Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

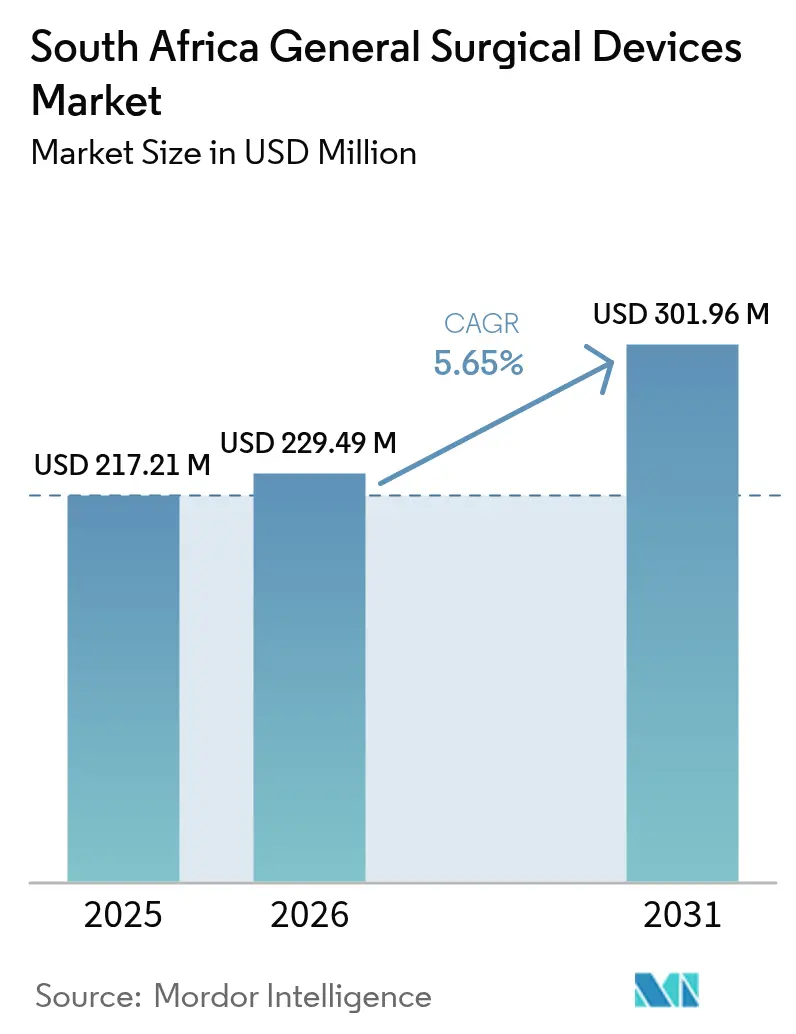

| Base Year Market Size (2025) | USD 217.21 Million |

| Market Size (2026) | USD 229.49 Million |

| Market Size (2031) | USD 301.96 Million |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

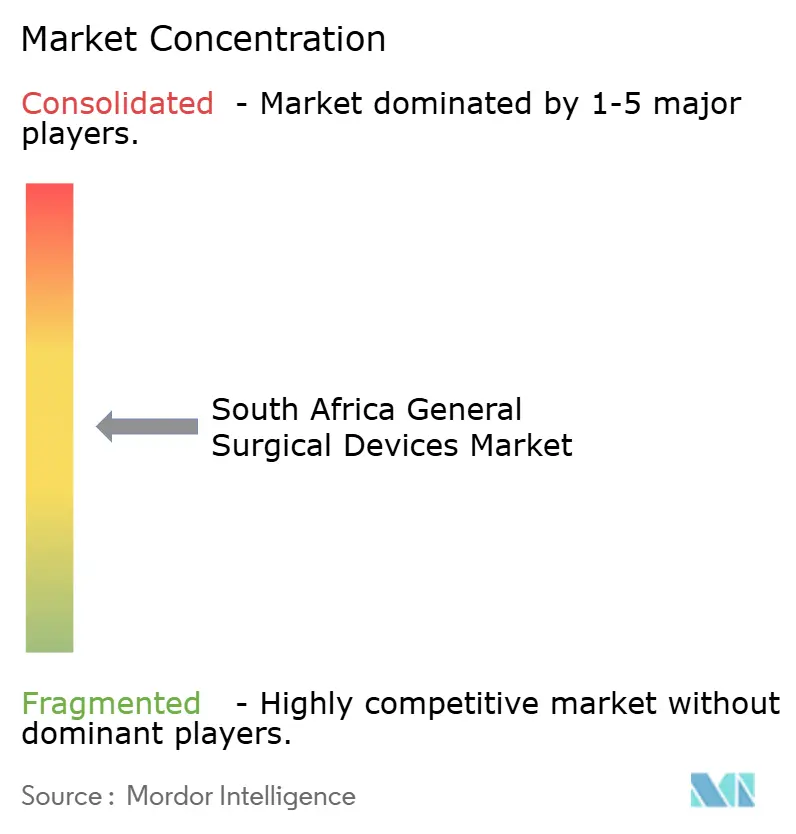

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa General Surgical Devices Market Analysis by Mordor Intelligence

South Africa General Surgical Devices Market size in 2026 is estimated at USD 229.49 million, growing from 2025 value of USD 217.21 million with 2031 projections showing USD 301.96 million, growing at 5.65% CAGR over 2026-2031. The growth outlook is underpinned by the National Health Insurance (NHI) roll-out, private-sector capital spending, and the proven clinical advantages of minimally invasive surgery. Trauma-related procedure volumes, together with a rising chronic-disease burden, keep core demand stable even during economic cycles. Load-shedding-induced equipment downtime pushes hospitals toward energy-efficient systems, while local content mandates complicate import strategies and invite partnership opportunities with domestic manufacturers. Vendor competition increasingly centers on digital ecosystems, robotic platforms, and backup power integration as hospitals seek to offset a nationwide shortage of more than 27,000 healthcare posts.[1]Source: Democratic Alliance, “27 000 Critical Skills Shortages in Health Sector,” da.org.za

Key Report Takeaways

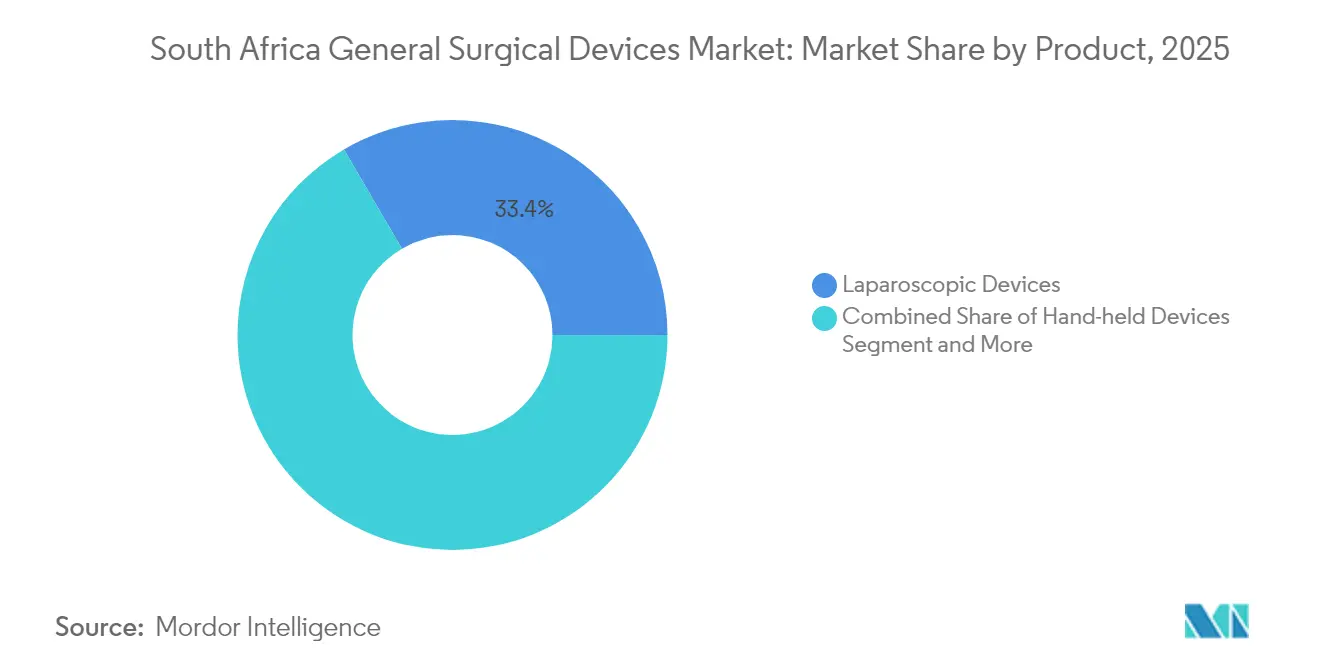

- By product category, laparoscopic devices led with 33.42% of the South Africa general surgical devices market share in 2025, while electrosurgical devices are projected to expand at a 6.15% CAGR through 2031.

- By application, orthopedics captured 26.05% share of the South Africa general surgical devices market size in 2025; gynecology and urology are set to grow at a 6.58% CAGR to 2031.

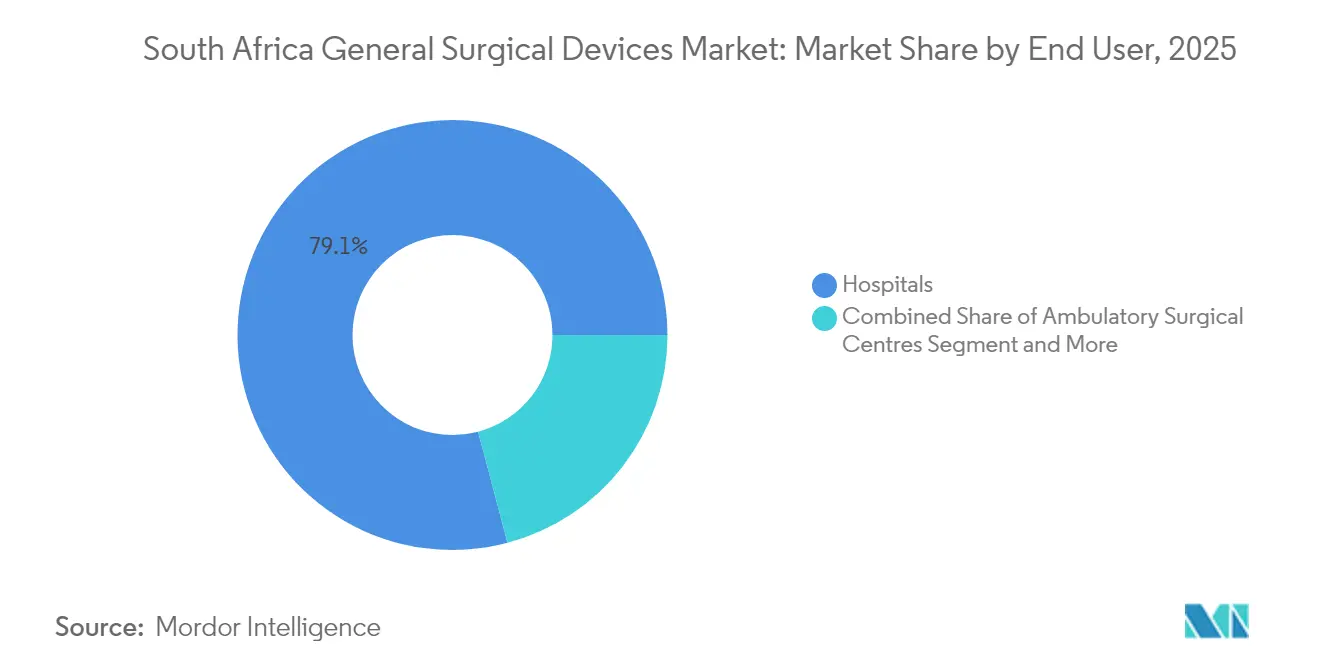

- By end user, hospitals held 79.12% of the South Africa general surgical devices market share in 2025, whereas ambulatory surgical centers (ASCs) record the fastest projected CAGR at 5.92% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa General Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Minimally Invasive Surgeries | +1.8% | National, with early gains in Gauteng, Western Cape, KwaZulu-Natal | Medium term (2-4 years) |

| High Incidence of Injuries and Road Accidents | +1.2% | National, concentrated in urban corridors | Short term (≤ 2 years) |

| Growing Prevalence of Chronic Diseases | +1.1% | National, with rural spill-over effects | Long term (≥ 4 years) |

| Expanding Geriatric Population and Health Spend | +0.9% | National, accelerated in metropolitan areas | Long term (≥ 4 years) |

| National Health Insurance Roll-Out Accelerating Device Procurement | +0.6% | National, phased implementation | Medium term (2-4 years) |

| Surge in Private Ambulatory Surgical Centres | +0.4% | Urban centers, private healthcare corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally Invasive Surgeries

Conversion to open surgery drops to 14.8% in major trauma centres that adopted laparoscopy, validating its clinical safety and spurring procurement decisions across tertiary hospitals. Robotic platforms introduced at leading facilities create a demonstration effect for surrounding provinces.[2]Source: Ahmed K. Awad, “Equity in the Cardiothoracic Surgical Workforce,” BMC Surgery, bmcsurg.biomedcentral.com Private providers, exemplified by Netcare’s Leica OH6 microscope installation, signal a willingness to fund premium optics that shorten theatre time. Workforce shortages also accelerate minimally invasive adoption because these technologies allow smaller surgical teams to perform complex procedures efficiently. The South Africa general surgical devices market benefits as hospitals align shorter stays with NHI reimbursement pressures.

High Incidence of Injuries and Road Accidents

South Africa’s road-fatality ranking sustains high trauma caseloads, particularly in Gauteng and KwaZulu-Natal, which increases throughput for orthopedic plates, screws, and power tools. Urban emergency departments thus standardize multipurpose instrument sets that handle diverse fractures, driving recurring purchases of consumables. Frequent load shedding forces operating theatres to stock energy-efficient towers and uninterruptible-power modules to keep trauma lists on schedule. Stable trauma volumes underpin forecasting accuracy for distributors in the South Africa general surgical devices market.

Growing Prevalence of Chronic Diseases

Cardiovascular, metabolic, and oncological conditions expand procedure pipelines for cardiac ablation, endoscopic tumor resections, and bariatric surgery. Device access constraints persist because only 3.3 anesthesiologists per 100,000 population are available, but programmatic partnerships between public and private sectors aim to enlarge training pipelines. Urban concentration of chronic-disease patients justifies investment in hybrid theatres equipped for multidisciplinary interventions, elevating demand for integrated device bundles. The South Africa general surgical devices market therefore diversifies beyond trauma items into chronic-care toolkits.

Expanding Geriatric Population and Health Spend

Age-related fragility fractures and cardiovascular conditions make elderly patients high users of orthopedic implants and vascular closure devices. Life Healthcare earmarked ZAR 2.1 billion for network upgrades in 2024, a signal that private operators anticipate sustained geriatric volume growth. Cost-effectiveness evidence drives procurement toward devices that shorten rehabilitation periods, such as cementless joint systems. The NHI design team faces pressure to include geriatric surgical pathways, assuring baseline volumes for suppliers across the South Africa general surgical devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inadequate Reimbursement and High Device Costs | -1.4% | National, acute in public sector | Short term (≤ 2 years) |

| Scarcity of Skilled Surgical Workforce | -1.1% | National, severe in rural areas | Medium term (2-4 years) |

| Local-Content Rules Raising Import Barriers | -0.8% | National, affecting international suppliers | Medium term (2-4 years) |

| Power-Grid Instability Causing Equipment Downtime | -0.6% | National, concentrated in manufacturing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inadequate Reimbursement and High Device Costs

The cost-containment imperatives within South Africa's healthcare system create persistent pressure on surgical device pricing and reimbursement frameworks. NHI tenders prioritize affordability, restricting premium technology uptake and delaying recoupment of R&D investment for multinational vendors.[3]Source: U.S. International Trade Administration, “South Africa – Healthcare: Medical Devices and Pharmaceuticals,” trade.gov Currency weakness inflates landed costs because 80% of surgical devices are imported. Private hospitals cross-subsidize public volumes but face shrinking margins as medical-aid payouts lag device inflation. These dynamics temper expansion aspirations for the South Africa general surgical devices industry.

Scarcity of Skilled Surgical Workforce

Vacancies of more than 21,000 specialist posts reduce theatre throughput, leaving sophisticated systems idle during off-peak periods. Foreign clinician recruitment provides a bridge but raises training-compatibility issues, prolonging ramp-up for robotics programmes. Suppliers now bundle simulation modules and remote proctoring features to improve adoption rates in the South Africa general surgical devices market. Surgical training programs require enhanced capacity and international partnerships to address long-term workforce development needs that can support expanded device utilization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Laparoscopic Leadership Drives Innovation

Laparoscopic devices accounted for 33.42% of the South Africa general surgical devices market in 2025 as hospitals embedded tower systems, trocars, and high-definition scopes into standard trauma and elective workflows. The South Africa general surgical devices market size for laparoscopic platforms is projected to rise steadily as reimbursement favors shorter inpatient stays. Energy-based electrosurgical units exhibit the quickest trajectory at 6.15% CAGR through 2031 because trauma theatres seek rapid hemostasis tools that lower transfusion demand.

Electrosurgical growth also reflects investment in integrated smoke-evacuation systems that align with occupational-health standards. Hand-held scissors, forceps, and retractors retain utility in resource-constrained settings, but advanced iterations with antimicrobial coatings gain share as infection-prevention protocols tighten. Wound-closure innovations such as smart bandages draw attention in tertiary wound-care programmes. Collectively, these trends widen the product palette and intensify competition within the South Africa general surgical devices market.

By Application: Orthopedic Dominance Meets Specialty Growth

Orthopedics contributed 26.05% to the South Africa general surgical devices market in 2025 owing to persistent traffic-injury volumes and industrial accidents. With ASC adoption of robotic knee systems, orthopedic teams expect shorter learning curves and improved implant alignment, consolidating revenue visibility for implant suppliers. In numerical terms, orthopedic devices commanded the largest South Africa general surgical devices market share at segment level in 2025.

Gynecology and urology interventions will post the highest CAGR of 6.58% through 2031 as demographic change and greater insurance coverage elevate procedure counts. Laparoscopic hysterectomy kits, ureteroscopes, and morcellators thus experience expanding order books. Cardiology and neurology remain constrained by sub-specialist shortages but constitute longer-term upside once training investments bear fruit. This evolving mix compels vendors to tailor portfolios for the South Africa general surgical devices market across multiple specialties.

By End User: Hospital Dominance Faces ASC Disruption

In 2025, hospitals held 79.12% of the South Africa general surgical devices market size, reflecting their entrenched status as full-service hubs capable of complex multi-disciplinary operations. Government exemption of 37 major hospitals from load shedding underscores their strategic role in trauma readiness. Nevertheless, ASCs post a 5.92% CAGR through 2031 as private chains expand footprint in affluent suburbs and employer-funded insurance steers same-day surgeries to lower-cost venues.

Specialty clinics focusing on ophthalmology or fertility procedures create micro-clusters of demand for niche instruments. Digital operating-room platforms that integrate scheduling, imaging, and analytics differentiate providers in competitive urban belts. As a result, procurement officers juggle bulk hospital contracts with agile ASC orders, adding complexity to supply-chain strategies serving the South Africa general surgical devices market.

Geography Analysis

Metropolitan provinces—Gauteng, Western Cape, and KwaZulu-Natal—generate the lion’s share of sales as they combine tertiary hospitals, private networks, and trauma pipelines. Installation of the first Leica OH6 microscope at Greenacres Hospital in Port Elizabeth highlights how technological leadership can emerge outside traditional hubs. Government plans to invest more than ZAR 1 trillion in public infrastructure over three years, with healthcare priority, promise new procurement corridors in secondary cities.

Rural districts remain underserved, hence mobile surgical units and tele-mentored laparoscopy programmes are trialed to bridge access gaps. Portable towers and battery-backed electrosurgical generators become procurement priorities for these areas. Load shedding hits rural theatres harder, creating demand for devices with low-power profiles and built-in energy storage. As NHI centralizes purchasing, provincial variations in formulary adoption are likely to narrow, recalibrating logistics frameworks for the South Africa general surgical devices market.

Border regions attract cross-national patients from Botswana, Mozambique, and Zimbabwe who seek higher acuity care, boosting throughput in Limpopo and Mpumalanga. Mining belts contribute a consistent orthopedics flow because of crush injuries and vibration-related musculoskeletal disorders. Collectively, these geographic nuances compel distributors to balance inventory across high-volume urban centers and demand-spike rural pockets, sustaining momentum for the South Africa general surgical devices market.

Competitive Landscape

The marketplace is moderately fragmented. Global majors such as Johnson & Johnson MedTech, Medtronic, and B. Braun SE hold strong channel presence but face Broad-Based Black Economic Empowerment (B-BBEE) quotas that encourage partnerships with local distributors. Transparency requirements under the 2024 Public Procurement Act raise the bar for compliance documentation, favoring corporates with robust governance systems.

Technology integration is now a primary battleground. Johnson & Johnson introduced the Polyphonic digital ecosystem to link imaging, stapling, and analytics into a single operative workflow, promising reduced downtime and predictive maintenance. Smith+Nephew partnered with HOPCo to embed artificial intelligence analytics at ASC clients for real-time benchmarking of surgical outcomes. Energy-efficient consoles and battery modules appeal to hospitals grappling with grid instability, offering an immediate competitive edge in tenders.

Local innovation is rising. South African entrepreneurs developed Digital X-Ray Glasses that display intraoperative imaging inside the surgeon’s field of view, potentially shrinking radiation exposure and instrument clutter. Such indigenous breakthroughs could erode import dependence and provide cost-effective solutions aligned with local-content thresholds. Overall, the South Africa general surgical devices market rewards firms that blend advanced technology with localized manufacturing or assembly.

South Africa General Surgical Devices Industry Leaders

Boston Scientific Corporation

B. Braun SE

Medtronic

Johnson & Johnson (Ethicon/DePuy)

Stryker Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The Versius Surgical Robotic System debuted at the University of the Free State, marking its first installation in Southern Africa.

- August 2024: Busamed Gateway Private Hospital commissioned a Da Vinci surgical robot, broadening access to robotic surgery in KwaZulu-Natal.

- November 2023: Terumo Corporation established Terumo South Africa (Pty) Ltd., strengthening its regional footprint.

South Africa General Surgical Devices Market Report Scope

As per the scope of the report, surgical instruments are used to perform specific actions for desired effects during a surgery or operation. Over time, many kinds of surgical instruments and tools have been invented. Surgical instruments are clinically and accurately designed to help the surgeons in performing surgeries.

The South African general surgical devices market is segmented by product (handheld devices, laparoscopic devices, electrosurgical devices, wound-closure devices, and other products) and application (gynecology and urology, cardiology, orthopedic, neurology, and other applications). The report offers the value (in USD million) for the above segments.

By Product

| Hand-held Devices |

| Laparoscopic Devices |

| Electrosurgical Devices |

| Wound-closure Devices |

| Other Products |

By Application

| Gynecology and Urology |

| Cardiology |

| Orthopaedic |

| Neurology |

| Other Applications |

By End User

| Hospitals |

| Ambulatory Surgical Centres |

| Specialty Clinics |

| By Product | Hand-held Devices |

| Laparoscopic Devices | |

| Electrosurgical Devices | |

| Wound-closure Devices | |

| Other Products | |

| By Application | Gynecology and Urology |

| Cardiology | |

| Orthopaedic | |

| Neurology | |

| Other Applications | |

| By End User | Hospitals |

| Ambulatory Surgical Centres | |

| Specialty Clinics |

Key Questions Answered in the Report

What is the current value of the South Africa general surgical devices market?

It is valued at USD 229.49 million in 2026.

How fast is the market expected to grow?

It is projected to expand at a 5.65% CAGR, reaching USD 301.96 million by 2031.

Which product segment leads the market?

Laparoscopic devices command the highest share at 33.42%.

Why are ambulatory surgical centres important for future growth?

ASCs show the fastest rise at a 5.92% CAGR as they offer cost-effective and convenient same-day procedures.

How does load shedding affect surgical device demand?

Frequent power cuts drive hospitals to procure energy-efficient devices and back-up power systems.

Page last updated on: