC states, spillover to Africa | Medium term (2-4 years) |

| Growth of Arabic audio learning apps | +1.5% | Middle East and North Africa region, North Africa | Short term (≤ 2 years) |

| Synthetic avatars for tele-pharmacies | +1.8% | Regional, early adoption in UAE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Digital-Transformation Programmes

Public-sector modernization budgets are galvanizing adoption across the Middle East and Africa synthetic media market. Vision 2030 earmarked USD 40 billion for Saudi AI investments, while the UAE targets a USD 100 billion economic contribution from AI by 2031.[1]Abu Dhabi Aims to be World’s First Fully AI-Native Government across all Digital Services by 2027 https://www.akingump.com/en/insights/ai-law-and-regulation-tracker/abu-dhabi-aims-to-be-worlds-first-fully-ai-native-government-across-all-digital-services-by-2027Abu Dhabi plans to become the first fully AI-native government by 2027 with AED 13 billion devoted to more than 200 AI solutions. Egypt’s new AI strategy seeks 250 domestic AI firms and 30,000 skilled professionals by 2030, bolstered by IBM’s pledge to train 100,000 Egyptians. These initiatives are streamlining procurement, establishing regulatory sandboxes, and underwriting the cloud and data infrastructure on which synthetic media services depend. As ministries shift citizen-facing portals to avatar-based interfaces, public-sector demand is expected to filter down to healthcare, education, and tourism enterprises, reinforcing long-term market momentum.

Sovereign-Wealth Fund Investments in GenAI Start-ups

Sovereign investors are accelerating the Middle East and Africa synthetic media market through large capital injections. Saudi Arabia’s Public Investment Fund is negotiating a USD 40 billion AI partnership with Andreessen Horowitz, and the UAE’s new MGX fund has set a USD 100 billion target for AI infrastructure. Qatar and Kuwait funds trebled AI allocations during 2024. This liquidity enables local startups such as Qeen.ai and Halo AI to raise multi-million-dollar seed rounds, while simultaneously enticing global vendors to open regional research hubs. The resulting ecosystem tightens feedback loops between capital, research, and commercialization, reducing time-to-market for Arabic-first models and expanding accessible use-cases from automated dubbing to virtual retail assistants.

Escalating Demand for Multilingual Video Production

Entertainment, education, and corporate users increasingly require rapid, cost-efficient video localization. IMAX deployed CAMB.AI’s speech-to-speech translation engine to roll out real-time dubbing of blockbuster releases across MENA theaters. At the enterprise level, more than 70% of Fortune 100 firms now rely on Synthesia’s avatar platform for internal communications, doubling adoption compared with 2023.[2]Synthesia surpasses $100 million in annual recurring revenue and secures strategic investment from Adobe Ventures https://www.synthesia.io/post/100-million-revenue-adobe-investment Advances in large Arabic models like G42’s JAIS 70B have slashed turnaround times for high-fidelity subtitles and lip-synched avatars, lowering production costs and growing addressable audiences. As regional streaming alliances expand cross-border catalogs, demand for multilanguage tools should keep the Middle East and Africa synthetic media market on a double-digit growth trajectory.

Rapid Adoption of AI-driven Content Localization

Localization capabilities are becoming more granular, shifting from generic Modern Standard Arabic to dialect-specific engines. AtlasIA’s Terjman V2 matches GPT-4-level accuracy for Moroccan Darija, while CNTXT AI’s Munsit-1 achieves a 26.68% word-error rate across six Arabic benchmarks. Dubai’s regulatory framework for synthetic data permits developers to customize content without violating privacy rules. In education, 3D teacher avatars are enhancing remote classrooms, and the 1000 African Voices project is extending coverage to 86 African accents. [3]1000 African Voices: Advancing inclusive multi-speaker multi-accent speech synthesis https://arxiv.org/abs/2406.11727Such depth in linguistic nuance unlocks hyper-personalized marketing, training, and public-service interactions, strengthening user trust and widening engagement funnels across the Middle East and Africa synthetic media market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deep-fake-related misinformation concerns | -1.8% | Global, heightened in conflict zones | Short term (≤ 2 years) |

| Scarcity of high-quality Arabic training datasets | -2.1% | MENA region, North Africa | Medium term (2-4 years) |

| Religious-content compliance hurdles | -1.2% | Islamic majority countries | Long term (≥ 4 years) |

| Fragmented AI-IP enforcement | -1.5% | Regional, cross-border challenges | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Deep-fake-related Misinformation Concerns

Political deepfakes depicting President Zelensky or African heads of state illustrate how synthetic content can undermine public trust. Saudi Arabia’s SDAIA issued consent-based deepfake guidelines, and the UAE introduced fines up to AED 1 million for unauthorized AI-generated media. While detection tools are improving, heightened scrutiny raises compliance costs for legitimate providers within the Middle East and Africa synthetic media market. Short-term uncertainty may delay rollouts in election-sensitive jurisdictions, but transparent watermarking and regional fact-checking consortia are expected to mitigate risk over time.

Scarcity of High-quality Arabic Training Datasets

Arabic’s complex morphology and dialect diversity demand large, curated corpora that remain limited. Commercial projects rely on patchwork resources, inflating model-training costs and limiting performance relative to English peers. Cultural sensitivities restrict data harvesting for voice and video, slowing progress in conversational avatars. Collaborative efforts such as G42’s open-source JAIS 70B and IBM’s data-donation program in Egypt are beginning to relieve the bottleneck, yet the deficit is forecast to cap near-term accuracy gains across the Middle East and Africa synthetic media market until at least 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Media Type: Video Maintains Leadership While Audio Accelerates

Video-based content accounted for a 34.29% Middle East and Africa synthetic media market share in 2024, underpinned by enterprise adoption of AI-rendered presenters and studio-quality CGI avatars. The segment benefits from robust broadband rollouts and high mobile-video consumption rates across GCC economies. Demand from e-learning portals and corporate L&D divisions is keeping utilization rates high, while studio partnerships with IMAX and MBC further validate commercial value.

Audio-based synthesis is projected to expand to an 11.17% CAGR, positioning it as the fastest-growing slice of the Middle East and Africa synthetic media market. CAMB.AI’s MARS5 engine, which covers more than 140 languages, and CNTXT AI’s speech-to-text milestones are shrinking production cycles for podcasts, audiobooks, and IVR systems. Cross-platform integration lets enterprises pair Arabic voice cloning with video avatars, curbing localization budgets by up to 60% compared with traditional dubbing.

By Technology: Generative AI Dominates, NLP Outpaces

Generative models held 41.68% of the Middle East and Africa synthetic media market in 2024, reflecting their maturity and broad application—from facial animations to large-scale scene generation. Investments by Adobe and United Al Saqer Group into companies like Synthesia and DNEG are funneling capital toward GPU clusters and proprietary diffusion engines, raising competitive barriers.

Natural-language processing is forecast to grow at 13.87% CAGR, the highest among the technology stacks. Breakthroughs such as Mistral AI’s Saba model and Falcon Arabic have narrowed the accuracy gap with English models while slashing inference costs. NLP advancements enable context-aware subtitle timing, emotion tagging, and script generation, magnifying the addressable spend of the Middle East and Africa synthetic media market size in content, commerce, and customer service.

By End-User Industry: Entertainment Leads, Gaming Races Ahead

Media and entertainment represented 27.29% of the Middle East and Africa synthetic media market size in 2024, driven by streaming wars and multiplex localization needs. Studios deploy AI for rapid dubbing and low-cost CGI, while broadcasters use real-time avatar anchors to personalize news segments. Monetization models now include synthetic-influencer merchandising and virtual-concert ticketing, underscoring long-term stickiness.

Gaming and metaverse platforms are on track for a 12.94% CAGR, making them the fastest-growing consumer of synthetic media across the region. VUZ’s USD 12 million funding and Saudi esports investments illustrate growing appetite for immersive avatars and real-time language translation inside multiplayer titles. Brands exploit these worlds for experiential campaigns, thereby linking advertising budgets to synthetic-world engagement metrics.

Geography Analysis

Saudi Arabia and the UAE anchor the Middle East portion of the Middle East and Africa synthetic media market. Saudi initiatives include a draft Global AI Hub law proposing three hub tiers and data-embassy privileges designed to attract foreign model developers. High-bandwidth 5G roll-outs and state-subsidized GPU clusters support large-scale synthetic-video rendering for entertainment and government e-services. Riyadh’s requirement for Arabic-first user interfaces compels providers to refine dialect specificity, driving R&D investments into localized training data.

The UAE’s growth story features aggressive public-private partnerships. Microsoft’s USD 1.5 billion equity stake in G42 coupled with Abu Dhabi’s AI-native-government roadmap signals long-term institutional demand. Regulatory innovation, such as the AI-powered rule-interpretation portal, compresses approval cycles for new products, giving the UAE first-mover advantage in the Middle East and Africa synthetic media market. Free-zone incentives and 0% corporate tax on qualifying AI activities further accelerate startup formation.

Africa’s opportunity is substantial but geographically fragmented. Egypt leverages its large developer workforce and IBM’s training pledge to create an AI-ready talent pool. Kenya’s National AI Strategy prioritizes multilingual data sets and digital-ID integration, boosting synthetic-media prospects in public-health campaigns. Nigeria and South Africa are refining AI-IP statutes and cloud-sovereignty provisions that aim to balance innovation with consumer protection. Sub-Saharan connectivity upgrades, including pan-African fiber projects, are laying network foundations essential for latency-sensitive voice-cloning services and cloud-rendered avatars.

Mordor Intelligence tracks the synthetic media market across other major regions such as North America, Europe, and Asia.

Competitive Landscape

Global tech majors and regional champions jointly shape a moderately concentrated Middle East and Africa synthetic media market. OpenAI, Google, and Meta supply foundational models, but local firms like CAMB.AI, G42, and CNTXT AI differentiate through Arabic accuracy and cultural alignment. Microsoft’s strategic investment in G42 grants preferred-partner access to sovereign datasets and accelerates deployment of Azure-based media pipelines inside GCC states.

Regional entertainment conglomerates are integrating synthetic-media toolkits to streamline production. DNEG’s USD 200 million Abu Dhabi hub illustrates vertical integration from VFX to AI-driven scene generation, reducing reliance on offshore post-production. Qatari and Kuwaiti funds add financial muscle, often demanding local compute footprints as a condition for equity stakes, thereby boosting domestic cloud-capacity buildouts.

White-space competitors focus on healthcare avatars, AI tutors, and retail-chat companions. Seed-stage rounds for Qeen.ai and Halo AI show early traction for e-commerce personalization and creator-economy tools. Compliance know-how is emerging as a moat; vendors versed in UAE deepfake fines and Saudi consent rules gain trusted-partner status, easing procurement hurdles for multinational clients exploring the Middle East and Africa synthetic media market.

Middle East And Africa Synthetic Media Industry Leaders

Meta Platforms Inc.

NVIDIA Corporation

Adobe Inc.

XPANSE CGI

UTURN Entertainment

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Google Cloud and Saudi Arabia’s PIF are launching a global AI hub in Riyadh with Saudi tech firm Humain, backed by a USD 10 billion investment. The hub will drive AI innovation for Saudi and American companies in the region.

- January 2025: Abu Dhabi has launched its Digital Strategy 2025–2027, investing AED13 billion to build an AI-powered government. Led by DGE, the plan includes full cloud adoption, process automation, 200+ AI solutions, and citizen training to boost innovation and security.

Middle East And Africa Synthetic Media Market Report Scope

| Audio-Based Synthetic Media |

| Image-Based Synthetic Media |

| Text-Based Synthetic Media |

| Video-Based Synthetic Media |

| Generative AI |

| Computer Graphics and Visual Effects |

| Natural Language Processing |

| Voice Synthesis and Recognition |

| Others (AR and VR, Generative Adversarial Networks, and others) |

| Media and Entertainment |

| Advertising and Marketing |

| Gaming and Metaverse |

| E-commerce and Retail |

| Education and Training |

| Healthcare and Life-Sciences |

| Other End-user Industries |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Kuwait | |

| Bahrain | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Media Type | Audio-Based Synthetic Media | |

| Image-Based Synthetic Media | ||

| Text-Based Synthetic Media | ||

| Video-Based Synthetic Media | ||

| By Technology | Generative AI | |

| Computer Graphics and Visual Effects | ||

| Natural Language Processing | ||

| Voice Synthesis and Recognition | ||

| Others (AR and VR, Generative Adversarial Networks, and others) | ||

| By End-User Industry | Media and Entertainment | |

| Advertising and Marketing | ||

| Gaming and Metaverse | ||

| E-commerce and Retail | ||

| Education and Training | ||

| Healthcare and Life-Sciences | ||

| Other End-user Industries | ||

| By Country | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Kuwait | ||

| Bahrain | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Middle East and Africa synthetic media market?

It is valued at USD 0.69 billion in 2025, with projections reaching USD 1.23 billion by 2030.

Which segment is growing fastest within regional synthetic media?

Natural-language processing technologies are forecast to post a 13.87% CAGR through 2030.

Why are Saudi Arabia and the UAE central to synthetic-media expansion?

Both governments have multi-billion-dollar AI funds, progressive regulations, and large-scale cloud infrastructure that attract global vendors.

How are sovereign wealth funds influencing market growth?

GCC-based sovereign funds increased AI allocations fivefold, providing capital to local startups and luring foreign partners.

Page last updated on: