Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Sweden Data Center Server Market Report Segments the Industry Into Type (Tier 1, Tier 2, and More), Form Factor(Half-Height Blades, Full-Height Blades, and More), End-User Verticals (BFSI, Manufacturing, and More), Data Center Type(Hyperscalers/Cloud Service Provider, and More) and by Application / Workload (Virtualisation and Private Cloud, Storage-Centric and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

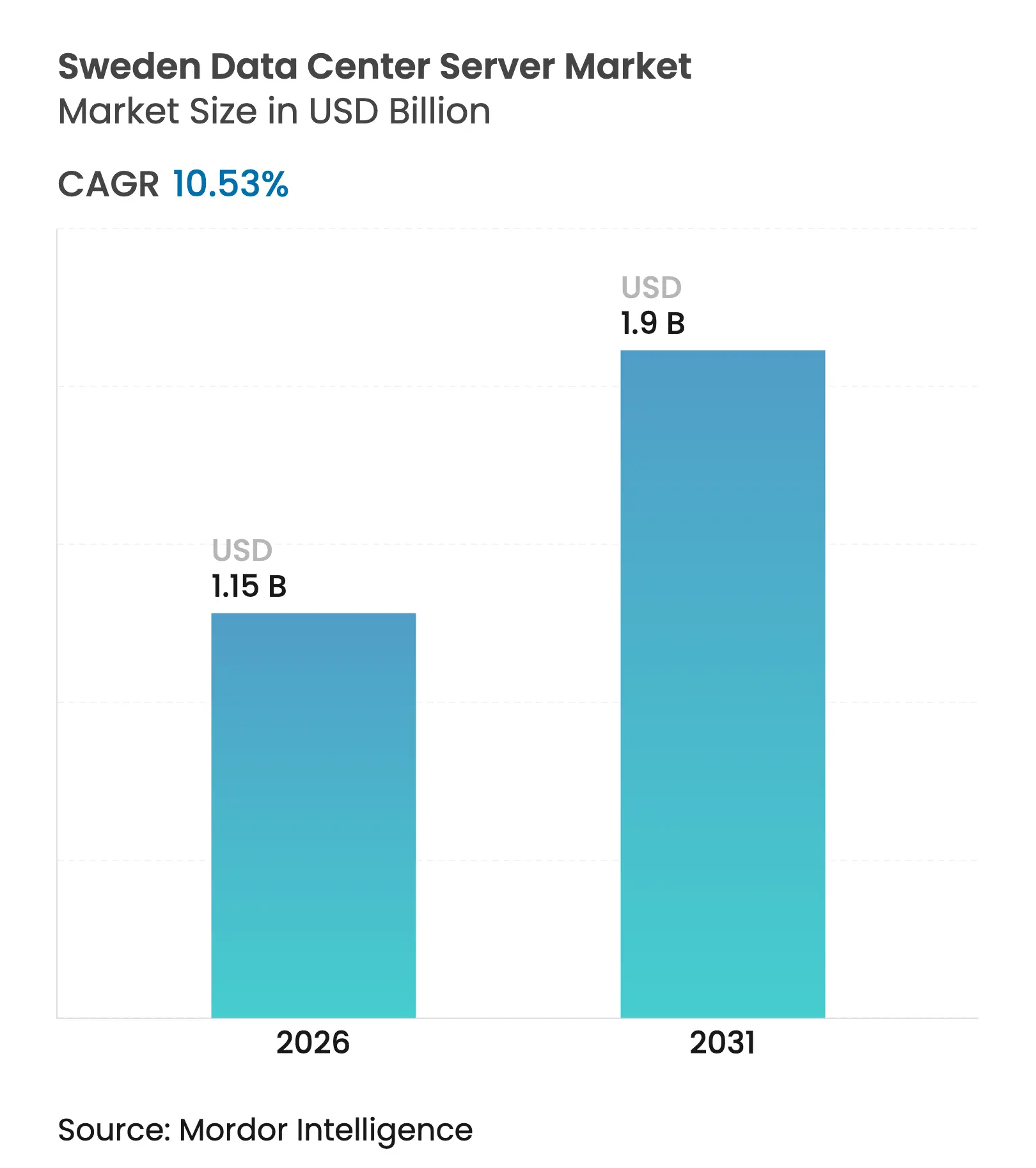

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 1.9 Billion |

| Growth Rate (2026 - 2031) | 10.53 % CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Sweden data center server market size was valued at USD 1.04 billion in 2025 and estimated to grow from USD 1.15 billion in 2026 to reach USD 1.9 billion by 2031, at a CAGR of 10.53% during the forecast period (2026-2031). Persistent hyperscale capital outlays, an ample supply of low-carbon hydro-power, and a cool climate that reduces cooling loads position Sweden as the Nordic anchor for next-generation data center infrastructure. International cloud providers are scaling local server fleets to support AI workloads, while domestic operators focus on energy-efficient designs to comply with the nation’s 2045 net-zero mandate. High-density GPU deployments are accelerating demand for advanced thermal management, and sustained 5G roll-outs are shifting procurement toward compact edge-ready form factors. At the same time, policy changes—such as removal of electricity tax incentives—have heightened the importance of CapEx discipline, prompting strategic partnerships and consolidation among local players.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Construction boom of hyperscale and colocation

facilities Construction boom of hyperscale and colocation

facilities | +2.8% | National, concentrated in Stockholm and Gothenburg regions | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+2.8%

|

Geographic Relevance

:

National, concentrated in Stockholm and Gothenburg

regions

|

Impact Timeline

:

Medium term (2-4 years)

|

Accelerated cloud and IoT adoption among Swedish

enterprises Accelerated cloud and IoT adoption among Swedish

enterprises | +2.1% | National, with higher penetration in urban centers | Short term (≤ 2 years) | |||

5G-enabled edge workload proliferation

5G-enabled edge workload proliferation

| +1.7% | National, prioritizing industrial corridors | Medium term (2-4 years) | |||

National sustainability mandates favouring

energy-efficient servers

National sustainability mandates favouring

energy-efficient servers

| +1.4% | National, aligned with 2045 climate neutrality goals | Long term (≥ 4 years) | |||

Abundant hydro-power lowering PUE and TCO Abundant hydro-power lowering PUE and TCO | +1.2% | Northern Sweden, leveraging renewable energy clusters | Long term (≥ 4 years) | |||

Server-hardware tax rebate (Data Centre Tax Relief

2024)

Server-hardware tax rebate (Data Centre Tax Relief

2024)

| +0.8% | National, subject to policy continuity | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Construction Boom of Hyperscale and Colocation Facilities

Mega-projects such as EcoDataCenter’s 240–360 MW Borlänge campus and CoreWeave’s USD 2.2 billion Swedish facility illustrate how unprecedented capital flows are reshaping server demand toward GPU-dense architectures suited for AI training at scale.[1]CoreWeave Press, “CoreWeave announces USD 2.2 billion European expansion anchored in Sweden,” coreweave.com The pipeline now exceeds 500 MW of announced capacity, with financing instruments—like Areim’s EUR 450 million sustainability-focused fund—ensuring build-outs remain on track despite higher construction costs. Operators are pairing high-density racks with liquid-ready designs to future-proof against 800 W GPUs. As campuses come online, Sweden's data center server market procurement volumes are set to surge, particularly for Tier 4-compliant systems demanded by banks and public agencies.

Accelerated Cloud and IoT Adoption Among Swedish Enterprises

More than half of Swedish enterprise workloads already reside off-premises, and government digitalization programs are reinforcing momentum by tying EUR 40 billion in economic value to cloud uptake. Manufacturing and utilities use-cases under the Industry 4.0 umbrella rely on edge gateways that preprocess sensor data before forwarding to centralized clusters. Consortia such as Ericsson-AstraZeneca-SAAB are adding new server classes that blend ruggedized chassis with high-bandwidth fabrics to meet deterministic latency needs. Together these shifts underpin a steady move toward hybrid architectures that bolster server refresh cycles every three years, placing sustained upward pressure on the Sweden data center server market.

5G-Enabled Edge Workload Proliferation

With nationwide 5G coverage and initiatives like Telenor’s 5G Solutions Lab, industrial players can place micro-data centers within factories, ports, and mines to run AI inference locally. Edge deployments require quarter-height blades and all-in-one enclosures capable of operating in constrained thermal envelopes, a configuration that favors Swedish suppliers proficient in ruggedization. The addressable footprint for edge nodes is predicted to double by 2027, meaning a growing share of Sweden data center server market shipments will target distributed sites rather than central campuses.

National Sustainability Mandates Favouring Energy-Efficient Servers

Climate neutrality legislation compels operators to publish power and water metrics annually, directing procurement toward servers with high core-per-watt ratios and liquid-cooling readiness.[2]CoreWeave Press, “CoreWeave announces USD 2.2 billion European expansion anchored in Sweden,” coreweave.com Google and Facebook’s Swedish facilities have shown PUE values as low as 1.05, proving that pairing renewable hydro-power with outside-air economization cuts lifetime operating costs. These benchmarks are now cited in RFPs, pushing OEMs to offer sensors that feed real-time carbon dashboards. Over time, sustainability pressure is likely to amplify demand for advanced immersion-cooled racks, reinforcing efficiency leadership as a strategic differentiator within the Sweden data center server market.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Escalating CapEx for green-field data centres

Escalating CapEx for green-field data centres

| -1.8% | National, particularly affecting new market entrants | Medium term (2-4 years) |

% Impact on CAGR Forecast

:

-1.8%

|

Geographic Relevance

:

National, particularly affecting new market entrants

|

Impact Timeline

:

Medium term (2-4 years)

|

Global CPU/GPU supply-chain volatility

Global CPU/GPU supply-chain volatility

| -1.5% | Global impact with regional delivery delays | Short term (≤ 2 years) | |||

Stricter environmental permitting delays

Stricter environmental permitting delays

| -1.2% | National, concentrated in environmentally sensitive areas | Medium term (2-4 years) | |||

Acute shortage of Nordic data-centre engineers

Acute shortage of Nordic data-centre engineers

| -0.9% | Regional, affecting all Nordic countries | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Escalating CapEx for Green-Field Data Centres

The average build cost has risen to USD 9.1 million per MW, reflecting global inflation in concrete, steel, and switchgear—an increase that disproportionately burdens smaller Swedish operators Savills. The July 2023 removal of electricity tax relief further eroded cost advantages, raising OpEx by up to 15% for new facilities. Well-capitalized hyperscalers absorb these hikes through scale economics, whereas regional players delay expansions or seek sale-leaseback arrangements, tempering near-term server orders in the Sweden data center server market.

Global CPU/GPU Supply-Chain Volatility

Tight HBM supply and rapid product rollouts from NVIDIA and AMD are lengthening lead times beyond 40 weeks for flagship accelerators. Swedish projects such as Linköping University’s BerzeLiUs supercomputer achieved full system delivery only after phased shipments, illustrating exposure to global bottlenecks.[3]Linköping University, “BerzeLiUs supercomputer lifts Swedish AI research capacity,” liu.se Prolonged delays ripple through capacity planning, forcing operators to hold excess buffer stock or stagger go-live schedules, thereby dampening short-term revenue predictability across the Sweden data center server market.

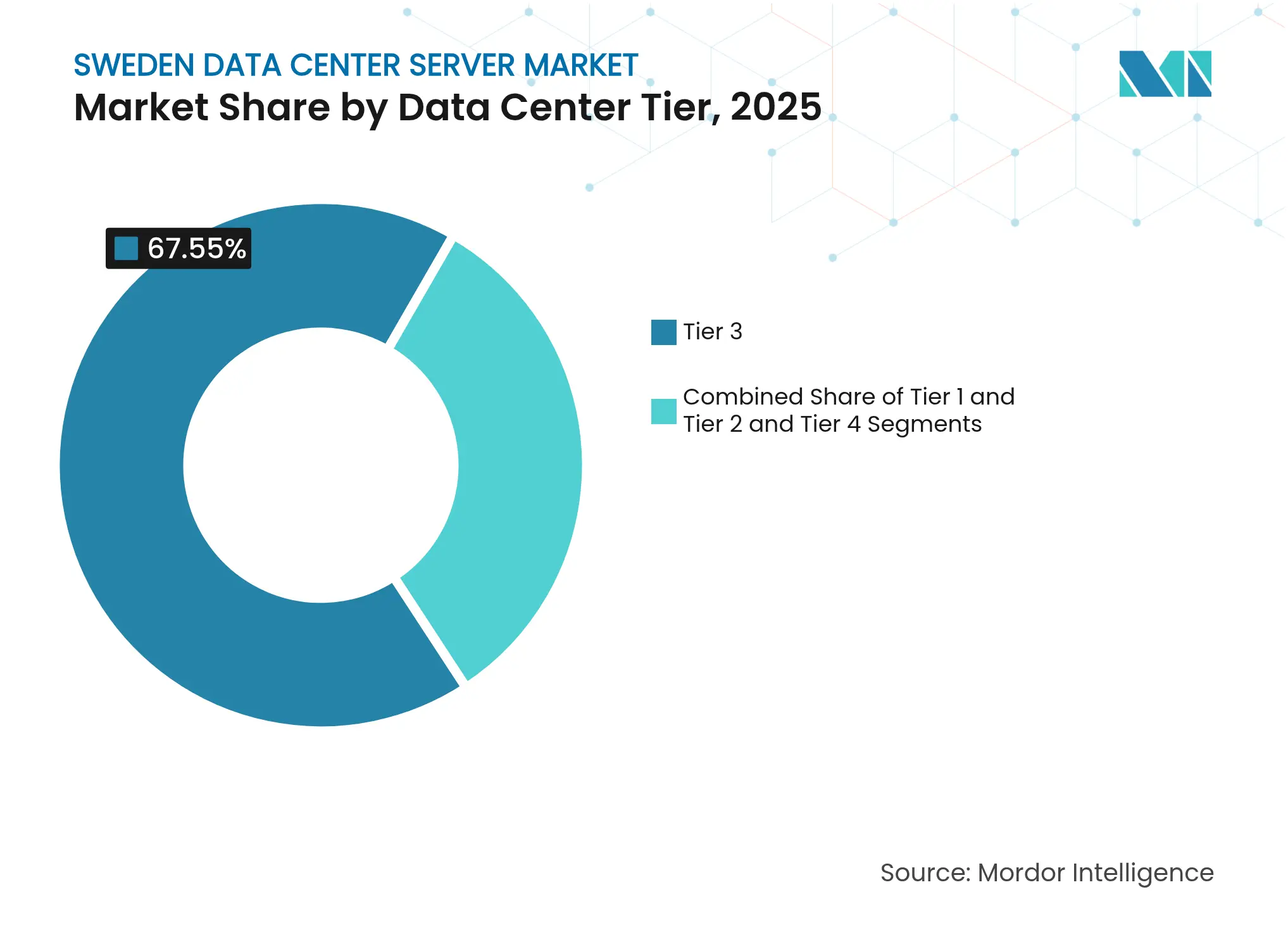

By Data-Center Tier: Mission-Critical Workloads Drive Tier 4 Expansion

Tier 3 sites currently dominate the Sweden data center server market size, retaining 67.55% revenue share in 2025 thanks to mature enterprise hosting needs. Yet Tier 4 footprints are expanding at 15.15% CAGR, propelled by banking, healthcare, and sovereign cloud mandates that require concurrently maintainable infrastructure for 99.995% availability. Northern campuses leverage dual-utility feeds and fault-tolerant designs to capture workloads shifting from post-Brexit London hubs. In parallel, Tier 1 and Tier 2 facilities remain relevant for dev-test environments and CDN caches, proving that Sweden’s tier mix spans the full uptime spectrum. As hyperscalers integrate on-site substations and modular substacks, the Sweden data center server market outlook tilts toward high-availability designs optimized for multi-tenant AI training clusters.

Even so, cost-conscious enterprises continue to refurbish Tier 3 halls with liquid-ready racks, taking advantage of Sweden’s naturally low ambient temperatures. Domestic regulations requiring healthcare and public-sector data to remain onshore reinforce demand for top-tier facilities operated by local players, ensuring that the Sweden data center server market share of Tier 4 providers will keep rising through 2030.

Note: Segment shares of all individual segments available upon report purchase

By Form Factor: Edge Computing Accelerates Micro-Blade Adoption

Half-height blades retained a leading position with 44.62% Sweden data center server market share in 2025, favoured for their balance of density and airflow. However, the advent of nationwide 5G and Industry 4.0 rollouts is pushing quarter-height and micro-blade adoption at a 11.98% CAGR, particularly for roadside and plant-floor cabinets where space and power are scarce. Ruggedized enclosures rated for extended operating temperatures are now standard in telecom procurement guidelines, steadily shifting the form-factor mix.

Hyperscale operators still value full-height blades for GPU-dense racks, but cooler ambient temperatures enable efficient air cooling even for 700 W PCIe cards, preserving room for traditional layouts. Microsoft’s Swedish campuses, for example, employ outside-air economization nine months a year, allowing extended use of standard blade designs without liquid loops. Over the forecast horizon, demand elasticity linked to mobile edge requirements will ensure diverse chassis needs, sustaining innovation across the Sweden data center server market.

By Application / Workload: AI Infrastructure Reshapes Server Requirements

Virtualization and private cloud stacks retained 37.95% market share in 2025, anchoring baseline demand from corporate ERP and productivity suites. Yet AI and ML workloads are climbing at 14.33% CAGR, fuelled by initiatives such as Ericsson’s dual-SuperPOD AI factory that blends DGX nodes with Mellanox InfiniBand to unlock exascale-class inference capacity. This shift is spurring demand for high-bandwidth memory, PCIe Gen5 fabrics, and advanced cooling loops.

High-performance computing projects under university and government sponsorship complement private-sector AI adoption, broadening the server mix to include water-cooled, direct-to-chip configurations. Edge-analytics workloads for autonomous mines and remote wind farms also contribute incremental units, proving that workload diversity underpins the resilient trajectory of the Sweden data center server market.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

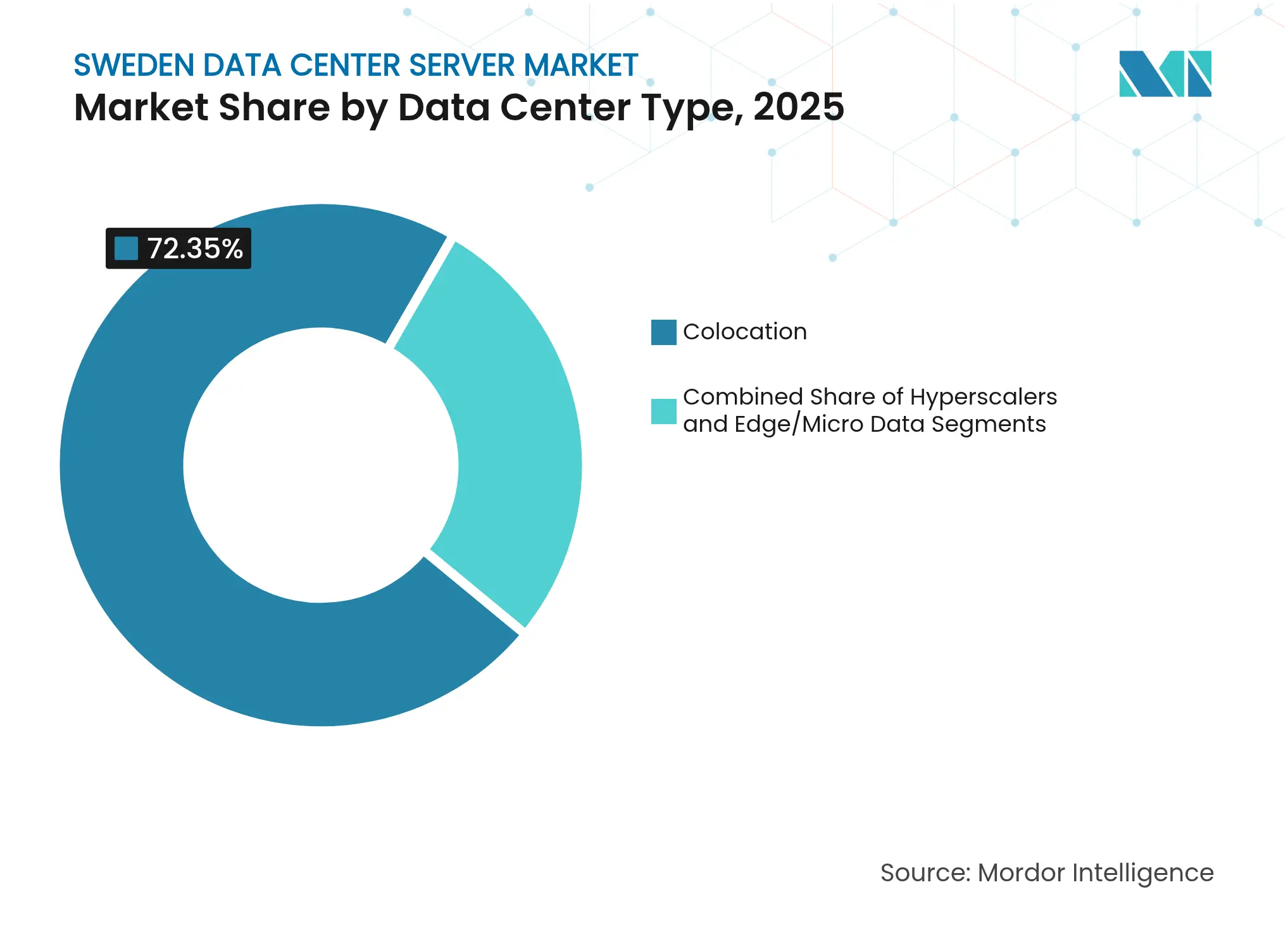

By Data-Center Type: Hyperscalers Challenge Colocation Dominance

Colocation hosts controlled 72.35% of revenue in 2025, yet hyperscale build-outs are forecast to grow 15.97% annually, narrowing the gap as Microsoft, Google, and CoreWeave add regional zones. Direct ownership gives cloud giants full control over power procurement, security, and topology fine-tuning advantages critical for AI clusters that may draw 120 kW per rack. Conversely, enterprises with sovereignty or latency requirements keep smaller cages inside carrier-neutral facilities, assuring tenancy variety within the Sweden data center server market.

Edge sites co-located at base-band hotels and rural aggregation nodes are also rising, though their power envelopes rarely exceed 200 kW. This bifurcation into mega-campuses and micro-pods signals that server vendors must optimize designs for both extremes, from 5 U-tall immersion tanks to short-depth 1 U boxes.

Note: Segment shares of all individual segments available upon report purchase

By End-Use Industry: Healthcare Digitalization Drives Server Demand

IT and telecom retained 27.88% revenue share in 2025 as operators expanded core and RAN compute. Nevertheless, healthcare and life sciences record 12.97% CAGR, buoyed by electronic health records, tele-oncology, and AI-assisted imaging. Under GDPR, patient data must remain within the EU, pushing hospitals toward domestically hosted clusters. Manufacturing is another major buyer, with automotive plants embedding real-time quality analytics in stamping presses, thereby requiring deterministic, millisecond-latency edge nodes.

Energy firms deploy servers to orchestrate VPPs and balance intermittent wind output, while financial institutions modernize risk engines but keep latency-sensitive trading platforms on-prem. This cross-industry mosaic ensures that no single vertical dominates the Sweden data center server market, enhancing resilience against sector-specific downturns.

Southern Sweden, anchored by Stockholm and Mälardalen, concentrates two-thirds of installed rack capacity owing to proximity to subsea cable landings, financial centers, and a dense fiber grid. These sites prioritize high-density AI racks and redundant dark-fiber routes to continental Europe. Northern clusters around Luleå and Östersund exploit ambient temperatures that average 4 °C and abundant hydro-power tariffs as low as EUR 0.03 per kWh, delivering sub-1.1 PUE scores that minimize lifetime OpEx. Facebook’s Luleå campus exemplifies this advantage by achieving a 1.05 PUE and avoiding 70,000 t of CO₂ annually, a benchmark that shapes operator expectations across the Sweden data center server market.

Central Sweden serves as a latency-balanced location, enabling under-20 ms round-trip times to both Frankfurt and London exchange points—an attribute attractive to BFSI workloads seeking Brexit-proof redundancy. Cross-border fiber restorations with Norway and Finland further support multi-homed designs that raise overall service availability. However, sparsely populated northern regions face talent shortages; engineering salaries have risen 12% since 2022 as operators compete for electrical and mechanical specialists. Government fast-track visas and proposed income-tax breaks in the 2025 budget aim to bolster Sweden’s attractiveness to foreign experts.

Geography also shapes supply-chain strategies. Ports at Gothenburg and Helsingborg handle containerized server shipments, but winter storms can disrupt schedules, leading many hyperscalers to establish bonded warehouses inside Stockholm-Arlanda’s free-trade zone. By storing buffer inventory near deployment sites, operators hedge against global logistic volatility, enabling smoother rollouts and reinforcing customer confidence in the Sweden data center server market.

Market Concentration

The Sweden data center server market is moderately consolidated. Dell, HPE, and Lenovo defend enterprise footprints through bundled lifecycle services and attractive leasing programs. NVIDIA dominates AI accelerators, yet AMD’s MI300 gains traction among price-sensitive research clusters. Cisco and Huawei supply integrated compute-network blades for converged stacks, while Supermicro and Inspur win deals for GPU-dense, customizable nodes favored by hyperscalers. Strategic differentiation increasingly hinges on sustainability credentials: Dell’s PowerEdge XE9785 supports immersion readiness, whereas HPE’s Cray EX liquid-cooled variant aligns with net-zero procurement goals.

Edge-focused entrants such as Kontron and Adlink target ruggedized micro-sites, bundling NEBS compliance to suit telecom-pole deployments. CoreWeave’s entry introduces a specialized AI-cloud alternative that co-locates GPU clusters with high-speed NVMe-over-Fabric, challenging generic colocation offerings. Intellectual-property investments remain high: AMD disclosed an 18% YoY rise in patent filings for energy-efficient memory controllers, underscoring IP as a competitive lever.

M&A activity intensifies as operators streamline portfolios: EcoDataCenter divested three legacy facilities to CapMan Infra to focus on hyperscale builds, and Scandinavian Data Centers installed grid-stabilizing battery arrays to entice ESG-minded tenants. These moves signal a shift toward vertically integrated, sustainability-first business models across the Sweden data center server market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES & FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study views the Sweden data center server market as the annual value of brand-new, rack-mounted or blade computing units that are installed inside purpose-built colocation, enterprise, edge, and hyperscale facilities to process, store, and route digital workloads. These units bundle processors, memory, internal storage, power supplies, and on-board networking cards that are ready to slot into a 19-inch rack.

Scope Exclusion: Refurbished or gray-market servers, personal computers, workstations, and server management software are left outside the baseline.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed Nordic data-center operators, local system integrators, and global OEM channel executives across Stockholm, Luleå, and Gothenburg. These discussions verified pricing corridors, lead-time trends, and workload migration rates that secondary data could only imply, letting us refine penetration assumptions and vet preliminary growth drivers.

Desk Research

We extracted foundational data from tier-1 public sources such as Sweden's National Board of Trade, Statistics Sweden, Eurostat customs codes for HS 8471, and the Swedish Data Center Industry Association's capacity tracker. Technical patterns were clarified by scanning peer-reviewed IEEE papers, European Patent Office filings, and regional sustainability directives that shape server design. To frame corporate footprints, our team pulled revenue splits and shipment commentary from listed vendors' 10-K filings and investor decks, while D&B Hoovers and Dow Jones Factiva enriched the competitive landscape. These examples illustrate, rather than exhaust, the secondary pool consulted.

A second pass involved reconciling import ledger values with reported hyperscaler capex, mapping average selling prices (ASPs) published in trade press to quarterly shipment indices, and aligning server refresh cycles with reported rack utilization targets in open government procurements.

Market-Sizing & Forecasting

A top-down reconstruction starts with Sweden's installed IT load (MW) and planned capacity additions, which are then multiplied by workload-specific server density coefficients to derive shipment volumes. These totals are further filtered through quarterly ASP series to obtain value. Supplier roll-ups and sampled procurement invoices act as a bottom-up reasonableness check. Variables powering the model include hyperscaler new-build pipeline (MW), enterprise virtualization ratios, server refresh cadence (in months), average core count per unit, electricity pricing trends, and krona-USD exchange movement. Forecasts apply a multivariate regression that blends capacity growth, real GDP, and cloud-workload share, with interval estimates adjusted through consensus reached in expert calls. Gaps created by opaque private deals are bridged using edge-case triangulation with Volza shipment records.

Data Validation & Update Cycle

Outputs face variance checks against historical import statistics and IDC-tracked EMEA server shipments; anomalies trigger analyst peer review before sign-off. The model refreshes every twelve months, with interim updates when large hyperscale projects or tax policy shifts occur.

Why Mordor's Sweden Data Center Server Baseline Commands Reliability

Benchmark comparison

Published numbers often diverge because firms select different hardware scopes, currency conversions, and update cadences.

Our disciplined tier-based lens and annual refresh mean each figure ties back to verifiable rack deployments rather than assumed expenditure.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 1.04 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 0.24 B (2024) | Regional Consultancy A | Excludes hyperscale self-build volumes and uses list ASPs without channel discounts | ||

USD 0.35 B (2023) | Trade Journal B | Counts only enterprise refresh shipments and applies five-year-old ASP benchmarks |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Opportunities in Singapore's Chemical Logistics Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.