Poland Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

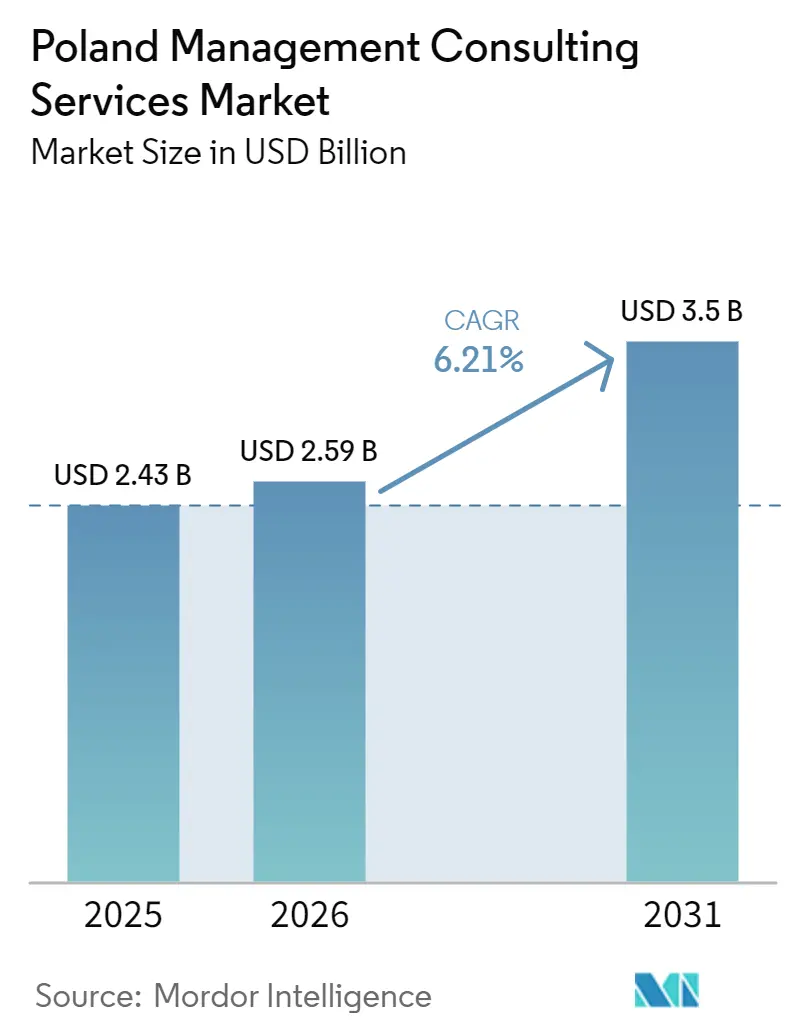

| Base Year Market Size (2025) | USD 2.43 Billion |

| Market Size (2026) | USD 2.59 Billion |

| Market Size (2031) | USD 3.5 Billion |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

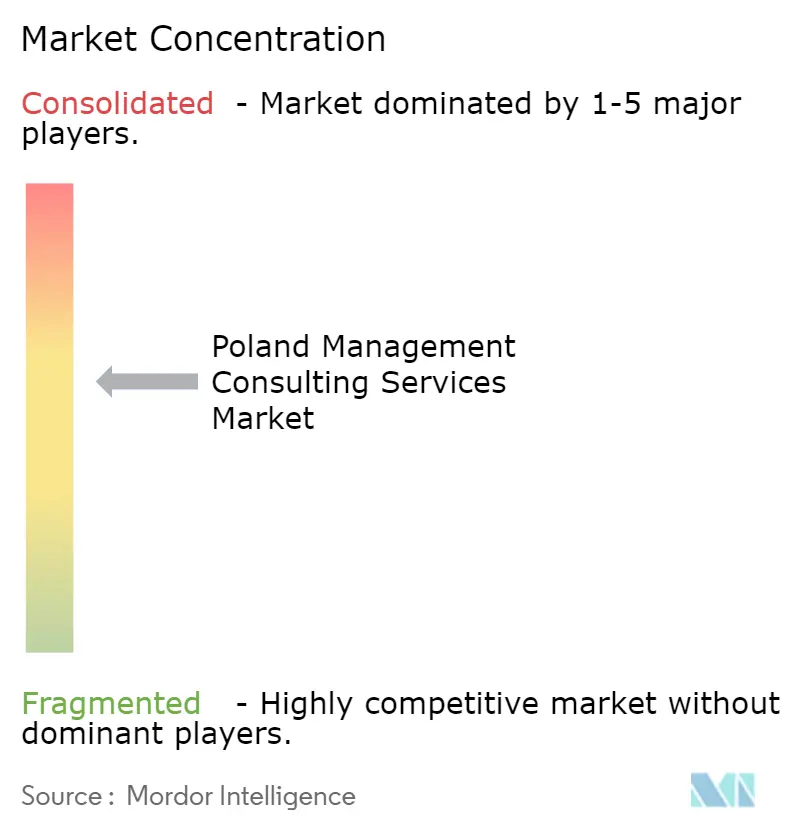

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Management Consulting Services Market Analysis by Mordor Intelligence

The Poland management consulting services market size is projected to expand from USD 2.43 billion in 2025 and USD 2.59 billion in 2026 to USD 3.5 billion by 2031, registering a CAGR of 6.21% between 2026 to 2031. Robust pipeline funding from the National Recovery Plan has shifted demand from high-level strategy to hands-on digital execution, especially in cybersecurity, cloud migration, and ESG compliance. Consulting firms benefit from Poland’s rise as Central Europe’s leading professional-services hub, yet they face margin pressure caused by double-digit wage inflation and tight talent supply. Near-shoring mandates from Western Europe continue to funnel projects into Polish delivery centers, while the EU’s NIS2 and CSRD regulations create recurring advisory revenues. Competitive intensity remains moderate, with global integrators dominating large-enterprise accounts and local specialists capturing public-sector and SME work.

Key Report Takeaways

- By consulting service line, Strategy Consulting led with 31.47% revenue share in 2025, while Digital Transformation Consulting is forecast to grow at a 6.78% CAGR through 2031, underscoring a pivot from visioning to execution.

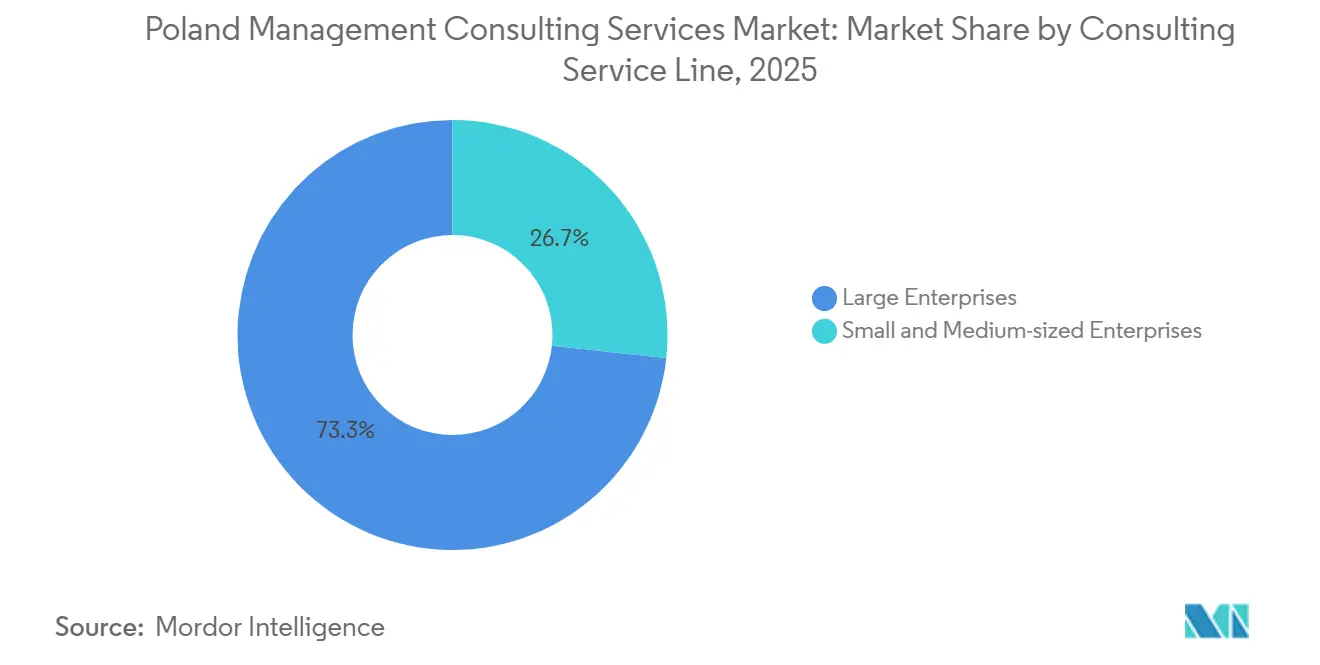

- By organization size, Large Enterprises commanded 61.83% of 2025 revenues, but Small and Medium-Sized Enterprises are projected to expand at a 6.52% CAGR on the back of EU-funded digitalization incentives.

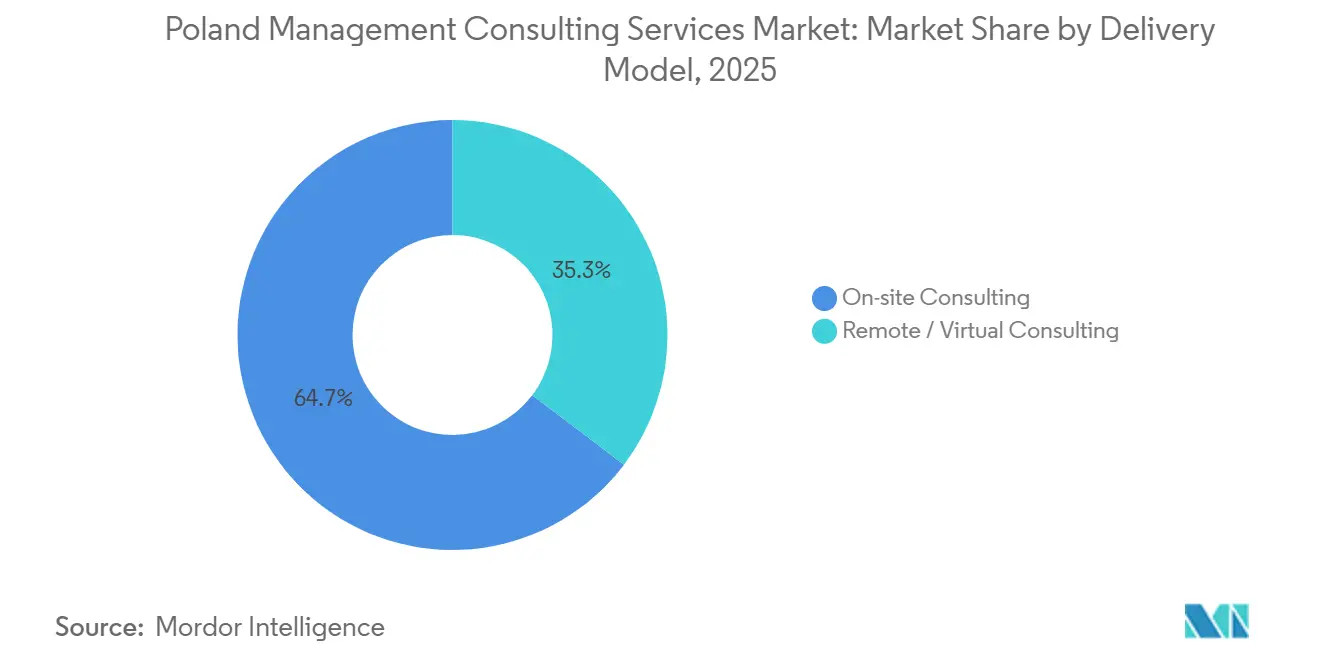

- By delivery model, On-Site Consulting accounted for 53.92% share in 2025, whereas Hybrid Consulting is poised to rise at a 6.43% CAGR as firms blend physical workshops with remote execution.

- By end-user industry, IT and Telecommunications held 22.16% share in 2025, yet Energy and Resources is expected to post the fastest 6.61% CAGR, fueled by Poland’s coal-to-renewables transition.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Poland Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-funded digital-transformation spend surge | +1.3% | National, early focus in Mazowieckie, Małopolskie, Dolnośląskie | Medium term (2-4 years) |

| Escalating demand for cybersecurity and cloud expertise | +1.1% | National, spillover to SSC hubs | Short term (≤ 2 years) |

| Consulting uptake by Poland’s fast-growing SME base | +0.9% | National, higher in Śląskie, Wielkopolskie | Medium term (2-4 years) |

| Public-sector reform projects backed by National Recovery Plan | +0.8% | National, led by central and voivodeship bodies | Long term (≥ 4 years) |

| Near-shoring of Western European SSC and BPO mandates | +0.7% | Mazowieckie, Małopolskie, Dolnośląskie, Pomorskie | Medium term (2-4 years) |

| Mandatory ESG and CSRD disclosure driving sustainability advisory | +0.6% | National, focused on listed entities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU-Funded Digital-Transformation Spend Surge

Poland’s National Recovery Plan channels EUR 59.8 billion (USD 65.2 billion) into broadband, 5G, education digitalization, and cybersecurity projects scheduled through 2026, ensuring a multiyear advisory pipeline.[1]European Commission, “Poland’s National Recovery and Resilience Plan,” commission.europa.eu Disbursements favor consortia that pair global integrators with local specialists, enabling knowledge transfer while meeting domestic-content rules. Asseco and Comarch already secured prime roles in e-government and health-tech programs, accelerating revenue visibility.[2]Asseco Poland S.A., “Financial Results 2025,” asseco.com The European Commission’s approval of Poland’s revised plan in 2024 unfroze funds, compressing engagement cycles as 68% of 2025 allocations flowed to implementation over design. Consulting demand therefore skews toward program management, systems integration, and change management, locking in repeat business through 2027.

Escalating Demand for Cyber-Security and Cloud Expertise

CERT Polska recorded a 34% year-over-year rise in reported cyber incidents in 2024, cementing Poland as Europe’s most targeted nation.[3]CERT Polska, “Cybersecurity Threat Landscape Report 2024,” cert.pl The NIS2 Directive, transposed in February 2026, now covers 18 sectors and fines up to EUR 10 million (USD 11 million) or 2% of global turnover, compelling enterprises to commission gap assessments. Yet only 22% of in-scope entities had completed readiness checks by late 2025, leaving a compliance backlog. Parallel cloud-migration programs gain speed, with Poland’s digital economy projected to reach USD 123 billion by 2030. Advisory firms thus bundle security architecture, zero-trust frameworks, and multi-cloud strategy, but must temper expectations as just 4% of SSC AI pilots have scaled, highlighting execution risks.

Consulting Uptake by Poland’s Fast-Growing SME Base

Poland’s 2.1 million SMEs produced 51.7% of national value added in 2024, yet their consulting spend trails large enterprises threefold.[4]Statistics Poland, “Statistical Yearbook of the Republic of Poland 2024,” stat.gov.pl EU programs such as Digital Europe subsidize up to 85% of eligible digital costs, unlocking accessible project budgets of EUR 15,000-50,000 (USD 16,500-55,000) per engagement. Boutique firms thrive by productizing e-commerce, cloud ERP, and cyber hygiene bundles that fit SME timetables and cash flows. The segment’s projected 6.52% CAGR depends on low-touch sales channels and standardized delivery that sidestep heavy customization. Still, high client churn, 42% within two years, forces firms to build customer-success capabilities to protect recurring revenue streams.

Public-Sector Reform Projects Backed by National Recovery Plan

The plan allocates EUR 6.3 billion (USD 6.9 billion) to modernize public administration and the judiciary, mandating 100% digital public services by 2026.[5]Polish Ministry of Finance, “National Recovery Plan Implementation Dashboard,” gov.pl Projects include integrating 11 legacy case-management systems, training 10,000 judges, and deploying AI chatbots across citizen services, tasks requiring legal, technical, and change-management expertise. Contracts span three to five years and include performance-based fees tied to service uptake, often 15%-20% above commercial day rates. The judiciary module alone is valued at EUR 1.2 billion (USD 1.3 billion), illustrating the scale of opportunity. Political urgency before 2027 elections further accelerates decision cycles, securing long-tail demand for advisory partners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent shortage and wage inflation in consulting workforce | -0.9% | National, acute in Mazowieckie, Małopolskie, Dolnośląskie | Short term (≤ 2 years) |

| Client cost-cutting amid macro volatility | -0.7% | National, sensitive in manufacturing and retail | Short term (≤ 2 years) |

| Commoditization of entry-level consulting services | -0.4% | National, affects tier-2 and tier-3 firms | Medium term (2-4 years) |

| Data-residency rules dampening cross-border virtual delivery | -0.3% | National, impacts EU engagements | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Talent Shortage and Wage Inflation in Consulting Workforce

Senior-consultant wages rose 12% in cybersecurity and 10% in digital transformation during 2025, outpacing the 7.3% professional-services average. Poland’s 525,000-strong IT talent pool must now serve consulting, product development, and SSC sectors simultaneously, fueling bidding wars that erode margins. Retention is fragile as fintech and e-commerce firms entice staff with equity packages absent in traditional partnership tracks.[6]Statistics Poland, “Statistical Yearbook of the Republic of Poland 2024,” stat.gov.pl, Association of Business Service Leaders, “Business Services Sector in Poland 2025,” absl.pl Firms respond by near-shoring analytics work to Ukraine and Romania, automating delivery with AI tools, and acquiring boutiques to lock in scarce skill sets, though each tactic introduces its own execution risks.

Client Cost-Cutting Amid Macro Volatility

Poland’s GDP growth cooled to 2.9% in 2025, while inflation still averaged 6.2%, prompting enterprises to scrutinize discretionary consulting spend. Manufacturing clients deferred non-essential projects as export orders to Germany fell 6%, and retail operators renegotiated hourly rates into fixed-price contracts that shift delivery risk. To sustain pipelines, firms now pitch ROI-tied pricing, bundle advisory with managed services, and automate project tracking, but those adjustments require up-front tooling investments that strain smaller balance sheets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Digital Execution Becomes the Center of Gravity

Strategy Consulting captured 31.47% of the Poland management consulting services market share in 2025, mirroring its role as the entry point for C-suite relationships. Advisory teams commanded EUR 2,500-4,000 (USD 2,725-4,360) day rates, almost double operations-focused work. Digital Transformation Consulting is forecast to add 6.78% CAGR to the Poland management consulting services market size through 2031, propelled by cloud migration, AI rollouts, and cybersecurity mandates. Operations Consulting remains essential for manufacturers adjusting supply chains toward near-shoring, while Risk and Compliance Consulting expands on the back of NIS2 and CSRD obligations. HR Consulting and Financial Advisory round out service portfolios, supporting tight labor markets and active M&A pipelines.

Growth momentum comes from Poland’s digital economy expanding at 12% annually, triple headline GDP, which guarantees a steady queue of execution projects. Enterprises now expect advisors to carry accountability beyond slideware, pushing firms to deepen implementation skill sets. Software vendors bundling configuration support into license fees threaten commoditization, so consultants differentiate through change-management depth and sector knowledge. As segments converge, hybrid teams that pair strategy specialists with technologists gain favor, raising utilization rates and cross-selling opportunities across the Poland management consulting services market.

By Organization Size: SMEs Close the Advisory Gap

Large Enterprises delivered 61.83% of revenue for the Poland management consulting services market in 2025, purchasing multi-year programs that span strategy through managed services. Procurement consolidation means two or three integrators often win master service agreements, locking in big-ticket pipeline visibility. Smaller companies, however, gained momentum as public subsidies lowered entry barriers, and they now represent the fastest expansion vector for the Poland management consulting services market size, advancing at a 6.52% CAGR.

SMEs engage for discrete projects averaging EUR 25,000-75,000 (USD 27,250-81,900), typically around e-commerce enablement, cloud ERP adoption, and baseline cyber hygiene. Government co-financing covers up to 85% of eligible costs, transforming perceived advisory luxuries into affordable performance levers. Yet client churn reaches 42% within two years, so consultants invest in self-service onboarding portals and post-go-live support to defend renewal revenue. High volume compensates for smaller ticket values, anchoring predictable growth for boutique players across the Poland management consulting services market.

By Delivery Model: Hybrid Becomes the New Normal

On-Site engagements retained 53.92% share in 2025, chiefly in public sector, finance, and healthcare where executives prize physical presence for sensitive data access. Travel restrictions eased, but rising costs and ESG awareness continue to drive interest in mixed models. Consequently, Hybrid Consulting is projected to grow 6.43% CAGR, steadily enlarging its slice of the Poland management consulting services market share through 2031.

Hybrid arrangements trim travel expense by 30%-40% and widen the talent funnel beyond Warsaw and Kraków, crucial when vacancy rates top 12% for senior technology roles. Consultants conduct design sprints on site, then shift analytics, documentation, and PMO tasks to remote squads using collaboration suites. Productivity dips 20% in early transition phases, yet recuperates once communication protocols settle. Clients now write hybrid delivery clauses directly into RFPs, signaling durable change in buying behavior throughout the Poland management consulting services market.

By End-User Industry: Energy and Resources Surges on the Coal-to-Renewables Pivot

IT and Telecommunications remained the single largest buyer group at 22.16% of 2025 revenue, driven by 5G deployment and rising cyber risk. Energy and Resources, however, is forecast to post the strongest 6.61% CAGR, underpinned by Poland’s goal to lower coal’s generation share from 70% in 2024 to 30% by 2030. This shift positions the vertical as a heavyweight contributor to the Poland management consulting services market size expansion.

Utility operators need road maps for offshore wind, solar PV, and grid digitalization, tasks that fuse engineering, regulatory, and financing skill sets. Advisory budgets increase further once construction starts, offering multi-year revenue visibility. Manufacturing, retail, and healthcare continue to demand Industry 4.0, omnichannel, and telehealth solutions, though spending patterns remain sensitive to macro swings. Collectively, vertical diversity insulates overall growth prospects for the Poland management consulting services market.

Geography Analysis

Mazowieckie, anchored by Warsaw, supplied roughly 42% of 2025 consulting turnover, making it the dominant regional nucleus inside the Poland management consulting services market. The city hosts 1,200 service centers, employs 180,000 SSC workers, and concentrates 85% of Fortune 500 subsidiaries, pushing average project values 30% above the national mean.

Małopolskie, centered on Kraków, contributed about 18% and specializes in technology and operations projects thanks to a deep academic pipeline of 35,000 graduates each year. Dolnośląskie and its capital Wrocław captured 12%, leveraging automotive and electronics clusters plus proximity to German supply chains. Pomorskie and Wielkopolskie together added close to 15%, with port logistics, offshore wind, and food processing sustaining steady advisory demand.

The remaining 13% dispersed across Śląskie, Łódzkie, and Podkarpackie, where hybrid delivery lets Warsaw partners serve emerging hubs without brick-and-mortar footprints. Talent scarcity tightens hardest in Mazowieckie, where cyber and AI wages run 40% higher than in Kraków, eroding margins if delivery cannot be off-shored. As remote norms stick, geographic revenue concentration is expected to flatten, diversifying growth pockets across the Poland management consulting services market.

Competitive Landscape

The top 10 players held an estimated 48% stake in the Poland management consulting services market in 2025, indicating moderate fragmentation. Accenture, Deloitte, PwC, KPMG, and EY anchor the large-enterprise and public-sector space on the strength of recognized brands and global delivery capacity.

Strategy specialists McKinsey, BCG, and Bain remain the go-to partners for high-stakes boardroom topics, yet their Poland teams are relatively lean, which elevates fee pressures on mid-sized deals. Local champions Asseco, Comarch, MDDP, and Grant Thornton Poland monetize deep regulatory insight and Polish-language fluency, often edging out multinationals on SME and government bids. Technology vendors such as Microsoft and SAP blur boundaries by wrapping consulting into software agreements, intensifying rivalry inside the Poland management consulting services market.

Emergent AI-native boutiques pitch algorithmic strategy formulation at 70% lower price points, although take-up is limited to early adopters willing to tolerate lower touch. Wage inflation above 10% pushes all providers to automate delivery through proprietary platforms like Deloitte’s GreenLight and PwC’s Digital Fitness, further widening the gap between firms able to fund R&D and those forced to rely on staff leverage alone. Offshore centers in India and the Philippines court Polish buyers with 50% discount rates, adding pricing tension and urging domestic firms to focus on value-add niches to defend their share of the Poland management consulting services market.

Poland Management Consulting Services Industry Leaders

Accenture plc

Deloitte Touche Tohmatsu Limited

PricewaterhouseCoopers LLP

KPMG International Limited

Ernst & Young Global Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Poland enacted the NIS2 Directive, triggering a 40% jump in cybersecurity RFP volume during Q1 2026.

- January 2026: The European Commission approved the Omnibus I package, cutting CSRD scope by 80% and reshaping ESG advisory demand.

- November 2025: Deloitte Poland began a EUR 12 million (USD 13.1 million) program to train 10 000 public-sector employees in cybersecurity through 2027.

- September 2025: PwC Poland introduced its Digital Fitness App, cutting diagnostic project duration by 35%.

Poland Management Consulting Services Market Report Scope

The Belgium Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current size of the Poland management consulting services market?

The market stands at USD 2.59 billion in 2026 and is projected to reach USD 3.5 billion by 2031.

Which consulting segment is growing the fastest?

Digital Transformation Consulting is forecast to grow at 6.78% CAGR, reflecting enterprises' shift from strategic planning to hands-on execution.

How will hybrid delivery models affect project pricing?

Hybrid setups cut travel costs by up to 40% and allow firms to tap broader talent pools, but they require upfront investment in collaboration tools and process standardization.

What role do SMEs play in future demand?

EU co-financing and productized service bundles are pushing SME consulting revenues to grow at a 6.52% CAGR, narrowing the gap with large-enterprise spending.

Which industry vertical offers the strongest growth outlook?

Energy and Resources leads with a projected 6.61% CAGR as Poland accelerates its coal-to-renewables transition.

How severe is the talent shortage for consulting firms?

Senior-level wage inflation reached 12% in cybersecurity and 10% in digital transformation during 2025, with vacancy rates climbing above 12% in key urban hubs.

Page last updated on: