Denmark Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

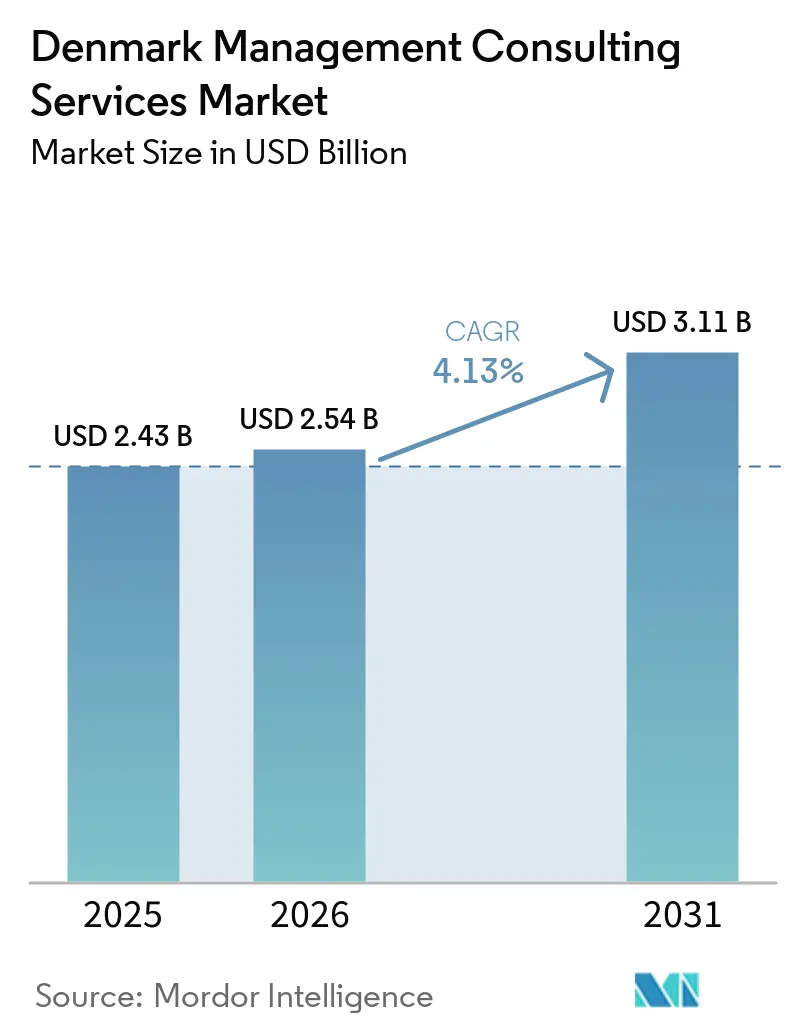

| Base Year Market Size (2025) | USD 2.43 Billion |

| Market Size (2026) | USD 2.54 Billion |

| Market Size (2031) | USD 3.11 Billion |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

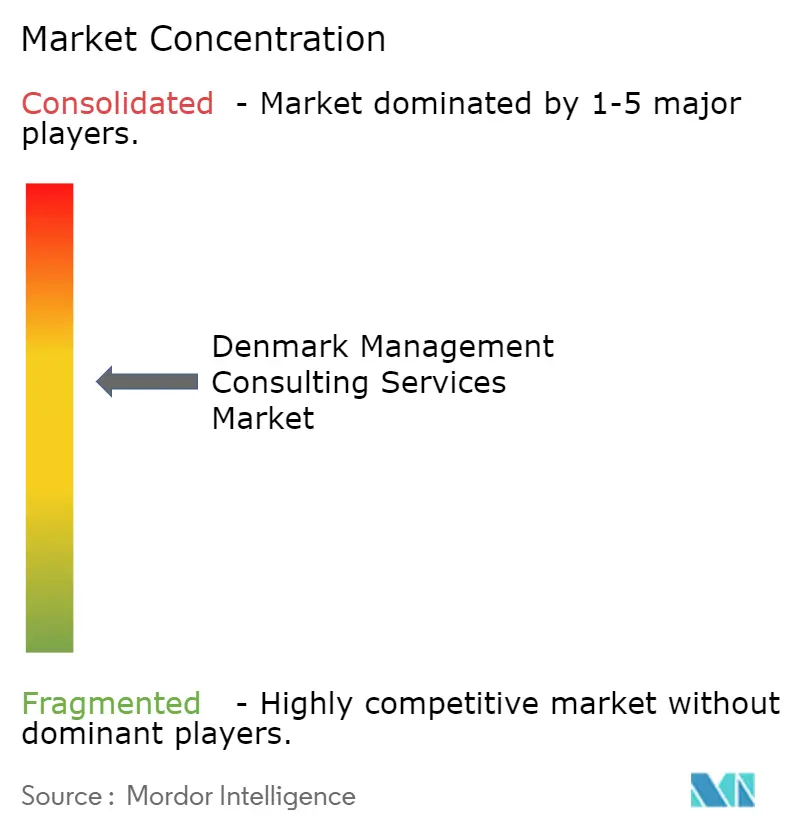

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Management Consulting Services Market Analysis by Mordor Intelligence

The Denmark management consulting services market size is expected to increase from USD 2.43 billion in 2025 to USD 2.54 billion in 2026 and reach USD 3.11 billion by 2031, growing at a CAGR of 4.13% over 2026-2031. Denmark’s consulting spend tends to align with regulatory compliance cycles rather than GDP swings, so the market shows steady rather than spectacular expansion. Demand is broad-based but especially strong where new EU directives converge, notably CSRD, DORA and NIS2, which collectively redefine the scope of advisory needs for finance, manufacturing and the public sector. Intense digital-government programs, heavy investment in offshore wind and the country’s outsized private-equity deal flow further deepen the advisory wallet, while a small domestic talent pool keeps pricing power with experienced partners. Competitive rivalry remains high as global integrators, Nordic specialists and boutique strategy firms all race to bundle risk, digital and ESG capabilities.

Key Report Takeaways

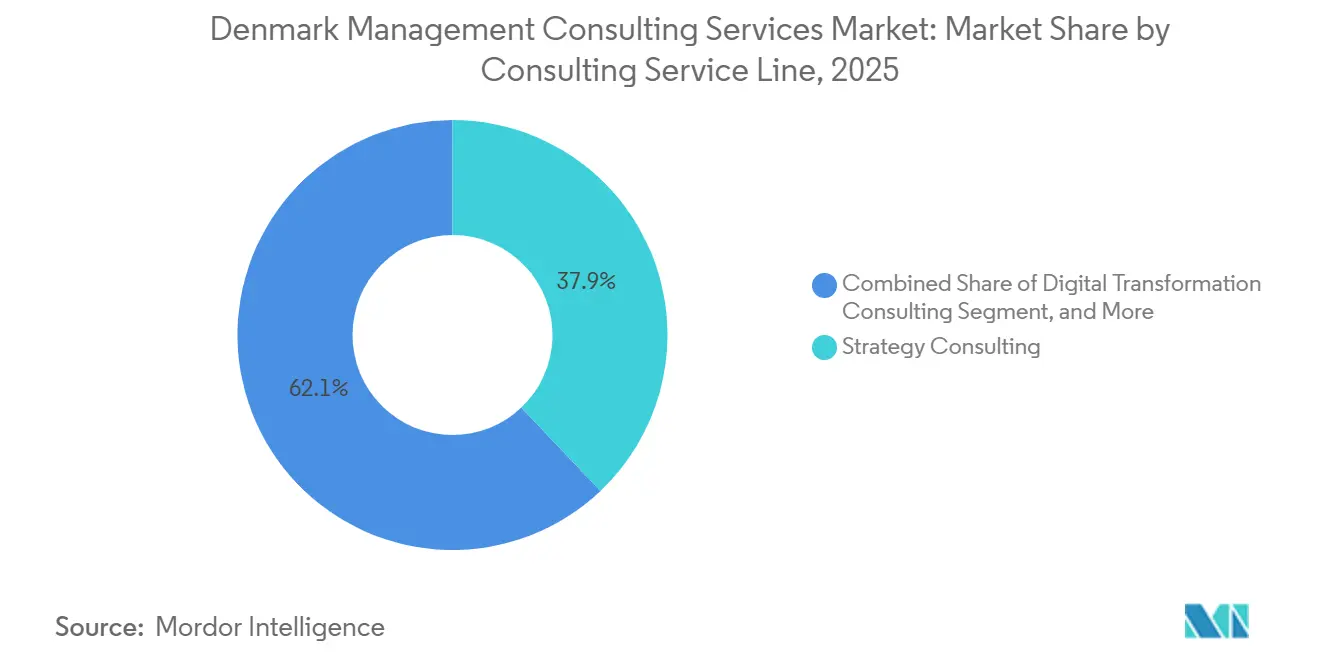

- By consulting service line, Strategy Consulting led with 37.92% revenue share in 2025, while Risk and Compliance Consulting is projected to advance at the fastest 4.63% CAGR through 2031.

- By organization size, Large Enterprises commanded 64.26% of 2025 spend, whereas Small and Medium-Sized Enterprises are forecast to expand at a 4.24% CAGR on the back of subsidy-backed digitalization demand.

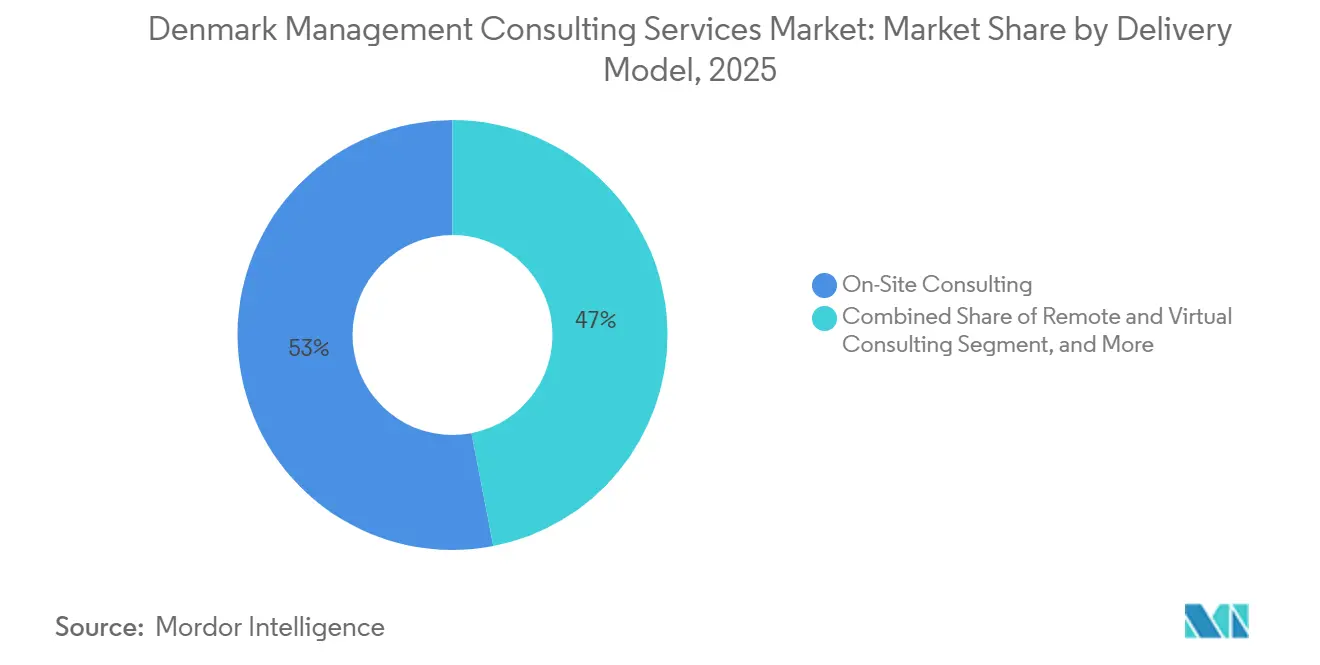

- By delivery model, On-Site Consulting held 53.04% share in 2025 and Remote and Virtual Consulting is poised to grow at a 4.81% CAGR as clients nearshore routine work.

- By end-user industry, Banking and Insurance accounted for 26.17% of 2025 revenue, yet Healthcare is expected to post the fastest 4.36% CAGR to 2031 on the back of national EHR interoperability mandates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Denmark Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory CSRD Compliance Creating Mid-Cap Consulting Windfall | +1.2% | National, strongest in Copenhagen and Aarhus corridors | Short term (≤ 2 years) |

| Accelerated Digital-Transformation Budgets in Danish Public Sector | +0.9% | Nationwide across central agencies and 5 regional health authorities | Medium term (2-4 years) |

| Rising Regional Demand for Sustainability and ESG Advisory | +0.7% | Nordic spillovers into Danish operations of multinationals | Medium term (2-4 years) |

| Strong Private-Equity Deal Flow Requiring Due-Diligence Support | +0.6% | Financial-services and technology clusters nationally | Short term (≤ 2 years) |

| Near-shoring by Nordic Multinationals Boosting Local Spend | +0.4% | Denmark, Sweden and Norway | Long term (≥ 4 years) |

| North Sea Energy-Security Projects Driving Offshore Advisory | +0.3% | Jutland wind zones and Bornholm energy island | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory CSRD Compliance Creating Mid-Cap Windfall

The EU Corporate Sustainability Reporting Directive (CSRD) binds large Danish corporates today, but mid-caps must file from fiscal 2026, compressing implementation timelines. A 2024 readiness survey showed 68% of Danish firms with 250-499 employees had yet to start materiality assessments, driving a short, intense advisory surge. Double-materiality rules add complexity that mid-sized manufacturers and logistics firms cannot handle in-house, so multi-disciplinary consultancies combining ESG data, process redesign and assurance support are in pole position. Early enforcement notices for greenwashing confirm that quality, not just speed, will decide who avoids restatements, keeping demand elevated through 2028.

Accelerated Digital-Transformation Budgets in the Danish Public Sector

Denmark allocated DKK 266.7 million (USD 38.1 million) to AI projects in 2024 and committed another DKK 80 million (USD 11.4 million) for digital sovereignty programs running 2026-2029.[1]Danish Agency for Digital Government, “AI and Automation Investments 2024,” DIGST.DK Consolidated multi-year IT frameworks worth DKK 598 million (USD 85.4 million) now require vendor-neutral advisory on contracts above DKK 10 million, structurally favoring pure-play consultancies over software sellers.[2]Danish Business Authority, “Digital Sovereignty Fund 2026-2029,” ERHVERVSSTYRELSEN.DK Parallel NIS2 and cybersecurity mandates that many municipalities missed in 2025 further lock in demand until at least 2027.

Rising Regional Demand for Sustainability and ESG Advisory

Eighty-two percent of large Nordic firms already connect executive pay to ESG metrics, up sharply from 2022 levels.[3]Nordic Council of Ministers, “Green Transition Report 2024,” NORDEN.ORG Denmark’s leadership in offshore wind and its flagship Bornholm energy-island project mean environmental-impact assessment, carbon-accounting and stakeholder-engagement consulting requests increasingly originate in Copenhagen but spill across the region. Sustainability-linked finance is another lever: Ørsted’s 2024 issuance of EUR 150 million (USD 169.5 million) in green-linked loans requires independent performance verification.[4]Ørsted, “Annual Report 2024,” ORSTED.COM Expected ISO 14097 accreditation rules could consolidate the segment by 2027.

Strong Private-Equity Deal Flow Requiring Due-Diligence Support

Nordic private equity posted EUR 45.4 billion (USD 51.3) in Q3 2024 deals, with Denmark punching above its economic weight by taking 18% of the transaction count. Buyers now seek deep operational and ESG diligence in addition to classic financial and legal work, expanding consulting spend per deal. Denmark’s competitive carried-interest tax rate keeps global funds active, though fee pressure has grown as sponsors internalize routine analysis and reserve consultants for cyber-security or supply-chain deep dives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent Scarcity and Escalating Consultant Wage Inflation | -0.8% | Copenhagen metro and Aarhus tech corridor | Short term (≤ 2 years) |

| Generative-AI Self-Service Tools Cannibalizing Entry-Level Projects | -0.6% | Nationwide with Nordic spillovers | Medium term (2-4 years) |

| Procurement-Price Pressure from Framework Buyers | -0.4% | Public sector and top-10 corporates | Medium term (2-4 years) |

| Stricter Conflict-of-Interest Rules Limiting Multi-Mandate Wins | -0.3% | Sectors overseen by the Danish Financial Supervisory Authority | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Talent Scarcity and Consultant Wage Inflation

IT-consultant wages rose 6.2% in 2024, well above the 4.13% market CAGR, as Denmark’s near-full employment strains the talent pool.[5]Danish IT Industry Association, “Wage Inflation Report 2024,” ITB.DK Senior-level shortages force mid-tier firms to rely on costly contractors whose day rates exceed DKK 12,000 (USD 1,714), eroding margins. Immigration policy has loosened, but Danish-language proficiency remains critical for public-sector work, so relief will be slow.

Generative-AI Self-Service Tools Shrink Entry-Level Hours

AI copilots now automate up to 40% of tasks once billed by junior consultants, including data synthesis and slide production. Early Danish adopters such as Novo Nordisk rolled out Microsoft Copilot to 3,200 knowledge workers in 2024.[6]Novo Nordisk, “Annual Report 2024,” NOVONORDISK.COM Firms must either train juniors in AI-augmented delivery or accept lower project economics as clients cite reduced effort during fee negotiations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Compliance Fuels the Shift

The Denmark management consulting services market share favored Strategy Consulting at 37.92% in 2025. However, Risk and Compliance work will grow fastest, supported by overlapping EU mandates that require granular regulatory interpretation. The Denmark management consulting services market size for these services is projected to expand steadily as firms embed ESG data architectures and cybersecurity controls into broader transformation programs. Operations Consulting continues to face pricing pressure, while HR and Financial Advisory consulting enjoy niche spikes tied to talent shortages and private-equity activity. Clients increasingly request integrated teams spanning strategy, digital and risk, a trend that disadvantages single-practice boutiques.

Multi-line engagements are becoming the norm. Big Four firms cross-sell assurance-ready ESG reporting from their audit bases, while technology outsourcers bundle managed services with advisory, blurring competitive boundaries. Cyber-resilience assessments mandated by the 2025 National Cyber Strategy are now a recurring revenue stream, yet managed-security-service providers enter the advisory arena, forcing pure consultancies to double-down on sector expertise.

By Organization Size: Subsidized SME Digitalization

Large Enterprises still anchor the Denmark management consulting services market, holding 64.26% of 2025 spending. They contract multi-year, multi-tower engagements for M&A integration, ERP renewal and global operating-model redesign. In contrast, SME demand, though smaller in absolute value, is the fastest mover as digital-voucher programs reimburse up to 50% of consulting fees. The Denmark management consulting services market size for SMEs is set to grow in tandem with these subsidies, even though smaller contracts raise client-acquisition costs. Succession planning in family businesses further supports valuation and restructuring advisory, but consultants must package repeatable offerings to maintain margins.

Scaling SME work hinges on productized deliverables like fixed-scope CSRD readiness kits. Nordic challengers accustomed to price-capped public-sector frameworks find these packages natural, while global integrators often struggle to downscale their methodologies. Whether SMEs continue their brisk uptake beyond subsidy periods will depend on measurable ROI from early digital migrations.

By Delivery Model: Hybrid Becomes Mainstream

On-Site Consulting captured 53.04% share in 2025 because board-level strategy and M&A still value face-to-face workshops. Yet Remote and Virtual models are climbing at a 4.81% CAGR as Danish companies nearshore routine analytics to Poland and the Baltics. Hybrid delivery, which blends weekly in-person sprints with offshore execution, now dominates new RFPs. The Denmark management consulting services market share for virtual delivery rises fastest where data-residency and classified-information barriers are minimal.

That said, healthcare and financial-services clients must comply with stringent GDPR transfer rules, so fully virtual projects remain limited in these verticals. Consultants offset this by employing Danish-based cybersecurity pods that handle restricted data, while offshore teams tackle lower-risk tasks. High travel costs and sustainability commitments also make clients favor low-carbon hybrid models.

By End User Industry: Healthcare Surges on Interoperability

Banking and Insurance accounted for 26.17% of 2025 revenue, driven by core-bank upgrades and DORA compliance. Still, Healthcare’s 4.36% forecast CAGR will outpace all other verticals as hospitals integrate electronic patient records across five regions by 2027.[7]Danish Health Data Authority, “Interoperability Mandate 2025,” SUNDHEDSDATASTYRELSEN.DK The Denmark management consulting services market size tied to hospital IT is already swelling with EUR 200 million earmarked for EHR projects.

Energy and Resources consulting spikes with every offshore-wind auction, while Manufacturing grabs Industry 4.0 advisory linked to robotics and automation. Public-sector consulting holds 18% share, supported by centralized framework agreements that lower transaction costs but compress margins. Retail and logistics form a fragmented tail, yet benefit from carbon-accounting mandates under Denmark’s Climate Action Plan.[8]Danish Climate Action Plan, “Green Transition Investments 2024-2030,” KEFM.DK

Geography Analysis

Copenhagen accounts for roughly 62% of national consulting spend, reflecting its concentration of corporate headquarters, ministries and finance houses. Aarhus contributes about 15%, buoyed by a vibrant tech scene clustered around the university. Odense and Aalborg together hold 8%, linked to robotics and medtech, while remaining demand comes from Jutland and the islands, often tied to public-sector or agricultural projects.

Decentralization policies are moving 3,800 public-sector positions to towns such as Esbjerg and Randers by 2027, nudging consulting demand outside the capital. However, firms face a cost dilemma: open regional offices or risk lower tender win rates. Infrastructure megaprojects like the Fehmarn Belt tunnel will connect Denmark more tightly to Germany, spurring cross-border logistics consulting that requires pan-EU credentials.

The Nordic Digital Single Market initiative aims to harmonize procurement rules across Denmark, Sweden, Norway and Finland by 2026. That will open cross-border public-sector tenders, but also increase competitive intensity. Meanwhile, Danish compliance experience under CSRD and DORA positions domestic consultancies to export implementation playbooks to Germany and the Netherlands, turning regulatory burden into regional advantage.

Competitive Landscape

The top ten firms jointly hold about 55% of the Denmark management consulting services market, indicating moderate concentration. Global integrators such as Accenture, Deloitte and McKinsey win large transformation programs that require ISO-certified methodologies and cross-border reach. Yet framework contracts set fixed hourly bands, trimming the premium these brands once enjoyed.

Nordic specialists, Implement Consulting, Netcompany, Rambøll, use Danish-language fluency and deep public-sector ties to wrest mid-cap deals, often undercutting global peers by 15-20% on price. Generative-AI adoption is now a differentiator; firms automating research, drafting and scenario modeling can cut delivery hours 15-20% and share savings with clients. Boutique strategy outfits retain strength in M&A and board advisory where senior judgment trumps AI outputs, but face pressure to add risk and digital wings.

Regulatory shifts also reshape the field. Conflict-of-interest rules stop audit arms from offering certain advisory services to audit clients, freeing work for independent consultancies in banking and energy. Sustainability-linked finance advisory is one white-space niche: Denmark issued EUR 8 billion (USD 9.04 billion) in green bonds in 2024, and these deals require impact measurement skills many traditional advisors lack.

Denmark Management Consulting Services Industry Leaders

Accenture plc

Bain & Company Denmark A/S

The Boston Consulting Group Nordic A/S

McKinsey & Company Denmark

Deloitte Consulting P/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Accenture won a DKK 120 million (USD 17.1 million) contract with the Ministry of Finance to modernize tax administration, integrating AI-driven fraud detection and self-service portals.

- November 2025: Deloitte Denmark secured a EUR 25 million (USD 28.3 million) CSRD advisory mandate from A.P. Møller-Maersk to build sustainability data infrastructure and assurance workflows.

- September 2025: McKinsey opened an Energy Transition practice in Copenhagen, hiring 15 specialists from Ørsted and Vestas to target offshore-wind finance and hydrogen-economics projects.

- July 2025: Boston Consulting Group partnered with Novo Nordisk on a EUR 50 million (USD 56.5 million) circular-economy pharmaceutical-packaging program.

Denmark Management Consulting Services Market Report Scope

The Denmark Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current Denmark management consulting services market size and its 2031 forecast?

The market stands at USD 2.54 billion in 2026 and is projected to reach USD 3.11 billion by 2031 at a 4.13% CAGR.

Which consulting service line is growing fastest in Denmark?

Risk and Compliance Consulting is expected to expand at a 4.63% CAGR through 2031, outpacing all other service lines.

Why is healthcare consulting demand accelerating in Denmark?

A national mandate requires interoperable electronic patient records by 2027, turning IT upgrades into compliance-driven projects and lifting healthcare's CAGR to 4.36%.

How are delivery models shifting in Danish consulting?

Hybrid models that mix on-site workshops with remote execution are growing fastest, buoyed by nearshoring and mature video collaboration.

What restrains growth despite rising demand?

Acute talent shortages push consultant wages higher, while generative-AI tools let clients internalize entry-level tasks, pressuring consulting margins.

Which regions outside Copenhagen offer emerging opportunities?

Decentralization policies that relocate thousands of public-sector roles to Esbjerg, Randers and other towns are redistributing consulting demand beyond the capital.

Page last updated on: