Benelux MVNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

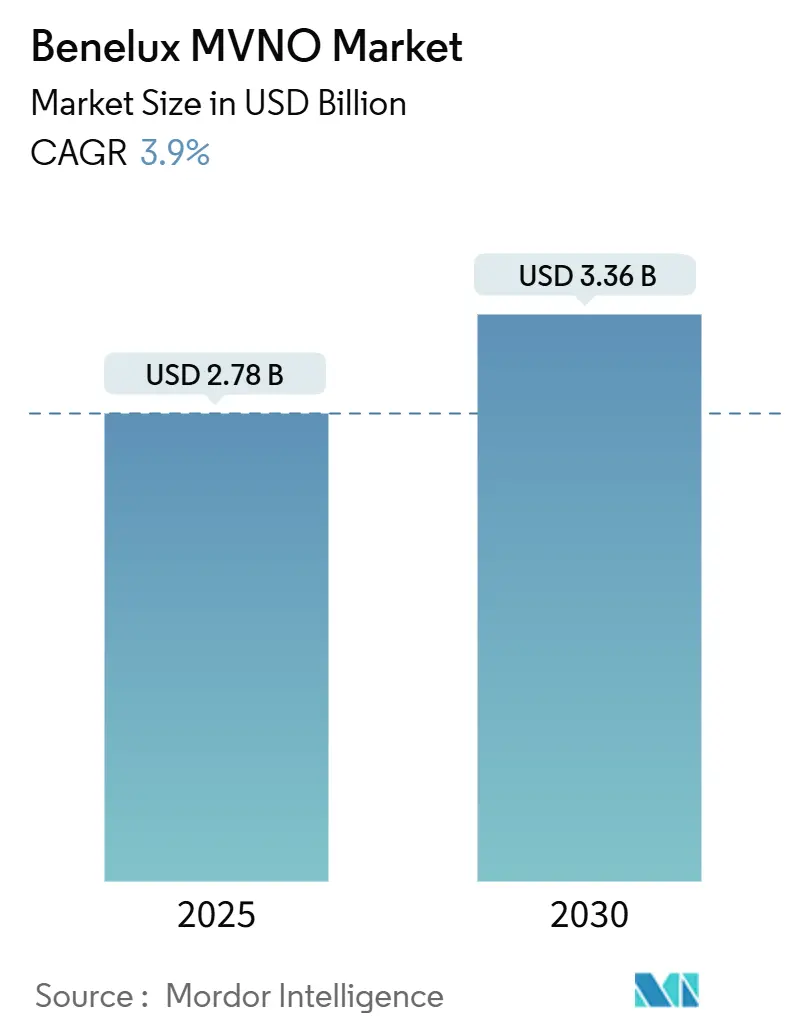

| Market Size (2025) | USD 2.78 Billion |

| Market Size (2030) | USD 3.36 Billion |

| Growth Rate (2025 - 2030) | 3.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benelux MVNO Market Analysis by Mordor Intelligence

The Benelux MVNO Market size is estimated at USD 2.78 billion in 2025, and is expected to reach USD 3.36 billion by 2030, at a CAGR of 3.9% during the forecast period (2025-2030). In terms of market size, the market is expected to grow from 4 million subscriber in 2025 to 4.94 million subscriber by 2030, at a CAGR of 4.25% during the forecast period (2025-2030).

The Benelux MVNO market benefits from nationwide 4G saturation, 95% 5G household coverage in Belgium, and clear wholesale-access rules that let virtual operators piggy-back on the radio networks of Proximus, KPN, Orange, Telenet and POST. Reseller and Light MVNO modes still dominate volumes, yet a steady pivot toward Full MVNO architectures is visible as cloud-native business-support systems shrink upfront costs. Enterprise IoT connectivity, e-SIM–based digital onboarding, and EU-wide wholesale rate-cap extensions underpin incremental revenue streams even as price competition heats up. Consolidation remains a parallel force: KPN bought Youfone for USD 200 million in 2024 while Waterland Private Equity acquired Lebara for EUR 513 million, signaling how incumbents view virtual brands as valuable channel assets.

Key Report Takeaways

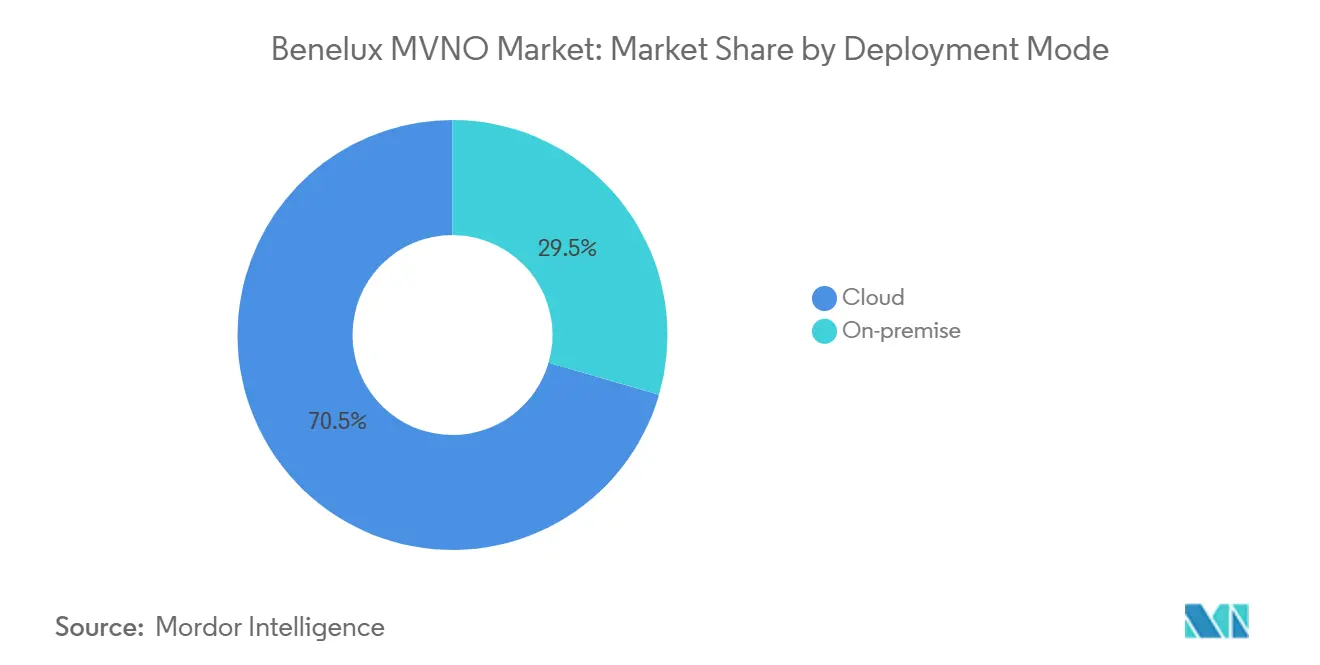

- By deployment model, cloud-hosted solutions controlled 70.51% of 2024 revenue while also delivering the fastest 8.21% CAGR through 2030.

- By operational mode, Reseller and Light MVNOs held 59.62% of 2024 revenue; in contrast, Full MVNOs are set to post the highest 14.75% CAGR to 2030.

- By subscriber type, the consumer segment contributed 84.08% of revenue in 2024, whereas IoT-specific lines show the strongest 23.56% CAGR to 2030.

- By application, discount propositions captured 41.52% of 2024 revenue; cellular M2M connectivity advances at a 21.94% CAGR over the forecast horizon.

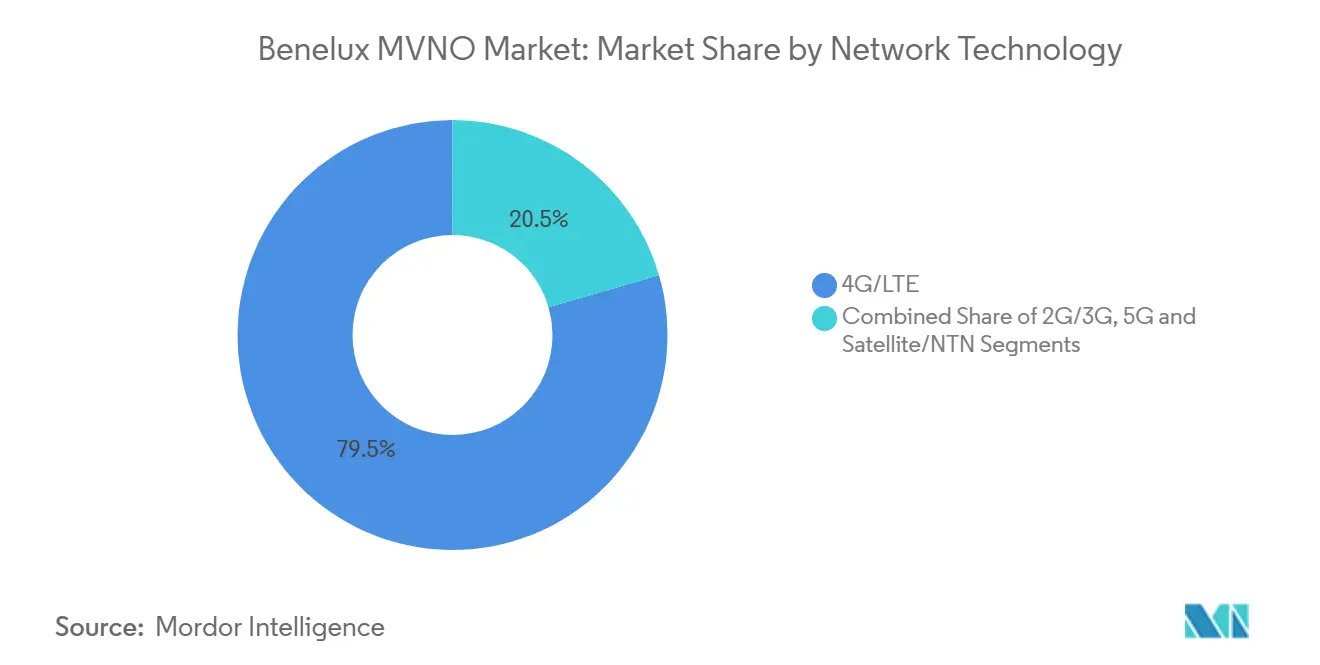

- By network technology, 4G/LTE accounted for 78.69% of 2024 connections, yet 5G subscriptions rise at a robust 28.33% CAGR to 2030.

- By distribution, online and app-only channels attracted 58.04% of gross additions in 2024 and will expand at a 6.66% CAGR to 2030.

Benelux MVNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for low-cost data-centric plans | +0.8% | Belgium, Netherlands, Luxembourg | Medium term (2-4 years) |

| Rise of e-SIM & digital-only onboarding | +0.6% | Netherlands core; spill-over to Belgium | Short term (≤ 2 years) |

| Enterprise IoT connectivity outsourcing | +0.7% | Dutch & Belgian industrial zones | Long term (≥ 4 years) |

| EU wholesale rate-cap extension after 2025 | +0.5% | EU-wide; Benelux included | Medium term (2-4 years) |

| Satellite-NTN back-haul for remote areas | +0.3% | Luxembourg; rural Belgium & Netherlands | Long term (≥ 4 years) |

| ESG-driven “green SIM” offerings | +0.2% | Urban centers across Benelux | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for low-cost data-centric plans

The Benelux MVNO market gains momentum from a widening gap between premium tariffs at host MNOs and deeply discounted bundles from virtual brands. DIGI Belgium’s arrival triggered aggressive EUR 5 unlimited-data offers by hey!telecom against Proximus’s EUR 24.99 for 50 GB, steering data-hungry youth toward MVNOs.[1]Test-Aankoop, “Mobile Tariff Benchmarking 2024,” test-aankoop.be Belgian mobile-data traffic has tripled since 2019 as reported by the national regulator, confirming a secular shift toward heavy-data usage. [2]Belgian Institute for Postal Services and Telecommunications, “Annual Telecom Report 2024,” bipt.beWith wholesale LTE and 5G access priced at regulated ceilings, virtual operators transform this consumption surge into subscriber gains without shouldering network CAPEX. Price-led switching is especially pronounced among prepaid migrants and students who show low brand allegiance yet high elasticity to gigabyte pricing. Consequently, discount-focused brands continue to reinforce the overall Benelux MVNO market narrative of value leadership.

Rise of e-SIM and digital-only onboarding

Digital onboarding reduces acquisition costs by roughly 40% versus retail stores, a structural edge for the Benelux MVNO market. The Netherlands leads adoption: KPN, Odido and multiple MVNOs already support fully digital activation that completes within minutes. Belgian regulators support transparency dashboards that list e-SIM-capable devices and coverage maps, catalyzing take-up. Automation also embeds KYC checks that meet stricter anti-fraud mandates without human intervention, letting smaller brands scale faster. International MVNOs such as Lycamobile gain extra utility because cross-border travelers can add local plans instantly, minimizing churn lost to roaming charges. Cloud-native BSS stacks from Netcracker underpin these journeys, allowing MVNOs to launch campaigns in weeks rather than quarters.

Enterprise IoT connectivity outsourcing

Factories, ports and logistics hubs across Rotterdam, Antwerp and Eindhoven increasingly outsource SIM life-cycle management to specialists, accelerating IoT line growth within the Benelux MVNO market. Proximus offers managed private-LTE services that bundle SIMs, devices and analytics, illustrating how host carriers cooperate rather than compete in this niche. IoT MVNOs differentiate through NB-IoT and LTE-M profiles optimized for low-power industrial sensors, supporting predictive-maintenance use cases. Regulations under BEREC allow permanent roaming for machines, easing deployment hurdles across borders. Enterprises favor multi-year service contracts, stabilizing revenue streams against volatile consumer churn. As Industry 4.0 budgets rise, IoT connections will expand faster than human subscriber lines, diversifying the revenue mix for the Benelux MVNO market.

EU wholesale rate-cap extension after 2025

The European Commission’s decision to prolong voice, SMS and data roaming caps safeguards margin visibility for smaller brands that lack scale to negotiate deep discounts. BEREC monitoring shows nearly one-third of roaming providers would operate at a loss if caps expired, so regulatory continuity is material for the Benelux MVNO market. Predictable costs let MVNOs lock in multi-year customer pricing without hedging for upstream volatility. Migrant-focused players such as Lebara and Lycamobile rely on this certainty to bundle generous intra-EU allowances. Host MNOs are obliged to offer 4G and 5G access under technology-neutral clauses, preventing quality discrimination that could otherwise undermine the MVNO value proposition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter KYC & anti-fraud mandates | -0.4% | EU-wide; Benelux included | Short term (≤ 2 years) |

| Margin squeeze from 5G network-slicing fees | -0.7% | Netherlands & Belgian 5G zones | Medium term (2-4 years) |

| Intensified price warfare from new entrant DIGI | -0.3% | Belgium | Short term (≤ 2 years) |

| Heightened antitrust probes into fiber sharing | -0.2% | Belgium, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter KYC and anti-fraud mandates

Identity-verification updates that require bank-grade checks add friction to prepaid onboarding and elevate overhead for migrant-focused MVNOs. Belgium now obliges real-time government-ID validation for every SIM, and Dutch authorities levy fines for documentation lapses. Virtual brands catering to transient workers risk elongating signup flows, which could erode the Benelux MVNO market’s traditional speed advantage. The new rules also force upgrades to back-office APIs and facial-recognition tools, straining thin IT budgets. While compliance bolsters network security, it may curb net-add velocity for smaller entrants in the near term.

Margin squeeze from 5G network-slicing fees

Network slicing lets host MNOs tier wholesale quality and charge premiums for low-latency slices—an option many MVNOs view as unavoidable for enterprise clients. Early fee proposals suggest uplifts of 15-20% over standard 5G access, compressing the gross margin cushion in the Benelux MVNO market. [3]Orange Belgium, “Satellite-NTN Service Launch Press Note,” corporate.orange.beFull MVNOs that bought their own core hope to offset costs by arbitraging across multiple hosts, yet negotiations remain asymmetric. If fees push final prices upward, price-sensitive SMEs might remain on 4G service levels, slowing uptake of advanced IoT packages and undermining revenue projections.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Flexibility

Cloud-based deployments generated 70.51% of 2024 revenue, the highest share within the Benelux MVNO market. Operators adopt hyperscale infrastructure to spin up new rate plans, integrate e-SIM APIs and support multi-tenant billing without owning physical data centers. This approach also positions brands for 5G core upgrades because network functions are delivered as software. On-premise setups linger in tightly regulated finance verticals, yet their slower 2.3% CAGR keeps them marginal.

The Benelux MVNO market therefore favors OPEX-light architectures that free capital for marketing. Telenet’s migration to a Netcracker SaaS stack allowed partner brands to shorten time-to-market for promotions from eight weeks to ten days, driving agility. International groups such as Lebara similarly rely on a single cloud spine to serve five European countries, ensuring compliance mapping by locale while avoiding duplicated infrastructure teams. As wholesale 5G SA launches begin, cloud-native cores will be essential for dynamic network slicing brokerage, reinforcing their strategic weight.

By Operational Mode: Full MVNO Models Gain Control

Reseller and Light modes still headline 59.62% of 2024 turnover for the Benelux MVNO market, delivering rapid market entry with minimal technical lift. Yet Full MVNOs grow 14.75% per year, reflecting a quest for gross-margin lift and freedom to multi-host across borders. Full players maintain their own HLR/HSS and can negotiate separate transit deals, letting them arbitrage termination costs.

Regulatory guardrails from BEREC guarantee nondiscriminatory 5G access, encouraging scale-ups to invest in EPC or 5GC assets. Mobile Vikings took this path before its sale to Proximus, leveraging deeper network control to create youth-oriented bundles. Meanwhile, service-operator intermediates such as Youfone demonstrate a hybrid route: owning the brand and customer care while outsourcing heavy network logic until scale justifies further capex. The shift underscores how technical sovereignty is now a lever for value extraction in the Benelux MVNO market.

By Subscriber Type: Enterprise IoT Segments Accelerate Growth

Consumers accounted for 84.08% of 2024 lines, mirroring the historic prepaid focus of the Benelux MVNO market. However, IoT-only profiles will post the quickest 23.56% CAGR, expanding the total SIM base far beyond population ceilings. Enterprises prefer managed-connectivity contracts bundled with analytics, private APNs and SLA dashboards, which MVNOs can supply without retail overhead.

Longer device lifecycles in logistics and utilities extend average revenue life, stabilizing cash flows. Permanent-roaming clauses now embedded in EU rules let a Dutch-issued SIM roam indefinitely in Belgian smart-city cameras, removing provisioning complexity. For MVNOs, this structural demand shift opens fresh upsell paths, counterbalancing flat consumer ARPU trends that otherwise cap topline growth.

By Application: M2M Connectivity Transforms Industry

Discount voice-and-data bundles still represented 41.52% of 2024 spend, underlining the Benelux MVNO market’s price-led heritage. Yet cellular M2M contracts demonstrate a 21.94% CAGR, buoyed by metering, asset-tracking and industrial-sensor rollouts. Because devices tend to be SIM-locked to a single service for years, churn is negligible; as a result, lifetime value eclipses that of prepaid handsets.

Orange Belgium’s new satellite-NTN add-on at EUR 49 per month exemplifies how MVNOs can stitch together hybrid footprints for remote oil pipelines or wind farms, a capability not economical for purely terrestrial networks. As enterprises digitalize operations end-to-end, demand for low-bit-rate, high-volume SIM estates will keep rising, inserting fresh momentum into the Benelux MVNO market.

By Network Technology: 5G Deployment Reshapes Economics

4G/LTE furnished 78.69% of active lines in 2024 after a decade of near-complete coverage. Belgium’s 95% household 5G reach, validated by BIPT surveys, sets the stage for a rapid swing to next-gen radios BIPT.BE. The 5G slice market accelerates at 28.33% CAGR, promising latency-sensitive industrial control and cloud gaming services.

Legacy 2G/3G networks face sunset dates by 2027, pushing M2M operators to upgrade modules or arrange fallback roaming files. Satellite/NTN links, still small, offer a resiliency premium for mission-critical sectors. Taken together, spectrum shifts will recast wholesale fee structures and service portfolios across the Benelux MVNO market.

By Distribution Channel: Digital Transformation Accelerates Acquisition

Online portals, brand apps and third-party e-wallets delivered 58.04% of 2024 gross adds and will grow 6.66% annually. Digital KYC and e-SIM provisioning compress the signup funnel to under five minutes, appealing to mobile-first Gen-Z audiences and roaming professionals alike. Physical stores remain pertinent for device finance and elderly support but see flat traffic.

Carrier sub-brands exploit owned retail to upsell fixed-mobile bundles, while SIM wholesalers like SuperSim supply supermarkets under white-label chalkboard pricing. The overarching direction points to a low-touch, API-driven commerce stack that reinforces the cost advantage of the Benelux MVNO market.

Geography Analysis

Belgium anchors the Benelux MVNO market with four host MNOs and 95% 5G household coverage, ensuring virtual brands can launch premium tiers without dead-zone risk. BIPT enforces technology-neutral wholesale terms, and the Belgian Competition Authority polices fiber-sharing pacts, both actions keeping the playing field level. Proximus’s purchase of Mobile Vikings highlights the strategic value incumbents place on youth-centric digital brands.

The Netherlands contributes elevated growth through early e-SIM adoption and corporate IoT outsourcing. KPN, Odido and Vodafone grant multi-network wholesale deals, and ACM’s oversight of the EU Digital Services Act extends compliance duties to app-store channels, intersecting MVNO acquisition funnels. KPN’s USD 200 million deal for Youfone reveals a fertile merger pipeline that recasts competitive boundaries inside the Benelux MVNO market.

Luxembourg, though smaller, wields outsized strategic weight given its financial-services density and multilingual workforce. POST’s nationwide 5G SA coverage combined with ILR’s open-access stance lets international MVNOs enter quickly. Cross-border commuters appreciate tariff symmetry with neighboring markets, sustaining roaming-inclusive bundles that lift ARPU. Overall, geographic variety injects resilience into the Benelux MVNO market by diversifying regulatory and demand profiles.

Competitive Landscape

The Benelux MVNO market displays moderate concentration: the top five brands account for roughly 55% of active SIMs, leaving room for niche entrants. Lebara’s EUR 513 million topline and four-million customer footprint showcase the economies achievable via multi-country operations. KPN, Proximus and Orange use acquisitions to reclaim fast-growing segments they had previously ceded, a hedge against wholesale revenue cannibalizing retail.

Digital transformation is the primary competitive lever. Brands adopt cloud BSS, e-SIM and AI-driven support bots to shrink OPEX and uplift NPS scores. Full MVNOs like Voiceworks invest in private 5G cores to win SME contracts that demand custom QoS. Meanwhile, ESG positioning such as carbon-neutral “green SIM” lines differentiates amid commoditized gigabyte pricing.

Technological edge also emerges from satellite-NTN back-haul, offering uptime guarantees for industries in shadow zones. Host-network slicing opens tiered quality layers but could entrench MNO power if MVNOs fail to secure equitable terms. Regulatory vigilance from BEREC and national watchdogs remains critical in preserving contestability within the Benelux MVNO market.

Benelux MVNO Industry Leaders

Lycamobile

Lebara

Youfone

Simyo

Mobile Vikings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: hey!telecom broadened its fixed-broadband bundle at EUR 29 monthly for unlimited data and 200 Mbps.

- August 2024: Waterland Private Equity acquired Lebara, a major European MVNO with EUR 513 million revenue and more than 4 million customers across five markets, including the Netherlands.

- July 2024: Belgian Competition Authority opened a probe into the Proximus-Telenet fiber co-investment covering 2.7 million homes.

- May 2024: Belgium enacted enforcement powers for the EU Digital Markets Act, assigning duties to the Belgian Competition Authority.

Benelux MVNO Market Report Scope

| Cloud |

| On-premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| Belgium |

| Netherlands |

| Luxembourg |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale | |

| By Country | Belgium |

| Netherlands | |

| Luxembourg |

Key Questions Answered in the Report

What is the forecast revenue for the Benelux MVNO market in 2030?

It is projected to reach USD 3.36 billion, growing at a 3.90% CAGR from 2025.

Which deployment model leads adoption among Benelux virtual operators?

Cloud-based platforms dominate with a 70.51% 2024 revenue share and the fastest 8.21% CAGR.

How fast will IoT-specific MVNO subscriptions grow through 2030?

IoT lines are expected to rise at a 23.56% CAGR as enterprises outsource connectivity.

What share of 2024 connections relied on 4G/LTE technology?

4G/LTE accounted for 78.69% of active SIMs, although 5G is the fastest-growing layer.

Why are Full MVNO models gaining traction?

They provide deeper network control and multi-host flexibility, fueling a 14.75% CAGR despite higher investment demands.

Which country currently shows the highest 5G coverage in Benelux?

Belgium reaches 95% household 5G coverage, giving MVNOs broad access to next-gen radio capacity.

Page last updated on: