Medical Animation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

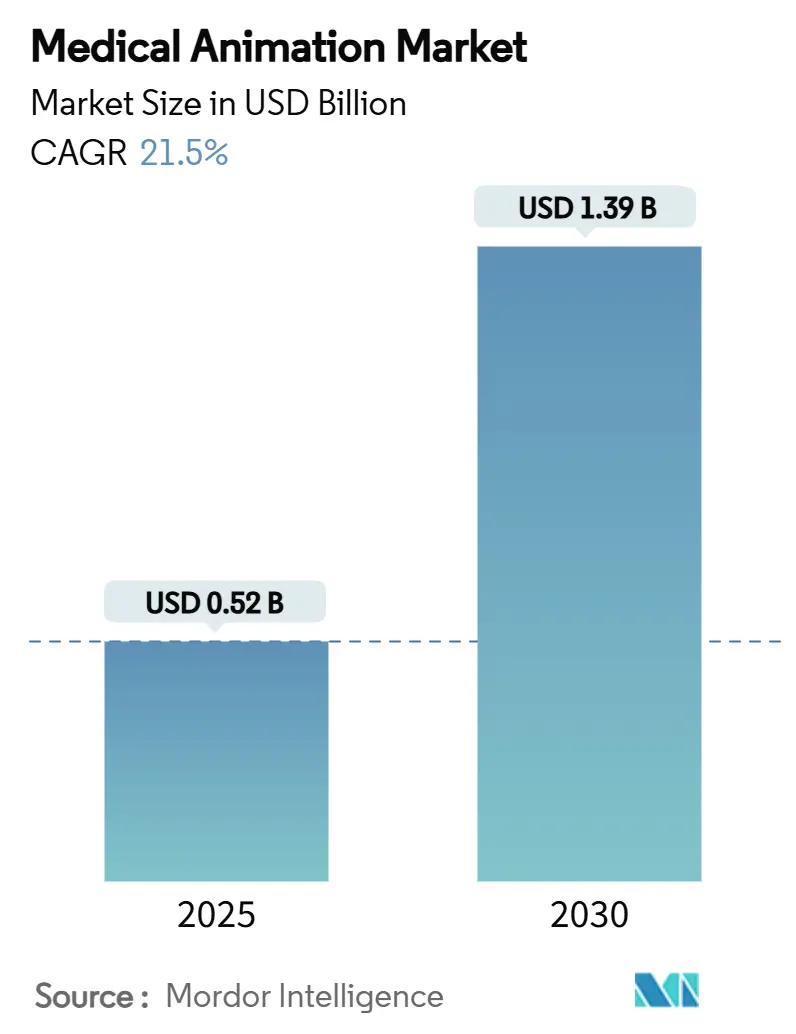

| Market Size (2025) | USD 0.52 Billion |

| Market Size (2030) | USD 1.39 Billion |

| Growth Rate (2025 - 2030) | 21.50% CAGR |

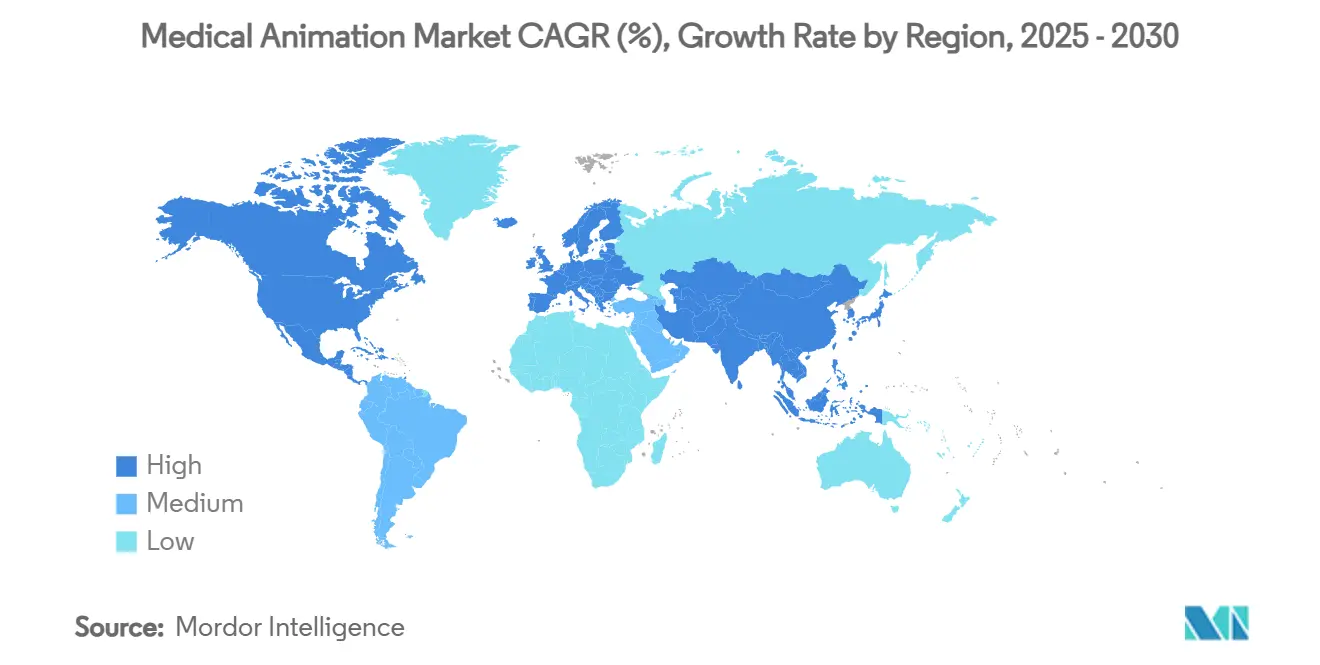

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Animation Market Analysis by Mordor Intelligence

The medical animation market size stands at USD 0.52 billion in 2025 and is projected to reach USD 1.39 billion by 2030, reflecting a vibrant 21.5% CAGR during the forecast period. Surging demand for AI-assisted 3D and 4D visualizations, expanding use of virtual and augmented reality in surgical training, and growing regulatory acceptance of synthetic visuals are catalyzing growth across pharmaceutical, biotech, and healthcare systems. Established studios are blending generative algorithms with real-time rendering to cut production cycles, while device and drug developers deploy evidence-rich animations to speed dossier reviews and strengthen market differentiation. North America leads current revenues, but Asia Pacific is scaling swiftly on the back of digital health investments, expanding medical education programs, and cost-competitive production hubs. Across every region, healthcare providers recognize that animated content supports more transparent patient communication, more efficient clinician training, and measurable gains in treatment adherence.

Key Report Takeaways

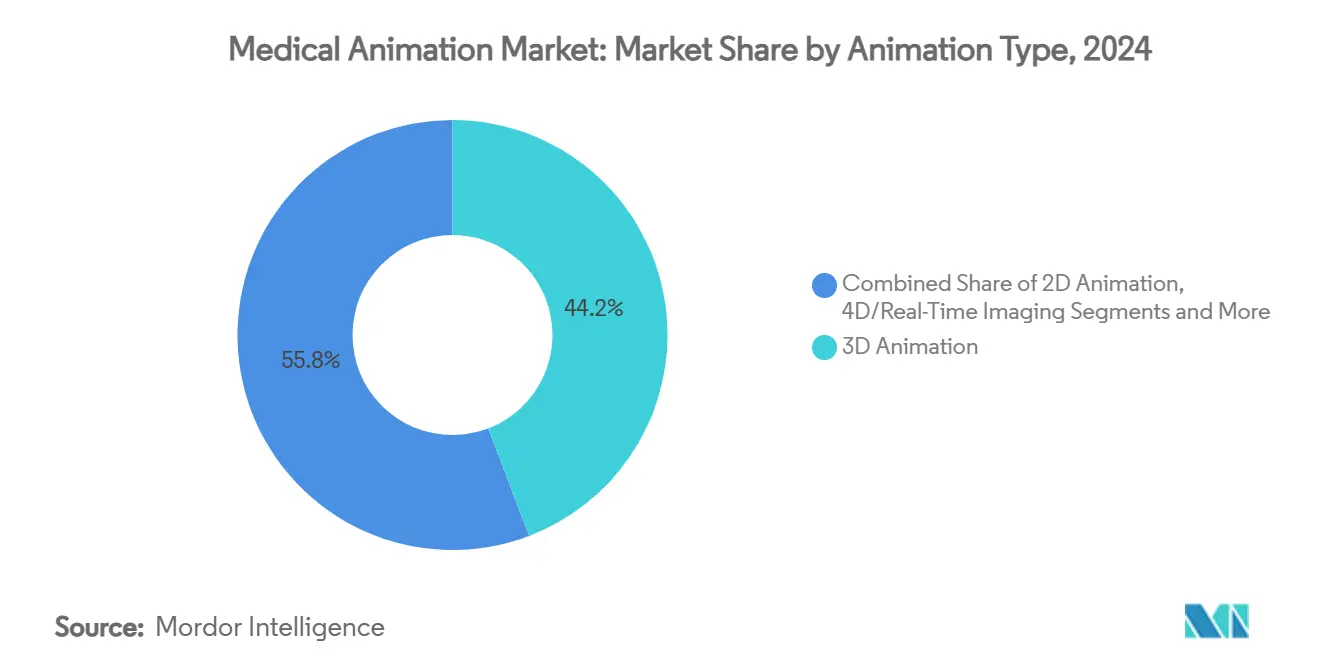

- By animation type, 3D captured 44.2% of the medical animation market share in 2024, while 4D/real-time imaging is forecast to expand at a 19.0% CAGR through 2030.

- By application, drug mechanism of action led with 37.1% revenue share in 2024; patient education is advancing at an 18.0% CAGR to 2030.

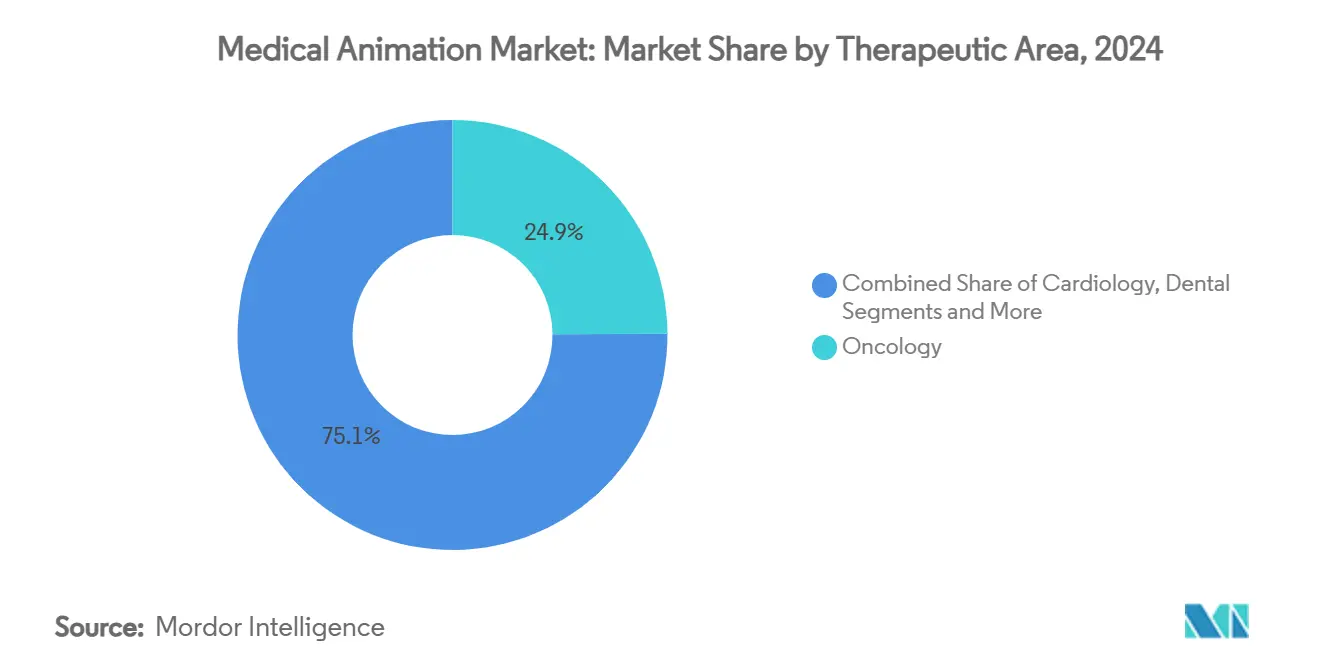

- By therapeutic area, oncology held 24.9% of the medical animation market size in 2024 whereas orthopedics records the fastest 17.0% CAGR between 2025 and 2030.

- By end user, life science companies accounted for 41.0% share in 2024; academic and research institutes are growing at 16.2% CAGR through 2030.

- By geography, North America commanded 44.6% revenue share in 2024, while Asia Pacific is projected to post an 18.5% CAGR to 2030.

Market Trends and Insights

Drivers Impact Analysis of Medical Animation Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 3D/4D adoption for drug MOA & marketing | +3.50% | Global; strongest in North America & EU | Medium term (2-4 years) |

| Mobile & digital patient-education demand | +4.20% | Global; highest momentum in APAC | Short term (≤2 years) |

| Complex-disease surgical training needs | +2.80% | North America & EU core; expanding to APAC | Long term (≥4 years) |

| Device innovators using animation for regulatory dossiers | +1.90% | North America & EU | Medium term (2-4 years) |

| AI-generated animation shortens production cycles | +1.80% | Global; early adoption in developed markets | Short term (≤2 years) |

| VR/AR with haptics for remote low-resource training | +1.70% | Global; emphasis on emerging markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

3D/4D Adoption for Drug MOA & Marketing

Pharmaceutical companies are increasingly integrating 3D and 4D visualizations into dossier submissions to illustrate intricate molecular interactions, a trend reinforced by the FDA’s precedent-setting approval of roughly 1,000 AI-enabled medical devices.[1]JAMA Network, “Regulation of Artificial Intelligence–Enabled Medical Devices by the FDA,” jamanetwork.com These dynamic stories help regulators grasp targeted therapy pathways, elevate promotional campaigns, and support omnichannel engagement strategies. Early adopters are already pairing real-time imaging with predictive modeling to personalize drug-mechanism videos for sub-populations, reinforcing the commercial value of high-granularity visuals. Studios that combine scientific rigor with cinematic polish command premium margins and enjoy repeat business from top 20 pharma sponsors. As blockbuster biologics proliferate, demand for immersive, mechanism-centric assets is set to intensify across mature and emerging markets.

Mobile & Digital Patient-Education Demand

Telehealth expansion and smartphone penetration are pushing providers to embed concise, language-localized animations inside patient portals and care apps. India-based ERemedium has shown that 3D videos delivered at the point of care can lift consultation efficiency and recall scores among diverse populations. Systematic reviews confirm that animated explanations outperform static leaflets on knowledge retention and adherence metrics.[2]MDPI, “AI-Guided Force Prediction for Augmented Reality Surgical Trainers,” mdpi.com Hospitals leveraging QR-code video systems, such as Nucleus Medical Media’s QRx platform, report measurable gains in satisfaction surveys and reduced follow-up calls. These outcomes align with value-based reimbursement models, encouraging wider adoption of evidence-based storytelling in both developed and resource-constrained settings.

Complex-Disease Surgical Training Needs

Rising surgical complexity in oncology, spine, and neuro disciplines is fueling a shift from didactic lectures to simulation-rich curricula. Ghost Productions’ Wraith-VR suite enables geographically dispersed surgeons to practice high-risk steps collaboratively, trimming travel costs and aligning competencies. Academic partners validate that immersive rehearsal lowers intra-operative errors and accelerates skill acquisition, a priority as practitioners adopt novel robotic and minimally invasive techniques. Complementary advances such as biomimetic tissue phantoms and AI-guided force feedback round out multi-modal training pipelines, bridging the gap between virtual anatomy and tactile nuance. Vendors able to bundle realistic animation with haptics and analytics stand to capture a growing slice of institutional budgets allocated to patient-safety initiatives.

Device Innovators Using Animation for Regulatory Dossiers

Class III device sponsors now routinely embed cinematic cut-aways, cross-sectional fly-throughs, and stress-test simulations in Premarket Approval packages to substantiate safety mechanisms.[3]U.S. Department of Health and Human Services, “Strategic Plan for Artificial Intelligence in Health,” hhs.gov For example, Ghost Productions’ visualization of Varithena’s foamed micro-occlusion dynamics offered reviewers clear evidence of controlled vein closure, contributing to a smoother approval path. Animated prototypes also strengthen investor pitches and surgeon-education toolkits, creating multi-channel ROI on the initial content spend. As EU MDR and US FDA continue to refine data requirements, device firms that front-load compelling visuals may compress review cycles, accelerate launch timelines, and out-position rivals in crowded therapeutic categories.

Restraints Impact Analysis of Medical Animation Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production Costs Of Premium Content | -2.10% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Shortage Of Certified Medical Animators | -1.40% | North America & EU primarily | Short term (≤ 2 years) |

| Regulatory Scepticism Toward Synthetic Visuals | -1.80% | North America & EU regulatory markets | Medium term (2-4 years) |

| Cloud-Asset Data-Security/Privacy Risk | -1.20% | Global, with emphasis on HIPAA-regulated markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Costs of Premium Content

Creating rigorously validated 3D or 4D sequences demands specialized software, GPU farms, and interdisciplinary teams that include PhD-level scientists. A 60-second premium animation can cost between USD 20,000 and USD 150,000, a range that stretches budgets at smaller hospitals and NGOs. Validation loops add further expense as subject-matter experts and regulatory reviewers iterate on molecular accuracy, labeling, and risk messaging. While cloud rendering and AI assistive tools are lowering some overheads, price sensitivity remains acute in emerging economies, limiting the adoption of high-resolution content for routine care. Studios are exploring tiered service models to broaden access, but the cost barrier continues to temper overall market acceleration.

Shortage Of Certified Medical Animators

The Association of Medical Illustrators accredits a limited pool of professionals who possess both biomedical knowledge and advanced animation skills, creating talent bottlenecks. Demand for such hybrid expertise now outpaces supply, leading to extended project queues and wage inflation in key hubs. Large studios mitigate risk by investing in continuous training and AI-supported workflows, yet quality control remains a chokepoint as projects scale. Universities are launching interdisciplinary programs, but graduates take years to accumulate clinical fluency. Until the talent pipeline deepens, production capacity constraints will persist as a tangible headwind to the medical animation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Medical Animation Market Segment Analysis

By Animation Type:

3D Dominance Faces 4D Disruption3D animation captured 44.2% of the medical animation market share in 2024, underscoring its entrenched role in regulatory submissions, marketing campaigns, and foundational e-learning modules. The segment’s reliability, device agility, and cost profile make it the default choice when projects require visual depth but not real-time interactivity. Despite this dominance, 4D and real-time imaging solutions are expanding at a 19.0% CAGR as clinicians demand motion-synchronized visuals for radiation therapy planning, cardio-pulmonary assessments, and intra-operative guidance.

Market participants advancing 4D pipelines integrate volumetric captures with physics-based engines to replicate tissue deformation and blood-flow dynamics in near real time. Such immersive outputs command premium pricing and attract multidisciplinary R&D teams seeking to visualize patient-specific data. AI-assisted segmentation accelerates workflow efficiency, narrowing the cost gap between 3D and 4D deliverables. As hardware accelerators and XR headsets gain clinical certification, 4D adoption is set to redraw competitive boundaries across the medical animation market.

By Application:

Patient Education Accelerates Beyond Drug MOADrug mechanism of action assets retained 37.1% revenue leadership in 2024, confirming the pharmaceutical sector’s reliance on concise molecular storytelling to secure approvals and support omnichannel marketing. However, patient education modules are growing at an 18.0% CAGR, propelled by evidence that animations improve comprehension scores and adherence levels in value-based care environments.

Regulated payers now reward hospitals for deploying multimedia tutorials that cut readmissions, prompting providers to license expansive content libraries or commission tailored sequences addressing language, literacy, and cultural nuances. Meanwhile, surgical training simulations translate complex procedures into stepwise visual playbooks that reduce OR errors and accelerate credentialing. Collectively, these dynamics diversify revenue streams within the medical animation market, encouraging studios to optimize pipelines for both clinician-facing precision and consumer-grade storytelling.

By Therapeutic Area:

Oncology Leadership with Orthopedics MomentumOncology accounted for 24.9% of the medical animation market size in 2024, reflecting the discipline’s need to demystify multi-modal regimens involving immunotherapies, radiotherapy, and targeted biologics. Rapid advances in personalized medicine and companion diagnostics require updated visuals that track biomarker stratification and adaptive dosing strategies, sustaining high content turnover. Orthopedics, by contrast, is moving fastest at a 17.0% CAGR as sports medicine, trauma fixation, and robotic joint-replacement techniques gain traction among aging populations.

Cardiology harnesses 4D imaging to model valvular interventions and electrophysiology mapping, while neurology relies on sub-millimeter resolution to depict deep-brain stimulation or tumor resection pathways. Dental and cosmetic surgery segments adopt chairside animations to manage expectations and boost case acceptance. Each therapeutic niche values fidelity, but budget envelopes and use-case cadence vary, driving studios to craft modular asset strategies to serve the broad canvas of medical animation market demand.

By End User:

Academic Growth Challenges Life Science DominanceLife science companies generated 41.0% of 2024 revenues as they embedded animations across discovery, clinical development, and brand campaigns. Comprehensive service contracts with top 20 pharma groups often bundle mechanism videos, investor decks, and congress booths into multi-year frameworks. Academic and research institutes, though, are posting a robust 16.2% CAGR, spurred by curriculum digitization, cross-disciplinary grants, and ed-tech partnerships such as Cengage Group’s 2025 purchase of Visible Body’s 24,000-asset library cengage.com.

Hospitals and clinics lean on point-of-care animations to shave consultation times and document informed consent, while device manufacturers commission detailed walkthroughs for training and post-market surveillance. Forensic and legal entities round out demand with high-fidelity reconstructions for courtroom exhibits. As remote learning and tele-medicine normalize, each cohort’s appetite for scalable, update-ready content underpins steady expansion of the medical animation market.

Geography Analysis

North America Medical Animation Market

North America’s 44.6% revenue share in 2024 mirrors the region’s deep life-science ecosystem, favorable reimbursement climate, and supportive AI regulatory agenda. The FDA’s iterative guidance on machine-learning devices encourages innovators to submit animation-rich evidence packages, reinforcing local studio pipelines. Academic medical centers elevate domestic demand by integrating VR-based coursework into competency frameworks, while Canadian and Mexican producers increasingly co-develop projects for bilingual audiences.

APAC Medical Animation Market

Asia Pacific is accelerating at an 18.5% CAGR to 2030, fueled by hospital modernizations, ed-tech investments, and rising clinical trial participation. India’s ERemedium showcases the scalability of cloud-served patient-education libraries across multilingual markets. China’s provincial governments fund XR labs within teaching hospitals, while Japan and South Korea leverage established technology bases to pioneer haptic-enabled simulators. Cost-competitive talent pools allow regional studios to capture outsourced work from global pharma clients, widening the production capacity of the medical animation market.

EMEA and South America Medical Animation Market

Europe maintains steady growth on the back of strong pharmaceutical clusters and pan-EU research programs that mandate open-access dissemination. German specialists such as SigmaCollect deliver cinematic motion design for biotech conferences, while Nordic start-ups pair animation with augmented reality to streamline device implantation training. Middle East & Africa see incremental gains tied to medical-city developments and scholarship-backed residency programs, and South America positions itself as a nearshore content hub, particularly for Spanish and Portuguese language assets. Across continents, cross-border collaborations, remote workflows, and cloud rendering converge to expand the collective medical animation market footprint.

Competitive Landscape

The medical animation market exhibits moderate concentration, with leading studios—Random42, Ghost Productions, and Nucleus Medical Media—leveraging scientific talent, proprietary pipelines, and long-standing pharma relationships to secure repeat business. Each houses in-house medical directors who oversee compliance and ensure anatomical veracity, differentiating them from generalist animation agencies. Mid-tier firms carve niches in cardiology, orthopedics, or device dossiers, while boutique outfits specialize in multilingual localization or interactive e-learning microsites.

Technology leadership is critical. Ghost Productions’ Wraith-VR combines real-time rendering with multi-user collaboration, positioning the firm at the frontier of surgical simulation. Random42 integrates AI-driven particle simulations to illustrate nanotherapeutic delivery, while newcomers such as GenBio AI automate organ-level modeling to shorten pre-production timelines. M&A activity is picking up; Cengage Group’s acquisition of Visible Body signals that large ed-tech and software vendors view animation libraries as strategic assets that can be repurposed across curricula, marketing, and enterprise training.

Competitive intensity is likely to rise as global studios tap offshore labor, AI algorithms commoditize baseline asset creation, and hospitals internalize simple animation tasks. Yet barriers remain high for premium scientific storytelling, where regulatory scrutiny and clinician trust require accredited expertise. Studios that embrace hybrid workflows—combining generative AI, cloud collaboration, and rigorous peer review—are best positioned to capture incremental value in an expanding medical animation market.

Medical Animation Industry Leaders

Random42 Scientific Communication

Infuse Medical

Hybrid Medical Animation

Ghost Productions

Scientific Animations

- *Disclaimer: Major Players sorted in no particular order

Medical Animation Market Companies Covered in this Report

- Random42 Scientific Communication

- Infuse Medical

- Hybrid Medical Animation

- Ghost Productions

- Scientific Animations

- Nucleus Medical Media

- XVIVO Scientific Animation

- Blausen Medical

- iSO-FORM

- Trinsic Animation

- Visible Body

- Medmovie

- Geometric Medical

- AXS Studio

- Animated Biomedical Productions

- Syntropy Studio

- Trinity Animation (Healthcare)

- FuseHealth

- Nanobot Medical

- Biovisuals

Recent Industry Developments in Medical Animation Market

- June 2025: The Wyss Institute announced AI-enabled molecular modeling breakthroughs that integrated film-grade animation tools for coronavirus drug discovery.

- April 2025: GenBio AI launched Phase 1 of its Digital Organism platform, featuring six multi-scale models for rapid therapy simulation.

- August 2024: Ghost Productions highlighted the shift toward 3D visualization for intra-operative guidance and interdisciplinary research.

- July 2025: Nucleus Medical Media rolled out its QRx Video System, integrating QR-linked animations with CRM analytics.

Global Medical Animation Market Report Scope

Segmentation Overview

| 2D Animation |

| 3D Animation |

| 4D / Real-Time Imaging |

| Flash Animation |

| Drug Mechanism of Action |

| Patient Education |

| Surgical Training |

| Molecular & Cellular Animation |

| Emergency Care & Other Apps |

| Oncology |

| Cardiology |

| Dental |

| Plastic / Cosmeceutical Surgery |

| Orthopedics |

| Neurology |

| Others |

| Life Science Companies |

| Medical Device Manufacturers |

| Hospitals & Clinics |

| Academic & Research Institutes |

| Forensic & Legal Firms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Animation Type | 2D Animation | |

| 3D Animation | ||

| 4D / Real-Time Imaging | ||

| Flash Animation | ||

| By Application | Drug Mechanism of Action | |

| Patient Education | ||

| Surgical Training | ||

| Molecular & Cellular Animation | ||

| Emergency Care & Other Apps | ||

| By Therapeutic Area | Oncology | |

| Cardiology | ||

| Dental | ||

| Plastic / Cosmeceutical Surgery | ||

| Orthopedics | ||

| Neurology | ||

| Others | ||

| By End User | Life Science Companies | |

| Medical Device Manufacturers | ||

| Hospitals & Clinics | ||

| Academic & Research Institutes | ||

| Forensic & Legal Firms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the medical animation market by 2030?

The medical animation market is forecast to reach USD 1.39 billion by 2030 on the back of a 21.5% CAGR.

Which region will witness the fastest growth through 2030?

Asia Pacific is expected to outpace other regions with an 18.5% CAGR, driven by digital health investments and expanding medical education programs.

Why are patient-education animations gaining traction?

Studies show animated content improves understanding and adherence, aligning with value-based care incentives and reducing readmission costs.

How are AI tools influencing production timelines?

Generative algorithms automate modeling and rendering, shrinking production cycles from months to weeks while preserving scientific rigor.

Which animation type is growing the fastest?

4D and real-time imaging solutions are expanding at a 19.0% CAGR, reflecting demand for motion-synchronized visuals in planning and training.

What is the main barrier hindering market expansion?

High production costs for premium, scientifically validated content remain a key restraint, especially for emerging-market hospitals and NGOs.

Page last updated on: