Global Surgical Clips Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

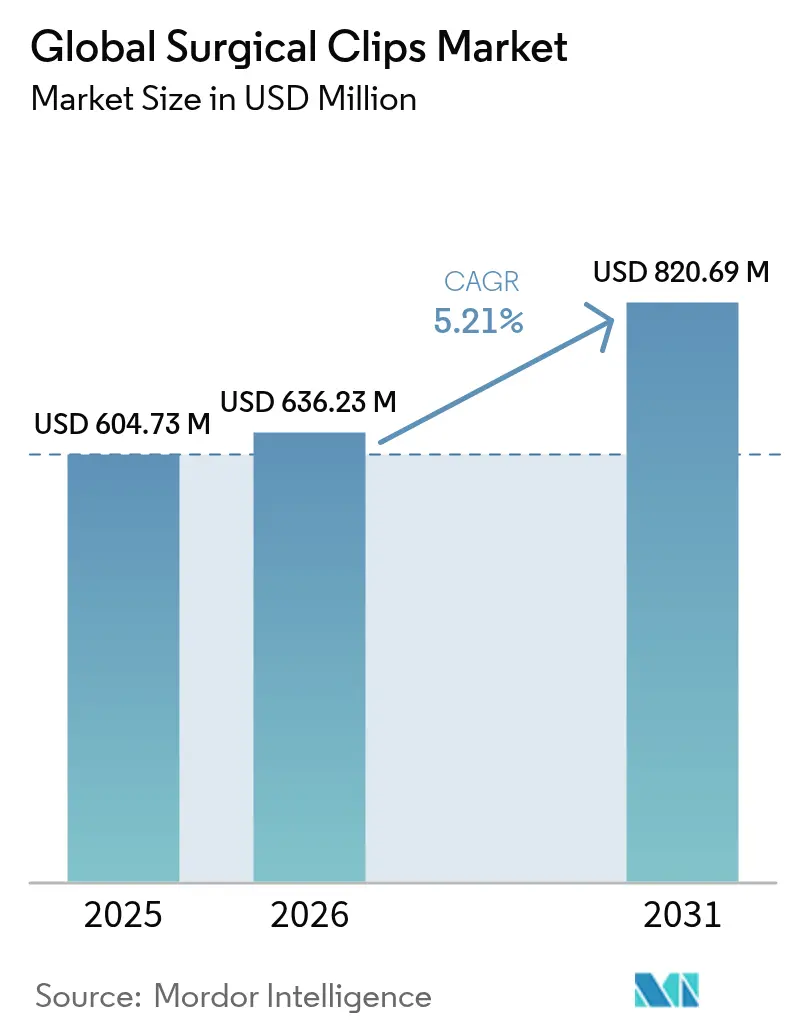

| Market Size (2026) | USD 636.23 Million |

| Market Size (2031) | USD 820.69 Million |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Surgical Clips Market Analysis by Mordor Intelligence

The surgical clips market size is expected to grow from USD 604.73 million in 2025 to USD 636.23 million in 2026 and is forecast to reach USD 820.69 million by 2031 at 5.21% CAGR over 2026-2031. Sustained growth comes from the global rise in minimally invasive procedures, the steady shift toward ambulatory settings, and continuing innovation in clip materials and applicators. Aging demographics enlarge the eligible patient pool, while higher body-mass index profiles and broader antithrombotic use raise the need for dependable hemostasis solutions. Hospitals in developed economies are upgrading to MRI-compatible polymer options, whereas emerging markets prioritize cost-efficient titanium sets. Makers that combine automated delivery with advanced imaging compatibility hold competitive advantages as health systems link device choice to quality and readmission metrics.

Key Report Takeaways

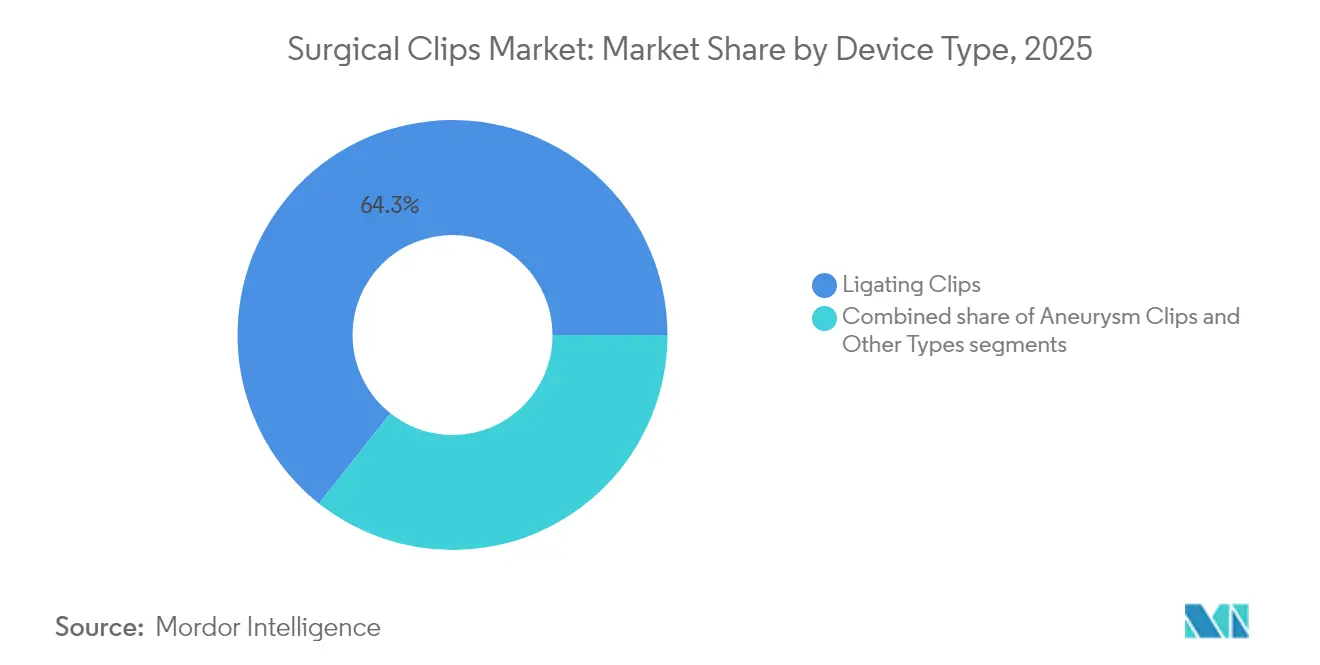

- By device type, ligating clips led with 64.33% of the surgical clips market share in 2025, while aneurysm clips are projected to grow at a 5.88% CAGR through 2031.

- By material, titanium commanded 67.55% share of the surgical clips market size in 2025; polymer variants are expanding at a 5.54% CAGR to 2031.

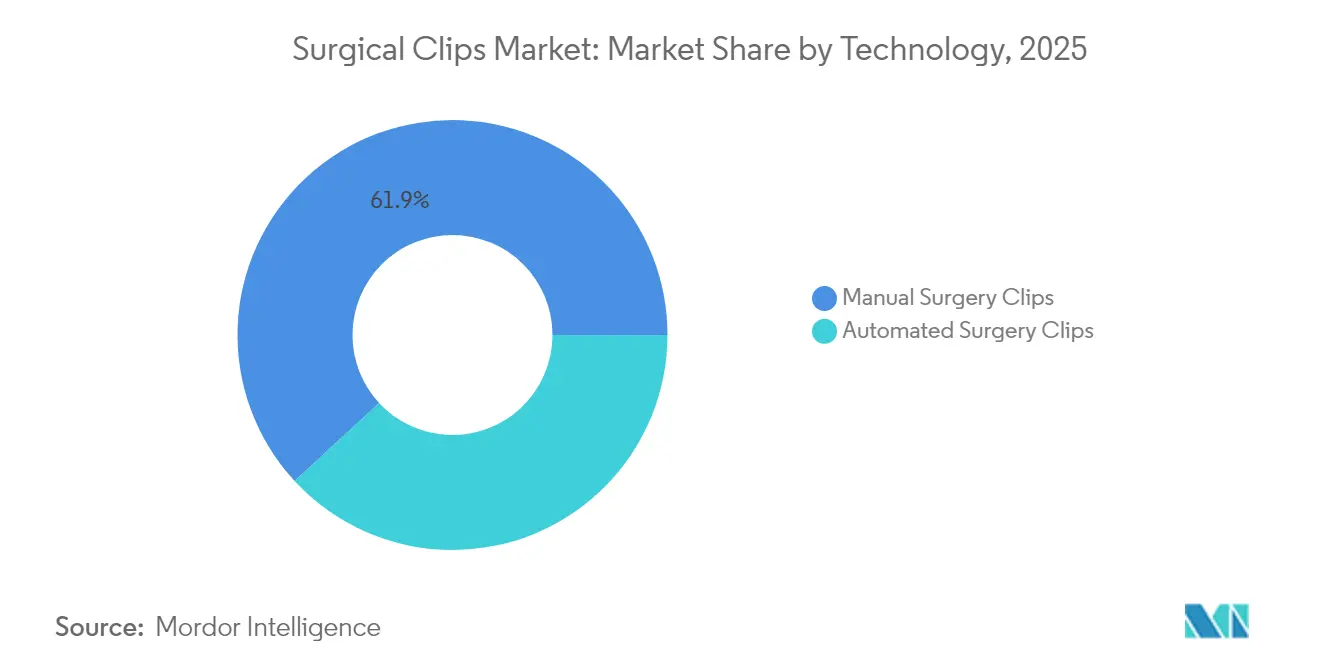

- By technology, manual products held 61.88% revenue share in 2025; automated systems to record the fastest pace at 6.15% CAGR to 2031.

- By end-user, hospitals controlled 55.96% of the surgical clips market share in 2025, whereas ambulatory surgery centers are expanding at a 5.82% CAGR through 2031.

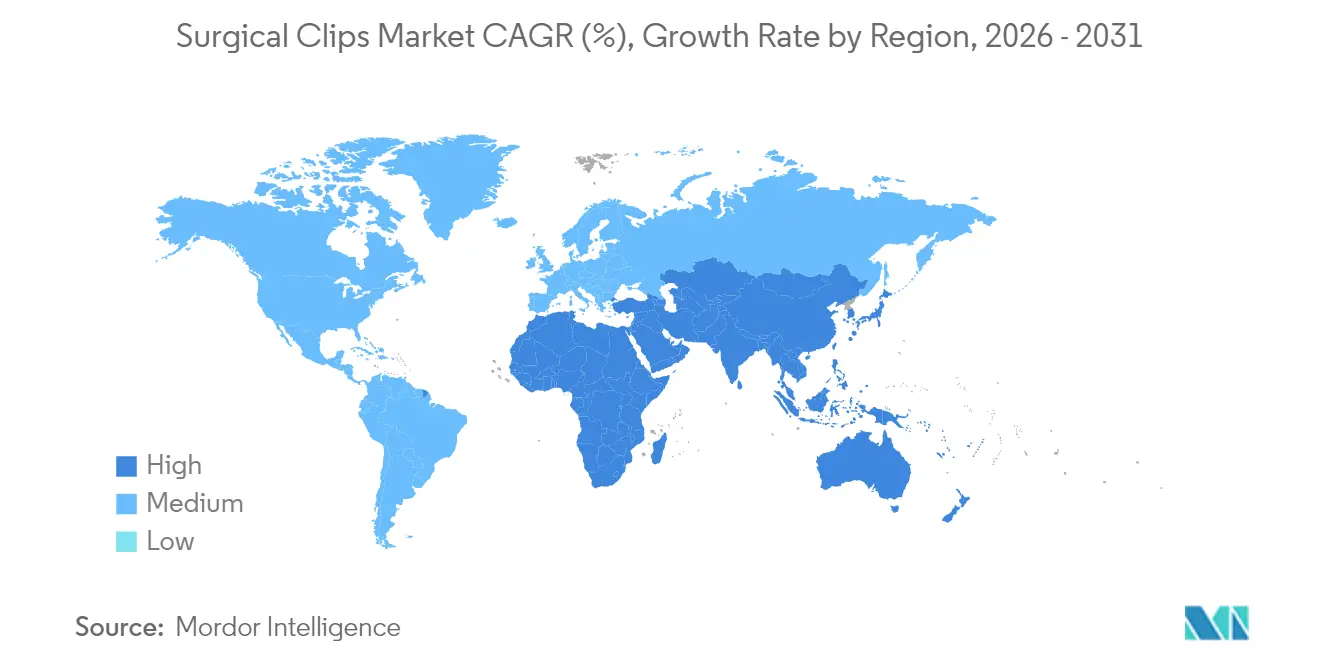

- By geography, North America captured 41.21% of the surgical clips market size in 2025; Asia-Pacific is advancing at a 5.98% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Clips Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in surgical procedures worldwide | +1.2% | Global, with higher impact in North America & Asia-Pacific | Medium term (2-4 years) |

| Surge in global geriatric population | +0.9% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Rising healthcare expenditure & access to MIS | +0.8% | North America & EU primary, APAC emerging | Medium term (2-4 years) |

| Shift toward MRI-compatible polymer/absorbable clips | +0.6% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Regulatory push for single-use sterile ligation devices | +0.4% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Proliferation of hybrid operating rooms | +0.3% | North America & EU core, selective APAC adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increase in surgical procedures worldwide

Steady growth in hernia, orthopedic, and bariatric interventions lifts procedural volume and directly drives the surgical clips market. Hernia repairs alone are expected to rise 19.7% by 2050 to 1.72 million new cases[1]Dai, F. “Spatiotemporal trends in hernia disease burden and health workforce correlations in aging populations: a global analysis with projections to 2050,” BMC Gastroenterol, bmcgastroenterol.biomedcentral.com every year. Ambulatory settings report double-digit gains in hip and knee work that depend on quick, reliable vessel ligation. Robotics adoption reinforces demand as the da Vinci 5 platform applies 43% less tissue force, allowing finer clip placement for fragile structures. Growing BMI profiles and wider antithrombotic therapy amplify the need for sturdy yet atraumatic devices across specialties. The combined effect channels recurring unit sales and encourages broader clip portfolios.

Surge in global geriatric population

Median surgical age moved from 55.5 years in 2008 to 58.5 years in 2020 and is on track for 61.5 years by 2030. Older candidates present comorbid diabetes and vascular fragility that heighten bleeding risk, making secure clipping essential. Titanium remains a staple, yet polymer lines gain acceptance because they avoid metal allergies and reduce postoperative imaging artifacts. Providers also adopt applicators with low-profile jaws that suit calcified or delicate tissue common in older adults. As payers tie reimbursement to complication rates, dependable clip performance in geriatric cohorts becomes a purchasing priority and sustains momentum for the surgical clips market.

Rising healthcare expenditure and access to MIS

The United States expects surgical spending to swell from 4.6% to 7.3% of GDP by 2025. Similar trends in Western Europe and affluent Asian economies create budget room for premium devices, including automated or MRI-friendly clips. Concurrently, Asia-Pacific medical-tech outlays could touch USD 140 billion by 2025, deepening the installed base of laparoscopic towers and raising clip usage. Value-based procurement encourages products that shorten theater time or minimize readmissions, further cementing the role of the surgical clips market in modern MIS ecosystems.

Shift toward MRI-compatible polymer or absorbable clips

Conventional titanium devices can leave 5.7 × 8.5 mm² to 17.7 × 20.7 mm² artifacts on MRI scans[2]Kremser, C., “Quantification of breast biopsy clip marker artifact on routine breast MRI sequences: a phantom study,” Eur Radiol Exp, link.springer.com, limiting postoperative assessment. Polymer and biodegradable alloys solve this problem and can even cut per-case cost by USD 75 without sacrificing clinical outcomes. Recent FDA quality-system amendments, effective February 2026, accent device lifecycle management, giving early movers in polymer or magnesium blends a regulatory edge. As imaging pathways standardize around MRI follow-up, hospitals swap legacy metal stock for polymer lines, thereby enlarging the surgical clips market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clip migration & bile-duct/vascular complications | -0.8% | Global, higher impact in regions with high laparoscopic surgery adoption | Short term (≤ 2 years) |

| Adoption of robotic staplers & energy sealing devices | -0.6% | North America & EU primary, expanding to APAC | Medium term (2-4 years) |

| Adoption of robotic staplers & energy sealing devices | -0.6% | North America & EU primary, expanding to APAC | Medium term (2-4 years) |

| Titanium allergy & slippage safety alerts (ECRI) | -0.5% | Global, concentrated in developed markets with advanced reporting | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Clip migration and bile-duct or vascular complications

More than 100 documented cases link delayed cholecystectomy clip migration to serious biliary events that sometimes surface decades after surgery. Hem-o-lok polymer variants and legacy metals alike appear in reports, signaling a design-agnostic risk. Average migration occurs 26 months post-procedure, leading to costly ERCP retrievals and feeding both surgeon caution and regulatory vigilance. Awareness forces clinicians to limit clip counts, explore alternative sealants, and demand better applicator precision, temporarily tempering growth in the surgical clips market.

Adoption of robotic staplers and energy sealing devices

Advanced vessel sealers such as ENSEAL X1 and LigaSure Maryland XP unite cutting with hemostasis, trimming the need for separate clips in complex work. Robotic platforms deliver targeted energy that minimizes leakage and standardizes outcomes, nudging procedural preference away from standalone clips. Capital costs and training hurdles keep adoption uneven, yet the trend is clear across high-volume centers. As integrated systems mature, they could erode manual clip volumes, capping growth in segments of the surgical clips market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Aneurysm Clips Drive Innovation Despite Ligating Dominance

Ligating devices generated the largest contribution to the surgical clips market in 2025, reflecting their 64.33% share in routine laparoscopic and open work. Unit demand remains high for cholecystectomy, colorectal, and general abdominal procedures that rely on quick vessel closure. Uptake persists in lower-resource settings, ensuring stable baseline volumes and reinforcing market resilience.

Aneurysm clips, although smaller in revenue today, grow fastest at 5.88% CAGR as neurovascular caseloads climb with an aging population. Silicon-nitride and zirconia ceramics demonstrate superior closing force without jaw crossing, giving neurosurgeons MRI-safe options for complex locations. Manufacturers bundle these clips with micro-applicators that fit narrow surgical windows, creating premium niches inside the wider surgical clips market. Continuous R&D into jaw geometry and spring metallurgy improves long-term patency and supports broader adoption.

By Material: Polymer Clips Gain Ground on Titanium Dominance

Titanium held 67.55% of segment revenue in 2025 thanks to decades of clinical proof and surgeon familiarity. Its strength-to-weight ratio and inert surface limit tissue reaction, providing dependable performance for diverse procedures. Hospitals continue large-scale buying due to streamlined sterilization and bulk pricing arrangements.

Polymer lines register 5.54% CAGR through 2031 as clinicians pursue MRI clarity and avoid metal allergies. Studies record USD 75 savings per case when switching from metal to polymer clips while maintaining comparable complication profiles. Biodegradable magnesium-titanium hybrids emerge in research pipelines and could remove post-healing foreign bodies altogether. As imaging protocols tighten and patient allergy testing rises, polymer and hybrid shares will likely advance, diversifying the surgical clips market.

By Technology: Automation Advances Challenge Manual Clip Dominance

Manual applicators gathered 61.88% of 2025 revenue as their simple mechanics and low cost favor routine settings. Surgeons value tactile feedback and minimal setup, keeping manual demand robust in community hospitals and emerging markets.

Automated platforms, however, expand at 6.15% CAGR. Systems like Resolution 360 offer 1-to-1 rotation and reduce closure time by nearly five minutes in endoscopic bleeding control, translating into faster room turnover. When paired with robotic arms, automation assures uniform clip pressure and placement even for novice users. Cost and learning curves slow uptake but centers that prioritize reproducibility adopt automated clips, lifting high-value brackets of the surgical clips market.

By End-User: ASCs Challenge Hospital Dominance Through Efficiency

Hospitals captured 55.96% of global sales in 2025 by handling trauma, multi-organ transplants, and other intricate cases requiring a wide clip inventory. Their purchasing decisions weigh supply chain reliability and multifunctional kits to standardize care pathways.

Ambulatory surgery centers grow at a 5.82% pace as payers push elective work to cost-effective outpatient venues. ASCs favor compact clip assortments that align with standardized MIS protocols, driving volume contracts for basic titanium or polymer sets. The efficient workflow and shorter patient stay expand day-surgery capacity, adding fresh nodes in the surgical clips market.

Geography Analysis

North America accounted for 41.21% of the surgical clips market share in 2025, sustained by high procedure counts, broad insurance coverage, and rapid adoption of MRI-compatible lines. Surgical spending is set to hit 7.3% of GDP by 2025, supporting premium procurement and keeping the surgical clips market vibrant in the region. FDA quality-system reforms, effective in 2026, further encourage manufacturers to invest in advanced materials.

Asia-Pacific is the fastest-expanding region for the surgical clips market, with a 5.98% CAGR. Rising incomes and health-insurance penetration in China, India, and Southeast Asia push higher elective surgery counts. Domestic makers supply cost-advantaged titanium options, while high-tier urban centers import polymer and automated systems. Government investments in surgical robotics and hospital infrastructure strengthen regional demand through the forecast period.

Europe posts a 4.91% CAGR on the back of aging demographics and rigorous device oversight. Hospitals in Germany, France, and the Nordics value traceability and imaging safety, helping polymer and biodegradable lines gain traction. Group purchasing across national systems steers consistent adoption, while local innovators refine ceramic aneurysm clips that meet stringent MRI guidelines. The Middle East and Africa grow 5.73% as Gulf states channel oil revenue into state-of-the-art surgical suites that prefer premium polymer sets. Emerging sub-Saharan markets focus on affordable manual titanium solutions yet still post rising volumes thanks to expanding urban hospitals. South America advances 5.37% under Brazil and Argentina’s public-private partnerships that enhance access to MIS.

Competitive Landscape

The surgical clips market shows moderate fragmentation. Top multinationals such as Johnson & Johnson’s Ethicon line, Medtronic, and Boston Scientific compete with niche innovators focusing on MRI-safe or biodegradable devices. Ethicon’s PROXIMATE linear cutters demonstrate 34% higher mean leak pressure than rival staplers, indirectly promoting its clip portfolio for adjunct closure tasks. Boston Scientific’s Resolution family reduces closure time by 4 minutes 45 seconds, appealing to endoscopy suites seeking throughput gains.

Medtronic leverages its LigaSure Maryland XP vessel sealer to blend clip functions with energy delivery, creating cross-selling opportunities. In March 2025, Olympus entered gastrointestinal hemostasis with the Retentia HemoClip, extending its presence beyond visualization into clipping consumables. Regional players in China and India produce titanium lines at attractive prices, supplying domestic hospitals and challenging importers in budget segments.

Strategic focus centers on materials R&D, automation, and bundled solutions. Companies pursue patents covering spring mechanisms, jaw geometry, and bioresorbable alloys. Partnerships with robotics firms ensure clip compatibility with next-generation consoles, while digital traceability features align with post-market surveillance rules. These moves keep competition dynamic and propel technological progress within the surgical clips market.

Global Surgical Clips Industry Leaders

B. Braun Melsungen AG

Boston Scientific Corporation

Grena Limited

Johnson & Johnson Services, Inc.

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Olympus introduced the Retentia HemoClip for endoscopic GI bleeding management Medical Device Network.

- February 2025: Teleflex announced a corporate split into two listed entities, with RemainCo concentrating on surgical and vascular devices Teleflex.

- February 2025: Teleflex agreed to buy BIOTRONIK’s Vascular Intervention business for EUR 760 million to strengthen its interventional suite Teleflex.

- November 2023: Medtronic launched the Penditure LAA Exclusion System, an implantable clip for left atrial appendage management in concurrent cardiac surgery.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we view the surgical clips market as the worldwide revenue derived from titanium, polymer, or alloy clips, plus their hand-held or powered applicators, that surgeons deploy inside the body to ligate vessels, ducts, or tissues across open, laparoscopic, and robot-assisted procedures. Values are reported in USD, capturing new unit sales and associated applicators across 17 major country groups.

Scope Exclusion: External skin-closure clips, endoscopic staplers, and energy-based sealing devices are kept outside this study's boundary.

Segmentation Overview

- By Device Type

- Ligating Clips

- Aneurysm Clips

- Other Types

- By Material

- Titanium

- Polymer

- Other Materials

- By Technology

- Automated Surgery Clips

- Manual Surgery Clips

- By End-User

- Hospitals

- Ambulatory Surgery Centers

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

To validate secondary findings, Mordor Intelligence engages cardiovascular and general surgeons, procurement heads at hospitals, and regional device distributors in North America, Europe, Asia-Pacific, and Latin America. Their feedback confirms clip-to-procedure ratios, average selling prices, adoption of absorbable polymers, and foreseeable reimbursement shifts, which together tighten model assumptions.

Desk Research

Our analysts first collect foundational signals from public datasets such as the WHO Hospital Procedure Database, OECD Health Statistics, UN World Population Prospects, and the FDA MAUDE adverse-event files, which reveal usage volume shifts and safety alerts. Industry associations like the Society of American Gastrointestinal and Endoscopic Surgeons and the European Association for Cardio-Thoracic Surgery supply guideline updates and procedure mix splits that refine demand pools. Company 10-Ks, device registrations in EUDAMED, customs trade codes for HS 901890, and reputable press coverage add pricing clues and competitive moves.

Subscription tools, including D&B Hoovers for manufacturer revenues and Dow Jones Factiva for deal tracking, complement the open sources. The list is illustrative; many additional references were consulted for cross-checks and clarification.

Market-Sizing & Forecasting

A top-down construct starts with national surgical procedure counts and specialty splits, then applies clip utilization coefficients and weighted ASPs to rebuild annual spend. Select bottom-up checks, notably sampled supplier revenues and channel inventory audits, are used to fine-tune totals. Key variables inside the model include elective surgery backlog clearance rates, growth in minimally invasive surgery penetration, geriatric population expansion, average clip sets per cholecystectomy, and raw-material cost trends that influence pricing. We forecast through 2030 with multivariate regression on those drivers, stress-tested by scenario inputs gathered from our expert panel. Data gaps in supplier roll-ups are bridged by regional med-tech import trends and hospital capital-budget disclosures.

Data Validation & Update Cycle

Outputs pass a three-layer review that checks variance against external procedure series, flags outliers, and prompts analyst re-contact where deviations exceed preset bands. Reports refresh each year and are mid-cycle updated when recalls, major M&A, or regulation changes materially shift the baseline.

Why Our Surgical Clips Baseline Commands Reliability

Published estimates often diverge because firms apply different product mixes, inflation conversions, or refresh cadences. Our disciplined scope selection and annual refresh rhythm reduce those distortions.

Key gap drivers include some publishers bundling staplers and energy sealers, others applying aggressive compound inflation on 2023 prices, and a few extrapolating pre-pandemic procedure growth without backlog adjustments.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 604.73 Mn (2025) | Mordor Intelligence | - |

| USD 865.9 Mn (2024) | Global Consultancy A | Includes staplers and considers global ASP uplift of 8 % p.a. without procedure cap |

| USD 715 Mn (2024) | Trade Journal B | Counts external skin clips and applies single regional price to all geographies |

| USD 406.71 Mn (2023) | Industry Association C | Uses company revenue sampling that omits polymer-only newcomers and adjusts no channel margins |

These comparisons show that Mordor's consistent product scope, mixed-source price stack, and procedure-anchored demand math deliver a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

Why are hospitals switching from titanium to polymer surgical clips?

Hospitals seek to eliminate MRI imaging artifacts and reduce the small risk of metal allergies, prompting a shift toward polymer options that provide clearer postoperative scans and broader patient tolerance.

How are ambulatory surgery centers influencing procurement strategies for surgical clips?

ASCs favor standardized clip sets that streamline workflow and lower per-procedure costs, pressuring suppliers to offer bundled, easy-to-load systems rather than large, diverse inventories.

What role does robotic surgery play in the adoption of automated clip applicators?

Robotic platforms demand precision and consistency, so surgeons increasingly pair them with automated applicators that ensure uniform compression and accurate placement in confined anatomical spaces.

Which safety concern is most frequently cited by surgeons when selecting clip technology?

Clip migration—particularly in biliary and vascular procedures—remains the dominant worry, driving interest in improved jaw designs and alternative sealing methods that minimize displacement risk.

How is the aging population reshaping design priorities for surgical clips?

Older patients’ fragile tissues require clips with gentler closure forces and enhanced biocompatibility, encouraging manufacturers to develop lighter materials and applicators tuned for delicate handling.

What impact do evolving regulatory standards have on material innovation in surgical clips?

Emerging rules emphasize device lifecycle management and traceability, accelerating research into biodegradable alloys and polymer formulations that can simplify long-term patient monitoring and safety reporting.

Page last updated on: