Germany Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

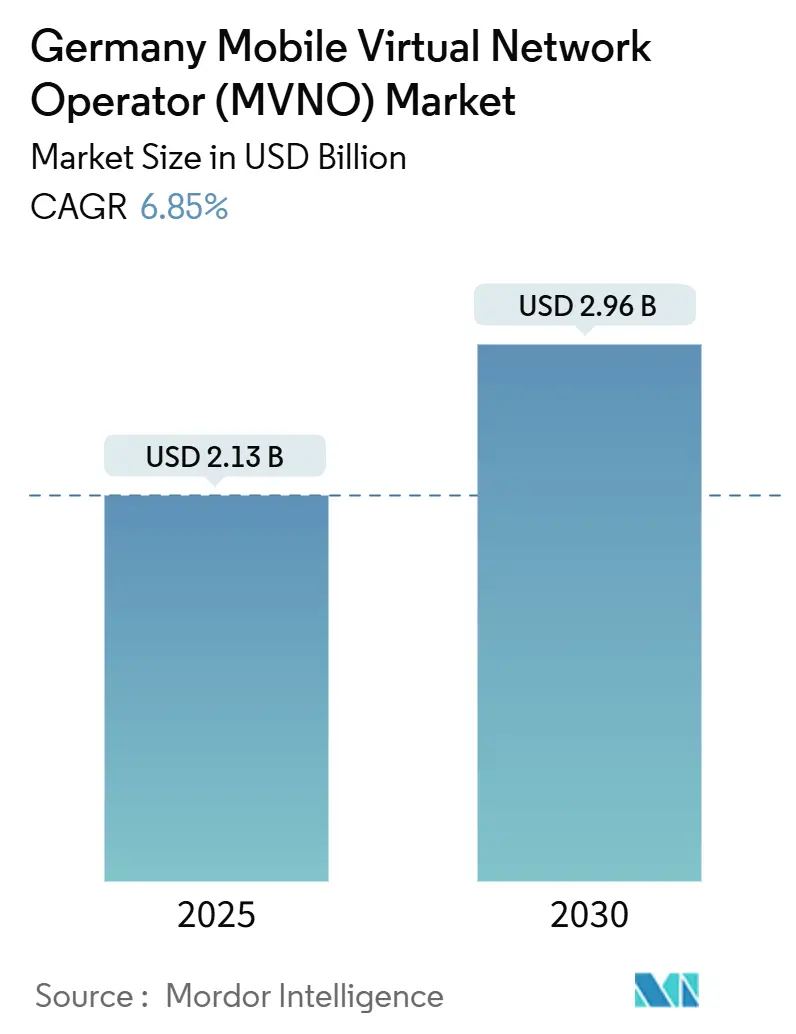

| Market Size (2025) | USD 2.13 Billion |

| Market Size (2030) | USD 2.96 Billion |

| Growth Rate (2025 - 2030) | 6.85% CAGR |

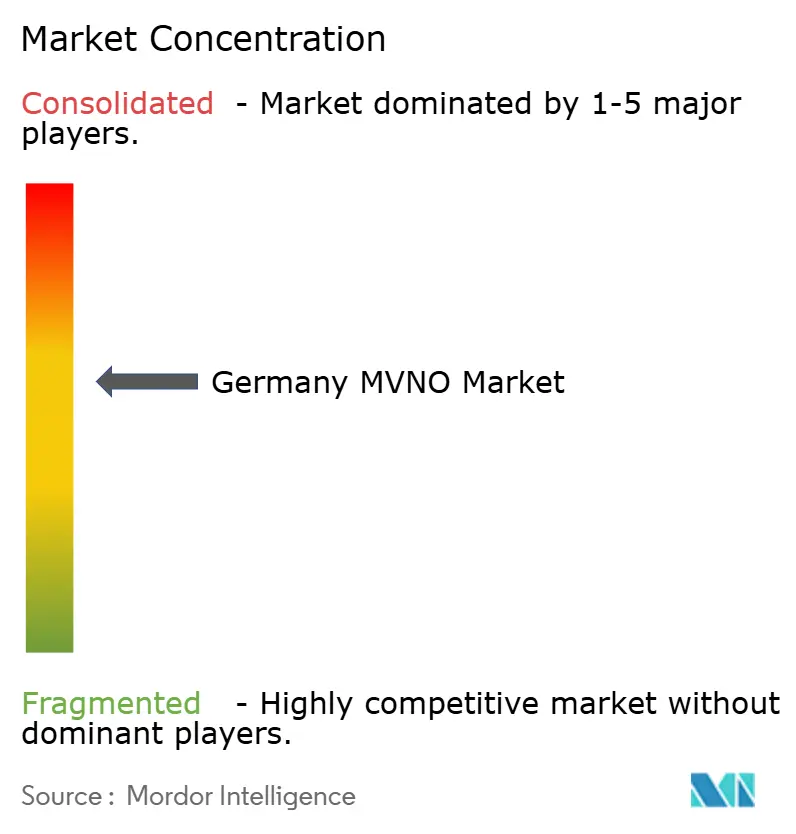

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The Germany Mobile Virtual Network Operator Market size is estimated at USD 2.13 billion in 2025, and is expected to reach USD 2.96 billion by 2030, at a CAGR of 6.85% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 29.89 million Subscribers in 2025 to 40.38 million Subscribers by 2030, at a CAGR of 6.20% during the forecast period (2025-2030).

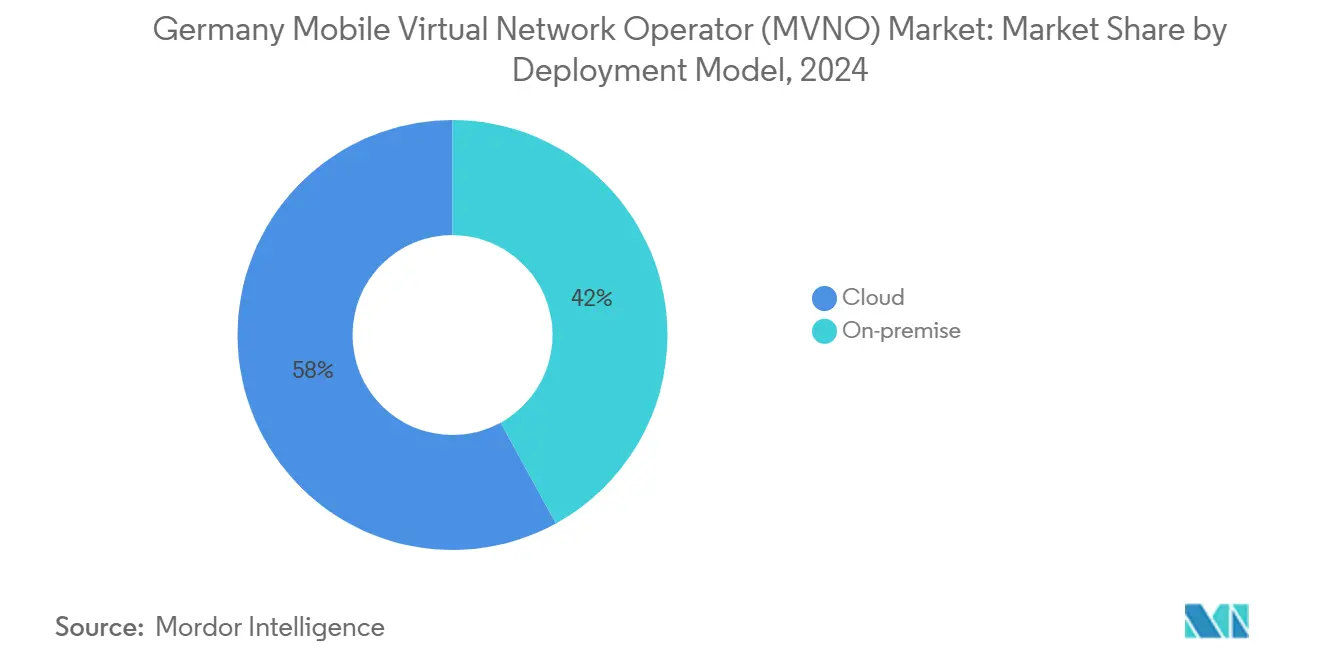

The outlook reflects sustained resilience despite wholesale-pricing pressures, with growth anchored in cloud-native operations, full-MVNO architectures, and digital-only distribution plays. Cloud deployments already account for 58% of the Germany MVNO market and continue to accelerate as operators trade capital-intensive on-premise systems for scalable infrastructure. Full MVNO models, commanding 46% share, signal a clear preference for end-to-end network control that unlocks richer service customization. Regulatory tailwinds such as EU wholesale-roaming caps preserve MVNO cost advantages, while the rapid take-up of eSIM and the emerging need for machine-centric connectivity across manufacturing hubs create fresh revenue streams [1]Deutsche Telekom AG, “Deutsche Telekom Continues Its Growth Course and Is Raising Its Guidance for the Full Year 2025,” telekom.com.

Key Report Takeaways

- By deployment model, cloud infrastructure captured 58% Germany MVNO market share in 2024 and is forecast to advance at a 13.18% CAGR to 2030.

- By operational mode, full MVNO structures held 46% of the Germany MVNO market size in 2024, and are forecast to advance at a CAGR of 10.97% through 2030.

- By subscriber type, consumers dominated with 72% revenue share in 2024; IoT-specific lines are projected to grow at 17.75% CAGR to 2030.

- By application, discount services led with 40% of the Germany MVNO market share in 2024, but cellular M2M connections are expected to expand at a 16.72% CAGR through 2030.

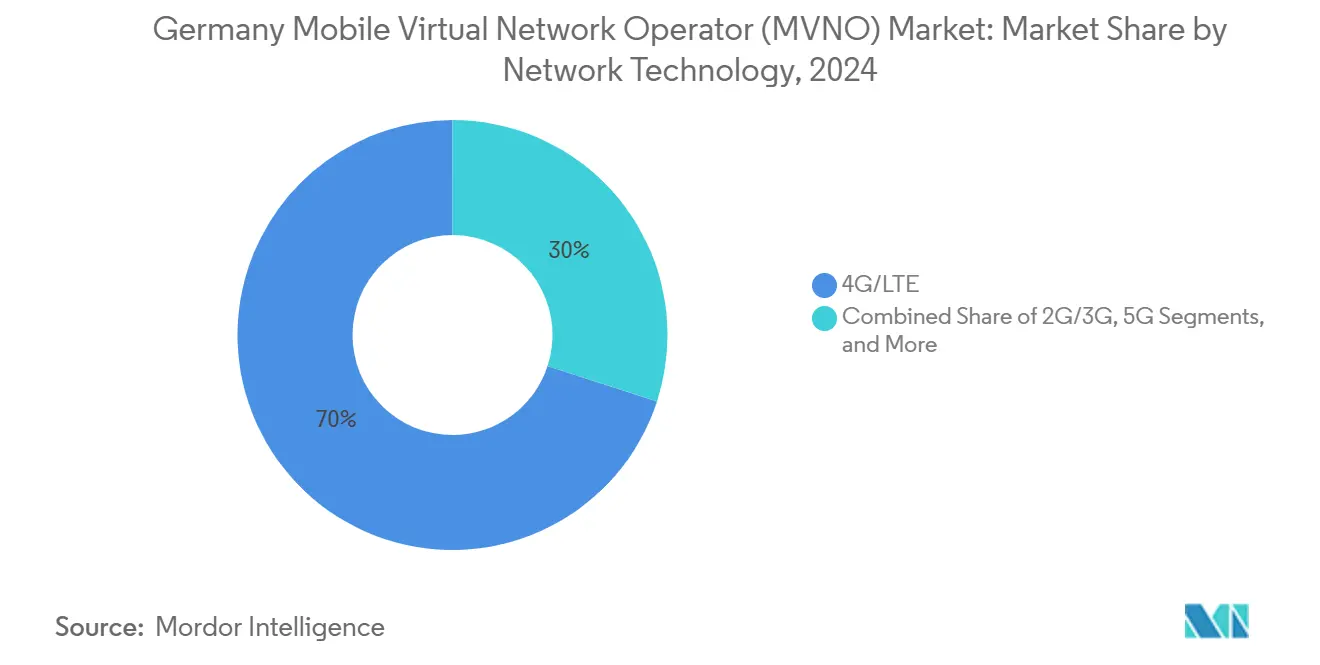

- By network technology, 4G/LTE accounted for 70% of the Germany MVNO market size in 2024, whereas 5G subscriptions are rising at a 26.72% CAGR to 2030.

- By distribution channel, online and digital-only sales contributed 43% share of the Germany MVNO market in 2024 and are forecast to grow at 14.70% CAGR to 2030.

Germany Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU wholesale-roaming price caps sustain MVNO cost advantages | +1.2% | Germany, with EU-wide regulatory framework | Medium term (2-4 years) |

| Price-sensitive consumers seek flexible low-cost plans | +1.8% | National, with concentration in urban centers | Short term (≤ 2 years) |

| Enterprise IoT/M2M connectivity demand surges | +2.1% | National, with industrial clusters in Bavaria, North Rhine-Westphalia | Long term (≥ 4 years) |

| eSIM-only onboarding lowers barriers for digital MVNOs | +0.9% | National, with early adoption in metropolitan areas | Medium term (2-4 years) |

| 2019 spectrum-auction service provider access clause fosters openness | +0.6% | National regulatory framework | Long term (≥ 4 years) |

| Satellite/NTN coverage unlocks rural MVNO plays | +0.4% | Rural regions, particularly in eastern Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Wholesale-Roaming Price Caps Sustain MVNO Cost Advantages

Regulated roaming charges continue to fall, with wholesale data dropping from EUR 2.00 in 2022 to EUR 1.00 by 2027, allowing MVNOs like Lycamobile to keep tariffs competitive for heavy-roaming communities [2]European Commission, “2025 Update of the Mobile Cost Model for Roaming and Voice Call Termination in the EU,” digital-strategy.ec.europa.eu. Predictable cost curves support long-range pricing strategy even as 5G roll-outs reshape network economics. Operators still grapple with unregulated SMS termination fees, yet the European Commission’s 2025 cost-model update promises alignment with next-gen networks. Compliance oversight by BEREC ensures consistent enforcement but leaves MVNOs to negotiate case-by-case solutions for traffic routed outside the EU.

Price-Sensitive Consumers Seek Flexible Low-Cost Plans

German shoppers are shifting to no-frills monthly packages such as Aldi Talk’s 15 GB plan at EUR 9.99, forcing rivals to mirror aggressive data buckets [3]Henning Gajek and Markus Weidner, “Tchibo Mobil kündigt Preissenkung für Jahrespaket S an,” teltarif.de. Lidl Connect’s unlimited on-demand offer and Tchibo Mobil’s 35 GB promotional tier reinforce a value-play cycle that compresses average revenue per user. Freenet’s 2025 report shows a 3% ARPU decline, highlighting profitability pressures amid customer-driven downgrades. As discount promotions proliferate, MVNOs must recalculate lifetime value and double down on churn-retention analytics.

Enterprise IoT/M2M Connectivity Demand Surges

German industry’s move toward fully automated factories has lifted demand for low-cost, wide-area cellular links. Deutsche Telekom’s Make Everything Cellular Connected program prices IoT connectivity at EUR 10 per device per year, paving the way for specialized MVNOs to bundle connectivity with analytics. Backed by Deutsche Telekom and SoftBank, 1NCE’s USD 60 million 2025 funding illustrates investor appetite for pure-play IoT MVNOs. Industrial hubs in Bavaria and North Rhine-Westphalia now seek carrier-grade connectivity for logistics, automotive, and robotics, amplifying long-run growth prospects.

eSIM-Only Onboarding Lowers Barriers for Digital MVNOs

The rise of eSIM allows fully digital activation without physical logistics, trimming acquisition cost and enabling instant switches through apps. Vodafone’s tie-up with Gigs shows how brands can launch turnkey MVNO propositions using API-driven provisioning. GSMA forecasts 1 billion eSIM smartphones in use by 2025, scaling to 6.9 billion by 2030, creating a vast pool of devices ready for app-centric service journeys. Deutsche Telekom’s commercial network-API suite further reduces integration friction, inviting software firms to embed connectivity in wider digital platforms.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wholesale pricing power of MNOs compresses MVNO margins | -1.4% | National, with particular impact on smaller operators | Short term (≤ 2 years) |

| Market saturation triggers intense price wars | -0.8% | National, with urban market concentration | Medium term (2-4 years) |

| Slow rollout of 5G-SA network-slicing APIs for MVNOs | -0.6% | National infrastructure development | Medium term (2-4 years) |

| GDPR/BDSG compliance drives up IT operating costs | -0.3% | National regulatory framework | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Wholesale Pricing Power of MNOs Compresses MVNO Margins

Three host networks control nearly all radio access, giving Deutsche Telekom, Vodafone, and Telefónica leverage to raise wholesale rates or limit 5G features. Deutsche Telekom’s 99.6% 4G household reach underscores its negotiation strength [4]Deutsche Telekom AG, “Deutsche Telekom Expects Further Earnings Growth for 2025 After a Record Year in 2024,” telekom.com. Although Bundesnetzagentur obliges incumbents to engage in good-faith talks, enforcement is weak; smaller MVNOs often accept slim margins to stay alive. The capital needed for standalone 5G networks means incumbents can pass upgrade costs downstream, squeezing service-based rivals.

Market Saturation Triggers Intense Price Wars

Germany counts 105.4 million active SIMs, leaving operators to poach users in a zero-sum game. Retail brands such as Aldi and Lidl subsidize tariffs with grocery profits, undercutting pure-play MVNOs. Drillisch’s retreat from certain prepaid offers points to the difficulty of maintaining profitability when every gigabyte is a bargaining chip. As 1&1 evolves into the fourth MNO, temporary wholesale deals will again stir promotional turbulence before the ecosystem stabilizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Dominates Digital Transformation

Cloud platforms command 58% Germany MVNO market share and are on track for a 13.18% CAGR. Adoption is driven by instant scalability, zero-touch upgrades, and access to AI-based analytics that sharpen customer targeting. Operators avoid heavy lift-and-shift capex, preferring pay-as-you-grow pricing that aligns with tight margin profiles. Compliance hurdles around data residency are easing thanks to hyperscaler-run German zones, making cloud the default choice for new entrants. The Germany MVNO industry still retains on-premise setups for high-security enterprise use cases, but those footprints will continue to shrink as network-slice orchestration and edge computing mature.

Second-order impacts include faster product launch cycles and access to third-party developer ecosystems via open APIs. Deutsche Telekom’s network API marketplace gives cloud-based MVNOs ready access to quality-of-service and identity services that once required bespoke integration. Altogether, cloud migration underpins digital-first branding, frictionless onboarding, and advanced self-care, cornerstones of future differentiation in the Germany MVNO market.

By Operational Mode: Full MVNO Models Drive Network Control

Full MVNOs run their own core networks, enabling direct billing, policy control, and service creation. This autonomy justifies the format’s 46% Germany MVNO market share and 10.97% CAGR outlook. The trade-off is higher operating complexity, yet control over customer data delivers superior monetization potential. 1NCE’s 30 million IoT devices attest to the model’s scalability when paired with a single-purpose segment focus.

In contrast, reseller and service-operator formats suit brands prioritizing quick entry and minimal upfront cost. However, they increasingly struggle to stand out as data buckets homogenize. Forward-looking MVNOs weigh the capital outlay of a full core against the long-term ability to orchestrate differentiated network slices for gaming, AR/VR, or industrial control. Those with credible financial backing are pivoting toward full-stack control to future-proof their positions in the Germany MVNO market.

By Subscriber Type: Consumer Dominance Faces IoT Disruption

Consumer lines still account for 72% of the Germany MVNO market size, but IoT-specific SIMs are the fastest climber at 17.75% CAGR on the back of Industry 4.0 initiatives. German manufacturers embrace connected sensors to optimize uptime, fueling persistent demand for low-bandwidth, high-density subscriptions. Enterprise users occupy the middle ground, balancing predictable voice/data needs with bespoke service-level agreements. The Germany MVNO market offers clear evidence of a pivot toward device-centric revenues that outlast volatile consumer churn cycles.

For incumbents, the consumer realm remains a battlefield of price promotions and brand marketing. Tchibo Mobil’s long-running retail presence illustrates the staying power of trust and convenience, while app-native challengers aim at Gen-Z segments with integrated lifestyle propositions. As IoT volumes swell, MVNOs that master vertical solutions and security-certified SIM management will gain outsized influence over the Germany MVNO industry.

By Application: Discount Services Lead, M2M Accelerates

Discount plans hold 40% Germany MVNO market share, underlining Germany’s price-sensitive culture. Yet cellular M2M is set to outpace all other categories at 16.72% CAGR through 2030, driven by smart-factory roll-outs and logistics tracking. Business plans that bundle unified communications and cloud PBX retain steady growth, while niche applications, from travel SIMs to migrant-community packages, fill specific gaps.

Hybrid terrestrial-satellite services, now available from Deutsche Telekom at EUR 211.50 per month, extend M2M coverage into remote energy and agriculture sites. As device counts multiply, operators must rationalize back-office processes to manage millions of low-ARPU endpoints. The Germany MVNO market, therefore, splits between high-volume, low-value machine traffic and human lines where experience and brand loyalty remain key.

By Network Technology: 4G Dominance Transitions to 5G Leadership

4G/LTE underpins 70% of the Germany MVNO market in 2024, but 5G is racing ahead at 26.72% CAGR. Early 5G standalone trials promise network-slice-enabled SaaS offers such as cloud gaming with guaranteed latency. MVNOs reliant on wholesale access must negotiate timely exposure to these capabilities or risk losing relevance. Legacy 2G/3G networks near sunset, while satellite and non-terrestrial networks complement terrestrial gaps, especially along rail corridors and rural valleys.

Deploying 5G functions over cloud cores lowers barriers to entry, yet spectrum access remains tightly held. The 2019 auction’s service provider clause did force hosts to open up, but actual slice availability is staggered. Consequently, strategic alliances with satellite operators and API-first network partners will decide who captures premium 5G value in the Germany MVNO market.

By Distribution Channel: Digital Transformation Accelerates

The online/digital-only sales already contribute 43% of Germany's MVNO market revenue, propelled by eSIM activation and app-based self-care, and are expected to reach a CAGR of 14.70% over the projected period. Online journeys cut SIM logistics costs and broaden reach beyond brick-and-mortar. Traditional retail remains important for handset bundling and over-the-counter support, but footfall is trending down as post-pandemic consumers favor remote interactions. Carrier sub-brand stores address niche demographics, while wholesale partnerships open doors to corporate procurement and embedded connectivity plays.

Successful operators optimize digital funnels with real-time analytics, dynamic pricing, and micro-service-based personalization. API-powered identification and electronic signatures streamline compliance, easing account creation hurdles. These capabilities position the Germany MVNO market to pivot quickly toward emerging service models such as context-aware tariffs triggered by location or usage behavior.

Geography Analysis

Germany’s federal economy and dense urbanization shape MVNO opportunity zones. Metropolitan clusters such as Berlin, Munich, and Cologne supply concentrated consumer bases that favor app-centric acquisition strategies. Industrial heartlands in Bavaria and North Rhine-Westphalia amplify IoT demand for production monitoring and predictive maintenance services. In 2025, Deutsche Telekom added 200 rural mobile sites and upgraded 1,000 base stations to 5G, expanding wholesale reach for partners targeting underserved areas.

Eastern regions, historically lagging in coverage, now present white-space growth potential as satellite-assisted offers bridge last-mile gaps. Nationwide EU roaming rules further empower diaspora-focused MVNOs such as Lebara to serve cross-border callers without punitive cost escalation. Nonetheless, local compliance with GDPR and BDSG drives higher operating overhead, pushing smaller brands to adopt cloud-resident, audit-ready data platforms to stay viable within the Germany MVNO industry.

Federal spectrum policy also shapes the competitive chessboard. The Bundesnetzagentur’s 2025 extension requires incumbent MNOs to negotiate wholesale 5G access on fair terms, a move designed to preserve service-level competition while stimulating infrastructure investment. Regional economic programs encouraging smart-city pilots add further impetus for IoT-specialized MVNOs to forge municipal partnerships, particularly in logistics hubs and autonomous mobility corridors.

Competitive Landscape

The Germany MVNO market is semi-consolidated: no single virtual operator exceeds a 15% share, yet the top five providers still hold a collective 62%. Brand equity, retail alliances, and integration prowess decide competitive standing more than raw subscriber totals. Discount leaders rely on grocery or coffee-house footprints to cross-sell SIM cards, whereas digital-native entrants capitalize on influencer channels and app-store visibility.

Strategic pivots now revolve around platform economics and embedded connectivity. Vodafone’s partnership with Gigs exemplifies a telecom-as-a-service model that lets non-telco brands launch co-branded propositions in weeks. Deutsche Telekom’s commercial API suite offers third parties quality of service and identity hooks once reserved for network owners, extending the reach of MVNO innovation. IoT specialists such as 1NCE prove that a laser-focused vertical can achieve rapid scale and attract blue-chip funders.

While retail brands inject low-price competition, high-touch enterprise MVNOs target value-added services: secure VPNs, private LTE, and industrial-grade SLAs. The looming arrival of 5G slicing APIs promises new differentiation levers, but only MVNOs with full-core setups are technically equipped to capitalize promptly. Cost leadership, niche specialization, and platform partnerships therefore remain the three pillars of competitive strategy in the Germany MVNO market.

Germany Mobile Virtual Network Operator (MVNO) Industry Leaders

Freenet AG (mobilcom-debitel / klarmobil)

Aldi Talk (Medion AG)

Congstar GmbH

Lycamobile Germany GmbH

Lebara Mobile Germany Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Lidl Connect rolled out unlimited on-demand tariffs from EUR 9.99, intensifying prepaid price competition.

- June 2025: Vodafone Germany was hit with a EUR 45 million GDPR fine, underscoring rising compliance risk.

- April 2025: 1NCE secured a USD 60 million investment round led by Deutsche Telekom and SoftBank to scale its IoT MVNO footprint.

- January 2025: Tchibo Mobil launched a 35 GB Smart L promo at EUR 9.99, sustaining discount momentum.

Germany Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller/ Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller/ Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How large is the Germany MVNO market in 2025?

It is valued at USD 2.13 billion, with a projected rise to USD 2.96 billion by 2030.

What is the expected CAGR for German MVNO providers through 2030?

The Germany MVNO market is forecast to grow at a 6.85% CAGR during 2025–2030.

Which segment is expanding fastest within German MVNO subscriptions?

IoT-specific SIMs are set to grow at a 17.75% CAGR, outpacing consumer and enterprise lines.

How dominant are digital-only distribution channels?

Online and app-based sales already generate 43% of revenue and carry a 14.70% CAGR outlook.

What impact do EU roaming regulations have on German MVNO pricing?

Declining wholesale roaming caps preserve cost advantages, adding roughly 1.2 percentage points to forecast CAGR.

How is 5G adoption progressing among German MVNOs?

While 4G still holds 70% share, 5G subscriptions are increasing at 26.72% CAGR as hosts expose new APIs.

Page last updated on: