Slovak Republic Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

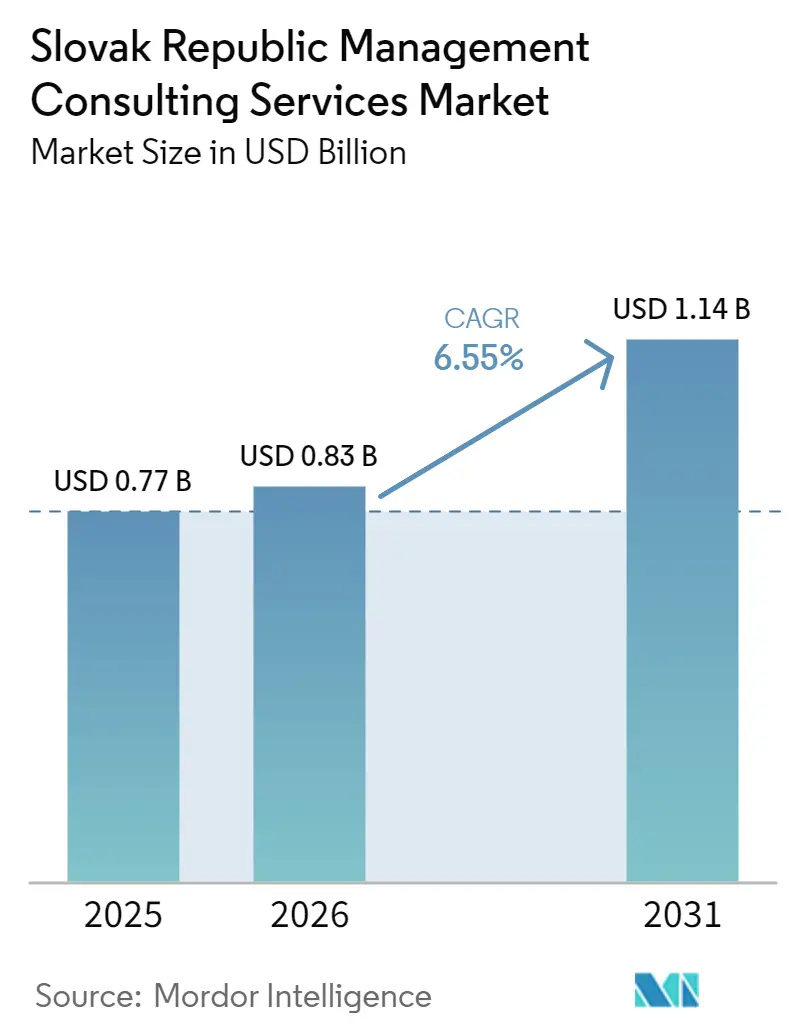

| Base Year Market Size (2025) | USD 0.77 Billion |

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.14 Billion |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Slovak Republic Management Consulting Services Market Analysis by Mordor Intelligence

The Slovak Republic management consulting services market size is expected to grow from USD 0.83 billion in 2026 to reach USD 1.14 billion by 2031, expanding at a CAGR of 6.55% from 2026 to 2031. Robust demand stems from accelerating digital-government programs, tighter EU compliance mandates, and large-scale automotive electrification projects. Advisory firms now serve as the connective tissue between multilayered EU funding instruments and local execution capacity, moving the market beyond its historical cost-optimization focus. Competitive intensity is rising as Big Tech-backed managed-service players introduce outcome-linked pricing, prompting traditional consultancies to defend share by deepening regulatory strategy and M&A offerings. Meanwhile, the public sector’s shift toward AI-enabled citizen services under the National Informatization Concept is anchoring a multi-year consulting pipeline that cushions the industry against cyclical slowdowns.Policy tailwinds outweigh near-term headwinds. On balance, structural demand drivers outweigh restraints, positioning the Slovak Republic management consulting services market for sustained mid-single-digit expansion through the end of the decade.

Key Report Takeaways

- By consulting service line, strategy consulting led with 27.96% revenue share in 2025 while risk and compliance consulting is projected to deliver the fastest 7.09% CAGR through 2031.

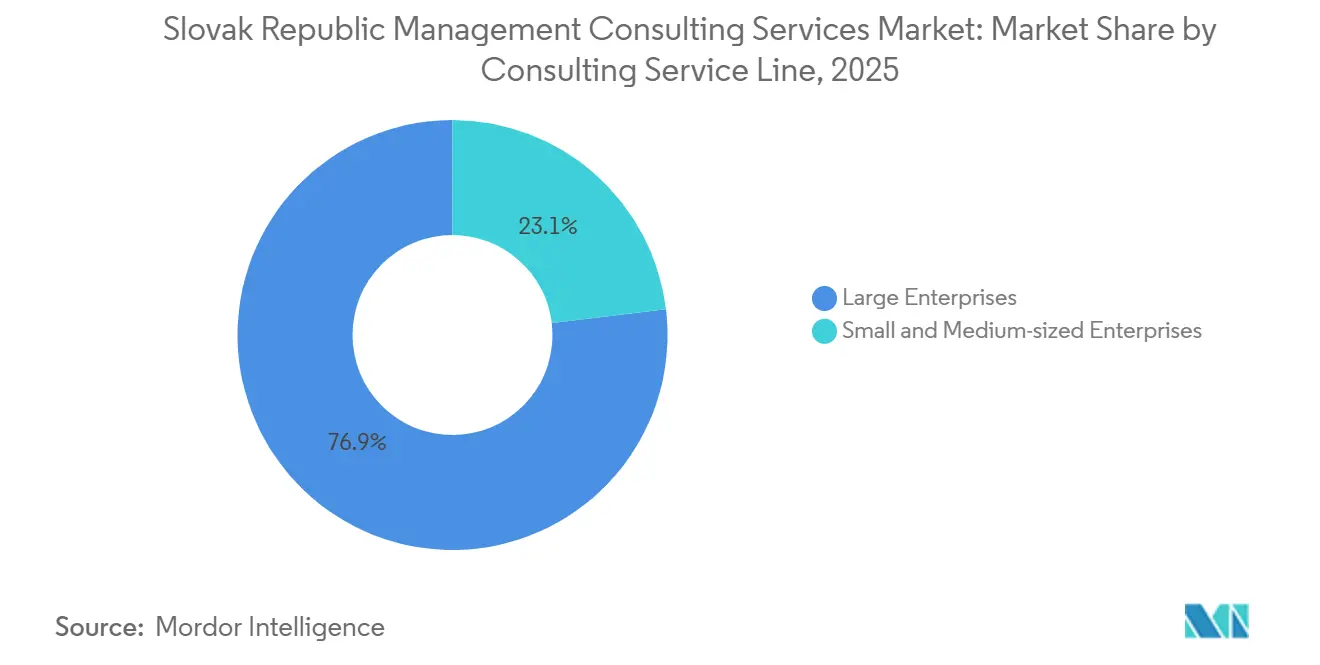

- By organization size, large enterprises accounted for 62.88% of spending in 2025, whereas small and medium-sized enterprises are poised for a 6.67% CAGR over 2026-2031.

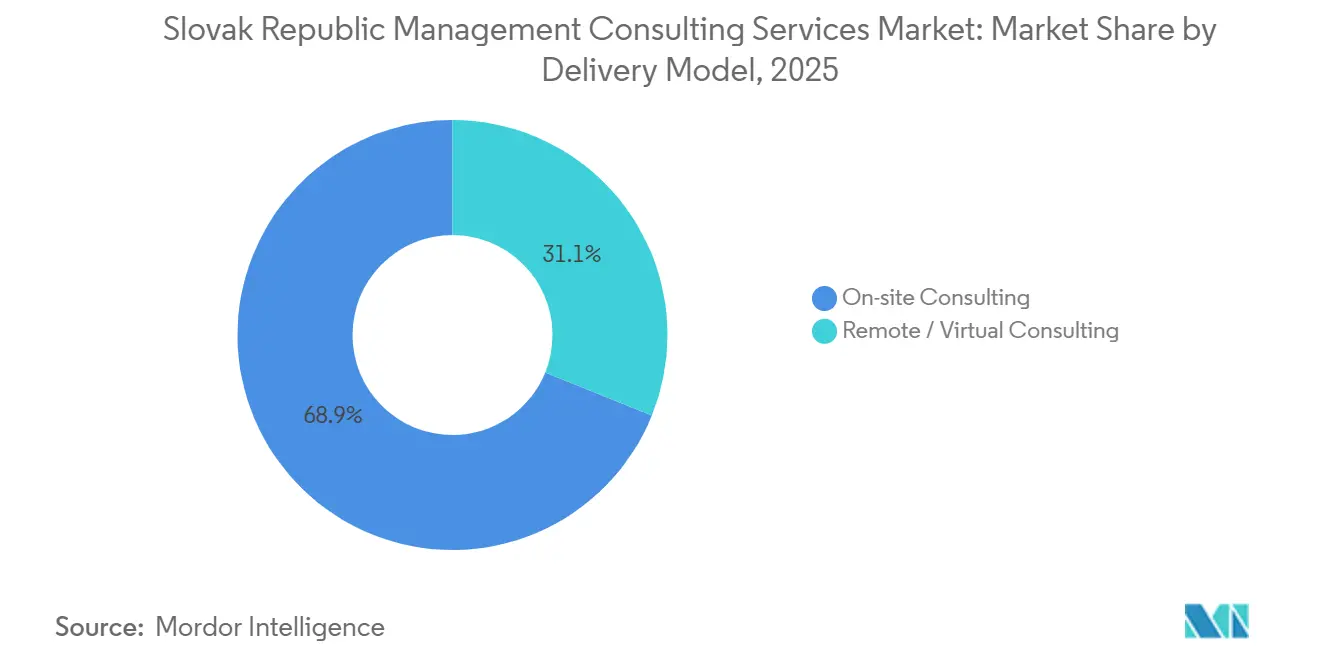

- By delivery model, on-site consulting held 54.93% share in 2025, yet remote and virtual consulting is forecast to grow at a 6.93% CAGR during the same horizon.

- By end-user industry, IT and telecommunications dominated with 22.14% share in 2025, while the public sector is set to record the highest 6.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Slovak Republic Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Digital-Transformation Spending | +1.8% | National, concentrated in Bratislava and Košice | Medium term (2-4 years) |

| EU Structural-Fund Modernization Programs | +1.5% | National, priority regions Upper Nitra, Košice, Banská Bystrica | Long term (≥ 4 years) |

| Near-Shoring Inflows From DACH Manufacturers | +1.2% | Western Slovakia, notably Bratislava, Trnava, Nitra | Medium term (2-4 years) |

| Heightened Cybersecurity and Data Compliance | +1.0% | National, essential and important entities across all sectors | Short term (≤ 2 years) |

| AI-Driven Process Automation in Government | +0.7% | National, pilot deployments in Bratislava ministries | Medium term (2-4 years) |

| Green Supply-Chain Advisory Under EU Green Deal | +0.6% | National, automotive and heavy-industry clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Digital-Transformation Spending

The National Digital Decade Strategic Roadmap earmarks EUR 2.3 billion (USD 2.4 billion) for digital priorities, creating durable pipelines for SME digitalization programs, broadband roll-outs, and data-governance frameworks. Mandatory open-API policies shift consulting value from proprietary system integration to interoperability design, favoring firms with data-architecture skills. January 2025 cyberattacks on the land registry and health insurer fast-tracked resilience budgets, and with 49.5% of SMEs lacking cybersecurity plans, incident-response retainers are in high demand. Because ministries must deliver IT Development Concepts through 2030, this driver sustains revenue beyond initial strategy phases into execution and monitoring.

EU Structural-Fund Modernization Programs

The Recovery and Resilience Plan directs EUR 6.4 billion (USD 6.72 billion) into Slovakia, of which EUR 1.2 billion (USD 1.26 billion) targets digital transformation, while Program Slovensko 2021-2027 allocates EUR 12.6 billion (USD 13.3 billion) to cohesion goals.[1]European Commission, “European Structural and Investment Funds,” europa.eu Strict state-aid and milestone rules overwhelm municipal and SME capacity, spawning engagements in grant writing, feasibility studies, and blended-finance structuring. The industrial decarbonization scheme alone channels EUR 357 million (USD 374 million) toward 1.2 million tCO₂ reductions, demanding bottom-up emissions inventories and EU Taxonomy alignment. Because cohesion cycles run to 2027 and audits extend afterward, consulting demand endures well into the next decade.

Near-Shoring Inflows From DACH Manufacturers

Automotive OEMs produced about 1 million vehicles in 2022, 50.3% of industrial output, and new state aid of EUR 1.8 billion (USD 1.89 billion) since 2023 backs 10 battery projects.[2]Ministry of Economy of the Slovak Republic, “Government Focuses on Five Key Areas to Support the Automotive Industry,” economy.gov.sk German-speaking manufacturers relocating capacity to Slovakia need localization roadmaps, supplier mapping, and workforce-reskilling programs. The government’s July 2025 five-priority framework on decarbonization and autonomous-vehicle regulation amplifies advisory opportunities, especially in Bratislava, Trnava, and Nitra where clusters are dense.

Heightened Cybersecurity and Data Compliance

Cyber Security Act 366/2024, effective January 2025, mandates external audits every two years and fines up to EUR 10 million (USD 10.5 million) or 2% of turnover. Concurrent GDPR enforcement and a pending AI governance bill introduce multi-layered obligations, forcing mid-sized manufacturers and utilities to outsource risk assessments, data-protection impact analysis, and post-market monitoring. Short implementation deadlines translate into near-term revenue spikes for compliance specialists.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent Shortage and Wage Inflation | -0.9% | National, acute in Bratislava and Košice tech hubs | Short term (≤ 2 years) |

| SME Cost Sensitivity Amid Inflation | -0.6% | National, rural and peripheral regions | Medium term (2-4 years) |

| Outcome-Linked Fees Compress Billable Hours | -0.4% | National, chiefly large-enterprise projects | Medium term (2-4 years) |

| Competition From Big-Tech Entrants | -0.3% | National, multinational client base centered Bratislava | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Talent Shortage and Wage Inflation

ICT specialists form only 4.2% of Slovak employment versus the 4.8% EU average, and just 15% of firms provide ICT training.[3]U.S. International Trade Administration, “Slovakia - Digital Economy,” trade.gov Automotive OEMs absorb 176,000 workers, intensifying the race for bilingual analysts. Brain drain to DACH markets inflates wages, eroding consulting margins. Although a national MOOC on AI aims to expand skills, relief will not materialize before 2027, sustaining short-term delivery bottlenecks.

SME Cost Sensitivity Amid Inflation

Projected 3.4% inflation in 2026 squeezes SME budgets.[4]International Monetary Fund, “World Economic Outlook Database,” imf.org Clients push for fixed-price or outcome-linked fees, transferring performance risk to advisors. Slow EU-fund disbursement further strains cash flow, compelling consultancies to extend payment terms. These pressures will persist until inflation moderates and Social Climate Fund disbursements begin to lift liquidity post-2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Compliance Complexity Drives Risk Advisory Surge

Strategy consulting retained 27.96% of the Slovak Republic management consulting services market share in 2025 as automotive multinationals mapped electrification roadmaps, localized supply chains, and met EU Green Deal targets. Risk and compliance consulting, however, is projected to post the fastest 7.09% CAGR through 2031 as NIS2 audits, GDPR enforcement, and the forthcoming AI governance bill layer new obligations on mid-tier manufacturers and utilities. Demand for conformity assessments, technical-documentation support, and post-market monitoring has already doubled intake at the Big Four’s dedicated cyber-risk units since early 2025. Operations consulting benefits from automotive plants shifting to circular-economy models under the government’s five-priority framework, while HR practices focus on reskilling 128,000 assembly workers for battery-electric production. Digital transformation teams handle open-API architecture and cloud migrations mandated by the National Informatization Concept, and financial advisory units see a steady stream of M&A due-diligence mandates linked to logistics and retail consolidation.

The Slovak Republic management consulting services market size dynamics within this segment hinge on enforcement vigor. Should the National Security Authority levy the maximum EUR 10 million (USD 10.5 million) fines allowed under the Cyber Security Act, compliance-driven spend could widen the segment’s revenue gap versus traditional strategy engagements. Conversely, lenient oversight may delay SME investment until the next regulatory wave. Mid-tier firms such as BDO and Grant Thornton are carving out niches in grant-monitoring services for EU-funded projects, expanding competitive pressure below the Big Four’s fee bands. Technology integrators like Unicorn Systems bundle consulting with implementation, shortening project cycles and compressing billable hours for pure-play advisors, yet client preference for independence in regulator-facing work keeps premium pricing intact for risk specialists.

By Organization Size: SME Awakening to EU-Fund Complexity

Large enterprises captured 62.88% of 2025 spending as automotive OEMs and nationwide banks commissioned multi-year cloud migrations and AI customer-care platforms. These buyers now press for outcome-linked fee models that shift performance risk to consultants, mirroring Accenture’s 25% cost-reduction guarantee for Škoda Auto’s multilingual service bot. Small and medium-sized enterprises are nonetheless slated for a 6.67% CAGR through 2031 because structural-fund rules overwhelm in-house capacity; every milestone-based disbursement under Program Slovensko 2021-2027 requires exhaustive compliance files, audit trails, and state-aid opinions.

Within the broad Slovak Republic management consulting services market, SME clients are gravitating toward regional advisers fluent in Slovak procurement law and EU taxonomy jargon, accepting remote delivery as long as deadlines and audit checkpoints are met. Payment-timing risk remains material because fund releases lag expenses, but consultancies mitigate exposure through phased invoicing tied to European Commission approvals. The Social Climate Fund’s EUR 1.5 billion (USD 1.575 billion) allocation from 2027 will further expand the addressable base by underwriting municipal energy-poverty projects that require feasibility and monitoring studies. Talent scarcity still favors large firms able to import specialists from regional hubs, yet remote collaboration tools are narrowing that edge, empowering boutique outfits to bid competitively on grant-compliance assignments in peripheral regions.

By Delivery Model: Remote Gains Traction Through API-Economy Push

On-site engagements held 54.93% of 2025 revenue because factory-floor process redesign and ministerial change-management workshops still rely on face-to-face interaction. Nonetheless, remote and virtual consulting should expand at a 6.93% CAGR to 2031 as ministries expose datasets via open APIs and cloud platforms, enabling distributed advisor teams to plug directly into government sandboxes.[5]Ministerstvo Investícií Regionálneho Rozvoja A Informatizácie SR, “Vláda Slovenskej Republiky Schválila Národnú Koncepciu Informatizácie Verejnej Správy,” mirri.gov.sk Hybrid models split stakeholder workshops into periodic on-site sessions while technical work,code review, data governance, grant-dashboard builds, runs virtually, cutting travel costs by almost 40% according to BearingPoint project audits.

Cost-conscious SMEs now request remote-first proposals as default, a trend that could lower entry barriers for cross-border advisers fluent in Slovak. The shift also allows the Slovak Republic management consulting services market to tap specialized expertise from Prague or Vienna without residency hurdles, widening talent supply. Big Tech entrants reinforce the model by bundling managed-service SLAs with evergreen platform subscriptions, effectively converting traditional projects into annuity-like service contracts. Cultural expectations around in-person governance meetings will keep on-site share above 45% through the forecast window, yet the faster growth of virtual delivery underscores a structural change in utilization management and margin mathematics.

By End User Industry: Public Sector Emerges as Growth Engine

IT and telecommunications led with 22.14% of 2025 revenue as operators rolled out 5G and supercomputer PERUN, but the public sector is poised for a 6.78% CAGR through 2031 on the back of a EUR 2.3 billion (USD 2.4 billion) digital-government budget plus the EUR 17.87 million (USD 18.76 million) InnovAIte Slovakia AI program.[6]Výskumno-Inovačný Portál, “InnovAIte Slovakia,” vvi.gov.sk Ministries require ethics frameworks, procurement blueprints, and change-management roadmaps before deploying the 12 AI life-situation assistants promised under the National Informatization Concept. Manufacturing remains a durable second pillar as Volvo readies 250,000-unit EV output from 2026 and battery supply chains absorb EUR 1.8 billion (USD 1.89 billion) in fresh investment commitments.

Energy, resources, and healthcare engagements layer additional opportunity. The updated National Energy and Climate Plan demands EUR 11.8 billion (USD 12.39 billion) in incremental investment, driving decarbonization feasibility studies and financing-strategy mandates. Hospitals contract advisors to extend e-prescription rollouts and refine diagnosis-related-group costing. Banking digital-core upgrades, as seen in the EUR 2.19 million (USD 2.30 million) Slovenská záručná a rozvojová banka project, prove that even mid-tier lenders will spend when cost-benefit is explicit. Across sectors, outcome-linked models that guarantee KPI delivery are proliferating, encouraging clients to shift risk while presenting consultants with both upside and margin compression.

Geography Analysis

Bratislava anchors demand because it hosts the seat of government, the largest concentration of ICT talent, and most multinational headquarters, accounting for well over half of Slovak Republic management consulting services market revenue in 2025. Proximity to ministries gives the capital a lock on digital-government and compliance engagements, and PwC’s Intelligent Processing Centre plus KPMG’s 500-strong staff underline its magnet effect. Western regions, Trnava and Nitra, benefit from clustered automotive OEM plants that require localization strategies and decarbonization roadmaps as state aid tops EUR 885.1 million (USD 926 million), reinforcing strong local utilization of strategy and operations specialists.

Košice is emerging as the secondary consulting hub on the back of the PERUN supercomputer contract, a vibrant university pipeline, and logistics real-estate deals that Kinstellar advised in 2025. Consulting firms are staffing digital-delivery pods in the city to capitalize on lower wage levels while serving eastern-region clients remotely. Peripheral coal-transition areas, Upper Nitra, Banská Bystrica, draw EU Just Transition funds for clean-energy roadmaps and social-resilience programs, creating niche opportunities for boutiques versed in EU taxonomy and stakeholder engagement. Here, bilingual advisors leverage virtual workshops to cut travel overhead, extending the Slovak Republic management consulting services market size benefits into regions historically underserved.

Rural broadband gaps and limited charging infrastructure still restrain complex digital projects in the east and center, but the Recovery and Resilience Plan’s commitment to 3,000 new charging points and expanded VHCN coverage will incrementally unlock advisory scope. As ministries expose datasets via open APIs, regional municipalities can source remote expertise, reducing Bratislava’s historical advantage and distributing fee pools more evenly. Consultancies that open satellite offices or partner with local universities stand to capture first-mover benefits as structural funds flow into sub-national programs through 2031.

Competitive Landscape

The Slovak Republic management consulting services market is moderately concentrated, with the Big Four retaining a combined majority share yet facing a growing slate of challengers. PwC Slovakia ranks first by revenue and leverages its Intelligent Processing Centre in Bratislava to automate document workflows for cross-border clients, trimming average project cycles by nearly 15 percent. KPMG Slovakia expanded partnership ranks in October 2025 and now fields more than 500 professionals, allowing the firm to spin up multidisciplinary squads on short notice for biennial NIS2 audits. Deloitte Advisory has redirected its analytics hub toward public-sector AI governance work, chasing a surge of ministries that need post-market monitoring dashboards before the Draft AI Act comes into force. EY Slovakia, with offices in Bratislava, Košice, and Žilina, differentiates through Slovak-language tax-incentive toolkits that resonate with near-shoring German manufacturers.

New entrants are compressing margins in routine advisory. IBM Consulting and Capgemini Slovakia pitch outcome-linked managed services that convert traditional projects into multi-year platform subscriptions, undercutting classic time-and-materials rates by as much as 20 percent. Accenture’s AI customer-care deployment for Škoda Auto, which automated up to 40 percent of multilingual queries, exemplifies how technology incumbents pivot from labor arbitrage to results guarantees. BearingPoint exported its BeMind AI accelerators into the Slovak market during 2025 pilot projects, reporting productivity lifts of roughly one-third and foreshadowing wider use of generative AI code assistants across delivery stacks. Mid-tier players such as BDO Advisory, Grant Thornton, and Mazars target cost-sensitive SMEs that still require stringent EU-fund compliance but cannot absorb Big Four pricing.

Domestic IT integrators are also climbing the value chain. Unicorn Systems, Itera Slovakia, and Eset Services combine consulting with proprietary cybersecurity or middleware platforms, capturing share in open-API architecture projects mandated by the National Informatization Concept. Local boutiques strengthen their competitive posture by offering bilingual teams and deep ties to regional development agencies administering Just Transition and Social Climate funds. As a result, pure-play consultancy success increasingly hinges on specialization in high-stakes mandates, regulatory sandboxes, M&A due diligence, or Green-Deal decarbonization strategies, where institutional trust and Slovak legislative fluency remain decisive advantages. Over the forecast window, technology-enabled delivery and risk-sharing fee structures are expected to reallocate roughly one-quarter of total billable hours toward platform-based contracts, gradually redefining the competitive frontier.

Slovak Republic Management Consulting Services Industry Leaders

PricewaterhouseCoopers Slovensko, s.r.o.

Deloitte Advisory, s.r.o.

KPMG Slovensko, spol. s r.o.

Ernst & Young Slovakia, spol. s r.o.

Accenture, s.r.o.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The Ministry of Justice unveiled the AI Slov-Lex modernization, a five-module suite designed to augment legal research and drafting, opening procurement lanes for ethics and change-management consulting.

- March 2026: Law firm Čechová and Partners promoted Miroslav Zaťko to partner amid rising cross-border M&A activity.

- December 2025: The government approved the National Informatization Concept for 2026-2030, committing to 12 AI life-situation assistants and mandating IT Development Concepts in every ministry.

- November 2025: Kinstellar advised P3 Logistic Parks on a logistics-asset acquisition, highlighting sustained warehousing consolidation.

Slovak Republic Management Consulting Services Market Report Scope

The Slovak Republic Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the projected value of the Slovak Republic management consulting services market in 2031?

The market is forecast to reach USD 1.14 billion by 2031, growing at a 6.55% CAGR from 2026.

Which consulting service line is expected to grow fastest through 2031?

Risk and compliance consulting is projected to register the highest 7.09% CAGR as new EU mandates tighten audit requirements.

Why are small and medium-sized enterprises increasing their consulting spend?

Complex EU structural-fund rules and milestone-based disbursements exceed in-house capabilities, pushing SMEs to hire advisors for grant writing and compliance monitoring.

How is remote delivery altering project economics?

Ministries opening APIs allow consultants to perform data-architecture and monitoring tasks virtually, trimming travel costs and expanding the talent pool available to Slovak clients.

Which geographic regions outside Bratislava will see the fastest consulting growth?

Koice, Upper Nitra, and Banská Bystrica are set to benefit from supercomputer projects and Just Transition funding streams, driving double-digit consulting demand in those areas.

What fee models are gaining traction among large enterprises?

Outcome-linked contracts that tie advisory compensation to measurable cost savings or KPIs are expanding, especially in AI customer-care and process-automation engagements.

Page last updated on: