Switzerland Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 17.49 Billion |

| Market Size (2026) | USD 18.37 Billion |

| Market Size (2031) | USD 23.51 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

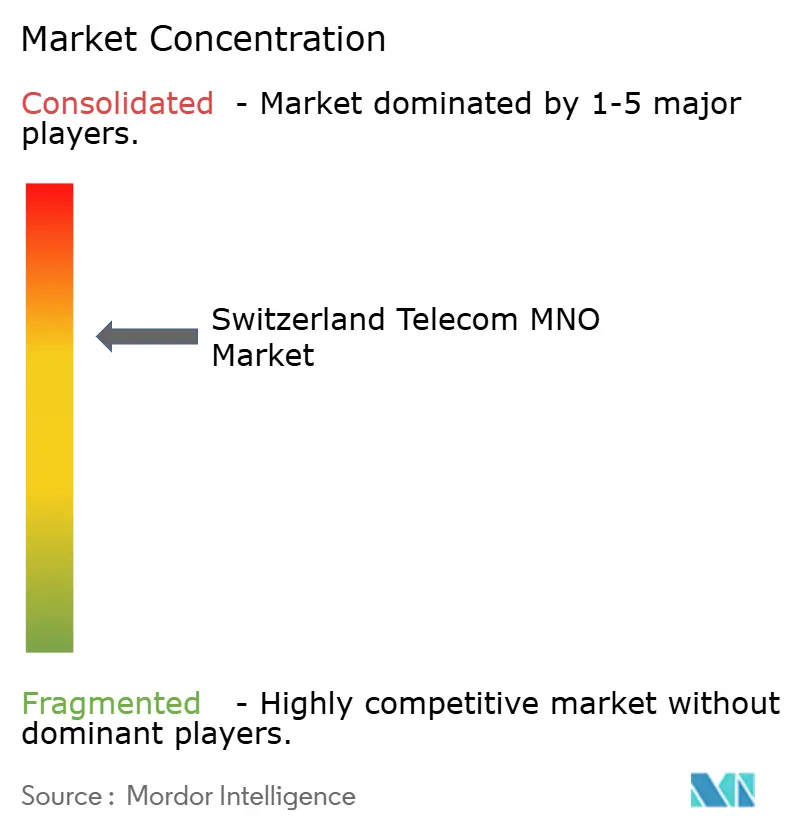

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Telecom MNO Market Analysis by Mordor Intelligence

The Switzerland Telecom MNO Market size was valued at USD 17.49 billion in 2025 and estimated to grow from USD 18.37 billion in 2026 to reach USD 23.51 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031).

The revenue trajectory reflects the country’s long-standing commitment to digital infrastructure, underpinned by annual operator investments of more than CHF 2.3 billion that are expanding 5G coverage and driving fiber penetration toward 80% of households by 2030.[1]Federal Communications Commission, “Mobile Coverage,” comcom.admin.ch Growth momentum stems from data-intensive consumer behavior, enterprise digitization, and regulatory incentives that encourage infrastructure sharing while preserving Switzerland’s rigorous environmental standards. Competitive intensity centers on network quality; Swisscom’s 99% mobile reach and 86% 5G+ population coverage safeguard its premium positioning even as Sunrise UPC and Salt narrow performance gaps. Opportunities broaden through bundled fixed-mobile offers, industrial IoT, and private 5G campus networks, while operators counterbalance saturated subscriber growth with higher-value data services, cloud, and cybersecurity propositions.

Key Report Takeaways

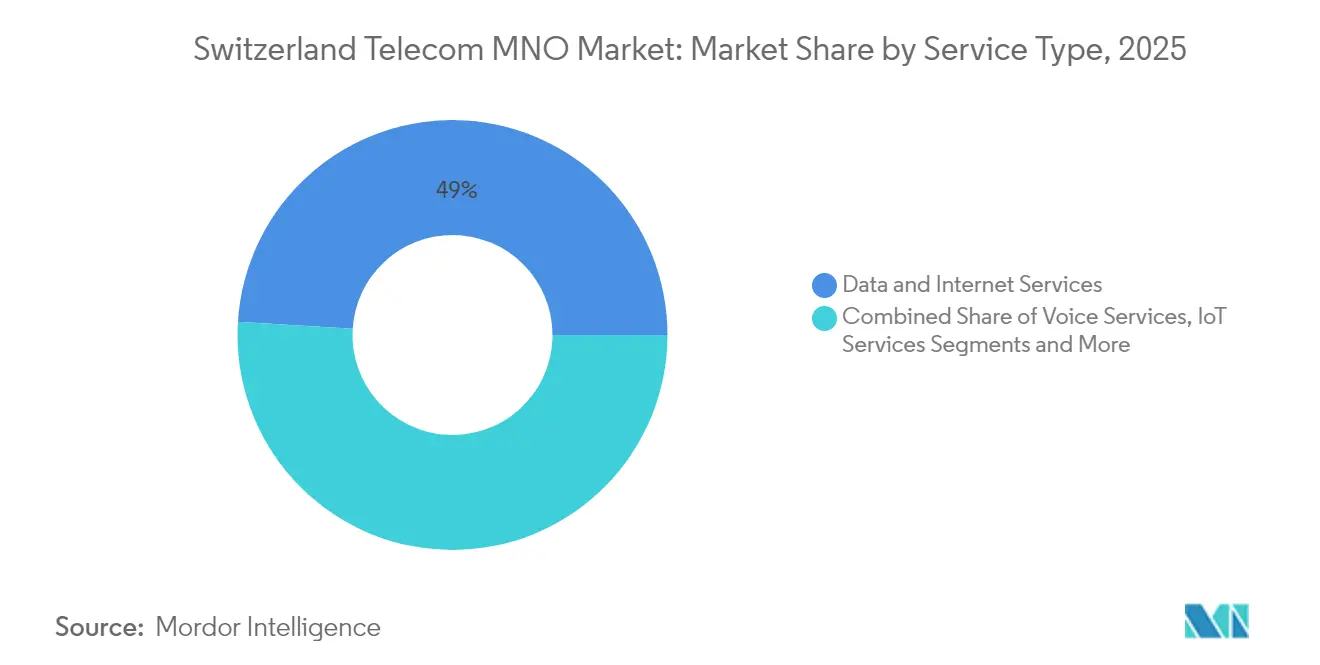

- By service type, data and internet services led with 49.02% of Switzerland telecom MNO market share in 2025, whereas IoT and M2M services are expanding at 5.22% CAGR through 2031.

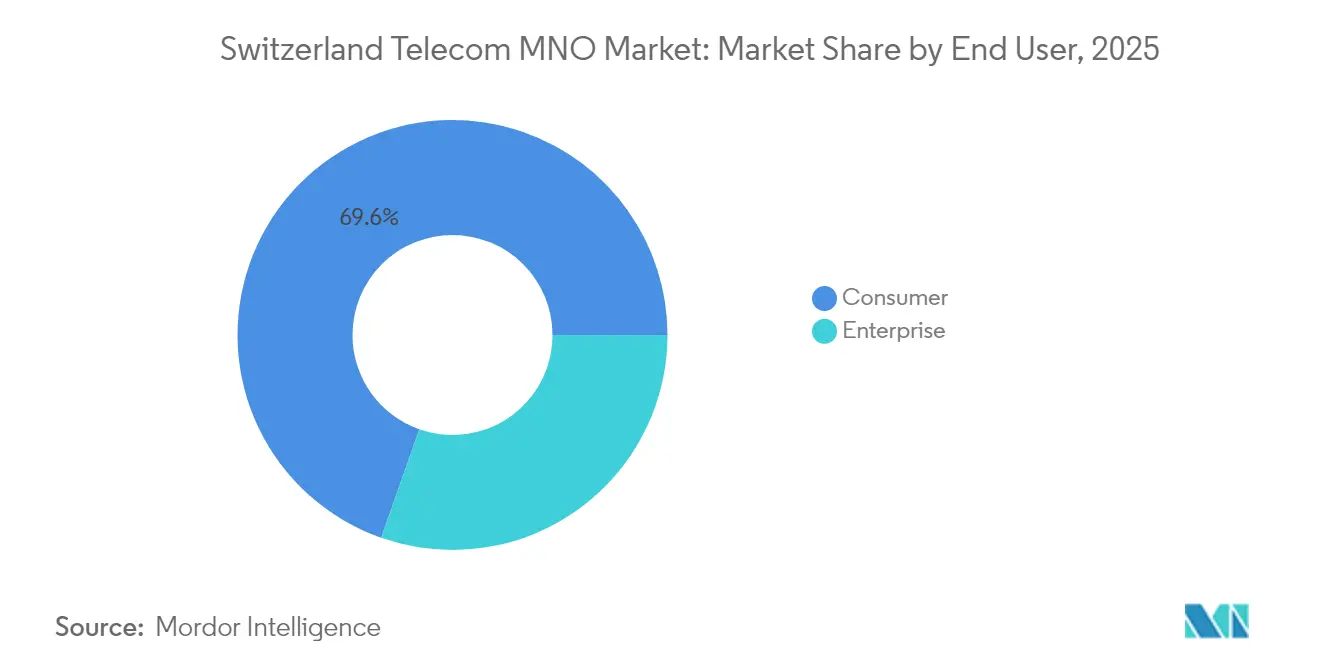

- By end-user, the consumer segment led with 69.62% of Switzerland telecom MNO market share in 2025, while the enterprise segment is projected to expand at a 5.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide 5G coverage enabling new enterprise & consumer use-cases | +1.2% | National; early gains in Zurich, Geneva, Basel | Medium term (2-4 years) |

| Surge in demand for converged fixed-mobile bundles | +0.8% | National; stronger in urban areas | Short term (≤ 2 years) |

| Regulatory support & incentives for infrastructure sharing | +0.6% | National | Long term (≥ 4 years) |

| Accelerating fiber backbone and last-mile deployments | +1.0% | National; priority rural roll-outs | Medium term (2-4 years) |

| Industrial IoT adoption in high-value manufacturing & pharma | +0.7% | Basel & Zurich corridors | Long term (≥ 4 years) |

| Growth of private 5G campus networks for precision agriculture | +0.4% | Alpine and agricultural regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nationwide 5G coverage enabling new enterprise & consumer use-cases

Switzerland telecom market operators translate near-ubiquitous 5G reach into premium retail and enterprise tariffs. Swisscom’s 99% 5G footprint and Sunrise’s March 2025 5G SA launch permit network slicing, enabling industrial IoT workloads that demand latency below 10 ms and throughput above 1 Gbps. Median 5G speeds of 187 Mbps versus 32 Mbps for 4G justify speed-tiered pricing and boost mobile ARPU. Enterprises deploy private 5G at precision-manufacturing plants and smart-tourism sites, bolstering connectivity revenue beyond traditional SIM sales. Consumer monetization accelerates through cloud gaming and XR services, with 5G subscriptions expected to exceed 90% of mobile connections by 2028.[2]Ericsson, “5G Driving Revenue Growth in Top 20 Markets,” ericsson.com Operators must still navigate stringent Swiss EMF rules that prolong rural roll-outs yet preserve public acceptance.

Surge in demand for converged fixed-mobile bundles

Rising household digital budgets and preference for single invoices drive 44% of subscribers toward converged offers. Swisscom’s inOne serves 2.51 million customers, or 66% of its mobile base, underpinning churn rates below 5%. The Sunrise-UPC combination leverages cable assets to cross-sell mobile, broadband, and pay-TV, while Salt partners with Open Access fiber providers to bundle gigabit plans competitively. Bundles lift average revenue per user by 8-12% versus stand-alone products and create upsell paths to content and cloud storage services. Intensifying bundle competition increases Switzerland telecom market differentiation through service richness rather than price alone.

Regulatory support & incentives for infrastructure sharing

The Federal Communications Commission (ComCom) accelerates network deployment through streamlined permitting and co-investment mandates. CHF 730 million in public funds target rural gigabit coverage, lowering capex barriers for operators extending fiber and 5G in low-density areas. Wholesale access obligations offer smaller players predictable pricing, tempering market entry barriers without diluting incumbent investment appetite. Over the long term these measures add 0.6 percentage points to Switzerland telecom market CAGR by expanding addressable demand and lowering cost-to-serve.

Accelerating fiber backbone and last-mile deployments

Swisscom alone invests CHF 1.7 billion annually to raise fiber-to-the-home passings to 75-80% by 2030. Federal broadband promotion bills subsidize rural builds, aiming for nationwide gigabit coverage. Fiber enables symmetric 10 Gbps retail tiers and underpins wholesale backhaul for 5G small cells, strengthening monetization across mobile and fixed lines. Enterprises migrating workloads to cloud platforms demand reliable multi-gigabit links, further stimulating service uptake. Although rollout prioritizes economic centers for near-term returns, public funding bridges rural viability gaps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-total mobile penetration limits new subscriber growth | -0.9% | National | Short term (≤ 2 years) |

| Switzerland's stringent EMF limits raise 5G deployment costs | -0.6% | National; high-density areas | Medium term (2-4 years) |

| Decline in legacy voice revenue from OTT substitution | -0.5% | National | Short term (≤ 2 years) |

| Rising energy costs inflate network operating expenses | -0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Near-total mobile penetration limits new subscriber growth

Mobile SIM density exceeds 103% of residents, constricting organic additions. Operators therefore prioritize upselling existing accounts to 5G premium tiers and multi-device data bundles. Competitive promotions focus on switching inducements, compressing margins in the consumer voice segment. Growth consequently pivots to enterprise IoT, managed security, and cross-border expansion, exemplified by Swisscom’s EUR 8 billion purchase of Vodafone Italia in January 2025.

Switzerland's stringent EMF limits raise 5G deployment costs

Swiss radiation thresholds are roughly 10× stricter than EU guidelines, compelling dense small-cell grids and advanced beam-forming antennas that raise per-site capex by 15-25%. Municipal approval processes lengthen rollout lead times, particularly in heritage urban zones. Operators mitigate by site-sharing and adaptive-power management, but cost pressure still slows rural 5G SA adoption.[3]Federal Office of Communications, “Technology,” bakom.admin.ch

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Capture Half the Revenue Base

Data and Internet Services controlled 49.02% of Switzerland telecom market share in 2025, reflecting high smartphone adoption, video streaming, and cloud application uptake. The segment’s robust traffic growth aligns with fiber backhaul expansion and 5G monetization, enabling operators to introduce speed-based plans that lift ARPU. Voice revenue erosion persists but is offset by data-driven value-added offerings such as cloud gaming passes and zero-rating for selected platforms. Over the forecast, Data Services revenue is projected to track a 5.86% CAGR, reinforcing its primacy in Switzerland telecom market size. Messaging and OTT services, despite cannibalizing SMS, generate incremental content revenue through platform partnerships. IoT connectivity revenue, currently a single-digit share, accelerates with industrial 5G private networks in factories and hospitals, adding long-tail growth.

The secondary service cluster—IoT and M2M—benefits from Basel’s life-sciences cluster deploying sensor-laden cleanrooms, while Alpine resorts adopt smart-tourism solutions to personalize visitor services. Operators nurture these niches with flexible SIM management platforms and low-power wide-area technologies, solidifying Switzerland telecom market differentiation.

By End-User: Enterprises Drive the Fastest Expansion

Enterprises represented 30.38% of telecom spend in 2025 yet are forecast to expand at a 5.43% CAGR to 2031, outpacing consumer growth. Digital transformation across pharmaceuticals, precision engineering, and financial services fuels demand for secure, low-latency connectivity, managed SD-WAN, and cybersecurity bundles. Enterprise contribution to Switzerland telecom market size exceeds USD 7.25 billion by 2031, widening margin profiles due to lower churn and integrated solution sales. Operators cultivate sector-specific offerings—private 5G for robotics-rich plants, SASE for global banks, and IoT analytics for agritech—deepening strategic partnerships. Consumer revenue remains relatively stable, sustained by bundled pricing, but its share of Switzerland telecom market size narrows modestly as enterprise services scale.

Geography Analysis

Switzerland telecom market displays homogeneous national coverage yet reveals regional nuances that influence service uptake. Metropolitan hubs—Zurich, Geneva, Basel—account for roughly 60% of data traffic and host the highest ratios of 5G Unlimited premium plans. Fiber household penetration already surpasses 70% in these cantons, enabling symmetrical 10 Gbps tiers. Rural cantons benefit from federal subsidies that underwrite gigabit builds, raising national fiber reach to 57% in 2025 and targeting 80% by 2030. Alpine regions leverage private 5G to power precision agriculture and avalanche early-warning systems, diversifying Switzerland telecom market use cases beyond urban cores.

Cross-border mobility remains critical given Switzerland’s non-EU status. Roaming traffic generated CHF 102.18 million in 2024 and continues to climb with business travel recovery and inbound tourism. Operators thus include large EU roaming allowances in mid- to high-tier plans, securing differentiation on travel convenience. Energy-price inflation adds uniform cost pressure across cantons, prompting 2025 price hikes of 1.8-8.1% that were largely accepted thanks to Switzerland’s high disposable incomes.

National digital policy under the Digital Switzerland 2025 framework stresses AI governance and open-source adoption, prompting public-sector connectivity tenders that value data-sovereignty guarantees. Operators with ISO-27001-compliant data centers near Bern and Lausanne gain procurement advantages. Overall, regional disparities in infrastructure density narrow steadily, fostering inclusive growth across Switzerland telecom market.

Competitive Landscape

Swisscom, Sunrise UPC, and Salt collectively hold about 99% of mobile subscriptions, underscoring a concentrated yet vigorously contested Switzerland telecom market. Swisscom’s 57% share derives from consistent network-quality leadership documented by independent benchmarks for seven consecutive years. The operator channels CHF 1.7 billion annually into fiber and 5G SA, underpinning premium pricing that supports EBITDA margins above 40%. Sunrise UPC leverages Liberty Global’s cable heritage, combining DOCSIS 3.1 gigabit internet with mobile to entice switchers; its 25% mobile share and 28% broadband share position it as the main challenger. Salt’s aggressive unlimited-data bundles and second-place network-score ranking translate to 17% of mobile lines, while its 4% broadband share grows via Open Access fiber collaborations.

Strategic moves highlight geographic diversification and technological leadership. Swisscom’s January 2025 acquisition of Vodafone Italia amplifies scale economics and supplies roaming cost synergies valued at EUR 600 million annually. Sunrise’s March 2025 nationwide 5G SA launch enables differentiated low-latency enterprise slices, strengthening its B2B proposition. Salt raises tariffs by up to 8.1% to absorb a 19% spike in electricity costs yet maintains churn below 10% owing to competitive device bundles. Across the board, operators invest in network energy efficiency—virtualized RAN and AI-driven sleep modes—to temper cost inflation.

Emerging rivals include Digitec Galaxus, whose March 2025 10 Gbps FTTH plan at CHF 39 disrupts retail broadband price anchors. MVNOs remain niche, constrained by wholesale rate structures but offer low-cost data-only propositions. Industrial partners such as Siemens cooperate with operators to deliver turnkey private 5G and IoT sensor networks in hospitals and factories, broadening value capture along the connectivity-solution continuum.

Switzerland Telecom MNO Industry Leaders

Swisscom AG

Sunrise Communications AG

Salt Mobile SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Swisscom completed its EUR 8 billion acquisition of Vodafone Italia, anticipating EUR 600 million in annual synergies while retaining distinct Swiss operations.

- March 2025: Sunrise activated Switzerland’s first 5G Standalone network supporting network slicing and ultra-low-latency enterprise use cases.

- February 2025: Swisscom reported FY 2024 net income of CHF 1.54 billion, down 9.9% due to acquisition costs, and issued 2025 revenue guidance of CHF 15-15.2 billion.

- June 2025: Sunrise introduced five new “Sunrise Connect” mobile tariffs with higher EU roaming allowances.

Switzerland Telecom MNO Market Report Scope

Telecommunication, commonly referred to in its plural form or abbreviated as 'telecom', involves the electronic transmission of information across distances. This is typically achieved through cables, radio waves, or various communication technologies. Notably, these transmission methods can be segmented into communication channels through multiplexing, enabling a single medium to handle multiple simultaneous communication sessions.

The Swiss telecom market is segmented by service (voice services [wired and wireless]), data and messaging services, and OTT and PayTV services. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming And International Services, Enterprise And Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming And International Services, Enterprise And Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

Which service line currently brings in the most money for Swiss operators?

Data and Internet Services contributed 49.02% of total 2025 revenue, boosted by 5G and fiber uptake.

How extensive is 5G coverage across the country?

Swisscom’s network reaches 99% of residents, while national availability across all providers exceeds 93% in major cities and 86-87% in rural areas.

Why did leading providers raise retail prices in early 2025?

Electricity costs climbed 19–23%, so operators passed through 1.8–8.1% increases to protect margins.

What role do bundled fixed-mobile offers play in subscriber retention?

Converged packages serve 44% of households and lift average revenue per user by roughly 8-12% compared with stand-alone plans.

Page last updated on: