Switzerland Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

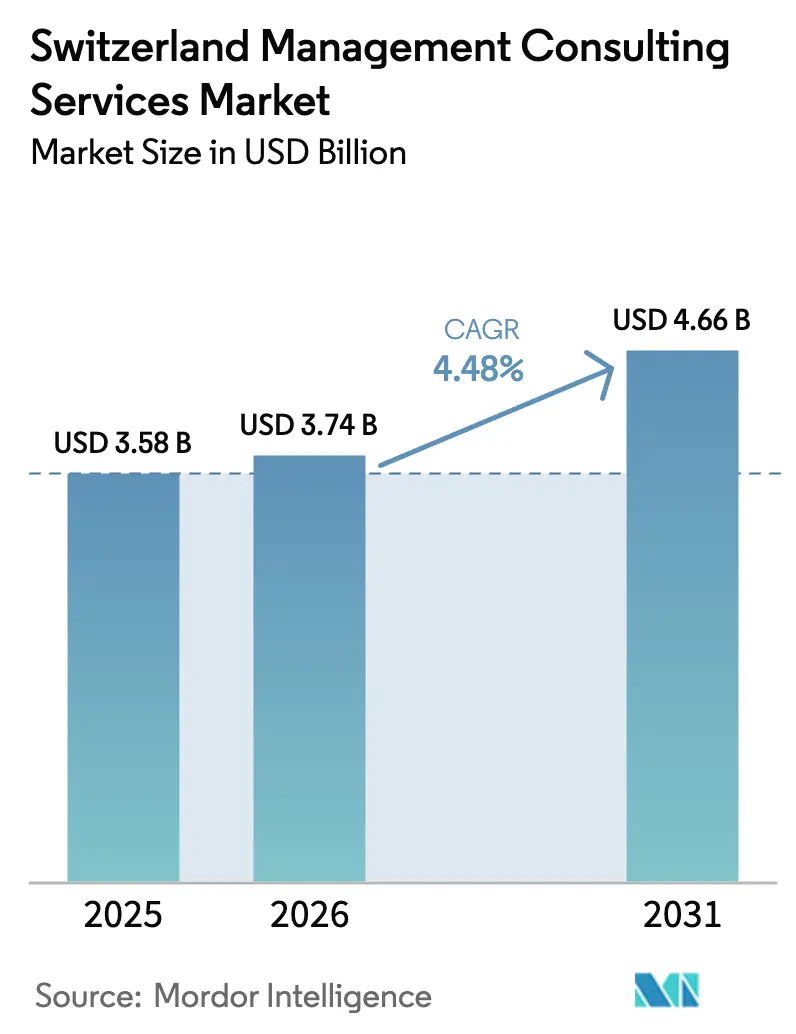

| Base Year Market Size (2025) | USD 3.58 Billion |

| Market Size (2026) | USD 3.74 Billion |

| Market Size (2031) | USD 4.66 Billion |

| Growth Rate (2026 - 2031) | 4.48% CAGR |

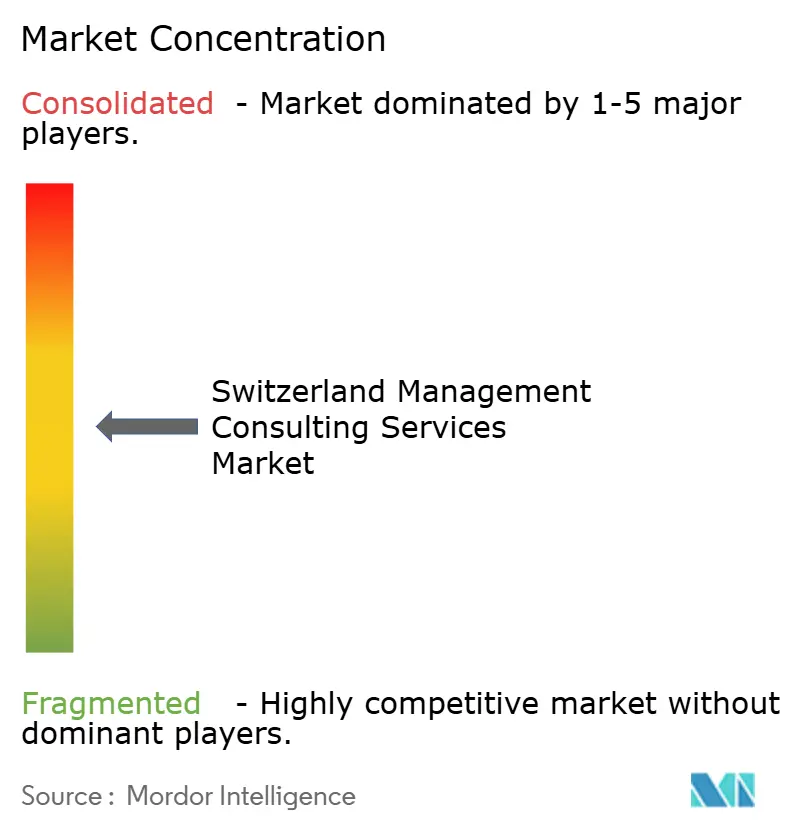

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Management Consulting Services Market Analysis by Mordor Intelligence

The Switzerland management consulting services market size is expected to grow from USD 3.58 billion in 2025 to USD 3.74 billion in 2026 and is forecast to reach USD 4.66 billion by 2031 at 4.48% CAGR over 2026-2031. This trajectory reflects a mature yet resilient advisory ecosystem where global firms and Swiss boutiques compete for sophisticated, regulation-heavy mandates. Structural demand comes from financial services, pharmaceuticals, and precision manufacturing, while digital acceleration, ESG compliance, and Industry 4.0 drive new project pipelines. Intensifying regulatory scrutiny and rapid generative-AI adoption raise the strategic value of expert guidance. On the supply side, talent scarcity and the spread of outcome-based pricing reshape delivery economics, encouraging hybrid on-site and remote models.

Key Report Takeaways

- By organization size, large enterprises held 71.12% of Switzerland management consulting services market share in 2025; SMEs are growing fastest at a 6.52% CAGR through 2031.

- By service type, operations consulting led with 30.05% revenue share in 2025, while technology consulting is advancing at a 5.42% CAGR to 2031.

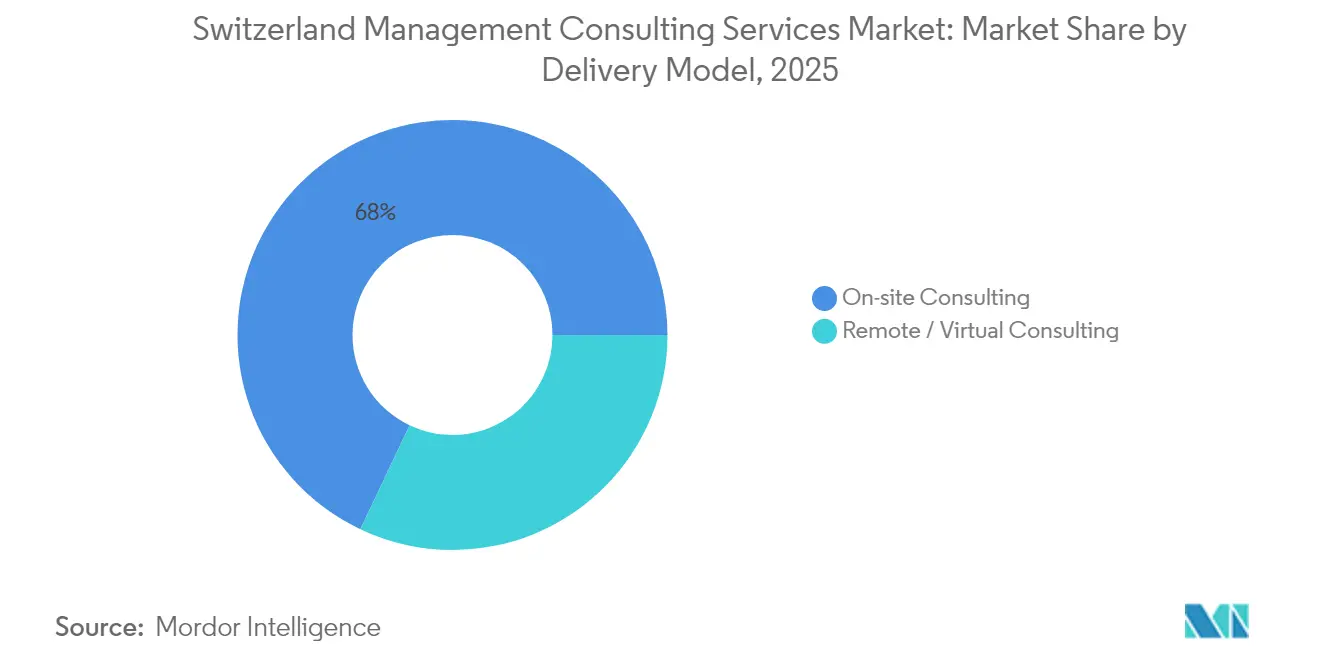

- By delivery model, on-site consulting captured 67.95% share of the Switzerland management consulting services market size in 2025 and remote models are expanding at a 6.57% CAGR through 2031.

- By end-user industry, financial services accounted for 25.54% share of the Switzerland management consulting services market size in 2025 and healthcare and life sciences is growing at a 4.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-first transformation programmes | +1.2% | National; Zurich, Geneva, Basel | Medium term (2-4 years) |

| Regulatory complexity in BFSI and life sciences | +0.9% | Nationwide financial centers and pharma hubs | Long term (≥ 4 years) |

| Cost-out and operational-excellence mandates | +0.7% | Industrial cantons such as Aargau and Solothurn | Short term (≤ 2 years) |

| Sustainability and ESG-reporting pressure | +0.6% | National with EU spillovers | Medium term (2-4 years) |

| Generative-AI adoption race | +0.8% | Early adoption in finance and pharma nationwide | Short term (≤ 2 years) |

| Canton-level export-promotion incentives | +0.4% | Varies by local economic programmes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital-first transformation programmes across Swiss corporates

Cloud and AI investments worth USD 400 million from Microsoft signal the scale of enterprise digitization, pushing every sector to modernize core systems. [1]Kripa B., “Microsoft Announces USD 400 Million Investment,” TelecomTalk, telecomtalk.info Fifty-two percent of Swiss organizations now automate end-to-end processes, surpassing global benchmarks and demanding large-scale implementation support. Healthcare providers such as Ente Ospedaliero Cantonale are overhauling telemedicine portals, while manufacturers like Kägi Söhne AG shorten workforce-planning cycles from one day to minutes through factory automation. Integration with legacy platforms remains a bottleneck for 64% of companies, expanding advisory engagements around change management and reskilling.

Regulatory complexity in BFSI and life sciences fueling advisory demand

FINMA’s climate-risk rules effective January 2025 require scenario testing and board-level oversight, elevating consulting demand for compliance frameworks. Climate-related disclosure obligations intersect with the Climate Protection and Innovation Act and new Swiss Bankers Association ESG guidance, compelling banks to embed sustainability in risk appetites. [2]KPMG, “Swiss Financial Climate Regulations,” kpmg.comPharma giants like Roche channel CHF 1.2 billion into new Basel labs while navigating stringent GMP updates. Consulting firms facilitate policy interpretation, gap assessments, and system upgrades across both sectors.

Sustainability and ESG-reporting pressure on listed firms

Eighty percent of Switzerland’s largest companies publish non-financial metrics, yet only one-third align with TCFD principles, signaling unmet reporting needs. Upcoming EU Corporate Sustainability Reporting Directive adds financial-materiality disclosures, mandating deeper data collection. Leaders such as Givaudan cut GHG emissions 48% since 2015, illustrating best-practice pathways other firms aim to replicate. [3]Givaudan, “2024 Integrated Report,” givaudan.com Compliance costs for high-risk AI tools may top CHF 3.7 million, further elevating advisory spend.

Generative-AI adoption race requiring strategy and implementation support

Generative AI could boost Swiss GDP by CHF 80-85 billion by 2030, yet only 2% of firms scale AI enterprise-wide. UBS already pushes 5,000 AI-generated analyst videos annually, showcasing early operationalization. Manufacturing analytics startups such as EthonAI attract CHF 15 million funding, reflecting fast-moving client interest. Consulting engagements address strategy road-mapping, vendor selection, and workforce reskilling as 39% of companies lack internal AI skills.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute talent shortages inflating consultant day rates | -0.8% | Zurich, Geneva, Basel | Short term (≤ 2 years) |

| Intensifying competition from freelance platforms and boutiques | -0.6% | Nationwide via digital channels | Medium term (2-4 years) |

| Data-sovereignty concerns around remote delivery | -0.4% | Nationwide; impacts cross-border work | Medium term (2-4 years) |

| Outcome-based pricing reducing billable hours | -0.3% | Nationwide; affects standardized services | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute talent shortages driving consultant-day-rate inflation

Seventy-two percent of AI-related vacancies take more than six months to close, lifting rates as high as CHF 400 per hour for financial-services expertise. Salary premiums reach 15% in Zurich, 10% in Geneva, and 8% in Basel. Pharmaceutical and finance projects suffer the sharpest bottlenecks, prompting firms to widen global searches and invest in retention bonuses. Cross-border hiring adds legal complexity that often requires separate advisory work on labor law compliance.

Intensifying competition from freelance platforms and boutiques

Digital marketplaces expose Swiss clients to global talent, allowing freelancers to charge CHF 100-300 per hour for marketing advice and capturing share from traditional consulting. Boutiques such as Adlatus leverage former executives to target SMEs, while integrated tech consultancies like ELCA undercut broader strategy firms with turnkey solutions. Price pressure escalates in commoditized tasks, compelling incumbents to bundle services, automate standard analyses, and focus on high-complexity niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Large Enterprises Dominate Despite SME Acceleration

Large enterprises accounted for 71.12% of Switzerland management consulting services market share in 2025 as their complex integration projects and regulatory burdens command multi-year advisory engagements. Swisscom’s EUR 8 billion takeover of Vodafone Italia required extensive post-merger integration work, illustrating typical large-client scope. These organizations frequently demand holistic digital-transformation roadmaps, regulatory gap assessments, and operating-model redesigns, anchoring steady revenue for full-service firms.

SMEs are expanding at a 6.52% CAGR, lifted by canton export-promotion schemes and federal digitization grants that lower barriers to professional services. Switzerland Global Enterprise supported 6,361 SMEs in 2021, feeding a pipeline of cross-border expansion projects. ERP upgrades typify SME mandates: 72% already use cloud solutions and increasingly integrate AI-powered analytics, as seen in Leutwyler Kühlanlagen AG’s four-month ERP rollout that shaved administrative overhead. As more SMEs pursue internationalization, demand for scalable compliance and market-entry consulting grows, fostering niche specialization among boutique firms.

By Service Type: Operations Excellence Leads Technology Surge

Operations consulting held 30.05% share of the Switzerland management consulting services market size in 2025, driven by precision manufacturers seeking lean processes and cost control. Wilhelm Schmidlin AG used ABB robots and Kaizen principles to secure 50% domestic bathtub share, exemplifying production-efficiency mandates that feed advisory demand. Engagements span value-stream mapping, supply-chain risk management, and shop-floor automation.

Technology consulting is the fastest-growing service at 5.42% CAGR to 2031, reflecting cloud migration, cybersecurity, and AI adoption imperatives. Pharmaceutical contract manufacturer Siegfried cut maintenance spend from CHF 12 million to less than CHF 8 million by outsourcing to tech-enabled partners, signaling ROI potential for digital retrofits. Strategy and HR consulting maintain steady relevance around expansion planning and hybrid-work policy design, while sustainability-focused advisory grows as corporations adapt to mandated ESG disclosures.

By Delivery Model: Remote Consulting Gains Despite On-site Preference

On-site engagements captured 67.95% of Switzerland management consulting services market size in 2025, reflecting a preference for face-to-face collaboration during sensitive regulatory and integration projects. FINMA-driven climate-risk undertakings often keep consultants embedded within client teams to protect confidential data. However, remote and virtual consulting is expanding at a 6.57% CAGR as clients pursue cost efficiency and broader talent pools.

Hybrid models combine strategic on-site workshops with remote implementation sprints. Swisscom’s Medical Connector Suite links more than 200 healthcare facilities through secure digital channels, showing how consultants can deliver remotely while meeting stringent data-protection rules. Data-sovereignty laws require explicit consent for processing sensitive data, pushing firms to deploy Swiss-based cloud zones or localized servers, which in turn becomes a niche advisory field. Cross-border labor regulations add paperwork when consultants work from EU/EFTA states, necessitating legal structuring to stay compliant.

By End-user Industry: Financial Services Leadership Amid Healthcare Acceleration

Financial institutions commanded 25.54% share of the Switzerland management consulting services market size in 2025. Banks face overlapping FINMA directives and Swiss Bankers ESG rules, requiring stress-testing frameworks, AI-governance protocols, and climate-risk scenario planning. Generative-AI pilots, such as UBS’s analyst avatars, further intensify advisory demand for data-governance and change-management services.

Healthcare and life sciences is the fastest-growing end-user at 4.71% CAGR thanks to digital-health modernization and strict GMP compliance. Roche’s CHF 1.2 billion Basel Innovation Center underscores the scale of transformation requiring process redesign and sustainability alignment. Manufacturers and industrial clients continue to seek Industry 4.0 roadmaps, while IT-telecom, energy, government, and real-estate segments generate specialized mandates in cloud, net-zero strategies, e-government, and smart-building solutions.

Geography Analysis

Zurich anchors the Switzerland management consulting services market with premium billable rates 15% above the national mean. Concentrations of banking, insurance, and multinational headquarters fuel complex strategy and compliance projects. Geneva ranks second, enjoying 10% premiums driven by private banking, commodity trading, and international-organization projects that demand multilingual expertise. Basel secures 8% premiums through its dense pharma cluster, where GMP, digital-lab, and ESG mandates generate high-value work.

Peripheral cantons increasingly foster consulting demand via innovation programmes. Hightech Aargau links SMEs with research institutes, prompting operational-excellence consultations across the region. Solothurn hosts over 10% of national medtech jobs, pulling advisory firms into device-regulation and factory-automation engagements. Thurgau’s economic office attracts overseas manufacturers seeking Swiss hubs, requiring market-entry assessments and facility set-ups.

Federal economic-promotion funding of CHF 646.13 million for 2024-2027 prioritizes SME digitization, seeding advisory opportunities across every canton. Switzerland Global Enterprise provides export counselling via cantonal chambers and Swiss Business Hubs abroad; 88% of assisted companies report positive international outcomes, driving follow-on mandates around logistics, compliance, and partner sourcing. Remote delivery expands reach into smaller cantons, though data-locality rules often anchor core analysis within Swiss borders, preserving domestic revenue streams.

Competitive Landscape

The market remains moderately fragmented. Global strategy houses—McKinsey, BCG, Bain—compete for multiyear transformation blueprints alongside Big Four advisory divisions handling audit-adjacent compliance. Boutique specialists address ESG, AI, and sector-specific needs. Integrated tech-consulting hybrids such as ELCA combine software engineering with management advice, winning mandates where digital execution is inseparable from strategy.

Freelance platforms and alumni networks democratize access to senior talent, allowing SMEs to bypass incumbents for targeted guidance at CHF 100-300 per hour. Outcome-based contracts gain traction, shifting risk to consultants who now bundle analytics tools and accelerators to guarantee efficiency gains. Global firms respond by investing in Swiss delivery centers and industry cloud assets, while boutiques specialize deeper—for example, Connexis focuses strictly on CSR advisory for listed firms. M&A activity signals consolidation: SoftwareOne’s proposed acquisition of Crayon sets up a 13,000-employee IT-services leader headquartered in Stans.

White-space opportunities lie in data-sovereignty consulting, AI-ethics frameworks, and cross-border labor-law structuring. Firms that can prove ROI through digital twins, automated reporting, and lean transformation toolkits gain an edge as clients demand measurable outcomes over hourly inputs.

Switzerland Management Consulting Services Industry Leaders

McKinsey & Company, Inc.

Deloitte AG (Switzerland)

PricewaterhouseCoopers AG (Switzerland)

Accenture plc

Boston Consulting Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Microsoft invests USD 400 million in Swiss cloud and AI infrastructure, catalyzing advisory spend on enterprise AI roadmaps.

- April 2025: ABB reveals plan to spin off its robotics unit for a 2026 IPO, opening separation-management consulting opportunities.

- February 2025: Sygnum becomes a unicorn after adopting Societe Generale-FORGE’s EURCV stablecoin, expanding digital-asset advisory demand.

- January 2025: SoftwareOne announces intent to acquire Crayon Group, forming a CHF 1.6 billion-sales cloud-services leader.

Switzerland Management Consulting Services Market Report Scope

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Technology Consulting |

| Other Service Types |

| On-site Consulting |

| Remote / Virtual Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real-Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other End-User Industries |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Technology Consulting | |

| Other Service Types | |

| By Delivery Model | On-site Consulting |

| Remote / Virtual Consulting | |

| By End-user Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real-Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment and Sports | |

| Hospitality and Travel | |

| Other End-User Industries |

Key Questions Answered in the Report

How large is the Switzerland management consulting services market in 2026?

The Switzerland management consulting services market size is USD 3.74 billion in 2026 and is projected to reach USD 4.66 billion by 2031.

Which organization size category grows fastest in Swiss consulting demand?

Small and medium-sized enterprises post the fastest expansion at a 6.52% CAGR over 2026-2031, spurred by digitization grants and export-promotion initiatives.

What service type records the highest growth rate to 2031?

Technology consulting advances at a 5.42% CAGR over 2026-2031 as companies accelerate cloud migration, cybersecurity, and AI deployments.

Why is financial services the leading end-user segment?

Banks face overlapping FINMA climate-risk mandates and ESG rules that require extensive compliance and digital-transformation advisory work.

Which geographic areas command premium consulting rates?

Zurich commands 15% salary premiums, with Geneva at 10% and Basel at 8%, reflecting sector clusters that demand specialized expertise.

How are talent shortages affecting consulting costs?

Prolonged vacancies in AI and regulatory roles push consultant day rates up to CHF 400 per hour for niche financial-services expertise.

Page last updated on: