Short Video Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

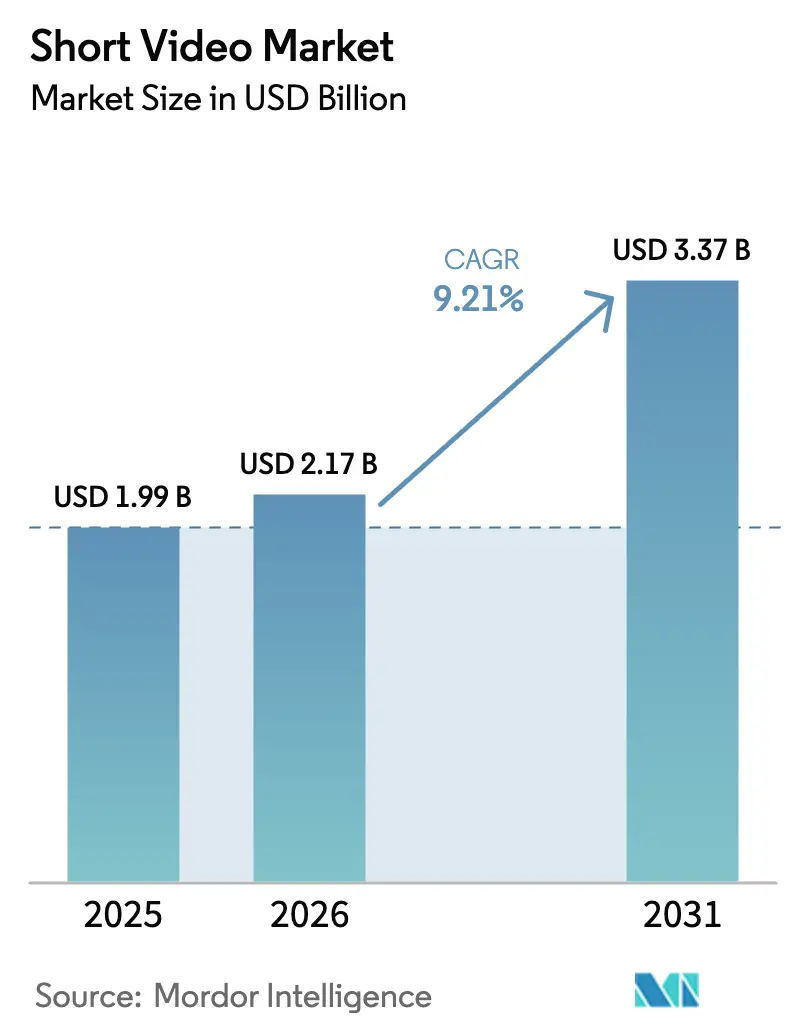

| Market Size (2026) | USD 2.17 Billion |

| Market Size (2031) | USD 3.37 Billion |

| Growth Rate (2026 - 2031) | 9.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Short Video Market Analysis by Mordor Intelligence

The short video market size was valued at USD 1.99 billion in 2025 and estimated to grow from USD 2.17 billion in 2026 to reach USD 3.37 billion by 2031, at a CAGR of 9.21% during the forecast period (2026-2031). Strong mobile-first habits, rapid 5G rollout, and the steady infusion of AI creation tools underpin this expansion. Platforms that add in-stream shopping features now convert entertainment time into purchase moments, giving advertisers new paths to measurable sales. Real-time engagement formats such as live video are rising fast, helped by low-latency 5G that keeps viewers connected during interactive sessions. Meanwhile, tougher youth-safety rules in North America and Europe raise compliance costs but also push innovation in age-appropriate recommendation engines.

Key Report Takeaways

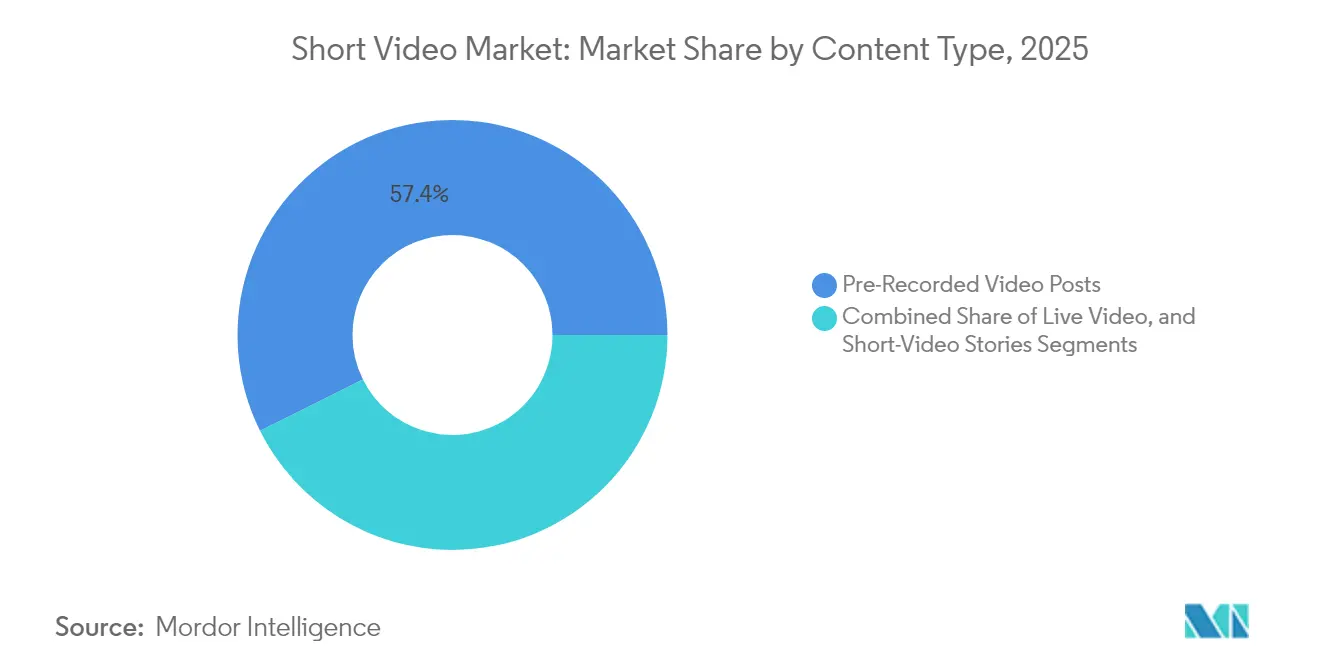

- By content type, pre-recorded clips held 57.35% of short video market share in 2025, while live video is forecast to lead growth at a 12.10% CAGR to 2031.

- By monetization model, advertising supported 75.20% revenue in 2025; in-app tipping and purchases are projected to expand at 12.90% CAGR through 2031.

- By deployment, mobile applications accounted for 90.60% of the short video market size in 2025 and are set to grow at 9.70% CAGR.

- By operating system, Android captured 66.40% revenue in 2025; iOS is expected to post the quickest rise at 11.20% CAGR.

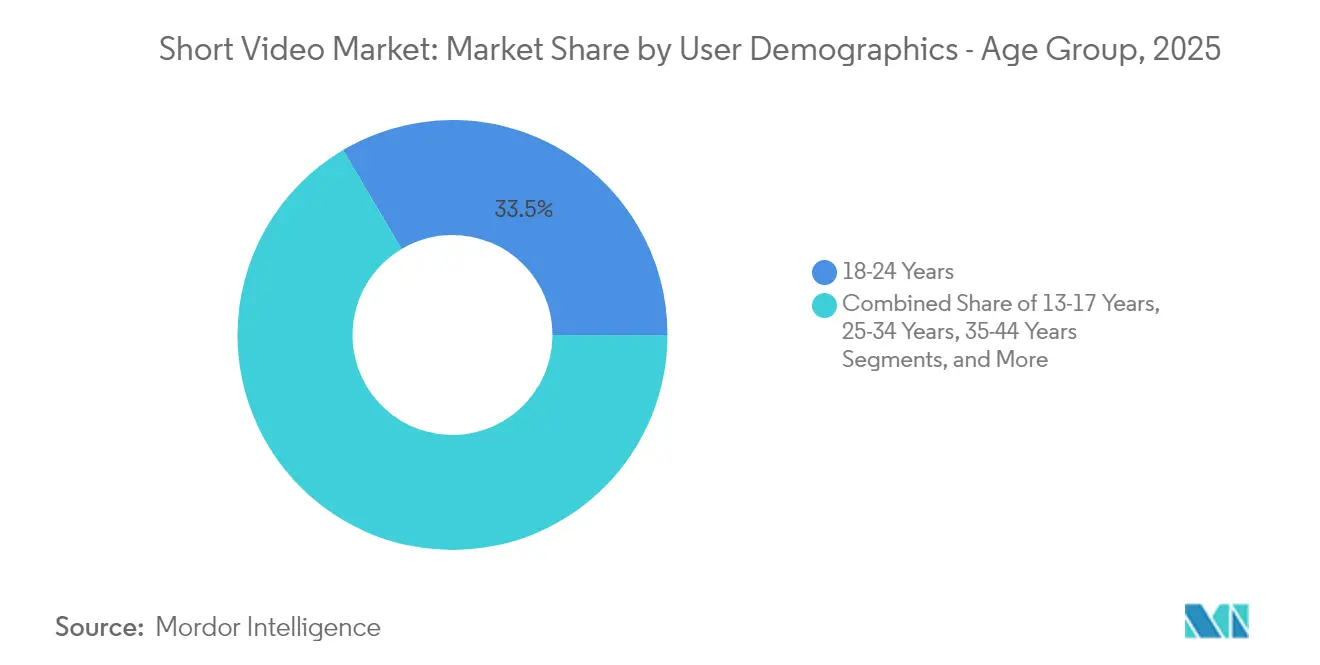

- By age group, users aged 18-24 commanded 33.50% share in 2025, while the 13-17 cohort is advancing at 12.20% CAGR through 2031.

- By industry, media and entertainment contributed 48.30% of 2025 revenue; retail-linked live commerce is forecast to accelerate at 13.40% CAGR.

- By region, Asia-Pacific dominated with 44.60% revenue in 2025, and the Middle East & Africa is set to pace growth at 11.50% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Short Video Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G-enabled cheap mobile data drives short-video consumption in Asia-Pacific | +2.1% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Commerce-enabled short videos boost advertiser ROI in North America & Europe | +1.8% | North America & EU | Short term (≤ 2 years) |

| AI generative editing tools lower barriers for user-generated content creation | +1.5% | Global | Short term (≤ 2 years) |

| Brand budget reallocation to vertical video ad units | +1.3% | Global | Short term (≤ 2 years) |

| Demand for micro-learning & bite-sized educational content | +1.0% | Global | Medium term (2-4 years) |

| Hyper-local language monetization fuels creator growth in emerging markets | +0.9% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G-Enabled Cheap Mobile Data Drives Short-Video Consumption in Asia-Pacific

Regional network upgrades are widening bandwidth and slashing data costs. GSMA forecasts 641 million 5G connections in India by 2030, while its wider Asia-Pacific outlook shows mobile data traffic quadrupling this decade.[1]GSMA, “The Mobile Economy Asia Pacific 2024,” gsma.comEricsson projects smartphone users worldwide will average 35 GB monthly data by 2026, with video taking roughly three-quarters of that load. The improved capacity lets platforms stream 4K clips without buffering, encourages longer in-session times, and supports emerging live-commerce layers that rely on sub-second latency.

Commerce-Enabled Short Videos Boost Advertiser ROI in North America and Europe

Shopping tools now appear directly inside vertical clips, connecting discovery to checkout in a single scroll. YouTube introduced shoppable product stickers for Shorts in June 2025, giving creators a non-advertising path to earn from product placements. Brands value these placements because they observe full-funnel events, from view to sale, inside the same channel. This transaction visibility shortens attribution cycles and supports premium ad rates, especially for consumer-goods campaigns aimed at Generation Z.

AI Generative Editing Tools Lower Barriers for User-Generated Content Creation

Text-to-video and template-based editing now let novice users publish studio-grade reels in minutes. YouTube is testing Google’s Veo 3 model inside Shorts to automate scene generation and effects. Such tools are most transformative in emerging markets where expensive hardware was a hurdle. Greater clip velocity benefits platforms that reward frequent posting, yet it also creates algorithmic pressure to separate quality from volume.

Brand Budget Reallocation to Vertical Video Ad Units

Mobile-first viewing has nudged advertisers to pivot. Dentsu expects global online-video ad spending to grow 8% annually through 2028, with vertical formats taking an outsized slice because they fill the full phone screen and prevent rotation friction.[2]Dentsu, “Global Ad Spend Forecast 2025,” dentsu.com The change is amplified by algorithm bias in favor of native portrait creatives, raising organic reach and lowering effective CPMs for brands that invest early.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory scrutiny of algorithmic recommendations (EU-DSA, US-KOSA) | –1.4% | North America & EU | Short term (≤ 2 years) |

| Escalating deep-fake & content-moderation costs | –1.1% | Global | Medium term (2-4 years) |

| Fragmented creator monetization reducing platform loyalty | –0.8% | Global | Medium term (2-4 years) |

| High CDN costs for 4K short-video in developing regions | –0.6% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Scrutiny of Algorithmic Recommendations (EU-DSA, US-KOSA)

The European Commission began formal inquiries into TikTok, YouTube, and Snapchat under the Digital Services Act in October 2024, requesting disclosure of ranking factors and user-choice settings.[3]European Commission, “Requests for information on recommender systems,” digital-strategy.ec.europa.eu In the United States, the Kids Online Safety Act cleared the Senate in July 2024, introducing duty-of-care rules for users under 17. Compliance forces platforms to rebuild recommendation logic, elevate manual review spending, and potentially limit personalized feeds for minors, which could lower watch times and ad impressions.

Escalating Deep-Fake & Content-Moderation Costs

Synthetic media is driving operational expense. Venture capital investment in deepfake-detection startups topped USD 200 million during 2023-2024 as providers rushed to meet platform demand.[4]Nitasha Tiku & Tatum Hunter, “Firms selling deepfake detection,” washingtonpost.com Platforms now pair automated scans with human reviewers, pushing per-video moderation costs higher each year. Smaller entrants struggle to match the scale of global incumbents, nudging the short video market toward further consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Content Type: Live Video Drives Real-Time Engagement

Pre-recorded clips retained 57.35% revenue in 2025, yet live streams are forecast to post a 12.10% CAGR to 2031, the fastest within the short video market. Viewer appetite for real-time interaction fits naturally with 5G - low latency keeps chats synchronous and enables on-screen product drops. The short video market size for live streams is set to rise sharply as Asian platforms merge flash-sale shopping with influencer broadcasts. Indonesia and Thailand already host in-app checkout pilots where viewers purchase during live demos. Pre-recorded clips continue to benefit from AI-assisted edits that compress production cycles. Ephemeral stories hold a niche use-case, giving creators a low-pressure outlet for unpolished moments that sustain daily engagement.

Creator strategy now blends all three formats: hooks in short stories, deeper narrative in polished clips, and immediate revenue in live showcases. As algorithms evolve, platforms mix these signals to shape discovery panels, rewarding creators who master multiple content modes within the same profile.

By Monetization Model: Diversification Beyond Advertising

In 2025, ads produced 75.20% of platform revenue, but alternative channels are growing faster. Tips, virtual gifts, and micro-transactions are projected to rise at 12.90% CAGR, a sign that users are willing to pay directly for value. This trajectory lowers volatility tied to CPM swings and seasonality. ShareChat’s practice of splitting revenue roughly evenly between ads and virtual coins shows hybrid structures gaining ground. The short video market size related to fan-funded payments could double by 2030 if direct-to-creator bonds strengthen. Subscriptions, brand collaborations, and in-clip shopping add further layers, creating a menu of income streams that make platforms stickier for talent.

Competition for top creators intensifies as Meta, YouTube, and TikTok roll out upfront bonuses and reduced take-rates to keep star uploaders exclusive. Sustainable monetization diversity now ranks alongside algorithm reach as a decisive factor in where creators post first.

By Deployment: Mobile-Native Dominance

Mobile apps accounted for 90.60% of 2025 usage, underscoring the handheld DNA of the short video market. The remaining 9.40% sits with web and smart-TV views, channels that serve discovery and casual browsing rather than daily binge sessions. Cross-platform tolerance matters, yet core engagement is still measured in portrait swipes, haptic taps, and push-driven returns. The short video market share linked to applications is unlikely to fall soon, given app-store placement and OS-level notification advantages.

Web portals do provide an entry path for older demographics or office-desktop users, and YouTube’s pivot to large-screen living-room viewing hints at broader future screens. However, flagships concentrate R&D on in-app experiences like AR filters, in-capture shopping carts, and community-tab polls that rely on native APIs.

By Platform Operating System: Android's Emerging-Market Advantage

Android led with 66.40% revenue in 2025, reflecting handset share in India, Southeast Asia, and Africa. iOS, while smaller in volume, is forecast to grow at 11.20% CAGR and delivers higher ARPU through in-app buys and tipping. The short video market size on iOS is expected to climb steadily as premium features such as 4K HDR uploads and exclusive badge systems stay paywalled behind Apple In-App Purchase compliance.

Snapchat’s recent India creator program shows how Android domination in tier-2 and tier-3 cities forces platforms to optimize for mid-range device memory footprints and patchy connectivity livemint.com. Over time, server-side rendering and dynamic bitrate tools may narrow the perceived quality gap, but monetization per user will likely stay skewed toward iOS.

By User Demographics - Age Group: Youth Engagement Drives Growth

Users aged 18-24 held 33.50% share in 2025, confirming that college and early-career viewers still anchor the audience core. The 13-17 bracket, though smaller today, is rising at 12.20% CAGR, reflecting how pre-teen smartphones and school-year leisure slots feed consumption. Platforms now design dual tracks: one algorithm for adults and another for minors, both needing high retention but different data privileges under KOSA rules

Older segments remain the white space. Education clips, travel hacks, and creator-led personal finance tips are slowly attracting viewers over 35, but ad spend follows youth eyeballs. Successful outreach to broader demos will demand clearer content labels and opt-in personalization so that first-time users feel safe layering short clips into their daily media diet.

By End-User Industry: Entertainment Leads, Commerce Accelerates

Media and entertainment produced 48.30% of 2025 revenue, a legacy of music-synced dance trends and meme culture. Retail-focused live commerce now shows the fastest runway at 13.40% CAGR, aided by influencer-led flash sales in Brazil and Southeast Asia. The short video market size for retail interactions could surpass pure entertainment by the decade’s end if conversion funnels stay friction-free.

Education, hospitality, and fintech follow behind, each experimenting with micro-learning modules, destination teasers, and payment explainers. The format’s near-instant feedback loop lets brands A/B-test messages daily, shortening creative cycles that were once measured in quarters.

Geography Analysis

Asia-Pacific generated 44.60% of revenue in 2025, a weight driven by China’s Douyin, India’s booming creator ecosystem, and Southeast Asia’s mobile-centric youth. India’s consumer-internet economy is forecast to hit USD 1 trillion, and daily active users of short clips have already grown 3.6 times since pre-pandemic levels. China hosts parallel giants such as Xiaohongshu with 300 million lifestyle fans, showing that sizable domestic user pools can support multiple winners. Ongoing 5G rollout supplies the bandwidth floor for 4K vertical streams and AR effects, so engagement hours keep climbing even as markets mature.

The Middle East & Africa, while smaller today, holds the highest projected growth at 11.50% CAGR through 2031. Smartphone affordability, youth-heavy populations, and rising local-language content libraries all widen the funnel. Broadband penetration in Africa stands at 12% yet is forecast to reach 17.3% by 2030. That connectivity uplift, combined with creator programs focused on regional dialects, positions the short video market for outsized momentum once infrastructure gaps narrow.

North America and Europe operate as regulatory pace-setters rather than volume leaders. The EU Digital Services Act and the forthcoming technical standards for recommender transparency impose redesign cycles that ripple globally. A possible TikTok restriction in the United States could shuffle ad budgets toward YouTube Shorts and Instagram Reels. Despite slower user growth, these regions deliver the industry’s highest ARPU, thanks to brand demand for premium placements and a larger share of commerce-enabled clips.

Competitive Landscape

The field remains fragmented. ByteDance, Meta, and Google vie for creator mindshare by pairing reach with revenue incentives, but none holds a decisive monopoly. TikTok runs localized live-commerce pilots and pushes into Latin America to diversify geo-risk. Instagram Reels explores a stand-alone app strategy, signaling that focused surfaces may outperform multi-format feeds. YouTube Shorts leans on existing channel subscriptions, integrating Veo-powered AI to quick-start clip production.

Strategic M&A focuses on AI tooling. Meta discussed acquiring Runway after investing USD 14.3 billion in Scale AI to secure in-house video generation. Elon Musk’s xAI picked up Hotshot to expand synthetic-video capability dig.watch. Infrastructure consolidation also marches on: Bending Spoons bought Brightcove to fold streaming tech into its mobile-app suite.

Creator bargaining power rises as switching frictions drop. Meta now pays select influencers to post Instagram content on rival platforms, flipping the old exclusivity logic on its head. Smaller regionals, like ShareChat and QuickTV in India, court local talent with micro-dramas and language-specific discovery rails. As monetization models multiply, the decisive edge shifts toward platforms that balance compliance, creator upside, and commerce pipes under one UX.

Short Video Industry Leaders

Beijing Wei Ran Internet Technology

Facebook (Instagram)

Doupai

ByteDance Ltd. (Toutiao)

Tencent Holdings Ltd. (Weishi)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: YouTube rolled out shopping stickers for Shorts, opening direct buyer journeys inside vertical clips.

- June 2025: Meta explored a purchase of AI-startup Runway following its Scale AI investment.

- April 2025: Meta posted Q1 2025 revenue of USD 42.31 billion, up 16% YoY, supported by video ad demand.

- March 2025: xAI bought Hotshot to add generative-video technology.

- February 2025: Instagram confirmed it is considering spinning Reels into its own app.

- January 2025: Perplexity AI revised a USD 50 billion offer for TikTok’s US assets, proposing up to 50% government ownership after IPO.

Global Short Video Market Report Scope

Short-form videos, typically lasting between 5 to 90 seconds, have gained prominence on popular platforms like Instagram, TikTok, and YouTube. These brief durations cater to users' shorter attention spans.

The study tracks the revenue accrued through the sale of short videos by various players across the globe. It also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The short video market is segmented by type (live video and video posts), deployment (application-based and website-based), platform(android, iOS, and windows), end-user(education, media and entertainment, live commerce, and others), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Live Video |

| Pre-Recorded Video Posts |

| Short-Video Stories (Ephemeral) |

| Advertising-Supported |

| Subscription-Based (SVOD, Freemium) |

| In-App Purchases and Tipping |

| Brand-Sponsored Commerce (Shoppable Tags) |

| Application-Based Platforms |

| Web-Based Platforms |

| Android |

| iOS |

| Windows and Others |

| 13-17 Years |

| 18-24 Years |

| 25-34 Years |

| 35-44 Years |

| 45+ Years |

| Education and EduTech |

| Media and Entertainment |

| Retail and Live Commerce |

| Travel and Hospitality |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Content Type | Live Video | |

| Pre-Recorded Video Posts | ||

| Short-Video Stories (Ephemeral) | ||

| By Monetization Model | Advertising-Supported | |

| Subscription-Based (SVOD, Freemium) | ||

| In-App Purchases and Tipping | ||

| Brand-Sponsored Commerce (Shoppable Tags) | ||

| By Deployment | Application-Based Platforms | |

| Web-Based Platforms | ||

| By Platform Operating System | Android | |

| iOS | ||

| Windows and Others | ||

| By User Demographics - Age Group | 13-17 Years | |

| 18-24 Years | ||

| 25-34 Years | ||

| 35-44 Years | ||

| 45+ Years | ||

| By End-User Industry | Education and EduTech | |

| Media and Entertainment | ||

| Retail and Live Commerce | ||

| Travel and Hospitality | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the short video market?

The short video market size stood at USD 2.17 billion in 2026 and is forecast to reach USD 3.37 billion by 2031.

Which region leads revenue today?

Asia-Pacific accounts for 44.60% of global revenue, reflecting large user bases and rapid 5G adoption.

Which content format is growing fastest?

Live video streams are projected to grow at a 12.10% CAGR through 2031 as real-time shopping and chat features gain traction.

How are platforms monetizing beyond advertising?

Tips, virtual gifts, and in-clip shopping are expanding at 12.90% CAGR, giving creators direct fan income that complements ad revenue.

What regulations could slow growth?

The EU Digital Services Act and the US Kids Online Safety Act require new transparency and youth-safety measures, raising compliance costs and potentially lowering engagement for personalized feeds.

Which age group will drive future expansion?

Users aged 13-17 are rising quickest at 12.20% CAGR, signaling that the next generation of consumers will deepen short video adoption even further.

Page last updated on: