Surgical Tables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

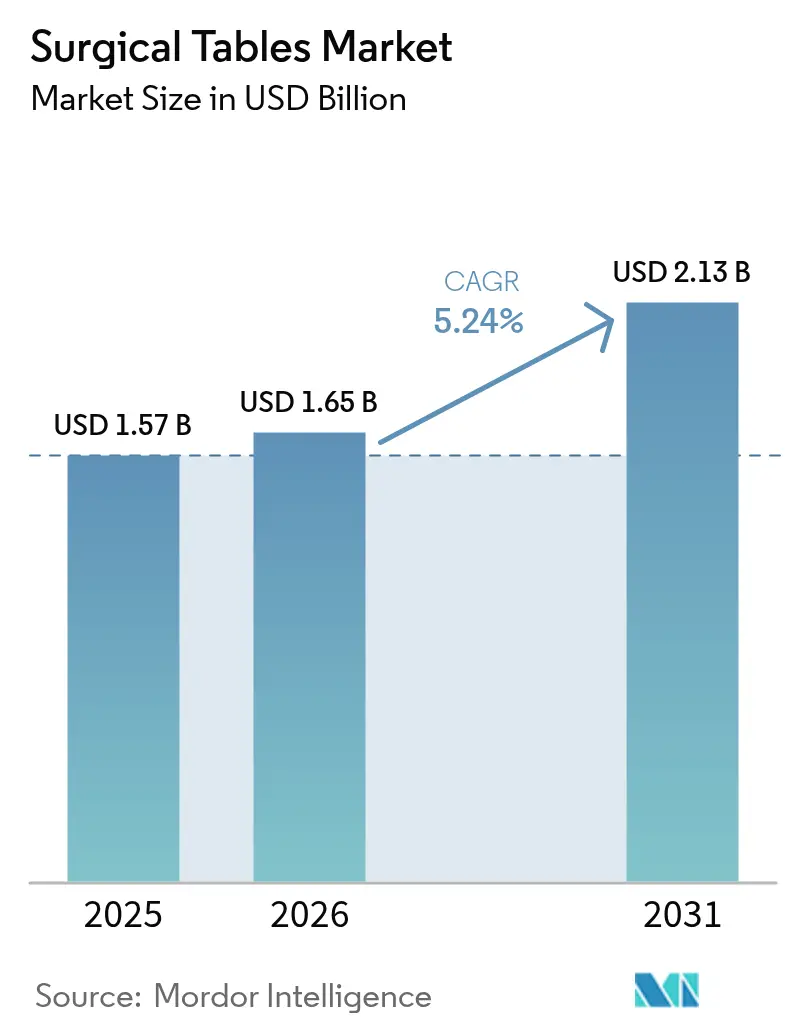

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 2.13 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

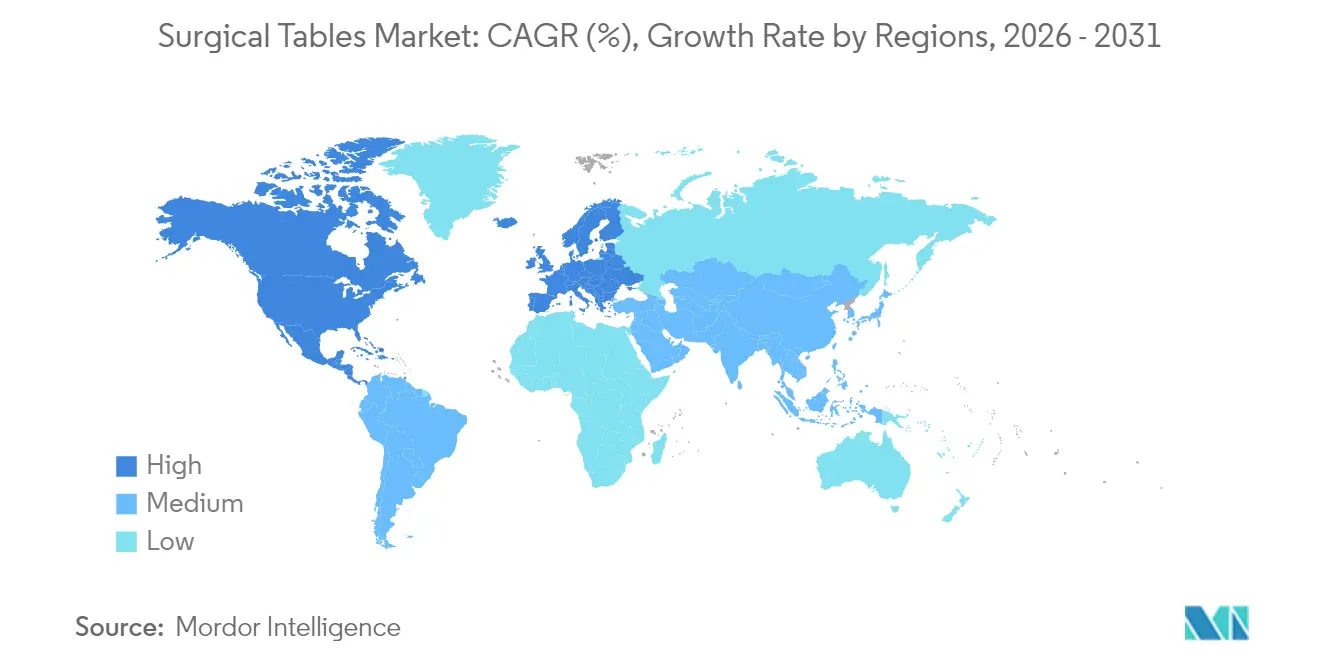

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Tables Market Analysis by Mordor Intelligence

The Surgical Tables Market size was valued at USD 1.57 billion in 2025 and estimated to grow from USD 1.65 billion in 2026 to reach USD 2.13 billion by 2031, at a CAGR of 5.24% during the forecast period (2026-2031). Demographic aging is lifting orthopedic and cardiovascular caseloads, outpatient care is shifting more procedures into ambulatory surgical centers (ASCs), and robotics‐ready operating rooms (ORs) are raising the technical bar for patient-positioning platforms. Hospitals are upgrading to carbon-fiber radiolucent tops to support real-time imaging, while sustainability mandates in Europe and North America reward energy-efficient modular designs. Competitive strategies increasingly revolve around bundled OR ecosystems that tie surgical tables to imaging, lighting, and robotic offerings, helping providers simplify procurement and integration. Premium-segment manufacturers are also launching service and financing programs that mitigate capital-budget constraints for mid-tier hospitals.

Key Report Takeaways

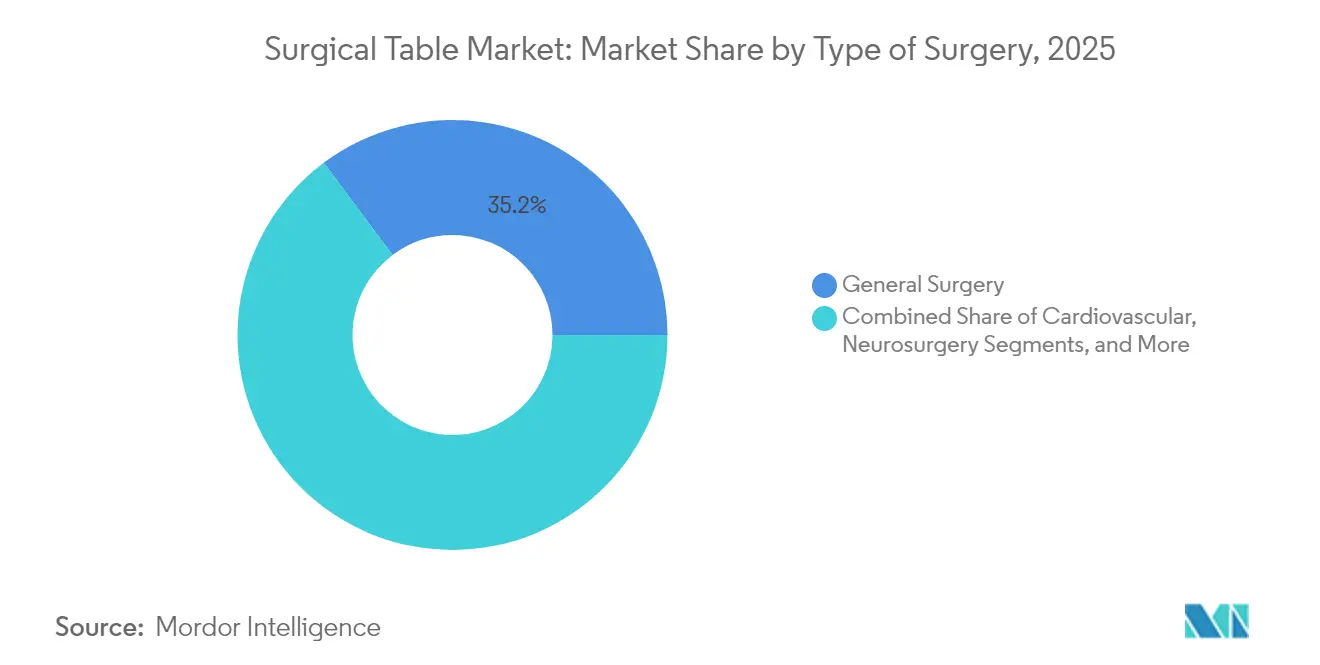

- By type of surgery, general surgery held 35.22% of the surgical tables market share in 2025, whereas orthopedic & trauma procedures are projected to grow at a 6.49% CAGR to 2031.

- By material, metal platforms commanded 52.05% of the surgical tables market size in 2025; carbon-fiber composite tables are forecast to expand at a 5.72% CAGR through 2031.

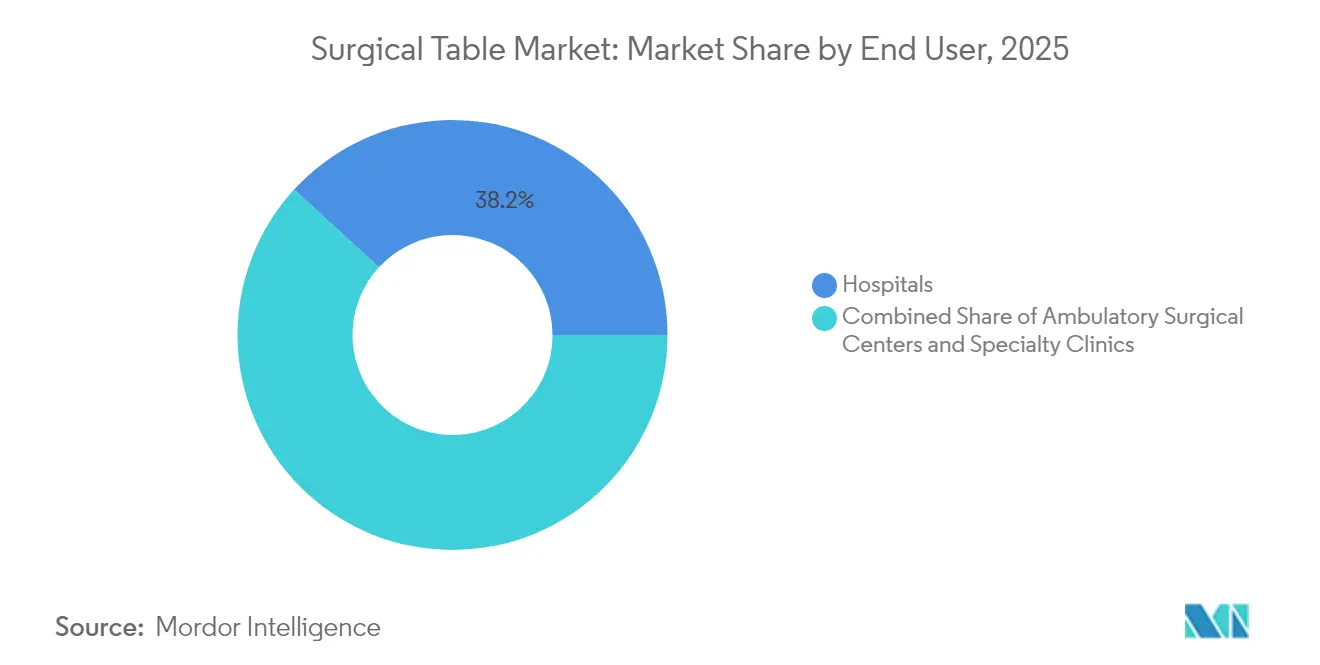

- By end user, hospitals accounted for 38.18% of the surgical tables market share in 2025, while ASCs are advancing at a 6.03% CAGR to 2031.

- By geography, North America led with a 38.30% revenue share in 2025; Asia-Pacific is the fastest-growing region with a 6.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Surgical Tables Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical procedure volumes & ASC expansion | +1.2% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

| Aging population driving higher orthopedic & cardiac caseload | +1.0% | Global, particularly North America, Europe, and developed APAC markets | Long term (≥ 4 years) |

| Integrated-OR & robot-ready table upgrades | +0.8% | North America & EU, expanding to APAC core markets | Medium term (2-4 years) |

| Carbon-fiber radiolucent tops enabling intra-op imaging | +0.6% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Surge in minimally invasive & robotic surgeries requiring advanced patient-positioning functionality | +0.7% | North America & Europe, with rapid expansion to APAC | Medium term (2-4 years) |

| Hospital sustainability mandates favoring energy-efficient, modular table platforms | +0.4% | Europe & North America, with emerging adoption in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising surgical procedure volumes & ASC expansion

Outpatient sites perform the bulk of U.S. procedures and continue to attract complex orthopedic and gastroenterology cases because they operate at 45-60% lower costs than hospital outpatient departments and cut average wait times by 20% [1]Health Industry Distributors Association, “Ambulatory Surgery Center Market Report,” Health Industry Distributors Association, hida.org. ASC growth is encouraging vendors to deliver compact, multi-specialty tables that fit smaller footprints and rotate quickly between cases. To keep capital outlays down, manufacturers now market modular bases that accept specialty tops, letting centers defer upgrades until volumes justify them. Group-purchasing contracts and equipment-as-a-service financing further lower barriers to adoption.

Aging population driving higher orthopedic & cardiac caseload

Population aging elevates demand for joint reconstruction, fracture repair, and interventional cardiology procedures that require precise positioning and bariatric weight limits. U.S. orthopedic volumes are projected to reach 6.6 million procedures annually, reinforcing the need for heavy-load lifts and pressure-injury mitigation sensors. Bariatric-capable tables with integrated pressure mapping, such as XSENSOR’s ForeSite OR, reduce hospital-acquired pressure injuries that affect up to 45% of surgical patients.

Integrated-OR & robot-ready table upgrades

Hospitals moving toward single-vendor ecosystems increasingly bundle angiography systems, C-arms, and robotics with compatible surgical tables. Intuitive Surgical’s da Vinci 5 platform, featuring Force Feedback that can cut tissue force by 43%, demands ultra-stable, data-connected tables to avoid motion artifacts during robotic manipulation [2]David Robinson, “Haptic Feedback in Intuitive’s da Vinci 5,” Intuitive Surgical, intuitive.com. Siemens Healthineers’ Artis OR Table couples a radiolucent floating top with angiography gantries, illustrating how integrated solutions improve workflow and simplify service contracts.

Carbon-fiber radiolucent tops enabling intra-op imaging

Carbon fiber supports low-attenuation imaging across spinal, trauma, and endovascular procedures. Composite sandwich designs using LAST-A-FOAM FR-3700 cores trim weight while lowering raw-material costs and machining time. A 2025 pelvic-fracture study showed that an auxiliary carbon-compatible table priced at USD 700 matched the imaging quality of a USD 50,000 dedicated carbon table, highlighting disruptive potential in cost-sensitive markets [3]Yong-Cheol Yoon, “Innovating Pelvic Fracture Surgery: Development and Evaluation of a New Surgical Table for Enhanced C-Arm Imaging and Operational Efficiency,” Journal of Clinical Medicine, mdpi.com.

Surge in minimally invasive & robotic surgeries requiring advanced patient-positioning functionality

Robotics extends minimally invasive techniques to complex procedures, pushing tables to offer extreme Trendelenburg angles, 360° rotation, and quick-lock accessories. Studies on da Vinci 5 Force Feedback show improved novice-surgeon performance, fueling broader deployment and table upgrades inside teaching hospitals.

Hospital sustainability mandates favoring energy-efficient, modular table platforms

European and North American health systems now reference ASHRAE 189.3 and ISO 50001 in procurement to achieve net-zero targets. Vendors respond with lower standby power draws, recyclable components, and refurbishable modules that comply with FDA remanufacturing guidance issued in May 2024. Lifecycle assessments demonstrating double-digit energy savings increasingly influence tender scores, especially in public-sector hospitals.

Restraints Impact Analysis of Surgical Tables Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance |

|---|---|---|

| Premium pricing & capex freezes in mid-tier hospitals | -0.8% | Global, with strongest impact in emerging markets and rural healthcare systems |

| Shortage of skilled OR technologists for advanced tables | -0.5% | Global, particularly acute in North America and Europe |

| Carbon-fiber supply chain volatility | -0.4% | Global, with particular impact on premium segment manufacturers |

| Stricter reprocessing and regulatory compliance raising lifetime ownership costs for providers | -0.3% | Global, with strongest impact in highly regulated markets like North America and Europe |

| Source: Mordor Intelligence | ||

Premium pricing & capex freezes in mid-tier hospitals

Rising operating costs and inflation have caused smaller hospitals to delay capital purchases, selectively opting for refurbished equipment or multi-year leasing. Medicare reimbursement has slipped for total joint arthroplasty even as volumes climb, compressing margins and making high-end imaging-compatible tables harder to justify [4]Editorial Staff, “Medicare Reimbursement Trends in Total Joint Arthroplasty,” Journal of Orthopaedic Experience & Innovation, journals.sagepub.com. Vendors are countering with staged upgrade paths that let facilities install a base and add connectivity kits later, plus service contracts that bundle maintenance, remanufacturing compliance, and software updates.

Shortage of skilled OR technologists for advanced tables

Perioperative staffing gaps slow the roll-out of high-spec tables that need specialized calibration and troubleshooting. Annals of Surgery projects a shortage of more than 100,000 surgeons by 2030, implying parallel deficits in technologists trained to manage complex patient-positioning protocols. Training roadshows such as Medtronic’s mobile labs attempt to bridge the gap by bringing simulation trucks to 38 states annually, yet turnover still drives upskilling costs for providers.

Carbon-fiber supply chain volatility

High-grade fiber and epoxy pricing swings complicate procurement for premium tables. Manufacturers hedge through multi-sourcing and by engineering hybrid composite-metal decks that decrease fiber content without sacrificing imaging quality. Supply disruption encourages providers to diversify vendors, raising qualification costs and delaying projects in trauma centers that rely on radiolucent capability for intraoperative scans.

Stricter reprocessing and regulatory compliance raising lifetime ownership costs

The FDA’s 2024 final guidance on remanufacturing requires any significant refurbishment to meet new-device quality standards, increasing documentation burdens and, in turn, service contract fees. Facilities must also validate cleaning cycles to protect delicate sensors embedded in next-generation tops, adding recurring operational spend that can erode return-on-investment models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Surgical Tables Market Segment Analysis

By Type of Surgery:

General surgery maintains dominance while orthopedic momentum buildsGeneral surgery held 35.22% of the surgical tables market share in 2025. Hospitals favor versatile, quick-switch platforms that serve appendectomies in the morning and bariatric cases in the afternoon. The segment’s broad procedural mix supports economies of scale for replacement purchases, and its workflows align with standardized accessories such as removable armboards and lithotomy leg supports. Meanwhile, robotic cholecystectomy adoption is nudging many providers to replace manual hydraulic bases with motorized column systems featuring footswitch memory profiles for speed and consistency.

Orthopedic & trauma procedures are set to log a 6.49% CAGR to 2031, the fastest in the market. Knee and hip robotics like Zimmer Biomet’s TMINI Miniature Robotic System depend on rigid, low-vibration surfaces that maintain sub-millimeter accuracy during milling. Table manufacturers respond with longitudinal slide and tilt ranges that expose distal femurs without repositioning, shortening anesthesia times and radiographic exposure. Neurosurgery and cardiovascular specialties occupy smaller shares but command premium pricing because they demand carbon tops, 360° C-arm clearance, and head fixation interfaces that integrate with navigation systems. As hospitals pursue cross-disciplinary hybrid rooms, demand is shifting toward universal platforms that support spinal, vascular, and cranial workflows on the same chassis, reducing inventory and service overhead.

By Material:

Metal reliability faces composite innovationMetal frames made up 52.05% of surgical tables market size in 2025, prized for durability, easy part availability, and lower acquisition prices. Stainless steel bases withstand repeated disinfectant exposure and accept heavier patients, meeting safety regulations without special training. However, clinicians increasingly request radiolucency to avoid imaging artifacts; here, carbon-fiber composite decks excel. Composite tables are forecast to grow at a 5.72% CAGR, benefiting from foam-core sandwich architecture that cuts weight by 25% and passes CT photons with minimal attenuation. Manufacturers like ACP Composites incorporate FR-3700 polyurethane cores to balance cost and stiffness. Hybrid designs merge aluminum bases with bolt-on carbon tops, giving budget-constrained facilities an incremental path to imaging capability and reducing dependence on volatile fiber supply chains.

By End User:

Hospital volume leadership meets ASC dynamismHospitals generated 38.18% of 2025 revenue, reflecting their role in high-acuity, multi-disciplinary care that requires full-featured, robot-ready tables. They also drive demand for integrated fleet management software that tracks utilization, service schedules, and sensor diagnostics across dozens of rooms. ASCs, however, are expanding at a 6.03% CAGR. Their growth is propelled by payer site-neutral policies and consumer preference for same-day surgery. To win this segment, manufacturers package compact bases with specialty tops—orthopedic traction, cystoscopy, or spine imaging—delivered as factory-calibrated kits. Specialty clinics, although smaller, often pioneer novel technologies; early adoption of AI-based pressure-mapping pads illustrates how niche settings influence broader procurement once evidence of value emerges.

Geography Analysis

North America Surgical Tables Market

North America captured 38.30% of 2025 revenue, supported by high procedure volumes and early uptake of advanced robotics. The U.S. ASC market alone could reach nearly USD 59 billion in revenue by 2028, spurring orders for cost-optimized, quick-turnover tables. Medicare’s push for site-neutral reimbursement further accelerates equipment migration from hospitals to ASCs, while regional service networks from Getinge and STERIS reduce downtime and reinforce brand stickiness.

Europe Surgical Tables Market

Europe forms a mature, replacement-driven market where sustainability and regulatory rigor shape purchasing. ASHRAE 189.3 guidelines influence tender scores, nudging buyers toward energy-efficient motor drives and recyclable packaging. Getinge’s Surgical Workflows segment posted 15.6% revenue growth in Q4 2023, helped by hospitals refreshing legacy fleets with integrated OR suites. Capital grants tied to green public-procurement criteria are likely to sustain steady demand despite flat procedural growth.

APAC Surgical Tables Market

Asia-Pacific is the fastest-growing region, projected at a 6.56% CAGR. Healthcare infrastructure investment and widening medical-tourism flows drive adoption of hybrid rooms in China, India, and ASEAN states. Medtronic’s Robotics Experience Studio in Singapore illustrates how training hubs accelerate diffusion of advanced OR technologies throughout the region. Venture funding dipped 22% over the past two years, yet domestic manufacturing initiatives in Vietnam and Korea help offset import tariffs and supply bottlenecks, supporting localized table production.

Regulatory Landscape

Surgical tables are regulated as medical devices, requiring quality-system controls and market authorization aligned to each major jurisdiction. In the European Union, operating tables fall under Regulation (EU) 2017/745 (MDR), with EUDAMED mandatory use approaching; the 28 May 2026 date marks the milestone for initial actor and UDI registrations. In the United States, the FDA medical device regulatory framework governs establishment registration and applicable premarket pathways, while tariff actions under Section 301 in 2026 influence landed costs and procurement decisions for OEMs and health systems.

Value Chain Analysis

The value chain begins with upstream materials and component suppliers, notably medical-grade stainless steel frames, carbon-fiber radiolucent tabletop tops, electro-mechanical actuators, control electronics, and specialty polymers for pads and accessory interfaces. OEMs such as Stryker, Getinge, STERIS, Hill-Rom (Baxter), Skytron, and Mizuho OSI assemble systems and validate performance and safety against standards such as IEC 60601-2-46, then configure tables with procedure-specific tops and accessories for general surgery, orthopedic and trauma, cardiovascular, and neurosurgery applications. Downstream, distribution and installation depend on regional service networks and specialized logistics providers that can handle heavy, high-value equipment, coordinate site readiness, and manage commissioning and training. Bottlenecks in this chain center on long lead times for actuator and controller subassemblies and intermittent electronics availability for connected-table features, while carbon-fiber feedstock volatility affects premium radiolucent platforms. Health systems are also pushing item-master standardization and supply chain integration to simplify multi-site purchasing and service, reinforcing bundled offerings that combine tables with other OR infrastructure and lifecycle support.

Competitive Landscape

Competition is moderate, with technological breadth and lifecycle service capabilities acting as key differentiators. Getinge, Stryker, and STERIS combine tables, lights, and infection-control equipment into bundled proposals, streamlining hospital procurement and reinforcing installed-base loyalty. Stryker recorded 10.7% organic sales growth in Q4 2024, crediting strong demand for capital products, including surgical tables, across its MedSurg segment.

Strategic acquisitions are reshaping the field. KARL STORZ’s planned purchase of Asensus Surgical extends its OR portfolio into digital laparoscopy, potentially unlocking cross-selling synergies with high-spec tables configured for 3D vision towers. Carbon-fiber innovators seek partnerships with composite material suppliers to secure feedstock and protect margins against volatility. Service innovation also figures prominently: vendors embed predictive analytics sensors to pre-empt downtime, positioning premium service contracts as a hedge against the FDA’s remanufacturing compliance costs.

White-space opportunities persist in emerging markets, where cost-effective universal bases address multispecialty demand without the overhead of high-end robotics. Smaller manufacturers targeting these geographies often collaborate with regional distributors to localize service and training, but they must still demonstrate regulatory compliance and imaging compatibility to gain traction among fast-modernizing hospitals.

Surgical Tables Industry Leaders

Steris Plc

Skytron LLC

Stryker Corporation

Mizuho OSI

Getinge AB

- *Disclaimer: Major Players sorted in no particular order

Surgical Tables Market Companies Covered in this Report

- Getinge

- Stryker

- Steris plc

- Trumpf Medical (Baxter/Hill-Rom)

- Mizuho

- Skytron

- Schaerer Medical AG

- Merivaara

- Alvo Medical

- LINET Group

- Mindray Medical Intl.

- Opt SurgiSystems Srl

- Eschmann Holdings

- Allengers Medical Systems

- Nuvo Inc.

- AGA Sanitätsartikel GmbH

- Meditek Canada

- Staan Bio-Med Engg. Pvt Ltd

Market Opportunities and Future Outlook

Robotics-ready operating rooms and integrated OR ecosystems are evident in the market, with a May 2026 Johnson & Johnson pivotal study for the OTTAVA robotic surgical system showing robotic arms integrated into a standard-sized surgical table. Hospitals upgrading to radiolucent and hybrid-room workflows are seeking carbon-fiber and hybrid composite solutions that reduce imaging artifacts while maintaining load capacity and durability. A second opportunity area is differentiation through precision positioning, bariatric capability, and workflow efficiency tailored to ambulatory surgical centers and multi-specialty rooms. In 2026, Mindray unveiled the HyBase V8 mobile operating table and Famed Zwiec introduced X-Line operating tables with high positioning precision, while sustainability-focused procurement in Europe and North America, including ISO 50001 tied scoring, supports modular designs that can be refurbished and updated in line with FDA remanufacturing guidance issued in May 2024, expanding the service and lifecycle programs.

Recent Industry Developments in Surgical Tables Market

- February 2026: Skytron, LLC secured a Department of Veterans Affairs contract valued at USD 1,232,121 for operating tables and associated accessories. The contract reflects ongoing federal procurement for capital equipment in the surgical table segment and extends Skytron's service and installation capabilities through a formal procurement channel.

- April 2025: Skytron introduced the Voir portfolio to the surgical market, expanding its video integration capabilities alongside core surgical infrastructure. This expansion aligns with providers seeking integrated OR ecosystems that streamline procurement and service support.

- December 2024: Getinge completed installation of its Surgical Workflows portfolio, including OR tables, at UT Health San Antonio Multispecialty and Research Hospital. The reference-site deployment demonstrates a shift toward integrated suites that standardize workflows and consolidate service contracts across new hospital builds.

Surgical Tables Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the surgical tables market covers revenue generated from new operating tables used to position patients during procedures, including powered and non-powered models, that are purchased by hospitals, ambulatory surgical centers, and specialty clinics.

Scope exclusions: Refurbished or rental tables and disposable patient positioning aids are excluded from the market value in this methodology.

Segments Covered in This Report

- By Type of Surgery

- General Surgery

- Orthopedic & Trauma

- Cardiovascular

- Neurosurgery

- Others

- By Material

- Metal

- Carbon-fiber Composite

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with mapping a demand picture around surgical activity and health system capacity, then translating it into equipment replacement behavior. We anchored the macro environment using public sources such as CDC procedure and hospital utilization statistics, OECD health indicators, and WHO health expenditure and infrastructure datasets.

To convert those signals into device demand, we reviewed sources such as US FDA device databases and safety communications, UN Comtrade import and export data for relevant equipment categories, and peer-reviewed clinical and biomedical journals that describe operating room setups and imaging needs. Company annual reports, investor presentations, and reputable press coverage were used to understand product positioning, pricing direction, and channel focus. Select paid database subscriptions for company financials and patent databases were referenced to validate revenue ranges and innovation intensity where public disclosure was limited. These examples are illustrative only, and many other public sources were also consulted for data collection, validation, and clarification during the research process.

Primary Interviews and Surveys

Primary work focused on cross-checking replacement cycles, typical purchasing bundles, and average selling price movement across powered and non-powered tables, before assumptions were finalized. We spoke with manufacturers, distributors, hospital procurement teams, and operating room leaders across APAC, EMEA, and the Americas, which helped close gaps where public reporting was thin and align the model to actual buying behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | APAC: 47% |

| Mid tier: 42% | Functional/Unit leaders: 27% | EMEA: 34% |

| Smaller Players: 22% | Managers: 59% | Americas: 19% |

Market-Sizing & Forecasting

Sizing begins with a top-down build that reconstructs the addressable demand pool from surgical procedure volumes, operating room and hospital infrastructure growth, and typical table-to-OR equip rates, then adjusts for replacement timing. When the market is split by region, we apply the same logic separately because surgical mix, facility build-out, and procurement cycles do not move in parallel everywhere.

Key inputs that shaped the model included annual surgical procedure counts by major specialty, number of hospitals and ambulatory surgical centers in operation, new operating room additions, replacement cycle ranges for core OR tables, and price differences between powered and non-powered configurations (including imaging-compatible platforms where applicable). Where data was not directly available, gaps were handled through bounded ranges, then narrowed using expert feedback and consistency checks against trade flows and disclosed revenue cues.

Forecasting used scenario analysis supported by a light multivariate regression. We treated procedure growth, healthcare capital spending direction, and facility expansion as the main drivers, then stress-tested under slower and faster replacement cases. Results were corroborated with selective bottom-up approximations, such as sampled average selling prices multiplied by estimated unit volumes from channel checks, to validate totals and tune the final curve without forcing a complete supplier roll-up.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, so the final number is not dependent on a single dataset or one interview set. We check variances against related indicators such as procedure intensity, facility counts, and trade direction, then investigate outliers that appear at the regional or year level.

Before sign-off, the model and assumptions go through multi-step internal review, and respondents may be re-contacted when a pricing step-change, replacement-cycle shift, or policy update produces a meaningful swing. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Surgical Tables Market Size Measured Against Other Published Estimates

Published market sizes for surgical tables can look different even when they appear to cover the same product. The spread usually comes down to what is counted and when it is counted. Differences in base year selection, whether values reflect shipments or installed-base replacement, and how pricing is normalized across regions often explain the variation.

The benchmark table shows a noticeable range, and in Mordor Intelligence's model the value is limited to new surgical tables sold to hospitals, ambulatory surgical centers, and specialty clinics. Refurbished or rental tables and disposable positioning aids are not counted in the revenue pool. Some external estimates anchor earlier years and then apply a single growth rate, which can understate step-ups tied to OR expansion cycles or overstate growth if replacement timing is assumed too aggressive. Currency conversion timing and whether imaging-compatible platforms are treated as part of the table value or split out can also shift the final USD number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.65 B (2026) | |

| Global Consultancy A | USD 1.54 B (2025) | Uses an earlier base year and may blend operating table revenues with a broader operating room equipment context in some regions, which shifts scope and the pricing normalization used for totals. |

| Industry Publisher B | USD 1.10 B (2024) | Anchors on an older year and applies a smoother growth path over a longer horizon, and the inclusion rules for imaging-compatible platforms and specialty tables are not as clearly tied to end-user purchasing behavior. |

The side-by-side comparison mainly shows that year choice, inclusion of adjacent equipment or secondary markets, and pricing and currency handling account for most of the differences. By tying the model to procedure-driven demand, facility capacity signals, and validated replacement behavior, we can keep assumptions visible and repeatable when the market is updated.

Key Questions Answered in the Report

What is the current Surgical Tables Market size?

It is valued at USD 1.65 billion in 2026 and is forecast to grow at 5.24% annually to reach USD 2.13 billion by 2031.

Who are the key players in Surgical Tables Market?

Steris Plc, Skytron LLC, Stryker Corporation, Mizuho OSI and Getinge AB are the major companies operating in the Surgical Tables Market.

What challenges restrict adoption of advanced surgical tables?

Capital-budget constraints at mid-tier hospitals, shortages of skilled OR technologists, carbon-fiber supply volatility, and stricter FDA remanufacturing rules raise lifetime ownership costs.

Which region has the biggest share in Surgical Tables Market?

In 2025, the North America accounts for the largest market share in Surgical Tables Market.

Which region offers the highest growth potential?

Asia-Pacific leads in growth with a 6.56% CAGR, buoyed by hospital construction, medical tourism, and rapid uptake of robotics-ready OR infrastructure.

Page last updated on: