Orthopedic Bone Cement And Casting Materials Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

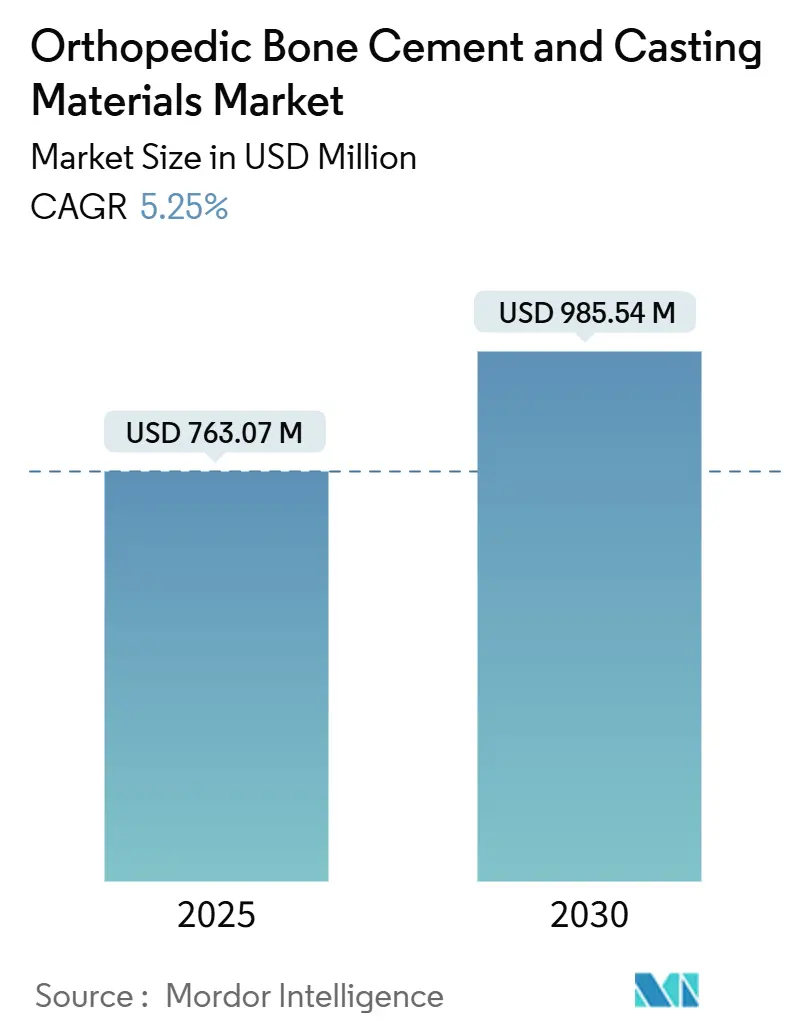

| Market Size (2025) | USD 763.07 Million |

| Market Size (2030) | USD 985.54 Million |

| Growth Rate (2025 - 2030) | 5.25% CAGR |

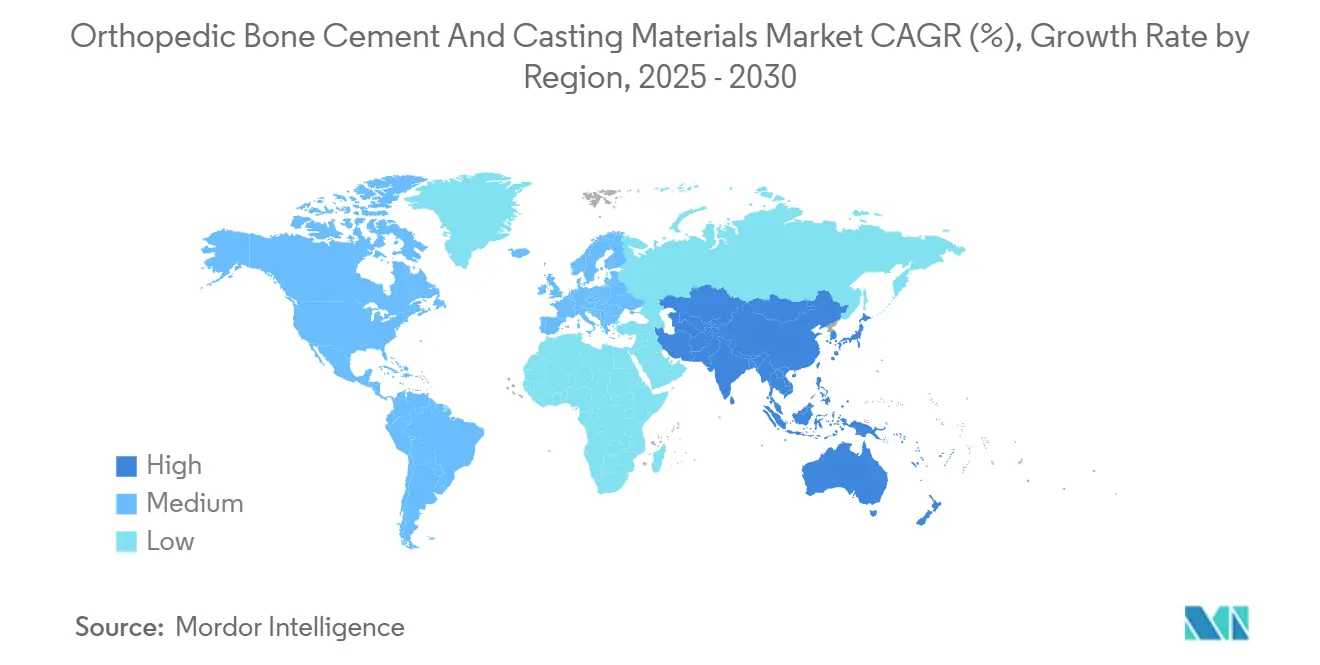

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Orthopedic Bone Cement And Casting Materials Market Analysis by Mordor Intelligence

The Orthopedic Bone Cement And Casting Materials Market size is estimated at USD 763.07 million in 2025, and is expected to reach USD 985.54 million by 2030, at a CAGR of 5.25% during the forecast period (2025-2030).

Favorable demographic shifts, accelerating joint-replacement volumes, and continuous material innovations underpin the steady growth outlook. Procedural demand rises as aging populations seek mobility restoration, while antibiotic-loaded and bioactive formulations expand the clinical utility span. Regulatory clearances for cementless and cement-augmented implants coexist, providing surgeons with flexibility and allowing for sustained cement volumes. Fast-curing chemistries further support the outpatient migration of hip, knee, and vertebral procedures. Finally, the persistent incidence of trauma in low- and middle-income countries keeps baseline demand resilient despite macroeconomic cost constraints.

Key Report Takeaways

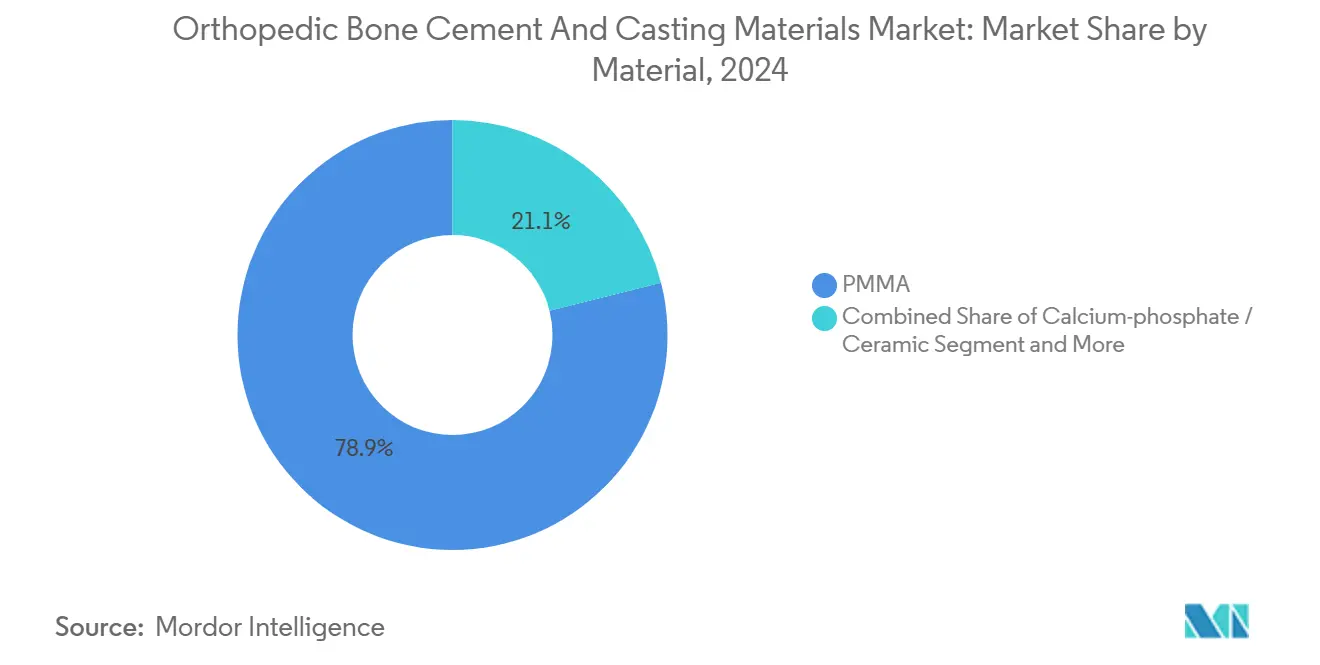

- By material, polymethyl methacrylate led the orthopedic bone cement and casting materials market with a 78.86% market share in 2024.

- By product viscosity, medium-viscosity cements accounted for 46.12% of the orthopedic bone cement and casting materials market size in 2024.

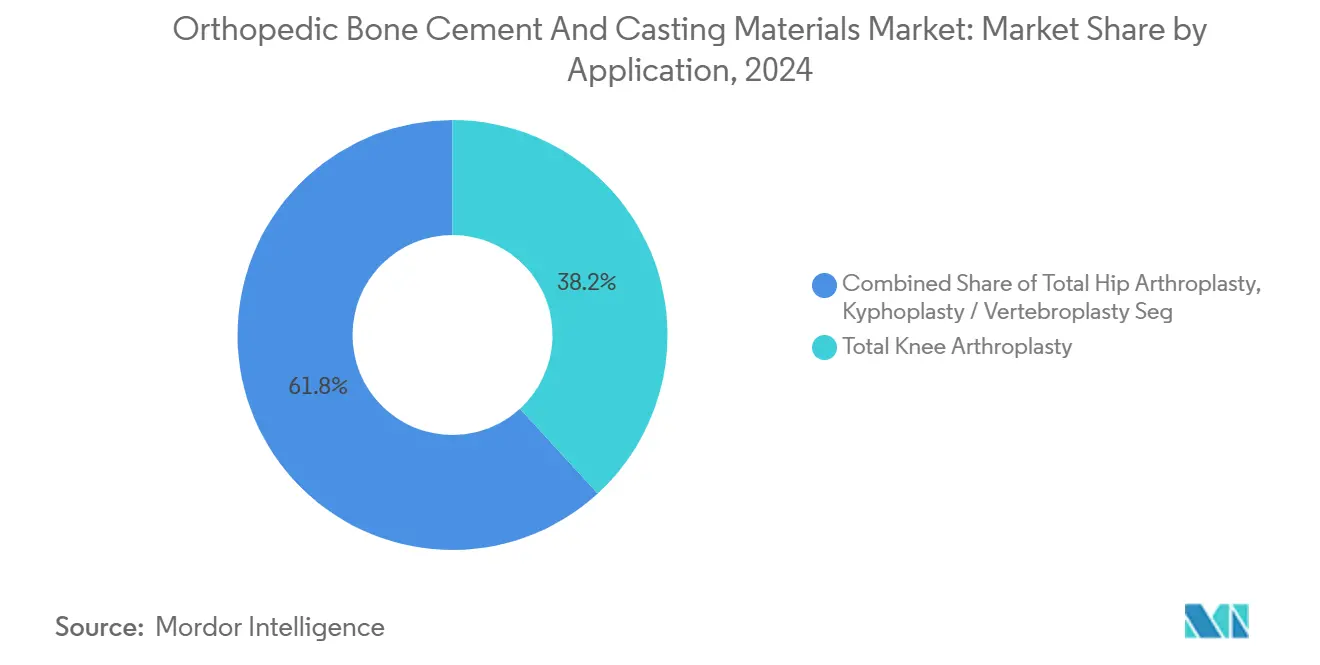

- By application, total knee arthroplasty captured 38.22% revenue share in 2024, whereas total hip arthroplasty is advancing at a 6.91% CAGR through 2030.

- By end-user, hospitals held 6a 0.56% share in 2024, while ambulatory surgical centers are projected to expand at a 7.34% CAGR to 2030.

- By geography, North America commanded a 45.62% share in 2024; the Asia-Pacific region is the fastest-growing, with a 7.22% CAGR from 2024 to 2030.

Global Orthopedic Bone Cement And Casting Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Number of Trauma & Road-Accident Cases | +0.8% | Global, with higher impact in LMICs | Medium term (2-4 years) |

| Growing Volume of Joint-Replacement & Spinal Surgeries | +1.2% | North America & Europe primary, Asia-Pacific emerging | Long term (≥ 4 years) |

| Rising Osteoporosis Prevalence in Ageing Populations | +1.0% | Global, concentrated in developed economies | Long term (≥ 4 years) |

| Rapid Uptake of Antibiotic-Loaded Bone Cements | +0.9% | Global, led by infection-prone demographics | Medium term (2-4 years) |

| ASC Shift: Demand For Fast-Curing Cements | +0.7% | North America primary, Europe following | Short term (≤ 2 years) |

| 3-D Printable Bio-Active Cements Enable Personalization | +0.6% | Advanced healthcare markets initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Number of Trauma & Road-Accident Cases

Musculoskeletal injuries range between 779 and 1,574 per 100,000 person-years in low- and middle-income countries, and 59.4% stem from road traffic accidents.[1]Source: Daniella Cordero et al., “The Global Burden of Musculoskeletal Injury in Low and Lower-Middle Income Countries,” LWW, otainternational.lww.com Lower-limb fractures constitute 67.4% of such trauma cases requiring surgery. Cement augmentation reduces the incidence of screw cut-out in geriatric trochanteric fractures from 5% to 0%, aligning with surgeon preference. Consequently, concentrated geographic demand surfaces in regions with underdeveloped traffic safety infrastructure. The incidence of persistent trauma supports baseline volumes for the orthopedic bone cement and casting materials market.

Growing Volume of Joint-Replacement & Spinal Surgeries

Total hip arthroplasty procedures are expected to triple from 498,000 in 2020 to 1,429,000 by 2040, while total knee arthroplasty could surpass 3.4 million in the same horizon. Within Medicare, hip and knee cases are projected to exceed 3.9 million procedures by 2060. Cemented fixation delivers 90% survival at 15-20 years, sustaining professional confidence. Spinal vertebroplasty and kyphoplasty further expand the utilization of cement, particularly in osteoporotic compression fractures. The data collectively underpin a durable growth pillar for the orthopedic bone cement and casting materials market size.

Rising Osteoporosis Prevalence in Ageing Populations

China alone hosts 145.86 – 317.54 million adults with osteoporosis, representing up to 29.49% prevalence depending on diagnostic criteria. The International Osteoporosis Foundation warns that global hip fracture incidence may double by 2050, potentially reaching 37 million fragility fractures annually. Bone quality deterioration necessitates the use of cement augmentation in joint and spinal fixation, thereby bolstering product demand. Developed economies bear the brunt as population pyramids invert, aligning cement consumption with demographic ageing trends. The orthopedic bone cement and casting materials market, therefore, mirrors broader osteoporosis epidemiology.

Rapid Uptake of Antibiotic-Loaded Bone Cements

Periprosthetic joint infection remains a leading revision cause; local antibiotic delivery via cement spacers yields up to 100% success in debridement scenarios and 82-100% in single-stage revisions. FDA clearances have broadened indications, encouraging global adoption. High-dose, multi-agent formulations address resistant staphylococcal profiles when rifampicin is contraindicated. Economic incentives to curb costly revisions further propel uptake, enhancing the orthopedic bone cement and casting materials market share of antibiotic-laden products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Orthopedic Surgeries | -0.6% | Global, acute in cost-sensitive markets | Medium term (2-4 years) |

| Bone-Cement Implantation Syndrome & Other Complications | -0.4% | Global, higher in elderly populations | Short term (≤ 2 years) |

| Stringent Regulatory Hurdles for Novel Additives | -0.3% | Advanced regulatory jurisdictions | Long term (≥ 4 years) |

| ESG Concern over MMA Emissions Influencing Procurement | -0.2% | Europe & North America primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Orthopedic Surgeries

Economic pressures constrain market expansion as healthcare systems grapple with rising orthopedic procedure costs and declining reimbursement rates, creating access barriers for cost-sensitive patient populations. France is expected to cut reimbursement by 5.7% in 2025 and plans 25% reductions by 2027, which could lead to implant shortages. The economic burden particularly affects safety-net hospitals that treat uninsured populations, with a mean loss of USD 1,846 per orthopedic admission due to inadequate reimbursement coverage. Cost containment pressures drive healthcare systems toward value-based procurement models that scrutinize cement costs relative to clinical outcomes, potentially limiting the adoption of premium formulations. Such economic pressures can defer elective procedures and promote price-sensitive procurement, thereby tempering the growth of the orthopedic bone cement and casting materials market.

Bone-Cement Implantation Syndrome & Other Complications

Clinical complications associated with cement use create adoption barriers and liability concerns that influence surgical decision-making and procedural protocols. Bone cement implantation syndrome (BCIS) incidence ranges up to 4.3% and carries a notable perioperative mortality risk.[2]Source: Yunze Yang et al., “Study of the Cement Implantation Syndrome,” md-journal.lww.com Research finds no protective effect from excluding patients with heart disease, implying a broad susceptibility. Thermal necrosis and monomer toxicity concerns prompt some surgeons to opt for cementless fixation, particularly for younger cohorts. Awareness programs and technique modifications partially mitigate risk, but the complication profile still constrains the orthopedic bone cement and casting materials market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: PMMA Dominance Faces Bioactive Challenge

PMMA commanded 78.86% orthopedic bone cement and casting materials market share in 2024, reflecting surgeon familiarity and decades of outcome data. The segment’s size reached USD 600 million, yet its forecast CAGR trails bioactive rivals at 4.8%.[3]Source: Hua Ding, “Bone Cement Distribution Patterns,” josr-online.biomedcentral.com Calcium-phosphate and ceramic mixes lead growth at 6.16% as they promote osseointegration and carry inherent antibacterial properties. Acrylic blends occupy a transitional position, offering enhanced toughness but limited differentiation. Bio-glass and nano-tantalum-fortified cements enhance imaging visibility and osteogenic signaling, with pilot trials achieving compressive strengths exceeding 100 MPa. Over the forecast window, PMMA retains bulk volumes, while bioactive entrants progressively erode share within high-performance niches of the orthopedic bone cement and casting materials market.

Clinically, PMMA’s exothermic cure, methyl-methacrylate odor, and limited bone-bonding capacity contrast with ceramic chemistry that mimics mineral phases. Reimbursement schemes still reward PMMA’s lower unit cost, yet infection-prone and osteoporotic cases push surgeons toward antibiotic-loaded or calcium-based alternatives. Regulatory pathways remain clearest for PMMA under FDA Class II special controls. Meanwhile, Europe’s MDR may accelerate adoption of newer chemistries as manufacturers harmonize evidence packages across regions, maintaining competitive tension inside the orthopedic bone cement and casting materials market.

By Product Viscosity: Medium Formulations Anchor Clinical Routine

Medium-viscosity cements accounted for 46.12% of the orthopedic bone cement and casting materials market size in 2024, valued at approximately USD 352 million. Surgeons appreciate the balanced working time of 4-6 minutes and the penetration depth, which is suitable for both arthroplasty and trauma applications. High-viscosity products expand at 6.68% CAGR, favored in vertebral augmentation and complex knee revisions, where reduced leakage mitigates neurological complications. Low-viscosity options remain niche, applied when deep cancellous infiltration is paramount.

Manufacturers deploy sealed mixing systems to minimize porosity and refine viscosity profiles—high-viscosity growth benefits from kyphoplasty uptake given controlled balloon cavity creation. Conversely, low-viscosity lines struggle within ASCs due to extended prep times. Throughout the horizon, viscosity segmentation aligns closely with shifts in procedural settings, ensuring continued relevance for diversified product portfolios across the orthopedic bone cement and casting materials market.

By Application: Knee Leads, Hip Accelerates

Total knee arthroplasty held a 38.22% share, translating to USD 292 million in cement sales for 2024. The procedure’s guideline-backed use of cemented tibial fixation preserves knee dominance. Nevertheless, hip arthroplasty’s 6.91% CAGR outpaces that of knees, as aging yet active populations seek mobility restoration. Vertebral procedures, including kyphoplasty, realize steady expansion through osteoporosis management programs, while trauma augmentation stabilizes screw purchase in weak bone.

Knee cement consumption benefits from the adoption of standardized mixing protocols and antibiotic doping mandates in cohorts at risk of infection. Hip growth reflects advanced stem designs compatible with both cemented and uncemented techniques, keeping cement volumes intact for revision or osteoporotic cases. Meanwhile, cementless alternatives are gaining traction among younger adults, introducing a nuanced sub-segmentation that vendors must navigate to protect the orthopedic bone cement and casting materials market share.

By End-User: Hospitals Remain Anchor Amid ASC Surge

Hospitals accounted for 60.56% of the 2024 value, totaling USD 462 million. Integrated trauma centers and tertiary joint-replacement programs secure steady cement purchasing. Yet ASC revenue is forecast to climb at a CAGR of 7.34% from 2025 to 2030, as payers prioritize outpatient delivery. Specialty orthopedic clinics, though smaller, capitalize on personalized implant demand and advanced imaging.

Hospitals favor bulk procurement and value-based contracts, which pressurize suppliers on price while ensuring volume certainty. ASCs require fast-curing formulations and compact mixing kits to streamline turnover. Vendors offering packaging efficiencies and rapid-set chemistries gain a competitive edge. Collectively, adaptive end-user targeting supports balanced expansion across the orthopedic bone cement and casting materials market.

Geography Analysis

North America contributed 45.62% of global revenue in 2024, anchored by high procedure density and Medicare reimbursement of joint replacements. Despite payment compression, the region maintains technology leadership and fosters ASC growth. Hip and knee episodes continue to rise, sustaining cement demand even as cementless options gain media coverage. FDA 510(k) approvals for antibiotic-loaded variants further entrench supplier portfolios.

Asia-Pacific registers the fastest 7.22% CAGR, lifted by China’s 145.86 – 317.54 million osteoporosis patient base. Expanding universal coverage in China and India funds greater elective surgery throughput, although pricing sensitivity dictates a tiered product offering. Local producers supply cost-efficient PMMA, while multinational firms introduce premium bioactive lines. Gradual harmonization of device regulations across ASEAN and NMPA reform accelerates market entry timelines.

Europe presents mixed prospects under stringent MDR requirements and reimbursement austerity. France’s planned 25% implant tariff cuts illustrate pressure on hospital budgets. Nonetheless, Germany, the United Kingdom, and Scandinavia sustain high-end revision volumes favoring antibiotic-loaded cements. Sustainability mandates spur demand for low-VOC chemistries, prompting R&D investments.

Competitive Landscape

The orthopedic bone cement industry is moderately consolidated. Five leading suppliers account for a substantial portion of global revenue, reflecting established manufacturing scale and regulatory acumen. Portfolio breadth spans standard PMMA, antibiotic-loaded variants and high-viscosity mixes. Zimmer Biomet’s Oxford Cementless Partial Knee secured FDA breakthrough device status in 2024, underscoring its dual cementless-cement compatible positioning. The firm’s 2024 net sales rose 4.3% year-on-year to USD 2.023 billion, showing sustained momentum in knees and hips.

Enovis expanded its reconstruction footprint by acquiring LimaCorporate, adding 3D-printed Trabecular Titanium implants that integrate with both cement and cementless fixation methods. Smith+Nephew reported 3.2% underlying orthopedic revenue growth in Q1 2025, leveraging the Journey II Knee and Other Reconstruction segment expansion. Start-ups pursue bio-glass and antibacterial nano-silver adjacencies, though regulatory costs can hamper commercialization.

Strategic themes include ASC-targeted packaging, ESG-oriented formulations, and AI-assisted mixing consoles aimed at dose accuracy. Vendors also invest in surgeon education platforms to preserve loyalty amid the cementless implant narrative. Overall, sustained innovation and selective M&A are expected to keep competitive intensity stable while fostering progressive technologies within the orthopedic bone cement and casting materials market.

Orthopedic Bone Cement And Casting Materials Industry Leaders

Stryker Corporation

Synimed SARL

Smith & Nephew plc

Zimmer Biomet Holdings Inc.

Johnson & Johnson (DePuy Synthes)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Zimmer Biomet launched Tekcem 1G and Tekcem 3G antibiotic cements in India for primary and revision arthroplasty fixation.

- May 2024: OsteoRemedies LLC received FDA clearance to expand the use of its Spectrum GV dual antibiotic bone cement in revision total hip arthroplasty procedures.

- April 2024: Global documented arthroplasty cases using PALACOS cement crossed 40 million, marking six decades of commercial availability.

Global Orthopedic Bone Cement And Casting Materials Market Report Scope

As per the scope of the report, bone cement can be defined as biomaterials obtained by mixing a powder phase and a liquid phase, which can be molded and implanted as a paste and can be implanted within the body. Orthopedic bone cement helps to support and strengthen prosthetic joints and broken bones. The orthopedic bone cement and casting material market is segmented by material (Polymethyl Methacrylate, or PMMA), ceramic, acrylic, and other materials, and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| PMMA |

| Calcium-phosphate / Ceramic |

| Acrylic blends & Co-polymers |

| Bio-glass & Other Advanced Materials |

| Low-viscosity |

| Medium-viscosity |

| High-viscosity |

| Total Hip Arthroplasty |

| Total Knee Arthroplasty |

| Kyphoplasty / Vertebroplasty |

| Trauma & Fracture Fixation |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Orthopedic Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | PMMA | |

| Calcium-phosphate / Ceramic | ||

| Acrylic blends & Co-polymers | ||

| Bio-glass & Other Advanced Materials | ||

| By Product Viscosity | Low-viscosity | |

| Medium-viscosity | ||

| High-viscosity | ||

| By Application | Total Hip Arthroplasty | |

| Total Knee Arthroplasty | ||

| Kyphoplasty / Vertebroplasty | ||

| Trauma & Fracture Fixation | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Orthopedic Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the orthopedic bone cement and casting materials market by 2030?

Forecasts place the market at USD 985.54 million in 2030 under a 5.25% CAGR.

Which material currently dominates orthopedic bone cement demand?

Polymethyl methacrylate commands 78.86% share owing to decades of clinical use.

Why are ambulatory surgical centers important for future cement demand?

ASCs are growing at a 7.34% CAGR, and their fast-turnover environment favors rapid-curing cement formulations.

How will antibiotic-loaded cements influence revision surgery rates?

Local antibiotic delivery has shown up to 100% infection control in debridement settings, reducing costly revisions.

Which region is expected to record the fastest growth?

Asia-Pacific leads with a 7.22% CAGR, driven by large osteoporosis populations and expanding surgical capacity.

What environmental factors are shaping product development?

ESG frameworks encourage low-VOC and MMA-reduced chemistries, pushing suppliers toward sustainable formulations.

Page last updated on: