Luxembourg Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

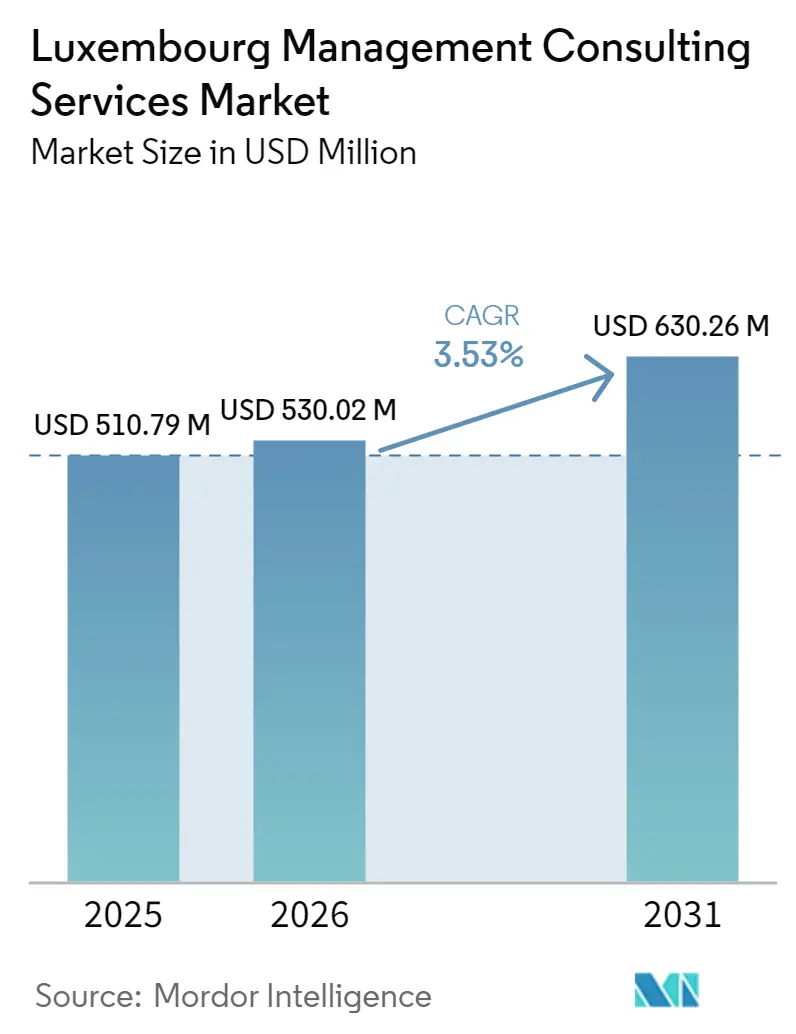

| Base Year Market Size (2025) | USD 510.79 Million |

| Market Size (2026) | USD 530.02 Million |

| Market Size (2031) | USD 630.26 Million |

| Growth Rate (2026 - 2031) | 3.53% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Luxembourg Management Consulting Services Market Analysis by Mordor Intelligence

The Luxembourg management consulting services market size is expected to increase from USD 510.79 million in 2025 to USD 530.02 million in 2026 and reach USD 630.26 million by 2031, growing at a CAGR of 3.53% over 2026-2031. Ongoing cloud migrations across the EUR 5.95 trillion fund-administration hub, stricter digital-operational-resilience rules, and higher ESG-reporting burdens underpin steady advisory demand. Growth remains measured because fee rates are benchmarked against lower-cost Brussels and Frankfurt offices, while the saturation of Big Four and MBB firms curbs pricing power. Government incentives such as the 18% investment-tax credit and Fit 4 Digital vouchers extend consulting uptake beyond universal banks to small manufacturers and professional-services firms. Demand volatility persists, however, because discretionary projects still ride on capital-market inflows and the pace of cross-border deal making.

Key Report Takeaways

- By consulting service line, Digital Transformation Consulting led with 32.87% revenue share in 2025, while Risk and Compliance Consulting is projected to advance at a 3.89% CAGR through 2031.

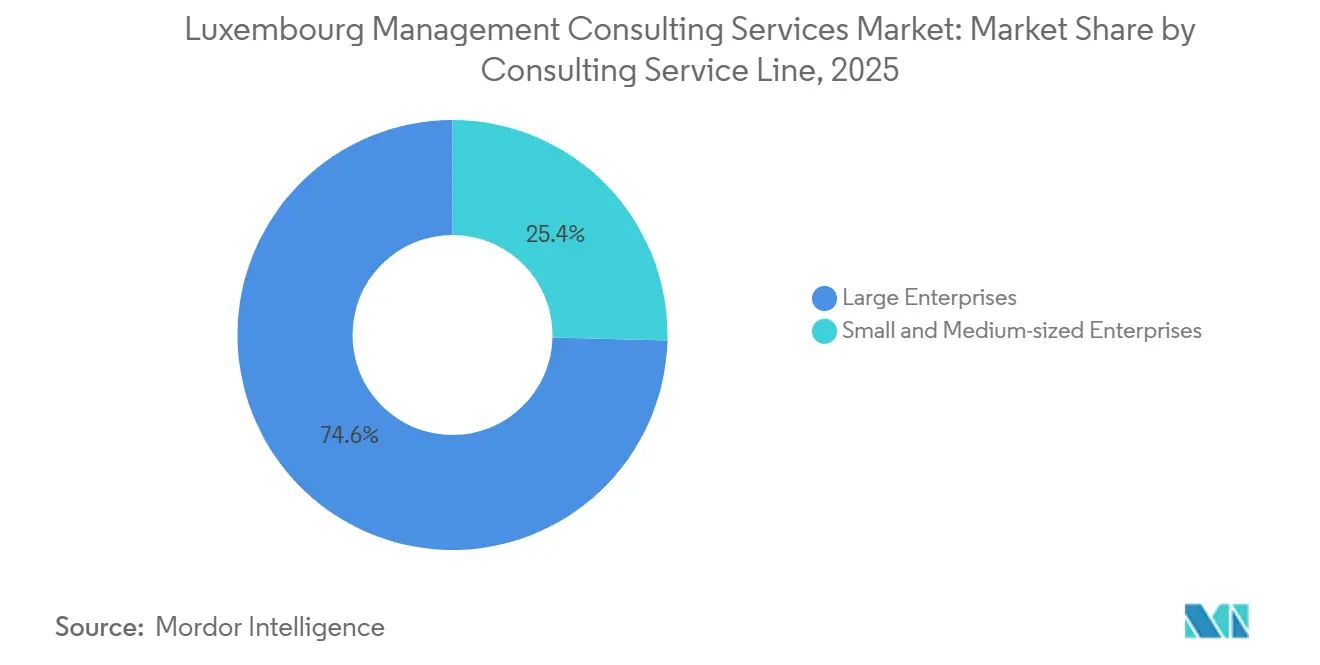

- By organization size, Large Enterprises held 61.72% of the Luxembourg management consulting services market share in 2025, whereas Small and Medium-Sized Enterprises are forecast to post the fastest 3.64% CAGR between 2026-2031.

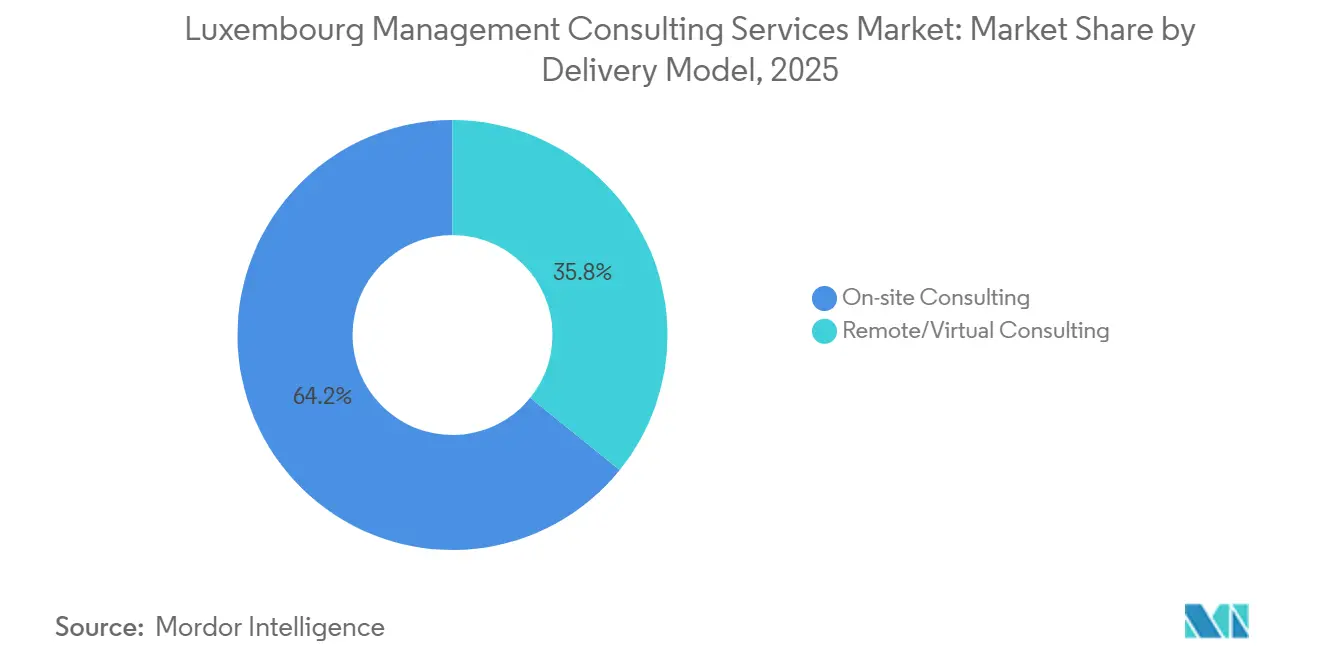

- By delivery model, On-Site engagements accounted for 54.06% of spending in 2025, yet Remote and Virtual Consulting is on track for the quickest 3.97% CAGR to 2031.

- By end-user industry, Banking and Insurance represented 27.18% of 2025 demand, while the Public Sector is expected to grow at a 3.71% CAGR under the Digital Government Strategy 2026-2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Luxembourg Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-Transformation Spend by EUR 5.5 Trillion Fund-Administration Hub | +1.2% | National, spillover to Belgium, France, Germany | Medium term (2-4 years) |

| ESG-Linked Compliance Mandates (CSRD, AML 5) | +0.9% | National, aligned with EU directives | Short term (≤ 2 years) |

| Government AI Infrastructure Program (EUR 120 million) | +0.5% | National, cross-border research links | Medium term (2-4 years) |

| Data-Residency Rules for EU Financial Cloud | +0.4% | National, EEA regulatory alignment | Short term (≤ 2 years) |

| Enhanced Investment-Tax Credit for Digital Projects | +0.3% | National | Medium term (2-4 years) |

| Hybrid-Work Cross-Border Tax Thresholds | +0.2% | National plus Belgium, France, Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital-Transformation Spend by Fund-Administration Hub

Luxembourg custodians and transfer agents continue to re-platform legacy SWIFT systems onto API-based stacks that support same-day NAV calculations and real-time investor dashboards. Fifty-eight new fund entities cleared by the CSSF during 2025 each mandated multi-quarter cybersecurity and integration roadmaps that consulting firms now treat as annuity workstreams. ETF assets domiciled in the Grand Duchy climbed to EUR 531.8 billion (USD 600.7 billion), accelerating demand for data-lake architectures and model-validation services that internal IT teams lack. Illiquid ELTIF portfolios require bespoke valuation engines, further widening the skills gap that external advisors fill. Green-bond listings on the Luxembourg Green Exchange surpassed EUR 1.3 trillion (USD 1.47 trillion), prompting a surge in ESG-data-aggregation mandates that feed directly into the Luxembourg management consulting services market.[1]Luxembourg Green Exchange. "Green Bond Listings." bourse.lu

ESG-Linked Compliance Mandates (CSRD, AML 5)

The phased rollout of the Corporate Sustainability Reporting Directive compels Luxembourg-domiciled funds to map Scope 1, 2, and 3 emissions, while AML 5 demands real-time screening of beneficial owners. Limited exemptions awarded to non-EU subsidiaries do little to lessen disclosure burdens because double-materiality assessments remain compulsory. Banks are therefore engaging consultants for rapid-diagnostic reviews and remediation playbooks that dovetail with CSRD data-governance programs. Upcoming AMLR rules and the AMLA supervisory template issued in early 2026 lock in a multiyear pipeline of compliance-consulting workstreams, bolstering revenue visibility across the Luxembourg management consulting services market.[2]European Anti-Money Laundering Authority, “Supervisory Template,” amla.europa.eu

Government AI Infrastructure Program (EUR 120 Million)

Public funding for the MeluXina-AI supercomputer grants domestic firms low-latency access to 2.5 petaflops of compute optimized for large-language-model fine-tuning. Alternative-investment managers are piloting sentiment-analysis engines on the platform but need external expertise to align outputs with the EU AI Act’s high-risk-system rules. Consulting practices now bundle algorithmic-bias audits with governance-framework design, creating fresh revenue pockets. Parallel public-sector spending on AI chatbots for citizen portals extends the addressable base for advisory firms beyond finance and into government agencies, widening the Luxembourg management consulting services market footprint.[3]LuxProvide, “MeluXina-AI and AI Factory,” luxprovide.lu

Data-Residency Rules for EU Financial Cloud

Circular 25/881 and sibling guidance require that critical workloads for banks and funds sit inside the EEA, effectively forcing cloud-exit strategies or hybrid topologies. The Clarence sovereign-cloud joint venture with LuxConnect and Proximus won an inaugural EUR 10 million (USD 11.3 million) hosting deal, signaling regulatory preference for on-shore infrastructure. Consulting firms are capitalizing by drafting cloud-supplier agreements, exit-playbooks, and residency attestations, all of which translate into incremental demand across the Luxembourg management consulting services market.[4]LuxConnect and Proximus, “Clarence Sovereign Cloud,” clarence.lu

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturation by Big Four and MBB Limiting Fee-Rate Upside | -0.6% | National | Long term (≥ 4 years) |

| High Dependency on Cyclical Fund Flows | -0.4% | National, exposed to global capital markets | Short term (≤ 2 years) |

| Talent Scarcity and Elevated Unemployment Inflating Salaries | -0.3% | National | Medium term (2-4 years) |

| Rising Telework Legislation Complexity | -0.2% | National plus Belgium, France, Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Saturation by Big Four and MBB Limiting Fee-Rate Upside

PwC, EY, Deloitte, KPMG, McKinsey, BCG, and Bain collectively garner most large-ticket mandates, leaving mid-tier firms with niche compliance or transfer-pricing work. Multinationals benchmark Luxembourg proposals against cheaper Brussels or Frankfurt offices, forcing local partners to shave margins. The result is a pricing ceiling that erodes top-line scalability even as project volumes stay healthy, tempering the overall growth trajectory of the Luxembourg management consulting services market.

High Dependency on Cyclical Fund Flows

Advisory budgets track net inflows into the EUR 5.82 trillion (USD 6.58 trillion) fund sector, making discretionary projects vulnerable to equity drawdowns and rate shocks. The 2022 correction already illustrated how redemptions can freeze transformation roadmaps. STATEC now flags a 6.3% unemployment rate alongside slowing GDP growth, signs that another downturn would quickly compress consulting pipelines and drag on the Luxembourg management consulting services market.[5]STATEC, “Unemployment Rate - February 2026,” statistiques.public.lu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Compliance Momentum Overtakes Digital First Mover

Risk and Compliance engagements, projected to expand at a 3.89% CAGR, benefit from the convergence of DORA go-live deadlines, CSRD disclosure cycles, and the upcoming AML Regulation. In contrast, Digital Transformation assignments, although still commanding 32.87% revenue share, are normalizing as first-wave cloud migrations reach maturity. The Luxembourg management consulting services market size for compliance-focused work therefore sees steadier contract renewals, especially for recurring penetration tests and regulatory-change portfolios that stretch over multiple fiscal years. Meanwhile, strategy consulting remains dominated by MBB boutiques advising on holding-company restructurings, but limited headquarters presence in Luxembourg constrains its ceiling.

Government tax incentives and the Fit 4 Digital voucher scheme continue to stimulate fresh ERP and CRM projects, yet saturation appears in legacy system overhauls. Consulting practices now pivot toward composable architectures and GenAI proof-of-concepts hosted on sovereign-cloud nodes, signaling a gradual shift from lift-and-shift work to value-layer innovation. Cross-disciplinary offerings that weave ESG metrics into finance-transformation roadmaps are emerging as competitive differentiators within the Luxembourg management consulting services market share landscape.

By Organization Size: SME Uptake Accelerates on Voucher Funding

Small and Medium-Sized Enterprises capture an expanding slice of advisory demand thanks to EUR 5,000 (USD 5500) Fit 4 Digital grants and the SME Package Digital subsidy. Although Large Enterprises still fund 61.72% of overall spend, framework contracts and internal centers of excellence reduce their annual call-offs, keeping their growth rate behind the SME cohort. The Luxembourg management consulting services market size linked to SMEs therefore shows incremental upside as voucher recipients convert diagnostics into paid implementation projects.

Persistent difficulty recruiting data engineers and cloud architects, despite a recent uptick in highly qualified unemployment, forces SMEs to outsource interim expertise. Mid-tier advisors such as Grant Thornton plug this gap with bundled VAT, transfer-pricing, and cybersecurity services. Large Enterprises, by contrast, negotiate volume discounts with Big Four networks that cap fee inflation, underlining divergent pricing dynamics inside the Luxembourg management consulting services market.

By Delivery Model: Remote Formats Push Hybrid Engagements Forward

Remote and Virtual Consulting, projected to post a 3.97% CAGR, benefits from Luxembourg’s bilateral telework thresholds that let cross-border staff work up to 34 days abroad without new tax or social-security filings. Client executives now accept virtual design-thinking sprints and video-enabled steering committees, so firms deploy collaboration suites to keep utilization high while limiting travel overheads. On-Site Consulting, still holding 54.06% share in 2025, retains primacy for regulatory inspections and senior-stakeholder workshops, yet it loses routine analytics and documentation tasks to offshore delivery hubs that connect through sovereign-cloud nodes. The Luxembourg management consulting services market size linked to hybrid formats is therefore expanding because programs start with in-person kick-offs and pivot to remote execution once workstreams stabilize.

Demand for tax and payroll advice around Belgium’s, France’s, and Germany’s differing day-count rules creates an ancillary stream of workforce-strategy work. Firms package that guidance with technology toolsets that log employee locations and automate treaty compliance, converting statutory complexity into recurring advisory revenue. Remote security requirements also raise the bar for ISO-aligned data-governance processes, so certifications such as Europrivacy have become competitive differentiators. Gartner’s 2026 recognition of CGI’s remote SAP methodology further validates virtual implementation models and encourages mid-tier players to invest in similar accelerators. Collectively, these shifts keep the Luxembourg management consulting services market share for remote delivery on an upward track without cannibalizing essential face-to-face engagements.

By End-User Industry: Public Budgets Spur Next Wave of Growth

Public-Sector outlays are set to rise at a 3.71% CAGR as the Digital Government Strategy 2026-2030 funds AI chatbots, data-interoperability layers, and citizen-portal upgrades. Ministries launch program-management offices to coordinate tenders, and consultancies secure multi-year assignments covering architecture blueprints, procurement support, and legacy-system retirement. Banking and Insurance, which contributed 27.18% of 2025 revenue, continues to modernize core platforms, yet new project starts decelerate once major compliance milestones are met. Instead, life and non-life carriers engage specialists for actuarial-model recalibration and climate-scenario testing, assignments that are shorter and more cyclical than initial system replacements.

IT and Telecommunications spend aligns with 5G rollouts and a wave of M and A integrations, while manufacturing remains a niche because the national industrial base is small. Energy-and-Resources clients focus on renewable-financing structures and carbon-credit audits that dovetail with CSRD reporting needs. Healthcare consulting gains marginal traction through e-prescription pilots and cross-border patient-record exchanges but stays sub-scale in absolute terms. Professional-services, real-estate, and logistics firms round out residual demand by seeking tax structuring, supply-chain digitalization, and ESG dashboards. The Luxembourg management consulting services market size tied to public administration therefore drives the headline outlook, offsetting moderation in private-sector discretionary budgets.

Geography Analysis

Luxembourg City’s Kirchberg and Cloche d’Or districts dominate engagement origination, yet the 250,000 daily commuters from Belgium, France, and Germany supply critical labor elasticity. Proximity to Brussels and Frankfurt eases talent bottlenecks because bilingual consultants can shuttle across borders while staying within telework thresholds, a practice that cushions salary inflation in the compact domestic market. The Belval innovation campus in the south hosts university spin-offs and public-private labs, giving rise to small but growing advisory assignments in materials science and fintech commercialization.

Cross-border tax and social-security optimization keeps payroll-consulting pipelines full, particularly as firms adopt hybrid work and need automated treaty-compliance engines. Luxembourg’s holding-company regime also attracts private-equity sponsors structuring pan-European deals, so transaction-related advisory spans legal, tax, and post-merger integration work. Regulatory reach extends beyond national borders because the CSSF supervises more than 3,800 entities whose operations touch the entire European Economic Area, anchoring a steady flow of DORA and CSRD compliance projects.

Regional differentiation inside the country is limited by its small footprint, yet rural Éislek generates modest tourism-strategy engagements and the Moselle valley hosts sustainability audits for vintners adopting organic certification. Meanwhile, sovereign-cloud build-outs position the nation as a data-residency safe haven, prompting Belgian and German banks to consider hosting workloads in Luxembourg under CSSF-compliant frameworks. Collectively, these dynamics keep the Luxembourg management consulting services market size concentrated in the capital but increasingly dependent on Greater-Region labor flows and cross-border regulatory harmonization.

Competitive Landscape

Market concentration stays high, with Big Four and MBB firms retaining the bulk of multi-million-euro mandates through bundled audit-tax-advisory frameworks and global delivery leverage. PwC Luxembourg booked EUR 314 million (USD 354.9 million) during FY24, and EY followed closely with EUR 306 million (USD 345.8 million), underscoring the pricing ceiling mid-tiers face when competing for transformation deals. Deloitte and KPMG reinforce their positions via proprietary cloud accelerators and managed-services offerings that convert one-off projects into annuity streams, a tactic that stabilizes utilization during fund-flow dips.

Mid-tier challengers such as Grant Thornton and BearingPoint differentiate on regulatory-technology depth or sector specialization but struggle to match the scale economies of integrated networks. Technology alliances are emerging as force multipliers: PwC’s GenAI Business Center with Microsoft packages large-language-model proofs of concept alongside compliance wrappers, while KPMG’s tie-up with Allvue embeds fund-accounting software into risk-reporting workflows. Boutique ESG and cybersecurity shops carve out niches around CSRD double-materiality and DORA penetration testing, although limited brand equity keeps their deal sizes small.

The competitive narrative now pivots to responsible-AI and digital-asset custody, where regulation is evolving faster than in more mature advisory domains. Bain’s appointment of a regional managing partner dedicated to Benelux signals renewed MBB investment, yet the shortage of Fortune 500 headquarters in the country caps the pipeline of pure-play strategy engagements. Most firms therefore tilt toward value-creation work for private-equity portfolios and sovereign-wealth funds, spreading risk across geographies while sustaining the Luxembourg management consulting services market share they already command.

Luxembourg Management Consulting Services Industry Leaders

-

Accenture S.A. Luxembourg

-

Deloitte Luxembourg S.à r.l.

-

PricewaterhouseCoopers, Société cooperative (PwC Luxembourg)

-

Ernst and Young S.A. Luxembourg

-

KPMG Luxembourg, Société cooperative

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The CSSF outlined 2026 supervisory priorities for investment funds, spotlighting DORA third-party risk and sustainability-disclosure accuracy.

- February 2026: Bain named Cédric Bovy as Benelux managing partner to scale private-equity and corporate-transformation work.

- January 2026: EY Luxembourg secured Europrivacy accreditation under ISO/IEC 27701, enhancing its GDPR-aligned remote-delivery credentials.

- January 2026: CGI earned Leader status in Gartner’s Magic Quadrant for SAP S/4HANA Application Services, reinforcing its virtual-implementation capability.

Luxembourg Management Consulting Services Market Report Scope

The Luxembourg Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the projected Luxembourg management consulting services market size by 2031?

It is forecast to reach USD 630.26 million.

Which consulting service line is expected to grow fastest through 2031?

Risk and Compliance Consulting, with a projected 3.89% CAGR.

How do telework agreements influence consulting delivery models?

Bilateral treaties allow up to 34 remote workdays abroad, accelerating demand for remote and hybrid consulting formats.

Why is the public sector a key growth area for consultancies?

The Digital Government Strategy 2026-2030 funds AI pilots and portal modernization, driving multi-year advisory contracts.

What limits fee-rate upside for firms in Luxembourg?

Saturation by Big Four and MBB practices forces price benchmarking against lower-cost neighboring offices.

Which technology trend is creating new advisory niches?

Responsible-AI governance linked to the EU AI Act is generating demand for bias audits and compliance frameworks.

Page last updated on: