Surgical Rasps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

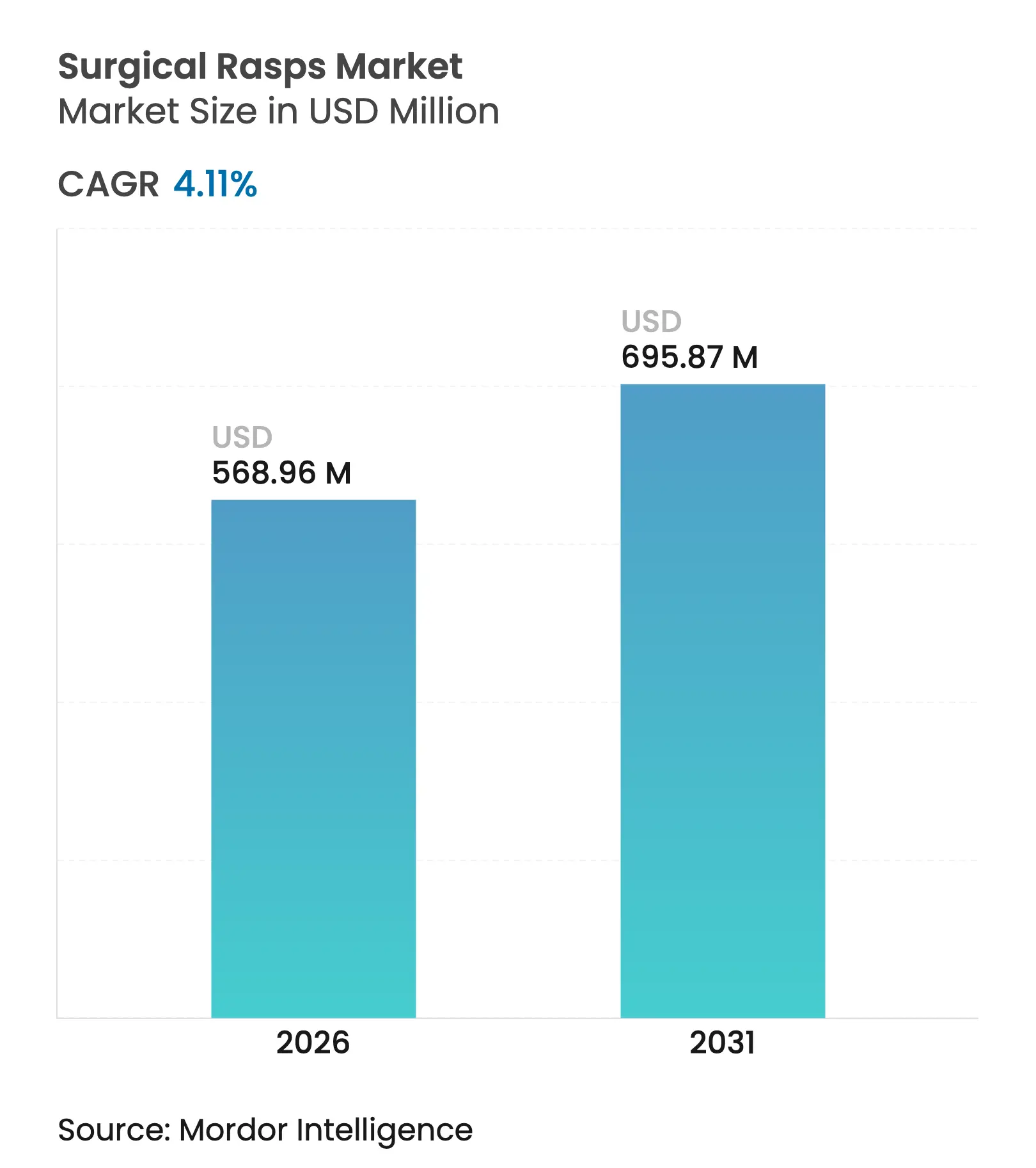

| Market Size (2026) | USD 568.96 Million |

| Market Size (2031) | USD 695.87 Million |

| Growth Rate (2026 - 2031) | 4.11 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

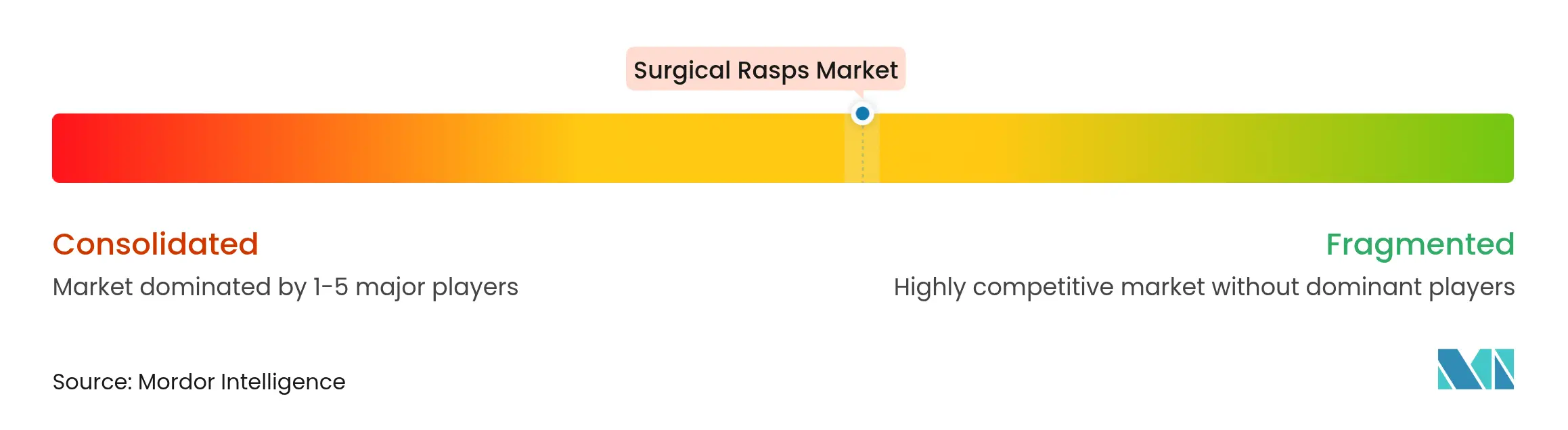

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Surgical Rasps Market Analysis by Mordor Intelligence

The surgical rasps market size was valued at USD 546.50 million in 2025 and estimated to grow from USD 568.96 million in 2026 to reach USD 695.87 million by 2031, at a CAGR of 4.11% during the forecast period (2026-2031). Accelerated procedure volumes, stricter infection-control rules, and rapid migration of orthopedic cases to ambulatory surgery centers (ASCs) anchor growth in every region. Hospital systems are upgrading from reusable hand-held instruments to ergonomic, powered rasp platforms that trim operating time and ease surgeon fatigue. Single-use variants are gaining traction because they remove reprocessing costs and satisfy regulators pressing for lower surgical site-infection rates. Competition is intensifying as major orthopedic suppliers embed rasps into robotic workstations and patient-specific implant workflows, while emerging players court ASCs with cost-effective disposable kits.

Key Report Takeaways

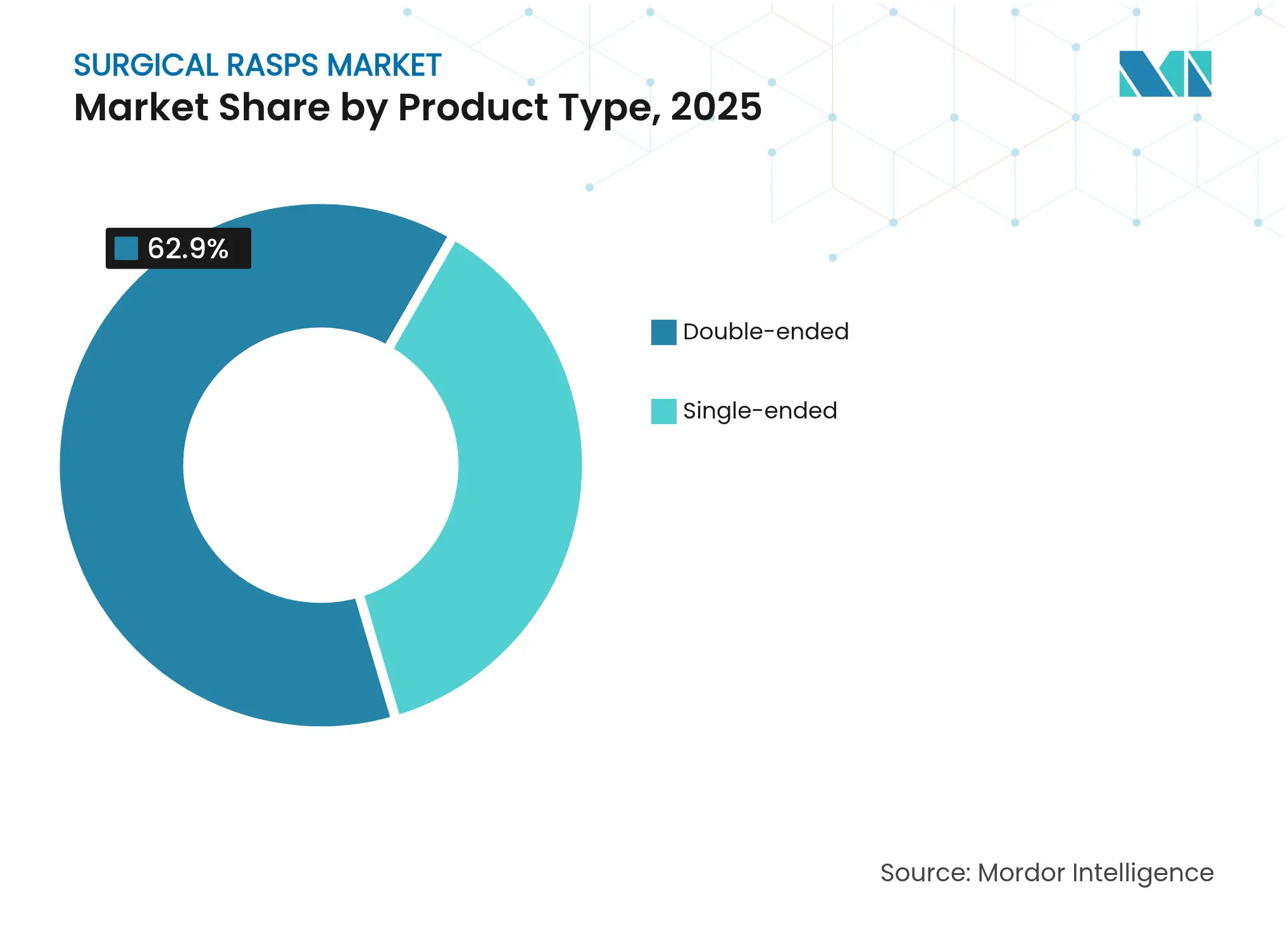

- By product type, double-ended rasps accounted for 62.90% of surgical rasps market size in 2025; single-ended instruments post a 4.63% CAGR to 2031.

- By technology, manual hand-held instruments led with 60.85% of surgical rasps market size in 2025, whereas powered oscillating systems are advancing at a 4.82% CAGR through 2031.

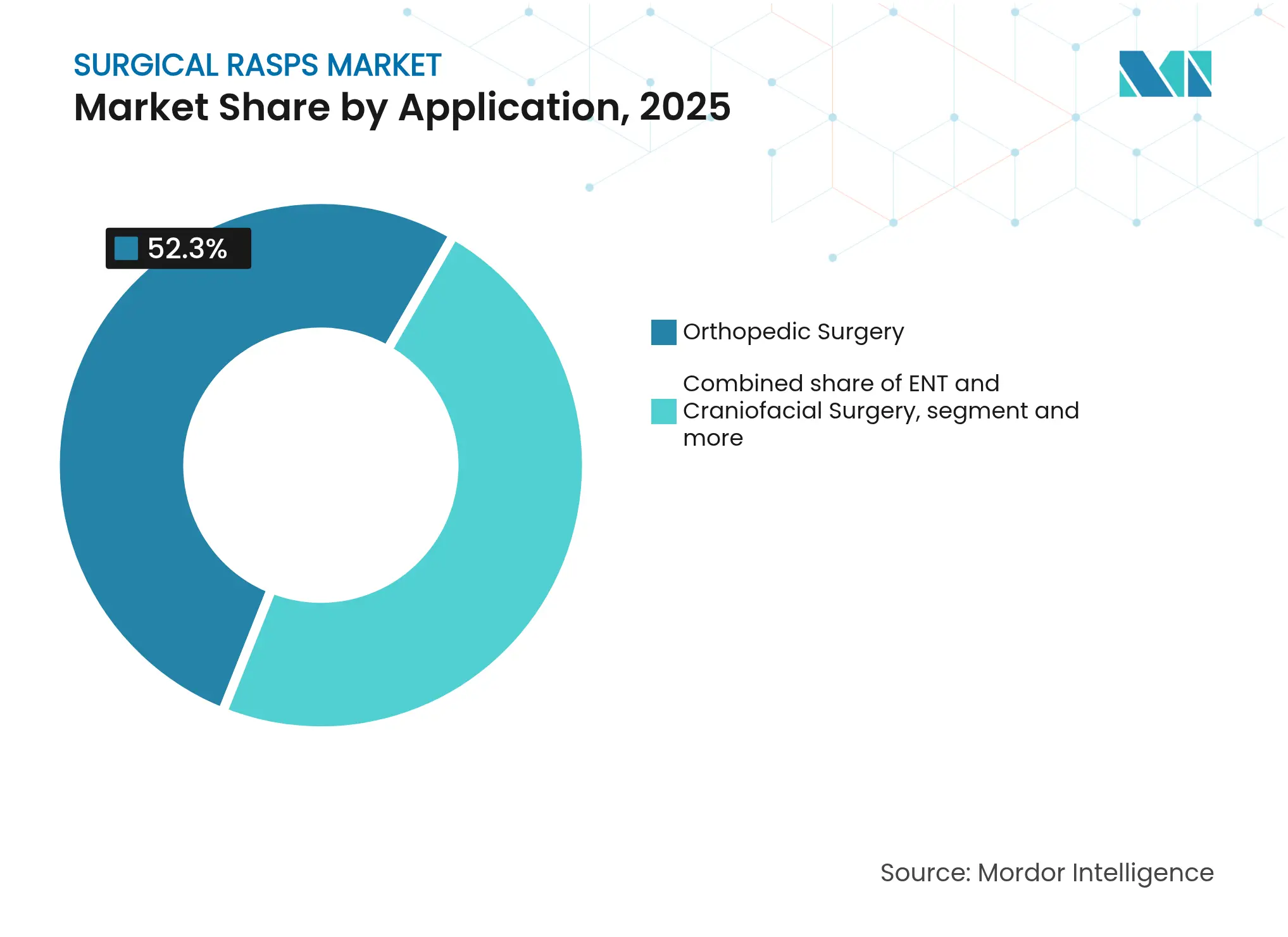

- By application, orthopedic surgery commanded 52.30% of surgical rasps market share in 2025; plastic & cosmetic surgery is set to rise at a 5.05% CAGR to 2031.

- By end user, hospitals and clinics held 70.95% surgical rasps market share in 2025; ASCs deliver the fastest growth at 5.41% CAGR.

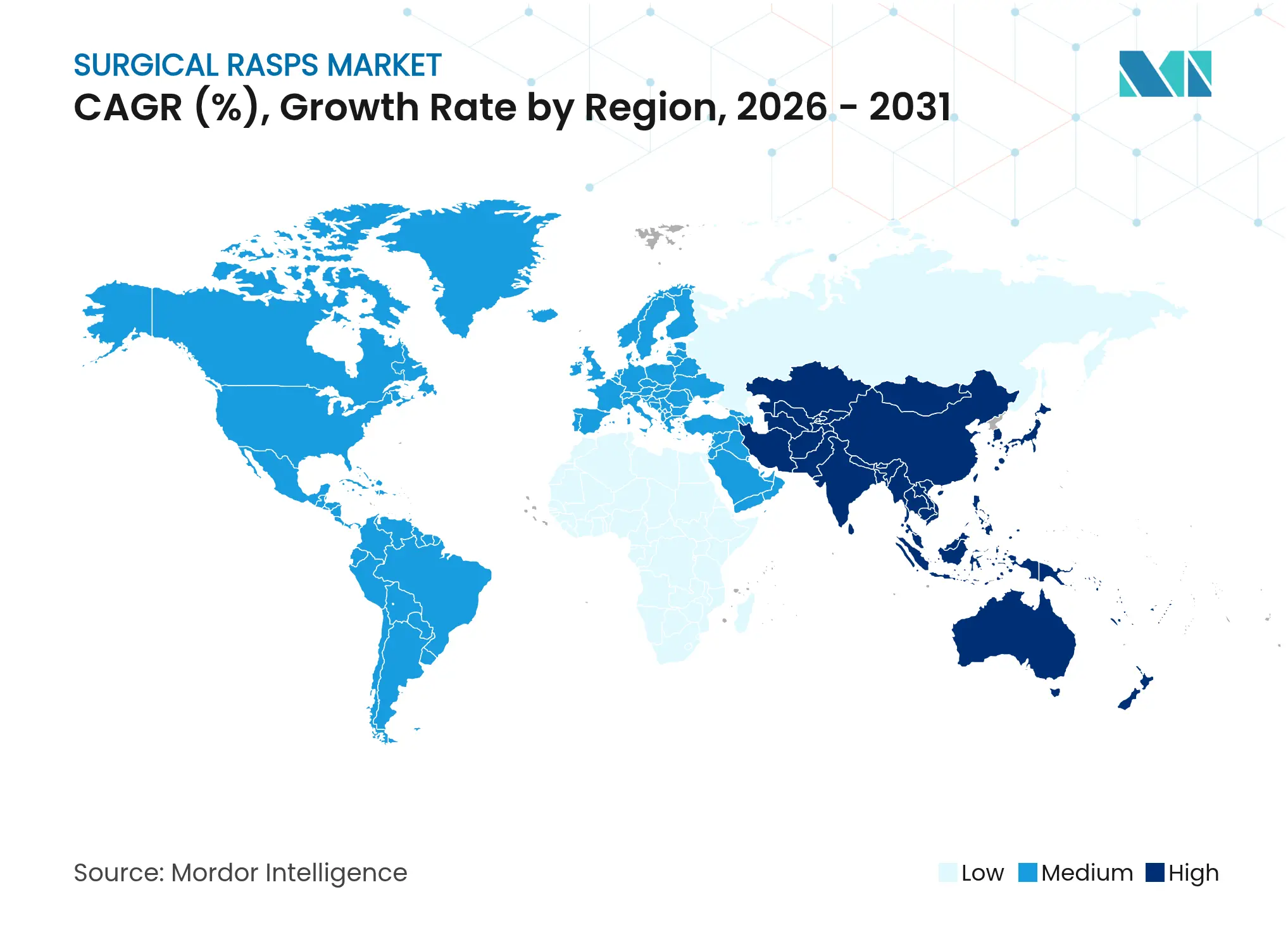

- By geography, North America dominated with 42.10% revenue share in 2025, while Asia-Pacific expands quickest at a 5.82% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Rasps Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing volume of orthopedic & reconstructive procedures Increasing volume of orthopedic & reconstructive procedures | +1.2% | Global, with concentration in North America & APAC | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Global, with concentration in North America & APAC | Impact Timeline:Medium term (2-4 years) |

Expansion of ambulatory surgery centers (ASCs) Expansion of ambulatory surgery centers (ASCs) | +0.8% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) | |||

Rising healthcare spending in emerging economies Rising healthcare spending in emerging economies | +0.6% | APAC core, with gains in China, India, Southeast Asia | Long term (≥ 4 years) | |||

Technological advances in powered & ergonomic rasps Technological advances in powered & ergonomic rasps | +0.5% | Global, led by North America & EU innovation hubs | Medium term (2-4 years) | |||

Patient-specific implant trend driving customised rasps Patient-specific implant trend driving customised rasps | +0.4% | North America & EU, expanding to APAC premium markets | Long term (≥ 4 years) | |||

Regulatory push for single-use rasps to cut infection risk Regulatory push for single-use rasps to cut infection risk | +0.3% | Global, with strictest enforcement in EU & North America | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Volume of Orthopedic & Reconstructive Procedures

Total joint arthroplasties moved decisively toward same-day discharge when 72% of Medicare replacements took place outside traditional inpatient wards in 2023. The 2025 Outpatient Prospective Payment System rule raises hospital operating rates by 2.9% and adds seven orthopedic codes to the ASC covered list, funnelling higher-acuity work into outpatient suites. Aging baby boomers push procedure demand at least 25% higher over the coming decade, necessitating standardized, single-use rasps that bypass sterilization queues. Robotic navigation and patient-specific jigs let surgeons perform complex bone reaming in outpatient theatres, uplifting sales of precision-engineered devices that slot seamlessly into digital planning platforms. Artificial-intelligence tools further refine bone-cutting trajectories, spurring orders for rasps that preserve sub-millimetre tolerances.

Expansion of Ambulatory Surgery Centers (ASCs)

ASC procedure volumes are rising at a 6.9% CAGR, aided by 2025 payment parity initiatives that grant site-neutral reimbursements across 6,100 facilities. Because ASCs deliver orthopedic interventions for 144% less cost than hospital outpatient departments, payers aggressively steer cases to these centres. Purchasing managers favour sterile, ready-to-use rasps that abolish reprocessing overhead, shrink turnover time, and shield facilities from sterilization non-compliance risk. ASCs increasingly accept higher-acuity spine and shoulder revisions, fuelling demand for rasp kits tuned to niche bone contours. Workflow software and compact robots tailored for ASC footprints reinforce the pivot to disposable or semi-disposable powered rasps that maintain throughput without sacrificing ergonomic control.

Rising Healthcare Spending in Emerging Economies

China’s health outlays climbed to CNY 2.25 trillion in 2023, while Japan projects ¥89 trillion in 2040, both funnelling resources into orthopedics and aesthetic surgery.[1]U.S. Department of Commerce, “Healthcare Resource Guide – India,” commerce.govGovernment insurance schemes now reimburse robotic-assisted joint replacements across Japan and South Korea, lifting expectations for compatible rasp instruments. Middle-income consumers in India, Thailand, and Indonesia increasingly finance elective knee, spine, and craniofacial surgeries, broadening the installed base for premium single-use rasps. Local manufacturing incentives invite multinationals to assemble mid-tier products regionally, trimming logistics costs and custom-duty outlays. Medical-tourism clusters in Singapore and Dubai, seeking Western-quality tooling, underpin additional upside for advanced rasp designs.

Technological Advances in Powered & Ergonomic Rasps

Next-generation systems integrate brushless motors, torque governors, and push-to-lock adapters that let scrub nurses swap cutting heads within seconds. Recent patents cover disposable rasp blades co-moulded with polymer hubs to cut weight and ease post-case segregation for recycling. Stryker’s EZout revision platform lowers extraction force and leaves 60% less particulate debris than manual tools, curbing acetabular micro-fracture risk [techortho.com]. Cordless packs remove power-cord clutter, while LED fault lights guide troubleshooting without disrupting sterile fields. Surface-engineering breakthroughs create nano-polished teeth that slice cancellous bone cleanly, reducing post-operative inflammation documented across orthopaedic trials.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High-volume/low-value pricing pressure High-volume/low-value pricing pressure | -0.7% | Global, most acute in North America & EU | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.7% | Geographic Relevance:Global, most acute in North America & EU | Impact Timeline:Short term (≤ 2 years) |

GPO-driven price squeeze on reusable instruments GPO-driven price squeeze on reusable instruments | -0.5% | North America core, expanding to EU markets | Medium term (2-4 years) | |||

Substitution by powered burrs & ultrasonic bone scalpels Substitution by powered burrs & ultrasonic bone scalpels | -0.4% | Global, led by premium markets in North America & EU | Long term (≥ 4 years) | |||

Environmental scrutiny of single-use instruments Environmental scrutiny of single-use instruments | -0.2% | EU core, with spillover to North America & APAC | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High-Volume/Low-Value Pricing Pressure

Medicare spent USD 6.1 billion on ASC services for 3.3 million beneficiaries in 2022; yet device reimbursements lag cost inflation. Group purchasing organizations (GPOs) pool spend across expansive hospital networks, extracting double-digit price cuts from manufacturers. Device-benefit managers escalate the squeeze by buying implants directly and leasing them to facilities, masking true net pricing behind confidentiality clauses. Reusable rasps face added scrutiny once ANSI/AAMI ST108 raised decontamination water-quality demands, elevating life-cycle costs. Vendors counter by pitching outcome-based contracts tying rasp fees to infection rates, but margins still compress when bids pivot on lowest delivered price.

Substitution by Powered Burrs & Ultrasonic Bone Scalpels

Orthopedic subspecialists increasingly deploy high-speed burrs that sculpt bone faster in narrow cavities, while ultrasonic scalpels deliver micrometre-level precision without thermal necrosis. Early clinical data show 15% shorter operative windows in facial osteotomies and 20% lower blood loss, pressuring traditional rasp uptake. Academic centres adopt these alternatives enthusiastically, influencing resident preferences that flow into future purchasing cycles. Manufacturers hedge by integrating rasp cutting faces onto burr shanks, but cannibalization risk persists where capital budgets already accommodate powered burr consoles.

Segment Analysis

By Product Type: Double-Ended Dominance Faces Single-Use Disruption

Double-ended instruments generated 62.90% of surgical rasps market size in 2025, favored by inpatient theatres that amortize reusable tools across high-volume arthroplasty lists. Their two-face design supports rapid swaps between coarse and fine teeth without exchanging hand pieces. Yet single-ended rasps, expanding at a 4.63% CAGR, align better with procedural customization and sterile-pack workflows popular in cosmetic rhinoplasty and craniofacial reconstruction. Growth attaches to ASC procurement models that prize disposability over central-service reprocessing. Surgeons performing patient-specific joint replacements increasingly request bespoke single-ended rasps mated to 3D-printed cutting guides, reinforcing momentum toward individualized instrumentation. While hospitals will still order multiuse double-ended tools for bulk orthopedic traffic, niche aesthetic and paediatric centres tilt procurement toward lightweight single-ended variants that pair with low-profile powered drivers.

A rebound in procedure volumes following pandemic postponements ensures both formats stay relevant. European regulators’ recycling mandates are prompting engineers to redesign double-ended shafts in recyclable stainless-steel alloys and to embed RFID tags that track life-cycle counts. In parallel, patent activity reveals hybrid designs where a disposable rasp tip threads onto a reusable handle, blending ecological stewardship with infection-control compliance. Suppliers ranked outside the top five are leveraging such hybrids to bypass entrenched hospital contracts and win high-margin cosmetic accounts.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Manual Systems Yield to Powered Precision

Manual hand-held rasps retained 60.85% of surgical rasps market share in 2025 thanks to simplicity, low acquisition cost, and tactile feedback critical in delicate nasal and otologic work. But powered oscillating systems are accelerating at a 4.82% CAGR as ergonomic fatigue, OSHA musculoskeletal regulations, and quest for reproducible cuts push surgeons toward mechanized motion. Studies document 83% lower forces transmitted to the acetabular rim when powered rasps replace mallet strikes, diminishing micro-fracture risk that can trigger implant loosening. Battery packs lasting a full joint-replacement list eliminate bulky cables, enhancing aseptic flow. Manual versions still dominate in austere theatres where autoclave cycles cost pennies and surgeons trust familiar haptics, yet hybrid battery-assist handles priced within 20% of premium manual sets are eroding that last outpost.

Global orthopedic societies add key-performance indicators around operative time and implant fit, metrics where powered rasps excel. Consequently, health systems with value-based-care contracts adopt automation bundles that include powered rasps, navigation sensors, and data-logging software. Vendors expand service agreements to cover yearly motor calibration and loaner pools, turning razor-and-blade economics into multi-year subscription revenue streams. Manual tools will coexist, but the long-term arc favours powered precision, especially as advances in haptic feedback motors recreate the feel of cortical breach without manual force.

By Application: Orthopedic Foundation Expands Into Aesthetic Growth

Orthopedic procedures accounted for 52.30% of 2025 revenue, cementing the specialty’s anchor role in the surgical rasps market. Total knees, hips, and shoulder revisions require consistent rasping to ensure press-fit implant fixation, driving large order volumes. At the same time, plastic and cosmetic surgery applications record a 5.05% CAGR, propelled by social-media visibility and growing disposable income among millennials. Facial feminization, rhinoplasty, and mandibular contouring need smaller, highly polished rasps that reduce scarring, prompting incremental revenue beyond reconstructive staples.

Ear, nose, and throat teams adopt reciprocating rasps for osteotomies around the orbital rim, while dental implantologists exploit piezo-surgical cuts finished with micro-rasps to refine osteotomy walls. Craniofacial centres publish data showing 30% fewer nerve injuries when powered rasps replace chisels during sagittal split osteotomy, furthering cross-specialty adoption. As aesthetic medicine expands into outpatient boutique suites, suppliers field compact kits labelled by procedure to streamline inventory control and meet stringent ASC turnover targets.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospital Dominance Challenged by ASC Innovation**

Hospitals and clinics generated 70.95% of 2025 revenue, sustained by entrenched vendor contracts, central sterile departments, and bundled-payment frameworks. Yet ASCs are the true disruptors, growing at 5.41% CAGR as payers reward their 30%–50% cost edge on joint replacements. ASC managers avoid reprocessing complexity by stocking individually sterilized single-use rasps, a procurement model that dents hospital negotiating leverage. Specialty orthopedic centres, a sub-set of ASCs, schedule high-throughput joint days that value powered rasps calibrated for consistent broach depth, accelerating turnover without sacrificing alignment accuracy.

Academic medical centres fill a separate niche, running early-feasibility trials on robotic rasping arms that record bone density metrics in real time for intra-operative decision support. Although these institutions represent a small revenue slice, their technology endorsements often sway protocol committees nationwide. Over the forecast window, hospitals will cede modest share to ASCs but retain leadership in trauma and revision cases demanding multiday stays and broad instrument trays.

Geography Analysis

North America retained 42.10% revenue share in 2025 as the United States expanded its 6,100-strong ASC network and Canada boosted elective orthopedic funding under national surgery backlog agreements. FDA guidance on orthopedic disposables accelerates approval of single-use rasps, while GPO contracting cycles shape national pricing. Mexico’s medical-tourism corridors in Baja California and Jalisco import mid-tier rasps bundled with implant packages, widening regional uptake.

Asia-Pacific records the fastest 5.82% CAGR through 2031, buoyed by USD 610 billion healthcare spending projected for India by 2026 and a Chinese med-tech ecosystem nurturing more than 100 surgical-robot start-ups. Beijing’s 14th Five-Year Plan spotlights domestic orthopedic tools, channeling subsidies toward powered rasp line-builds that undercut import tariffs. Japan and South Korea expand insurer coverage for robotic arthroplasty, stimulating cross-sales of compatible rasps. In Southeast Asia, Thailand and Indonesia court inbound patients seeking cost-effective cosmetic osteotomies, a trend lifting premium single-use rasp demand.

Europe, a mature yet sustainability-focused market, revises the EU Packaging and Packaging Waste Regulation so that all medical packaging must be designed for recycling by 2030, a stipulation compelling instrument firms to rethink blister packs and protective trays.Germany anchors regional volume with high hip-revision rates, while the United Kingdom’s integrated-care boards pool orthopedic tenders, reinforcing GPO-style price pressure. France mandates environmental impact labels on single-use devices, nudging hospitals toward hybrid disposable-tip rasp systems. Growth in the Middle East & Africa and South America lags yet remains meaningful as Gulf states invest in orthopedic centres of excellence and Brazil’s SUS public system accelerates backlog reduction programmes.

Competitive Landscape

Market Concentration

The surgical rasps market remains moderately fragmented. DePuy Synthes, Stryker, and Zimmer Biomet command double-digit shares, each embedding rasps inside broader robotic ecosystems. Stryker’s System 8 EZout couples powered rasps with digital torque feedback, while DePuy’s VELYS platform routes procedural analytics to cloud dashboards. Zimmer Biomet’s 2025 pilot of a machine-vision broaching arm underscores the convergence of hardware and AI. The proposed Stryker–Zimmer Biomet merger, still under antitrust review, could concentrate majority of the global sales into a single entity, reshaping tender dynamics.

Second-tier players such as Smith+Nephew and Medacta push differentiation through lightweight, single-use rasp kits optimized for outpatient joint revisions. 3D-printing specialists offer bespoke rasp geometries turned around in 48 hours, appealing to craniofacial surgeons tackling anomalous anatomies.

Patent filings surged in 2024, spotlighting disposable handle adapters and dual-function forceps that clamp bone fragments while providing rasping edges.[3]United States Patent and Trademark Office via Justia, “Rasp Handle Adapter Patent No. 12016576,” patents.justia.com Competitive moats increasingly hinge on software integration, preventive-maintenance telemetry, and ESG credentials tied to recyclable materials. Vendors courting ASC chains bundle service and training, betting that procedural standardization will lock in multi-year supply contracts.

Surgical Rasps Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Patent No. 12016576 for a rasp-handle adapter featuring push-to-lock retention and ergonomic grip was granted after a February 2023 filing.

- August 2023: Patent No. 11723674 covering a hybrid plastic–metal disposable rasp head targeting infection-control markets was issued.

- March 2023: Shanghai Ninth People’s Hospital introduced a reciprocating rasp technique for mandibular anterior subapical osteotomy, reducing operation time and collateral tissue damage compared with traditional chisels.

Table of Contents for Surgical Rasps Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increasing volume of orthopedic & reconstructive procedures

- 4.2.2Expansion of ambulatory surgery centers (ASCs)

- 4.2.3Rising healthcare spending in emerging economies

- 4.2.4Technological advances in powered & ergonomic rasps

- 4.2.5Patient-specific implant trend driving customised rasps

- 4.2.6Regulatory push for single-use rasps to cut infection risk

- 4.3Market Restraints

- 4.3.1High-volume/low-value pricing pressure

- 4.3.2GPO-driven price squeeze on reusable instruments

- 4.3.3Substitution by powered burrs & ultrasonic bone scalpels

- 4.3.4Environmental scrutiny of single-use instruments

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product Type

- 5.1.1Double-ended

- 5.1.2Single-ended

- 5.2By Technology

- 5.2.1Manual / Hand-held

- 5.2.2Powered / Oscillating

- 5.3By Application

- 5.3.1Orthopedic Surgery

- 5.3.2ENT and Craniofacial Surgery

- 5.3.3Plastic and Cosmetic Surgery

- 5.3.4Dental Surgery

- 5.3.5Others

- 5.4By End User

- 5.4.1Hospitals and Clinics

- 5.4.2Ambulatory Surgical Centers

- 5.4.3Specialty Orthopedic Centers

- 5.4.4Others

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Ambler Surgical

- 6.3.2Bornemann Maschinenbau GmbH

- 6.3.3Surgipro Inc.

- 6.3.4Millennium Surgical Corp. (Avalign Technologies, Inc.)

- 6.3.5DePuy Synthes (Johnson & Johnson)

- 6.3.6Zimmer Biomet Holdings Inc.

- 6.3.7Stryker Corporation

- 6.3.8Smith & Nephew plc

- 6.3.9B. Braun SE (Aesculap)

- 6.3.10Teleflex Incorporated

- 6.3.11Aspen Surgical Products, Inc.

- 6.3.12KLS Martin Group

- 6.3.13Arthrex Inc.

- 6.3.14Integra LifeSciences Holdings

- 6.3.15GerMedUSA Inc.

- 6.3.16gSource LLC

- 6.3.17Novo Surgical Inc.

- 6.3.18Sklar Surgical Instruments

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the surgical rasps market as the worldwide sales revenue generated from new, reusable or disposable, hand-held or powered bone-shaping instruments that surgeons employ to contour, smooth, or decorticate osseous tissue during orthopedic, dental, craniofacial, and plastic procedures.

Scope exclusion: veterinary rasps, custom 3-D printed single-case rasps, and aftermarket sharpening services are not counted.

Segmentation Overview

- By Product Type

- Double-ended

- Single-ended

- Double-ended

- By Technology

- Manual / Hand-held

- Powered / Oscillating

- Manual / Hand-held

- By Application

- Orthopedic Surgery

- ENT and Craniofacial Surgery

- Plastic and Cosmetic Surgery

- Dental Surgery

- Others

- Orthopedic Surgery

- By End User

- Hospitals and Clinics

- Ambulatory Surgical Centers

- Specialty Orthopedic Centers

- Others

- Hospitals and Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- China

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed practicing orthopedic surgeons, ASC procurement managers, and instrument distributors across North America, Europe, and three key Asia-Pacific markets. Conversations verified average selling prices, learning-curve discard rates, and the gradual shift toward single-use rasps, thereby filling gaps left by public statistics and validating quantitative model assumptions.

Desk Research

We began with open datasets such as WHO procedure volumes, OECD Health Statistics on joint-replacement rates, World Bank 65-plus population trends, and FDA MAUDE alerts to benchmark product safety signals. Trade associations, for example, the American Academy of Orthopedic Surgeons and the International Dental Federation, supplied annual implant numbers that anchor demand. Company 10-Ks, device recall notices, and hospital procurement portals clarified pricing corridors. Select paid databases, notably D&B Hoovers for company revenue splits and Dow Jones Factiva for transaction news, helped triangulate competitive footprints. This list is illustrative; many additional sources informed data checks and narrative framing.

Market-Sizing & Forecasting

A top-down reconstruction starts with national procedure counts (hip, knee, trauma, maxillofacial, dental), which are then multiplied by rasp utilization rates and weighted average selling prices. Supplier roll-ups and sample channel checks provide a selective bottom-up view to reconcile totals. Core inputs include: 1) primary joint-replacement volumes, 2) prevalence of osteoporosis and trauma admissions, 3) penetration of powered rasps, 4) average price differentials between reusable and disposable units, and 5) public capital-expenditure budgets for ASCs. Five-year forecasts employ multivariate regression with age-cohort growth, procedure intensity, and ASP trend as drivers, while scenario analysis stress-tests currency swings or reimbursement shifts. Missing granular shipment data is bridged with expert-agreed penetration proxies.

Data Validation & Update Cycle

Outputs pass a two-tier analyst review where anomalies versus historical series or peer ratios trigger re-checks. Before release, we refresh import-export signals and major recall news. The model is updated annually, with interim revisions when material events emerge.

Why Mordor's Surgical Rasps Baseline Earns Trust

Benchmark comparison

Published estimates often diverge because firms apply distinct product scopes, price ladders, and refresh cadences.

Key gap drivers in this niche include whether disposable rasps are counted, how ASP erosion is modeled, and if dental rasp usage is bundled with orthopedic demand. Mordor's analysts report the full global scope and refresh the model every twelve months, whereas some peers use narrower geographic cuts or apply straight-line ASP discounts without validating against hospital tenders.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

546.5 - 2025 | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

535.9 - 2024 | Global Consultancy A | Excludes powered rasps and uses list prices, inflating CAGR | ||

512.2 - 2022 | Industry Association B | Uses historical import data only; no price normalization | ||

488.2 - 2023 | Regional Consultancy C | Omits dental applications and applies regional weights globally |