Sternal Closure Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

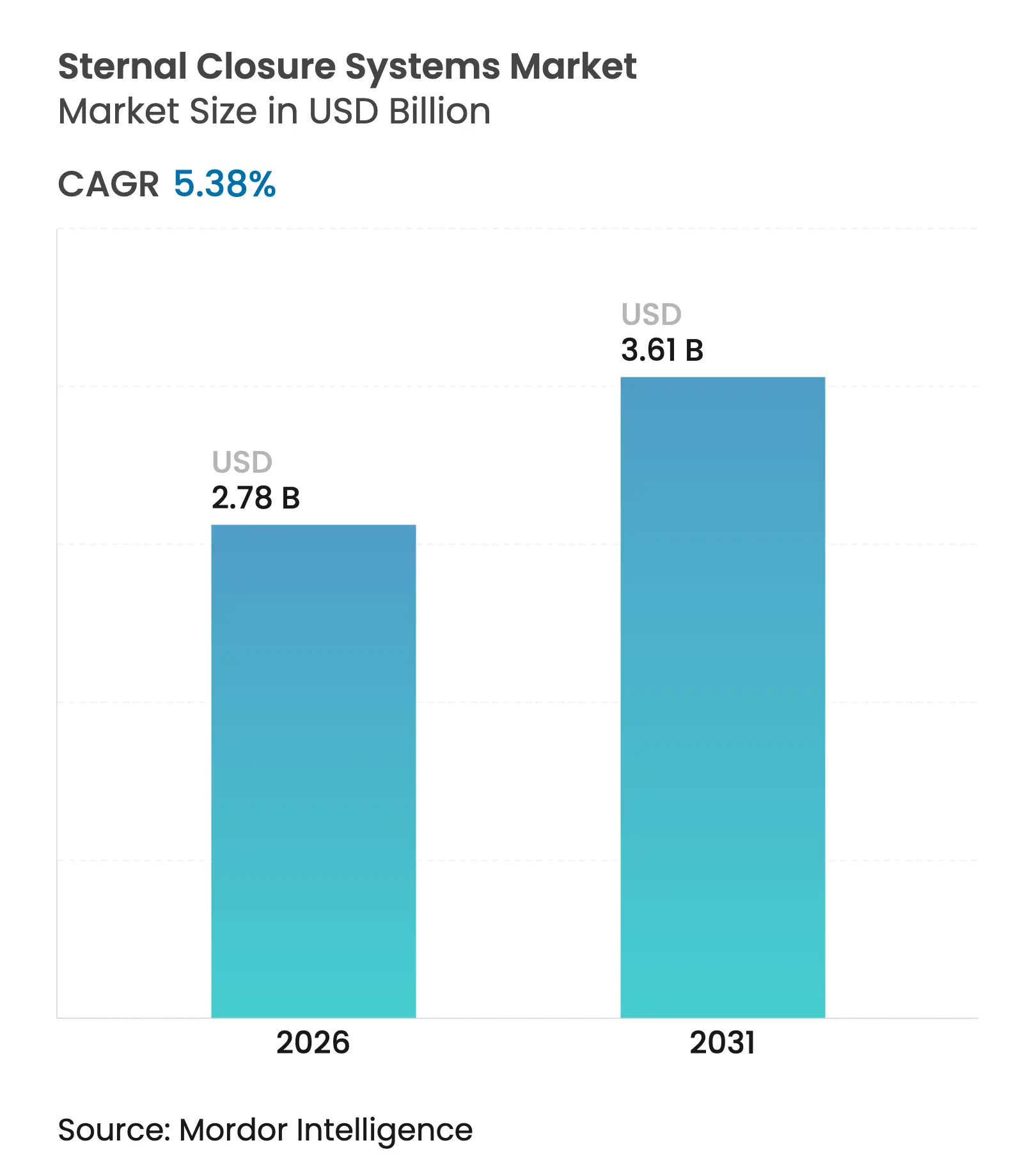

| Market Size (2026) | USD 2.78 Billion |

| Market Size (2031) | USD 3.61 Billion |

| Growth Rate (2026 - 2031) | 5.38 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Sternal Closure Systems Market Analysis by Mordor Intelligence

sternal closure systems market size in 2026 is estimated at USD 2.78 billion, growing from 2025 value of USD 2.64 billion with 2031 projections showing USD 3.61 billion, growing at 5.38% CAGR over 2026-2031. Growth reflects the steady rhythm of global cardiac surgery volumes, with developed regions moving toward replacement demand and emerging economies adding new procedure capacity. A visible shift from legacy wires to rigid plate-and-screw constructs anchors this expansion because hospitals now link closure performance to lower readmission penalties under value-based reimbursement. Demographic pressure adds momentum as octogenarian patients undergo more complex surgeries that raise sternal stability requirements. Regulatory agencies, especially the FDA, continue to tighten quality-system rules, favoring well-documented devices and slowing low-evidence entrants. Cost containment remains central, but bundled-payment models tilt decisions toward technologies that cut episode-of-care expenses through fewer complications.

Key Report Takeaways

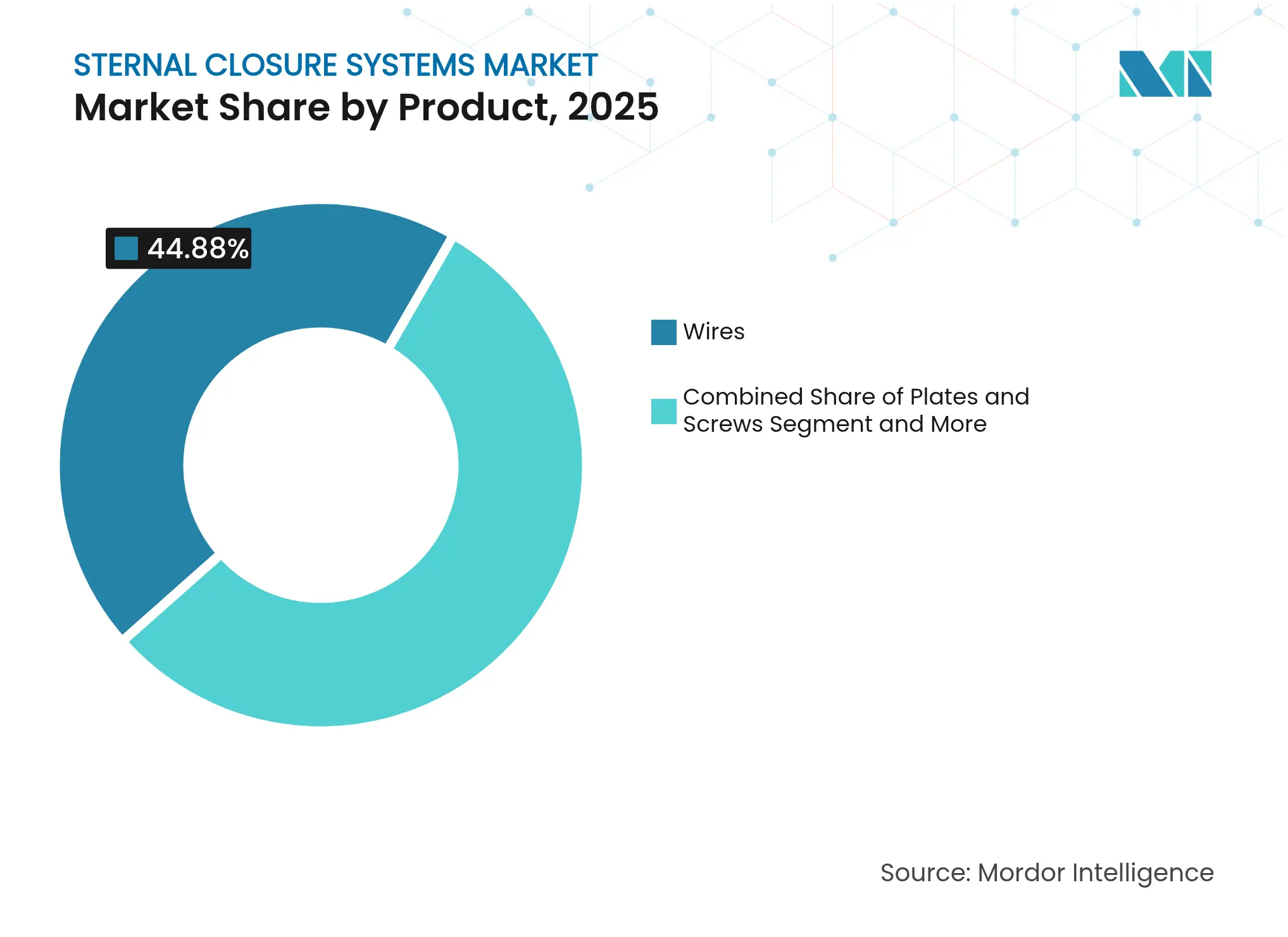

- By product type, traditional wires held 44.88% of the sternal closure systems market share in 2025, while plates and screws are projected to post the fastest 9.27% CAGR through 2031.

- By procedure, median sternotomy commanded 78.10% of the sternal closure systems market size in 2025, whereas bilateral thoracosternotomy is expected to register a 9.7% CAGR to 2031.

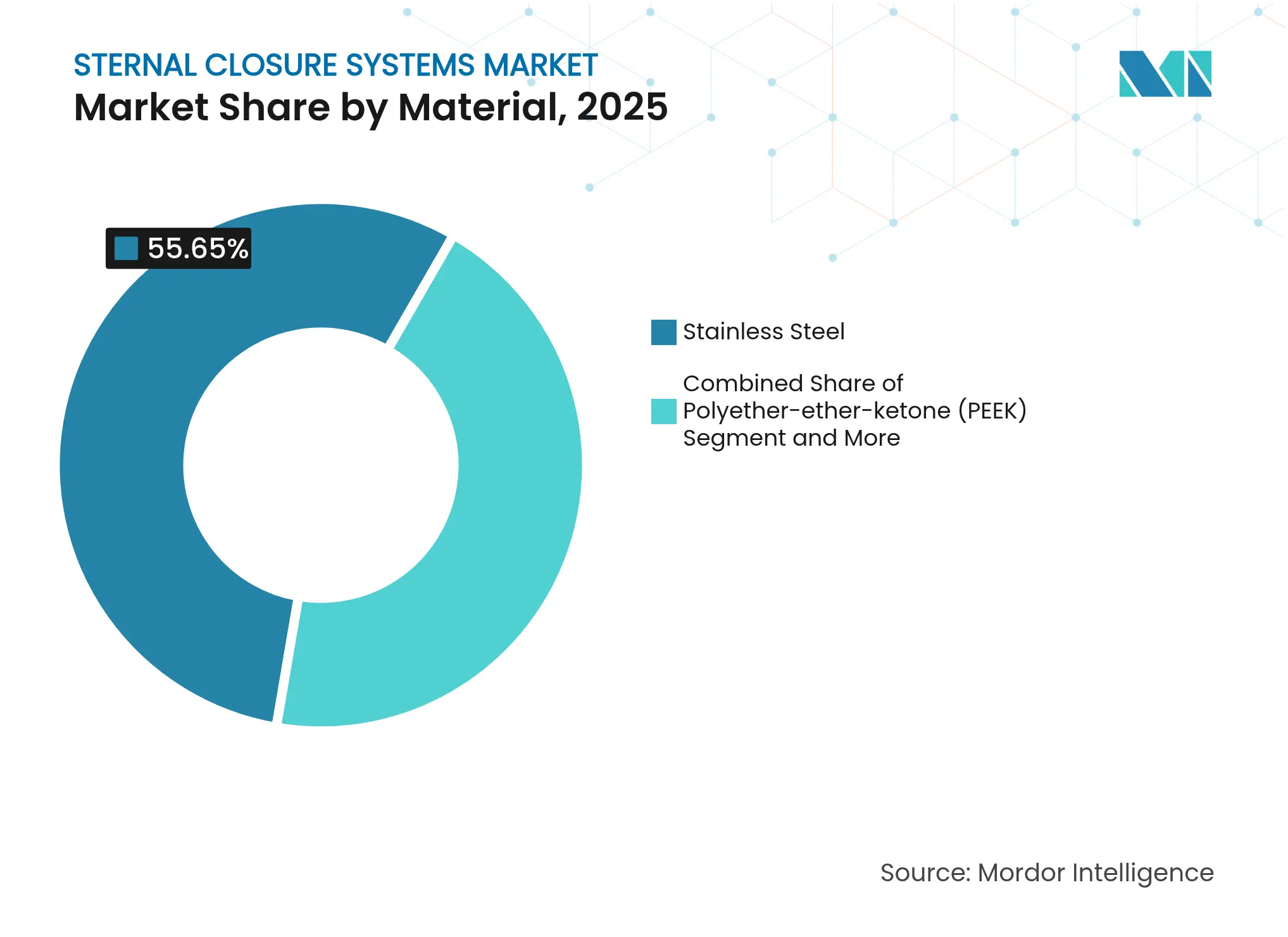

- By material, stainless steel dominated with 55.65% share of the sternal closure systems market size in 2025; titanium is forecast to expand at 10.6% CAGR over the same horizon.

- By end user, tertiary care hospitals accounted for 44.55% revenue share of the sternal closure systems market in 2025, and cardio-thoracic specialty clinics are on track for a 9.57% CAGR through 2031.

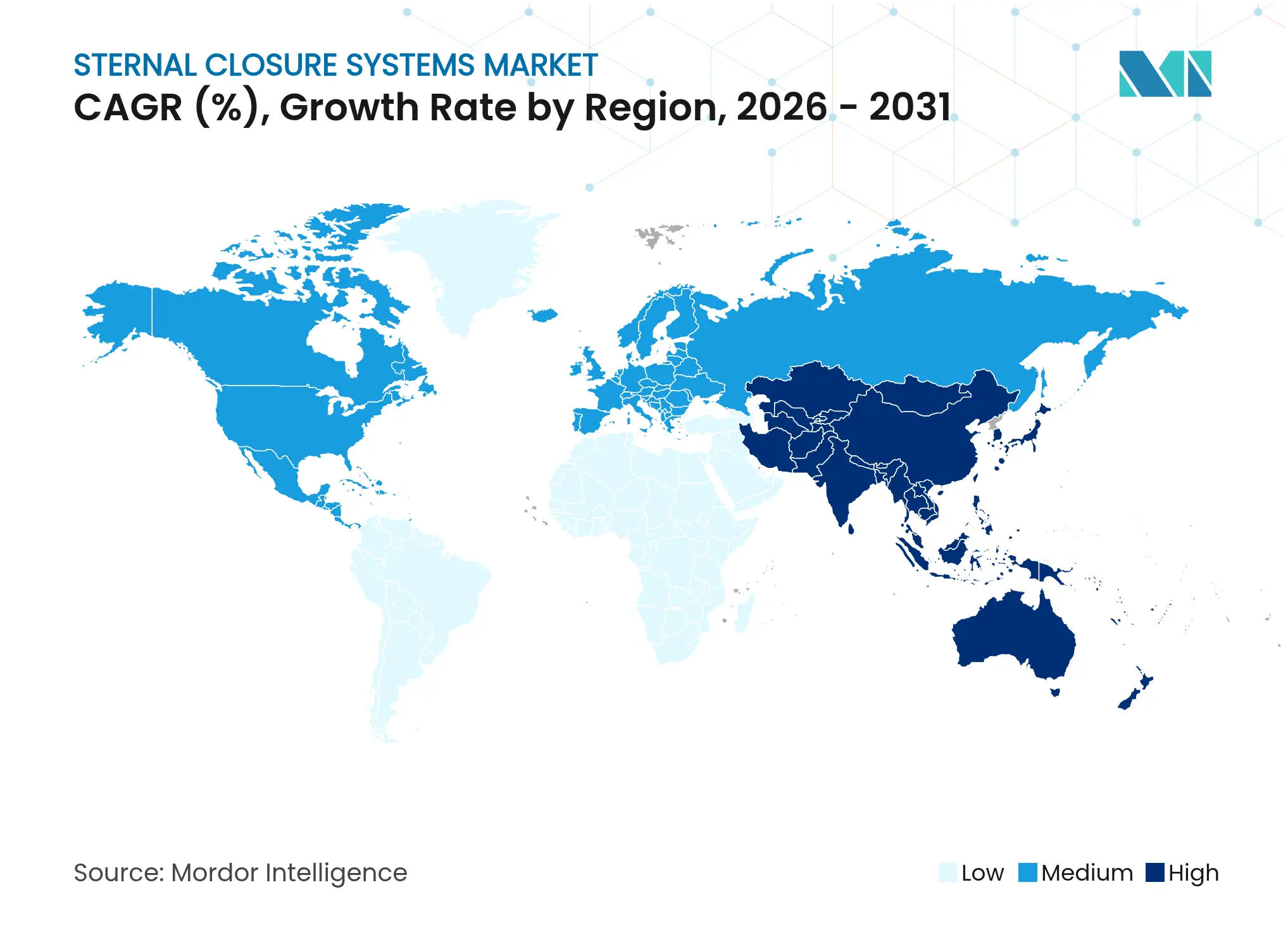

- By geography, North America held 41.95% revenue share in 2025; Asia-Pacific is on track to post the highest 11.34% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sternal Closure Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing Volume Of Open-Heart Procedures & Ageing

Demographics

Growing Volume Of Open-Heart Procedures & Ageing

Demographics

| +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+1.2%

| Geographic Relevance:

Global, with concentration in North America & Europe

| Impact Timeline:

Long term (≥ 4 years)

|

Rising Incidence Of Complex, Non-Healing Sternotomy Wounds

Rising Incidence Of Complex, Non-Healing Sternotomy Wounds

| +0.8% | Global, higher impact in developed markets | Medium term (2-4 years) | |||

Rapid Adoption Of Rigid Plate-And-Screw Fixation Systems

Rapid Adoption Of Rigid Plate-And-Screw Fixation Systems

| +1.5% | North America & Europe, expanding to APAC | Medium term (2-4 years) | |||

Hospital Bundled-Payment Programs Favouring

Low-Readmission Devices

Hospital Bundled-Payment Programs Favouring

Low-Readmission Devices

| +0.6% | North America, early adoption in EU | Short term (≤ 2 years) | |||

Emergence Of Bio-Absorbable Polymer/PEEK Sternum Implants

Emergence Of Bio-Absorbable Polymer/PEEK Sternum Implants

| +0.9% | Global, led by developed markets | Long term (≥ 4 years) | |||

AI-Guided Intra-Operative Imaging Improving Closure

Accuracy

AI-Guided Intra-Operative Imaging Improving Closure

Accuracy

| +0.7% | North America & EU, selective APAC adoption | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Volume of Open-Heart Procedures & Ageing Demographics

Cardiac units worldwide now treat a much larger cohort of patients aged 80 years and above, whose numbers within surgical case mix have multiplied twenty-fourfold since 2024. Longer life expectancy, advanced anesthesia protocols, and better peri-operative support enable surgeons to accept higher-risk, complex candidates. Elderly chests exhibit brittle bone quality and slower ossification, raising sternal instability hazards that conventional stainless-steel wires cannot fully mitigate. Hospitals increasingly allocate rigid fixation kits to this segment because readmission penalties tied to dehiscence often exceed the premium device cost. In value terms, every avoided wound complication saves up to USD 45,000 across the 90-day episode, making plate systems economically rational even for publicly funded institutions[1]Center for Devices and Radiological Health, “Xstim Spine Fusion Stimulator – P230025,” fda.gov. The demographic driver is therefore structural and sustains long-horizon demand for advanced systems within the sternal closure systems market.

Rising Incidence of Complex, Non-Healing Sternotomy Wounds

Deep sternal wound infection rates vary from 0.5% to 5%, but mortality still climbs above 25% when dehiscence occurs. Diabetes, obesity, and immunosuppression foster poor vascularization at the osteotomy margin, undermining wire-only constructs that permit micro-motion during respiration. Rigid plates distribute load along both cortical tables, maintaining contact to encourage callus formation throughout the 6-to-8-week healing window. Hospitals now stratify patients based on pre-operative HbA1c, BMI, and immune status, reserving titanium plates for the upper-risk quintile. This selective deployment yields demonstrable quality gains: one US multi-center study recorded a 43% drop in deep sternal wound complications after protocol change, trimming average length of stay by 2.6 days. Rising complexity of wound profiles thus elevates rigid fixation from optional to recommended in many guidelines, sustaining expansion of the sternal closure systems market.

Rapid Adoption of Rigid Plate-and-Screw Fixation Systems

Rigid fixation represents a philosophical pivot from approximation to osteosynthesis. Early concerns about extra operative minutes have been neutralized by third-generation systems with pre-contoured plates, self-drilling screws, and intuitive targeting guides that cut application time by 43% versus first-generation kits. Manufacturers now bundle single-use instruments, eliminating sterilization bottlenecks and standardizing workflow across operating rooms. Clinical registries show up to 28% lower 30-day readmission with rigid plates relative to wires in high-risk patients, reinforcing surgeon confidence. Switching costs remain real: teams require fresh competencies, and supply chains must stock plate caddies of multiple lengths. Yet once institutions cross the learning curve, consistency of closure quality and improved OR scheduling have raised surgeon satisfaction scores in tertiary centers. Combined, these factors accelerate rigid system penetration and underpin a meaningful share shift within the sternal closure systems market.

Hospital Bundled-Payment Programs Favouring Low-Readmission Devices

United States payment reform under the Transforming Episode Accountability Model (TEAM) will link 2026 reimbursement for coronary artery bypass graft surgeries to 90-day resource utilization. Device selection therefore influences hospital margins well beyond the operative suite. Internal audits at early-adopter centers show 37% episode-of-care cost reduction after introducing “perfect-care” protocols that prioritize premium sternal fixation for high-risk patients. European countries piloting similar bundled schemes observe parallel trends, with German university hospitals publishing 14% savings per case once rigid plates became protocol for diabetes patients. These findings intensify administrative focus on closure systems because the sternal joint is the single largest driver of post-discharge complications. Manufacturers able to supply health-economic dashboards that translate reduction in readmissions into margin preservation are winning formulary slots more quickly. Consequently, reimbursement innovation sustains premium demand inside the sternal closure systems market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Infection & Dehiscence Risks In High-BMI/Diabetic

Cohorts

Infection & Dehiscence Risks In High-BMI/Diabetic

Cohorts

| -0.9% | Global, higher impact in developed markets with obesity prevalence | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-0.9%

| Geographic Relevance:

Global, higher impact in developed markets with obesity

prevalence

| Impact Timeline:

Medium term (2-4 years)

|

High Device & OR Time Costs Vs. Conventional Wires

High Device & OR Time Costs Vs. Conventional Wires

| -0.7% | Cost-sensitive markets, emerging economies | Short term (≤ 2 years) | |||

Shortage Of Surgeons Trained On Rigid Fixation Systems

Shortage Of Surgeons Trained On Rigid Fixation Systems

| -0.5% | Global, more acute in emerging markets | Long term (≥ 4 years) | |||

Heightened Regulatory Scrutiny On Implant Particulates

(Micro-Plastics)

Heightened Regulatory Scrutiny On Implant Particulates

(Micro-Plastics)

| -0.4% | North America & EU regulatory jurisdictions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Infection & Dehiscence Risks in High-BMI/Diabetic Cohorts

Obese and diabetic patients represent the paradox of need versus risk. Their soft-tissue bulk and impaired microcirculation heighten infection susceptibility, and any foreign body can aggravate inflammatory cascades. Even titanium surfaces occasionally shed nano-scale particles, fueling concern about long-term bioreactivity. Clinicians therefore hesitate to approve novel constructs until safety in these cohorts is documented. A 2024 Polish cohort study flagged elevated metallic ion loads in diabetic implant recipients, prompting calls for extended surveillance protocols. Fear of malpractice litigation fosters a conservative stance and slows new-technology spread within the sternal closure systems market.

High Device & OR Time Costs vs. Conventional Wires

Rigid fixation systems retail at 10-15 times the price of standard No.6 stainless wires. They also necessitate battery-powered drills, single-use drivers, and inventory stocking across plate configurations, elevating capital burden. In emerging markets where fee-for-service remains dominant, hospitals cannot yet recoup that outlay. Shorter OR throughput during the adoption phase compounds the budget impact. While bundled-payment models will eventually reward complication avoidance, many institutions still evaluate devices solely on purchase price. Regulatory paperwork such as FDA Particulate Guidance adds further cost for manufacturers, filtering down to hospitals[2]U.S. Food and Drug Administration, “Orthopedic Non-Spinal Bone Plates, Screws, and Washers 510(k) Guidance,” federalregister.gov. This restraint therefore tempers rapid conversion from wires and caps overall CAGR of the sternal closure systems market.

Segment Analysis

By Product: Gradual Shift from Wires to Plates

Traditional stainless-steel wires controlled 44.88% of the sternal closure systems market share in 2025. Unit volume dominance persists because surgeons in low-risk coronary bypass cases prefer a familiar, inexpensive technique. Plates and screws, however, recorded a vigorous 9.27% CAGR, capturing share in geriatric valve replacements and redo sternotomies where shear loads are higher. Legacy cement and adhesive lines remain niche, primarily for complex reconstructions involving bone loss. Bio-absorbable plates, fabricated from polylactide and reinforced PEEK fibers, appeal in pediatric repairs but face adult uptake barriers due to particulate scrutiny. Economic modeling shows that rigid plates become cost-neutral when infection incidence drops by 0.4 percentage points; tertiary centers already exceed that threshold, explaining their early conversion. Device manufacturers support the transition with surgeon workshops and intramedullary load calculators, enabling evidence-based selection rather than brand influence. Over the forecast horizon, plates are projected to reach 34.50% unit mix, leaving wires to retreat yet remain essential for low-budget facilities, ensuring plural technology coexistence within the sternal closure systems market.

Advanced plate systems like Johnson & Johnson’s MatrixSTERNUM introduced modular designs that help customize span, screw vector, and load sharing with minimal bend adjustments, reducing intra-operative guesswork. This engineering flexibility dovetails with hospital inventory preferences because a single tray can cover body mass index extremes. Meanwhile, mini-screw technology trims profile height, allowing easier soft-tissue closure and lowering postoperative discomfort. Collectively, these refinements push rigid fixation deeper into everyday practice and lift premium ASPs, which in turn uplifts total revenue even if overall case volumes plateau. Although wires will not vanish, their relative revenue impact will shrink compared with plate-centric growth inside the sternal closure systems market.

Note: Segment shares of all individual segments available upon report purchase

By Procedure: Sternotomy Still Reigns but Minimally Invasive Access Expands

Median sternotomy continued as the workhorse, securing 78.10% of the sternal closure systems market size in 2025. Complete exposure to the heart is indispensable for multivessel bypasses and complex valve reconstructions. Closure across the entire sternum demands robust fixation that counters respiratory torsion, historically the domain of full-length wire cerclage. Bilateral thoracosternotomy created a high-growth pocket, adding a 9.7% CAGR because hybrid valve-plus-CABG protocols and robotic harvesting techniques favor lateral access. Surgeons adopting bilateral windows need shorter plates with offset screw geometry to avoid internal mammary pedicles, spurring niche product lines.

Hemi-sternotomy, often used for isolated aortic valve replacement, balances exposure and tissue preservation, providing a middle ground on fixation complexity. It fosters demand for contourable fixation strips that accept either wires or screws, letting teams tailor closure to anatomy. Regulatory bodies now require procedure-specific bench testing. Plate vendors respond with finite-element models that prove load dispersion under asymmetric breathing cycles. As the mix migrates toward limited-access surgery, versatile closure kits capable of segmental stability across variable cut lengths will command pricing power, reinforcing growth of premium tiers in the sternal closure systems market.

By Material: Titanium Surges on Biocompatibility Edge

Stainless steel retained 55.65% volume share in 2025 owing to price advantage and entrenched supply chains. Titanium expanded at 10.6% CAGR, benefiting from lower modulus, superior fatigue resistance, and near-complete corrosion immunity. Clinical imagery shows reduced artifact during CT-guided evaluation because titanium’s atomic weight attenuates beams less than steel. Surgeons use these clear scans to gauge callus bridging earlier, allowing faster mobilization. PEEK implants offer radiolucency and neutral elasticity but draw regulator attention after reports of micro-particle embolism in vascular coatings, tempering enthusiasm until long-term data accrue. Composite constructs combining titanium load arms with carbon-fiber webs remain experimental yet promise weight savings.

The economics of titanium improved after additive-manufacturing lines reached scale in 2024, slicing per-plate cost by 23%. Producers like Zimmer Biomet qualify electron-beam powder bed processes under FDA ISO-13485 amendments, enhancing reproducibility. Sustainability narratives also favor titanium because scrap recycling back into powder has advanced. Over the projection window, material substitution will intensify, propelling titanium toward majority status in revenue terms, whereas stainless will persist as budget default within sections of the sternal closure systems market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Specialist Centers Shape Premium Mix

Tertiary care hospitals led with 44.55% revenue because their intensive-care units and perfusion services support multifaceted cardiac operations that mandate high-level closure technology. These centers qualify for enhanced reimbursement bundles that reward complication avoidance, making a strong case for plates over wires. Cardio-thoracic specialty clinics posted a 9.57% CAGR through 2031, leveraging focused staff training and streamlined protocols that cut OR turnover times. Such clinics often negotiate bulk supply agreements, locking in device pricing yet committing to rigid fixation standardization.

Ambulatory surgery centers dabble in limited sternotomy for select low-risk valve procedures but account for a small fraction of volume as accreditation bodies impose stringent overnight-stay rules for cardiac surgery. Academic hospitals drive research on bio-absorbable systems, hosting first-in-human trials and collecting long-tail outcome evidence essential for regulator dossiers. Commercial adoption patterns therefore correlate tightly with institutional capability maturity. Vendors now align sales teams by account archetype—complex centers, focused clinics, or emerging cardiac programs—to tailor economic justifications and training pathways, reinforcing segmentation discipline within the sternal closure systems market.

Geography Analysis

North America captured 41.95% of 2025 revenue due to extensive cardiac surgery infrastructure and early embrace of rigid fixation reimbursement pathways. Hospitals in the United States already integrate closure choices into 30-day readmission metrics tracked under Hospital Value-Based Purchasing, a practice that sets the technological tone for Canada and Mexico. FDA oversight raises documentation hurdles but also signals long-term stability once approvals are secured. Growth remains steady rather than explosive, tied more to replacement demand and technology refresh cycles than to procedure expansion.

Europe contributes a balanced growth profile underpinned by centralized purchasing but evidence-driven device evaluation. The Medical Device Regulation compels continuous post-market surveillance, pushing manufacturers to maintain clinical databases that prove benefit in real-world registries. Germany and the United Kingdom lead plate adoption because academic networks publish outcome data rapidly, swaying clinician sentiment continent-wide. Southern and Eastern Europe focus on cost-optimized titanium kits, importing from regional producers that meet MDR yet undercut multinational prices. Currency volatility and healthcare budget negotiations influence unit flow, but ageing populations promise demand resilience inside the European slice of the sternal closure systems market.

Asia-Pacific posts the fastest 11.34% CAGR. China’s public–private hospital modernization programs increased open-heart capacity by 14% year on year, while India’s private tertiary chains invest in high-acuity cardiac floors that attract medical tourism. Japan retains strict Shonin device clearance, extending time to market but rewarding durable safety records once obtained. Lower-income ASEAN members favor hybrid procurement, often equipping flagship state hospitals with titanium plates while community centers still rely on wires. Cultural emphasis on scar minimization spurs minimally invasive procedure uptake, indirectly supporting plate adoption. Vendors successful in this region run dual portfolios: imported titanium for tier-1 cities and stainless assembled locally for price-sensitive provinces, achieving breadth in the sternal closure systems market.

Competitive Landscape

Market Concentration

Competitive intensity ranks moderate because switching costs and training dependencies discourage quick brand turnover. Johnson & Johnson (DePuy Synthes) leverages cross-disciplinary fixation know-how to provide an umbrella portfolio from wires to modular plates. Zimmer Biomet and Stryker convert orthopedic design playbooks into cardiac plates with notch-free edges that lessen soft-tissue irritation. Regional entrants such as KLS Martin maintain strongholds in specific geographies by customizing instrument trays to local surgeon preferences. Start-ups like Figure 8 Surgical explore cable-plate hybrids promising faster placement, but must hurdle clinical evidence expectations before national tenders will engage.

Strategic emphasis gradually shifts from product to ecosystem. Vendors now pair hardware with digital case-planning software that simulates screw trajectory on CT data, allowing pre-operative rehearsal. Cloud-based outcome dashboards feed anonymized data back to manufacturers who refine plate geometries faster. AI guidance companies eye the closure act for real-time torque feedback, a domain where device majors may partner or acquire to sustain edge. Regulatory documents published in late 2024 added particulate emission limits for polymer implants, favoring firms with advanced in-house test facilities able to certify compliance without subcontract delays. Overall, brands with deep clinical evidence pipelines and integrated training revert to capture most incremental share within the sternal closure systems market.

Sternal Closure Systems Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: MTF Biologics and Kolosis BIO partnered to market ATLAS Sternal Repair Matrix and IKON Allograft Surgical Matrix, expanding biologic options for high-risk chest closure.

- August 2024: DePuy Synthes released the MatrixSTERNUM modular titanium plate system, enabling surgeon-specific fixation patterns for geriatric and revision cases.

Table of Contents for Sternal Closure Systems Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing Volume of Open-Heart Procedures & Ageing Demographics

- 4.2.2Rising Incidence of Complex, Non-Healing Sternotomy Wounds

- 4.2.3Rapid Adoption of Rigid Plate-And-Screw Fixation Systems

- 4.2.4Hospital Bundled-Payment Programs Favouring Low-Readmission Devices

- 4.2.5Emergence of Bio-Absorbable Polymer/PEEK Sternum Implants

- 4.2.6AI-Guided Intra-Operative Imaging Improving Closure Accuracy

- 4.3Market Restraints

- 4.3.1Infection & Dehiscence Risks In High-BMI/Diabetic Cohorts

- 4.3.2High Device & OR Time Costs Vs. Conventional Wires

- 4.3.3Shortage Of Surgeons Trained On Rigid Fixation Systems

- 4.3.4Heightened Regulatory Scrutiny On Implant Particulates (Micro-Plastics)

- 4.4Technological Outlook

- 4.5Porter's Five Forces

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product

- 5.1.1Wires

- 5.1.2Plates & Screws

- 5.1.3Bone Cement & Adhesives

- 5.1.4Bio-absorbable Systems

- 5.1.5Others

- 5.2By Procedure

- 5.2.1Median Sternotomy

- 5.2.2Hemi-sternotomy

- 5.2.3Bilateral Thoracosternotomy

- 5.3By Material

- 5.3.1Stainless Steel

- 5.3.2Titanium

- 5.3.3Polyether-ether-ketone (PEEK)

- 5.3.4Composite/Bio-absorbable Polymers

- 5.4By End User

- 5.4.1Tertiary Care Hospitals

- 5.4.2Cardio-Thoracic Specialty Clinics

- 5.4.3Ambulatory Surgery Centers

- 5.5Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Johnson & Johnson (DePuy Synthes & Ethicon)

- 6.3.2Zimmer Biomet Holdings

- 6.3.3Stryker Corporation

- 6.3.4KLS Martin Group

- 6.3.5B Braun SE

- 6.3.6Acumed LLC

- 6.3.7Medtronic plc

- 6.3.8Orthofix Holdings Inc

- 6.3.9Abyrx Inc

- 6.3.10Kinamed Inc

- 6.3.11Jace Medical

- 6.3.12Praesidia SRL

- 6.3.13IDEAR SRL

- 6.3.14RTI Surgical

- 6.3.15Arthrex Inc

- 6.3.16Jeil Medical Corp

- 6.3.17Neos Surgery SL

- 6.3.18MedXpert GmbH

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Sternal Closure Systems Market Report Scope

As per the scope of the report, sternal closure systems are intended for use in stabilizing and refocusing fractures of the anterior chest wall. The systems are used in sternal fixation following sternotomy and sternal reconstructive surgical procedures to promote fusion. The market is segmented by Product (Wires, Plates and Screws, Bone Cement, Others), Procedure (Median Sternotomy, Hemisternotomy, Bilateral Thoracosternotomy), Material (Stainless Steel, Polyether Ether Ketone, Titanium), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.