Sweden Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

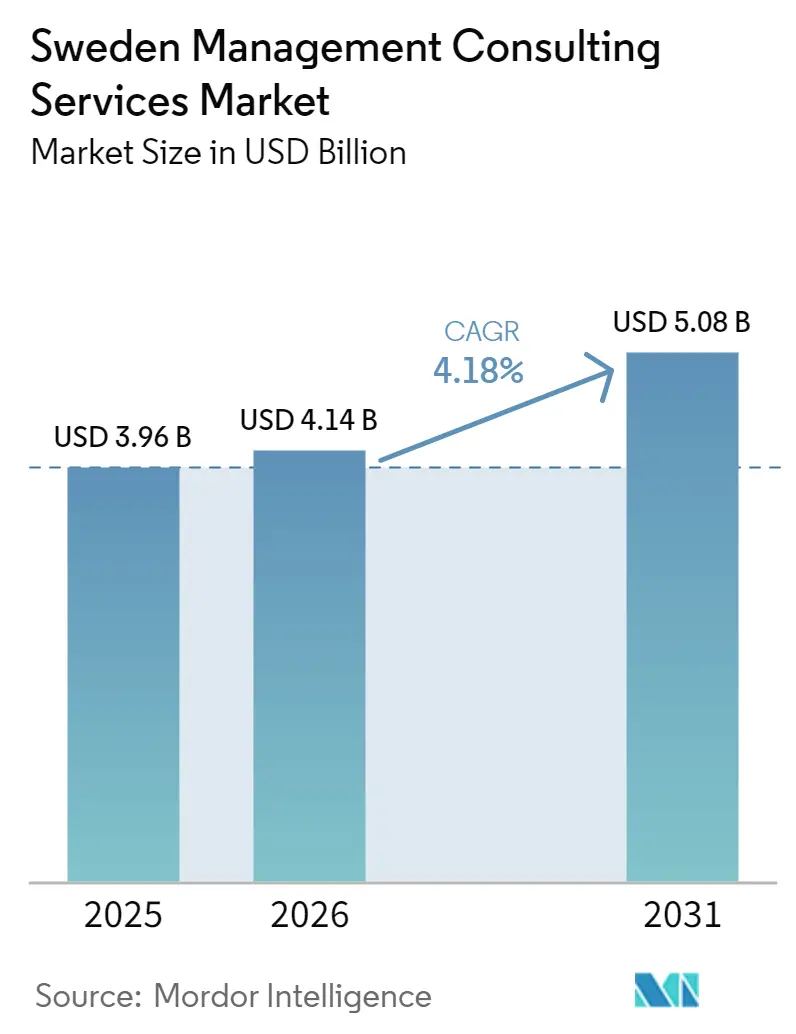

| Base Year Market Size (2025) | USD 3.96 Billion |

| Market Size (2026) | USD 4.14 Billion |

| Market Size (2031) | USD 5.08 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

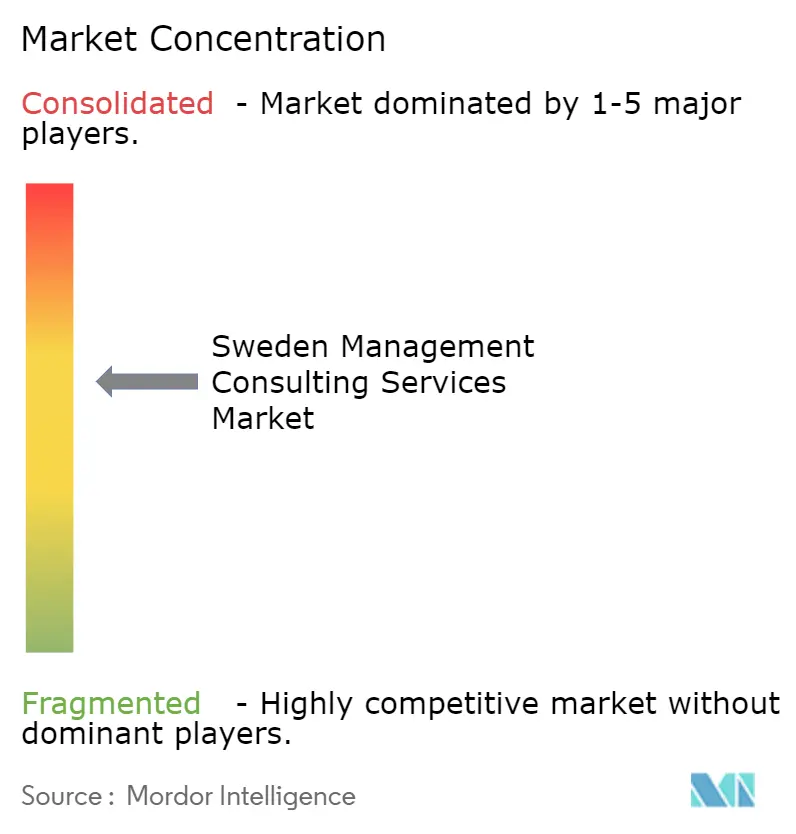

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Management Consulting Services Market Analysis by Mordor Intelligence

The Sweden management consulting services market size was valued at USD 3.96 billion in 2025 and estimated to grow from USD 4.14 billion in 2026 to reach USD 5.08 billion by 2031, at a CAGR of 4.18% during the forecast period (2026-2031). Advisory spend is shifting toward resilience programs, ESG compliance and cyber hardening as public and private organizations race to align with NATO, CSRD and NIS2 milestones. Defense spending that now targets 5% of GDP, sweeping energy-transition investments and an AI Strategy that underwrites public-sector pilots are enlarging the Sweden management consulting services market beyond its pre-2024 pattern. Demand is gravitating to firms that can bundle regulatory knowledge, technology enablement and change-management skills, while subscription pricing and productized assets keep entry barriers low for mid-market buyers. Competitive pressure, however, is eroding margin as offshore players scale remote delivery and local boutiques undercut on commoditized work, prompting larger firms to prune low-value service lines.

Key Report Takeaways

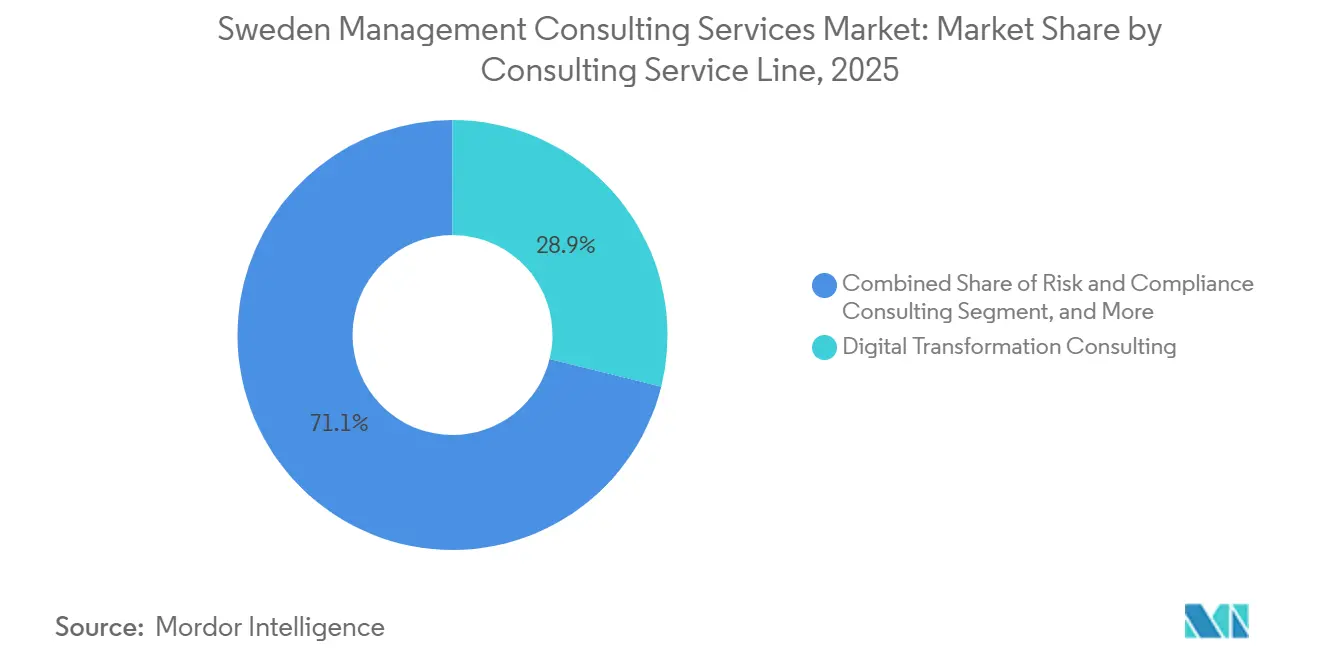

- By consulting service line, Digital Transformation Consulting led with 28.86% of Sweden management consulting services market share in 2025, whereas Risk and Compliance Consulting is projected to register the fastest 4.89% CAGR through 2031.

- By organization size, Large Enterprises accounted for 64.92% of 2025 spending, while Small and Medium-Sized Enterprises are poised to advance at a 4.67% CAGR to 2031.

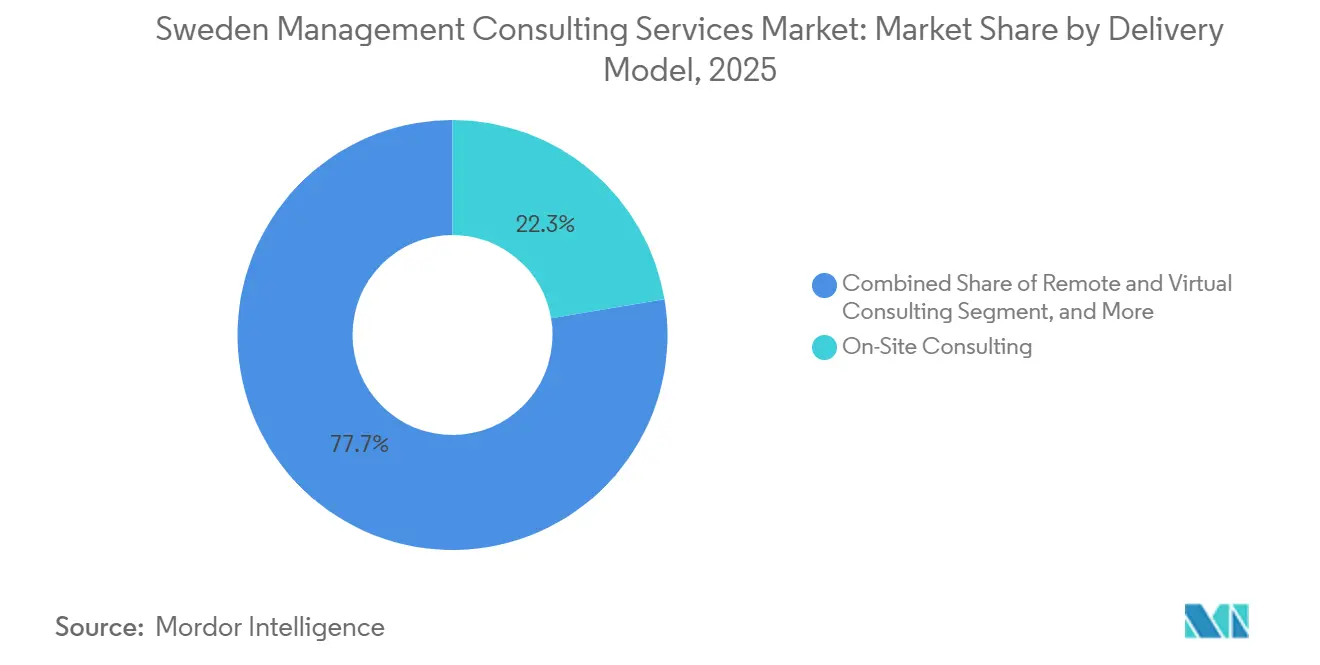

- By delivery model, On-Site Consulting retained a 22.34% slice of the Sweden management consulting services market size in 2025, yet Hybrid Consulting is expected to expand at a 4.76% CAGR over the same horizon.

- By end-user industry, Banking and Insurance held 22.14% of 2025 revenue, whereas Energy and Resources is forecast to post a 4.92% CAGR as decarbonization capital accelerates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Sweden Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Digital-Transformation Mandates Across Swedish Enterprises | +1.2% | National, concentrated in Stockholm, Gothenburg, Malmö tech hubs | Medium term (2-4 years) |

| Rising Demand for ESG and Sustainability Advisory Driven by EU Taxonomy Compliance | +1.0% | National, aligned with EU-wide CSRD implementation | Short term (≤ 2 years) |

| Mandatory NIS2 Cybersecurity Directive Boosting Resilience Consulting | +0.9% | National, priority in energy, transport and finance | Short term (≤ 2 years) |

| NATO Accession-Induced Surge in Defense and Security Consulting | +0.8% | National, spillover to wider Nordic cooperation | Medium term (2-4 years) |

| Scale-Up and IPO-Readiness Advisory Demand From Sweden’s Tech Ecosystem | +0.6% | National, startup clusters in Stockholm and Gothenburg | Medium term (2-4 years) |

| Result-Based and Subscription Pricing Models Expanding Consulting Addressable Spend | +0.4% | National, higher adoption among SMEs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Digital-Transformation Mandates Across Swedish Enterprises

Sweden’s AI Strategy 2026 funds pilot projects that move quickly from proofs of concept to production rollouts, fuelling multi-disciplinary programs across public and private sectors.[1]Government Offices of Sweden, “AI Strategy 2026,” Government Offices of Sweden, government.se Netlight’s 140% surge in AI assignments shows how clients now demand end-to-end design, build and run services rather than isolated workshops. Ethical-AI rules embedded in the forthcoming EU AI Act compel firms to integrate legal, risk and change-management workstreams into every transformation program. Partnerships such as CGI’s AI lab for the Swedish Board of Agriculture demonstrate that compliance and technology expertise now travel together. Consultants able to marry governance frameworks with generative-AI engineering are therefore winning larger, longer contracts, reinforcing the upward trajectory of the Sweden management consulting services market.

Rising Demand for ESG and Sustainability Advisory Driven by EU Taxonomy Compliance

CSRD transposition obliges roughly 2,000 Swedish companies to publish granular, assured ESG metrics, creating a reporting burden well beyond legacy sustainability teams.[2]European Commission, “Corporate Sustainability Reporting Directive (CSRD),” European Commission, finance.ec.europa.eu Firms like BearingPoint that achieved B-Corp status and secured analyst recognition for ESG program management are capturing mandates for double-materiality analysis and assurance readiness. Energy-transition capital, SEK 170 billion (USD 18 billion) set aside for grid upgrades and SEK 36 billion for bio-CCS auctions, ties finance access to Taxonomy alignment, so advisory on project finance, permitting and disclosure has become indispensable.[3]BearingPoint, “Annual Report 2024,” BearingPoint, bearingpoint.com Consultants connecting sustainability strategy with capital-market signaling now command premium fees and materially lift the Sweden management consulting services industry growth curve.

Mandatory NIS2 Cybersecurity Directive Boosting Resilience Consulting

The October 2024 Cybersecurity Act widened the pool of critical entities from 500 to more than 2,000, forcing boards to treat cyber risk as a strategic priority carrying fines up to EUR 10 million (USD 11.3 million). With half of specialist IT roles hard to fill, clients rely on external advisers for OT security, incident response and supply-chain resilience. Multi-year frameworks such as AFRY’s agreement with Svenska Kraftnät show how infrastructure hardening locks in predictable consulting revenues.[4]AFRY, “Framework Agreements and Major Contracts,” AFRY, afry.com As utilities modernize grids to absorb 90 TWh of offshore wind, demand for cross-domain cyber-and-engineering expertise accelerates, bolstering the Sweden management consulting services market.

NATO Accession-Induced Surge in Defense and Security Consulting

Sweden’s pledge to lift defense outlays to 5% of GDP unlocks advisory work spanning procurement reform, interoperability audits and classified IT architecture. AFRY’s SEK 1.5 billion (USD 162 million) contract with FMV underlines the breadth of project-management and technical expertise required. Clearance requirements and long procurement cycles curb new entrants, so consultancies with existing defense credentials enjoy high win rates and visibility. The pipeline extends to supply-chain localization and export-control compliance, broadening the addressable spend that feeds directly into the Sweden management consulting services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent Shortage and Consultant Wage Inflation | -0.7% | Stockholm, Gothenburg, Malmö metros | Short term (≤ 2 years) |

| Fee Compression From Intensifying Competition Among Local and Global Firms | -0.5% | National, mid-market and commoditized lines | Medium term (2-4 years) |

| Cyclical CAPEX Exposure in Manufacturing and Industrial Client Base | -0.3% | Automotive and heavy-industry clusters | Medium term (2-4 years) |

| Off-Shore Remote-Delivery Players Driving Price Pressure | -0.2% | IT and digital transformation segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Talent Shortage and Consultant Wage Inflation

Two-thirds of Swedish consultancies report recruiting difficulties, while attrition climbed to 12.8% in 2025. PayScale benchmarks show base salaries lag fast-growing tech firms, so traditional employers are boosting pay faster than they can raise bill rates, compressing margins industry-wide.[5]PayScale, “Management Consultant Salary in Sweden,” PayScale, payscale.com Scarcity is worst in AI, OT security and functional-safety roles, where LinkedIn data confirms 50% of vacancies are hard to fill. Firms now invest aggressively in learning platforms, remote-work flexibility and international hiring, but near-term wage pressure still shaves growth from the Sweden management consulting services market.

Fee Compression From Intensifying Competition Among Local and Global Firms

Revenue growth slowed to 2.6% and average margins to 4.4% in 2025 as clients demanded outcome-based pricing.[6]Cinode, “Konsultkollen 2025: Growth Slows Significantly in the Swedish Consulting Sector,” Cinode, cinode.com Big Four divestitures of SME units illustrate how firms jettison low-yield business, yet boutiques thrive by specializing in AI and energy-transition niches. The swing to subscription models cuts upfront spend and makes revenue less predictable, lowering overall price points and dampening the Sweden management consulting services industry expansion until firms rebalance portfolios toward higher-value offerings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Compliance Work Becomes the Prime Growth Engine

Risk and Compliance Consulting is forecast to expand at a 4.89% CAGR through 2031, outpacing the overall Sweden management consulting services market size and threatening to overtake Digital Transformation’s 28.86% 2025 lead. Digital Transformation Consulting, while still the largest contributor in 2025, faces commoditization as scalable AI platforms reduce bespoke coding hours. Strategy and operations projects retain board-level relevance, especially around productivity reforms and fossil-free steel production, but many engagements now embed regulatory deliverables that push clients toward compliance specialists. The cumulative effect is a shift in fee mix that elevates market resilience, yet rewards firms that invest in deep regulatory expertise and cross-functional delivery models.

Compliance momentum is anchored in the sheer volume of new obligations, from NIS2 incident-response protocols to CSRD double-materiality matrices, that midsize Swedish entities cannot meet internally. Advisory pipelines therefore lengthen, improving revenue visibility for firms entrenched in this segment. Meanwhile, productized SaaS assets for demand-sensing and persona analytics, launched by players such as BearingPoint, temper growth in pure-play digital consulting. Collectively, these forces recast the Sweden management consulting services market size distribution in favor of legally intensive workstreams.

By Organization Size: Modular Models Unlock SME Expansion

Large Enterprises generated 64.92% of 2025 spend, yet their growth trails the Sweden management consulting services market size baseline because procurement consolidation and internal centers of excellence cut external hours. In contrast, SMEs benefit from subscription pricing that cuts upfront commitment, nudging them toward advisory engagement earlier in the scaling journey. The surge of Swedish unicorns preparing IPO filings magnifies governance and risk-control needs, drawing fresh revenue into the Sweden management consulting services market. Consultancies that package IPO readiness, financial controls and talent architecture as modular sprints appeal to founders keen to preserve cash while meeting investor thresholds.

Corporate carve-outs by KPMG and EY show how incumbent firms recalibrate portfolios away from low-margin SME work. Yet mid-tier acquirers and cloud-native consultancies step into the gap with templated solutions and shared-risk contracts. As more unicorns transition from growth funding to public-market discipline, SME advisory revenue is likely to compound faster than the broader Sweden management consulting services industry, though absolute spend will still trail enterprise budgets

By Delivery Model: Hybrid Gains Traction Under Talent Constraints

Hybrid Consulting is projected to rise 4.76% annually through 2031, the quickest pace among models, as firms blend remote centers of excellence with targeted on-site work to conserve scarce specialist capacity. Although On-Site engagements kept a 22.34% slice of the Sweden management consulting services market share in 2025, wage inflation and travel cost spikes make full-time staffing harder to justify except for security-cleared defense projects. Remote work alone cannot satisfy NIS2 audit protocols or high-risk AI system validations that mandate in-person verification, so clients adopt hybrid as the pragmatic middle ground.

Under this model, discovery and design phases run virtually while implementation sprints place small teams on the factory floor, grid substation or naval base. AFRY’s SEK 1.5 billion (USD 144 million) framework with the Defence Materiel Administration exemplifies the blend: architects work off-site while certified engineers rotate on-site for acceptance tests. Margin improves because remote staff can bill across multiple clients, yet quality hinges on robust collaboration platforms and shared delivery playbooks. High-growth boutiques such as Netlight, which opened a London hub to tap British AI talent for Swedish clients, prove the scalability of the approach. As more firms refine governance around distributed teams, hybrid is expected to set the delivery standard for the Sweden management consulting services market size in the next five years.

By End-User Industry: Energy Transition Drives the Next Demand Wave

Banking and Insurance finished 2025 with a commanding 22.14% revenue share, but Energy and Resources is set to register the strongest 4.92% CAGR as decarbonization budgets swell. Sweden’s National Energy and Climate Plan directs SEK 170 billion (USD 16.3 billion) to grid upgrades and SEK 36 billion (USD 3.5 billion) to bio-CCS auctions, catalyzing multiyear consulting frameworks that lift the Sweden management consulting services market size tied to infrastructure. The push reaches into metals as well, SSAB’s Luleå overhaul at EUR 4.5 billion (USD 5.1 billion) spawns operational, environmental and financing mandates that ripple through the supply chain.

Manufacturing still drives operations consulting because automotive electrification and circular-economy goals demand factory overhauls and logistics redesign. However, project timing can swing with capex cycles, injecting volatility into order books. Healthcare and public-sector clients remain steady consumers of digital and data advisory, though their budget ceilings trail private-sector appetites. Retail, logistics and consumer goods engagements are increasingly sustainability-linked, leveraging Scope-3 accounting and circular design as entry points. Overall, the accelerating energy transition secures a durable growth floor and widens the Sweden management consulting services market share captured by firms with deep sector techno-economic expertise.

Geography Analysis

Sweden’s consulting activity clusters around Stockholm, Gothenburg and Malmö, reflecting the co-location of headquarters, universities and R&D hubs. These metros concentrate the talent and client density that sustain quick-turnaround engagements, thereby anchoring half of Sweden management consulting services market revenue. Stockholm alone houses the majority of the country’s 48 unicorns, amplifying demand for IPO readiness, governance and scaling advisory. Gothenburg’s automotive and maritime complexes drive operations consulting centered on electrification and logistics, while Malmö’s proximity to Copenhagen creates cross-border projects that blend Danish and Swedish regulatory environments.

Northern Sweden is emerging as a fresh advisory frontier. Large-scale renewable projects and SSAB’s fossil-free steel investment pull consultancies toward Luleå, Skellefteå and other towns near hydropower resources. These assignments are site-intensive, necessitating hybrid delivery where remote design teams support on-site engineers conducting environmental and safety audits. Cross-border dynamics also matter; global firms use Stockholm as a springboard to Nordic and Baltic markets, intensifying competition and expanding the total opportunity pool within the Sweden management consulting services market.

The regional footprint is further shaped by infrastructure geography. Grid modernization ties consulting spend to transmission corridors operated by Svenska Kraftnät, requiring touchpoints across multiple counties. Ports designated as critical infrastructure under NIS2, including Gothenburg and Malmö, become hotspots for cyber-and-resilience advisory. Consequently, while national regulation is uniform, physical asset locations pull consulting capacity into specific regions, balancing the market away from the Stockholm-centric pattern that prevailed a decade ago.

Competitive Landscape

The Sweden management consulting services market is moderately fragmented, hosting global strategy houses, Big Four audit-linked consultancies, Nordic engineering-plus-advisory groups and upwardly mobile boutiques. Cinode’s 2025 data reveal that average revenue growth slowed dramatically, yet specialist firms such as Aixia and Triive posted triple-digit gains by focusing on AI, energy transition and industrial transformation. Capgemini’s position as top IT service provider underscores the growing advantage of firms offering integrated stacks that span advisory, implementation and managed services.

Margin pressure drives portfolio pruning. KPMG and EY divested SME units to concentrate on higher-value enterprise and compliance work. Productization is another lever; BearingPoint’s 208-strong asset library converts know-how into recurring revenue that buffers fee compression. Technology partnerships act as force multipliers: CGI’s Gemini Enterprise alliance with Google gives it generative-AI depth comparable to larger rivals, while Netlight’s UK office lets the firm import scarce talent at lower cost. ESG credibility is becoming a competitive moat, with clients favoring advisers that themselves hold B-Corp status or Science-Based Targets. Overall, success hinges on domain depth, delivery innovation and the credibility to steer clients through regulatory complexity.

Sweden Management Consulting Services Industry Leaders

KPMG Sweden

Boston Consulting Group Inc.

Accenture Plc

McKinsey & Company, Inc.

Deloitte Touche Tohmatsu Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Knowit received Microsoft Support Services Designation, enhancing its enterprise cloud and AI credentials.

- March 2026: Bain Capital invested in Tingstad, signaling private-equity appetite for Swedish mid-market logistics specialists.

- February 2026: Consid booked SEK 220 million (USD 23.7 milion) in contracts, buoyed by a SEK 5.12 billion USD 553 million) (framework with Svenska Kraftnät.

- January 2026: SSAB’s EUR 4.5 billion (USD 5 billion) fossil-free steel mill in Luleå gained EU net-zero project status, unlocking long-term advisory work.

- January 2026: CGI unveiled a Gemini Enterprise partnership to integrate generative AI in Swedish public-sector engagements.

Sweden Management Consulting Services Market Report Scope

The Sweden Management Consulting Services Market Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current size of the Sweden management consulting services market and how fast will it grow?

It stood at USD 3.96 billion in 2025, is expected to reach USD 4.14 billion in 2026 and USD 5.08 billion by 2031, reflecting a 4.18% CAGR between 2026 and 2031.

Which consulting service line is growing fastest in Sweden?

Risk and Compliance Consulting is projected to post the quickest expansion, with a 4.89% CAGR through 2031 as firms address CSRD and NIS2 deadlines.

How are small and medium-sized enterprises changing demand for advisory services?

SMEs are adopting subscription and outcome-based models, driving a 4.67% CAGR that outpaces spending by large enterprises.

Why is hybrid delivery gaining popularity among Swedish consultancies?

Talent shortages and cost controls encourage firms to blend remote expertise with targeted on-site work, making hybrid the fastest-growing delivery model at 4.76% CAGR.

Which end-user sector will account for the strongest consulting growth?

Energy and Resources leads with a forecast 4.92% CAGR, propelled by grid upgrades, offshore wind projects and industrial decarbonization investments.

What is the biggest challenge facing consulting firms in Sweden?

Sustained wage inflation, especially for AI and cybersecurity specialists, is squeezing margins and raising project costs across the industry.

Page last updated on: