Arteriotomy Closure Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.14 Billion |

| Market Size (2031) | USD 3.06 Billion |

| Growth Rate (2026 - 2031) | 7.44% CAGR |

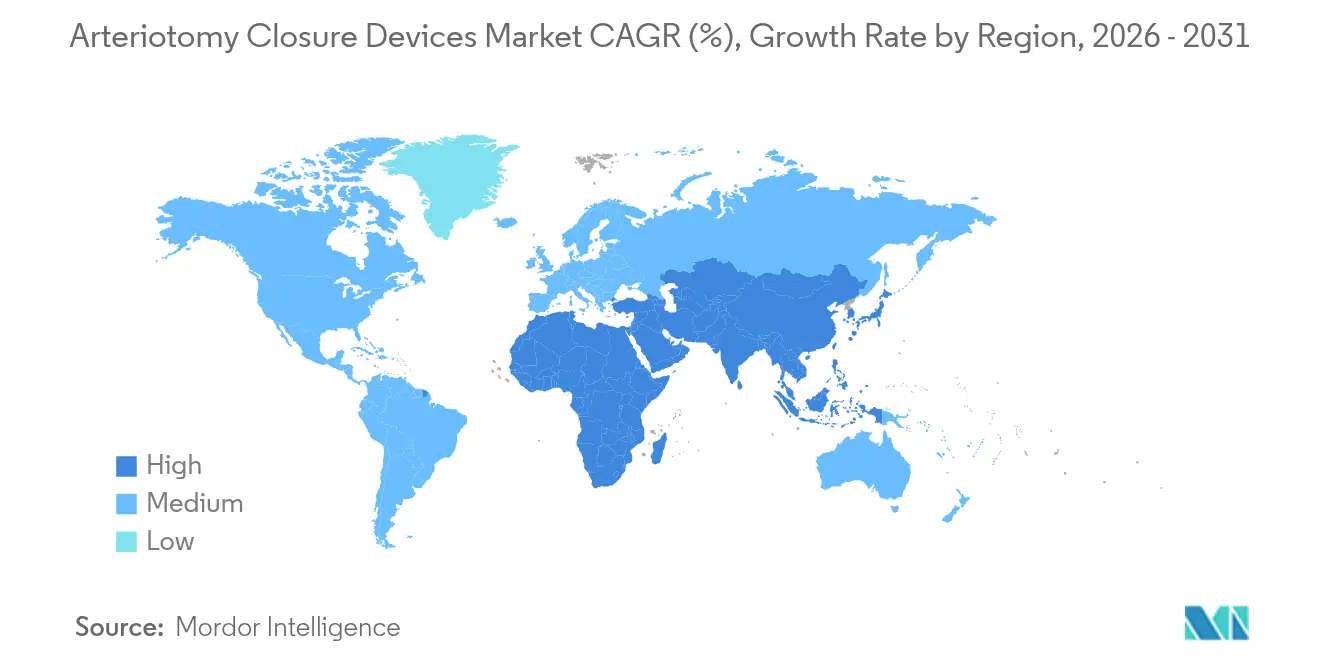

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Arteriotomy Closure Devices Market Analysis by Mordor Intelligence

Arteriotomy Closure Devices Market size in 2026 is estimated at USD 2.14 billion, growing from 2025 value of USD 1.99 billion with 2031 projections showing USD 3.06 billion, growing at 7.44% CAGR over 2026-2031.

A continued shift toward same-day discharge protocols, the ubiquity of minimally invasive cardiovascular procedures, and strong evidence of reduced hemostasis times are the principal catalysts propelling the arteriotomy closure devices market. Hospitals recognize the operational gains from these solutions, with average time to ambulation dropping from 6.1 hours to 2.8 hours in electrophysiology cases that use closure devices. Large-bore structural heart interventions such as TAVR and EVAR have also accelerated demand, as their arteriotomies can exceed 20F and command premium-priced closure technologies. In parallel, emerging polymer sealants eliminate retained-implant concerns and are helping passive devices gain traction. Finally, robust reimbursement codes in North America and growing procedure volumes in Asia Pacific sustain a healthy pipeline of opportunity for established and new entrants alike.

Key Report Takeaways

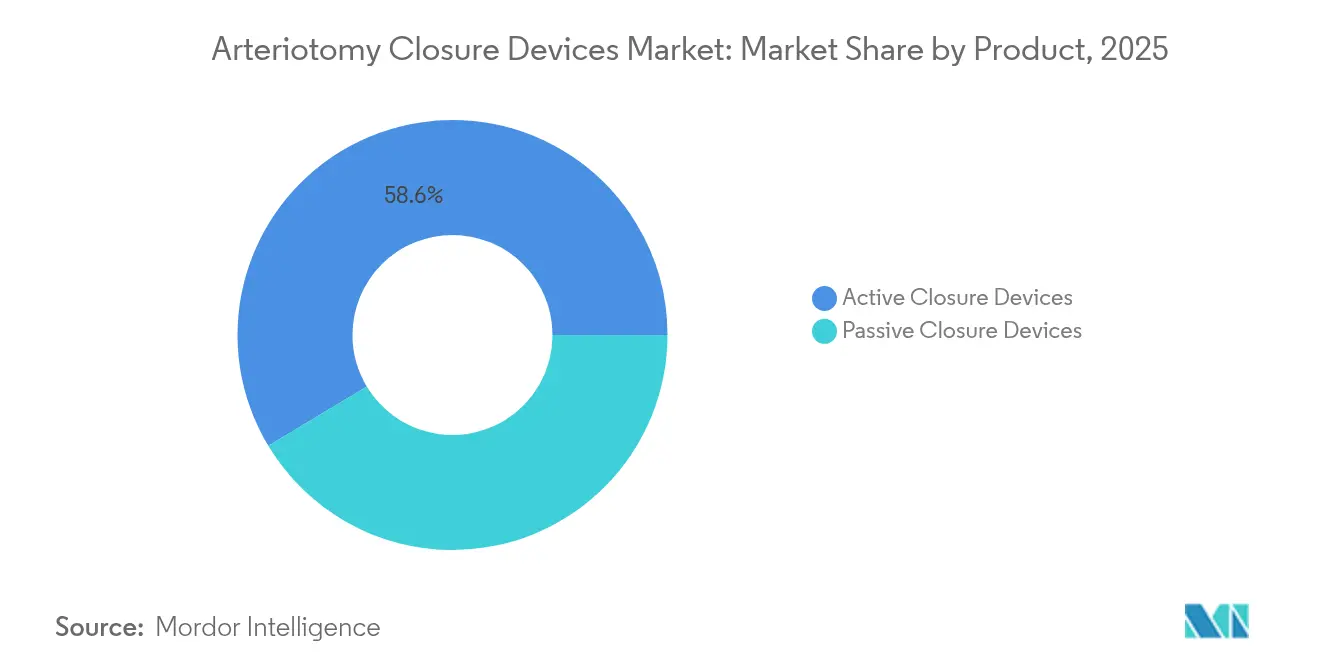

- By product type, active closure devices led with 58.62% revenue share in 2025, while passive devices are projected to expand at an 11.49% CAGR through 2031, the fastest among all categories.

- By application, femoral access procedures accounted for 61.05% of the arteriotomy closure devices market share in 2025, whereas large-bore access is projected to advance at a 9.26% CAGR through 2031.

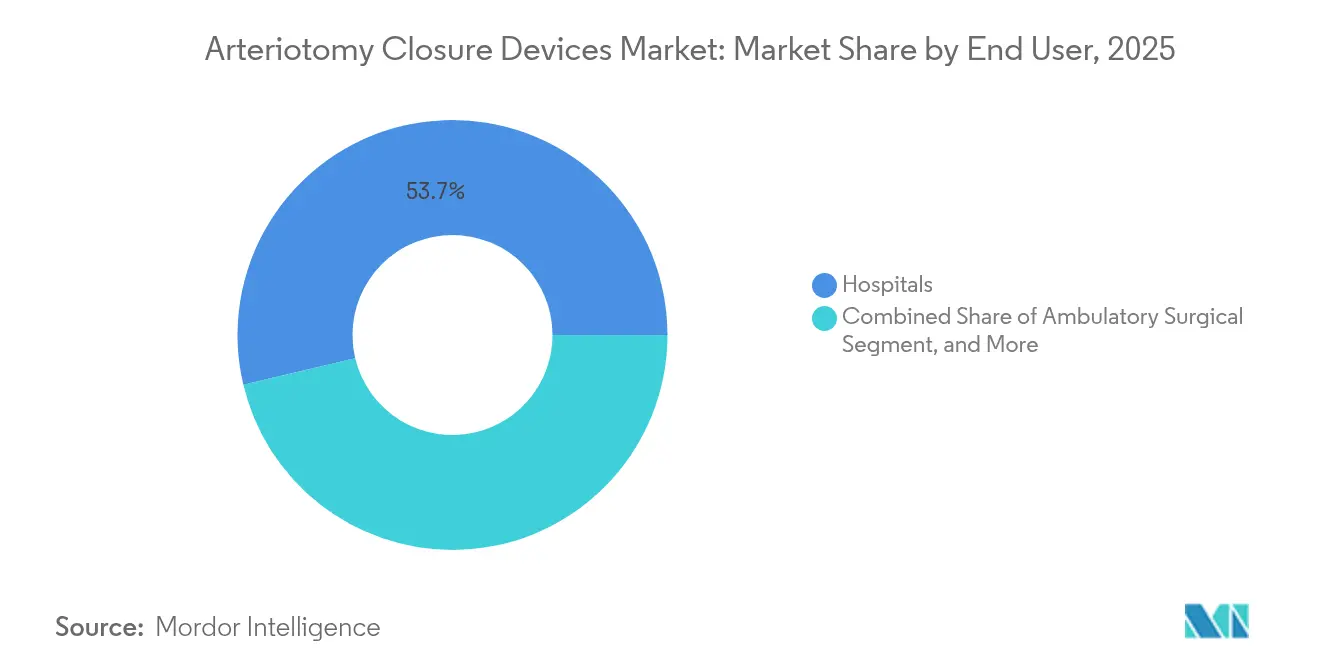

- By end user, hospitals captured 53.72% of the arteriotomy closure devices market size in 2025; however, ambulatory surgical and cath-lab centers are projected to show the highest growth at a 10.02% CAGR over the forecast horizon.

- By geography, North America held a 42.98% share of the arteriotomy closure devices market in 2025; the Asia Pacific is projected to be the fastest-growing region, with 8.83% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Arteriotomy Closure Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of cardiovascular & peripheral vascular disorders | +1.8% | Global | Long term (≥ 4 years) |

| Rising geriatric population & PCI volumes | +1.2% | North America & Europe | Medium term (2–4 years) |

| Rapid uptake of transradial & same-day discharge cath-lab programs | +1.5% | Global, early gains in North America | Short term (≤ 2 years) |

| Growth in large-bore interventions (TAVR, EVAR) requiring percutaneous closure | +2.1% | North America & Europe | Medium term (2–4 years) |

| Reimbursement reforms incentivizing outpatient vascular procedures | +1.3% | North America & Europe | Short term (≤ 2 years) |

| Breakthrough bio-absorbable/polymer sealants improving safety profile | +0.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Cardiovascular & Peripheral Vascular Disorders

Global cardiovascular disease affected 655 million individuals in 2024, and peripheral arterial disease cases have risen 23% since 2010, resulting in sustained growth across diagnostic angiography, PCI, and peripheral interventions that all require reliable closure solutions.[1]JAMA Editors, “Time to Hemostasis Comparative Study,” jamanetwork.com Procedure complexity in diabetic populations often demands repeat access, translating into steady, recurring demand within the arteriotomy closure devices market. Devices cut hemostasis time to around 1 minute versus 10 minutes for manual compression, allowing cath-labs to increase daily caseloads. Precision therapies targeting specific arterial beds likewise necessitate differentiated closure platforms, broadening the product mix that facilities must stock. Consequently, manufacturers that can offer comprehensive portfolios spanning sheath sizes from 5F to 24F are poised to capture incremental revenue.

Rising Geriatric Population & PCI Volumes

Patients older than 75 are the fastest-growing PCI cohort; comorbid calcification and anticoagulation elevate bleeding risk, making device-based closure preferable to manual compression. Outreach data show technical success rates of 94% and major complication rates below 1% when operators deploy closure systems in octogenarian cases.[2]PubMed Central, “Technical Success of Closure Devices in Octogenarians,” pubmed.ncbi.nlm.nih.gov Same-day discharge adds further momentum, particularly since Medicare broadened outpatient PCI reimbursement in 2024. Health-systems also emphasize patient quality-of-life, and quicker ambulation lessens fall risk and hospital-acquired infections. Together these factors reinforce structural, long-term demand drivers for the arteriotomy closure devices market.

Rapid Uptake of Transradial & Same-Day Discharge Cath-Lab Programs

Same-day discharge rates for elective PCI reached 79% in leading cardiac centers by 2024, primarily due to dependable closure technologies that reduce observation times and nurse workload.[3]Journal of the American College of Cardiology, “AMBULATE Trial Findings,” jacc.org Financially, facilities save USD 1,500–2,000 per case, a compelling incentive in value-based care environments. Electrophysiology procedures benefit strongly: the AMBULATE trial documented a 54% cut in time to ambulation and a 58% fall in opioid use when venous closure devices were utilized. COVID-19 constraints further accelerated adoption of outpatient models, prompting permanent infrastructural investments in standalone cath-labs equipped with modern closure tools. Regulatory guidance has now standardized discharge criteria, making same-day protocols routine rather than exception.

Growth in Large-Bore Interventions (TAVR, EVAR) Requiring Percutaneous Closure

TAVR volumes grew 15% year over year through 2024, and sheaths exceeding 20F require robust closure. Specialized devices priced three to four times higher than standard systems have achieved 98% arterial hemostasis with only 0.6% major vascular complications in prospective registries. Closing large arteriotomies eliminates surgical cut-downs, trimming procedure times by up to 34 minutes and supporting patient preference for minimally invasive approaches. As indications expand to intermediate-risk cohorts, the arteriotomy closure devices market gains a premium tailwind.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High ASPs of active closure devices | -0.8% | Global, emerging markets particularly | Medium term (2–4 years) |

| Device-related complications & steep learning curve | -0.6% | Global | Short term (≤ 2 years) |

| Cost-containment pressures in emerging markets | -0.4% | Asia Pacific, Latin America, MEA | Medium term (2–4 years) |

| Supply-chain dependency on medical-grade collagen & PEG | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High ASPs of Active Closure Devices

Active closure systems range from USD 200 to 400 each, significantly above the USD 50-100 cost of manual compression kits. When large-bore TAVR cases require multiple devices, per-procedure spend can exceed USD 1,000, straining budgets in price-sensitive regions. Although bundled purchasing can offset inpatient days saved, public hospitals in emerging markets often lack capital flexibility, slowing penetration outside tier-one centers.

Device-Related Complications & Steep Learning Curve

Pseudoaneurysm, arterial occlusion, and infection are infrequent yet severe events that demand surgical intervention if closure fails. Data show a pronounced learning curve, with complication rates falling only after operators complete roughly 30 cases. Smaller facilities without sustained volumes may therefore default to manual compression. Manufacturers continue to expand proctor programs and simplify deployment mechanisms, yet operator proficiency remains a gating factor to broader uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Active Devices Maintain Scale; Passive Devices Accelerate

Active platforms accounted for 58.62% of 2025 revenue within the arteriotomy closure devices market, primarily due to suture-mediated systems that span 5F-21F sheath sizes and achieve a 97.5% technical success rate in real-world registries. Their immediate hemostasis supports cath-lab throughput, and broad procedural coverage underpins their market leadership.

Passive solutions, however, are expected to post an 11.49% CAGR through 2031, as bio-absorbable polymers address previous concerns over retained collagen plugs. Early clinical experience suggests 1-minute average hemostasis and rapid resorption within 30 days, which helps passive entries secure an incremental share, particularly in younger and bariatric populations where foreign-body avoidance is paramount.

By Application: Femoral Dominance Persists; Large-Bore Access Surges

Femoral arterial interventions accounted for 61.05% of the 2025 demand, aligning with the entrenched provider familiarity and anatomy that accommodates diverse sheath sizes. Facilities embracing same-day discharge appreciate the 1-2 minute closure times that femoral devices achieve compared to 8-15 minutes via manual compression, which enables daily lab throughput.

Large-bore applications are poised for a 9.26% CAGR, mirroring the 15% annual rise in TAVR usage and continued EVAR adoption. Percutaneous closure of 24F arteriotomies eliminates the need for surgical cutdowns and shortens case times by up to 34 minutes, presenting high-margin revenue streams for suppliers in the arteriotomy closure devices market.

By End User: Hospitals Lead; Ambulatory Centers Disrupt

Hospitals accounted for 53.72% of 2025 sales, driven by their comprehensive trauma management capabilities and close collaboration with device manufacturers for training and adoption. Bundled payments that penalize readmissions further motivate hospitals to prefer devices over manual compression when the risk of bleeding is elevated.

Ambulatory surgical and catheterization centers are expected to log a 10.02% CAGR. Their dependence on swift ambulation places closure-system performance at the heart of operational economics; devices that reduce observation windows from 6 to 12 hours to 2 to 4 hours directly expand daily case capacity and enhance patient satisfaction.

Geography Analysis

North America captured 42.98% of 2025 global revenue in the arteriotomy closure devices market. Medicare and private insurers reimburse closure tools without added patient cost, prompting universal adoption for PCI and electrophysiology procedures. United States operators also cite medico-legal imperatives favoring device-based closure to minimize bleeding complications. Canada’s single-payer model supports closure uptake where cost-utility studies show diminished inpatient days, while Mexico’s growing private hospital sector is upgrading cath-lab capabilities aligned with premium closure technologies.

Europe remains a mature but sizeable arena characterized by stringent evidence requirements and value-oriented purchasing frameworks. Germany leads implantation volumes; the United Kingdom quickly embraces cost-effective plug-based devices; and France and Italy sustain steady growth due to high procedural load and favorable coding for same-day discharge. Post-Brexit regulatory divergence complicates product registration timelines, yet EU MDR certification continues to promote technology differentiation on safety credentials.

Asia Pacific is projected to deliver the fastest regional CAGR of 8.83% to 2031 on the back of expanding cardiac care infrastructure and rising incidence of ischemic heart disease. China’s investment in public and private cath-labs accelerates volume growth, while domestic device players increasingly partner with global leaders for technology transfer. Japan’s advanced reimbursement and procedural sophistication underpin early adoption of bio-absorbable closure platforms. India’s demand outlook remains robust, albeit tempered by acute price sensitivity that requires tiered product offerings and lean distribution.

Regulatory Landscape

In the United States, large-bore vascular closure systems are regulated as Class III devices under the FDA Premarket Approval (PMA) pathway, while many lower-risk closure products proceed via 510(k) clearance. This high-barrier PMA route is used for next-generation large-bore platforms, as shown by Vivasure Medicals June 2025 PMA submission for PerQseal Elite. In Europe, market access is anchored on CE certification under the EU Medical Device Regulation (MDR), which raises requirements for clinical evidence, post-market clinical follow-up, and technical documentation compared with the legacy directives. MDR transition provisions and milestone-based timelines shape continuity of supply for established portfolios, while international expectations around biocompatibility and thrombogenicity testing, including the ISO 10993 series, remain central for materials used in collagen, PEG, and polymer or sealant-based closure systems.

Competitive Landscape

The arteriotomy closure devices market exhibits moderate consolidation. Abbott’s Perclose family exemplifies a first-mover advantage in suture-based closure, while Terumo’s Angio-Seal plug system enjoys an entrenched share due to decades of safety data and a recent USD 30 million capacity expansion. Medtronic maintains a solid presence with its VenaSeal and ClosureFast ecosystem, complementing arterial offerings.

Competitive pressures are intensifying as mid-tier firms harness material-science advances. Vivasure earned a 2025 CE mark for its fully bioresorbable PerQseal Elite, signaling potential disruption in large-bore niches. Teleflex paid EUR 760 million (USD 893 million) for BIOTRONIK’s vascular intervention unit to integrate product pipelines and expand geographically vertically. Future rivalry will likely center on bioabsorbability, ease of use, and algorithm-guided deployment that reduces operator variability.

Arteriotomy Closure Devices Industry Leaders

Abbott Laboratories

Terumo Corporation

Medtronic

Cardinal Health (Cordis)

Haemonetics Corporation (Cardiva Medical)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace is expanding in large-bore and mid-bore access management as hospitals and ambulatory cath-lab centers operationalize same-day discharge pathways and place a premium on fast hemostasis with fewer access-site complications. Recent regulatory actions reinforce this direction: the FDA approved Haemonetics VASCADE MVP XL for 8-14F inner diameter sheath access sites in March 2026, and CyndRx received FDA approval in June 2026 for its AbsorbaSeal vascular closure device for acute arterial access site closure. In July 2026, xDot Medical obtained an FDA IDE to start a pivotal trial targeting large-bore femoral arterial and venous access sites.

Technology opportunities focus on reducing retained-implant concerns and improving consistency across operators, aligning with the report themes around bio-absorbable or polymer sealants and simplified deployment. An April 2026 publication evaluating plug-based closure devices in TAVR using VARC-3-defined vascular endpoints also points to continued clinical evaluation informing product choices, and it highlights a practical near-term commercialization focus on evidence packages tied to time-to-ambulation and discharge eligibility while extending labeled sheath ranges and indications to reflect multi-access needs across electrophysiology, structural heart, and peripheral interventions.

Recent Industry Developments

- July 2026: xDot Medical obtained an FDA IDE to start a pivotal trial targeting large-bore femoral arterial and venous access sites. This development advances evaluation of expanded closure indications across high-flow interventional workflows.

- June 2026: CyndRx received FDA approval for its AbsorbaSeal vascular closure device for acute arterial access site closure. The clearance broadens the companys arterial closure footprint and supports rapid hemostasis workflows in interventional procedures.

- March 2026: Haemonetics received US FDA approval for expanded labeling of the VASCADE MVP XL venous vascular closure system, extending coverage to larger sheath profiles. The update strengthens the companys position in higher-flow, larger-access electrophysiology and structural heart workflows where closure performance and throughput are tightly linked.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market includes devices used to close an arterial access site (arteriotomy) after catheter based procedures, where closure is achieved through sutures, plugs, clips, or assisted compression. The purpose is to reduce time to hemostasis and support earlier mobilization after femoral and other arterial punctures.

Scope exclusions: The sizing excludes general wound closure products and venous access closure products that are not intended for arterial puncture site closure.

Segmentation Overview

- By Product

- Active Closure Devices

- Suture-mediated Systems

- Clip-based Systems

- Passive Closure Devices

- Collagen Plug Devices

- Polymer/Sealant-based Devices

- External Compression & Assist Systems

- Active Closure Devices

- By Application

- Femoral Arterial Access Procedures

- Radial/Brachial Arterial Access Procedures

- Large-bore Access (TAVR, EVAR, TEVAR)

- By End User

- Hospitals

- Ambulatory Surgical & Cath-Lab Centers

- Specialty Cardiology Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the procedure and access mix context that drives closure-device demand. For top-level procedure volumes and care setting shifts, we reference public sources such as the US FDA device database, the US Centers for Medicare and Medicaid Services procedure and payment references, the OECD health statistics portal, and World Bank health indicators.

We also review clinical guidelines and evidence in peer reviewed journals (for example, outcomes by femoral versus radial access and reported complication rates by closure approach), along with regulatory summaries, product instructions for use, and safety communications. To cross-check the supply side, we use company filings and investor presentations where available, and we supplement with medical association and hospital network publications.

For selected checks, we use subscription databases for company financials and intelligence, patent search coverage, and shipment level import-export signals where product coding allows. These examples are not exhaustive, and many other public and paid sources were also referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary validation is done through structured discussions with device manufacturers, distributors, interventional cardiology and radiology clinicians, cath lab managers, and procurement teams who see utilization patterns directly. Inputs from these conversations are used to confirm realistic adoption by access site (femoral and radial), the shift toward large bore procedures in some centers, and typical price bands by product category and region.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 41% |

| Mid tier: 58% | Functional/Unit leaders: 35% | EMEA: 33% |

| Smaller Players: 14% | Managers: 52% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where procedure volumes and access site mix are reconstructed by geography, then converted into a device demand pool using penetration assumptions for closure devices versus manual compression. To keep the math grounded, we corroborate the totals with selective bottom-up approximations such as sampled average selling price (ASP) by device class multiplied by estimated units, supported by channel checks on units used per procedure in real settings.

Key inputs used in the model include the number of cardiac catheterization and peripheral interventions performed, the femoral versus radial share by region, the share of cases using large bore access, the typical closure device utilization rate by procedure type, and observed ASP differences between active and passive closure products. Where country level procedure data is incomplete, we fill gaps using proxy indicators such as cath lab capacity, hospital discharge trends, and expert validated ranges, then we adjust to maintain consistency with regional totals.

For forecasting, scenario analysis is applied around a central view informed by expert consensus on adoption and pricing. The forward path is shaped by expected shifts in access technique, patient mix, complication management preferences, and reimbursement and regulatory changes that influence hospital purchasing decisions. Assumptions are kept explicit so they can be re-run when new procedure statistics or pricing signals become available.

Data Validation & Update Cycle

Validation is handled through triangulation across demand indicators, supply signals, and interview feedback, and then by checking year over year movements for logical consistency. Outliers are reviewed at the country and regional level, and when a variance cannot be explained by procedure mix or price shifts, the assumptions are revisited and experts are re-contacted.

Before sign-off, the model and narrative go through a multi-step analyst review to ensure inputs, formulas, and unit conversions are consistent across regions and time. Reports are refreshed annually, with interim updates when material events occur such as major regulatory changes, reimbursement shifts, or notable product actions. Right before delivery, we do a final pass to ensure the latest publicly available data points are reflected in the market numbers and commentary.

Mordor Intelligence's Arteriotomy Closure Devices Market Size Compared With Other Published Estimates

Published market numbers for arteriotomy closure devices can vary even when the topic sounds identical, mainly because the demand pool is built differently and the pricing logic is not always consistent. Differences also show up when a study mixes adjacent products into the scope, or when the base year and currency timing are not aligned across regions.

By tracking procedure volumes by access site and refreshing ASP bands with primary checks, Mordor Intelligence keeps the model tied to device eligible cases and avoids blending in hemostatic agents or broader vascular access consumables. Some publishers also start from a different base year, and a few extend the forecast horizon in a way that assumes faster adoption without clearly stating the step changes, which can widen the spread in the stated market value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.14 B (2026) | |

| Global Consultancy A | USD 1.94 B (2024) | Uses an earlier base year and may apply a broader regional roll-up without fully showing how femoral versus radial access mix and large-bore procedure share change the eligible device pool, which can pull the value down versus later-year sizing. |

| Industry Publisher B | USD 1.64 B (2025) | Starts from a 2025 base and appears to rely more on high level growth application over the period, with limited clarity on whether pricing is modeled by active versus passive closure categories, which can create a lower starting point. |

Across the table, the gap is explained mostly by base year choice and by how tightly the estimate is linked to procedure based demand and product scope. When access site mix, utilization, and pricing are handled as separate inputs, the resulting total is easier to audit and update as new clinical and purchasing signals emerge.

Key Questions Answered in the Report

What is the current rteriotomy closure devices market size?

The arteriotomy closure devices market is projected to register a CAGR of 7.44% during the forecast period (2026-2031)

Who are the key players in rteriotomy closure devices market?

Teleflex Incorporated, Medtronic, Merit Medical, Otsuka Medical Devices Co. Ltd (Veryan Medical) and Cardinal Health (Cordis) are the major companies operating in the Arteriotomy Closure Devices Market.

Which is the fastest growing region in the arteriotomy closure devices market

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in arteriotomy closure devices market?

In 2025, the North America accounts for the largest market share in arteriotomy closure devices market.

Page last updated on: