Bone Cement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.23 Billion |

| Market Size (2031) | USD 1.61 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

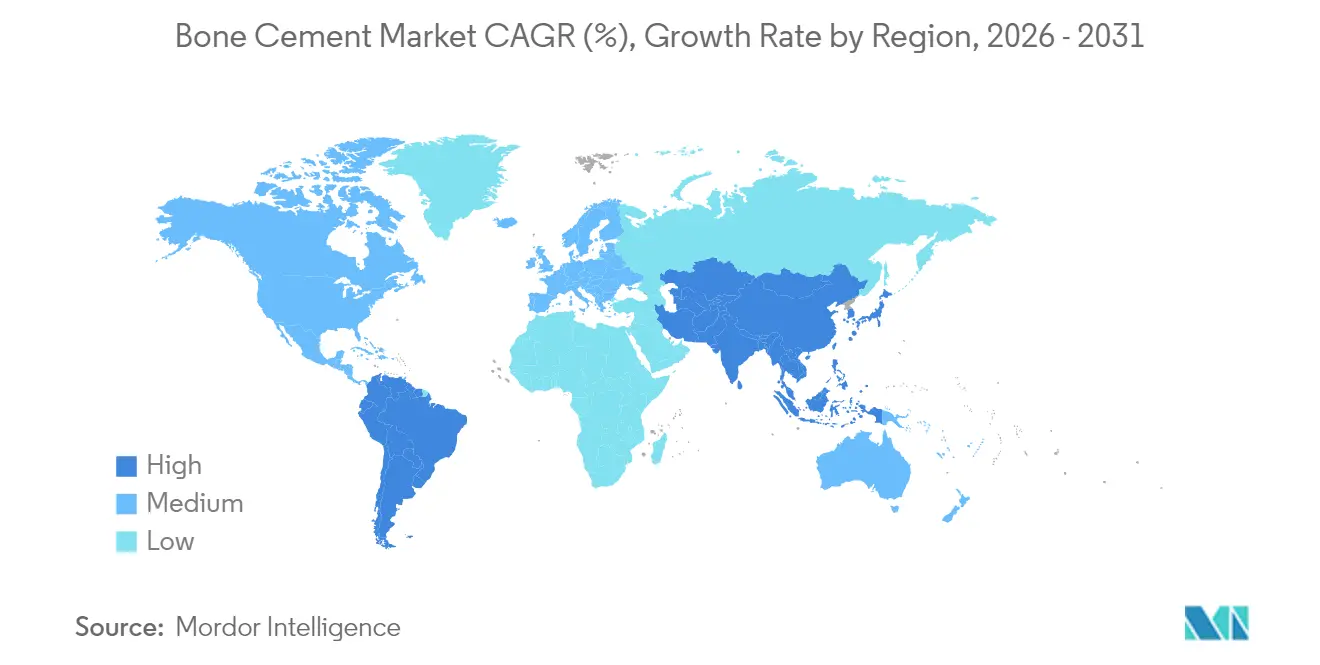

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

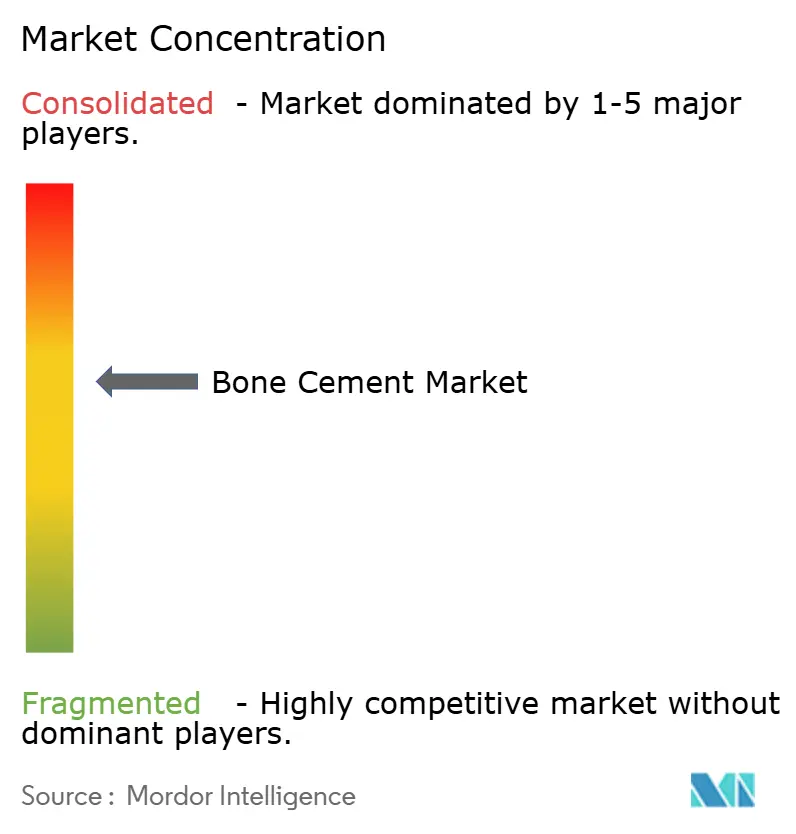

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bone Cement Market Analysis by Mordor Intelligence

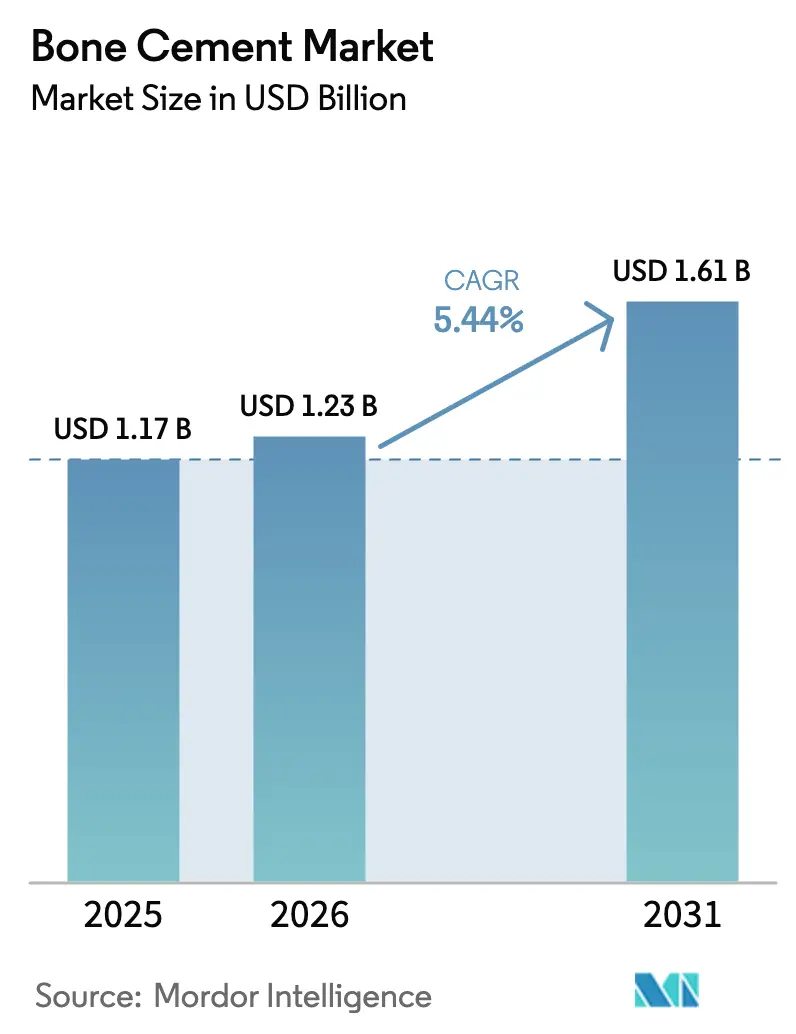

Bone Cement market size in 2026 is estimated at USD 1.23 billion, growing from 2025 value of USD 1.17 billion with 2031 projections showing USD 1.61 billion, growing at 5.44% CAGR over 2026-2031. Robust procedure growth among older adults, rapid uptake of minimally invasive spine surgeries, and steady advances in antibiotic‐loaded formulations collectively sustain demand. North America continues to lead revenue, yet Asia-Pacific delivers the quickest expansion on the back of wider health-insurance coverage, higher osteoporosis incidence, and accelerating hospital build-outs. Product innovation centers on high-viscosity polymethyl methacrylate (PMMA) blends that curb leakage, while calcium-phosphate alternatives gain attention for their bioactivity and lower exothermic profiles. Competitive intensity remains moderate as incumbents rely on clinical evidence and surgeon relationships to defend share against cementless implants and emerging bioactive cements. Growth opportunities also stem from AI-guided injection systems that cut complication rates and 3-D-printed patient-specific spacers that personalize fixation.

Key Report Takeaways

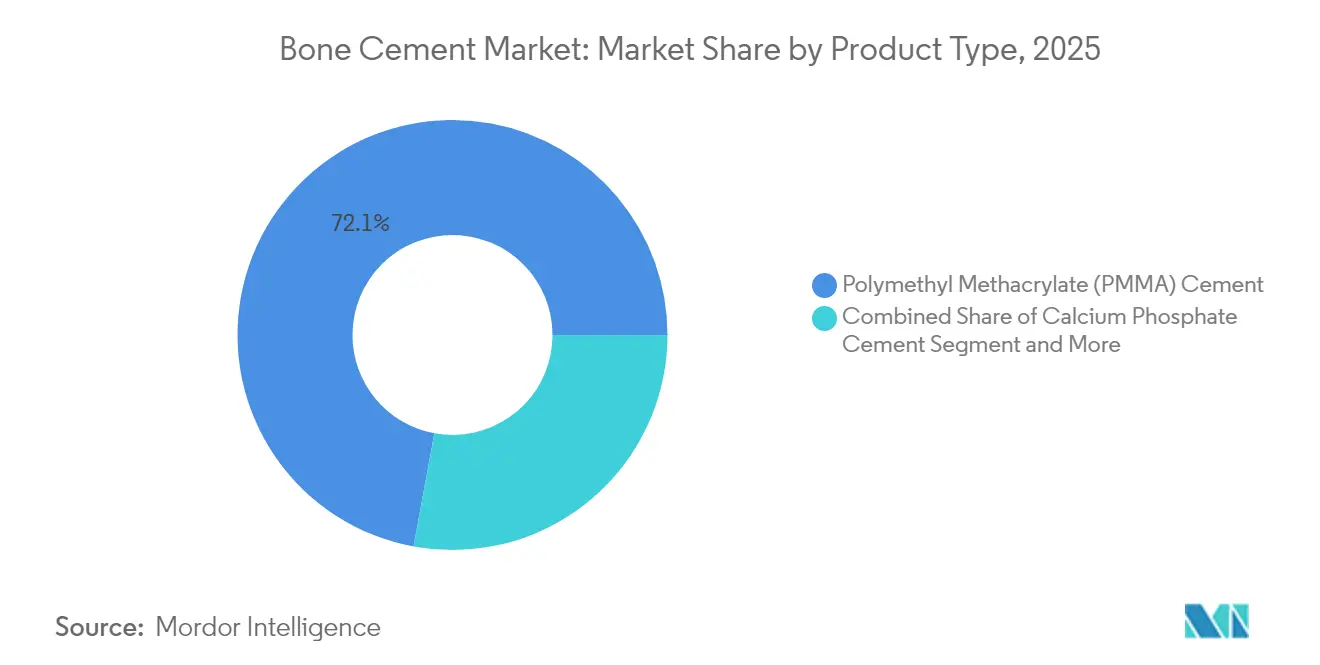

- By product type, Polymethyl Methacrylate (PMMA) Cement held 72.10% of bone cement market share in 2025, whereas calcium-phosphate cement is forecast to log the fastest 6.63% CAGR to 2031.

- By viscosity, medium-viscosity cement captured 44.65% of 2025 revenue, while high-viscosity grades are projected to advance at a 6.88% CAGR through 2031.

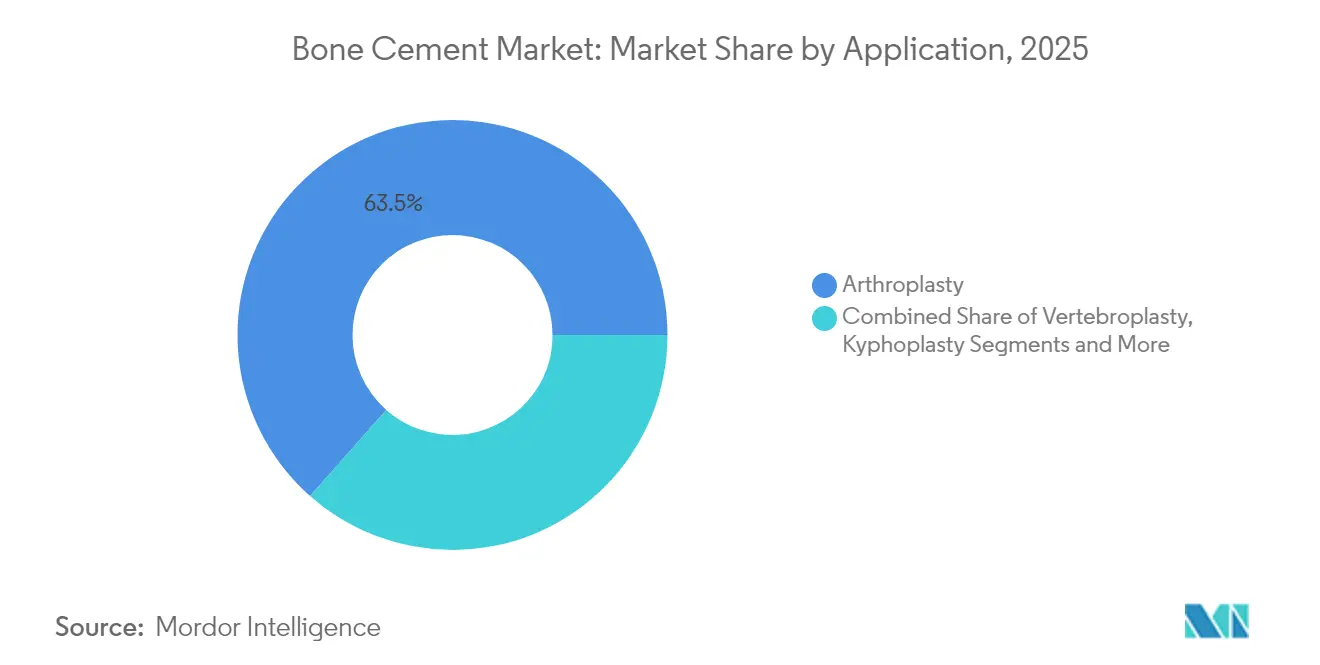

- By application, arthroplasty represented 63.48% of bone cement market size in 2025, whereas kyphoplasty is on track for the highest 6.52% CAGR over the outlook period.

- By end-user, hospitals accounted for 52.10% of 2025 demand, even as ambulatory surgical centers are poised for a 7.02% CAGR through 2031.

- By geography, North America commanded 41.05% of 2025 revenue, and Asia-Pacific is projected to expand at a 6.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bone Cement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing-Related Arthroplasty Volumes Rising Sharply | +1.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Sports & Road-Traffic Trauma Boosting Revision Surgeries | +1.2% | North America & APAC core, spill-over to Europe | Medium term (2-4 years) |

| Surge in Antibiotic-Laden Cement to Curb Post-Operative Infections | +1.0% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Outpatient Joint-Replacement Expansion in ASCs | +0.8% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| AI-Guided Injection Systems Reducing Cement Leakage | +0.6% | North America & EU, selective APAC markets | Long term (≥ 4 years) |

| 3D-Printed Patient-Specific Spacers Enabling Custom Mixes | +0.4% | North America & EU, limited APAC penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing-Related Arthroplasty Volumes Rising Sharply

Populations aged 65 and older are growing faster than any other demographic, and they increasingly seek mobility-restoring surgeries instead of living with disability. The rise reflects new anesthesia protocols, more durable implants, and value-based payment models that favor early intervention. Sustained procedure volumes translate directly into repeat demand for cement, especially in elderly bones of lower density that benefit from PMMA’s immediate fixation. Longer life expectancy also increases the pool of revision cases, further amplifying cement consumption. Collectively, these demographic and clinical shifts add roughly 1.8 percentage points to forecast CAGR.

Sports & Road-Traffic Trauma Boosting Revision Surgeries

Greater recreational sports participation and urban congestion elevate high-energy injury rates, driving revision orthopedics. The United States reported more than 7 million orthopedic injuries and 1.1 million emergency surgeries in a single year, with complex trauma requiring larger cement volumes for bone void filling.[1]Source: Molly P. Jarman et al., “The National Burden of Orthopedic Injury,” Journal of Surgical Research, ecommons.aku.edu High-grade fractures often entail staged fixation and augmentative cement, multiplying unit consumption per patient. Emerging economies mirror this trend as motorcycle ownership surges and road-safety enforcement lags. The aggregate effect lifts bone cement market growth by an estimated 1.2 percentage points through mid-decade.

Surge in Antibiotic-Laden Cement to Curb Post-Operative Infections

The escalating threat of prosthetic joint infections has catalyzed widespread adoption of antibiotic-loaded bone cement as a prophylactic measure. Antibiotic-loaded PMMA has slashed prosthetic-joint infection rates from 5% to under 1% over three decades.[2]Source: Tom A. G. van Vugt et al., “Antibiotic-Loaded PMMA Beads and Spacers,” Frontiers in Microbiology, frontiersin.org Hospitals now treat antibiotic-rich formulations as standard of care for high-risk patients, and newer blends incorporating antifungals preserve mechanical strength while targeting rare but lethal fungal invasions. Broader reimbursement acceptance, especially in Europe, accelerates clinical uptake. The driver contributes a net 1 percentage-point boost to CAGR by enlarging the overall eligible patient base. The clinical success of these formulations is driving broader acceptance and regulatory approvals across multiple markets.

Outpatient Joint-Replacement Expansion in ASCs

The structural shift toward outpatient joint replacement procedures represents a fundamental transformation in orthopedic care delivery models. Same-day hip and knee replacements are mainstream in ambulatory surgical centers, offering 40-60% cost savings with comparable outcomes. Policy moves that reclassify traditional “inpatient-only” procedures spur volume migration, raising demand for fast-setting or high-viscosity cements that shorten turnover time. As payer bundles increasingly reward lower site-of-care costs, ASC cement sales are set to outpace overall market expansion, adding 0.8 percentage points to CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent FDA & MDR Approval Timelines | -1.2% | Global, with highest impact in North America & EU | Medium term (2-4 years) |

| High Exothermic Polymerisation Causing Thermal Necrosis Risk | -0.8% | Global, with increased scrutiny in developed markets | Short term (≤ 2 years) |

| Growing Preference for Cement-Less Implants in Young Patients | -1.4% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Environmental Disposal Concerns for PMMA Residues | -0.6% | EU & developed APAC markets, spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent FDA & MDR Approval Timelines

Regulatory complexity surrounding bone cement modifications and new formulations is creating significant barriers to innovation and market entry. Special 510(k) pathways still require exhaustive bench testing data, and Europe’s MDR demands more clinical evidence, delaying launches by up to 18 months and adding significant pre-market costs. These regulatory hurdles disproportionately impact smaller companies and innovative startups that lack the resources to navigate complex approval processes, potentially stifling competition and technological advancement in the bone cement sector. The net effect drags the bone cement market expansion by 1.2 percentage points during the medium term.

High Exothermic Polymerisation Causing Thermal Necrosis Risk

The fundamental chemistry of PMMA polymerization presents an inherent safety challenge that continues to limit adoption in certain clinical applications. PMMA polymerisation can exceed 70 °C, jeopardizing peri-prosthetic tissue health.[3]Source: Gergo Tamas Szoradi et al., “Thermal Necrosis at the Cement–Bone Interface,” Applied Sciences, mdpi.com New cooling techniques and alternative monomers are promising but remain niche. Such safety concerns dampen surgeon enthusiasm, particularly for spinal channels near neural structures, trimming CAGR by 0.8 percentage points in the near term. The thermal necrosis risk creates liability concerns for healthcare providers and drives preference toward alternative fixation methods in temperature-sensitive anatomical locations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PMMA Dominance Faces Bioactive Challenges

PMMA maintained a commanding 72.10% bone cement market share in 2025 on the strength of long-term survivorship data and surgeon familiarity. The segment’s reliability keeps procurement departments aligned with legacy vendors, anchoring hospital formularies. Recent innovations, such as nano-tantalum carbide doping, improve radiopacity without undermining biomechanics. Yet calcium-phosphate cement is projected to post a 6.63% CAGR as orthopedic oncologists and trauma surgeons adopt its osteoconductive chemistry to accelerate bone integration. Glass-polyalkenoate cements find footholds in dental and craniofacial repairs where fluoride release is beneficial, while calcium-sulfate blends satisfy niche infection-management needs through resorbability.

Reimbursement revisions that reward faster union and fewer re-operations favor bioactive alternatives. However, scale economies, mature supply chains, and easier storage conditions preserve PMMA’s lead in the bone cement market. Continued R&D inside the conventional chemistry – such as low-monomer, high-viscosity variants – aims to extend PMMA’s lifecycle. The bone cement industry nevertheless perceives product diversification as inevitable, with first-mover brands positioning dual portfolios that marry PMMA cash flows to next-generation biomaterials.

By Viscosity: High Viscosity Gains Momentum Through Safety Profile

Medium-viscosity cement captured 44.65% revenue in 2025, serving as the workhorse for hip and knee arthroplasty. High-viscosity grades are forecast to expand at a 6.88% CAGR on evidence that leakage drops from 37.5% to 15% in vertebroplasty. Surgeons appreciate its dough-like handling and lower injection pressures, boosting operative confidence in spine cases. Low-viscosity mixes still earn favor for deep cancellous infiltration, though their declining usage mirrors heightened risk aversion.

Market education campaigns spotlight mechanical strength retention even after refrigeration-based working-time extensions. At the same time, fast-setting formulas shave theatre time by three to five minutes without sacrificing compressive endurance. Collectively, viscosity-specific innovations broaden surgeon toolkits, making the bone cement market more segmented and tailored to procedural nuance.

By Application: Arthroplasty Leadership Challenged by Spinal Growth

Arthroplasty procedures consumed 63.48% of 2025 volumes, buttressed by rising acceptance of shoulder, elbow, and ankle replacements in addition to hip and knee. The segment’s revenue base keeps the bone cement market anchored in large-joint orthopedics. Nonetheless, kyphoplasty is projected to register the fastest 6.52% CAGR as vertebral compression fractures climb with aging demographics. Vertebroplasty stays relevant for acute stabilization, though cement‐volume optimization studies now cap infusion at 40.5% of vertebral body capacity to avoid adjacent fractures.

Emerging bio-composite cements combining tri-calcium phosphate and chitosan foster improved osteointegration at lower curing temperatures, opening doors to younger cohorts and trauma indications. As clinical evidence accumulates, hospitals may recalibrate protocols toward spine and trauma segments, subtly rebalancing overall bone cement market size distribution.

By End-User: ASC Expansion Reshapes Care Delivery Models

Hospitals retained 52.10% revenue share in 2025 by virtue of managing complex revisions and multi-comorbidity cases that demand intensive post-operative care. Yet ambulatory surgical centers are on course for a 7.02% CAGR, catalyzed by bundled-payment incentives and consumer preference for same-day discharge. Orthopedic clinics handle routine fracture augmentations, serving as feeder channels to ASCs for eligible patients, while specialty spine centers champion technology adoption, including AI-guided injectors.

For cement suppliers, channel strategy now bifurcates: value-priced bulk packaging for hospitals and premium fast-setting packs for high-throughput ASCs. Training programs emphasize efficient mixing and reduced fumes to meet stringent outpatient ventilation standards. Such tailoring further differentiates offerings inside the bone cement market.

Geography Analysis

North America generated 41.05% of 2025 revenue, with high procedure density, favorable reimbursement, and early adoption of antibiotic-rich blends anchoring sales. Major integrated delivery networks lock multi-year contracts with incumbent vendors, which stabilizes baseline demand even as cementless implants nibble at the younger-patient tier. Numerous state and federal initiatives targeting opioid-sparing postoperative protocols also fuel wider elective-surgery throughput, reinforcing cement volumes.

Europe remains the second-largest cluster, characterized by stringent MDR compliance that pushes suppliers to furnish more real-world evidence. Germany, France, and the United Kingdom collectively represent over half of regional consumption, but Eastern European markets now post double-digit value growth as private hospital chains modernize orthopedic suites. Pan-EU procurement alliances increasingly evaluate life-cycle cost, thereby bolstering the shift to antibiotic-loaded and high-viscosity variants that promise lower revision rates.

Asia-Pacific holds the fastest 6.95% CAGR outlook as China, Japan, and India dramatically scale joint-replacement capacity. Government insurance expansion, rising osteoporosis prevalence, and medical-tourism corridors in Thailand and Malaysia underpin multi-year tailwinds. The region’s surgical-volume surge gradually narrows the bone cement market size gap with Western peers while inviting local entrants that focus on cost-sensitive yet clinically validated PMMA blends. Collectively, these dynamics keep the bone cement market on a geographically diversified growth path.

Regulatory Landscape

In the United States, polymethylmethacrylate (PMMA) bone cement is regulated as a Class II medical device under 21 CFR 888.3027. Market entry is commonly supported through the 510(k) pathway and FDA special controls guidance for PMMA bone cement. Special controls focus on performance and safety evidence aligned with recognized standards for acrylic resin cements (for example, ISO 5833:2002 for physical and mechanical testing), along with labeling and risk controls tied to handling, polymerization heat, and radiopacity.

In Europe, the Medical Device Regulation (EU MDR) raises evidence expectations for legacy and modified formulations, including ongoing post-market clinical follow-up activities and broader technical documentation under manufacturer obligations (for example, MDR Article 10). These requirements are most noticeable for iterative changes such as antibiotic loading, viscosity modifications, or delivery-system integration, which can extend change-control cycles and increase the value of real-world evidence packages alongside bench and biocompatibility testing.

Value Chain Analysis

The bone cement value chain starts with petrochemical and specialty-chemical inputs, including methyl methacrylate monomer (naphtha-derived), PMMA powder components, radiopacifiers such as barium sulfate, and, for antibiotic-loaded offerings, active ingredients such as gentamicin sulfate. These inputs feed into regulated manufacturing where blending, sterilization, and packaging integrity are critical. Cement performance is tightly linked to polymerization behavior, viscosity, working time, and radiopacity consistency.

Downstream distribution often relies on hospital tenders, long-term agreements, and consignment inventory models, with complementary sales of mixing and delivery accessories. Operational dependencies extend beyond the cement kit itself, including reverse logistics for consignment management and refurbishment of supporting equipment such as vacuum pumps used in mixing workflows. Recent supply disruptions have underscored how single-point failures, for example packaging or equipment faults, can trigger rapid substitution protocols across provider networks, shifting demand toward alternate approved brands that can maintain continuity of care.

Competitive Landscape

The bone cement market features moderate consolidation, with five global brands controlling a majority of sales yet facing niche innovators in bioactive and high-viscosity segments. Leaders leverage surgeon education, bundled instrument deals, and antibiotic-cement portfolios to retain formularies. Zimmer Biomet, for instance, introduced the Persona SoluTion PPS femur for metal-sensitive patients, the latest sign of a dual-strategy hedging cement and cementless bets.

Regional challengers exploit cost-advantage manufacturing to serve price-sensitive hospitals, especially in Asia-Pacific’s secondary cities. Some pair PMMA powders with locally compounded monomer liquids to skirt import duties, though global majors counter with turnkey mixing systems that cut operating-room prep to under two minutes. Antibiotic-focus specialists further fragment the landscape, marketing gentamicin or vancomycin blends for infection-prone cohorts.

AI-enhanced injector startups partner with radiology-equipment makers to embed cement parameters into spine-navigation consoles. While still sub-1% of revenue, such alliances signal value migration from material to delivery technology within the bone cement market. In response, incumbents increase R&D outlays or pursue selective acquisitions, mirroring broader med-tech convergence patterns.

Bone Cement Industry Leaders

Stryker

Johnson & Johnson (Depuy Synthes)

Zimmer Biomet

Smith & Nephew

Exactech

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A practical opportunity is increased resilience in manufacturing and contracting. Provider procurement groups have needed to operationalize substitution pathways during localized supply disruptions, including NHS Supply Chain communications around Heraeus Medical bone cement supply issues and follow-on production resumption updates. This operating reality creates room for suppliers that can support continuity through near-shore production footprints, dual-sourcing of critical inputs (monomer, radiopacifiers, antibiotic API), and redundancy at packaging lines, then convert those capabilities into long-term supply agreements and value-based contracting.

On the product side, antibiotic-loaded and procedure-specific cements provide a concrete route to differentiation, supported by ongoing FDA 510(k) activity for cement families and line extensions. Recent U.S. regulatory clearances and commercial launches for antibiotic-loaded PMMA cements, combined with higher outpatient arthroplasty throughput in ambulatory surgical centers, support demand for standardized, fast, and reproducible operating-room workflows. Suppliers that pair cement formulations with delivery and mixing systems, training, and real-world evidence packages are positioned for hospital formulary retention, while also extending into ASCs and specialty spine centers that prioritize leakage control and operating time reduction.

Recent Industry Developments

- July 2026: Apheon entered exclusive negotiations to acquire a majority stake in Teknimed, signaling strategic consolidation in orthopaedic biomaterials. The move could enable platform expansion and accelerated global growth in bone cement and related biomaterials.

- April 2026: Biomet France received U.S. FDA 510(k) clearance (K254107) for Refobacin Bone Cement R. The approval expands Biomet France's US bone cement portfolio and strengthens its competitive position.

- February 2026: Biocomposites announced the immediate UK launch of its SYNICEM bone cement range to address a supply crisis. Local manufacturing led to relief of supply constraints and could support share gain in the UK market.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from bone cement used by healthcare providers to fix implants and stabilize bone during orthopedic and spine procedures, including standard and antibiotic-loaded formulations sold across major regions.

Scope exclusions: We exclude dental adhesives, general tissue glues, and non-medical construction or industrial cements that are not used for human orthopedic care.

Segmentation Overview

- By Product Type

- Polymethyl Methacrylate (PMMA) Cement

- Calcium Phosphate Cement

- Glass Polyalkenoate Cement

- Calcium-Sulphate-Based Cement

- By Viscosity

- Low Viscosity

- Medium Viscosity

- High Viscosity

- By Application

- Arthroplasty

- Total Knee Arthroplasty

- Total Hip Arthroplasty

- Total Shoulder Arthroplasty

- Vertebroplasty

- Kyphoplasty

- Trauma & Fracture Repair

- Others

- Arthroplasty

- By End-User

- Hospitals

- Orthopaedic Clinics

- Ambulatory Surgical Centres

- Speciality Spine Centres

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand pool and to set realistic procedure and population anchors before assumptions were tested. We leaned on public health and utilization sources such as the CDC, OECD Health Statistics, World Health Organization datasets, and national arthroplasty registries for hip and knee procedures where available.

To keep the model grounded, we also reviewed sources such as the FDA for product clearances and safety communications, CMS for reimbursement context, and peer-reviewed orthopedic journals for cement usage practices (for example, the adoption of antibiotic-loaded cement in revision cases). Company annual reports, investor decks, and credible medical press were reviewed to understand portfolio mix and pricing direction, and paid company financials and intelligence subscriptions, plus a patent database, helped with cross-checks on coverage and the pace of innovation. These examples are not exhaustive, and additional public and paid sources were used for data collection, validation, and clarification during analysis.

Primary Interviews and Surveys

Primary work focused on validating how bone cement is actually used and purchased, since list prices and clinical preference can vary by hospital purchasing rules and by procedure type. We spoke with hospital procurement teams, distributors, orthopedic and spine clinicians, and industry roles across the Americas, EMEA, and APAC to fill data gaps and pressure-test the inputs behind volumes, ASPs, and adoption shifts.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 14% | APAC: 43% |

| Mid tier: 51% | Functional/Unit leaders: 39% | EMEA: 34% |

| Smaller Players: 15% | Managers: 47% | Americas: 23% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand reconstruction, where procedure volumes for joint replacement and vertebral augmentation were translated into cement consumption using typical grams-per-procedure and usage rates, and then converted to value through region-sensitive ASP assumptions. To keep totals realistic, we corroborated outputs with selective bottom-up checks, such as sampled supplier revenue splits, distributor channel checks, and simple volume times ASP roll-ups for a few high-visibility countries.

Key inputs that shaped the model included hip and knee arthroplasty counts, vertebroplasty and kyphoplasty activity, the mix between primary and revision surgeries (which shifts antibiotic-loaded uptake), viscosity preference by setting, and the pricing spread between PMMA and alternative chemistries. Where data was thin for smaller countries, we used proxy indicators like age mix, osteoporosis burden, and surgical capacity, then adjusted the implied per-capita procedure rates through expert review. Forecasting relied mainly on scenario analysis, with procedure-growth and ASP pathways agreed with interview feedback, followed by sensitivity checks on reimbursement and revision-rate changes.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent demand signals, including procedure benchmarks, demographic trends, and reported revenue exposure from relevant product lines. Variance checks were run by region and by application so any outliers in implied cement-per-procedure, ASP, or growth rates could be flagged and reworked, followed by a second-step analyst review before sign-off.

The report is refreshed annually, and interim updates are triggered when material events occur, such as major regulatory actions, pricing resets, or meaningful procedure disruptions. Before delivery, a final pass is completed so clients receive a view that reflects the latest available information and refreshed assumptions.

Mordor Intelligence's Bone Cement Market Size Compared With Other Published Estimates

Published market sizes for bone cement can look far apart because underlying boundaries and timing choices are rarely identical, even when the market name appears the same. Common drivers include what is counted as bone cement versus adjacent materials, how antibiotic-loaded products are treated, and whether values are captured at manufacturer level or further down the channel.

Refresh cadence and currency timing also matter, because procedure volumes and ASPs move differently across regions, and a model can drift if FX and price assumptions are not rechecked close to publication. By keeping the estimate tied to recently validated procedure trends and updating FX conversion points and ASP ladders during the final review, Mordor Intelligence reduces swings that can appear in older snapshots or in figures that blend bone cement with casting materials.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.23 B (2026) | |

| Industry Research Publisher A | USD 2.00 B (2024) | Uses an orthopedic bone cement framing with broader inclusion and limited visibility on how casting materials, glues, or adjacent biomaterials are excluded, and the base year is earlier, which can compound FX and price drift. |

| Industry Research Publisher B | USD 0.72 B (2024) | This figure is closer to an orthopedic bone cement and casting materials subset, which can undercount spine-focused demand and non-casting usage, and it appears to apply a narrower product scope than a full bone cement definition. |

The spread across the three values is mostly explained by what gets bundled into the category and how recently pricing and currency conversions were refreshed. When procedure-linked volumes, realistic cement-per-case factors, and transparent ASP steps are kept consistent, the final number becomes easier to trace and to update as new clinical and economic signals appear.

Key Questions Answered in the Report

What is the current size of the bone cement market?

The bone cement market size reached USD 1.23 billion in 2026 and is projected to hit USD 1.61 billion by 2031.

Which product type dominates the bone cement market?

PMMA cement led in 2025 with a 72.10% share, reflecting longstanding clinical trust and wide distribution.

Why are high-viscosity cements growing quickly?

High-viscosity formulations reduce leakage rates to 15%, improving safety in spine procedures and driving a forecast 6.88% CAGR.

Which region is expanding fastest?

Asia-Pacific is expected to grow at a 6.95% CAGR through 2031, supported by booming procedure volumes and rising healthcare access.

How does the shift to ambulatory surgical centers affect demand?

ASCs favor fast-setting, high-viscosity cements that enable same-day discharge, supporting a 7.02% CAGR in this channel.

What key restraint could limit bone cement adoption?

Growing preference for cementless implants among younger patients may shrink the addressable market over the long term.

Page last updated on: