Hirsutism Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

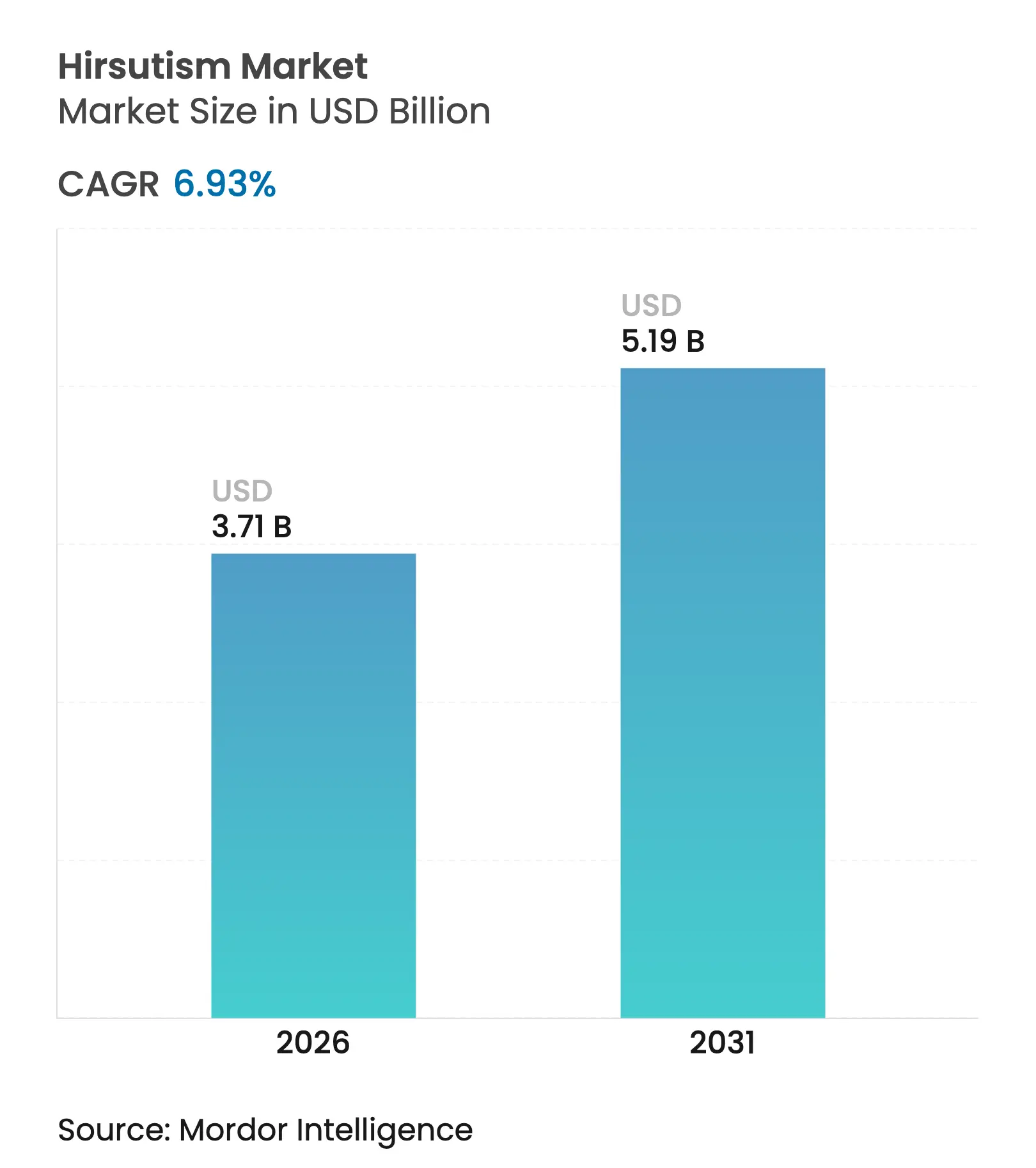

| Market Size (2026) | USD 3.71 Billion |

| Market Size (2031) | USD 5.19 Billion |

| Growth Rate (2026 - 2031) | 6.93 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Hirsutism Market Analysis by Mordor Intelligence

The Hirsutism Market size was valued at USD 3.47 billion in 2025 and estimated to grow from USD 3.71 billion in 2026 to reach USD 5.19 billion by 2031, at a CAGR of 6.93% during the forecast period (2026-2031). This strong trajectory reflects the growing pool of women diagnosed with polycystic ovary syndrome (PCOS), faster adoption of energy-based devices, and wider tele-dermatology access. PCOS now affects 65.77 million women worldwide, nearly doubling since 1990, and 19.12% of these patients develop hirsutism compared with 1.37% of the broader female population . Triple-wavelength diode lasers that deliver 66% hair-reduction efficacy are accelerating the shift from systemic drugs to minimally invasive options. Annual direct healthcare costs for U.K. women with PCOS average GBP 1,546 (USD 1,963) versus GBP 940 (USD 1,194) for controls, underscoring the economic burden propelling treatment uptake. Meanwhile, prolonged telemedicine flexibilities in the United States allow remote prescribing of anti-androgen therapies through December 2025, improving access for underserved populations.

Key Report Takeaways

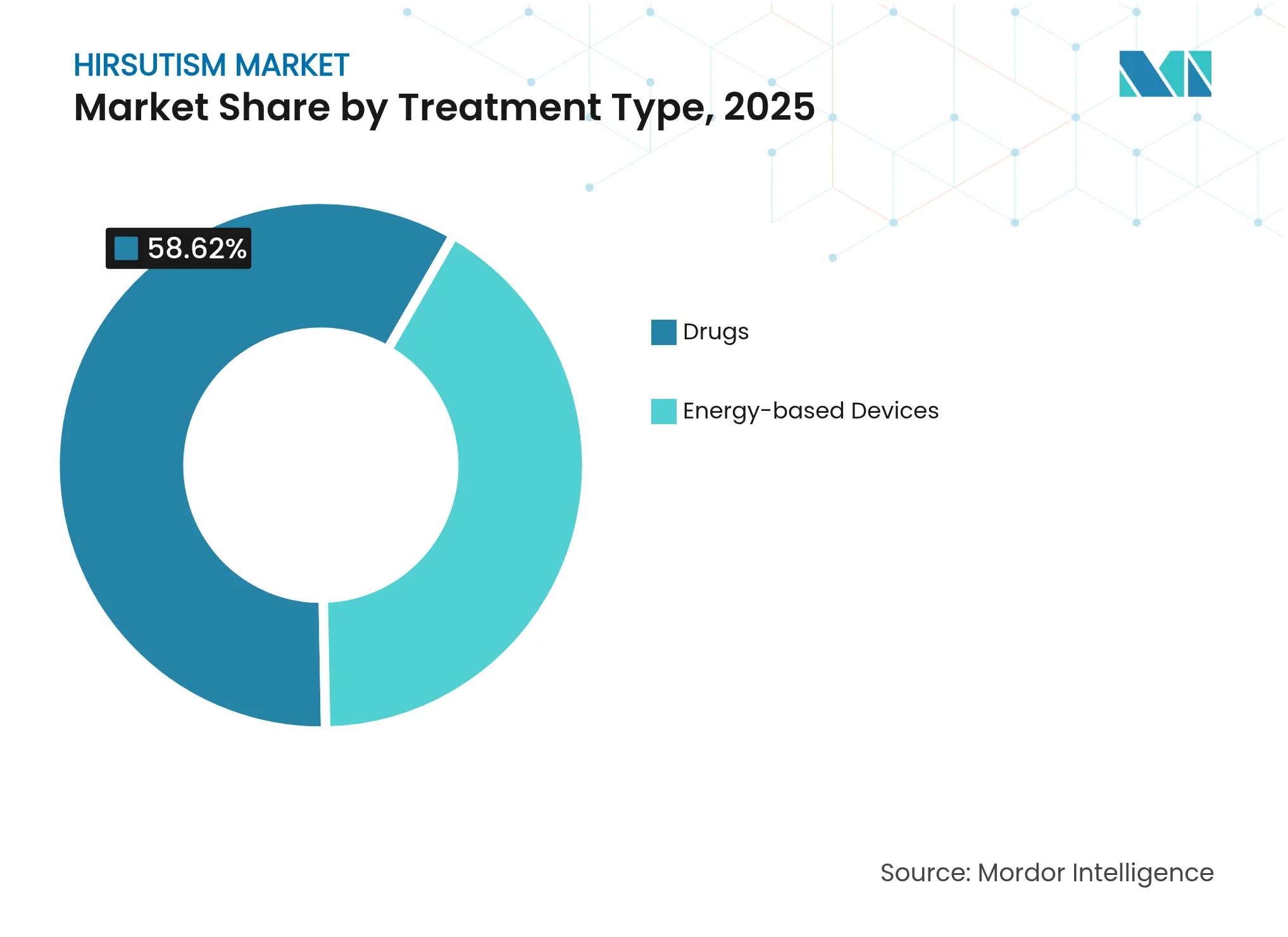

- Drug treatments led the hirsutism market with 58.62% revenue share in 2025, while energy-based devices are projected to grow at a 8.86% CAGR to 2031.

- PCOS-associated cases accounted for 66.74% of the hirsutism market share in 2025, whereas drug-induced and tumor-related hirsutism is poised for the fastest expansion at 9.03% through 2031.

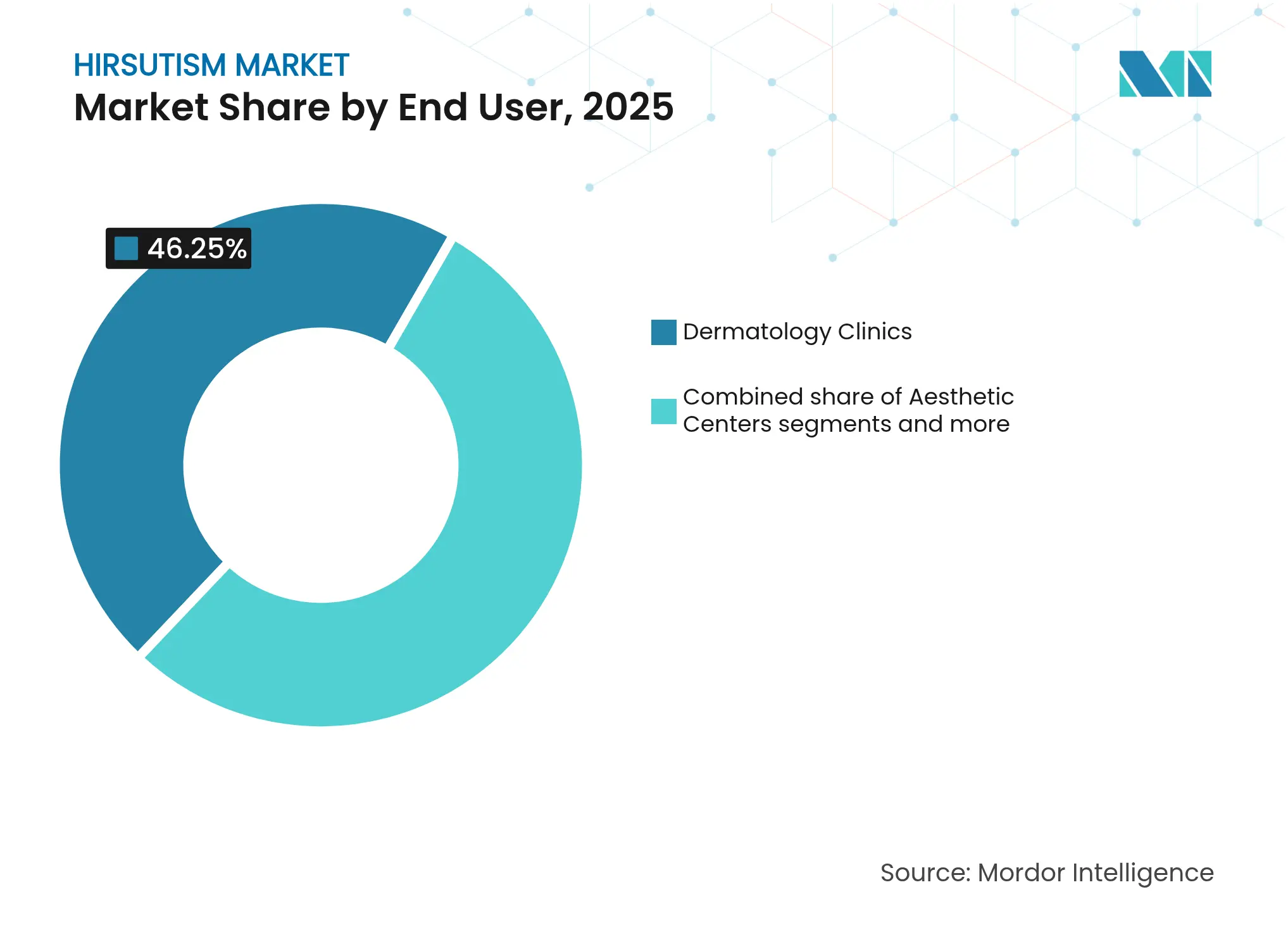

- Dermatology clinics held 46.25% of 2025 revenue; aesthetic centers and spas are set to register the highest 10.58% CAGR to 2031.

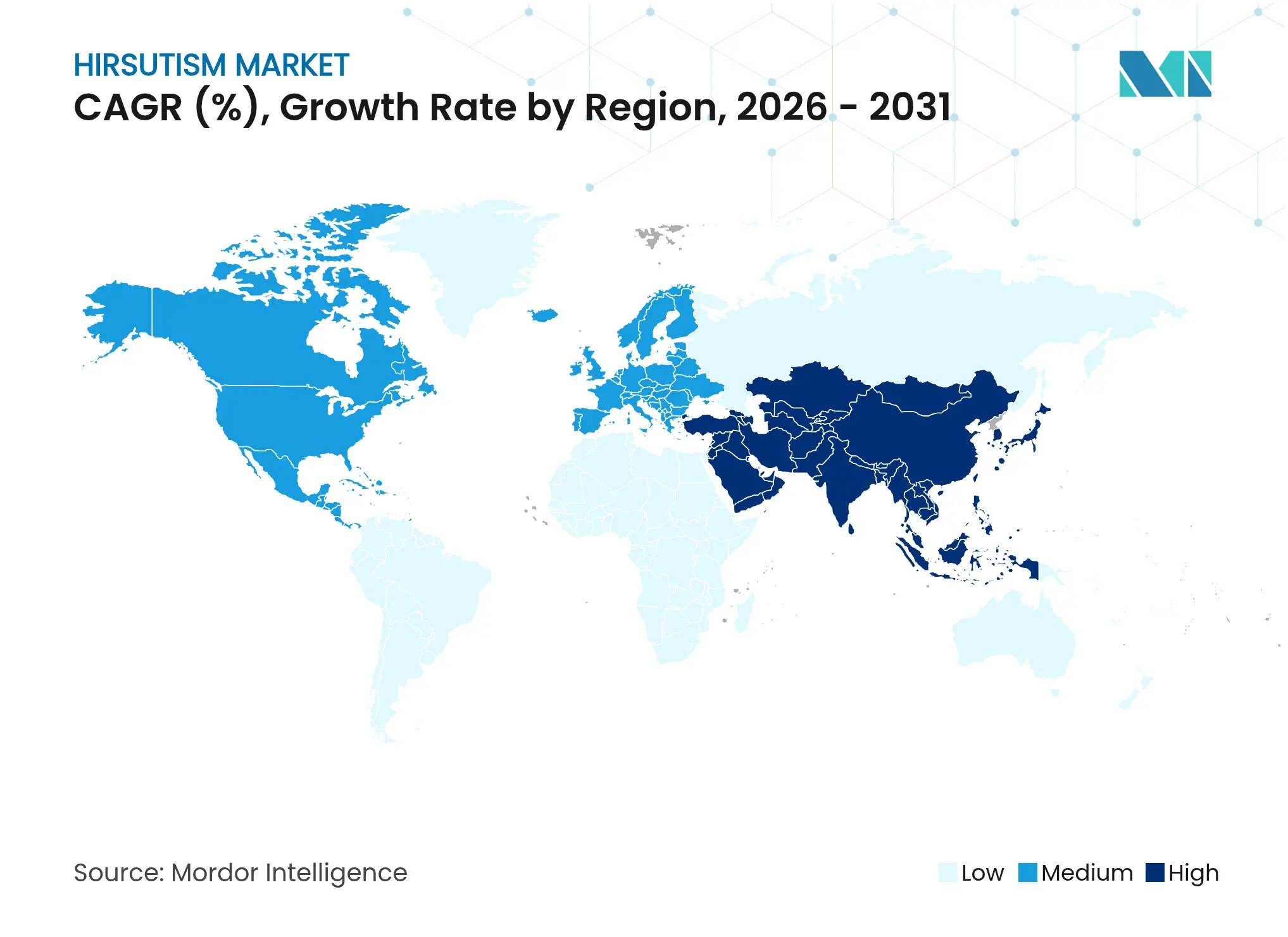

- North America captured 41.76% of 2025 sales, but Asia-Pacific is projected to advance at a 9.42% CAGR and eclipse all regions in incremental value added by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hirsutism Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising PCOS prevalence and earlier diagnosis Rising PCOS prevalence and earlier diagnosis | +2.1% | Global; highest in Asia-Pacific & Middle East | Medium term (2–4 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:Global; highest in Asia-Pacific & Middle East | Impact Timeline:Medium term (2–4 years) |

Shift toward minimally invasive procedures Shift toward minimally invasive procedures | +1.8% | North America & Europe; growing in Asia-Pacific | Short term (≤ 2 years) | |||

Increasing male uptake of laser devices Increasing male uptake of laser devices | +0.9% | North America & Europe | Long term (≥ 4 years) | |||

Growth of tele-dermatology and e-pharmacy Growth of tele-dermatology and e-pharmacy | +1.2% | Global; early gains in U.S., Canada, Australia | Medium term (2–4 years) | |||

Pipeline topical 5-α-reductase inhibitors Pipeline topical 5-α-reductase inhibitors | +0.7% | Global | Long term (≥ 4 years) | |||

Venture funding for at-home devices Venture funding for at-home devices | +0.8% | North America & Europe; spillover to Asia | Medium term (2–4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising PCOS Prevalence & Earlier Diagnosis

PCOS cases climbed from 34.81 million in 1990 to 65.77 million in 2024—an 89% surge that far outpaces population growth. Earlier screening explains part of this jump; Delhi NCR’s 17.4% prevalence illustrates how systematic case-finding uncovers latent demand. In the United Kingdom, incidence nearly doubled between 2004 and 2019, a trend mirrored in higher outpatient visits and medication use. PCOS patients consume 64% more medical services than peers without the disorder, providing sustained revenue for hirsutism solutions. These epidemiological forces keep the hirsutism market on an upward path as clinical guidelines increasingly recommend combined drug and device regimens.

Shift Toward Minimally Invasive Aesthetic Procedures

Consumer preference is tilting toward non-surgical interventions that promise shorter downtime and fewer systemic side effects. Medical spas now deliver roughly half of all aesthetic procedures in the United States, making laser hair removal a routine add-on in many dermatology offices. Clinical evidence for triple-wavelength diode systems proves especially compelling in patients with Fitzpatrick IV–V skin, who historically faced greater complication risks. FDA clearance of several at-home intense pulsed light (IPL) devices broadens market reach, though professional lasers retain efficacy advantages. Collectively, these factors steer the hirsutism market toward device-centric care models without entirely displacing systemic pharmaceuticals.

Increasing Male Consumer Uptake of Laser Devices

Rising social acceptance of cosmetic procedures among men is growing a niche yet influential customer segment. Market surveys show double-digit year-on-year increases in male bookings for laser hair removal services, especially targeting back and beard-line areas. This influx diversifies revenue sources, smooths seasonal demand fluctuations, and encourages clinics to invest in higher-capacity laser platforms. Although male hirsutism is hormonally distinct, overlapping technology needs make this consumer group a secondary but durable tailwind for device manufacturers.

Growing Tele-dermatology & E-pharmacy Adoption

The continuation of U.S. telemedicine flexibilities for controlled substances through December 2025 supports remote spironolactone and finasteride prescribing. A proposed “Special Registration” path will cement virtual care within the reimbursement ecosystem, promising long-term stability. Veterans Affairs expects to save USD 2.54 million annually by substituting video visits for in-person appointments, signaling institutional acceptance. Coupled with same-day e-pharmacy fulfilment, these rules reduce geographic care gaps and sustain prescription adherence, particularly among young adults who prefer digital health interactions.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Teratogenicity concerns with systemic anti-androgens Teratogenicity concerns with systemic anti-androgens | -1.4% | Global, with highest impact in regions with strict pregnancy protocols | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.4% | Geographic Relevance:Global, with highest impact in regions with strict pregnancy protocols | Impact Timeline:Short term (≤ 2 years) |

Lack of reimbursement for cosmetic laser sessions Lack of reimbursement for cosmetic laser sessions | -2.2% | North America & Europe primarily, expanding globally | Medium term (2-4 years) | |||

Post-inflation affordability gap in emerging regions Post-inflation affordability gap in emerging regions | -1.1% | Asia-Pacific, South America, MEA primarily | Medium term (2-4 years) | |||

Uneven clinical adoption of new molecular entities Uneven clinical adoption of new molecular entities | -0.8% | Global, with slower uptake in smaller markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Teratogenicity Concerns with Systemic Anti-androgens

Spironolactone remains a cornerstone therapy, yet pregnancy contraindications limit its use among women of childbearing age. Although case reports document normal fetal outcomes following inadvertent mid-gestation exposure to 240 mg daily spironolactone, regulatory guidance still mandates dual contraception and monthly testing. The administrative burden can deter both physicians and patients, prompting earlier migration to device-based interventions. Newer alternatives such as eplerenone carry lighter androgen blockade, but real-world obstetric safety data remain sparse, constraining immediate substitution.

Lack of Reimbursement for Cosmetic Laser Sessions

Major insurers classify laser hair removal as elective cosmetic care, excluding it from coverage except in narrow medical indications like pilonidal sinus disease. Policies from Cigna, Anthem, and Aetna impose similar exclusions, leaving patients to shoulder several hundred to several thousand USD per treatment course. With inflation pushing discretionary healthcare budgets downward, many prospective clients defer procedures, dampening overall procedure volume. The absence of standardized long-term outcome metrics further complicates advocacy efforts aimed at broadening payer coverage.

Segment Analysis

By Treatment Type: Devices Gain Momentum Despite Drug Dominance

Drug therapies secured 58.62% of 2025 revenue through widespread use of anti-androgen tablets, combined oral contraceptives, and insulin sensitizers. Spironolactone dosing above 100 mg daily remains routine, yet prescribers increasingly switch to lasers once pregnancy planning begins. Energy-based devices are forecast to post a 8.86% CAGR to 2031 as pulse-modulation advances trim session counts and downtime. Clinics are replacing single-wavelength units with multi-wavelength diode, alexandrite, and Nd:YAG platforms that handle diverse skin tones with fewer adverse events . Triple-wavelength systems demonstrated 66% hair-density reductions on Asian skin, a milestone that improves treatment equity across pigment-rich populations. FDA clearance of multiple over-the-counter IPL units opens a hybrid model in which in-clinic lasers establish results and home devices maintain them.

Device makers also pursue top-line growth through service contracts, tip-replacement kits, and software subscriptions that boost lifetime value per installed base. Meanwhile, eflornithine’s 2024 market withdrawal leaves white-space that pipeline topical 5-α-reductase inhibitors aim to fill with safer botanical or small-molecule candidates.

Note: Segment shares of all individual segments available upon report purchase

By Indication: PCOS Remains Core but Complex Cases Rise

PCOS-associated hirsutism generated 66.74% of 2025 spending, propelled by surging global prevalence and direct androgenic drivers. A systematic review of 423 PCOS patients showed laser or light therapies markedly improve Ferriman-Gallwey scores and self-esteem when combined with metabolic control. Drug-induced and tumor-related hirsutism is projected to outpace all other indications at 9.03% CAGR as oncology survival improves and androgenic medications proliferate. Multidisciplinary teams that coordinate endocrinology, oncology, and dermatology increasingly recommend device-led protocols to avoid drug interactions. Idiopathic cases, featuring normal androgen levels but heightened follicular sensitivity, respond inconsistently to hormones and therefore push clinics toward laser packages that offer predictable cosmetic outcomes.

By End User: Aesthetic Centers Narrow Gap with Dermatology Clinics

Dermatology clinics controlled 46.25% of 2025 revenue by bundling diagnostic labs, prescriptions, and laser suites under one roof. Yet aesthetic centers and medical spas are on track for a 10.58% CAGR through 2031, driven by hospitality-style amenities and social-media marketing. U.S. medical spas now complete 40-55% of all cosmetic procedures, a structural shift backed by private-equity funding that standardizes protocols and quickens technology refresh cycles. Hospital outpatient departments retain complex endocrine or tumor-linked cases, while home-use IPL devices gain traction among privacy-minded consumers.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America retained 41.76% market share in 2025, buoyed by established reimbursement for medically necessary drug regimens, high aesthetic spending, and rapid adoption of FDA-cleared home lasers. Private-equity ownership of 15% of dermatology practices accelerates device turnover and centralized purchasing. Extended telemedicine flexibilities through December 2025 further widen patient access to anti-androgen prescriptions, particularly in rural counties where dermatologist density is low.

Asia-Pacific is projected to log the fastest 9.42% CAGR, fueled by rising disposable incomes, aggressive clinic build-outs, and PCOS prevalence well above global norms, such as Delhi NCR’s 17.4% rate. China and India dominate device import volumes, while Japan and South Korea showcase early-adopter behavior for premium multi-wavelength lasers. Australia capitalizes on liberal telehealth reimbursement that channels rural patients into urban laser hubs. The proven effectiveness of triple-wavelength systems on Asian skin tones further accelerates adoption.

Europe posts steady gains underpinned by public-private insurance hybrids that fund endocrinology consults yet leave lasers self-paid. The U.K.’s PCOS incidence nearly doubled between 2004 and 2019, surfacing hidden demand for both pharmacologic and procedural care. Germany, France, and Italy anchor regional revenue, while Eastern Europe scales gradually following device-safety harmonization under EU MDR. South America and Middle East & Africa offer green-field opportunities, led by Brazil’s aesthetic culture and GCC medical-tourism corridors, though currency volatility and practitioner gaps temper pace.

Competitive Landscape

Market Concentration

North America retained 42.23% market share in 2024, buoyed by established reimbursement for medically necessary drug regimens, high aesthetic spending, and rapid adoption of FDA-cleared home lasers. Private-equity ownership of 15% of dermatology practices accelerates device turnover and centralized purchasing. Extended telemedicine flexibilities through December 2025 further widen patient access to anti-androgen prescriptions, particularly in rural counties where dermatologist density is low.

Asia-Pacific is projected to log the fastest 9.73% CAGR, fueled by rising disposable incomes, aggressive clinic build-outs, and PCOS prevalence well above global norms, such as Delhi NCR’s. China and India dominate device import volumes, while Japan and South Korea showcase early-adopter behavior for premium multi-wavelength lasers. Australia capitalizes on liberal telehealth reimbursement that channels rural patients into urban laser hubs. The proven effectiveness of triple-wavelength systems on Asian skin tones further accelerates adoption.

Europe posts steady gains underpinned by public-private insurance hybrids that fund endocrinology consults yet leave lasers self-paid. Germany, France, and Italy anchor regional revenue, while Eastern Europe scales gradually following device-safety harmonization under EU MDR. South America and Middle East & Africa offer green-field opportunities, led by Brazil’s aesthetic culture and GCC medical-tourism corridors, though currency volatility and practitioner gaps temper pace.

Hirsutism Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: FDA cleared InnoVoyce’s VYLO Laser System, expanding triple-wavelength options for professional clinics

- April 2024: FDA granted 510(k) clearance to an over-the-counter IPL device from Dongguan Boyuan Intelligent Technology.

Table of Contents for Hirsutism Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising PCOS prevalence & earlier diagnosis

- 4.2.2Shift toward minimally-invasive aesthetic procedures

- 4.2.3Increasing male consumer uptake of laser devices

- 4.2.4Growing tele-dermatology & e-pharmacy adoption

- 4.2.5Emerging topical 5-α-reductase inhibitors (pipeline)

- 4.2.6Venture funding for at-home energy-based devices

- 4.3Market Restraints

- 4.3.1Teratogenicity concerns with systemic anti-androgens

- 4.3.2Lack of reimbursement for cosmetic laser sessions

- 4.3.3Post-inflation affordability gap in emerging regions

- 4.3.4Uneven clinical adoption of new molecular entities

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Suppliers

- 4.7.3Bargaining Power of Buyers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts

- 5.1By Treatment Type (Value)

- 5.1.1Drugs

- 5.1.1.1Anti-androgen Tablets

- 5.1.1.2Oral Contraceptives

- 5.1.1.3Insulin-Sensitizers

- 5.1.1.4Topical Creams (e.g., Eflornithine)

- 5.1.2Energy-based Devices

- 5.1.2.1Laser Systems (Alexandrite, Diode, Nd:YAG)

- 5.1.2.2Intense Pulsed Light (IPL) Systems

- 5.1.2.3Radio-frequency / Combination

- 5.2By Indication (Value)

- 5.2.1PCOS-Associated Hirsutism

- 5.2.2Idiopathic Hirsutism

- 5.2.3Congenital Adrenal Hyperplasia

- 5.2.4Drug-Induced / Tumor-Related

- 5.3By End User (Value)

- 5.3.1Dermatology Clinics

- 5.3.2Aesthetic Centers & Spas

- 5.3.3Hospitals

- 5.3.4Home Use

- 5.4By Geography (Value/Volume)

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2India

- 5.4.3.3Japan

- 5.4.3.4South Korea

- 5.4.3.5Australia

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4South America

- 5.4.4.1Brazil

- 5.4.4.2Argentina

- 5.4.4.3Rest of South America

- 5.4.5Middle East and Africa

- 5.4.5.1GCC

- 5.4.5.2South Africa

- 5.4.5.3Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1Alma Lasers Ltd.

- 6.3.2Almirall S.A.

- 6.3.3Braun GmbH (P & G)

- 6.3.4Candela Medical

- 6.3.5Cipla Ltd.

- 6.3.6Cutera Inc.

- 6.3.7Dr. Reddy’s Laboratories Ltd.

- 6.3.8Hologic Inc. (Cynosure®)

- 6.3.9Koninklijke Philips N.V.

- 6.3.10Lumenis Ltd.

- 6.3.11Merck & Co., Inc.

- 6.3.12Pfizer Inc.

- 6.3.13Sciton Inc.

- 6.3.14Sun Pharma Industries Ltd.

- 6.3.15Teva Pharmaceutical Industries Ltd.

- 6.3.16Venus Concept Inc.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Hirsutism Market Report Scope

As per the scope of this report, hirsutism is referred to as a condition in women that results in excessive growth of dark or coarse hair in a male-like pattern on the face, chest, and back. The hirsutism market is segmented by therapy (procedures and medications), end user (hospitals, clinics, and and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.