Austria Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

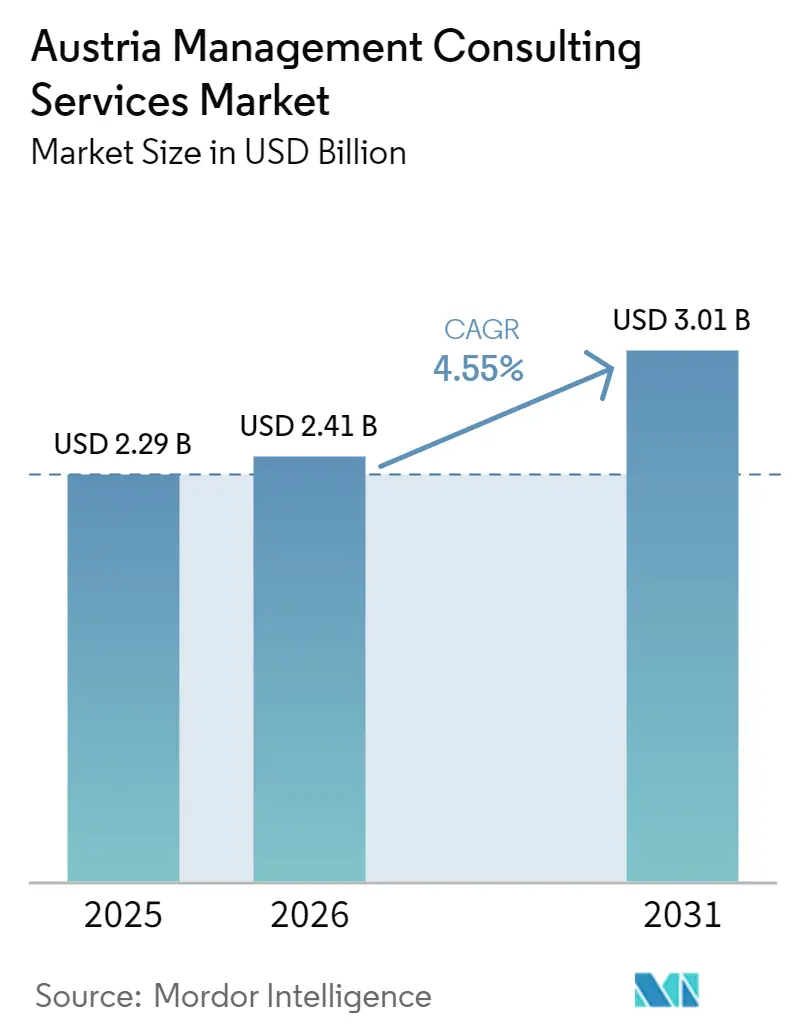

| Base Year Market Size (2025) | USD 2.29 Billion |

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 3.01 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Management Consulting Services Market Analysis by Mordor Intelligence

The Austria management consulting services market size is expected to grow from USD 2.29 billion in 2025 to USD 2.41 billion in 2026 and is forecast to reach USD 3.01 billion by 2031 at 4.55% CAGR over 2026-2031. Consulting demand rises as public agencies digitize mandatory workflows, industrial firms decarbonize to meet the Austrian Climate Protection Act, and roughly 15,000 family-owned businesses plan ownership transfers before 2031. Vienna’s federal ministries anchor large, regulation-driven projects, while Upper Austria’s steel and chemicals producers propel operations mandates linked to hydrogen adoption. Concurrently, clients institutionalize hybrid and remote delivery to ease the shortage of bilingual German-English digital consultants, a labor gap that topped 176,000 unfilled skilled positions in 2025. Cross-border German boutiques intensify competition by pricing engagements below Vienna cost levels and leveraging sector expertise in automotive, industrial tech, and renewable energy.

Key Report Takeaways

- By consulting service line, Strategy Consulting led with 33.16% of the Austria management consulting services market share in 2025, whereas Risk and Compliance Consulting posts the highest projected 4.81% CAGR through 2031.

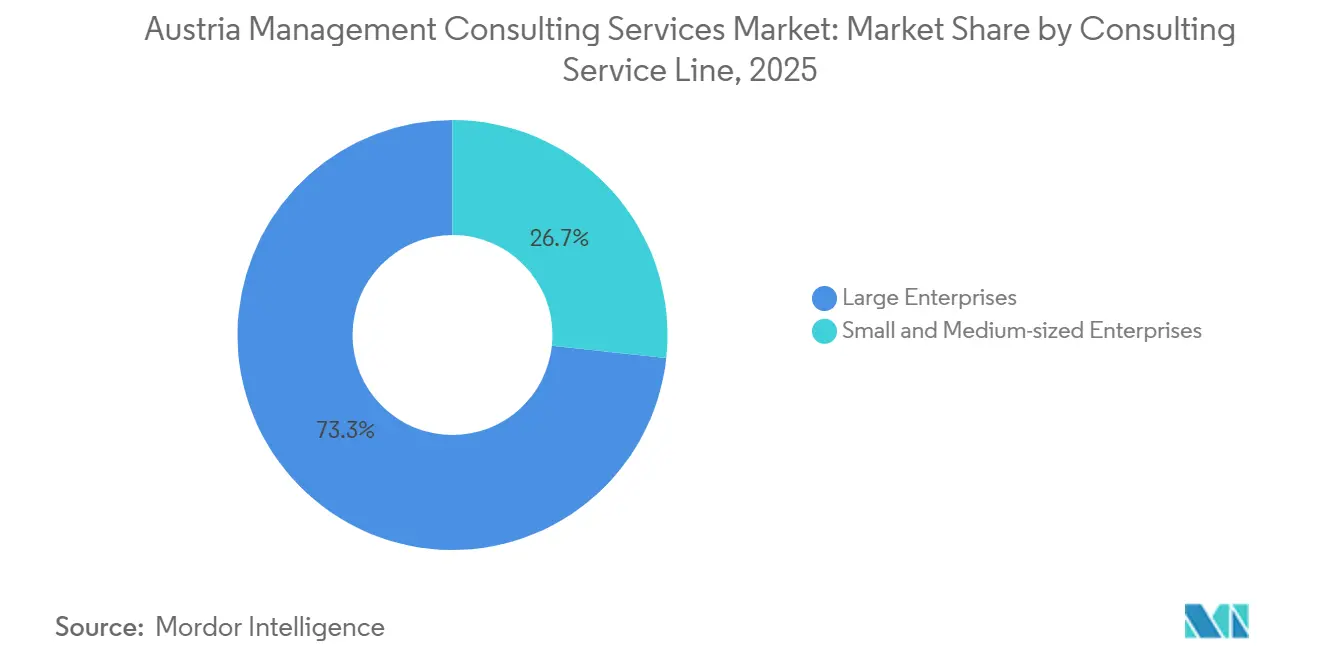

- By organization size, Large Enterprises accounted for 62.72% of 2025 spending, while Small and Medium-Sized Enterprises are projected to expand at a 4.64% CAGR over 2026-2031.

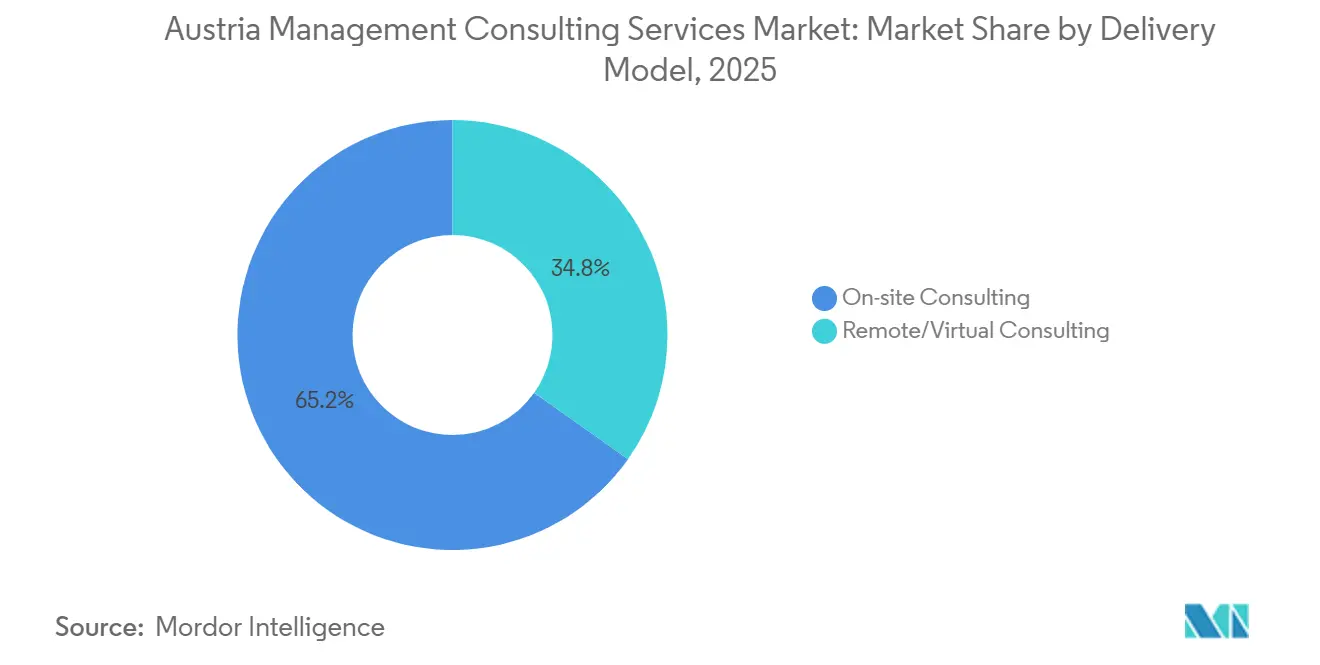

- By delivery model, On-Site Consulting commanded 68.87% of 2025 revenue, but Remote and Virtual Consulting is forecast to grow 4.72% per year during the period.

- By end user industry, the Public Sector held a 21.03% share in 2025, yet Energy and Resources is set to register the fastest 4.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Austria Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-First Public-Sector Transformation Mandates | +1.2% | Vienna, Graz, Linz | Medium term (2-4 years) |

| Push for Decarbonization Consulting in Austria’s Industrial Mittelstand | +1.1% | Upper Austria, Styria, nationwide | Long term (≥ 4 years) |

| Post-COVID SME Succession Wave Driving Strategy Revamps | +0.9% | Vienna, Salzburg, Tyrol | Short term (≤ 2 years) |

| EU-Funded Regional Innovation Hubs Boosting Tech Advisory Demand | +0.7% | Vienna, Graz, Linz | Medium term (2-4 years) |

| Corporate Tax-Reform Complexity (2024-25) Spurring Advisory Needs | +0.5% | Vienna, cross-border structures | Short term (≤ 2 years) |

| Accelerated AI Adoption Pressure Across Banking and Insurance | +0.6% | Vienna financial district | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-First Public-Sector Transformation Mandates

Austria’s ministries are replacing paper-based processes with cloud-native platforms to comply with EU cybersecurity directives, GDPR, and ISO 27001 requirements. The EUR 141 million (USD 159 million) IT Services 2025-2 framework covers NIS auditing, identity management, DevOps engineering, and analytics, ensuring multi-year backlogs for vendors that can blend technical and change-management expertise.[1]Tenderlake, “IT Services 2025-2,” tenderlake.com OECD-supported procurement digitization similarly pushes consultancies to redesign workflows, train civil servants, and install AI-supported decision engines. KPMG Austria responded by broadening state-aid and cybersecurity offerings, signaling that larger firms can absorb elongated RFP cycles better than boutiques.

Push for Decarbonization Consulting in Austria’s Industrial Mittelstand

The Transformation der Industrie program earmarks EUR 400 million (USD 450 million) annually from 2026 to fund energy-efficiency upgrades, electrification, and hydrogen pilots, guaranteeing a steady advisory pipeline through 2030.[2]Bundesministerium für Klimaschutz, “Transformation der Industrie,” bmk.gv.at Mega projects such as HI2Valley, aiming for 10,000 tonnes-per-annum (tpa) of green hydrogen by 2028, require regulatory navigation, EU-grant blending, and supply-chain orchestration. Wien Energie’s UpHy electrolyzer roll-out illustrates the multiservice opportunity across technical due-diligence, carbon accounting, and offtake contracting.[3]Wien Energie, “UpHy Green Hydrogen,” wienenergie.at EY’s 2024 merger with denkstatt created a 120-consultant ESG unit able to meet this surge. Mid-tier firms struggle to hire engineers versed in process heat, carbon capture, and hydrogen storage, widening the capability gap.

Post-COVID SME Succession Wave Driving Strategy Revamps

Roughly 150,000 Austrian family firms confront generational turnover, with 15,000 successions slated in the next five years.[4]Wirtschaftskammer Österreich, “Nachfolge in Unternehmen,” wko.at The Grace Period Act grants tax relief if heirs assume operational roles, yet imposes strict documentation that fuels demand for governance, valuation, and carve-out advice Digital backlogs compound complexity as many family enterprises still run on legacy ERPs and fragmented e-commerce stacks. Roland Berger’s post-merger banking integration playbook is now tailored for family-business governance, helping incoming leaders align culture and capture synergies . Private-equity interest is rising, demonstrated by AdEx Partners’ 2025 purchase of BMC Strategy Consultants to scale succession expertise.

EU-Funded Regional Innovation Hubs Boosting Tech Advisory Demand

Vienna’s AI and fintech lab, Graz’s mobility cluster, and Linz’s Industry 4.0 center channel Horizon Europe and Digital Europe funds into grant advisory, consortia management, and tech-transfer work. Salzburg’s EUR 15 million (USD 16.9 million) Life Sciences Center illustrates how regional co-funding sparks follow-on advisory spanning IP strategy and commercializationT. The Austrian Research Promotion Agency backs AI4SimProd, EuProGigant, and other projects that need feasibility studies, governance frameworks, and project management . Deloitte’s Graz campus, opening mid-2026, positions the firm to capture Styria’s innovation deal flow. Yet smaller cities lack comparable funding, concentrating consulting revenue in three metropolitan areas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Bilingual Digital Consultants (German-English) | -0.8% | Vienna, Graz tech corridors | Medium term (2-4 years) |

| Rising Price Competition from Cross-Border German Boutiques | -0.6% | Upper Austria, Styria | Short term (≤ 2 years) |

| Client In-House Capability Build-Up in Data Analytics | -0.4% | Vienna banks and insurers | Long term (≥ 4 years) |

| Slow Public-Sector RFP Cycles Amid Fiscal Tightening | -0.3% | Federal and municipal procurement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Bilingual Digital Consultants (German-English)

EY’s 2025 Mittelstandsbarometer found 67% of firms cite talent scarcity as their top risk, mirroring ibw’s estimate of 176,000 unfilled skilled roles nationwide.[5] Institut für Bildungsforschung der Wirtschaft, “Fachkräftemangel in Österreich,” ibw.at High salaries lure consultants to Germany or Switzerland, forcing Austrian firms to offshore tasks or narrow scope. Upper Austria’s 2025 English-language initiative targets schools, meaning relief arrives only in the late 2020s. BearingPoint’s BeMind AI platform, launched March 2026, automates analytics and reporting to stretch scarce human capacity. Adoption, however, remains uneven among regulated public-sector clients that demand on-site assurance.

Rising Price Competition from Cross-Border German Boutiques

German firms such as CYLAD and TTE Strategy opened Vienna offices in 2025, delivering work from lower-cost Bavarian hubs while preserving native language skills. Rates undercut Viennese averages by up to 20%, particularly in automotive, machinery, and renewable energy mandates. Roland Berger long pursued this playbook from Munich, leveraging experience in bank consolidation that saw Austria lose 49% of institutions since 2000. Austrian consultancies counter with intimate knowledge of subsidy programs and federal contacts, but advantages erode as German boutiques recruit Austrian nationals and win EU-wide tenders such as EFSA’s EUR 137 million (USD 154 million) framework.[6]DevelopmentAid, “Management Consulting Services Tender,” developmentaid.org Remote delivery, normalized by the pandemic, further reduces German cost barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Compliance Complexity Lifts Risk Advisory

Risk and Compliance Consulting is projected to advance at a 4.81% CAGR through 2031 as overlapping EU statutes, the Corporate Sustainability Reporting Directive, the AI Act, and Austrian tax reforms, force enterprises to seek specialized guidance. The Austria management consulting services market size for this segment benefits from multi-year engagements covering gap analysis, control design, and audit readiness. Strategy Consulting retained 33.16% of 2025 revenue, anchored by succession planning and carve-outs in the Mittelstand.

Consultants now bundle ESG software deployment with policy design, reflecting demand for holistic solutions. Transaction work remains robust: PwC structured Erste Group’s EUR 6.8 billion (USD 7.7 billion) stake purchase in Santander Bank Polska, requiring valuation, diligence, and integration roadmaps. Digital Transformation Consulting captures SAP S/4HANA migrations such as MED-EL’s USD 675 thousand project, showcasing how technology complexity cements long-tail advisory fees.

By Organization Size: SMEs Accelerate as Succession Meets ESG

Large Enterprises controlled 62.72% of spending in 2025, yet SME outlays are set to rise faster as family businesses confront succession, digital retrofits, and mandatory ESG disclosure. The Austria management consulting services market share held by SMEs expands as the Grace Period Act incentivizes heirs to formalize governance and modernize IT stacks.

RSM Austria’s 2025 merger with Moore Interaudit illustrates consolidation around owner-managed clients. Advisory scopes often span tax optimization, ERP selection, and CSRD alignment in a single mandate, demanding end-to-end project management. Large Enterprises, by contrast, increasingly internalize routine analytics and retain external advisors for AI governance or post-merger integration, compressing margins on commoditized work.

By Delivery Model: Hybrid Becomes the Default

On-site work retained 68.87% share in 2025, but talent scarcity and client cost pressure lift remote and virtual engagements at a 4.72% CAGR. Public-sector tenders such as IT Services 2025-2 explicitly authorize virtual delivery, legitimizing the model nation-wide.

Hybrid formats dominate digital transformation and ERP rollouts where discovery workshops occur on site, while coding, testing, and documentation run remotely. BearingPoint’s BeMind AI shows how automation augments distributed teams, although conservative sectors such as banking still demand partner-level presence for steering meetings. The Austria management consulting services market size for remote delivery remains constrained by cybersecurity certifications and data-sovereignty clauses in regulated industries.

By End User Industry: Energy Transition Outpaces Public-Sector Baseline

The Public Sector contributed 21.03% of 2025 revenue, driven by justice ministry digitization and OECD procurement modernization. Yet Energy and Resources is projected to log the fastest 4.68% CAGR through 2031 as hydrogen corridors, carbon-capture pilots, and grid modernization projects mature. The Austria management consulting services market size tied to hydrogen alone involves feasibility, subsidy navigation, and technology vendor selection.

Banking and Insurance engagements rise around AI adoption, with the Oesterreichische Nationalbank emphasizing AI governance in its 2026 supervisory agenda . Manufacturing projects orbit the Transformation der Industrie subsidy pool, requiring Industry 4.0 roadmaps and post-award management. Healthcare advisory gains momentum as ELGA mandates full electronic health record uploads and the EU Health Data Space looms.

Geography Analysis

Vienna remains the nucleus of the Austria management consulting services market, hosting all Big Four headquarters, global strategy houses, and a dense legal ecosystem. Federal ministries and state-owned champions such as OMV and Verbund commission continual strategy, regulatory, and digital mandates. The city’s talent shortage inflates salaries, prompting firms to nearshore routine analytics to Bratislava or Brno.

Graz is emerging as a second hub, aided by Deloitte’s 2026 campus and Styria’s cleantech start-ups. Proximity to Slovenia and Hungary enables cross-border advisory, particularly in mobility and renewable energy. Linz channels Upper Austria’s heavy industry; voestalpine’s decarbonization requirements create long-tail operations work, while the city’s EUR 36.6 billion (USD 41.2 billion) 2025 gross value added underlines client spending power.

Salzburg’s life-sciences center and tourism sector fuel IP strategy and digital upgrade mandates for family hotels. Cross-border dynamics intensify as German boutiques deliver from Munich yet maintain Vienna client teams, and as Austrian law firms such as Schoenherr expand into Central and Eastern Europe to chase M&A and capital-markets fees. EU-wide tenders further dilute local incumbency, rewarding firms with pan-European delivery footprints.

Competitive Landscape

The Austria management consulting services market shows moderate concentration: the Big Four collectively control roughly 40-45% revenue, leveraging multidisciplinary breadth and embedded federal relationships. Strategy majors (McKinsey, BCG, Bain, Roland Berger) capture high-value C-suite mandates, while global IT integrators (Accenture, Capgemini, IBM Consulting) dominate digital transformation.

Consolidation shapes capability plays: EY absorbed sustainability specialist denkstatt in 2024, RSM merged with Moore Interaudit in 2025, and AdEx Partners bought BMC Strategy Consultants to scale succession services. Technology-enabled models gain traction; BearingPoint’s BeMind AI and IBM’s Txture acquisition automate cloud-migration scoping, reducing delivery costs and differentiating offers. German boutiques intensify price pressure, but their rise forces Austrian incumbents to emphasize local regulatory expertise and expedited grant navigation.

White-space opportunities emerge in AI governance for regulated sectors, hydrogen infrastructure advisory, and bundled succession-plus-ESG services for SMEs. Market entry barriers remain moderate: EU procurement frameworks require ISO certifications and multi-language staffing, yet remote delivery lessens physical presence needs. Overall, strategic positioning now hinges on proprietary IP, sector specialization, and cross-border resource pooling rather than pure scale.

Austria Management Consulting Services Industry Leaders

Deloitte Touche Tohmatsu Limited

PricewaterhouseCoopers LLP

KPMG

Ernst & Young Global Limited

Accenture

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: EY Austria launched the EY Defence initiative, targeting cybersecurity and critical-infrastructure consulting across the EU.

- March 2026: BearingPoint debuted the BeMind AI platform to automate analytics and report generation for banking, insurance, and public-sector clients.

- March 2026: Forvis Mazars Austria integrated Starlinger Mayer Rechtsanwält:innen GmbH to deliver interdisciplinary legal and advisory services.

- February 2026: BearingPoint secured a USD 675 thousand contract for MED-EL’s SAP S/4HANA migration covering global rollout and change management.

Austria Management Consulting Services Market Report Scope

The Austria Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current size of the Austria management consulting services market?

The market stands at USD 2.29 billion for 2025 and is projected to reach USD 3.01 billion by 2031, growing at 4.55% CAGR over 2026-2031.

Which consulting service line is growing the fastest in Austria?

Risk and Compliance Consulting is forecast to record the highest 4.81% CAGR through 2031, propelled by new EU sustainability and AI regulations.

Why are Austrian SMEs increasing their consulting spend?

Family-owned firms face simultaneous succession, digital transformation, and ESG disclosure requirements, prompting a 4.64% CAGR rise in SME consulting outlays.

How is the talent shortage affecting project delivery models?

Scarcity of bilingual digital consultants drives adoption of hybrid and remote delivery, with virtual engagements growing 4.72% annually.

Which industry will generate the highest consulting growth to 2031?

Energy and Resources leads with a 4.68% CAGR as hydrogen and decarbonization projects accelerate under national climate targets.

What competitive factors shape pricing in the Austrian market?

Cross-border German boutiques offer lower rates, while local firms leverage regulatory expertise and proprietary IP to defend margins.

Page last updated on: