Stock Images Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

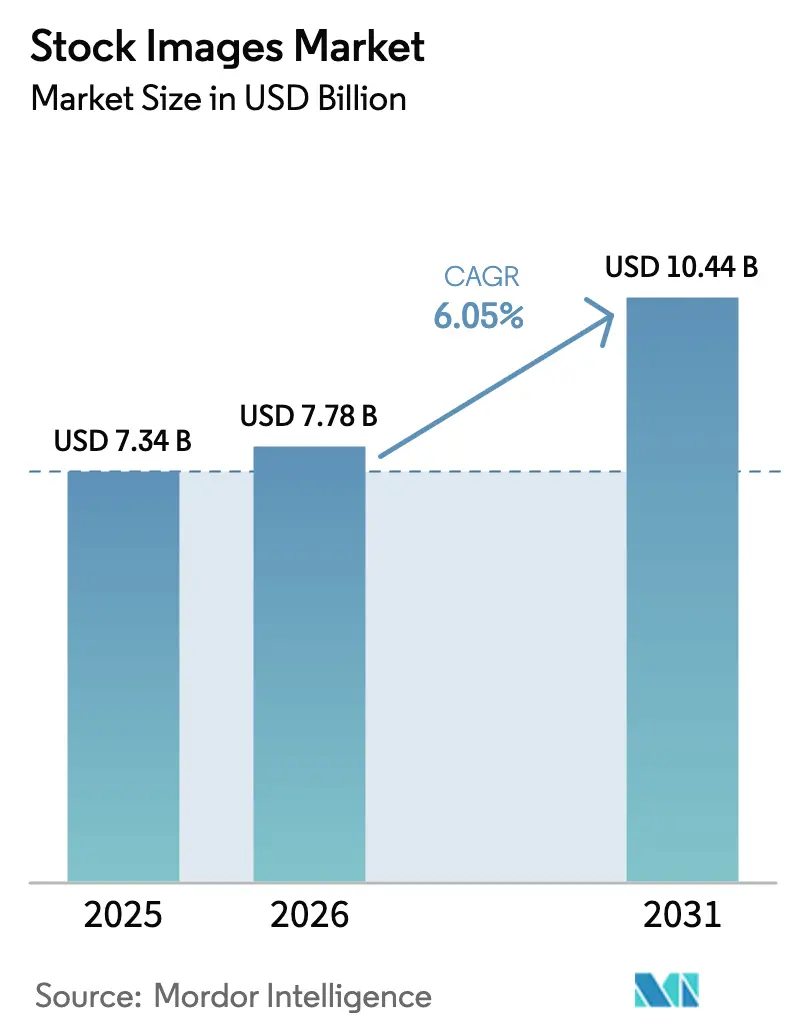

| Market Size (2026) | USD 7.78 Billion |

| Market Size (2031) | USD 10.44 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

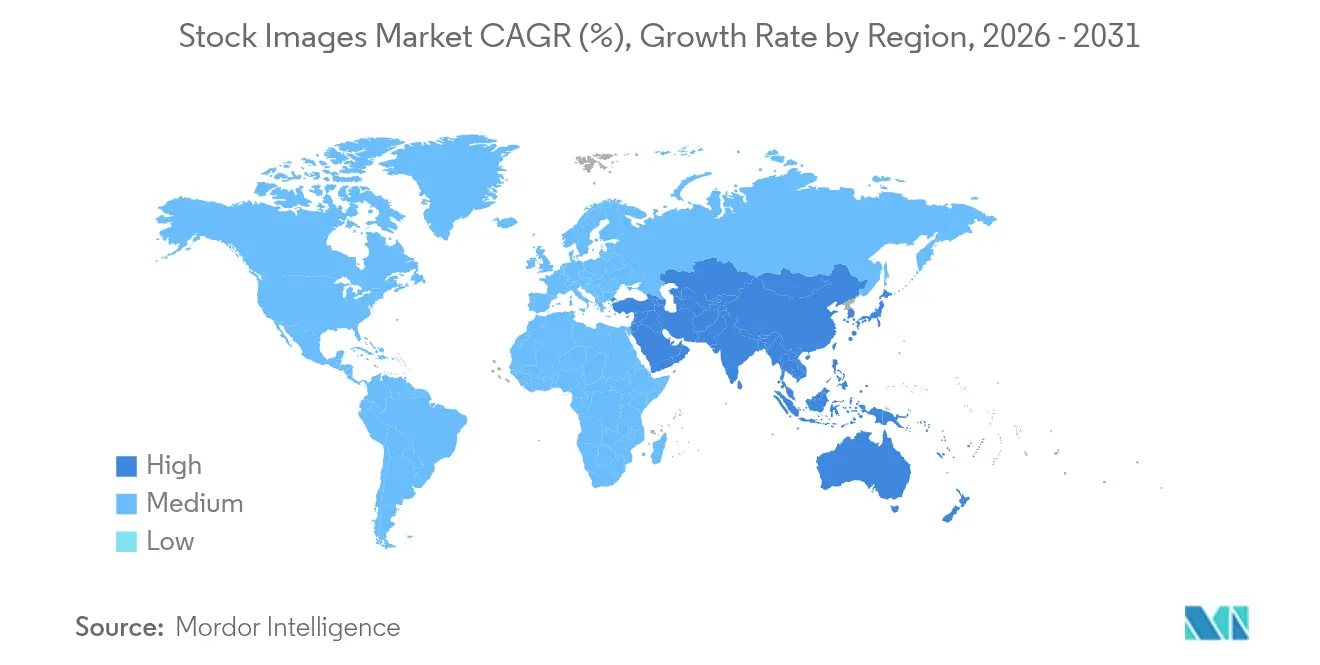

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stock Images Market Analysis by Mordor Intelligence

stock images market size in 2026 is estimated at USD 7.78 billion, growing from 2025 value of USD 7.34 billion with 2031 projections showing USD 10.44 billion, growing at 6.05% CAGR over 2026-2031. Robust demand for legally cleared visual assets, the rise of generative AI training deals and the migration toward subscription pricing all support the current growth trajectory of the stock images market. North America continues to anchor overall revenue on the back of sophisticated advertising spend, while Asia-Pacific’s e-commerce surge positions the region as the fastest-growing contributor to the stock images market. Competitive behaviour is evolving: market leaders such as Getty Images and Shutterstock now monetise AI partnerships instead of contesting them, and AI-native entrants like Freepik are reshaping the industry cost curve. [1]Tech.eu, “Europe's Quiet AI Giant Freepik is Moving Fast — and Taking Market Share,” tech.eu Meanwhile, the pending USD 3.7 billion Getty-Shutterstock merger signals a larger consolidation wave aimed at buffering pricing pressure and sharing development costs.

Key Report Takeaways

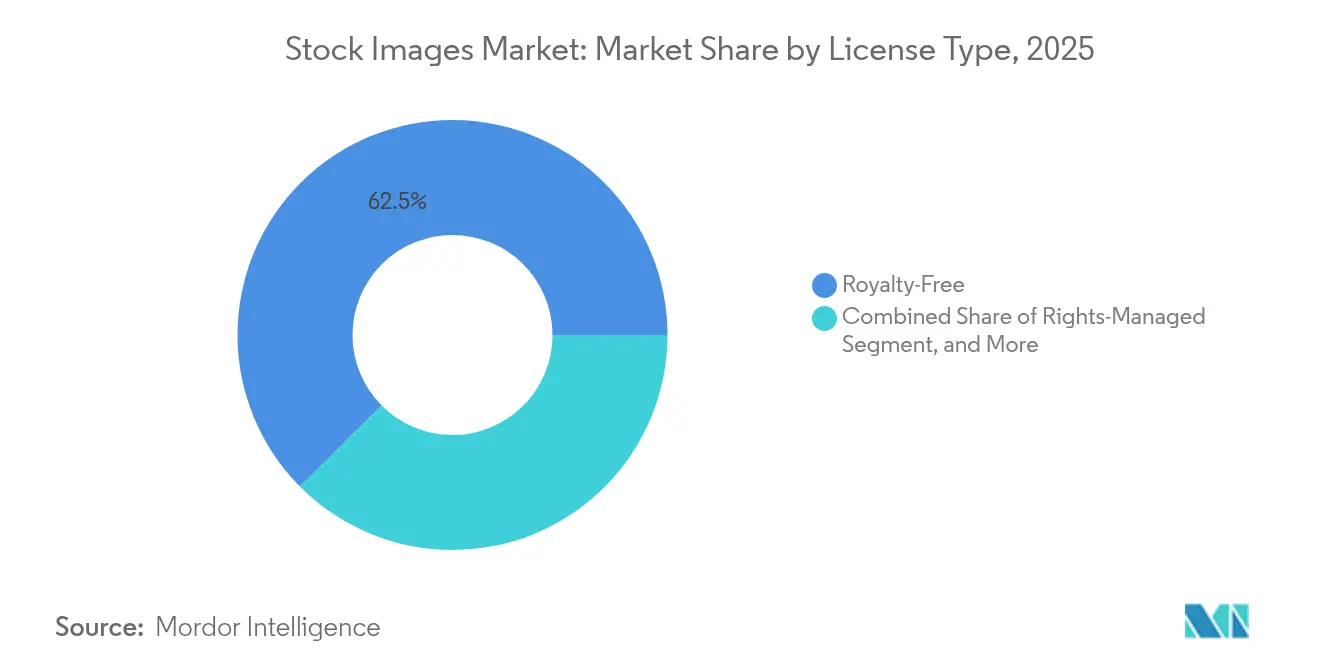

- By license type, royalty-free held 62.45% of stock images market share in 2025, while subscriptions are projected to expand at a 7.2% CAGR through 2031.

- By content format, still images led with 77.3% of the stock images market size in 2025; stock footage/video is advancing at an 7.75% CAGR to 2031.

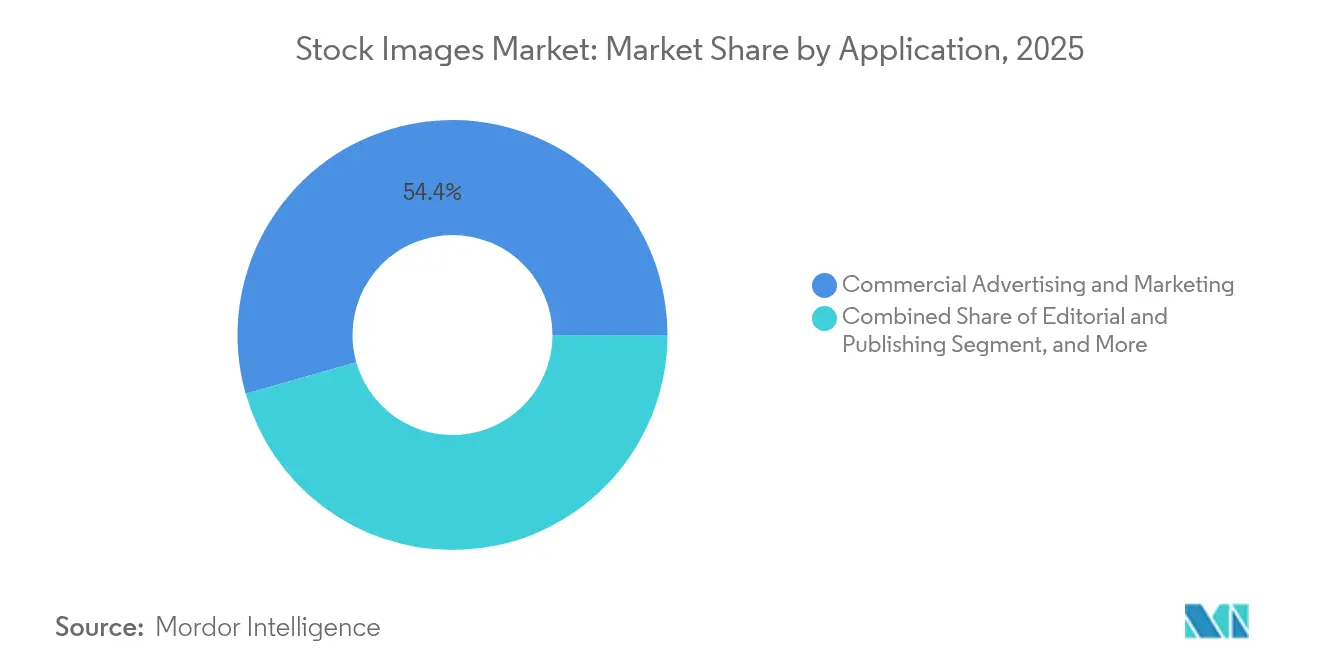

- By application, commercial advertising commanded 54.4% share of the stock images market size in 2025 and e-commerce imagery is forecast to grow at 7.45% CAGR.

- By end-user, media and publishing houses controlled 30.6% of stock images market share in 2025, whereas SMB adoption is rising fastest at a 7.55% CAGR.

- By geography, North America contributed 37.9% of revenue in 2025; Asia-Pacific is set to climb at an 7.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Stock Images Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of AI-training image demand | +1.20% | North America, spillover to EU | Medium term (2-4 years) |

| Rising DTC e-commerce visual spend | +0.90% | Asia-Pacific core, emerging markets | Long term (≥ 4 years) |

| Growth of creator-economy subscriptions | +0.70% | Europe and South America | Medium term (2-4 years) |

| OTT streaming campaign explosion | +0.50% | Middle East and Africa | Short term (≤ 2 years) |

| ESG storytelling needs | +0.30% | Nordic countries, broader Europe | Long term (≥ 4 years) |

| Regulatory crack-down on deepfakes | +0.40% | US and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of AI-training image demand in North America

Licensing complete, indemnified libraries for AI model development has unlocked a revenue pool that outstrips per-image sales economics. Shutterstock secured USD 138 million in AI data deals in 2024, validating the strategic value of long-tail archives to technology firms. Although these contracts lift near-term cash flow, they also offer the raw material for AI systems that could one day substitute routine imagery, forcing every participant in the stock images market to hedge between present opportunity and future risk.

Rising DTC e-commerce visual spend in Asia-Pacific

Direct-to-consumer sellers increasingly link conversion rates to differentiated imagery, prompting a shift from sporadic purchases to all-you-can-download subscriptions. Lifestyle, cultural and mobile-first aesthetics dominate briefs, creating a sustained pipeline of demand that reinforces Asia-Pacific’s 8% CAGR leadership within the stock images market.

Growth of creator-economy subscriptions in Europe and South America

Small creators require predictable, affordable access rather than large upfront fees. Subscription plans address that gap, expanding the paid user base by lowering the entry barrier and anchoring monthly recurring revenue. However, the same user segment gravitates toward free UGC alternatives, intensifying price competition across the stock images market.

OTT streaming campaign explosion in Middle East and Africa

Regional streaming platforms race to localise promotional assets, driving a spike in culturally attuned imagery needs. The rapid cycle of series premieres means short lead times favour agencies and libraries that already maintain deep local coverage. This demand foregrounds a significant incremental layer of growth within the wider stock images market even though it remains episodic.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Free UGC platforms eroding ASPs | -0.80% | Asia-Pacific SMB sector | Short term (≤ 2 years) |

| Generative-AI cannibalisation of routine imagery | -1.10% | Europe first, global reach | Medium term (2-4 years) |

| Multi-territory copyright litigation risk | -0.40% | US broadcast, global implications | Long term (≥ 4 years) |

| Authenticity backlash vs generic imagery | -0.30% | Latin America, expanding | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Free UGC platforms eroding ASPs in Asia-Pacific SMB sector

Cost-sensitive businesses are migrating toward free repositories, compressing average transaction values by directing demand away from traditional royalty-free libraries. [2]Stanford Report, “When AI-generated art enters the market, consumers win – and artists lose,” news.stanford.edu Lower unit economics force suppliers in the stock images market to recalibrate package sizes, reposition premium tiers or embrace higher-value custom projects.

Generative-AI cannibalisation of routine web imagery

When AI systems produce acceptable visuals on demand, baseline creative tasks commoditise. European buyers have been early adopters, spurred by structured regulation and a preference for secure, compliant workflows. This cannibalisation squeezes margins on low-complexity content, leaving the stock images market reliant on authenticity, specialised niches and legal indemnification to defend value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By License Type: Subscriptions Challenge Royalty-Free Dominance

Royalty-free agreements retained 62.45% of stock images market share in 2025, reflecting their broad usage rights that fit multichannel marketing workflows. Yet subscriptions, growing at 7.2% CAGR, are reshaping purchasing norms. SMBs and creator-economy players value unlimited downloads within defined caps, creating a reliable stream of recurring income for vendors. That pivot toward predictability spreads acquisition costs over time, mitigating the volatility that once characterised royalty-free demand. Rights-managed licences still serve high-stakes editorial campaigns but are steadily ceding ground to hybrid packages that blend exclusivity with AI-enabled generation inside the same interface.

The stock images market now rewards platforms that integrate indemnified generative AI modules under subscription umbrellas, as evidenced by Getty’s partnership with Nvidia to launch Generative AI by iStock. Such configurations future-proof catalogues while reinforcing legal confidence, a vital differentiator against non-licensed AI outputs. For creators, subscriptions offer larger predictable payouts through usage-based allocation methods, slightly offsetting the income decline tied to royalty-free’s plateauing volumes.

By Content Format: Video Growth Outpaces Still Images

Still imagery accounted for 77.3% of the stock images market size in 2025, maintaining primacy across print, web and social formats. Nevertheless, stock footage and short-form video are accelerating at an 7.75% CAGR as algorithmic feeds and OTT services prioritise motion. Video clips fetch higher unit prices because production expenses and technical know-how remain relatively steep, granting suppliers temporary protection from deep commoditisation. Illustrations and vectors continue to serve UX design and data storytelling, yet integration inside AI-first design suites is squeezing standalone demand.

Markets now perceive 3D renders and AI-generated composites as adjacent layers rather than separate verticals. Deloitte highlights an emerging workflow where AI produces an initial storyboard, which then gets refined by human editors before final export. This iterative loop enlarges the addressable base for platforms that can service still, video and mixed-media demands from a single dashboard, thereby reinforcing their position within the stock images market.

By Application: E-commerce Imagery Drives Growth

Commercial advertising dominated 54.4% of stock images market size in 2025, benefiting from long-standing agency relationships and large-scale media planning cycles. However, e-commerce product imagery is expanding at a 7.45% CAGR as conversion metrics prove tightly correlated with high-resolution visuals across listing pages, social ads and augmented-reality previews. Retailers require multiple angles and contextual lifestyle shots, amplifying average order values in content procurement.

Editorial publishers continue to face revenue contraction but remain high-usage customers due to news, sports and archival requirements. ESG reporting has emerged as a niche application where enterprises pay a premium for authentic depictions of environmental and social initiatives that withstand stakeholder scrutiny. Educational platforms, while volume heavy, remain cost sensitive, pulling in a blend of free and low-tier assets. Overall, the stock images market is fragmenting along value-based lines, with commodity web imagery losing share to vertical-specific packages with compliance assurances.

By End-user Industry: SMBs Accelerate Adoption

Media and publishing houses controlled 30.6% of stock images market share in 2025, supported by institutional workflows and a sustained appetite for evergreen visuals. Small and medium businesses, however, are scaling faster at a 7.55% CAGR by leveraging templates and do-it-yourself design suites embedded inside subscription libraries. These companies traditionally lacked budgets for bespoke shoots, making them receptive to predictable subscription tiers that package design tools, AI generation and stock photography under one invoice.

Advertising agencies continue to negotiate exclusive bundles for blue-chip clients, but a segment of creative work is migrating in-house at large enterprises, shrinking agency intermediation. Individual creators and influencers now constitute a recognised customer group: Freepik’s 800,000 paid subscribers underscore the power of an AI-first, affordably priced model for user-generated storytelling. Consequently, the stock images market balances enterprise-level premium packages with democratized self-service tiers, each requiring distinct pricing logic.

Geography Analysis

North America contributed 37.9% of global revenue in 2025, anchored by intensive advertising budgets, sophisticated tech ecosystems and early adoption of AI training deals that now represent a new cash-flow pillar for the stock images market. The region’s structural advantage lies in abundant venture capital for creative tooling, coupled with a mature legal framework for IP enforcement that adds a premium to vetted archives.

Asia-Pacific is projected to post an 7.7% CAGR through 2031 on the back of DTC retail expansion and mobile-first consumer behaviour, making it the fastest accelerator within the stock images market. Local sellers increasingly substitute generic Western images with culturally attuned visuals to boost authenticity, compelling global platforms to open regional curation hubs or partner with domestic creator networks.

Europe remains a stable yet innovative landscape. Strong creator-economy infrastructure supports subscription growth, while stricter AI governance frameworks push buyers toward indemnified imagery, tempering the cannibalisation risk of generative models. South America registers growing dissatisfaction with generic stock, driving adoption of culturally nuanced assets and triggering an authenticity premium. Middle East and Africa present an early-stage but high-potential quadrant: the OTT streaming boom necessitates localised advertising visuals, although supply shortfalls and bandwidth constraints still hamper rapid fulfillment. Collectively, nuanced regional requirements oblige providers to tailor product mixes, safeguarding relevance across the global stock images market.

Competitive Landscape

The stock images market is moderately concentrated as Getty Images, Shutterstock and Adobe Stock leverage vast archives, established sales channels and brand equity to retain core enterprise accounts. The announced Getty-Shutterstock merger, valued at USD 3.7 billion, would compress the leadership tier into a single heavyweight expected to capture material economies of scale and a projected USD 150-200 million in synergies. Regulatory review, however, introduces uncertainty just as generative AI upends legacy royalty revenue streams.

AI-native challengers such as Freepik scale rapidly by embedding automated design, AI art generation and freemium tiers that attract creators before up-selling to paid plans. Adjacent tech giants intensify competition: Adobe extends Firefly AI to mobile, directly integrating generation into Creative Cloud workflows, while Canva acquires AI-driven ad tooling to deepen enterprise penetration. White-space opportunities now cluster around ESG storytelling, culturally authentic regional libraries and indemnified AI data licensing, segments where nimble specialists can extract premiums less vulnerable to commoditisation.

Margin resilience increasingly hinges on legal protections, curation depth and hybrid AI+human workflows. Platforms that deliver iron-clad indemnity and culturally specific imagery command higher yields, reinforcing a bifurcation between generic free content and premium archives. As product roadmaps converge around integrated AI generation, differentiation will rely on brand trust and dataset provenance—attributes difficult for new entrants to replicate overnight but vital for sustaining leadership in the evolving stock images market.

Stock Images Industry Leaders

Dissolve Inc.

Getty Images Holdings Inc.

Shutterstock Inc.

Adobe Inc. (Adobe Stock)

Bigstock Photo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Shutterstock unveiled a new brand identity and AI-powered subscription bundles, adding unlimited downloads and data-licensing tiers.

- July 2025: Adobe expanded Firefly AI tools to mobile devices while Canva’s MagicBrief acquisition heightened competitive tension.

- June 2025: Getty Images narrowed its UK lawsuit against Stability AI to trademark claims, reshaping the legal discourse on AI training content.

- June 2025: Freepik’s AI-first platform surpassed 100 million users and 800 k paid subscribers, underscoring rapid share gains.

Global Stock Images Market Report Scope

Stock images are generic photos, illustrations and icons created without a particular project in mind. They are then licensed, usually for a fee, to individuals or organizations for use in marketing materials, websites, packaging, book covers and more.

The stock images market is segmented by type (free, paid), by application (editorial, commercial), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Royalty-Free |

| Rights-Managed |

| Subscription / Extended |

| Still Images |

| Stock Footage / Video |

| Illustrations and Vectors |

| 3D / AI-Generated Assets |

| Commercial Advertising and Marketing |

| Editorial and Publishing |

| E-commerce and Product Imagery |

| Corporate Communications and ESG Reporting |

| Education and Training |

| Media and Publishing Houses |

| Advertising / Creative Agencies |

| Large Enterprises |

| Small and Medium Businesses |

| Individual Creators and Influencers |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Mexico | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By License Type | Royalty-Free | |

| Rights-Managed | ||

| Subscription / Extended | ||

| By Content Format | Still Images | |

| Stock Footage / Video | ||

| Illustrations and Vectors | ||

| 3D / AI-Generated Assets | ||

| By Application | Commercial Advertising and Marketing | |

| Editorial and Publishing | ||

| E-commerce and Product Imagery | ||

| Corporate Communications and ESG Reporting | ||

| Education and Training | ||

| By End-user Industry | Media and Publishing Houses | |

| Advertising / Creative Agencies | ||

| Large Enterprises | ||

| Small and Medium Businesses | ||

| Individual Creators and Influencers | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Mexico | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the stock images market?

The stock images market stands at USD 7.78 billion as of 2026 and is set to reach USD 10.44 billion by 2031.

Which region grows fastest in the stock images market?

Asia-Pacific is forecast to expand at an 7.7% CAGR through 2031, outpacing all other regions.

How are AI training deals influencing revenue models?

Large archives now license datasets to AI developers, adding high-margin revenue that already lifted Shutterstock’s AI-related income to USD 138 million in 2024.

Why are subscriptions gaining traction over royalty-free purchases?

Subscriptions offer unlimited downloads, predictable monthly costs and embedded AI tools, aligning with creator economy and SMB needs.

What threat does generative AI pose to traditional stock libraries?

AI tools can generate routine imagery on demand, compressing prices for generic visuals and pushing suppliers to emphasise authenticity, indemnity and premium niches.

How will the Getty-Shutterstock merger affect competition?

If approved, the merged entity would achieve sizeable cost synergies and enlarged archives, likely intensifying antitrust oversight while reshaping supplier-buyer bargaining power.

Page last updated on: