Scar Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 26.93 Billion |

| Market Size (2031) | USD 42.44 Billion |

| Growth Rate (2026 - 2031) | 9.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Scar Treatment Market Analysis by Mordor Intelligence

The Scar Treatment Market size is expected to increase from USD 24.78 billion in 2025 to USD 26.93 billion in 2026 and reach USD 42.44 billion by 2031, growing at a CAGR of 9.52% over 2026-2031.

End-users are shifting from passive topical regimens to precision energy-based devices, spurred by rising acne prevalence, broader reimbursement for burn and trauma revision, and cultural acceptance of minimally invasive aesthetics. Energy-based platforms promise reproducible collagen remodeling with shorter downtime, while AI-guided parameter optimization is narrowing the skills gap between expert and novice operators. Stretch-mark management and pediatric burn care are emerging niches, and insurers in the United States and Western Europe have begun covering laser sessions when functional or psychological impairment is documented.[1]CMS Policy Team, “Medicare Coverage Policies Update 2024,” Centers for Medicare & Medicaid Services, cms.gov Although topical formulations still dominate unit volumes, clinic revenues are gravitating toward laser, radiofrequency, and ultrasound systems commanding procedure prices above USD 1,000 per session.[2]ISAPS Research Committee, “ISAPS International Survey on Aesthetic/Cosmetic Procedures 2024,” International Society of Aesthetic Plastic Surgery, isaps.org

Key Report Takeaways

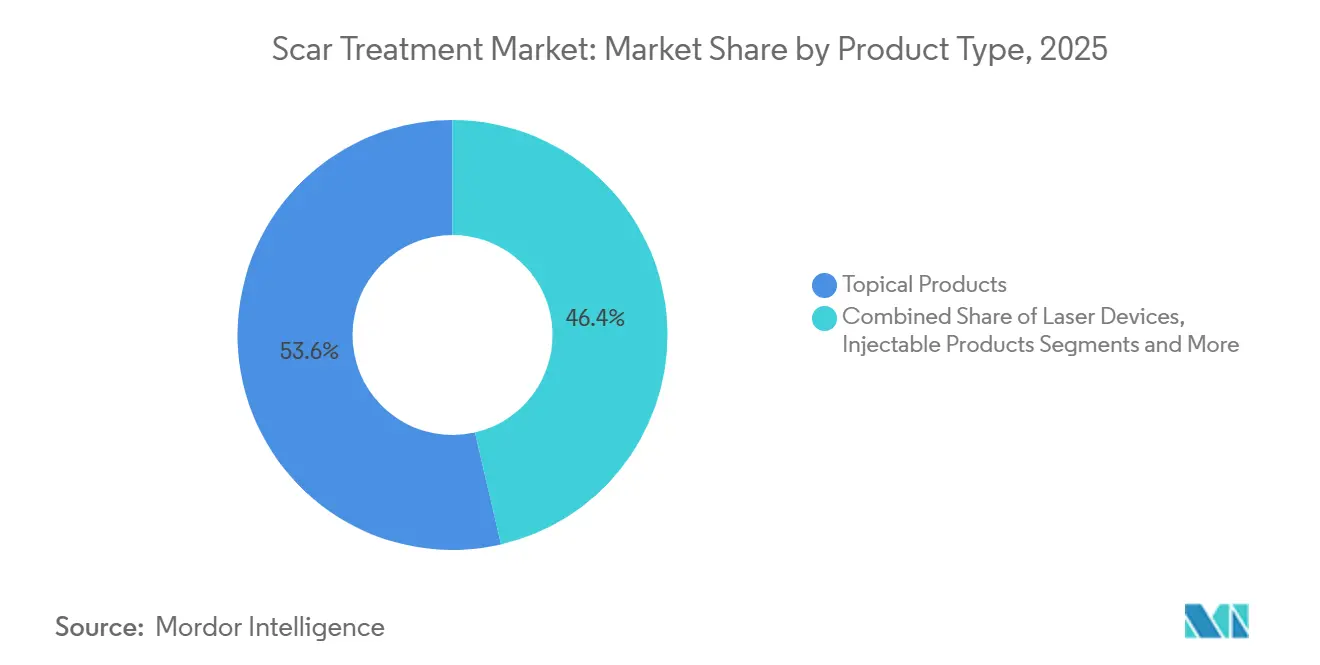

- By product type, topical products held 53.63% revenue share in 2025, while laser devices are projected to record an 11.68% CAGR through 2031.

- By treatment modality, non-energy-based approaches commanded 61.67% scar treatment market share in 2025, whereas energy-based interventions are set to advance at a 12.79% CAGR to 2031.

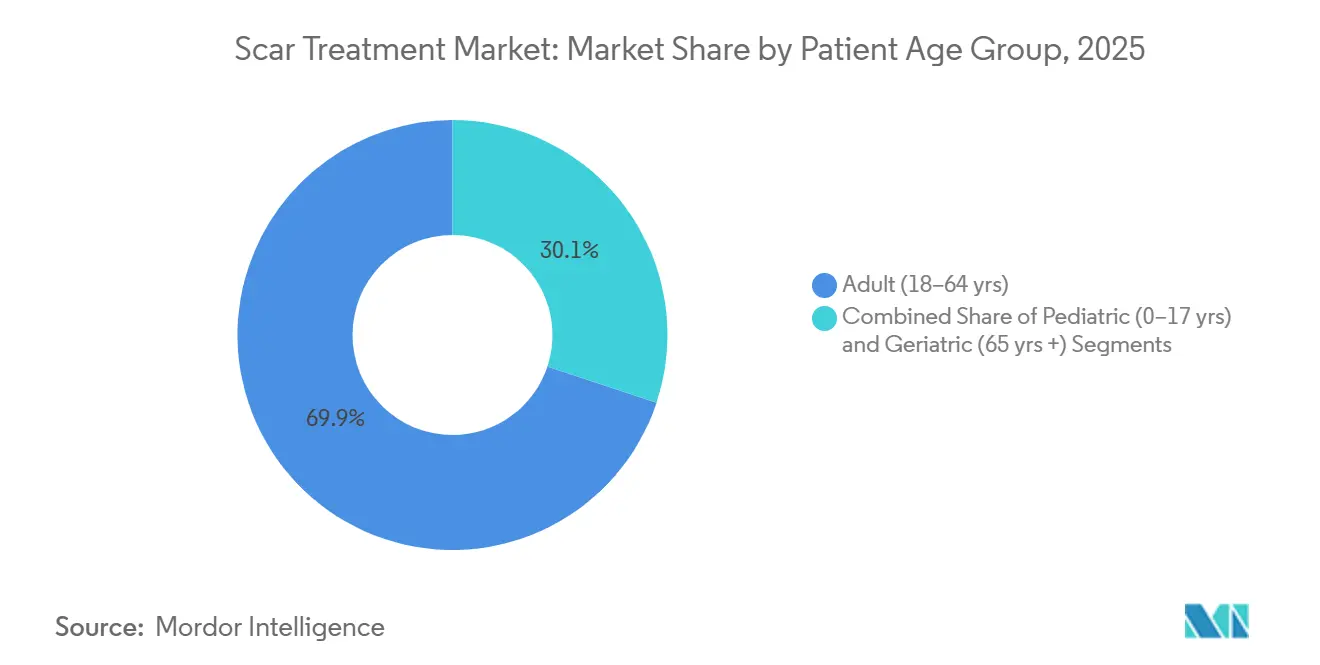

- By patient age group, adults accounted for 69.89% of revenue in 2025 and pediatrics are forecast to grow at a 10.93% CAGR over 2026-2031.

- By scar type, atrophic scars led with 32.85% of scar treatment market size in 2025, while stretch marks are expected to post an 11.58% CAGR up to 2031.

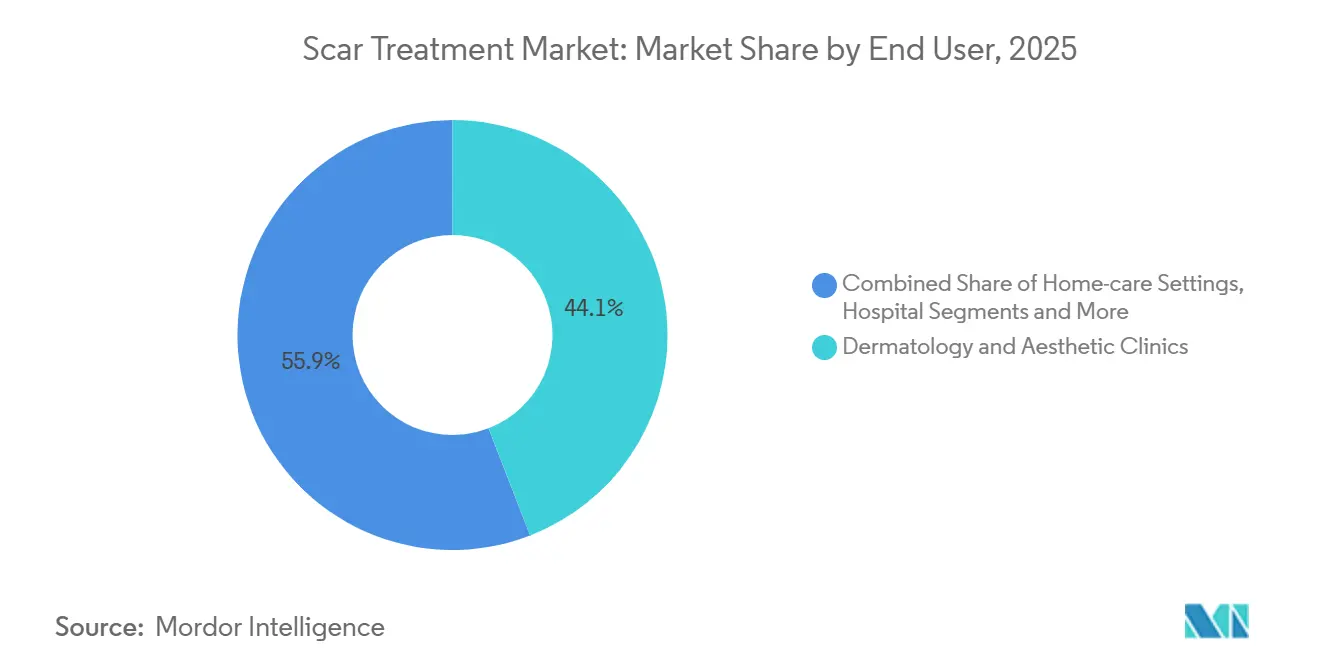

- By end user, dermatology and aesthetic clinics captured 44.12% of revenue in 2025, whereas home-care settings are projected to expand at a 13.67% CAGR through 2031.

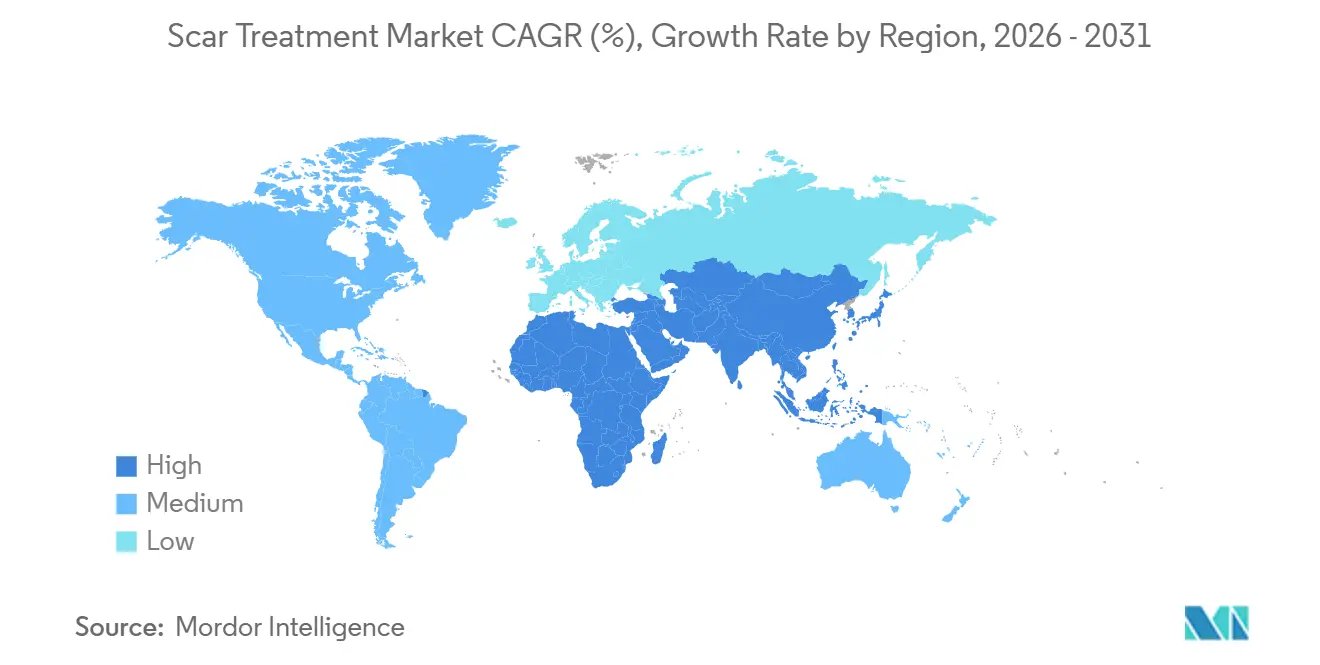

- By geography, North America dominated with 37.24% revenue share in 2025, while Asia-Pacific is anticipated to register an 11.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Scar Treatment Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Minimally Invasive Aesthetic Procedures | +1.8% | Global, with concentration in North America, Europe, and urban APAC | Medium term (2-4 years) |

| Rising Acne Prevalence among Adolescents & Young Adults | +1.5% | Global, particularly urban centers in APAC and Latin America | Long term (≥ 4 years) |

| Growing Medical Tourism for Cosmetic Dermatology in APAC | +1.2% | APAC core (Thailand, South Korea, India), spill-over to Middle East | Short term (≤ 2 years) |

| Reimbursement Expansion for Burn & Trauma Scar Revision | +0.9% | North America, Western Europe, select GCC markets | Medium term (2-4 years) |

| AI-Guided Laser Parameter Optimization | +1.4% | North America, Europe, Japan, South Korea | Short term (≤ 2 years) |

| Bioprinted Skin Substitutes Entering Late-Stage Pipeline | +0.7% | North America, Europe (clinical trial sites) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Minimally Invasive Aesthetic Procedures

Patient familiarity with botulinum toxin, fillers, and skin-tightening treatments is translating into demand for laser and radiofrequency scar revision. The 40% rise in minimally invasive procedures during 2020-2024 cemented bundled offerings where a single platform addresses wrinkles and acne scarring in one visit. Clinics report higher ticket sizes when scar packages accompany anti-aging care, and multi-indication consoles such as Cutera’s Excel V+ allow faster payback on capital outlays. Marketing emphasizes shorter downtime versus traditional ablative resurfacing, appealing to working adults. Training programs by device makers have proliferated, ensuring consistent protocol adoption across urban centers. The result is a virtuous cycle of consumer education, clinician confidence, and platform upgrades fueling the scar treatment market.

Rising Acne Prevalence Among Adolescents & Young Adults

Urban dietary shifts, stress, and pollution are extending acne into the late 20s, enlarging the pool of atrophic scar candidates. Epidemiology shows 85% of teenagers and up to 54% of adults over 25 experiencing active lesions. Fractional CO₂ and picosecond lasers achieve 50-70% scar depth reduction after three to five sessions, giving dermatologists evidence-based talking points.[3] S. K. Gupta et al., “Fractional CO₂ Laser for Acne Scarring: Systematic Review,” National Center for Biotechnology Information, ncbi.nlm.nih.gov FDA clearance of Cutera’s AviClear acne laser in 2022, with 87% one-year clearance documented in 2024, implies fewer new scars over time. Social media transparency around skin journeys reduces stigma and motivates early intervention. Together these factors expand both preventive and corrective segments of the scar treatment market.

Growing Medical Tourism for Cosmetic Dermatology in APAC

Procedure bundles in Bangkok, Seoul, and Delhi cost 50-70% less than comparable U.S. offerings, attracting self-pay patients needing multiple sessions. Thailand logged 2.8 million medical tourists in 2024, many booking fractional laser packages alongside vacation itineraries. South Korea’s dermatology revenue reached KRW 5 trillion (USD 3.8 billion) in 2024, with overseas clientele contributing 30%. Visa-on-arrival protocols, bundled hotel-clinic partnerships, and influencer testimonials reinforce momentum. This inflow boosts local clinic volumes, accelerates equipment turnover, and encourages manufacturers to locate service hubs across Asia-Pacific. Consequently, regional competition is intensifying, but economies of scale are lowering treatment prices worldwide.

Reimbursement Expansion for Burn & Trauma Scar Revision

Payers now consider psychological distress and quality-of-life scores when approving laser sessions, a policy shift codified in new CPT codes during 2024. Medicare’s coverage for fractional CO₂ treatment on ≥5% TBSA burn scars decreases financial hurdles for chronic sufferers. Insurers in Germany and France mirrored the move, citing social reintegration benefits. Pediatric burn centers leverage coverage to justify serial interventions that adapt to growth spurts. Device suppliers anticipate higher procedure throughput and are rolling out service contracts tied to reimbursed indications. The net effect is predictable volume growth, underpinning long-term forecasts for the scar treatment market.

Restraints Impact Analysis of Scar Treatment Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure Costs Outside Insurance Coverage | -0.8% | Global, most acute in North America and Western Europe | Short term (≤ 2 years) |

| Limited Efficacy Data for OTC Topical Products | -0.5% | Global, particularly affecting home-care segment | Medium term (2-4 years) |

| Strict Device Approval Timelines in Europe | -0.6% | Europe, with secondary impact on global launch sequencing | Medium term (2-4 years) |

| Shortage of Trained Laser Dermatologists in Africa | -0.3% | Sub-Saharan Africa, North Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procedure Costs Outside Insurance Coverage

Fractional CO₂ sessions cost USD 1,000-2,500 in North America, and three to five visits are common. Only functional burns or keloids sometimes qualify for insurance reimbursement, leaving acne scars and stretch marks self-pay. A 2024 ASDS poll showed 42% of interested patients walked away because of price. Cheaper entry-level lasers aim to cut session fees to USD 500-800 but may lack premium precision. Unless financing plans or coverage widens faster, sticker shock will temper near-term scar treatment market growth.

Limited Efficacy Data for OTC Topical Products

Silicone gels have proven value, yet onion extract and vitamin E remain popular despite weak data. A 2024 Dermatologic Surgery review of 37 RCTs confirmed significance only for silicone formulations. FDA classifies most OTC scar creams as cosmetics, so rigorous trials are not mandatory. Consumers may waste time on ineffective products, delaying evidence-based care and creating skepticism that spills over to professional treatments. Manufacturers of scientifically backed topicals are ramping education to defend credibility within the scar treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Scar Treatment Market Segment Analysis

By Product Type:

Topicals Retain Volume, Lasers AccelerateTopical products captured 53.63% of the scar treatment market share in 2025, driven by accessible silicone gels and sheets that cut scar height by up to 50% when used 12 weeks post-injury. However, laser devices are charting an 11.68% CAGR to 2031 as clinics invest in fractional CO₂, picosecond, and AI-enabled systems offering predictable collagen remodeling. That trajectory positions lasers to command a greater slice of scar treatment market size by decade’s end.

Capital purchases are eased by multi-indication consoles serving pigment, vascular, and resurfacing indications. Meanwhile, injectables and surface devices such as radiofrequency microneedling are rising on combination-therapy protocols that smooth texture and elevate depressions. Surgical excision remains a niche for refractory hypertrophic or contracture scars, but bioprinted grafts could disrupt this small segment once scaling resolves.

By Treatment Modality:

Energy-Based Closes the GapNon-energy methods, dominated by silicone occlusion and intralesional steroids, held 61.67% of 2025 revenue. Hydrating dressings modulate fibroblast activity, and triamcinolone injections flatten keloids by up to 70%. Yet energy-based procedures are growing 12.79% annually, narrowing the gap in scar treatment market size. Fractional CO₂ creates microthermal zones that trigger neocollagenesis, while picosecond lasers minimize thermal damage, crucial for darker skin types.

Radiofrequency microneedling systems such as Lutronic’s Genius heat the reticular dermis to 60-65 °C, contracting collagen without epidermal injury. Intense pulsed light and ultrasound occupy specialty niches for redness or shallow texture. Surgical and biologic interventions remain reserved for severe burns but could climb if regenerative grafts clear late-stage trials.

By Patient Age Group:

Adult Demand Dominates, Pediatric CAGR LeadsAdults aged 18-64 drove 69.89% of 2025 spending as acne scars, postpartum stretch marks, and surgical revisions fuel clinic traffic. Pediatric treatments, however, are rising at 10.93% CAGR, reflecting early burn-scar intervention protocols that advocate laser within six weeks of healing. FDA clearance of child-specific fluence settings on UltraPulse CO₂ and Halo hybrid lasers underscores safety progress.

Serial pediatric sessions over years create long-tail revenue for burn centers, while geriatric care focuses on post-oncology and trauma cases. Age-related fragility necessitates conservative fluences but does not dampen willingness for quality-of-life improvements, keeping all cohorts engaged in the scar treatment market.

By Scar Type:

Atrophic Tops, Stretch Marks SurgeAtrophic lesions accounted for 32.85% of 2025 revenue as fractional lasers and fillers target acne-related depressions. Picosecond systems like PicoWay deliver pigment-safe energy, expanding options for Fitzpatrick IV-VI populations. Stretch marks are accelerating at 11.58% CAGR, buoyed by postpartum aesthetics and radiofrequency microneedling trials showing 60% appearance improvement over six months.

Hypertrophic and keloid scars remain refractory; combination steroid-5-FU-PDL protocols flatten tissue but recurrence risk endures. Contracture scars after burns drive multimodal programs combining surgical release and laser resurfacing, cementing their role despite lower volume. Acne scars overlap with atrophic analytics yet retain standalone tracking for therapeutic targeting within the scar treatment market.

By End User:

Clinics Lead, Home-Care ExpandsDermatology and aesthetic clinics held 44.12% revenue in 2025, housing premium lasers and injectable services that capture higher ASPs. Bundled anti-aging and scar packages promote visit frequency and upsell pathways. Hospitals dominate burn reconstruction and complex contractures, leveraging OR capability and reimbursement. Ambulatory surgical centers appeal for outpatient excision and laser under mild sedation, balancing cost and accreditation.

Home-care, though small, is advancing 13.67% on the back of FDA-cleared handheld fractional devices and connected silicone patches delivering adherence analytics. Evidence gaps persist, but convenience draws cost-conscious consumers who might later escalate to clinic procedures, enlarging the funnel for the scar treatment market.

Geography Analysis

North America Scar Treatment Market

North America contributed 37.24% revenue in 2025, buoyed by mature insurance frameworks and 54,280 scar revision surgeries logged in 2024. Multiple next-generation platforms, such as Accure eCO₂ 3D and AVAVA’s AI-guided system, debuted here, reinforcing regional technology leadership. Cross-border traffic into Mexico and Canada continues as U.S. patients seek 40-60% procedure discounts.

Europe Scar Treatment Market

Europe maintains a significant slice, with Germany, France, and the United Kingdom spearheading device research. However, EU MDR has elongated approval cycles, prompting firms to prioritize U.S. launches. Southern markets like Italy and Spain capture value via inbound aesthetic tourism, offsetting domestic economic softness. The U.K. NHS funds functional cases, but private clinics fill gaps stemming from 12-month waitlists.

APAC and MEA Scar Treatment Market

Asia-Pacific is the growth engine at 11.22% CAGR, fueled by Thailand’s 2.8 million medical tourists, South Korea’s KRW 5 trillion dermatology sector, and China’s surging private-clinic build-out. Domestic OEM approvals in China lower device costs, broadening access. Japan and Australia remain premium markets, whereas India attracts budget-sensitive burn and keloid patients. GCC countries invest heavily in specialty centers, courting regional travelers, while Sub-Saharan Africa faces provider shortages that cap penetration.

Regulatory Landscape

Scar treatment offerings cut across multiple regulatory buckets globally, including medical devices (energy-based lasers, IPL, microneedling, phototherapy), drugs and biologics (injectables and advanced antifibrotics), and device-drug combination products. In the United States, FDA oversight is shaped by the Office of Combination Products and applicable device pathways, and the Quality Management System Regulation (QMSR) became effective on February 2, 2026, tightening requirements for design controls, supplier controls, and lifecycle quality systems for manufacturers that also sell scar-focused combination offerings.

Product classification and intended-use language still affect time-to-market for scar-adjacent technologies. In April 2026, FDA issued a final order classifying a phototherapy device intended to reduce the appearance of acute post-surgical incisions under 21 CFR 878.4880, highlighting how scar-reduction claims can map to specific device classifications. In Europe, compliance remains anchored in Regulation (EU) 2017/745 (EU MDR), with ongoing emphasis on post-market surveillance and notified body engagement. Supporting standards activity includes ISO 20417:2026 on information supplied by medical device manufacturers and the 2026 update of EN IEC 60601-2-57 for non-laser light source equipment used in therapeutic and aesthetic applications.

Value Chain Analysis

The scar treatment value chain runs from upstream specialty inputs through regulated manufacturing and multi-channel distribution. Key inputs include medical-grade silicones (polysiloxanes), adhesives, excipients, chemical precursors for topical formulations, and precision components and optics for energy-based platforms. Midstream, branded manufacturers cover topical and dressing leaders (for example, Smith+Nephew and Mölnlycke) and aesthetics and dermatology portfolios tied to devices and injectables (for example, Hologic (Cynosure), Bausch Health, and Merz), with manufacturing and validation structured around regulated quality systems and documentation requirements across device and combination product portfolios.

Downstream, products and procedures reach patients through hospitals and burn centers (often through tendering and GPO-style procurement), dermatology and aesthetic clinics (capital equipment sales paired with training and service), retail and pharmacy networks for OTC scar topicals, and a growing e-commerce channel for consumer scar-care regimens. Operational friction points include capacity constraints in specialty-grade silicone and adhesive supply, along with compliance-driven delays tied to ISO 13485 audit availability and EU MDR notified body recertification timelines, which can affect launch sequencing and availability across geographies.

Competitive Landscape

The scar treatment market skews moderately fragmented. Device majors includes Lumenis, Candela Medical, Cutera, and Hologic’s Cynosure, anchor high-energy platforms. Lumenis’ UltraPulse CO₂ sets the ablative benchmark, and its M22 IPL spans vascular and pigment concerns. Candela’s PicoWay picosecond laser excels for darker skin acne scars. Cutera’s Excel V+ consolidates vascular and resurfacing indications to maximize ROI.

Topical leaders include Biodermis and Perrigo’s ScarAway, leveraging silicone’s evidence base, while Mölnlycke’s Mepiform targets institutional sales. Injectable suppliers such as Merz and Galderma position fillers for atrophic elevation alongside lasers. Emerging disruptors chase AI parameter tuning, home-use devices, and bioprinted grafts; AVAVA’s FDA-cleared Focal Point exemplifies the convergence of software and photonics. Patent portfolios in handpiece ergonomics and algorithmic dosing create defensible moats, yet lower-cost Asian entrants are eroding price points, intensifying competition.

Scar Treatment Industry Leaders

Smith & Nephew plc

Johnson & Johnson

Bausch Health Companies Inc.

Mölnlycke Health Care AB

Hologic Inc. (Cynosure)

- *Disclaimer: Major Players sorted in no particular order

Scar Treatment Market Companies Covered in this Report

- Bausch Health (Solta Medical)

- Beijing Toplaser Technology Co. Ltd.

- Biodermis LLC

- Candela Medical

- Cutera

- Enaltus LLC (Kelo-Cote)

- Hologic

- InMode Ltd

- Johnson & Johnson (Neutrogena, Ethicon)

- Lumenis

- Lutronic Corp.

- Merz Pharma GmbH

- Molnlycke Health Care

- Perrigo Company plc (ScarAway)

- Rejuvaskin Global

- Sciton

- Smiths Group

- Candela Medical

- Zimmer Biomet

Market Opportunities and Future Outlook

Combination therapy protocols create near-term whitespace where device procedures and adjunctive agents are packaged into repeatable regimens. Clinical practice already blends fractional CO2 resurfacing with injectables such as triamcinolone, and published research and trial activity are expanding around newer regenerative and bioactive approaches, including polynucleotides and hyaluronic acid combinations for atrophic acne scars. A concrete signal of this pipeline activity is Mastelli S.r.l.s clinical trial record (NCT05936437), which lists a July 2025 completion for a polynucleotide and hyaluronic acid approach in atrophic acne scar treatment, supporting continued product development focus beyond conventional silicone-only care.

Technology-enabled delivery and home-care adjacencies also open an opportunity lane where treatment intensity and convenience are balanced. FDA-regulated microneedling devices already provide an established platform for aesthetic indications that include certain scar presentations, and they can bridge to enhanced topical delivery concepts discussed in the scientific literature, such as localized delivery approaches and microenvironment modulation. For manufacturers and providers, the opportunity is centered on building evidence-backed protocols, training, and channel strategies that connect OTC scar-care initiation to clinic-based escalation, while keeping claims, labeling, and quality-system requirements aligned with evolving device classifications.

Recent Industry Developments in Scar Treatment Market

- May 2026: Smith+Nephew highlighted progress initiatives in chronic wound care, reinforcing investment and commercial focus in advanced wound management portfolios that also feed demand for downstream scar-care products used in recovery pathways. Stronger wound-healing ecosystems support standardized discharge and home-care regimens where silicone-based scar management is commonly positioned.

- April 2026: Bausch Health (Ortho Dermatologics) expanded access by enabling online ordering for Biafine Skin Recovery Emulsion in the United States. Wider direct-to-consumer availability supports post-procedure and post-injury skin recovery routines that often accompany scar-management protocols.

- February 2026: Bausch Health (Solta Medical) launched the Clear + Brilliant Touch laser in Canada following Health Canada approval granted on May 20, 2025. The geographic expansion strengthens clinic-side technology availability for minimally invasive resurfacing workflows that overlap with acne-scar and texture-improvement treatment plans.

Scar Treatment Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers the revenues generated from products and in-clinic procedures used to reduce the appearance and symptoms of scars that can follow burns, injuries, acne, and surgeries. It includes common topical options and energy-based treatments that are delivered through clinical and retail channels.

Scope exclusions: We exclude cosmetic procedures that are not intended for scar revision and any non-scar aesthetic treatments.

Segments Covered in This Report

- By Product Type

- Topical Products

- Laser Devices

- Surface Treatment Devices (Dermabrasion & Micro-needling)

- Injectable Products (Dermal Fillers & Steroids)

- Surgical Invasive Procedures

- By Treatment Modality

- Non-Energy–Based (Topical, Silicone, Injectables)

- Energy-Based (Laser, RF, Ultrasound, IPL)

- Surgical & Biologic Interventions (Excision, Grafting, Bioprinted Skin)

- By Patient Age Group

- Pediatric (0–17 yrs)

- Adult (18–64 yrs)

- Geriatric (65 yrs +)

- By Scar Type

- Atrophic Scars

- Hypertrophic & Keloid Scars

- Contracture Scars

- Stretch Marks

- Acne Scars

- By End User

- Hospitals

- Dermatology & Aesthetic Clinics

- Ambulatory Surgical Centers

- Home-care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clear demand context for scars and how they get treated in real settings, since not every scar becomes a paid treatment event. We reviewed open, reputable sources such as the Centers for Disease Control and Prevention (CDC), the World Health Organization (WHO), the National Institutes of Health (NIH) and PubMed-indexed clinical literature, and government health statistics portals across major regions.

To translate care patterns into a market model, we also used items like clinical guidelines and position statements from dermatology and burn care associations, along with public hospital statistics and health system publications where available. Company annual reports, investor presentations, and press releases were used to understand product mix changes, pricing direction, and route-to-market shifts, and then cross-checked with a paid subscription we use for company financials, news flow, and patent data signals. These desk sources are illustrative only, and many other public and paid sources were also referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary conversations were used to test what is actually counted as scar treatment spend across channels, and to confirm how the treatment mix changes by scar type and by patient pathway (self-care versus provider-led). We spoke with a blend of clinicians, clinic administrators, distributors, and product-side experts across Americas, EMEA, and APAC, so assumptions on utilization, pricing, and adoption were grounded in day-to-day practice.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 17% | APAC: 48% |

| Mid tier: 49% | Functional/Unit leaders: 39% | EMEA: 31% |

| Smaller Players: 19% | Managers: 44% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic in a practical way, where prevalence and treatment-seeking behavior are translated into an addressable treated pool by geography, and then converted into value through typical pricing and procedure mix. When the model is structured this way, the key steps become traceable: we estimate how many scar cases are active, what share seeks any treatment, and how often a paid product or procedure is used in a year.

Inputs were chosen to match how scar care is delivered, such as burn and trauma incidence indicators, elective surgery volumes as a proxy for new scar formation, clinic visitation patterns for dermatology and aesthetics, mix shifts between topical products and energy-based procedures, and average selling price movement for common topical formats. Results were then checked with selective bottom-up approximations, including sampled price points across channels and a supplier and clinic roll-up sanity check in a few anchor countries, and gaps were handled by using proxy utilization rates from similar markets until interview feedback supported adjustments.

For forecasting, we leaned on scenario analysis supported by expert views on procedure adoption and retail availability, and then ran sensitivity checks on the two variables that usually move the total the most, which are treatment-seeking rate and price progression. Where volatility was seen in a region, we tightened assumptions using conservative ranges before the final outlook was locked.

Data Validation & Update Cycle

Outputs are validated through multiple checks so that unusual spikes or drops can be explained before publication. We compare totals against independent signals like procedure volumes, channel availability expansion, and reported sales direction from public disclosures, and then review variances at region level to spot where an assumption might be overstated.

A second analyst review is done before sign-off, and follow-up outreach is triggered when a metric falls outside expected ranges, such as an abrupt price jump without a matching mix change. Reports are refreshed annually, with interim updates when a material event impacts pricing, access, or utilization. Before delivery, a fresh analyst pass is completed so clients receive the most up-to-date view available at that time.

Mordor Intelligence's Scar Treatment Market Size Measured Against Other Published Estimates

Published market values for scar treatment can differ even when the topic name looks the same, because the included treatment types, the base year timing, and the way pricing is normalized are not consistent across sources. Differences also show up when one estimate leans more on procedure-heavy settings, while another leans more on retail topical products.

The benchmark table shows a wide spread mainly because, in Mordor Intelligence's model, the counted revenue is tied to scar management products and energy-based procedures, while excluding cosmetic services that are not meant for scar revision, which reduces scope overlap with broader aesthetics totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 24.78 B (2025) | |

| Global Consultancy A | USD 32.29 B (2025) | Uses a broader treatment basket that can implicitly pull in adjacent aesthetic procedure revenues and wider service fees, which inflates the value versus a scar-revision-only spend view. |

| Trade Journal B | USD 16.73 B (2023) | Uses an earlier base year and a more conservative channel capture in some regions, and the reported value can be sensitive to how in-clinic procedure pricing and currency timing are converted. |

Looking across the three figures, the gap is best explained by what gets counted as scar-related revenue and how the base year and price inputs are set. By keeping the model tied to a treated scar demand pool and then checking totals against real-world utilization signals, we can give buyers a number that is easier to trace, challenge, and reuse in planning.

Key Questions Answered in the Report

How large is the scar treatment market?

The scar treatment market size reached USD 26.93 billion in 2026 and is projected to hit USD 42.44 billion by 2031.

What is the main growth driver after 2026?

Rising acceptance of minimally invasive energy-based devices, delivering faster recovery and measurable outcomes, will underpin the 9.52% CAGR forecast.

Which product category is growing fastest?

Laser devices are on track for an 11.68% CAGR through 2031 as clinics favor fractional CO₂ and picosecond platforms for collagen remodeling.

Why is Asia-Pacific the most dynamic region?

Medical-tourism pricing 50-70% below Western levels, combined with advanced technology hubs in Thailand, South Korea, and India, is driving an 11.22% regional CAGR.

Are topical scar products clinically proven?

Silicone gels and sheets have robust evidence for flattening and softening scars, whereas onion extract and vitamin E lack statistically significant benefits in controlled trials.

How will AI influence future treatments?

AI-guided parameter optimization is reducing operator variability and procedure time, making advanced laser resurfacing more accessible across clinic networks.

Page last updated on: