Germany Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

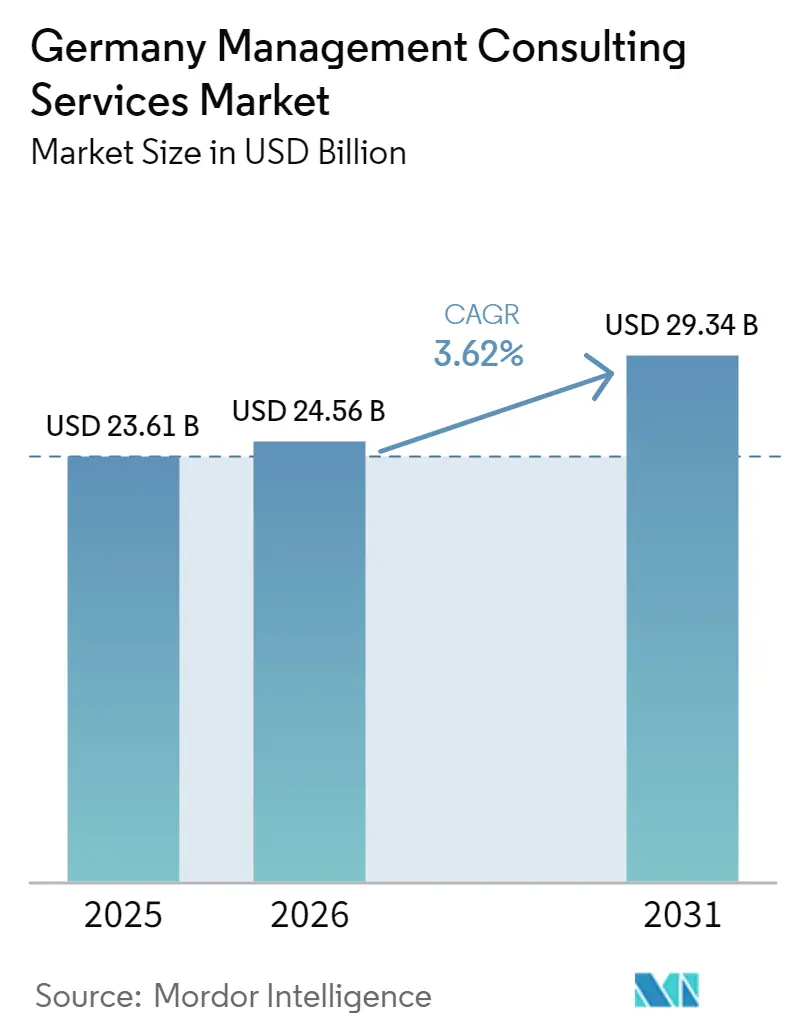

| Base Year Market Size (2025) | USD 23.61 Billion |

| Market Size (2026) | USD 24.56 Billion |

| Market Size (2031) | USD 29.34 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Management Consulting Services Market Analysis by Mordor Intelligence

The Germany management consulting services market size is projected to expand from USD 23.61 billion in 2025 and USD 24.56 billion in 2026 to USD 29.34 billion by 2031, registering a CAGR of 3.62% between 2026 and 2031. Demand remains resilient because German enterprises continue to modernize ERP landscapes, prepare for stricter European regulations, and address leadership succession. Growth is cushioned by public-sector digitalization funds, the Energiewende supply-chain overhaul, and rising ESG audit workloads. At the same time, talent scarcity and increasing use of freelance platforms keep pricing in check, while large corporations rely more on in-house advisory teams. Competitive pressure stays elevated because no firm controls more than 8% share, giving mid-tier specialists room to capture niche mandates in pricing, automotive transformation, and operational excellence.

Key Report Takeaways

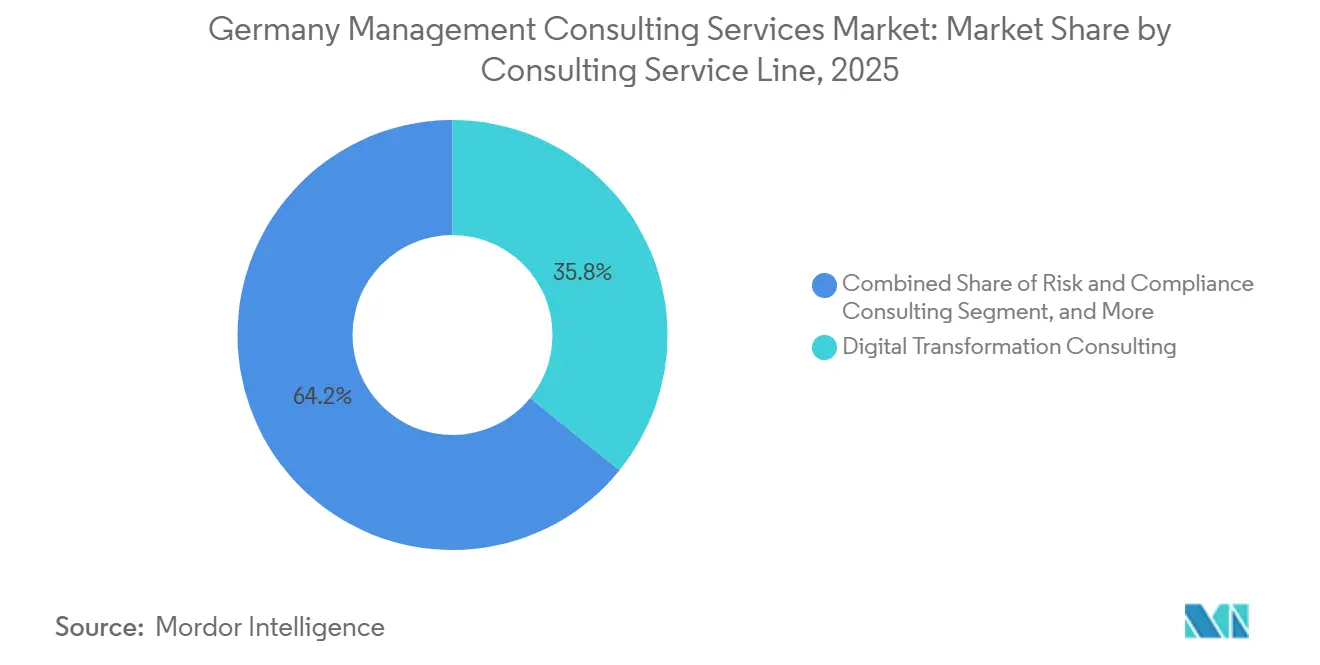

- By consulting service line, digital transformation held 35.83% revenue share of the Germany management consulting services market size in 2025, while Risk and Compliance is forecast to record the fastest 4.19% CAGR to 2031.

- By organization size, large enterprises accounted for 58.69% of 2025 spending, whereas small and medium-sized enterprises are on track for a 3.87% CAGR through 2031.

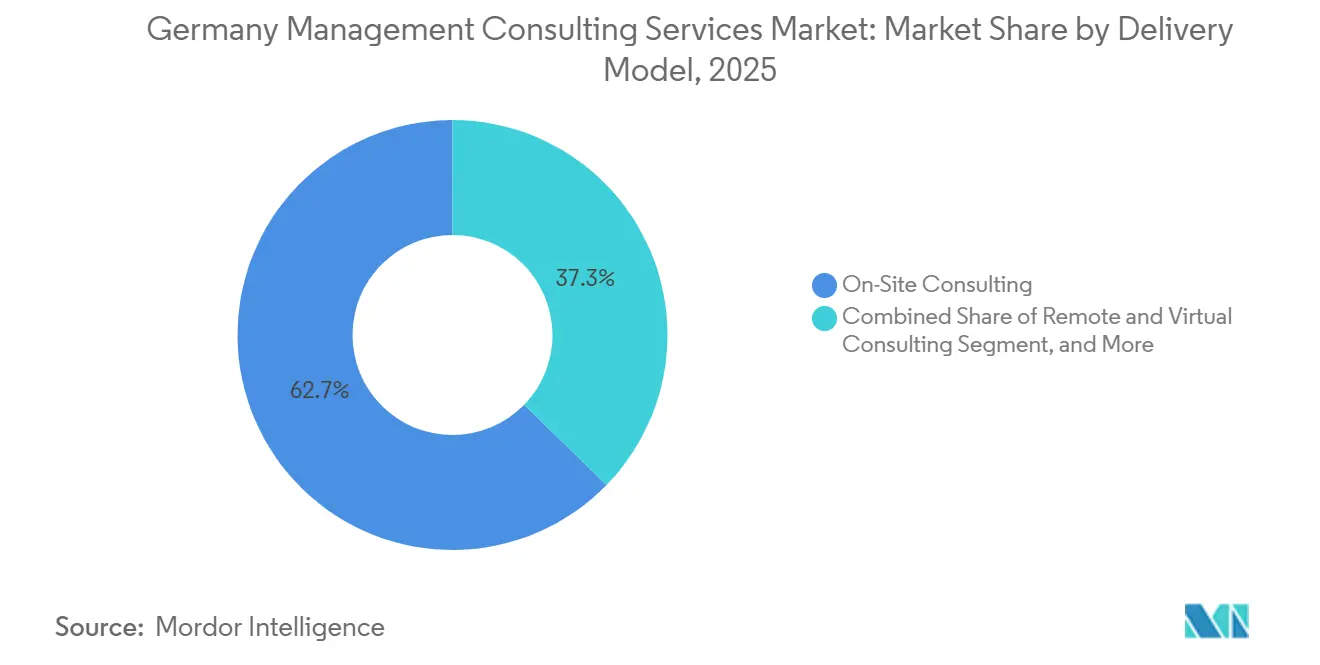

- By delivery model, on-Site Consulting retained 62.72% share of the Germany management consulting services market size in 2025, yet hybrid consulting is projected to advance at a 4.06% CAGR to 2031.

- By end user, manufacturing led with 18.13% of 2025 revenues, and energy and resources is expected to grow at a 3.98% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-Transformation Spending Boom | +1.2% | National, concentration in Baden-Württemberg, Bavaria, North Rhine-Westphalia | Medium term (2-4 years) |

| Regulatory Complexity in the EU and Germany | +0.9% | National, EU-wide spillover | Long term (≥ 4 years) |

| Post-Pandemic Cost-Optimization Focus | +0.6% | National, strongest in manufacturing and retail | Short term (≤ 2 years) |

| ESG Advisory Uptake Driven by the German Supply Chain Due Diligence Act | +0.8% | National, cross-border value chains | Medium term (2-4 years) |

| Generative AI Advisory Demand Surge | +0.7% | National, early adoption in IT, telecommunications, financial services | Short term (≤ 2 years) |

| Mittelstand Ownership Succession Wave | +0.5% | National, concentrated in southern and western Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital-Transformation Spending Boom

German companies continue to migrate core systems to SAP S/4HANA, invest in cloud infrastructure, and automate shop-floor processes. DSAG found that 68% of SAP users ranked S/4HANA migration among their top three IT priorities, with typical budgets above EUR 5 million (USD 5.65 million).[1]DSAG, “Investment Report 2026,” DSAG.de The BMWK “Digital Now” program reimbursed up to 50% of consulting fees for more than 12,000 SME applicants in 2025. Manufacturers deploying digital twins cut unplanned downtime by up to 20%, validating the return on investment that advisors use to justify multi-year programs. The EU Data Act heightens concern over vendor lock-in, so consultancies design multi-cloud strategies that preserve exit options. Although 36% of firms already run AI pilots, only 9% have scaled beyond proofs of concept, which leaves a large advisory backlog.

Regulatory Complexity in the EU and Germany

A dense stack of new rules, CSRD, DORA, the AI Act, and the Data Act, sits on top of Germany’s LkSG. BaFin’s 2026 agenda singles out ESG risk, third-party oversight, and climate stress tests, pushing banks and insurers toward external support.[2]BaFin, “Risiken im Fokus 2026,” bafin.de The Modernisierungsagenda introduces 200 procedural changes, so municipal authorities need process-redesign guidance. German insurers spend roughly 25% of operating outlays on digital upgrades but still must align with DORA incident-reporting windows. Antitrust scrutiny of digital platforms further raises demand for merger-clearance and market-definition expertise.

ESG Advisory Uptake Driven by the German Supply Chain Due Diligence Act

The LkSG obliges more than 2,900 German companies to run annual human-rights and environmental risk audits.[3]Federal Office for Economic Affairs and Export Control, “Digital Now Program Statistics 2025,” BAFA.de Average compliance costs reach EUR 1.2 million (USD 1.36 million) per midsize firm, covering supplier assessments and grievance channels. Automotive OEMs tracking cobalt provenance now deploy blockchain ledgers, raising IT-integration workloads. Anticipated EU-wide CSDDD rules may increase director liability, so boards pre-emptively strengthen governance with external help.

Generative AI Advisory Demand Surge

Consultancies themselves adopt large language models: Deloitte’s Claude AI rollout improved document productivity by 22%. Bain recorded a 25% uplift in completed tasks when teams paired human insight with AI assistance, though a Harvard and BCG study warned of a 12% error rise without proper oversight. German clients demand governance frameworks that satisfy the AI Act, bias audits, and Bundesdatenschutzgesetz rules, creating consulting workstreams around policy design and talent upskilling.[4]European Commission, “EU Data Act Fact Sheet,” ec.europa.eu

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consulting-Talent Shortage and Turnover | -0.8% | National, acute in Munich, Frankfurt, Hamburg | Short term (≤ 2 years) |

| Expansion of In-House Consulting Units | -0.6% | National, concentrated in DAX-listed firms | Medium term (2-4 years) |

| Freelance-Platform Price Compression | -0.3% | National, strongest in IT and digital transformation | Short term (≤ 2 years) |

| Client Skepticism Toward Fully Remote Engagements | -0.2% | National, sector dependent | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consulting-Talent Shortage and Turnover

Lünendonk reported that 55% of German consultancies view skills gaps as a severe growth barrier, while turnover hit 13.3% in 2021.[5]Lünendonk, “Consulting Market Study 2025,” luenendonk.de The country carried 149,000 unfilled IT roles in 2025, intensifying bidding wars for data engineers and cloud architects.[6]Bitkom, “IT-Skills Gap in Germany 2025,” bitkom.org Firms facing scarcity subcontract work or delay kick-offs, eating into margins. Retention tactics such as equity incentives and flexible schedules push personnel costs up by roughly 10% annually, squeezing profitability.

Expansion of In-House Consulting Units

Corporations like Deutsche Telekom and BASF now employ internal teams of 70 and 80-plus professionals, delivering strategy roadmaps at up to 60% lower day rates than external advisers.[7]Deutsche Telekom, “Strategy Consulting Unit Profile,” telekom.com This captive capacity moves routine digital transformation and cost-reduction work off the external market. As a result, independent consultancies must differentiate with proprietary analytics, cross-industry benchmarks, and C-suite networks to justify premium fees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Digital Transformation Commands Scale While Compliance Accelerates

Digital Transformation Consulting held 35.83% of the Germany management consulting services market share in 2025, underscoring client urgency to migrate legacy ERP, move workloads to the cloud, and embed data-driven workflows. That dominance supports a sizeable Germany management consulting services market size for tech-centric work, yet growth is moderating as enterprises finish first-wave SAP S/4HANA conversions and focus more on optimization projects. Risk and Compliance Consulting is projected to expand at a 4.19% CAGR through 2031, fueled by LkSG enforcement, EU green-taxonomy reporting, and the Digital Operational Resilience Act. Strategy Consulting retains premium pricing for M&A due diligence and portfolio realignment, but margins are under pressure from in-house teams and freelancer platforms. Operations specialists benefit from post-pandemic cost-takeout mandates, while HR advisory gains momentum as companies confront an aging workforce and acute skills gaps. Financial Advisory demand rises alongside the Mittelstand succession wave, which requires valuation, buyer search, and integration support.

Service-line boundaries continue to blur as firms embed generative AI across project phases. For example, strategy consultants now auto-synthesize market data, while compliance teams generate first-cut audit drafts in minutes. This tool convergence boosts productivity but commoditizes lower-value tasks, so providers differentiate through sector depth and proprietary analytics. Public-sector digitalization programs anchored in the Modernisierungsagenda add fresh workload for process-redesign and system-integration experts. Niche practices in sustainability and customer experience remain smaller but grow steadily by packaging ESG diagnostics with digital-commerce acceleration.

By Organization Size: Large Enterprises Dominate Spend, SMEs Grow Faster

Large Enterprises accounted for 58.69% of Germany management consulting services market share in 2025, reflecting multi-year transformation budgets, complex regulatory exposures, and steady M&A pipelines. Their robust spend maintains a sizable Germany management consulting services market size for blue-chip projects, yet captive advisory units at many DAX groups siphon off routine work. External consultants still win mandates tied to cross-border expansion, carve-outs, or crisis response where C-suite neutrality is vital.

Small and Medium-Sized Enterprises are forecast to grow at a 3.87% CAGR through 2031 as the Mittelstand succession wave accelerates. Roughly 186,000 to 215,000 firms require ownership transition by 2030, prompting valuation, tax, and integration work. Subsidies under the “Digital Now” program lower the cost barrier for SME digitalization projects, widening the client pool for mid-tier consultancies. Freelance platforms let smaller companies hire ex-MBB talent at sharply reduced day rates, but limited internal capacity often pushes them toward full-service firms that can manage change from design to execution.

By Delivery Model: Hybrid Gains Momentum

On-Site projects still captured 62.72% of 2025 revenue because manufacturing, energy, and public-sector clients value face-to-face diagnostics and stakeholder alignment. The Germany management consulting services market size for physical delivery therefore remains significant, particularly for shop-floor and war-room engagements. Yet Hybrid Consulting, combining remote analytics with periodic on-site sprints, is projected to grow at a 4.06% CAGR through 2031 as clients pursue cost discipline and consultants deploy secure collaboration suites.

Hybrid models raise consultant utilization by double digits and speed workstreams without sacrificing relationship depth. Fully Remote Consulting stays a niche because some executives doubt its effectiveness for complex change programs, especially in plants or government offices that rely on live walkthroughs. Nonetheless, AI-enabled document automation, virtual whiteboards, and immersive training reduce the number of billable travel days, pressuring traditional staffing pyramids and junior apprenticeship pathways.

By End User Industry: Manufacturing Leads, Energy Rises Fastest

Manufacturing generated 18.13% of 2025 consulting spend, anchored by automotive, machinery, and chemicals companies racing toward Industry 4.0. Plant owners invest in digital twins, predictive maintenance, and autonomous material flow to lift uptime and cut waste. This segment continues to drive large transformation roadmaps and operational-efficiency sprints.

Energy and Resources is expected to be the fastest-growing vertical at a 3.98% CAGR because the Energiewende reshapes generation portfolios, grid architecture, and hydrogen value chains. Utilities seek help with asset-rotation strategy, regulatory filings, and capital-project controls. Public-sector demand climbs as agencies digitize citizen services, while Banking and Insurance spending centers on climate-risk modeling, DORA readiness, and data-architecture upgrades. Healthcare consulting gains traction on hospital digitalization, workforce planning, and reimbursement reform tied to the Transformation Fund. Retail, logistics, and professional services round out the opportunity set with targeted projects in pricing, inventory analytics, and client-experience redesign.

Geography Analysis

Germany’s advisory spend is heavily concentrated in Baden-Württemberg, Bavaria, and North Rhine-Westphalia, which together host a majority of DAX headquarters, automotive clusters, and industrial Mittelstand champions. These three states collectively generate an outsized slice of the Germany management consulting services market size because companies there run capital-intensive transformation programs and engage advisors for global expansion. Berlin sees growing share from public-sector modernization projects linked to the federal Modernisierungsagenda and from tech startups scaling into regulated industries.

Eastern states remain under-penetrated because they house fewer large headquarters, but EU structural funds and renewable-energy investments are stimulating consulting demand around battery plants and onshore wind supply chains in Brandenburg and Saxony. Cross-border mandates frequently originate in German hubs yet extend into Asia, Africa, and South America as firms reconfigure supply networks to satisfy LkSG requirements. Cities such as Frankfurt and Hamburg lead financial-services engagements, whereas Düsseldorf and Stuttgart anchor industrial and energy portfolios.

Regional policy incentives shape niche opportunities. SME digitalization subsidies drive uptake in rural manufacturing belts, and healthcare transformation funds flow toward hospital networks across all Länder. Meanwhile, talent shortages are most acute in Munich and Frankfurt, prompting firms to establish delivery centers in secondary cities like Leipzig and Bremen to tap alternate labor pools without sacrificing client proximity.

Competitive Landscape

Germany’s management consulting arena remains fragmented, with the top four accounting firms collectively generating roughly EUR 11.66 billion (USD 13.18 billion) in domestic advisory fees during fiscal 2025 yet none topping an 8% share. Their strength in audit-adjacent risk and regulatory work keeps them central to compliance engagements, but price sensitivity and independence concerns sometimes benefit specialist boutiques. Multidisciplinary integrators such as Accenture and Capgemini are expanding manufacturing depth through recent acquisitions that bolster lean and product-lifecycle capabilities.

Strategy houses including McKinsey, BCG, Bain, and Roland Berger preserve pricing power for board-level topics, though staff shortages and client insourcing compress margins on conventional corporate-strategy projects. Simon-Kucher and Porsche Consulting thrive in high-margin niches, pricing science and automotive operations, leveraging proprietary IP and sector networks. Mid-tier firms like BearingPoint and MHP exploit demand for integrated advisory-implementation packages, especially among Mittelstand manufacturers seeking end-to-end execution help.

Technology is a key differentiator. Deloitte’s firm-wide rollout of Claude AI demonstrates how global players automate document review and analytics to improve productivity. Freelance talent platforms intensify fee pressure on standardized digital projects, while in-house units at large corporations capture routine transformation tasks. As a result, external providers concentrate on cross-industry benchmarking, complex change orchestration, and access to scarce specialist skills, especially in ESG, AI governance, and energy-system modeling.

Germany Management Consulting Services Industry Leaders

McKinsey & Company Inc. Germany

Boston Consulting Group GmbH

Roland Berger GmbH

PwC Strategy& (Germany) GmbH

Accenture GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Capgemini closed the acquisition of Piterion, adding PLM and MES expertise to strengthen smart-manufacturing delivery.

- March 2026: BCG and Inverto opened a Berlin office focusing on public-sector, procurement, and energy-transition engagements.

- January 2026: Simon-Kucher promoted 28 partners worldwide after FY 2025 revenue grew to EUR 606 million (USD 685 million).

- January 2026: BaFin issued “Risiken im Fokus 2026,” elevating ESG risk and DORA compliance on supervisory agendas.

Germany Management Consulting Services Market Report Scope

The Germany Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the projected value of the Germany management consulting services market in 2031?

The market is forecast to reach USD 29.34 billion by 2031, expanding at a 3.62% CAGR from 2026.

Which service line is expected to grow fastest through 2031?

Risk and Compliance Consulting shows the highest projected CAGR at 4.19%, reflecting rising regulatory complexity.

Why are hybrid consulting models gaining popularity?

Clients want lower travel costs and rapid access to expertise, while secure collaboration tools let consultants combine remote analytics with periodic on-site sprints.

How will the Mittelstand succession wave influence advisory demand?

Up to 215,000 ownership transitions by 2030 will sustain needs for valuation, buyer identification, and post-deal integration services.

Which end-user segment currently spends the most on external consulting?

Manufacturing leads with 18.13% of 2025 spend because of extensive Industry 4.0 retrofits and supply-chain modernization.

What competitive dynamic keeps consulting fees under pressure?

The growth of in-house advisory teams and freelancer platforms offers clients cheaper alternatives, forcing external firms to differentiate on sector depth and proprietary analytics.

Page last updated on: