India SUV Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

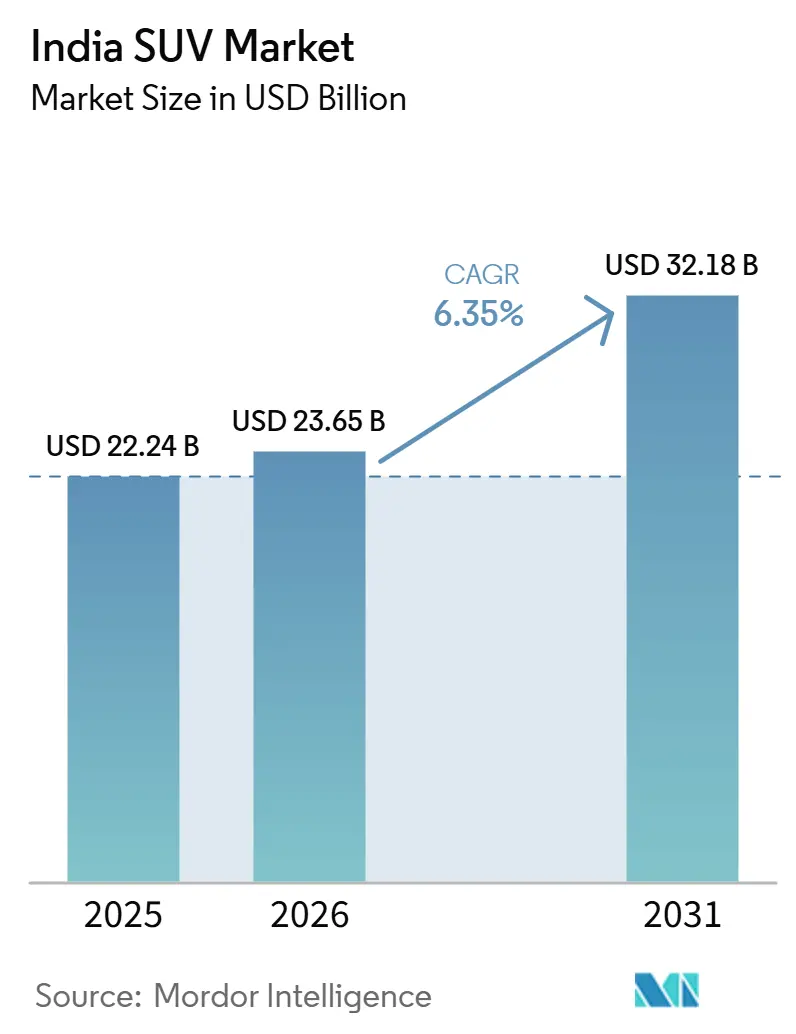

| Base Year Market Size (2025) | USD 22.24 Billion |

| Market Size (2026) | USD 23.65 Billion |

| Market Size (2031) | USD 32.18 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India SUV Market Analysis by Mordor Intelligence

The India SUV market size is expected to increase from USD 22.24 billion in 2025 to USD 23.65 billion in 2026 and reach USD 32.18 billion by 2031, growing at a CAGR of 6.35% over 2026-2031. Rising middle-class purchasing power, GST cuts on sub-4-meter models, and aggressive localization efforts are driving up demand, effectively trimming sticker prices and the total cost of ownership. Compact SUVs, even with features like Level 2 ADAS, connected-car services, and five-star Bharat NCAP safety ratings, continue to outprice hatchbacks. As battery costs decline and OEMs roll out more affordable offerings, electric SUVs are outpacing all other fuel types in growth. Competitive intensity is escalating, with new players like BYD and JSW MG Motor utilizing localized drivetrains and direct digital sales to undercut established players and attract tech-savvy urban consumers.

Key Report Takeaways

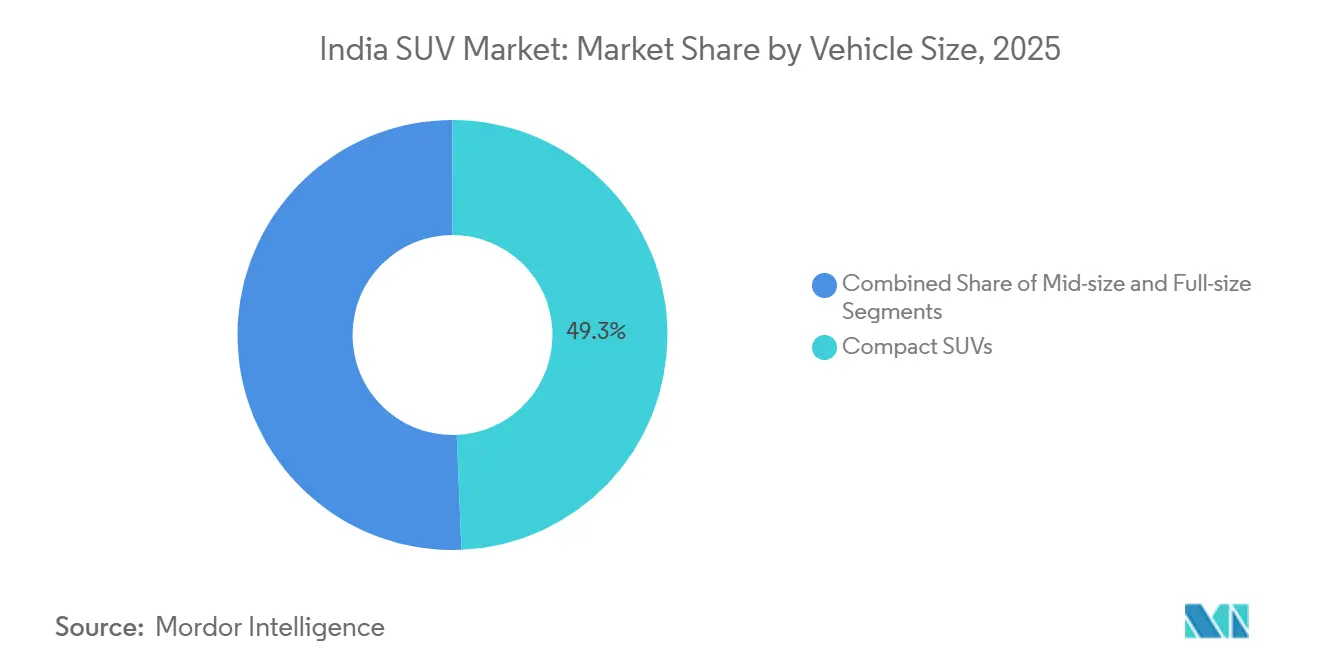

- By vehicle size, compact SUVs accounted for 49.33% of the Indian SUV market share in 2025. Compact SUVs are projected to register the fastest 7.35% CAGR between 2026 and 2031.

- By fuel type, petrol units accounted for 61.11% of revenue share in 2025, while electric SUVs are projected to post an 11.65% CAGR through 2031.

- By drivetrain, two-wheel-drive models accounted for 83.58% of demand in 2025. All-wheel-drive variants are expected to grow at the highest 11.43% CAGR over 2026-2031.

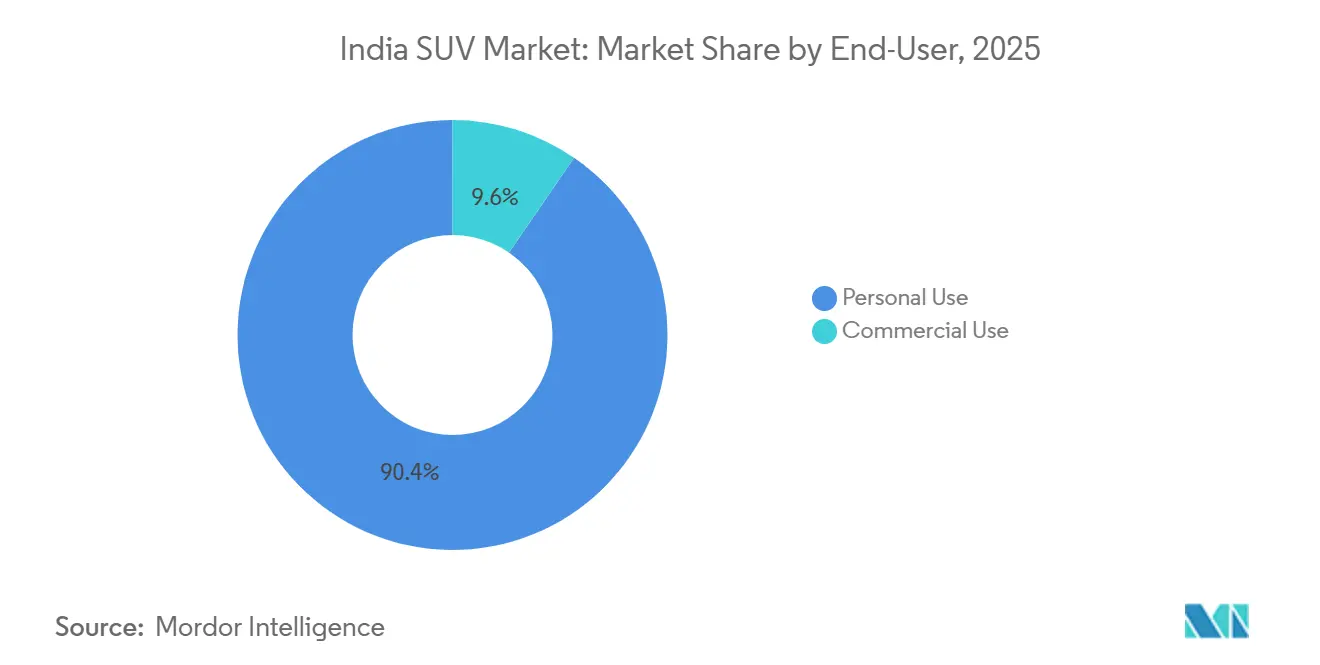

- By end user, personal buyers accounted for 90.44% of the Indian SUV market share in 2025. Commercial fleets are the fastest-growing buyer group, with a 9.91% CAGR projected through 2031.

- By seating capacity, five-seater layouts captured 71.65% of revenue in 2025. Seven-seater and larger configurations are poised to advance at an 8.83% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on suv market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India SUV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Disposable Income and Urbanization | +1.8% | Maharashtra, Karnataka, Tamil Nadu, Gujarat, Delhi NCR | Medium term (2-4 years) |

| Favorable GST Structure | +1.5% | Pan-India with higher impact in Uttar Pradesh, Bihar, Madhya Pradesh | Long term (≥ 4 years) |

| OEM Localization | +1.2% | Manufacturing hubs: Gujarat, Tamil Nadu, Karnataka, Haryana | Medium term (2-4 years) |

| National Highway and Expressway Network | +0.9% | Uttar Pradesh, Maharashtra, Rajasthan, Madhya Pradesh | Long term (≥ 4 years) |

| Digital Retail Channels | +0.6% | Tier-2/3 cities across Uttar Pradesh, Bihar, West Bengal, Odisha | Short term (≤ 2 years) |

| ADAS and Connected-Car Features | +0.5% | Metro cities: Mumbai, Delhi, Bangalore, Chennai, Hyderabad, Pune | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Middle-Class Disposable Income and Urbanization

India's middle class is set to boost discretionary spending, particularly on aspirational purchases like SUVs. The Prime Minister's Economic Advisory Council noted a significant uptick in vehicle ownership across both rural and urban landscapes. As urbanization progresses, there's a discernible shift towards vehicles that seamlessly blend city agility with recreational versatility. Compact SUVs are now favored for their elevated ground clearance, status enhancement, and shorter loan tenures. Moreover, younger first-time buyers, buoyed by attractive interest rates, are bypassing hatchbacks altogether.

Favorable GST Structure for Sub-4-Meter "Compact" SUVs

The GST Council reduced the compensation cess on sub-4-meter SUVs, lowering the effective tax burden and narrowing the price gap with hatchbacks. Compact SUV retail volumes grew significantly, according to the Federation of Automobile Dealers Associations [1]“Retail Vehicle Data November 2025,”, Federation of Automobile Dealers Associations, fada.in. OEMs with strong sub-4-meter portfolios, such as Maruti, Tata, Hyundai, and Mahindra, passed savings to consumers or reinvested in additional features, reinforcing the India SUV market’s shift toward compact models.

OEM Localization Lowering Sticker Prices & TCO

The Production Linked Incentive (PLI) Scheme, with an allocated incentive of INR 1.91 lakh crore, is a strategic reform initiative designed to enhance India’s manufacturing capabilities and boost localization rates for mass-market SUVs to high levels. Maruti Suzuki's new plant in Gujarat, alongside Mahindra's in Nagpur, is poised to significantly increase annual SUV capacity. Due to this deeper localization, sticker prices have decreased notably compared to recent launches, and maintenance costs have decreased as domestic parts have become more widely available [2]“PLI Scheme Attracts ₹35,657 Crore Commitments,”, Press Information Bureau, pib.gov.in.

Growing Affinity For ADAS And Connected-Car Features

Mahindra's Scorpio-N and XEV series propelled the rise in Advanced Driver Assistance Systems (ADAS) adoption, as these models incorporated advanced safety and convenience features that appealed to a broad consumer base. Meanwhile, the surge in connected-car subscriptions underscores consumers' readiness to invest monthly for telematics and over-the-air updates, highlighting a growing trend toward enhanced vehicle connectivity and digital integration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Fuel Prices | -1.1% | Pan-India with higher impact in rural areas and commercial segments | Short term (≤ 2 years) |

| CAFÉ II and RDE Emission Norms | -0.9% | Manufacturing states: Tamil Nadu, Gujarat, Karnataka, Haryana | Medium term (2-4 years) |

| Under-Developed High-Power EV Charging | -0.7% | Tier-2/3 cities, highway corridors across all states | Long term (≥ 4 years) |

| Persistent Semiconductor Shortages | -0.5% | Pan-India affecting all manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Fuel Prices and Subsidy Withdrawal on Diesel

Fuel price fluctuations and the slow phasing out of diesel subsidies are casting a shadow of uncertainty over SUV purchases, especially for diesel models that have long been the segment's frontrunners. While recent trends have shown a rise in diesel car sales, the Energy Transition Advisory Committee's push to ban diesel vehicles in cities with large populations is already swaying consumer choices. With the impending withdrawal of diesel subsidies, running costs are poised to climb, prompting fleet operators to reconsider their powertrain selections. Even though diesel continues to benefit high-mileage users, its market share is poised to dwindle as cleaner alternatives gain traction.

Stringent CAFÉ II and RDE Emission Norms Escalating Production Cost

OEMs paid significant penalties under CAFÉ II, underscoring the financial challenges posed by their SUV-focused lineups. This hefty outlay highlights the tightrope automakers walk, balancing consumer appetite for larger vehicles against stringent regulatory mandates. Proposed CAFÉ III targets threaten to add compliance hardware costs per vehicle. Concurrently, Real Driving Emissions rules are mandating selective catalytic reduction for diesel models and particulate filters for petrol models. These regulations not only tighten profit margins but also accelerate the industry's pivot towards electrification. Collectively, these mandates underscore the urgent need for automakers to innovate and recalibrate their portfolios, aligning with shifting environmental standards while safeguarding profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Size: Compact Dominance Drives Market Evolution

Compact SUVs generated 49.33% of the Indian SUV market share in 2025, and the Indian SUV market size for this segment is projected to rise at a 7.35% CAGR through 2031. A recent cess cut gave COMPACT SUVs a price edge. This advantage allowed Tata's Nexon, Maruti's Brezza, and Hyundai's Venue to dominate, clinching a significant share of the top retail positions. With Bharat NCAP awarding 5-star ratings to leading models, safety features like side- and pole-impact protection have become essential for buyers. As a result, mid-cycle facelifts are now standardizing six airbags and electronic stability control.

Even with aspirations for a premium image, mid-size SUVs find themselves in a higher tax bracket, stunting their volume growth. Meanwhile, full-size models face limitations due to their high entry prices. In metro India, where parking is a premium, there's a noticeable shift in demand towards sub-4-meter models, which conveniently fit into standard parking spaces. Consequently, OEM engineering strategies focus on optimizing interior space, enhancing infotainment, and bolstering safety features within the 4-meter limit, while safeguarding profit margins and avoiding higher GST brackets.

By Fuel Type: Electric Transformation Accelerates

Petrol units accounted for 61.11% of the 2025 revenue share, benefiting from lower entry prices and extensive service networks. As the retail price gap between diesel and petrol tightened, diesel's share dropped significantly. Additionally, the inclusion of selective catalytic reduction hardware increased the cost of each vehicle. The Indian SUV market for electric variants remains small in absolute terms, yet electric SUVs are projected to post an 11.65% CAGR through 2031, as state subsidies and battery costs decline significantly.

Hybrid SUVs hold a niche market share and are priced higher than their petrol counterparts, yet they offer significantly better fuel economy. Looking ahead, decreasing battery costs and OEMs' adoption of skateboard platforms are expected to reduce acquisition premiums. This development is likely to make total cost of ownership (TCO) calculations more favorable for electric powertrains, particularly in high-mileage scenarios.

By Drivetrain: 2WD Dominance With AWD Growth

Two-wheel-drive designs captured 83.58% of 2025 deliveries, a testament to cost sensitivity in the Indian SUV market. All-wheel-drive outlays of up to USD 3,000 restrict uptake to hilly terrains and affluent metro buyers. Nonetheless, AWD demand shows the fastest segment CAGR at 11.43% through 2031 as buyers equate on-demand traction with safety and resale value.

Electrification may accelerate this trend because dual-motor electric SUVs such as Mahindra's XEV 9e deliver AWD torque vectoring with less mechanical complexity and only marginal range penalties, making premium drivetrains more accessible in the long run.

By End-User: Personal Dominance With Commercial Acceleration

Personal buyers accounted for 90.44% of 2025 purchases, but fleet managers now view compact SUVs as lower-maintenance substitutes for sedans on rough urban roads. Commercial fleets are projected to expand at 9.91% CAGR through 2031. Ride-hailing platforms are seeing reductions in maintenance costs and increases in per-trip fares for compact SUVs compared to sedans, significantly shortening payback cycles.

Electric SUVs are enhancing fleet profitability by offering lower operating costs than petrol counterparts. In response, OEMs are crafting commercial-grade electric SUVs with extended range, quick charging, and streamlined interiors, aiming to tap into surging demand in India's SUV market.

By Seating Capacity: 5-Seater Leadership With 7-Seater Growth

Five-seat formats accounted for 71.65% of revenue share in 2025 because nuclear families average 3.1 members. Seven-seat layouts are projected to grow at an 8.83% CAGR to 2031 as joint families and tourism operators seek higher capacity. OEMs are pricing seven-seaters competitively, strategically undercutting MPVs while maintaining SUV aesthetics and ground clearance.

The third row is less usable: smaller SUVs offer limited legroom, making them suitable only for children, while larger models command higher ticket prices. However, upcoming skateboard EV platforms are expected to feature flat floors, enabling more spacious three-row configurations. This innovation could significantly boost the popularity of seven-seaters in India's SUV market.

Geography Analysis

Metros like Delhi-NCR, Mumbai, Bengaluru, Pune, Hyderabad, and Chennai account for a significant share of India's SUV sales. This concentration is supported by strong financing, rising disposable incomes, and a dense network of dealerships. On the other hand, rural and semi-urban regions are experiencing rapid growth, driven by improved road connectivity due to the development of new access-controlled highways.

Hyundai has increased its share of rural sales and plans to establish a majority of its future outlets in these areas. This strategy aligns with Kia’s efforts to expand its presence across more cities. Meanwhile, state-level incentives are creating disparities: Gujarat, Maharashtra, and Tamil Nadu are encouraging electric SUV adoption through subsidies, while states like Uttar Pradesh and Bihar lag behind due to lower per-capita incomes and limited charging infrastructure.

Production facilities are aligning with market trends. Toyota’s investment in Aurangabad aims to significantly increase its production capacity, highlighting the appeal of Maharashtra's supplier network. Additionally, the growth of digital retail is eliminating geographic barriers, with a majority of buyers now open to purchasing vehicles online. This shift enables OEMs to experiment with streamlined showrooms in smaller towns and rural areas without compromising their market reach.

Competitive Landscape

The Indian SUV market exhibits moderate concentration, with the top five players accounting for the majority of market share. Yet, competitive intensity remains fierce as manufacturers invest aggressively in capacity expansion, product development, and market penetration strategies. Mahindra’s leap to the second spot in H1 2025 illustrates how a focused portfolio can disrupt incumbent order. Platform sharing and standard drivetrains stretch R&D budgets, enabling brands to launch multiple body styles from a single architecture and compressing time-to-market.

Mahindra's MEB-platform supply partnership with Volkswagen Group (Skoda Auto VW India) typifies collaborative responses to soaring EV capex. Technological differentiation widens as Level 2 ADAS and over-the-air software updates proliferate—players with proprietary connected-car stacks harvest subscription income, offsetting razor-thin hardware margins. Semiconductor agility determines trim availability; firms securing long-term wafer agreements weather allocation shocks better, sustaining retail momentum amid supply turbulence.

Regulations reshape competition: CAFÉ II thresholds favor makers with hybrid line-ups, while RDE realities propel investment in after-treatment and light-weighting. Cost leadership through localization remains pivotal, as it explains Maruti Suzuki and Hyundai’s sustained volume edge. As margins thin in core segments, premium niches such as lifestyle 4x4s and electric crossovers offer avenues for profit, making them a strategic focus across the Indian SUV market.

India SUV Industry Leaders

Maruti Suzuki India Ltd.

Hyundai Motor India Ltd.

Tata Motors Ltd.

Mahindra & Mahindra Ltd.

Kia India Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Maruti Suzuki has unveiled the Victoris compact SUV, positioning it as the new flagship model within its Arena network. This launch highlights the company's strategic focus on strengthening its presence in the compact SUV market segment, catering to evolving consumer preferences for versatile and feature-rich vehicles.

- March 2025: Toyota has announced plans to launch three new sport-utility vehicles in the next year, positioning them below the Hyryder in its lineup. These upcoming models are expected to meet the growing demand for compact, affordable SUVs, further strengthening Toyota's presence in the competitive SUV market.

India SUV Market Report Scope

The Indian SUV market report is segmented by vehicle size (compact, mid-size, and full-size), fuel type (petrol, diesel, hybrid, and electric), drivetrain (2WD, 4WD, and AWD), end-user (personal use and commercial use), and seating capacity (5-seater and 7-seater). The market forecasts are provided in terms of value (USD) and volume (units).

| Compact (Up to 4 m) |

| Mid-size (4 to 4.6 m) |

| Full-size (Above 4.6 m) |

| Petrol |

| Diesel |

| Hybrid |

| Electric |

| 2WD |

| 4WD |

| AWD |

| Personal Use |

| Commercial Use |

| 5-Seater |

| 7-Seater and above |

| By Vehicle Size | Compact (Up to 4 m) |

| Mid-size (4 to 4.6 m) | |

| Full-size (Above 4.6 m) | |

| By Fuel Type | Petrol |

| Diesel | |

| Hybrid | |

| Electric | |

| By Drivetrain | 2WD |

| 4WD | |

| AWD | |

| By End-User | Personal Use |

| Commercial Use | |

| By Seating Capacity | 5-Seater |

| 7-Seater and above |

Key Questions Answered in the Report

How large is the India SUV market?

The India SUV market size reached USD 23.65 billion in 2026 and is on course to hit USD 32.18 billion by 2031, reflecting a 6.35% CAGR.

Which segment captures the highest India SUV market share?

Compact SUVs command 49.33% of volume, benefiting from a favorable tax structure and sub-4-metre footprints.

Which automaker is investing the most in new Indian SUV capacity?

Toyota is committing over USD 3 billion to expand its southern India factory and build a new Aurangabad plant expecting more than 1 million-unit combined capacity by 2030.

Which seating configuration shows higher growth?

Seven-seater and larger SUVs are expected to expand at an 8.83% CAGR to 2031.

Are commercial fleets adopting SUVs over sedans?

Yes, fleet operators see lower maintenance costs and higher trip fares, and commercial SUV purchases are growing at 9.91% CAGR.

Page last updated on: