Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

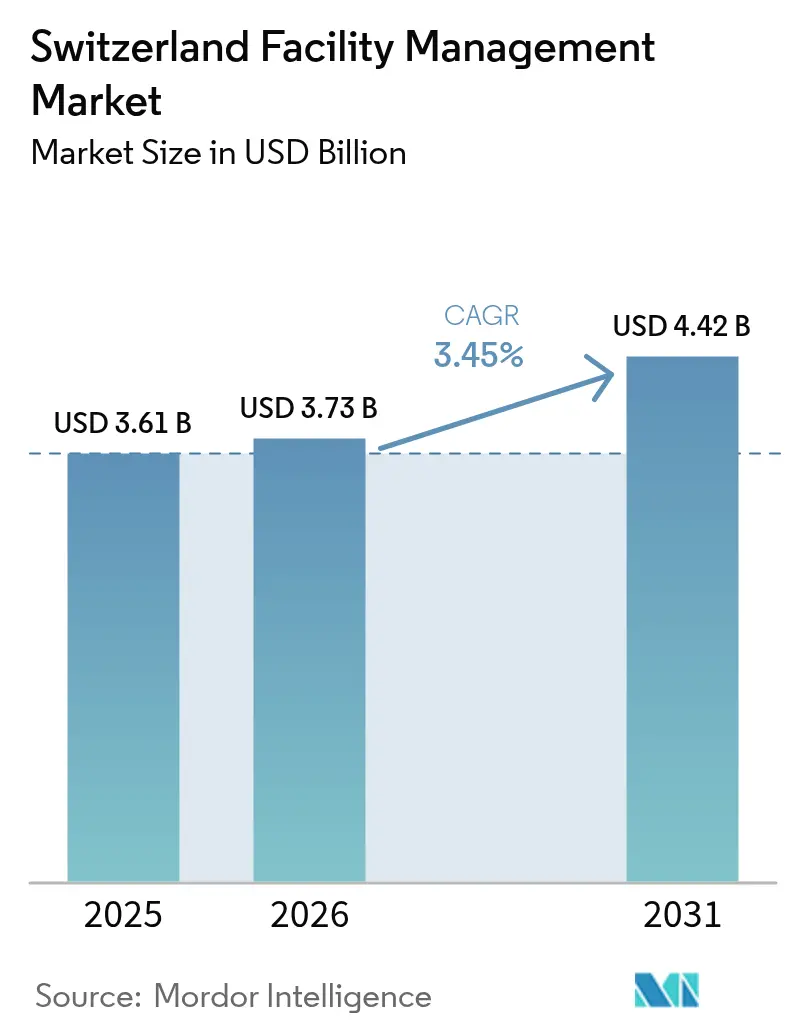

| Base Year Market Size (2025) | USD 3.61 Billion |

| Market Size (2026) | USD 3.73 Billion |

| Market Size (2031) | USD 4.42 Billion |

| Growth Rate (2026 - 2031) | 3.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Facility Management Market Analysis by Mordor Intelligence

The Switzerland facility management market size is expected to grow from USD 3.61 billion in 2025 to USD 3.73 billion in 2026 and is forecast to reach USD 4.42 billion by 2031 at 3.45% CAGR over 2026-2031. Steady GDP expansion, structural labour scarcity, rising automation and stringent ESG mandates are combining to create a resilient facility management market that rewards providers able to blend technical depth with data-driven service models. Hard Services currently dominate revenue because sophisticated building systems demand specialised maintenance, yet Soft Services are expanding faster as hybrid work elevates occupant-experience priorities. Outsourcing remains the preferred operating model; the 66.21% outsourced share in 2024 underlines how clients seek flexibility, scale and regulatory know-how that are hard to replicate in-house. Consolidation among international and domestic leaders is accelerating as the capital required for IoT roll-outs, predictive algorithms and ESG reporting outpaces the capacity of smaller regional firms. Against this backdrop the facility management market is steadily transitioning from labour-intensive contracts toward outcome-based agreements where energy, carbon and space-efficiency targets drive premium pricing.

Key Report Takeaways

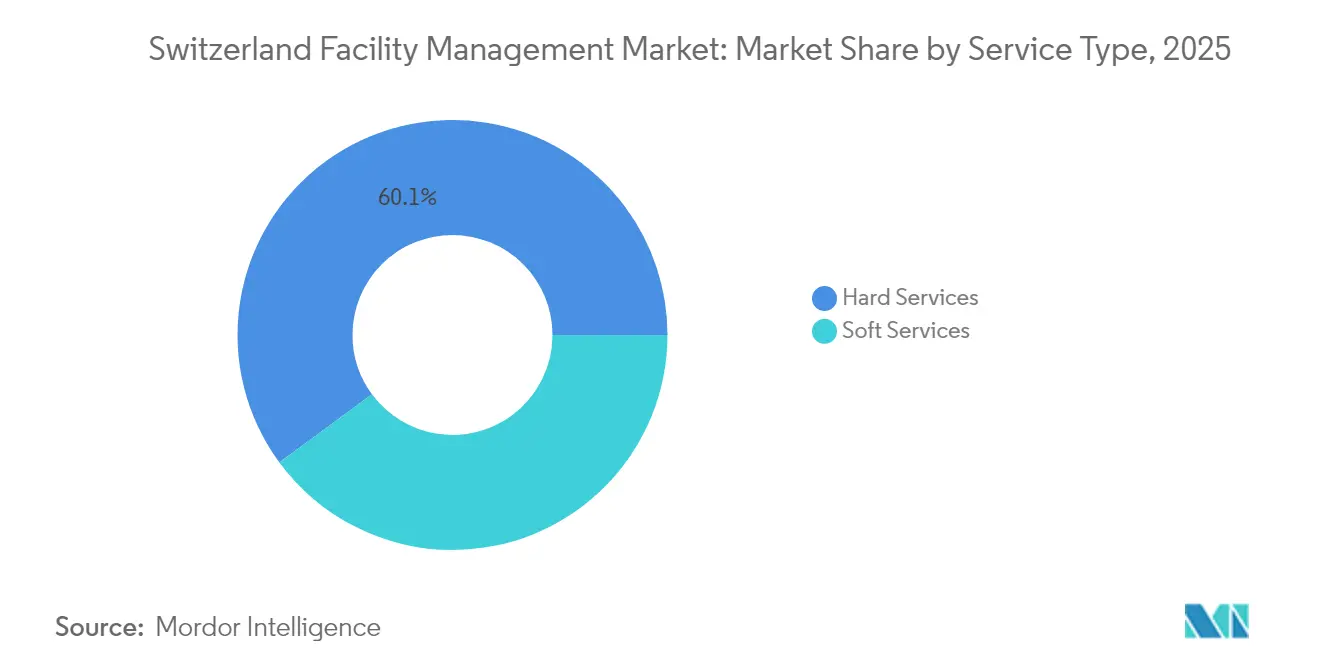

- By service type, Hard Services led with 60.10% revenue share in 2025, whereas Soft Services are projected to advance at a 3.88% CAGR through 2031.

- By offering, the outsourced model held 65.70% of the facility management market share in 2025 and is tracking a 3.62% CAGR to 2031.

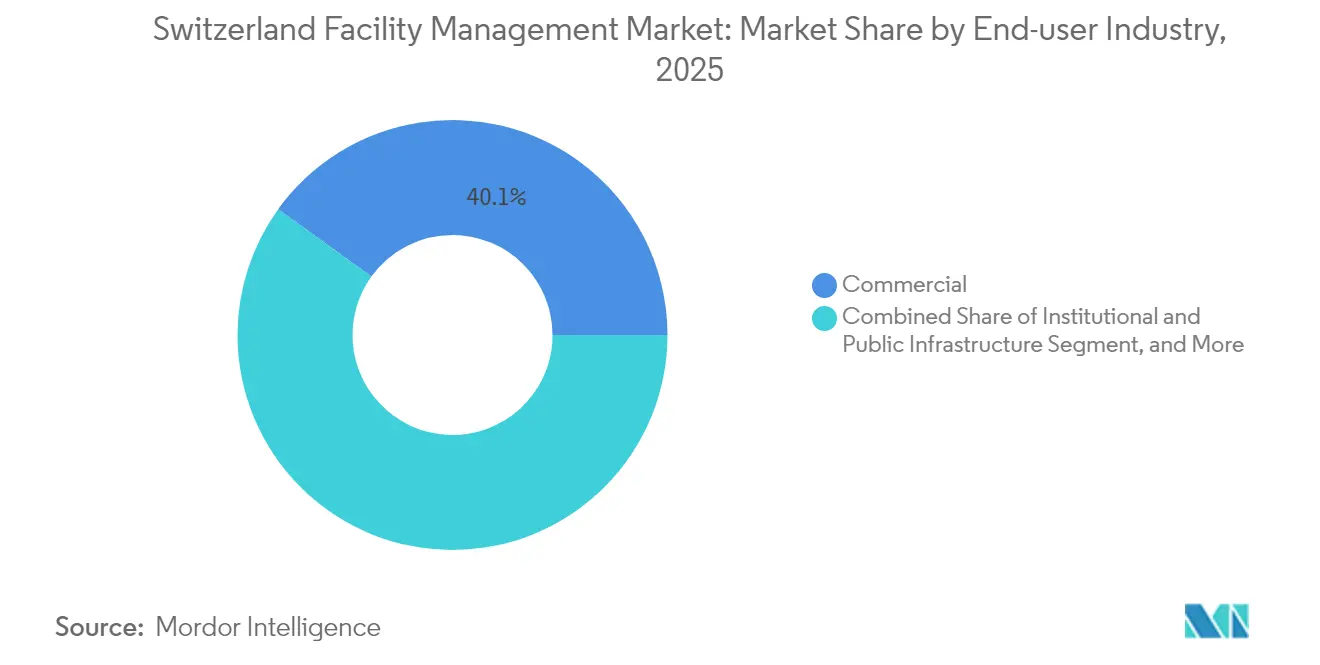

- By end-user industry, Commercial facilities commanded 40.05% of the facility management market size in 2025 while Institutional & Public Infrastructure is forecast to expand fastest at 3.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid Work Reshaping Space Utilization | +0.8% | National; Zurich, Geneva, Basel | Short term (≤ 2 years) |

| Value-Added Services Driving Margins | +0.6% | National; commercial hubs | Medium term (2-4 years) |

| Talent Shortage Driving Automation | +0.9% | National; acute in healthcare & IT | Long term (≥ 4 years) |

| Smart City Integration | +0.5% | Zurich, Geneva, Basel metros | Medium term (2-4 years) |

| ESG Regulations Accelerating Green Facilities | +0.7% | National; stricter in urban cantons | Long term (≥ 4 years) |

| Government Grants for Smart Building Retrofits | +0.4% | National; public infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hybrid Work Reshaping Space Utilization

Swiss occupiers are embedding three-day office schedules, with 64% planning workforce growth but only 16% expecting to lease more space, signalling a decisive pivot toward desk-sharing and space-on-demand strategies[1]JLL Research, “Decoding the Return-to-Office Puzzle in Switzerland,” JLL, jll.com. Flex-office supply in Zurich rose from 19 to 50 locations between 2019 and 2024, swelling usable space from 28,000 m² to 75,000 m² and underscoring the appetite for agile footprints[2]JLL Research, “Flex Offices in Switzerland – Here to Stay?,” JLL, jll.com. Only 27% of firms now envisage one-desk-per-employee layouts, down sharply from two-thirds in 2019, which pushes facility managers to master dynamic occupancy analytics. As collaborative zones eclipse conventional cubicles, demand intensifies for building-management platforms that automatically tune lighting, HVAC and air-quality to real-time head-counts. Clients value in-person collaboration over simple cost relief, so providers must deliver high-comfort shared environments rather than pure densification plays.

Value-Added Services Driving Margins

Mature Swiss occupiers increasingly benchmark service providers on employee wellness, hospitality and workplace-experience metrics, lifting demand for bundled concierge, food and smart-cleaning offerings that carry richer margins than standard maintenance. In premium commercial hubs, corporates contract for biophilic design upgrades and sensor-based indoor-air optimisation to support talent attraction. Facility managers able to integrate catering, security and reception under integrated FM contracts are winning longer tenures and performance-linked fee escalators. The trend mirrors the premium employers place on health, safety and ESG transparency, creating upsell pathways into consulting on carbon accounting, WELL certification and waste-segregation protocols. As a result, pure-play technical providers are broadening portfolios or partnering with hospitality specialists to defend share.

Talent Shortage Driving Automation

Switzerland’s unemployment rate fell to 2% in late 2024 while vacancies surpassed 120,000, signalling structural labour scarcity that is acute in facilities and healthcare services. By 2040 the economy could face a manpower gap of 430,000, prompting FM firms to mechanise repetitive tasks and adopt AI-backed scheduling that lifts worker productivity. Automation potential varies: agricultural and forestry FM tasks carry a 76% likelihood whereas health-sector routines sit below 20%, guiding selective robotics deployment. Schindler Switzerland’s “Liftcamps,” which retrain career-changers as elevator technicians, illustrate creative responses to talent scarcity. With labour costs already averaging CHF 63.62 per hour, providers see automation not as workforce replacement but as augmentation that keeps margins viable.[3]Federal Statistical Office, “Labour Costs,” bfs.admin.ch

ESG Regulations Accelerating Green Facilities

The Climate and Innovation Act obliges Switzerland to reach net-zero by 2050, unlocking a USD 20 billion retrofit market for energy-efficiency services. Mandatory TCFD reporting from January 2024 compels firms to publish granular climate-risk data, so FM partners are now core to measurement and disclosure workflows. Buildings account for 45% of national energy use and one-third of emissions; IoT-enabled heating optimisation already trims 10-20% of carbon in more than 700 Swiss buildings, with plans for 25,000 additional sensors[4]Swisscom Corporate News, “Cutting Costs and Carbon Emissions for Buildings Using Artificial Intelligence,” swisscom.ch. Green-compliant assets attract rental premiums; 85% of investors report higher valuations for ESG-aligned facilities, intensifying demand for providers who can verify performance. FM companies with carbon-analytics platforms thus convert regulation into competitive advantage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Operating Costs: Premium Market Pressures | -0.5% | National; Zurich & Geneva | Short term (≤ 2 years) |

| Fragmented Market Structure: Integration Challenges | -0.3% | National; rural cantons | Medium term (2-4 years) |

| Stringent Compliance and Certification Costs | -0.4% | National; urban areas | Long term (≥ 4 years) |

| Limited Flexibility in Long-term Real Estate Contracts | -0.2% | National; commercial sector | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Operating Costs: Premium Market Pressures

At CHF 63.62 per hour, Swiss labour is among the world’s priciest, squeezing FM margins and disadvantaging small local firms unable to scale[5]Federal Statistical Office, “Labour Costs,” bfs.admin.ch. A policy-rate cut to 0.25% in March 2025 stimulates real-estate demand but forces FM suppliers to recalibrate services as occupancy swings more rapidly. New lease rents rose 1.8% in Q1 2025 against a 1.08% vacancy low, driving more frequent contract renegotiations and pass-through clauses. Simultaneously, ESG reporting adds monitoring and certification costs that erode small-provider profitability. The cumulative burden propels consolidation as scale economies in technology and procurement become decisive.

Fragmented Market Structure: Integration Challenges

Switzerland’s 26 cantons enforce distinct real-estate and labour rules, obliging FM vendors to customise processes and digital tools for each jurisdiction[6]Switzerland Global Enterprise, “Cantonal Business Development,” s-ge.com. Language segmentation across German, French and Italian regions elevates training spend and undermines standardised delivery. Healthcare FM illustrates the difficulty: cantonal hospital systems stipulate divergent hygiene and data-protection standards that impede nationwide roll-outs. Divergent BMS protocols also limit IoT-sensor interoperability, complicating predictive-maintenance deployments. As a result, national efficiency programs progress slowly, and smaller cantonal players struggle to integrate into wider digital ecosystems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Remain Dominant Amid Infrastructure Sophistication

Hard Services accounted for 60.10% revenue in 2025, highlighting the critical role of technical maintenance in a country where building systems are highly automated and heavily regulated. The segment benefits from mandatory periodic inspections of fire safety, elevators and HVAC that secure recurrent revenue, while Switzerland’s alpine climate drives demand for high-spec heating and ventilation solutions. Asset-management subservices are scaling rapidly as IoT deployment accelerates; Siemens alone installed more than 7,000 sensors across Kantonsspital Baden, an illustration of sensor density now expected in critical facilities. Predictive maintenance platforms improve uptime and compliance, allowing FM providers to tie fees to KPI outcomes. Despite dominance, Hard Services growth trails Soft Services because many technical tasks are maturing toward price competition.

Soft Services are forecast to grow at a 3.88% CAGR to 2031, reflecting heightened emphasis on employee experience in hybrid workplaces. Cleaning protocols evolved during the pandemic into sensor-triggered, needs-based regimes that optimise labour and hygiene simultaneously. Catering and vending services integrate nutritional analytics and cashless payments, elevating perceived value. Security has shifted to cloud-enabled access control and video analytics, embedding FM into corporate risk management. As a result, Soft-Service contracts increasingly bundle hospitality and wellbeing solutions that command premium rates. Providers that combine data-driven space services with traditional soft capabilities are poised to outpace purely technical competitors.

By Offering Type: Outsourcing Builds Scale As Complexity Rises

The outsourced model represented 65.70% of total spend in 2025 and is set to compound at 3.62% annually to 2031, underscoring client preference for specialised expertise amid tightening labour supply. Integrated FM offerings bundle hard and soft tasks under unified KPIs, simplifying vendor oversight for multinationals and public entities. Outsourcers leverage scale to attract scarce technicians, invest in AI-based maintenance and absorb compliance risk. The facility management market size attached to integrated contracts is expanding fastest, particularly in healthcare where hospital EBITDA pressure demands holistic optimisation. Bundled FM also suits mid-market clients needing a single point of accountability yet unwilling to relinquish strategic control of core assets.

In-house management retained 34.30% share in 2025 but faces strain. Corporates must fund technology upgrades, maintain talent pipelines and reconcile ESG reporting in addition to core business priorities. Nonetheless, in-house teams persist in defence, energy and high-tech manufacturing where security or process integration outweigh outsourcing efficiencies. Some firms operate hybrid models, outsourcing technical tasks while keeping strategic space planning internal. Over the forecast, continued skills shortages and IoT capex will tip incremental volumes toward specialised providers.

By End-user Industry: Commercial Leads but Institutional Pipelines Surge

Commercial real estate-including banking offices, data centres and retail-held 40.05% of 2025 revenue. Financial-services anchors in Zurich and Geneva demand 24/7 uptime, cyber-secure BMS and WELL-certified workplaces. Data-centre FM requires advanced cooling optimisation; technology and hyperscale clients drove a 16% jump in CBRE’s Swiss FM revenue for Q1 2025. However hybrid work dampens net office take-up, compelling FM firms to pivot toward experience-centric amenities rather than pure space growth.

Institutional and Public Infrastructure is the fastest-growing vertical, projected at a 3.66% CAGR through 2031. Smart city grants, hospital modernisation and decarbonisation mandates create long contract visibility. Zurich earmarks CHF 1.25 million annually for smart-city trials, channelling work to FM specialists versed in IoT and open-data integration. Hospitals seek FM partners to lift EBITDA margins from the current 2.7% to sustainable levels by automating logistics and energy use. Transport and e-mobility networks likewise need high-availability maintenance that blends civil, electrical and digital skills, further enlarging outsourced pipelines.

Geography Analysis

Switzerland’s facility management demand is concentrated in metropolitan cantons where dense corporate footprints, advanced infrastructure and progressive regulation coalesce. Zurich leads spending owing to its role as a financial nucleus and first-mover on smart-city initiatives that aim to accommodate 25% population growth by 2030 through data-driven urban services. Premium landlords require continuous uptime, LEED & WELL certifications and high-spec security, sustaining price premiums for integrated FM contracts. Geneva follows, shaped by UN agencies, NGOs and multinational commodity firms whose stringent security and protocol standards raise service complexity. The city’s fully electric TOSA bus system pushes demand for specialists who can integrate vehicle-charging, depot maintenance and energy-management solutions.

Basel’s life-science cluster creates niche FM needs around cleanrooms, hazardous-waste handling and GMP compliance, generating steady high-margin opportunities. Eastern Switzerland (St. Gallen, Appenzell) shows rising adoption of outsourced FM as mid-sized manufacturing plants modernise to meet carbon targets. The Espace Mittelland, anchored by Bern, delivers reliable public-sector demand but lower margin potential because tender rules favour price-competitive bids. Ticino’s bilingual context calls for suppliers fluent in Italian legal and cultural frameworks, erecting soft barriers to entry for international players. Rural cantons remain fragmented; limited economies of scale deter large FM entrants, yet pilot smart-village schemes in Dietikon and Wädenswil signal long-term growth as IoT hardware becomes cheaper. Collectively these regional nuances necessitate flexible operating models that balance national standards with local compliance and language adaptation.

Competitive Landscape

The Switzerland facility management market is moderately fragmented but trending toward consolidation as capital-intensive digitalisation raises entry thresholds. ISS’s acquisition of gammaRenax in May 2024 brought 1,800 staff and 1,600 sites under its umbrella, strengthening its national footprint and proprietary FM Academy talent funnel. CBRE deepened global reach by purchasing Industrious, creating a Building Operations & Experience segment with USD 20 billion revenue that can cross-sell flexible workspace and integrated FM to Swiss multinationals. Siemens, Bouygues-Equans and SPIE focus on technical niches, leveraging engineering heritage to win high-spec hospital, energy and data-centre projects; Siemens’ 7,000-sensor hospital deployment epitomises technology-led differentiation.

Regional champions such as Wincasa and Dussmann protect share through local market intimacy and language agility. Wincasa’s new Target Operating Model establishes 26 walk-in centres, signaling a human-centric strategy to counter purely digital entrants. Dussmann recorded EUR 3 billion sales in 2023 and is rolling out a “Road to 2030” plan that emphasises bundled services and energy performance contracting. Meanwhile Equans Switzerland emerged from Bouygues E&S’ merger with Engie’s service arm, adding scale across building-life-cycle offerings from design to maintenance. Technology pure-plays delivering AI-driven energy analytics increasingly challenge incumbents on single-solution bids, nudging traditional players to invest or partner.

Strategic moves centre on IoT roll-outs, sustainability consulting and outcome-based pricing that ties revenue to energy-savings or uptime guarantees. Providers also expand academies and apprenticeship schemes to mitigate labour scarcity. As the top five players’ combined revenue roughly equals 45% of national spend, the market still offers room for niche specialists yet shows clear drift toward a more consolidated structure.

Switzerland Facility Management Industry Leaders

Honegger AG

Swiss FM AG

Livit FM Services Ltd.

PHM Group

SPIE Switzerland

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: CBRE reported a 16% rise in facilities-management net revenue for Q1 2025, driven by technology, healthcare and hyperscale data-centre clients.

- January 2025: Bouygues E&S and Equans completed their merger, establishing Equans Switzerland with a focus on facility management, energy supply and digitalisation across 100 Swiss locations.

- January 2025: CBRE Group acquired Industrious National Management Company, forming a Building Operations & Experience segment projected to generate USD 20 billion revenue and enhance global workplace-experience capabilities.

- January 2025: Dussmann Group surpassed EUR 3 billion sales in 2023, a 9.0% uplift, and launched its “Road to 2030” service-expansion strategy.

- December 2024: Compass Group recorded 10.6% organic revenue growth in 2024, highlighting first-time outsourcing and targeted support services within a USD 320 billion addressable market.

Switzerland Facility Management Market Report Scope

Facility Management refers to a range of services and disciplines provided by a separate department or a professional organization to ensure the functionality, efficiency, and safety comfort of the built environment, such as buildings, infrastructure, or an organization. The study offers a comprehensive analysis of Switzerland's facility management market segmented by type of service, type of offerings, and end-user industry.

The Switzerland facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current size of the Switzerland facility management market?

The facility management market size is USD 3.73 billion in 2026 and is projected to reach USD 4.42 billion by 2031.

Which facility management service type generates the highest revenue?

Hard Services dominate with 60.10% of 2025 revenue, driven by technical-infrastructure complexity.

Why is outsourcing growing faster than in-house facility management?

Acute labour shortages, escalating compliance costs and the need for IoT investment are pushing organisations toward specialised outsourced providers that deliver integrated solutions at scale.

Which end-user segment is expanding most rapidly?

Institutional and Public Infrastructure is forecast to grow at 3.66% CAGR through 2031, propelled by smart-city programs and healthcare modernisation.

How are ESG regulations affecting Swiss facility management providers?

Net-zero mandates and mandatory climate-risk disclosure boost demand for energy-efficiency retrofits and data-driven monitoring, favouring providers with advanced sustainability expertise.

What technological trends are redefining Swiss facility management contracts?

IoT sensors, predictive maintenance algorithms and outcome-based agreements that guarantee energy or carbon performance are transforming service delivery and pricing models.

Page last updated on: