France Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

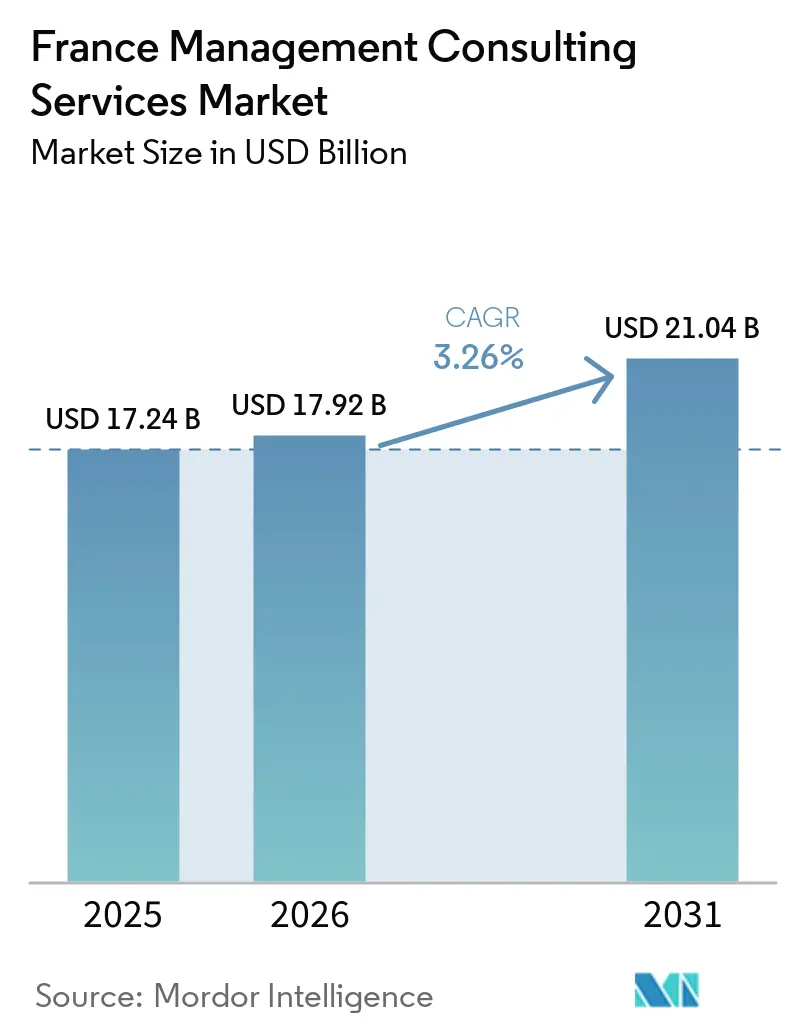

| Base Year Market Size (2025) | USD 17.24 Billion |

| Market Size (2026) | USD 17.92 Billion |

| Market Size (2031) | USD 21.04 Billion |

| Growth Rate (2026 - 2031) | 3.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Management Consulting Services Market Analysis by Mordor Intelligence

The France management consulting services market size is expected to increase from USD 17.24 billion in 2025 to USD 17.92 billion in 2026 and reach USD 21.04 billion by 2031, growing at a CAGR of 3.26% over 2026-2031. Demand is pivoting from broad diagnostic studies to short-cycle, outcome-oriented projects led by senior teams, a shift that is forcing firms to flatten staffing pyramids, codify delivery methods, and embed technology accelerators. Digital, sustainability, and regulatory needs are converging, so buyers now prioritize consultancies that combine sector depth, AI-enabled execution, and proven change-management playbooks. Competitive intensity is heightened by antitrust scrutiny of the Big Four, the rapid consolidation of France-based boutiques, and the rise of internal consulting units at large corporates. These forces intersect with chronic shortages of bilingual digital talent, fee pressure, and macro uncertainty, all of which restrain headline growth but funnel spending into high-value niches such as sovereign-cloud architecture, CSRD compliance, AI governance, and decarbonization road-mapping.

Key Report Takeaways

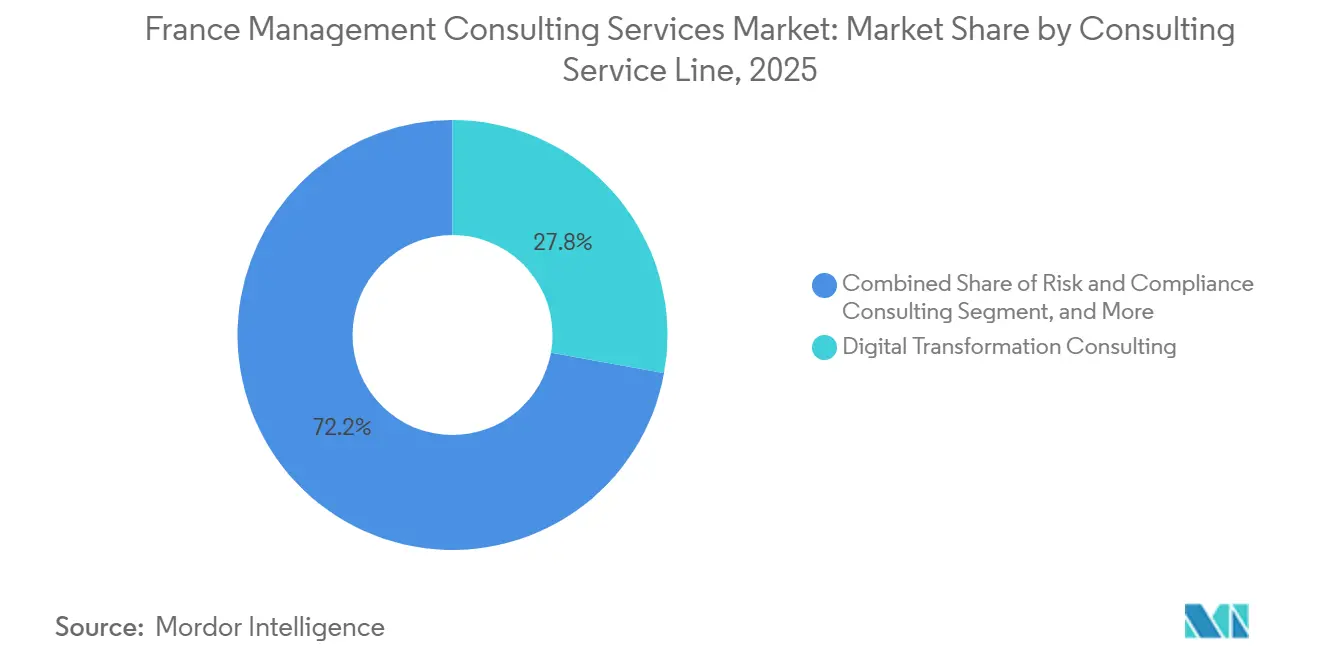

- By consulting service line, Digital Transformation Consulting led with 27.83% of France management consulting services market share in 2025, while Risk and Compliance Consulting is projected to post the fastest 3.56% CAGR through 2031.

- By organization size, large enterprises generated 63.42% of 2025 revenue, but small and medium-sized enterprises are forecast to expand at a 3.32% CAGR on the back of state-funded AI and reshoring incentives.

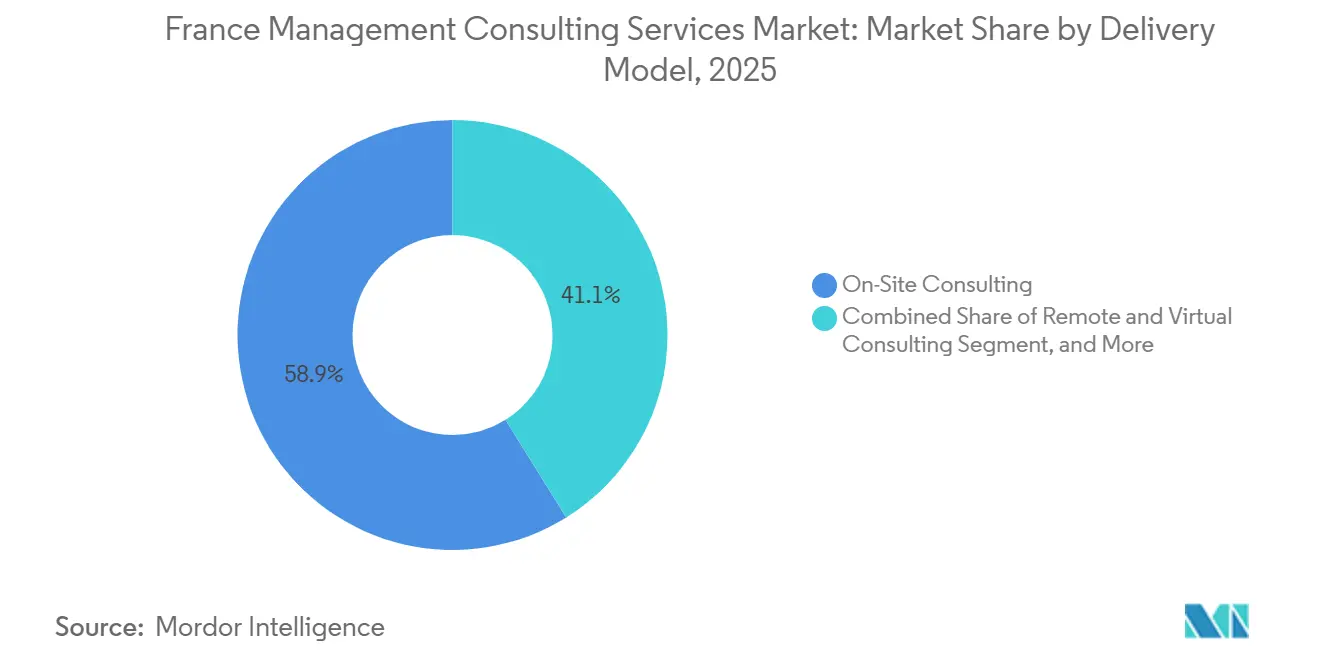

- By delivery model, on-site engagements contributed 58.87% of 2025 spend, and remote and virtual consulting is set to rise at a 3.64% CAGR as hybrid approaches balance proximity with cost control.

- By end user industry, IT and telecommunications held a 21.68% share of France management consulting services market size in 2025, whereas energy and resources is expected to grow fastest at 3.47% CAGR thanks to national decarbonization goals.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-Transformation Acceleration Across French Enterprises | +0.9% | National, major metro areas | Medium term (2-4 years) |

| Tightening EU and French Regulatory Frameworks Requiring Compliance Expertise | +0.8% | National, EU directives | Short term (≤ 2 years) |

| Surge in Sustainability and ESG Mandates | +0.7% | National, CAC 40 and ETI | Medium term (2-4 years) |

| AI-Powered Productivity Mandates Driving Advisory for Knowledge Automation | +0.5% | National, early adopters in finance, IT, manufacturing | Medium term (2-4 years) |

| Generational Succession Among Entreprises de Taille Intermédiaire | +0.3% | National, 75% outside Paris | Long term (≥ 4 years) |

| Government Incentives for Industrial Reshoring and Decarbonization Advisory | +0.4% | Key industrial regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital-Transformation Acceleration Across French Enterprises

French companies are condensing multiyear digital road maps into 18-month sprints, propelled by EUR 10 billion (USD 11.3 billion) of Bpifrance funding that subsidizes AI diagnostics and consulting for hundreds of SMEs each year.[1]Bpifrance, “Bpifrance deploys €10 billion to develop the AI ecosystem,” bpifrance.com Recent flagship programs, such as Pierre Fabre’s six-month multi-cloud migration with Atos, illustrate the client expectation that consultants will co-deploy solutions, not merely deliver recommendations. Deloitte reports that two-thirds of French firms now record measurable productivity gains from AI, yet only one-fifth translate those gains into revenue, creating white-space for consulting support that links efficiency to topline growth. Rapid scaling intensifies demand for talent, governance frameworks, and agile change-management methods that ensure new digital capabilities embed into day-to-day operations.

Tightening EU and French Regulatory Frameworks Requiring Compliance Expertise

Overlapping mandates such as CSRD, CSDDD, the AI Act, and NIS2 create as much as 60% indicator duplication, inflating compliance workloads beyond internal capacity.[2]Kennedys, “Regulatory evolution in Europe,” kennedyslaw.com France plans stricter thresholds than Brussels on pay-transparency reporting, with penalties up to 1% of payroll for non-compliance. Firms therefore outsource data mapping, unified governance platforms, and cross-regulation process design to consultancies able to orchestrate legal, technology, and change expertise. Until the European Commission’s simplification package takes effect, regulatory advisory remains a non-discretionary growth engine.

Surge in Sustainability and ESG Mandates

Sustainability has become a strategic buying criterion, not a branding exercise. Ninety-three percent of French consultancies cut mission-related emissions in 2025, and 60% now market dedicated ESG offerings. The CSRD’s assurance requirement fuels demand for ESG analytics and audit-readiness services, while France’s Anti-Fast Fashion Law forces textile clients to seek advice on supply-chain transparency and eco-labeling.[3]Kennedys, “Regulatory evolution in Europe,” kennedyslaw.com Concurrent litigation, La Poste, TotalEnergies, and EDF have all faced duty-of-vigilance suits, raises the financial stakes, favoring consultancies that integrate ESG with risk, valuation, and investor-relations support.

AI-Powered Productivity Mandates Driving Advisory for Knowledge Automation

Generative AI adoption surged in 2025: 60% of large firms instituted company-wide governance bodies, and 86% published responsible-AI charters. Marketing leads the pack, but other functions remain exploratory, so consultants coach clients on value-case selection, human-machine role design, and ROI tracking. Accenture’s alliance with Mistral AI showcases sovereign-cloud positioning that eases data-residency concerns and aligns with France’s SecNumCloud doctrine. Advisory demand now clusters around AI governance, workforce upskilling, and secure platform selection that balances performance with European compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Fee Pressure From Big Four and Global Giants | -0.6% | National, all sectors | Short term (≤ 2 years) |

| Expansion of Internal Consulting Capabilities at Large French Corporates | -0.4% | CAC 40, financial groups | Medium term (2-4 years) |

| Scarcity of Bilingual Digital Consulting Talent | -0.3% | Île-de-France, major tech hubs | Medium term (2-4 years) |

| Data-Sovereignty Barriers Limiting Cloud-Based Consulting Delivery | -0.2% | Public sector, regulated industries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Fee Pressure From Big Four and Global Giants

The Big Four are cutting structural costs to underwrite aggressive pricing. KPMG moved more than 200 partners into an independent-contractor vehicle, saving an estimated EUR 18 million (USD 20.3 million) in social charges and redeploying the savings to defend rates.[4]La Lettre A, “Les Big Four en plein repositionnement,” lalettre.fr Public buyers are also capping Big-Four dominance, as illustrated by the government’s recent exclusion of EY and Deloitte from a EUR 30 million (USD 33 million) anti-corruption compliance tender, thereby intensifying competition for private-sector work. Mid-tier firms must industrialize repeatable offerings without diluting bespoke expertise, or risk margin squeeze.

Expansion of Internal Consulting Capabilities at Large French Corporates

BNP Paribas now fields a 700-person consulting and transformation network, and Renault’s internal unit delivers around 40 missions yearly with 30 consultant.[5]BNP Paribas, “Consulting and Transformation,” bnpparibas.com, AFCI, “Renault Group,” afci-conseilinterne.fr These captive teams handle routine transformation and operational excellence, shrinking external addressable spend. External firms therefore focus on cross-border M&A integration, sovereign-cloud architecture, or AI governance-areas in which internal teams lack scale or regulatory reach. The talent war escalates because internal units recruit from the same elite schools that supply traditional consultancies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Compliance and Digital Lead Divergent Growth Paths

Digital Transformation Consulting accounted for the largest France management consulting services market share at 27.83% in 2025, reflecting sustained enterprise spend on cloud migration, data platforms, and AI scaling. Risk and Compliance Consulting, however, is projected to outpace all other lines at a 3.56% CAGR through 2031 as overlapping EU mandates and litigation risk drive non-discretionary demand. Strategy Consulting growth stalled in 2024 because political uncertainty delayed transformational bets, whereas operations work held firm thanks to lean-manufacturing and supply-chain resilience projects aligned with reshoring incentives. HR Consulting is benefiting from nationwide reskilling programs funded under France 2030, and Financial Advisory is stabilizing as cross-border M&A confidence returns.

Market momentum shows a structural bifurcation. Digital projects now shift from experimentation to industrial-scale governance, while compliance engagements become continuous programs embedded in enterprise risk architectures. Integrated offerings like KPMG Strategy’s AI-enabled transaction support position firms to capture advisory that straddles growth, M&A, and execution. Conversely, pure-play strategy boutiques must either specialize deeply or partner for implementation capacity to stay relevant in the evolving France management consulting services market.

By Organization Size: SME Transformation Unlocks Mid-Market Opportunity

Large enterprises generated 63.42% of total spend in 2025, yet SME budgets are projected to grow faster at 3.32% CAGR as state-backed AI and reshoring finance lower capital hurdles. Bpifrance’s AI Booster has already supported more than 600 SMEs with diagnostics and coaching, signaling a pipeline of mid-market transformation projects. France’s Green Industry Law, which halves environmental-permit timelines and allocates EUR 1 billion (USD 1.13 billion) to turnkey industrial sites, further stimulates advisory demand among regional manufacturers.

The France management consulting services market size for SME projects remains smaller than the corporate segment, but competition is thinner and engagements often involve end-to-end implementation, enabling consultancies to capture higher relative margins. The main challenge is packaging offerings at price points acceptable to family-owned ETI, many of which face leadership succession. Firms that blend modular digital tools with hands-on operational support will secure repeat business and long-term retention across this underserved client base.

By Delivery Model: Hybrid Consulting Balances Proximity and Efficiency

On-site work retained 58.87% share in 2025 because complex transformations still rely on in-person stakeholder alignment and change management. Remote and virtual engagements, however, are forecast to rise at 3.64% CAGR, reflecting client comfort with distributed delivery and the cost benefits of reduced travel. A hybrid model, combining critical in-person workshops with remote analytics and execution, has emerged as the dominant delivery paradigm in the France management consulting services market.

Consultancies are investing in secure collaboration platforms and AI-assisted drafting tools to maintain quality and speed while reducing physical presence. Strategy and financial-advisory mandates remain largely on-site due to confidentiality, whereas digital and HR projects migrate to hybrid structures. The France management consulting services industry increasingly judges firms on their ability to deploy senior resources efficiently across channels without sacrificing intimacy or responsiveness.

By End User Industry: Energy Transition and Financial Regulation Drive Sectoral Demand

IT and telecommunications led France management consulting services market size with a 21.68% slice in 2025, fueled by 5G rollout, cybersecurity, and cloud-sovereignty design. Energy and resources is expected to clock the fastest 3.47% CAGR through 2031 as France pursues net-zero, accelerates renewable mega-projects, and localizes critical supply chains. Banking and insurance continues to purchase advisory for DORA, NIS2, and AI adoption, while manufacturing spend is tied to Industry 4.0 and reshoring feasibility.

Healthcare and public sector engagements are growing around digital-health doctrine alignment and citizen-centric service redesign. Regulation is the common thread: industries facing stringent reporting or security obligations show steady, non-cyclical demand, whereas discretionary sectors temper spending when macro signals darken. Consultants able to triangulate technology, regulation, and operational know-how will win cross-industry programs that define the next growth wave for the France management consulting services market.

Geography Analysis

Île-de-France anchors demand, supplying roughly 30% of national GDP and hosting most CAC 40 headquarters, which rely heavily on external consultants for strategy, transactions, and regulatory readiness. Yet 75% of France’s 5,400 Entreprises de Taille Intermédiaire sit outside Paris, especially in Auvergne-Rhône-Alpes, Hauts-de-France, and Nouvelle-Aquitaine. These territories attract consulting assignments linked to industrial reshoring, succession planning, and operational excellence. Regional boutiques leverage local relationships and cost structures, while national firms staff satellite offices to capture mid-market opportunities.

France’s digital-sovereignty doctrine adds a spatial dimension. SecNumCloud certification steers sensitive workloads toward French-operated data centers, prompting advisory on hybrid architectures that pair U.S. hyperscaler tech with domestic control. Providers like S3NS and Bleu illustrate localization partnerships that demand nuanced vendor-selection, risk-assessment, and compliance consulting. Deloitte, Alcimed, and other firms have launched sovereignty practices to guide clients through cloud-residency and data-classification decisions.

Cross-border EU regulations, including CBAM and the Net-Zero Industry Act, further shape geographic demand. Companies in border regions must redesign supply chains to minimize carbon-border taxes, while renewable-project developers optimize tenders using non-price scoring criteria. Consultancies offering pan-European insight gain competitive advantage, particularly when they can deploy bilingual teams fluent in both Brussels policy and French market specifics.

Competitive Landscape

Competition is intense yet fragmented. The Big Four and global giants such as Accenture, McKinsey, BCG, and Bain vie with French independents like Wavestone, Sia Partners, and Eurogroup Consulting. Big Four firms are spinning off audit arms and bulking up legal, restructuring, and data capabilities to escape regulatory headwinds and margin erosion. KPMG’s 150-strong KPMG Strategy unit and Accenture’s acquisition of Orlade’s 200-person capital-projects team highlight capability bundling that blurs lines between traditional service silos.

Boutiques respond through specialization and consolidation. Willing tripled its Lille presence by buying Groupe Altera, while Kea and Partners doubled revenue after integrating Ylios. Sector specialists such as Ailancy Advisory flourish by offering pure-play financial-services transformation free of audit conflicts. Internal consulting arms at BNP Paribas and Renault divert routine transformation work from external suppliers, nudging the market toward complex, high-stakes engagements only external experts can tackle.

Technology partnerships are now decisive. Accenture’s sovereign-AI alliance with Mistral AI, Analysis Group’s link-up with Ricol Lasteyrie, and Deloitte’s cloud-sovereignty initiatives show how firms differentiate through IP ownership, data hosting models, and multidisciplinary teams. Regulatory probes, like January 2026 dawn raids on sustainability-audit collusion, may ultimately redistribute market share toward mid-tier and ESG-focused specialists.

France Management Consulting Services Industry Leaders

Accenture plc

Capgemini SE

Deloitte SAS

PricewaterhouseCoopers Advisory SAS

Ernst and Young Advisory France SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Accenture acquired Orlade, adding 200 capital-project specialists in energy, rail, and defense.

- March 2026: KPMG France launched the 150-expert KPMG Strategy practice to fuse growth, M&A, and AI capabilities.

- March 2026: Andersen Consulting expanded via a collaboration with cloud-engineering firm Teolia Consulting.

- March 2026: PMP Strategy appointed three new associate partners to bolster telecom, media, and tech coverage.

France Management Consulting Services Market Report Scope

The France Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

How large is the France management consulting services market in 2026?

The market is projected to reach USD 17.92 billion in 2026, on its way to USD 21.04 billion by 2031.

Which service line is growing the fastest?

Risk and Compliance Consulting is forecast to lead growth at a 3.56% CAGR through 2031 as overlapping EU mandates expand compliance workloads.

What delivery model will gain the most share?

Remote and virtual engagements are expected to rise the quickest, advancing at a 3.64% CAGR as hybrid delivery becomes the norm.

Why are SMEs becoming an attractive client segment?

Government-funded AI programs and industrial reshoring incentives lower investment barriers, enabling SMEs to undertake digital and operational transformations.

How are internal consulting units affecting external providers?

Captive teams at large corporates undertake routine transformation tasks, prompting external consultancies to specialize in complex, high-stakes projects requiring niche expertise.

Which industry vertical is likely to drive future consulting demand?

Energy and resources is positioned for the fastest expansion, buoyed by aggressive decarbonization targets and renewable-project pipelines.

Page last updated on: