Surgical Simulation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

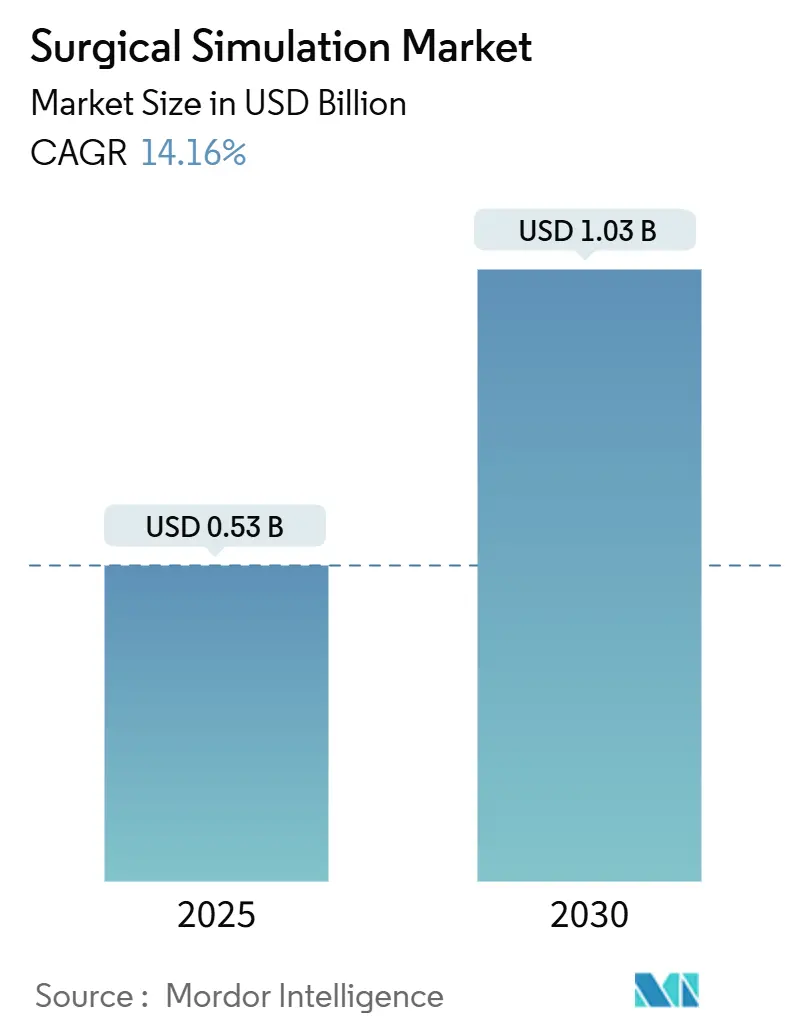

| Market Size (2025) | USD 0.53 Billion |

| Market Size (2030) | USD 1.03 Billion |

| Growth Rate (2025 - 2030) | 14.16% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Simulation Market Analysis by Mordor Intelligence

The Surgical Simulation Market size is estimated at USD 0.53 billion in 2025, and is expected to reach USD 1.03 billion by 2030, at a CAGR of 14.16% during the forecast period (2025-2030).

Mandatory competency rules, continuing declines in virtual-reality hardware prices, and hospital safety initiatives are accelerating spending across the surgical simulation market. The broader use of robotic operating rooms heightens the need for high-fidelity simulators that can accurately reproduce instrument articulation and tissue response. Cloud delivery lowers ownership barriers, enabling smaller teaching hospitals to adopt advanced systems without heavy IT builds. Together, these trends create a durable uplift in procurement plans, while AI-driven performance analytics strengthen proof-of-value discussions with finance teams.

Key Report Takeaways

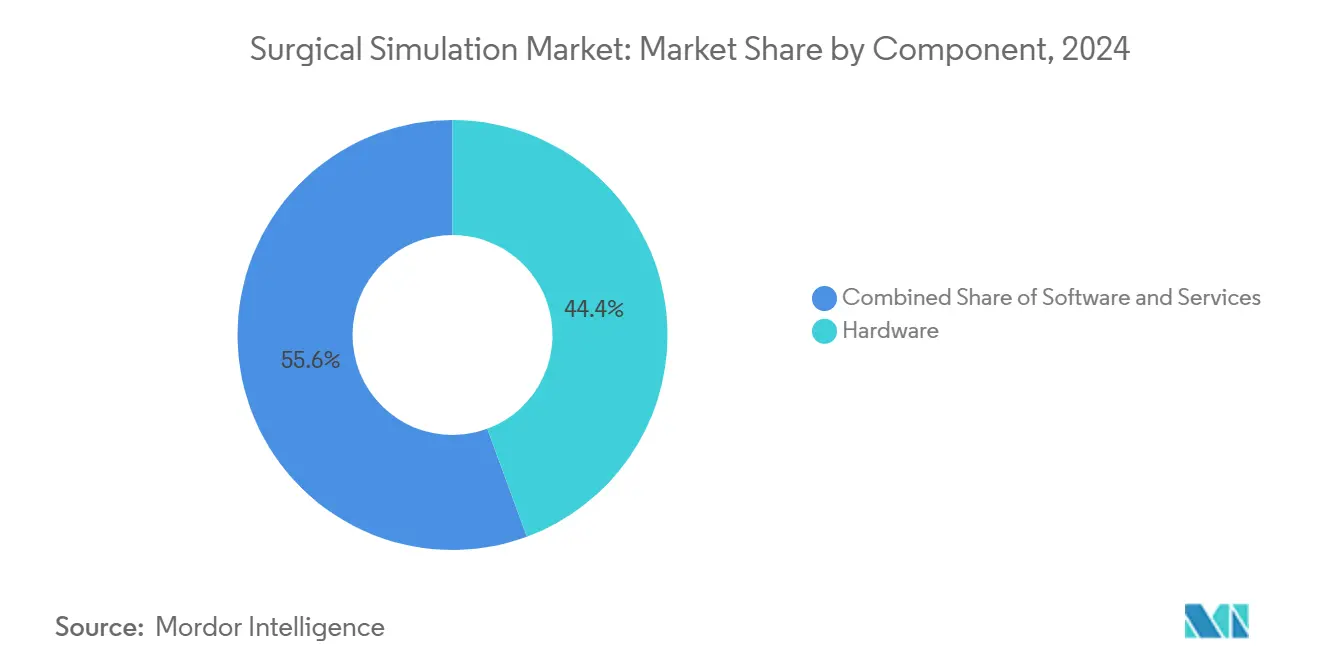

- By component, hardware captured 46.79% of the surgical simulation market share in 2024, while the software segment is projected to post the fastest 15.47% CAGR through 2030.

- By 2024, VR/AR simulators held a 41.32% share of the surgical simulation market size; cloud-based simulation platforms are projected to expand at a 16.29% CAGR through 2030.

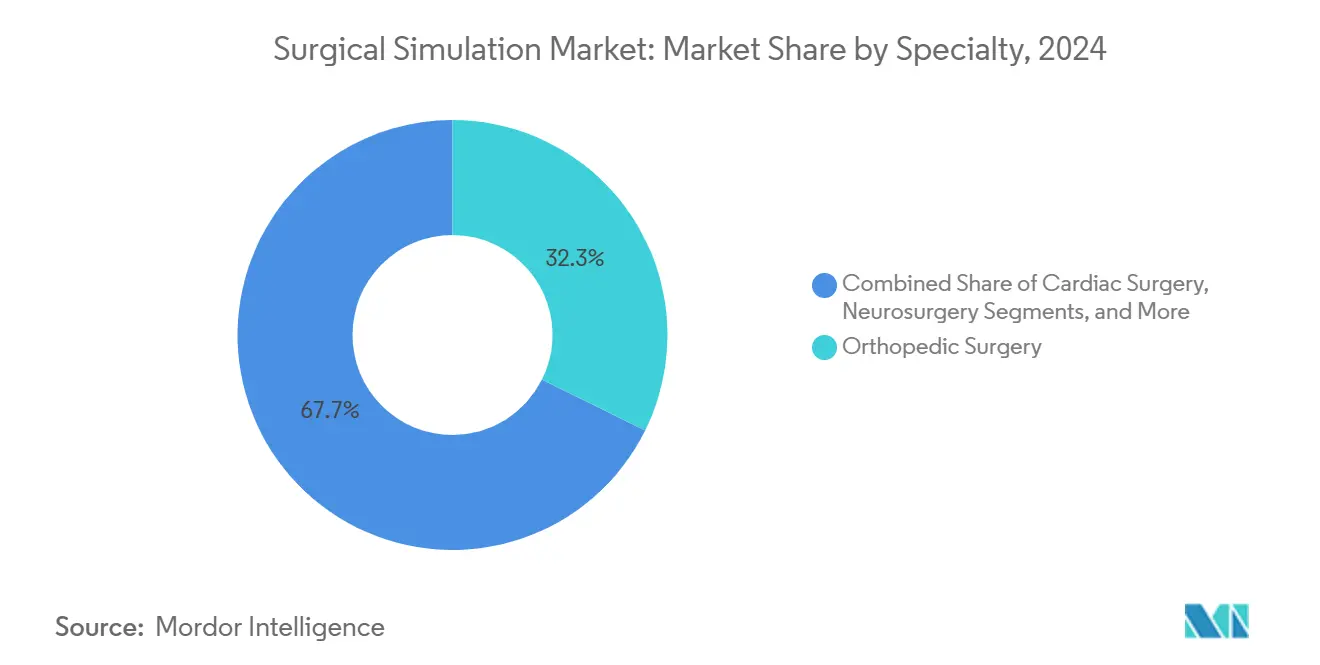

- By specialty, orthopedic surgery accounted for 32.32% of the surgical simulation market size in 2024, whereas neurosurgery is set to advance at a 14.57% CAGR to 2030.

- By end user, hospitals accounted for 58.13% of the surgical simulation market in 2024, while academic institutions recorded the fastest CAGR of 15.26% through 2030.

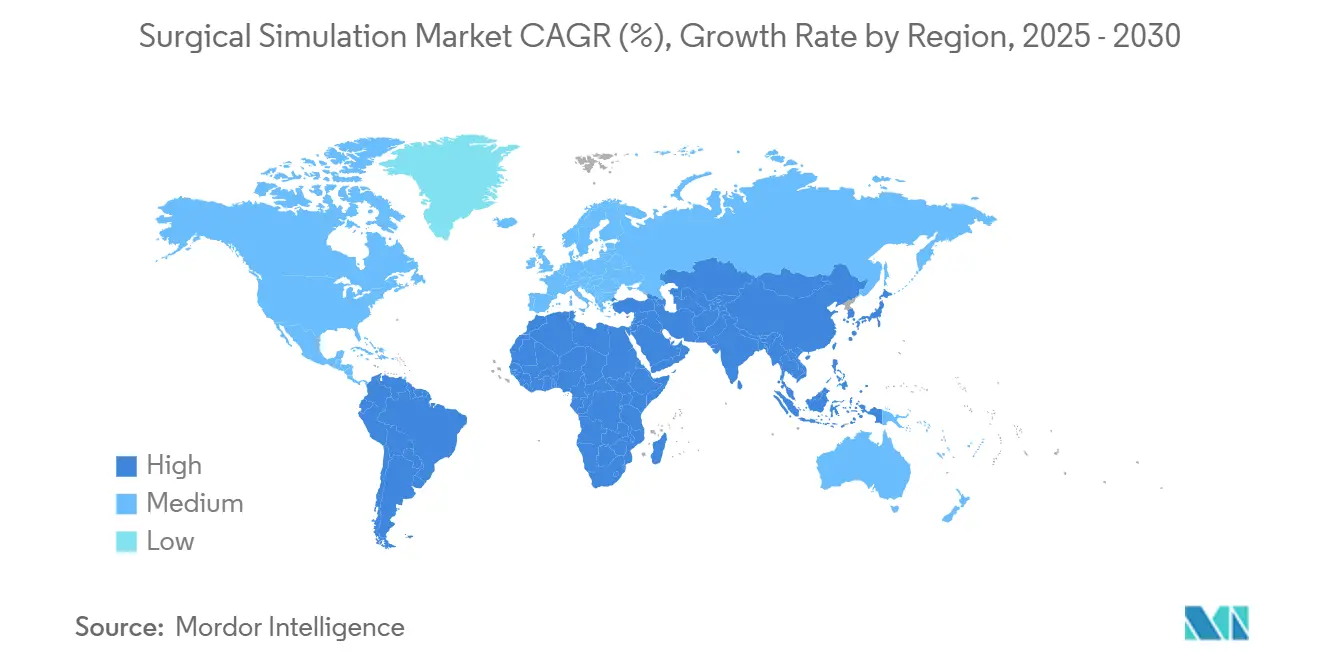

- By geography, North America retained a 41.83% share in 2024, and Asia-Pacific is projected to climb at a 16.64% CAGR through 2030.

Global Surgical Simulation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Minimally-Invasive & Robotic Procedures | +2.3% | Global, North America & Europe leading | Medium term (2-4 years) |

| Expanding Global Install-Base of Surgical Robots | +1.8% | North America, Europe, APAC | Long term (≥ 4 years) |

| Maturity of VR/AR & Haptics Cutting Ownership Cost | +1.6% | Global, developed markets | Short term (≤ 2 years) |

| Accreditation & Patient-Safety Mandates for Simulation | +1.4% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Cloud-Based “Simulation-as-a-Service” Ecosystems | +1.2% | Global, urban centers | Short term (≤ 2 years) |

| AI-Powered Adaptive Feedback & Credential Analytics | +0.9% | North America & Europe, global rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Minimally-Invasive & Robotic Procedures

Minimally invasive methods shorten patient recovery, yet they require advanced psychomotor skills that traditional apprenticeships rarely impart at scale. Surgical simulation market platforms replicate three-dimensional depth, force feedback, and camera navigation, allowing trainees to rehearse hundreds of cases without risk. Hospitals integrate simulation as a credentialing gate before surgeons perform live procedures, cutting adverse-event rates that lead to litigation. Outpatient centers prefer surgeons proficient in robotic workflows to ensure tight turnaround times. Collective pressure from payers, regulators, and malpractice insurers converts optional simulation exposure into a core licensing prerequisite in most residency programs.

Expanding Global Install-Base of Surgical Robots

Installations exceeded 8,000 systems worldwide in 2024, and every new console demands a dedicated training curriculum. Spending USD 2–3 million on hardware prompts executives to shorten surgeon onboarding cycles, and simulation provides a repeatable path to measured proficiency. Single-port and specialty robots expand the procedural mix, so vendors bundle simulators alongside consoles to close procurement deals more quickly. Credentialing committees are increasingly relying on exported simulator logs rather than paper assessments, thereby cementing recurring software license revenue streams across the surgical simulation market.

Maturity of VR/AR & Haptics Cutting Ownership Cost

Component prices fell 40% between 2022 and 2024 while GPU throughput quadrupled.[1] IEEE, “Standards for Medical Simulation 2024,” ieee.orgEntry-level haptic arms now sell for under USD 50,000, bringing realistic tissue feel within reach of district hospitals. Cloud rendering offloads graphics processing, allowing older laptops to run high-resolution models. Vendors repurpose consumer-gaming advances, accelerating release schedules without passing full R&D costs to customers. As a result, the surgical simulation market experiences a step change in unit volumes, as smaller institutions can finally justify capital outlay.

Accreditation & Patient-Safety Mandates for Simulation

The ACGME requires simulation across 23 surgical specialties, starting in 2024, affecting approximately 40,000 residents annually.[2]ACGME, “Program Requirements 2024,” acgme.org The Joint Commission ties hospital accreditation to verifiable staff competencies, and simulation logbooks meet this audit need. International medical schools adopt similar rules to harmonize with U.S. fellowship pathways, boosting global demand. Insurers discount premiums for facilities that prove structured simulation exposure, reinforcing the financial logic for adoption within the surgical simulation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Outlay | -1.7% | Global, developing markets | Short term (≤ 2 years) |

| Fragmented & Un-Standardized Curricula | -1.1% | Global | Medium term (2-4 years) |

| Budget Constraints in Low-Resource Settings | -0.9% | APAC, MEA, South America | Long term (≥ 4 years) |

| Rapid Hardware Obsolescence & Compatibility Risk | -0.8% | Global, tech-advanced markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Outlay

Top-tier systems cost USD 100,000–500,000, and annual service contracts account for 20% of the purchase price. During budget cycles, finance teams often prioritize imaging scanners, leaving simulation programs unfunded. In cash-based markets, depreciation schedules rarely align with three-year technology leaps, leading to write-down risk that discourages new orders. Vendors respond with leasing models and pay-per-use fees, but CFOs in small hospitals still view simulation as discretionary.

Fragmented & Un-Standardized Curricula

Programs adopt home-grown rubrics that hinder learner mobility between states or countries. Divergent scoring metrics complicate global fellowship approvals and force employers to re-test candidates, adding administrative cost. Without common milestones, content developers duplicate efforts across platforms, inflating prices. Industry groups have begun drafting open-standard APIs; however, consensus remains years away, which curbs integration velocity within the surgical simulation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Amid Software Acceleration

Hardware held a 46.79% market share in the surgical simulation market in 2024, driven by high-fidelity haptic arms and lifelike mannequins. Tactility remains critical for joint-replacement drills where millimeter-level feedback guides bone cuts. Over the outlook period, modular rigs enable centers to swap only sensor cartridges rather than full frames, thereby trimming refresh spending. Networked mannequins transmit sensor data to cloud dashboards, converting one-time sales into annual license streams.

Software platforms are growing at a 15.47% CAGR, driven by AI scoring engines and remote rendering. Libraries now cover more than 500 procedure variants, far beyond what a single institution could build internally. Facial-recognition log-ins simplify learner tracking across multi-site health systems. Embedded analytics export credential files directly into HR platforms, shortening onboarding steps for new hires inside the surgical simulation market.

Services—ranging from instructor workshops to content localization—provide a steady annuity flow. As curricula formalize, accreditation bodies demand certified faculty assessors, stimulating third-party training consultancies. Maintenance crews increasingly serve rigs through augmented-reality headsets, slashing travel time and maximizing uptime during peak residency seasons.

By Technology: VR/AR Leadership Challenged by Cloud Innovation

VR/AR simulators controlled 41.32% of the surgical simulation market in 2024, thanks to immersive visuals that mirror operating-room depth cues. Frame rates above 90 FPS eliminate vertigo, allowing sessions to remain productive. Start-ups are using eye-tracking to verify gaze discipline, which is particularly which is valuable during laparoscopic sequences where off-screen drift risks organ damage.

Cloud platforms, the fastest-growing slice at 16.29% CAGR, move compute loads to remote clusters, delivering high-resolution avatars on mid-range PCs. Institutions pay subscription fees rather than lump-sum licenses, easing capital constraints. Multisite nursing schools schedule simultaneous classes without duplicating servers, driving network effects that expand the customer base of the surgical simulation market.

Hybrid rigs blend 3-D-printed bones with augmented overlays so learners feel tactile feedback yet visualize virtual vessels. 3-D printing also supports rare-pathology replicas, turning anonymized CT datasets into physical models within 24 hours. Haptic upgrades retrofit into existing VR consoles, stretching asset life and smoothing budget approvals.

By Specialty: Orthopedic Strength Meets Neurosurgery Momentum

Orthopedic training retained 32.32% of the surgical simulation market size in 2024, driven by knee and hip replacements, which account for large procedure volumes. Bone-density algorithms now differentiate osteopenic from healthy tissue, improving screw-purchase drills. Sports-medicine modules teach arthroscopic knot tying under time pressure, mirroring real-life injury repairs in games.

Neurosurgery posts the highest 14.57% CAGR as tumor-resection pathways shift toward minimally invasive corridors. Patient-specific MRI imports let surgeons practice on twins of the actual brain they will operate on, cutting operative time and blood loss. Vendors bundle micro-instrument attachment kits so fellows grip devices identical to those in the theater, strengthening muscle memory across the surgical simulation market.

Cardiac, gastroenterology, and transplant tracks expand steadily. Transcatheter applications need precise catheter torque; simulators replicate end-organ perfusion and hemodynamic feedback, giving cardiologists confidence before first-in-human procedures. Liver-transplant scenarios train multidisciplinary teams on warm-ischemia timings, elevating donor-organ survival odds.

By End-User: Hospital Leadership with Academic Acceleration

Hospitals accounted for 58.13% of spending in 2024, reflecting their responsibility to certify staff before patient contact. Large systems negotiate enterprise licenses covering dozens of sites, lowering per-seat cost and cementing vendor relationships.

Academic institutes expand at a 15.26% CAGR, driven by curriculum mandates that embed simulation in the first year of medical school. Research budgets fund comparative-effectiveness studies, generating peer-reviewed evidence that further legitimizes investment decisions. Residency directors value simulators for their objective scoring, which reduces subjectivity in promotion reviews within the surgical simulation market.

Ambulatory surgery centers adopt lean portable rigs suited to tight floor space. Military and disaster-response agencies procure ruggedized units exceeding drop-shock standards, preparing medics for austere environments. Multilateral donors co-fund joint simulation hubs in low-income nations, enhancing regional trauma-care capacity.

Geography Analysis

North America accounted for 41.83% of the surgical simulation market in 2024, driven by stringent resident work-hour limits and pressures from malpractice litigation. Hospitals allocate simulation line items in multi-year capital plans, while philanthropic funds endow dedicated skills labs at university centers. Vendor competition centers on AI add-ons that enhance the relevance of already-installed rigs.

Europe follows with steady replacement demand as CE harmonization drives cross-border standardization. Simulation curricula are tied to Erasmus+ mobility programs, allowing trainees to carry digital badges across nations. Subsidies under the EU Recovery Plan earmark grants for digital health training, which include simulation upgrades, supporting an incremental lift to the surgical simulation market.

Asia-Pacific advances at a 16.64% CAGR through 2030, underpinned by China’s directive requiring simulators at over 200 medical schools by 2026. India’s National Medical Commission issued draft guidelines for competency-based postgraduate programs, signaling an oncoming surge in purchases. Urban private hospitals embrace cloud platforms to attract medical tourists looking for surgeons with proven simulator hours.

Middle East and Africa register emergent momentum as oil-export economies diversify into health science education hubs. Regional centers share high-end rigs across multiple countries, pooling costs. South America’s growth concentrates in Brazil where federal teaching-hospital networks pilot cloud subscriptions to bypass import tariffs on hardware, broadening participation in the surgical simulation market.

Competitive Landscape

The surgical simulation market exhibits moderate concentration, with the top five suppliers accounting for approximately 45% of the revenue. CAE, Laerdal Medical, and Surgical Science leverage broad catalogs and regulatory know-how to maintain installed-base loyalty. Mergers, such as Surgical Science acquiring Mimic Technologies for USD 25 million, aim to integrate haptic robotics modules into existing VR lines, offering turnkey ecosystems that simplify the buyer experience.

New entrants exploit cloud distribution to circumvent hardware moats. Fundamental VR and Osso VR offer software-only packages that run on consumer-grade headsets, enabling a fast rollout to community programs. Patents cluster around force-feedback actuators and algorithmic assessment engines, with 150 filings logged in 2024, underscoring an innovation race.[3]United States Patent and Trademark Office, “Patent Database Search 2024,” uspto.gov

Strategy pivots toward specialty niches. Mentice expands into endovascular stroke care, while VirtaMed targets hip arthroscopy kits approved under the CE mark. Vendors court pharmaceutical sponsors to underwrite disease-specific modules, opening nontraditional revenue channels inside the surgical simulation market.

Surgical Simulation Industry Leaders

CAE Inc.

Gaumard Scientific

Laerdal Medical

Mentice AB

Surgical Science

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: VirtaMed secured CE marking for its ArthroS hip arthroscopy simulator in Europe.

- October 2024: CAE Healthcare announced a USD 15 million expansion of its Montreal simulation center, adding 5,000 sq ft of space and 20 high-fidelity simulators.

- October 2024: Gaumard Scientific introduced the HAL S5301 patient simulator with enhanced respiratory mechanics.

Global Surgical Simulation Market Report Scope

| Hardware |

| Software |

| Services |

| VR/AR Simulators |

| 3-D-Printed & Physical Models |

| Haptic-Enabled Hybrid Platforms |

| Cloud / Web-Based Simulation |

| Orthopedic Surgery |

| Cardiac Surgery |

| Neurosurgery |

| Gastroenterology |

| Oncology / Reconstructive |

| Transplant & Other Specialties |

| Hospitals |

| Academic & Research Institutes |

| Surgical Training Centres & Ambulatory Surgical Centers |

| Military & Government Organizations |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Technology | VR/AR Simulators | |

| 3-D-Printed & Physical Models | ||

| Haptic-Enabled Hybrid Platforms | ||

| Cloud / Web-Based Simulation | ||

| By Specialty | Orthopedic Surgery | |

| Cardiac Surgery | ||

| Neurosurgery | ||

| Gastroenterology | ||

| Oncology / Reconstructive | ||

| Transplant & Other Specialties | ||

| By End-User | Hospitals | |

| Academic & Research Institutes | ||

| Surgical Training Centres & Ambulatory Surgical Centers | ||

| Military & Government Organizations | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the surgical simulation market in 2025?

The surgical simulation market size stands at USD 533.34 million in 2025 and is projected to double by 2030.

Which component leads current sales?

Hardware, especially high-fidelity haptic rigs, commands 46.79% of 2024 revenue.

What CAGR will cloud-based simulation platforms post through 2030?

Cloud platforms are forecast to grow at a 16.29% CAGR, the fastest among all technologies.

Which region is expanding most rapidly?

Asia-Pacific shows the highest growth, advancing at a 16.64% CAGR on the back of medical-school expansion in China and India.

How do accreditation mandates affect purchasing?

Rules from bodies such as ACGME require documented simulation hours, pushing hospitals and universities to integrate simulators into core curricula.

What is the main obstacle for low-income markets?

High upfront capital and maintenance costs limit adoption where health budgets prioritize essential equipment.

Page last updated on: